17

Sample Portfolios and Something About Gunslingers

Asset allocation is simply about seeking the highest possible return given our risk tolerance.

—JPP

FOLLOWING ARE STRATEGIC ASSET ALLOCATIONS FOR portfolios that broadly incorporate the principles we’ve discussed throughout this book. Tactical asset allocation should also be applied around these strategic weights, to take advantage of relative valuation opportunities based on the approach we discussed in Part One of this book.

My goal is to finish this book with practical recommendations. There’s a wide range of high-quality multi-asset portfolios offered to investors. In my view, these are the portfolios that best illustrate a thoughtful approach to asset allocation. They have delivered strong risk-adjusted returns and have done well in markets when diversification has failed. I rely on broad market indexes to represent asset classes, again, for illustrative purposes.

In the Global Multi-Asset Division at T. Rowe Price, we manage more than 200 different portfolios/products. These “samples” don’t constitute advice. Every investor’s situation is different, and an assessment of risk tolerance remains paramount (the hope is not via blood tests, per our earlier discussion in Chapter 11). But these portfolios can serve as good anchor points, or “templates” for portfolio construction.

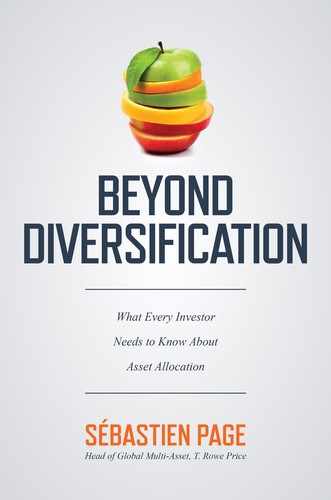

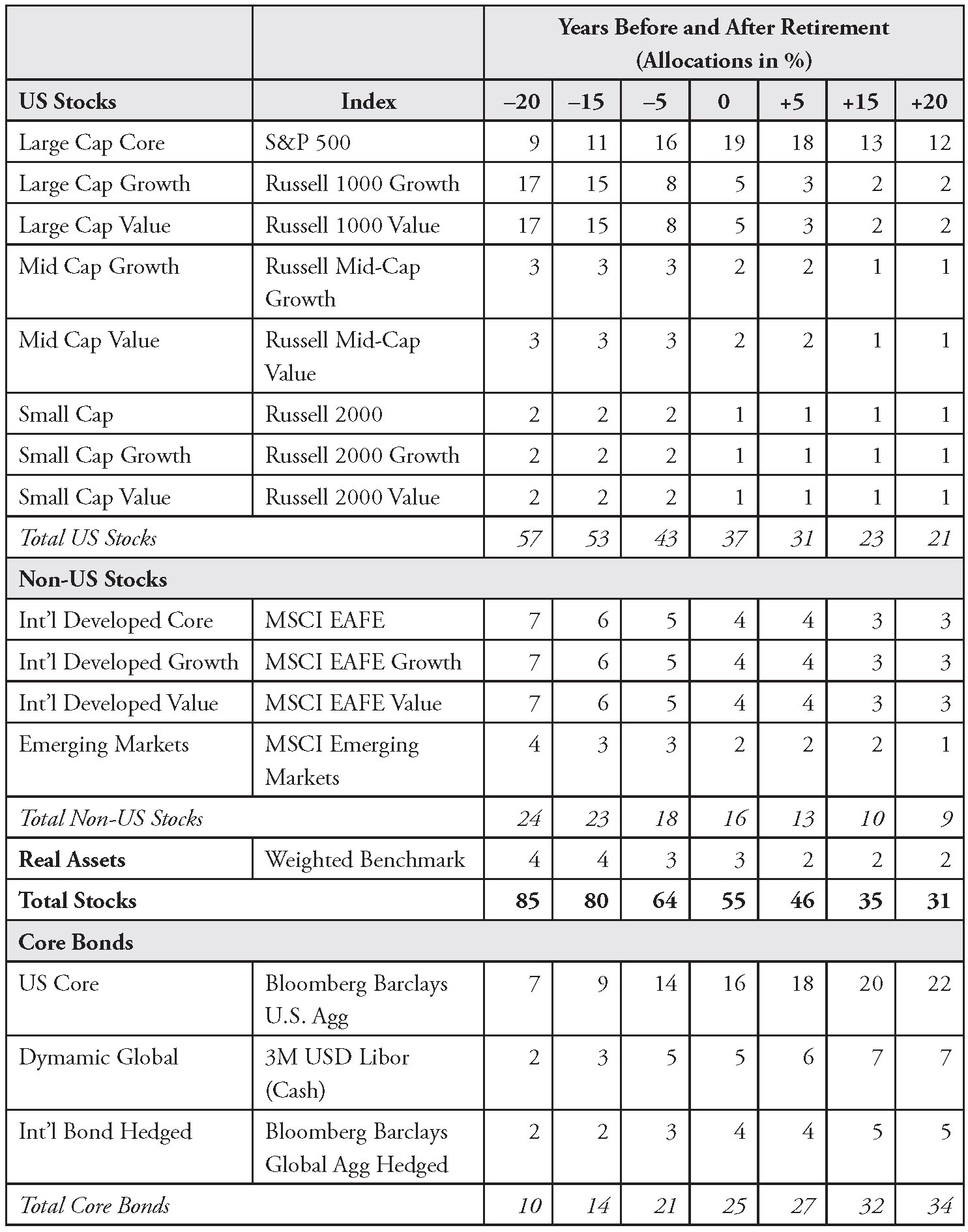

Target-Date Portfolios

Target-date portfolios, as discussed in Chapter 13, automatically adjust the stock-bond mix over time to account for the investor’s time horizon. Investors simply buy a fund that matches their expected retirement date, contribute to it along the way, and “forget it.” Meanwhile the fund manager reduces the allocation to stocks and adjusts the components as time passes. This process eliminates the need for the investors to regularly reoptimize their portfolio.

