Chapter

Developing New Trading Systems

Don’t count your chickens until they are incubated.

Introduction

A trading system is only as good as your market intuition. You can formulate and test virtually any trading system you can imagine with today’s software. The previous chapters studied the basic principles of system design. This chapter develops and tests several original trading systems to illustrate the application of those principles:

- A simple trend-following system—the 65sma-3cc system.

- A pattern-based system for long trades only—the CB-PB system.

- A trend-seeking, strength-of-trend system—the ADX burst system.

- An automatic mode-switching system—the trend-antitrend system.

- Intermarket systems for correlated markets—the gold bond systems.

- A system for picking bottoms—a bottom-fishing pattern.

- A system for increasing bet size—the extraordinary opportunity model.

In this chapter, each case illustrates a different design philosophy. The 65sma-3cc system is examined in the greatest detail; the same principles can be applied to all other systems. Long-term test results with continuous contracts are shown for every system.

This is not a recommendation that you trade these systems. These systems have all the limitations of hypothetical test results. They are discussed here only as examples of the art of developing systems that suit your trading style.

The Assumptions behind Trend-Following Systems

The basic assumptions behind a simple trend-following system are as follows:

- Markets trend smoothly up and down, and trends last a long time.

- A close beyond a moving average signals a trend change.

- Markets do not have large countertrend price swings.

- Prices do not move too far away from an intermediate moving average.

- Whipsaws are relatively few and do not cause large losses.

- Significant price moves last many weeks or months.

- Markets are predominantly in a trending mode.

The reality of a trend-following system is that:

- Markets are often in ranging mode with choppy swing moves, so losses in trading ranges are significant.

- There are large swings in trade equity, since the model “gives back” a large proportion of profits before signaling an opposite trend.

- These systems need a relatively “loose” stop in order to avoid missing about 5 percent of trades that account for major profitable moves.

- These systems often enter the market on strength or weakness, so that they can be stopped out during short but vicious countertrend moves.

The advantages of simple trend-following systems are:

- They provide guaranteed entry in the directions of the major trend.

- They are profitable over multiple markets and multiple time frames, as long as time frames are 6 months to 5 years in horizon.

- These systems are usually robust.

- These systems have well-defined risk-control parameters.

The 65sma-3cc Trend-Following System

This section discusses how to formulate and test a simple, nonoptimized, trend-following system that makes as few assumptions as possible about price action. It arbitrarily uses a 65-day simple moving average of the daily close to measure the trend. Sixty-five days is simply the daily equivalent of a 13-week SMA (13 × 5 = 65), representing one-quarter of the year. This is an intermediate length moving average that will consistently follow a market’s major trend.

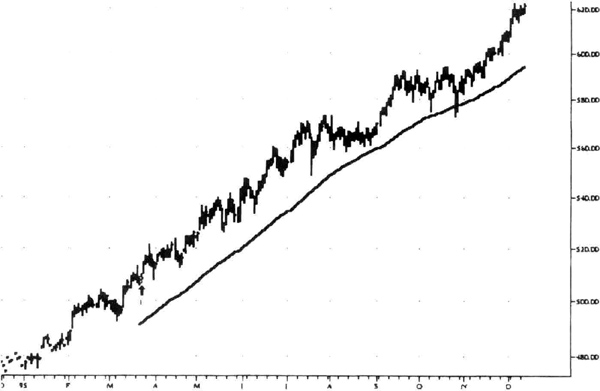

As shown in Figure 4.1, when the market is trending up, prices are above the 65-day SMA, and vice versa. In sideways markets, this SMA flattens out and prices fluctuate on either side. Clearly, the trading system picks up and sticks with the prevailing trend (see Figure 4.2).

There are many ways to make the decision that the trend has turned up. The usual way is to use a shorter moving average of, say, 10 days, and decide that the trend has changed when the shorter average crosses over or under the longer moving average. If you decide to use a short moving average, its “length” will be crucial to your results. Another weakness is that often prices will move faster than the shorter moving average, so that the entries can seem rather slow.

Hence, the 65sma-3cc system will require three consecutive closes (3cc) above or below the 65-day SMA (65sma) to determine that the trend has changed. For example, the trend will be said to have turned up after three consecutive closes above the 65-day SMA. Similarly, the trend will have turned down after three consecutive closes below the 65sma. Once again, the requirement of three consecutive closes is arbitrary. It could be ten consecutive closes or any other number. Clearly, the results will vary with the number of confirming closes.