Basically, these funds provide an autopilot solution. They are available in many tax-deferred 401(k) accounts as well as through advisors and as direct investments. In Table 17.1 (in the following section), I show the strategic allocations for a sample of target-date portfolios. As mentioned, these weights don’t include tactical deviations, which change over time. For simplicity I show seven key portfolios along the glide path, although a typical target-date series would shift from the asset mix based on the investor’s age in smaller increments.

Most portfolio managers of active target-date funds rely on well-staffed, dedicated research teams for strategic and tactical asset allocation. I have used index exposures for illustrative purposes in the table, but each component can be actively managed by portfolio managers who focus on security selection and rely on an army of analysts. Essentially, active target-date funds combine the entirety of an investment firm’s capabilities.

Is the Home Bias Really a Bias?

Notice in the table a moderate strategic home bias toward US assets. When we build portfolios outside the United States, we typically allow some degree of home bias as well (we “localize” them). For example, our target-date portfolios in Korea include an allocation to Korean equities and bonds that’s larger than their market capitalization weights in the world portfolio. The home bias accounts for liabilities, i.e., the fact that retirees spend their savings in their home country. If the local economy does well or if local prices inflate, retirees will want/need to spend more.1 In this scenario, the growth of their local assets will hedge the increase in spending needs (all else equal), and vice versa when the economy does poorly. (In this case, the need to spend decreases in a way that offsets portfolio losses.)

The same liability argument applies to bonds. If rates go up, retirees can buy a given income stream with less money, so they’ll tolerate losses on their local bond portfolio. If rates go down, retirees will pay more for an income stream, but they’ll be able to finance the income stream with appreciated local bond values. This concept is well known in the world of defined benefit plans.

Because defined contribution plans essentially solve for the same problem (accumulate assets to replace one’s salary in retirement), the concept applies here as well. The bottom line is that though global diversification remains important for growth and risk management, local assets hedge local spending, and so a home “bias” isn’t always a bias per se. Nonetheless, some investors want broad global market exposures, which we provide in various non-home-biased portfolios as well.

Here are other notable features of these sample portfolios:

![]() They include strategic alpha positions in high-return diversifiers such as high-yield and emerging markets bonds. These asset classes may offer both high-risk-adjusted-beta (index) returns over time and rich alpha opportunities.

They include strategic alpha positions in high-return diversifiers such as high-yield and emerging markets bonds. These asset classes may offer both high-risk-adjusted-beta (index) returns over time and rich alpha opportunities.

![]() For similar reasons, they tend to allocate slightly more to small and mid cap stocks than their market cap weights would indicate. These market capitalization weights have drifted down over time.

For similar reasons, they tend to allocate slightly more to small and mid cap stocks than their market cap weights would indicate. These market capitalization weights have drifted down over time.

![]() The real assets class is composed of global stocks that should perform well during inflationary environments (metals and mining, precious metals, real estate investment trusts, and energy companies). It includes US and non-US companies.

The real assets class is composed of global stocks that should perform well during inflationary environments (metals and mining, precious metals, real estate investment trusts, and energy companies). It includes US and non-US companies.

![]() In several of our models, as in the target-date portfolios, we also include allocations to Treasury Inflation-Protected Securities. Often, we debate the strategic role of inflation protection, because inflation has been so low for so long. Though we often underweight inflation-linked assets tactically, we believe inflation remains a “tail risk,” so a strategic allocation to inflation protection is warranted in most portfolios.

In several of our models, as in the target-date portfolios, we also include allocations to Treasury Inflation-Protected Securities. Often, we debate the strategic role of inflation protection, because inflation has been so low for so long. Though we often underweight inflation-linked assets tactically, we believe inflation remains a “tail risk,” so a strategic allocation to inflation protection is warranted in most portfolios.

![]() In our flagship Target Date Fund series at T. Rowe Price, almost all components are actively managed, although here I use index exposures for illustrative purposes. We also offer active-passive blends, which have recently become popular with 401(k) plan sponsors.

In our flagship Target Date Fund series at T. Rowe Price, almost all components are actively managed, although here I use index exposures for illustrative purposes. We also offer active-passive blends, which have recently become popular with 401(k) plan sponsors.

![]() Stocks are the main engine of growth in investors’ portfolios. Despite increased volatility along the way, over the long run, it can pay to allocate to stocks. In our portfolios we tend to allocate slightly more to stocks than our peers do. We manage this strategic equity risk through tail-risk-aware diversification and tactical asset allocation.

Stocks are the main engine of growth in investors’ portfolios. Despite increased volatility along the way, over the long run, it can pay to allocate to stocks. In our portfolios we tend to allocate slightly more to stocks than our peers do. We manage this strategic equity risk through tail-risk-aware diversification and tactical asset allocation.