Figure 4.1 September 1995 Japanese yen contract showing the 65-day SMA and the signals generated by the system.

Figure 4.2 The 65sma-3cc system stayed long throughout this major uptrend in the S&P-500 index in 1995.

If you are afraid of false signals (see Figure 4.3), then the number of closes you use will act like a filter in reducing the number of trades. In a fast-moving market, requiring a large number of consecutive closes will give delayed entries (see Figure 4.4). Conversely, if a market is moving sluggishly, a small number of consecutive closes will give false signals. Thus, there is a trade-off here that determines how quickly you recognize a change in trend.

Once you recognize a change in trend, you still have to decide how to enter the trade. You should enter the trade on the next day’s open, to guarantee that you can execute the signal and get a fill. For example, if the three consecutive closes criterion is satisfied as of this evening’s close, you should buy at the market on the open of the next trading day. You will get a fill somewhere in the opening range the next day. It is likely that you will be filled near the top of the opening range for buy orders, and near the bottom of the opening range for sell orders. This slippage should be ignored, and just lumped into your $100 allowance for slippage and commissions. The main effect of this entry mechanism is that you are not filtering out any entry signals, and ensuring that you will put on this position the first time the entry conditions are satisfied.

Figure 4.3 The choppy sideways action in December 1995 British Pound generated a string of whipsaw losses for the 65sma-3cc system.

Figure 4.4 These swing moves in December 1995 crude oil produced many trades but small profits because the 65sma-3cc system does not have a specific exit strategy.

There are a number of choices on how to actually enter the trade. For example, you could enter the trade on the close of the third consecutive close above or below the 65sma. A second choice would be to enter the next day on a stop order beyond the previous, or a nearby, high or low. In effect, you would also filter out some entry signals, because you would not get a fill on every signal. This may be useful in situations where prices briefly spike beyond the 65sma during prolonged trends.

A third entry choice would be to delay entry for x days after the signal, and then enter beyond a nearby n-day high or low. This is another way to filter down the entry signals in order to find more profitable ones. Note that if you use a limit order for your entries, occasionally you may not be filled at all, missing the entry by just a few ticks. Hence, you should enter on the next day’s open to assure an entry into the new trend.

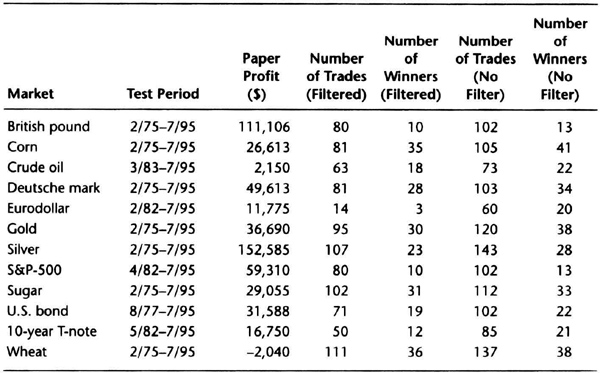

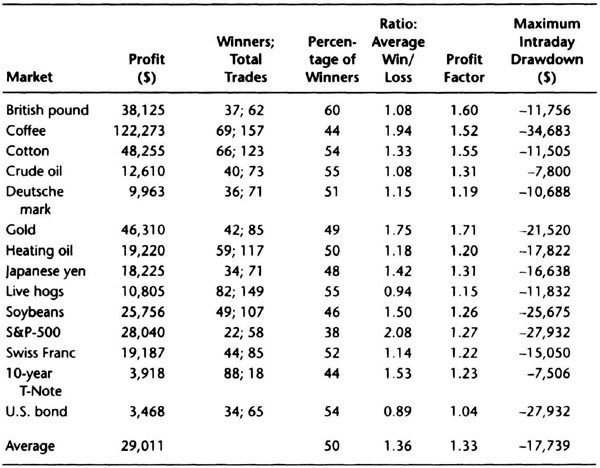

Before we proceed, let us put this entry signal through a critical test to check if the 65sma-3cc entries are better than random. Following the approach of Le Beau and Lucas (see bibliography for details), let us test the entry signal with exit on the close of the n-th day, without any stops, and no deductions for slippage and commissions. For simplicity, only the effect of long entries are shown. The proportion of trades that are winners should consistently be more than 55 percent. The test includes the long entry over 21 markets, stretching from January 1, 1975, through July 10, 1995, using a continuous contract. Because not all markets were trading back in 1975, all available data are used.