In Table 17.1, I also show historical annualized returns over various time periods. “CMA returns” refer to capital markets assumptions—expected returns for the next five years—which reflect our view of the current state of the world. These numbers are lower than historical returns because interest rates are close to an all-time low, as we discussed in Chapter 1, and alphas from active management (security selection and tactical asset allocation) are not included.2

TABLE 17.1 Asset Allocations Throughout the Life Cycle*

Target Allocation Portfolios

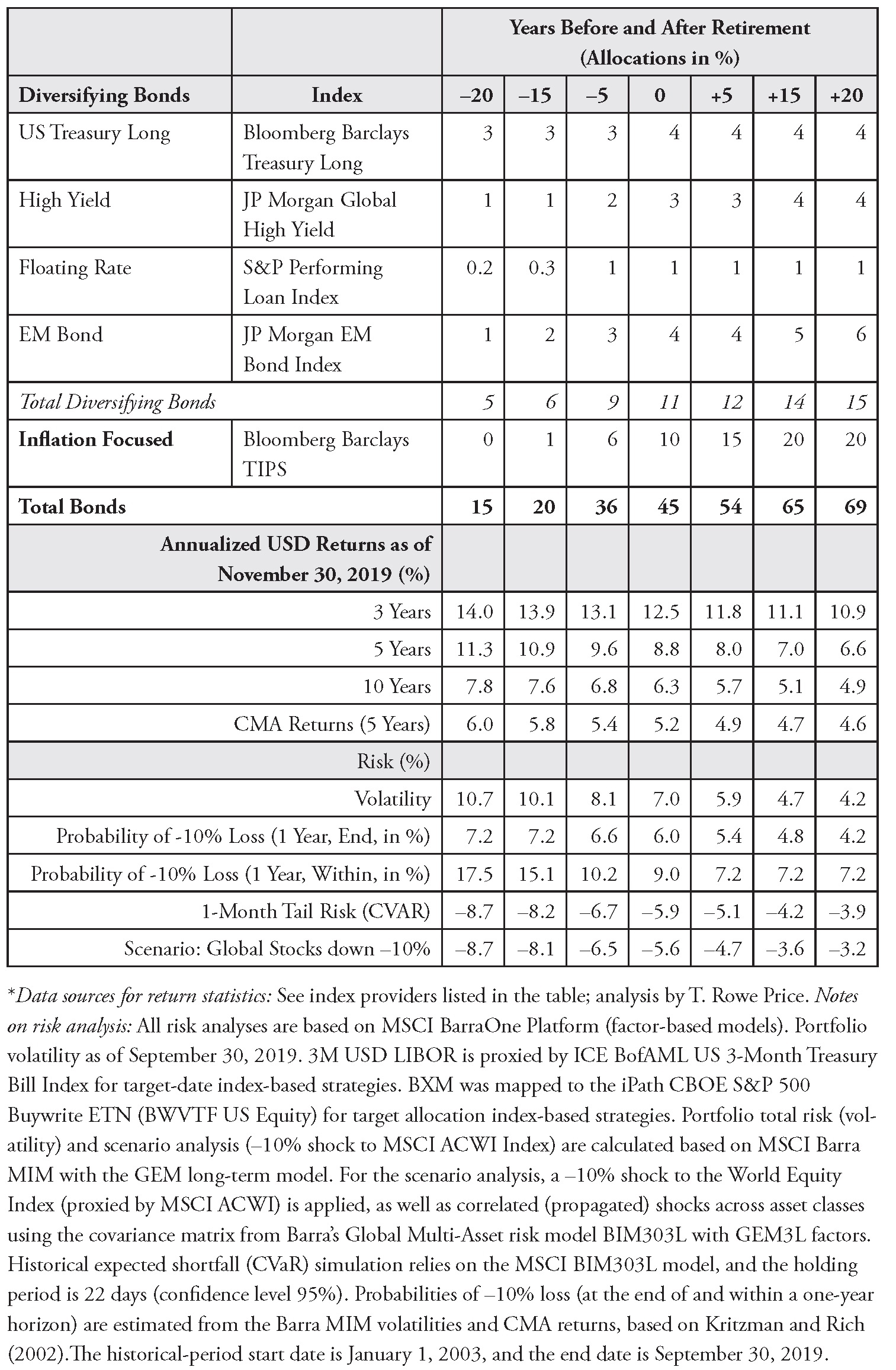

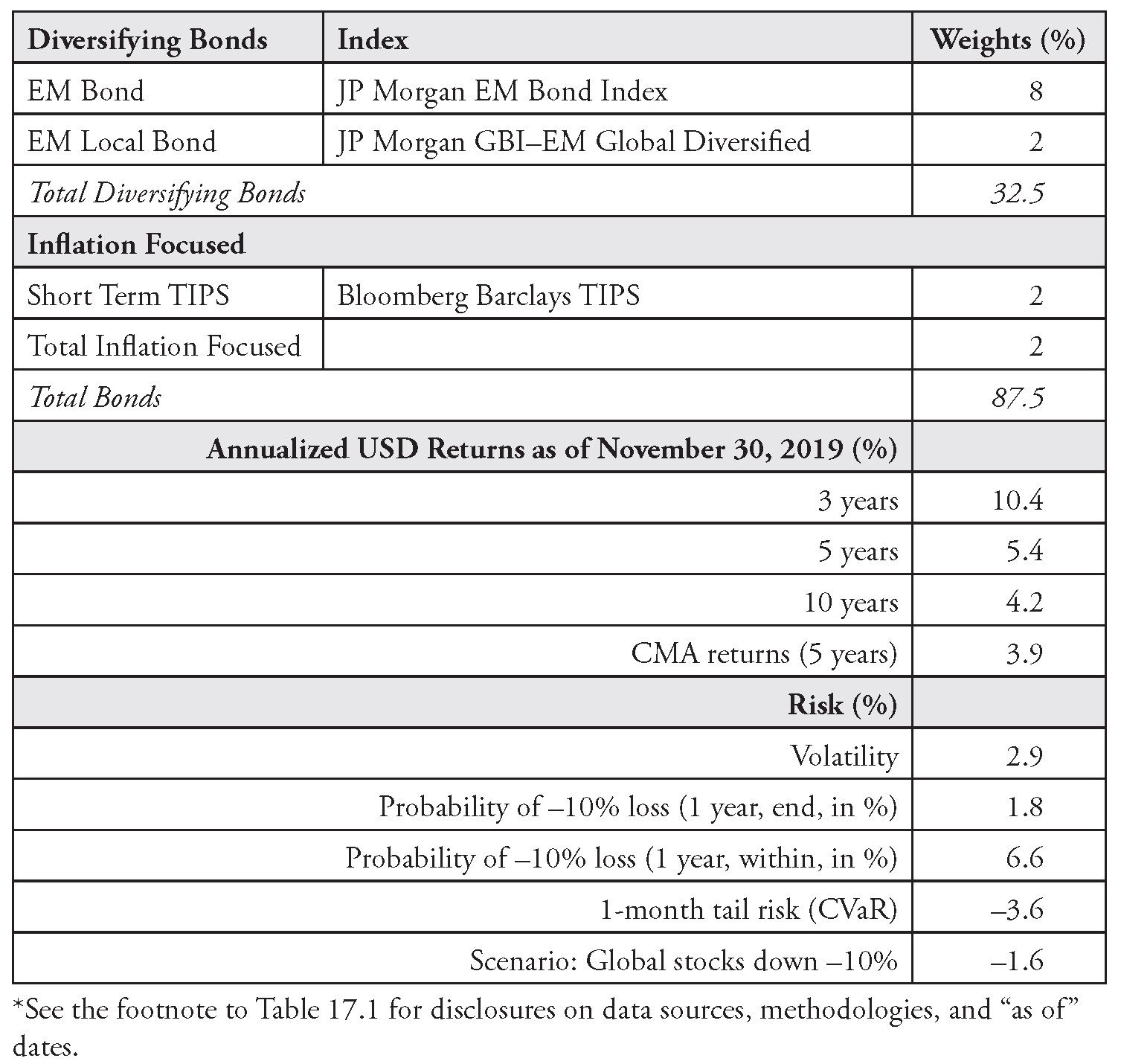

Conservative Income

This sample conservative income asset allocation (Table 17.2) provides a high level of current income, with moderate to low volatility, for US-focused investors. (In general, like other retirement-focused portfolios such as target- date funds, income portfolios tend to be “localized,” with a focus on the investor’s home country.)

It does, however, include a “kicker” of 12.5% in income-oriented stocks to boost returns over time and provide a long-term inflation hedge. Along with other portfolio features, such as diversified credit exposures and security selection alpha (if implemented via actively managed strategies), this equity allocation may help investors accumulate more capital than a pure bond portfolio.

In contrast, many conservative income portfolios invest entirely in fixed income assets. In doing so, they tend to strive for yield and to load up on indirect equity risk through high-yield bonds and other lower-rated sectors. These funds miss an opportunity to directly calibrate and benefit from stock-bond diversification. Though it varies greatly over time, this is one of the most robust forms of diversification, as we discussed in Chapter 9.

The fixed income portion of the portfolio is one of the most diversified across all the samples I show in this chapter, which is consistent with the portfolio’s large allocation to fixed income in general (87.5%). The dedicated US Treasury Long position helps diversify equity risk. We use this asset class both strategically and tactically in most of our portfolios. From a strategic perspective, it provides significant diversification to equity risk per dollar invested, due to its high-interest-rate sensitivity/long duration—a “risk parity” concept, if you will. For the same reason, from a tactical perspective, US Treasury Long is an efficient and highly liquid building block when we want to manage our total portfolio risk up and down based on our risk-on versus risk-off view of the markets.

The usual high-yielding sectors are present (high yield, floating rate, and emerging markets) to deliver income, and the core bonds components are customized for the conservative income objective. Through security selection, skilled portfolio managers in these asset classes seek to avoid systematic biases that often build up in index exposures, such as large oil risk factor exposures.

Dynamic global bonds, which are also in the Target Date Fund samples, are employed as a type of conservative strategy that is designed to do well when diversification fails elsewhere in the portfolio. The strategy focuses on a cash benchmark, includes direct equity/credit risk hedging positions, and capitalizes on relative value opportunities primarily in rates and currencies. In our portfolios, we classify dynamic global bonds as core bonds, given their conservative nature and volatility closer to core than diversifying sectors, or we categorize them under alternatives, given their focus on absolute return. In all cases, it’s the same strategy, but we find it useful to put it in different categories to reflect the role the bonds play in a given portfolio versus other components.