Table 4.1 shows that, on average, 55 percent of the long entries were profitable, suggesting that the 65sma-3cc model probably does better than random. The result for short trades is similar, and you can be reasonably confident that this model provides robust entry signals. Your task is now to combine this model with risk control and exit methods that match your trading mentality.

To summarize this nonoptirnized system, the actual trade entry is at the market on the open of the next trading day after the close of the day the signal is received. You will notice that there are no specific exit signals at this point, which means that the short entry signal is also the long exit signal, and vice versa. In practice this means that if you are long one contract, you will sell two contracts to go net short one contract, and vice versa.

Note that for the tests below we will add a condition to prevent back-to-back entries of the same type. This will allow an apples-to-apples comparison when studying the effect of adding stops or exits. You do not need this condition for actual trading.

To summarize what is not defined at this point: There are no specific risk-control rules in terms of an initial money management stop, nor any money-management rules to determine the number of contracts to trade. We will just trade one contract for simplicity without any risk-control stop. This is not a recommendation to trade without a risk control stop; the calculations are done without any stops here to illustrate a point. Later, we will examine how to add risk control and study the effect of money management.

Table 4.1 Testing 65sma-3cc long entry for randomness over 21 markets using all available data between 1/1/75 and 7/10/95. Exit on the close of the n-th day.

The 65sma-3cc system should make all its profits during strong trends. It should lose money in sideways or nontrending markets. And it should have between 20 and 50 percent profitable trades. We tested this model over 23 markets using 20 years of continuous contract data. If a contract was not traded for 20 years, then we used all available data from the starting date. The usual allowance of $100 per trade for slippage and commissions was made. Thus, this is a rigorous test for a nonoptimized system over a long test period, and across a large number of markets. The results are summarized in Table 4.2.

The results for this simple, nonoptimized trend-following system are encouraging. You could have made a paper profit of $1,386,747 by trading just one contract for each market, and been profitable on 19 of 23 widely diverging markets. The test sample generated 2,400 trades, so this is a highly significant test. Approximately 34 percent of all trades were profitable, a number typical of trend-following systems.

Table 4.2 Test results for 65sma-3cc trend-following system.

The ratio of average winning to average losing trades was excellent, at 3.3 averaged over the 2,400 trades. This number is useful for calculating the risk of ruin; a number above 2.0 is desirable, and anything over 3 is welcome news. The average trade made a profit of $558, an attractive amount, considering transaction and slippage costs. It is customary to seek a number over $250 for the average trade. The average profit per market was $60,293, approximately 2.74 times the average maximum intraday drawdown, of –$22,014. This is a healthy recovery factor, or coverage of the worst losing streak of the system.

In summary, a simple trend-following approach worked on many markets over a long time period with few assumptions and no optimization.

The results also point out some weaknesses of this system. The average profit per market is 90 percent of the standard deviation of the average profit. This means that profitability varied widely from market to market. The maximum intraday drawdown was 108 percent of its standard deviation, implying that the drawdowns also varied considerably among markets. The standard deviation of the average trade also implies that results can vary substantially over time or across markets. A further weakness is the relatively small number of profitable trades. Thus, we can summarize the principal weakness as a large variability in the results over time and across markets.

Combining the strengths and weaknesses, you would say that this is a sound trend-following system with good chance of being profitable over many markets over a long time period. But because of the large variability in results, you would have to trade this system relatively conservatively. You should allow a large equity cushion to absorb drawdowns.

A look under the hood of this trading system, so to speak, and a closer examination of the results of the analysis reveal further details of 65sma-3cc trades. A histogram of all 2,400 trades shows the distribution of trade profits and losses (see Figures 4.5 and 4.6). There are more large winners than large losers, and many small losers. Remember that these results were calculated without using an initial money management stop. Most of the trades are bunched between –$3,000 and $2,000, with the highest frequency near zero. There are few losing trades worse than –$5,000, balanced by even more trades with profits greater than $5,000. An initial money management stop will clean up the negative part of this histogram.

Thus, it should be obvious that most of the profits come from a relatively small number of trades. In Figure 4.6, 12.5 percent of the trades are seen to have closed-out profit greater than $3,000. Be aware that if you get out too soon, you are likely to miss one of 100 or so (4 percent) of the mega-trades that make trend-following worth the aggravation.