TABLE 17.2 Income Portfolio—Conservative, US Focused*

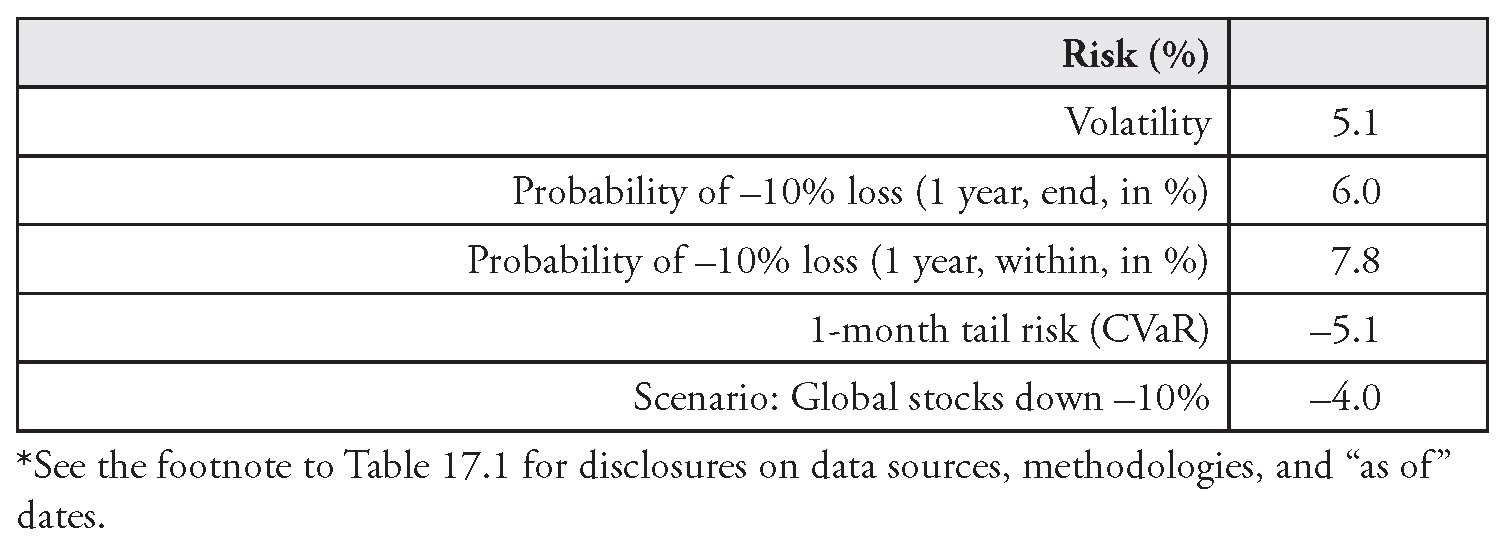

Diversified Income—Moderate Risk

Here (Table 17.3) we allocate 40% to stocks, compared with 12.5% for the conservative income portfolio. This sample portfolio seeks the highest total return over time consistent with a primary emphasis on income and a secondary emphasis on capital growth. Given the portfolio’s dual objectives, a 7% cash allocation provides an important diversifier to equity risk, adds liquidity, and helps anchor the portfolio’s risk closer to its benchmark. It also provides a tactical lever to calibrate risk exposure over time.

TABLE 17.3 Income Portfolio—Moderate, Diversified*

In this asset allocation, alternatives play an important role. We classify the volatility premium within US stocks, although it could also be classified as an alternative. We reviewed this strategy in Chapter 7 when we discussed my presentation at the CFA Institute in Montreal and looked at the correlation between covered call writing—the actively managed strategy we use to access the volatility premium—and a managed volatility strategy. Also, we revisited the topic when we discussed risk factors in Chapter 12. As mentioned, the volatility risk premium may be one of the few “factors” that appear to deliver robust performance over time. This strategy typically focuses on equity index options and comes with a targeted equity exposure (“delta hedging”).

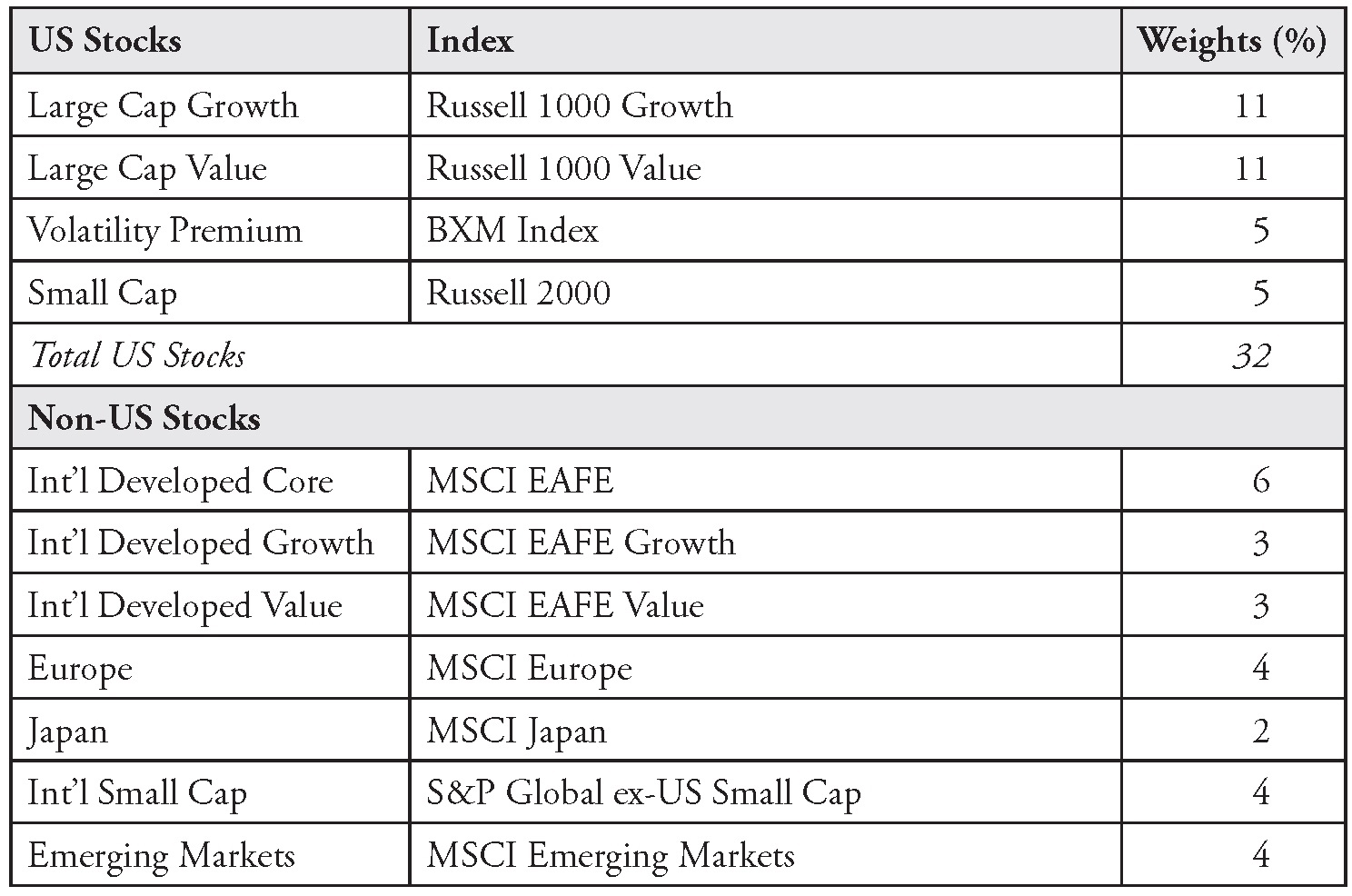

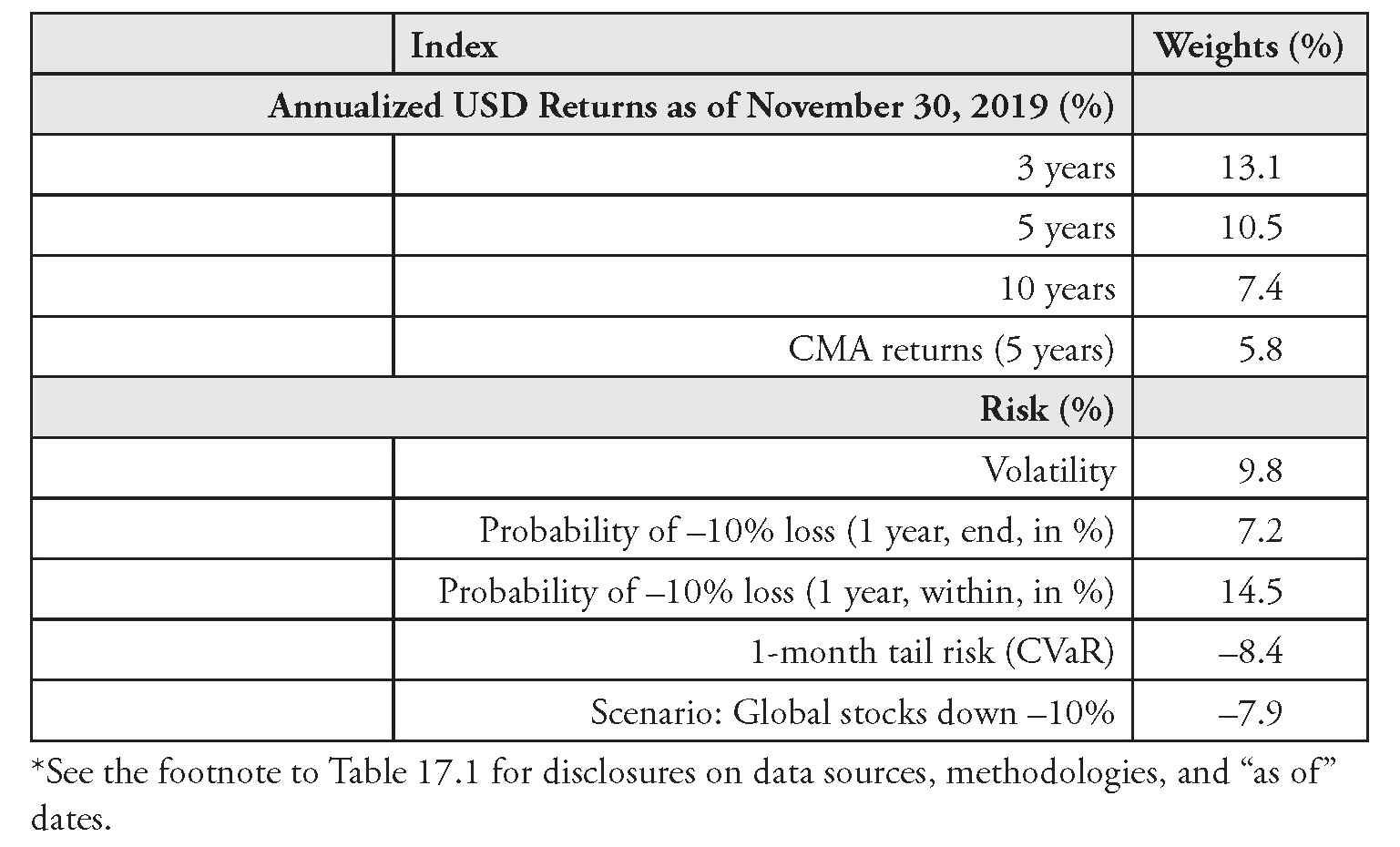

Diversified Global Portfolio

This sample asset allocation (Table 17.4) is meant to represent a flagship fund of funds that can be offered to investors globally. Its opportunity set includes developed markets and emerging markets equities, a wide range of global developed markets and emerging markets bond strategies, and various diversifying strategies designed to improve risk-adjusted returns. It’s the quintessential one-stop-shop solution. The strategic asset allocation is 60% stocks (without home bias), 28% global fixed income, including exposure to below-investment-grade securities, and 12% alternative investments. Alternative investments may include hedge funds and a dynamic global bond strategy (here classified as an alternative). The government credit allocation is structured with a longer-duration profile as a diversifier, or “hedge,” to equity volatility/potential fat-tail exposure in alternatives, with the long end focused on higher-quality bonds and Treasuries.

This type of asset mix is slowly rebuilding an investor base outside the United States, in Europe in particular. Over the last few years, European investors have poured billions into highly dynamic, absolute-return-oriented multi-asset products. The most popular strategies did well during the 2008–2009 sell-off and caught the subsequent upswing in asset prices. But I believe that a significant shift in preferences may have begun, as many of these “gunslinger” strategies have underperformed good old balanced strategies over the last several years. In Chapter 1, I made a snide comment on promises of “stock-like returns for bond-like volatility,” supposedly delivered through a handful of big macro bets made by very smart investors. European investors have grown more skeptical of this approach. It’s hard to deliver durable performance without breadth and diversification in active management activities, from strategic, to valuation-based tactical, to security selection. Without breadth and without the long-term tailwind of long positions in stocks, credit, and duration premiums, many macro gunslingers have struggled over the last few years.

TABLE 17.4 Balanced Portfolio—Global, Diversified*

Growth Portfolio

This high-octane asset allocation (Table 17.5) seeks the highest total return over time consistent with a primary emphasis on capital growth and a secondary emphasis on income. It invests in a diversified portfolio of about 80% stocks; 16% bonds, money market securities, and cash reserves; and 4% alternative investments. It provides a simple yet diversified set of building blocks, which corresponds to the preferences of US-domiciled investors.