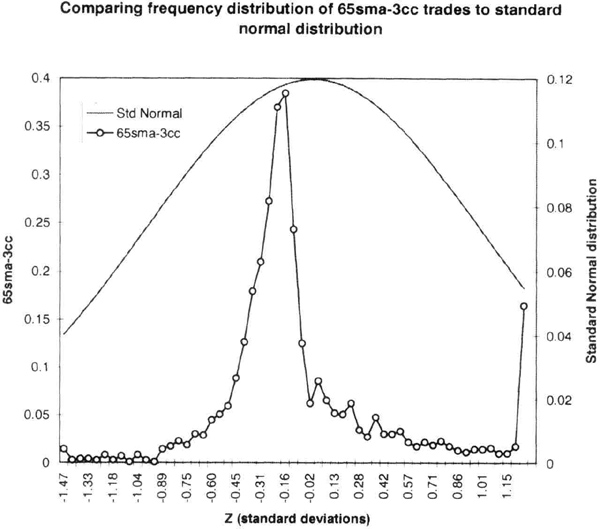

Many measurements follow what is called a standard normal distribution. For example, if you measured the diameter of ball bearings, the measurements will follow a normal distribution. The normal distribution is a bell-shaped probability distribution of the relative frequency of events. The standard normal is a special case of the normal distribution with a mean of zero and standard deviation equal to one. To compare the distribution of the 65sma-3cc trades to the standard normal distribution, we first have to “normalize” the bin sizes. The comparison is shown in Figure 4.7.

Figure 4.5 Histogram of all 2,400 trades for the 65sma-3cc trading system.

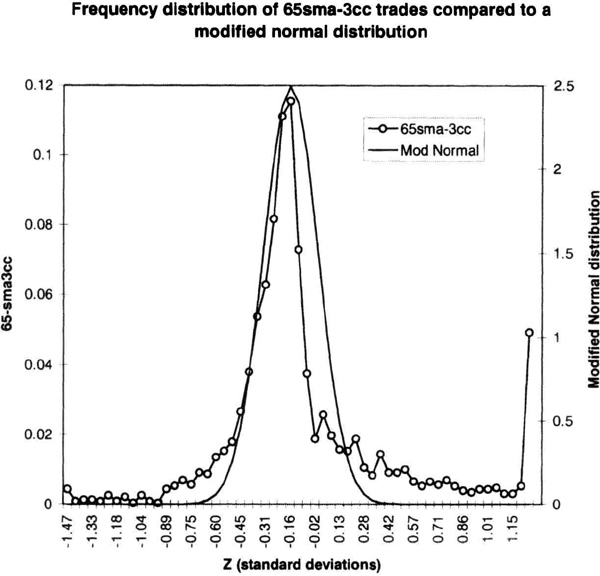

The 65sma-3cc curve is more sharply peaked than the standard normal curve. To generate a normal distribution that would fit our data, I used a Microsoft Excel® 5.0 spreadsheet and employed an iterative process of manually tweaking the values. The fitted normal curve, with a mean of –0.16 and standard deviation of 0.18 is shown in Figure 4.8. The fitted normal distribution shows that the actual 65sma-3cc distribution has “fat” tails. This simply means that there is a larger probability for the “big” trades than would be expected from the normal distribution. This chart shows that unusually large profits or losses are more likely than might normally be expected.

The modified normal distribution fits the observed curve nicely on the losing side, but the small positive trades fall off sharply. This implies that you will not get very many small positive trades with a trend-following model. Small trades will occur during broad consolidations, and these are not very common. Small losing trades are more likely during consolidations, as shown by the good fit on the left side of the peak.

Figure 4.6 A histogram of the 65sma-3cc system over a narrower range of profits and losses. Notice that only a small number of trades show large profits.

The huge spike at the right-hand edge of the Figure 4.6 represents the 4 percent or so of mega-trades that make trend following worthwhile. The distribution shows you it is easy to miss these trades, and if you do, your portfolio performance will drop off quickly. You should try to develop such a frequency distribution curve for your own systems to get a better feel for model performance.