TABLE 17.5 Growth Portfolio—US Focused*

Specialized Portfolios and Thoughts on Change in Our Investment Division

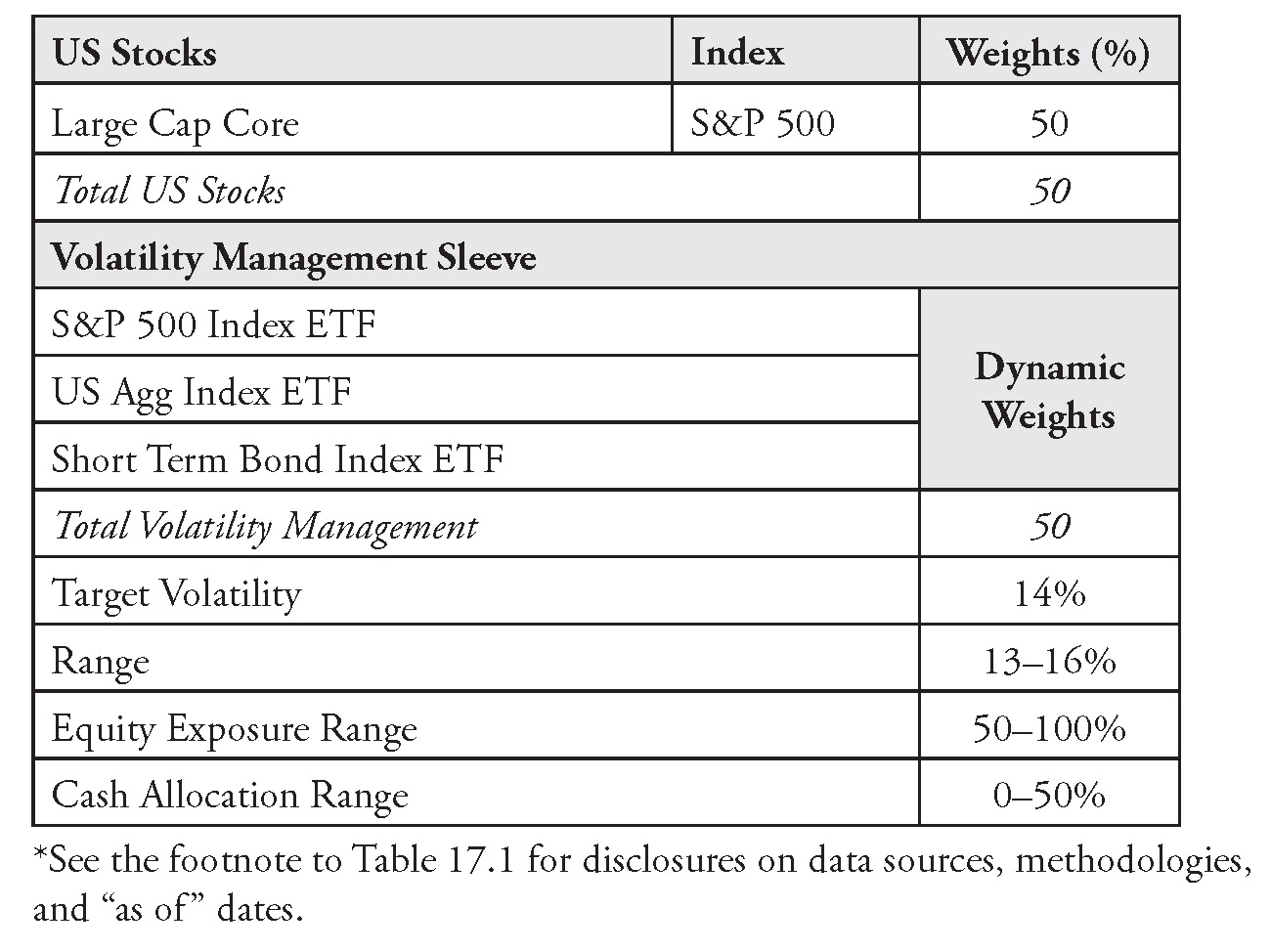

Target Volatility—“Defensive Equity”

This sample portfolio (Table 17.6) directly targets volatility, based on the managed volatility strategy we discussed in Chapter 7. It can be used as a defensive US equity exposure as part of an investor’s asset allocation. Half the portfolio is allocated to US stocks, while the other half is allocated to a dynamic sleeve composed of three ETFs: US stocks, US bonds, and “cash”/short-term bonds. Allocations within this sleeve change based on the volatility environment. When volatility increases, the strategy decreases the allocation to the stocks ETF, and vice versa when volatility decreases. As we have discussed earlier, this process helps manage the failure of diversification in times of market stress.

TABLE 17.6 Target Volatility—Defensive Equity*

These portfolios represent only a few examples of a much broader set of asset mixes that can be appropriate for various investors. Recently, in our Global Multi-Asset Division, we have made a substantial investment in our solutions capabilities. We have launched several localized multi-asset portfolios for non-US investors, based on a range of goals: income, absolute return, liability-driven, retirement, etc. The key to a successful solutions business is to start with client needs.

Also, we have built customized asset allocation models for intermediaries. These models are quite popular with advisors and their clients. Increasingly, advisors spend more time on financial planning and tax management questions, while they rely on third-party models to guide their clients to the appropriate asset mix. These models can be built as variations, or “tweaks,” on the sample portfolios I have presented in this chapter. They can be “proprietary,” i.e., allocated to building blocks managed by one single investment firm, or “open architecture,” i.e., allocated to multiple managers.

In the alternatives space, we have built an absolute return-oriented, multisleeve strategy that leverages our entire investment platform and includes allocations to long-short equity portfolios. One of our most interesting liquid alternative strategies is best described as an unconstrained, long-short multi-asset strategy that harvests a highly focused set of our platform’s best ideas (across macro, individual stocks, commodities, credit, special situations, etc.). The bottom line is that asset allocation and multi-asset investment management continue to evolve at a rapid pace.

The evolution of these capabilities illustrates how our Global Multi-Asset Division has gone through a period of accelerated change and modernization over the last four years. We have faced unprecedented competition. To continue to deliver value to our clients, we have developed and improved our capabilities at a breathless pace.

But unlike many competitors, we didn’t start with a blank canvas. We’ve built from a position of strength, with a large asset base and a strong, multidecade history of success in multi-asset investment management. We’ve had the usual ups and downs that come with an aggressive change agenda. We’ve had to work hard to maintain our core principles (our strong culture, our focus on existing clients and investment performance, etc.) and embrace new ideas and accelerated innovation.

About three years ago, when I met with our board of directors, I quoted one of the best race car drivers of all time, Mario Andretti: “If everything seems under control, you’re not going fast enough.” I suspect some of our directors felt uneasy with this quote. But I think others, especially those from the private sector, got the idea: no matter how successful a business, standing still is rarely a good option.

Notes

1. At least in nominal dollars.

2. T. Rowe Price Capital Markets Assumptions, 2019, https://www.troweprice.com/content/dam/ide/articles/pdfs/2019/q2/capital-market-assumptions .pdf.