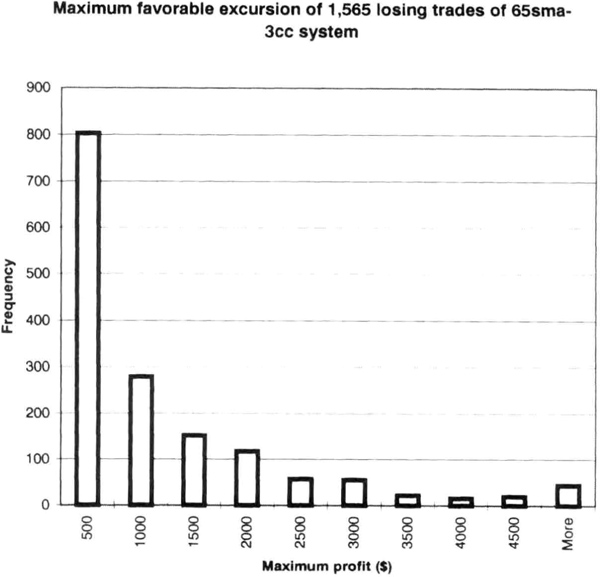

A closer look at losing trades reveals another weakness of the 65sma-3cc system. Figure 4.9 is a distribution of the maximum profit of each of the 1,565 trades that were closed out at a loss, called the maximum favorable excursion (MFE). The glaring weakness is that because there is no specific exit strategy, many trades with profits greater than $3,000 were eventually closed out at a loss. However, we have to be careful with our exit strategy, since only 4 percent of the trades were mega-winners. If we are not careful, we may lock in some profits from losing trades, but lose out on the truly big winners. Another way to use the information from the maximum favorable excursion plot is to select the profit point at which to move your trailing stop to break-even. For example, you can move your stop to break-even after a $2,000 profit and capture a significant proportion of losing trades.

Figure 4.7 The distribution of 65sma-3cc is peaked more sharply than the standard normal distribution.

You can also use the maximum adverse excursion plot to set profit targets for scaling out of large positions. For example, if you were trading ten contracts, you could sell some at each of the profit targets of $500, $1,000, $2,000 and $3,000. We continue our analysis by examining the maximum drawdown in 777 winning trades following John Sweeney (see bibliography for details). This drawdown is on an intraday basis. These trades show some loss, but were eventually closed out at a profit. The histogram (Figure 4.10) reveals several interesting insights. About 500 (64 percent) of the trades were immediately profitable, with a loss during the trade of less than –$250. Another 100 trades showed drawdowns of less than –$500.

Thus, almost 77 percent of the trades showed a loss of –$500 or less during their evolution. There were very few trades that showed losses greater than –$1,750 and then closed out at a profit. This suggests that we could set an initial stop at $1,000 and capture almost 88 percent of the winning trades. This is a realistic way to pick the point at which a mechanical initial money management stop could be placed.

Figure 4.8 A fitted normal distribution shows that the 65sma-3cc trade distribution has “fat” tails, and falls off more quickly for small positive trades.

The same information can be viewed as a cumulative frequency chart to see how many trades achieved a certain profit target (see Figure 4.11). This type of chart shows what proportion of trades had a maximum favorable excursion of, say, $500. It shows, for example, that 50 percent of trades had reached a $1,000 profit target, and so on.

In summary, the 65sma-3cc system test over 20 years of data and 23 markets showed it is a robust and profitable system that makes money in trending periods. Since we tested the system without any initial money management stop, there were several trades with losses greater than –$3,000. We can try to clean this up by placing a stop at $1,000, as shown by the MAE plot. The detailed analysis showed several profitable trades that were closed out at a loss. We would like to minimize such trades. There were about 4 percent truly huge trades with profits in excess of $5,000. We must find an exit strategy that does not miss out on such mega-profits.

Figure 4.9 A histogram of maximum profit in 1,565 losing trades over 20 years and 23 markets from the 65sma-3cc system. This is a maximum favorable excursion plot.

Effect of Initial Money Management Stop

Since the initial test of the 65sma-3cc model was encouraging, we can now do more testing. The first item of business is to insert an initial money management stop into this model. Our detailed analysis of the MAE showed that we could safely set our stop at $1,000, or even as high as $1,750, and capture substantially all profitable trades.

However, we should insert another condition into the formulation of the model before testing for the effect of initial stops. If our stop is too “tight” during testing, we will be stopped out right after the first signal. Then, there may be a succession of trades, all in the same direction (all long or short signals), that will also result in losing trades, before one of them kicks into the major trend. Thus, the analysis would be distorted. What we want is to pick off exactly the same trades as we did without any initial stop. To achieve this goal, we must insert rules that do not allow successive trades of the same type, to ensure that we will not have two back-to-back long or short trades if we get stopped out after the first signal. In effect, with this rule, if we get stopped out, we must wait for the opposing signal before getting in. Of course, you do not need this condition for actual trading.

Figure 4.10 Analysis of 777 winning trades: maximum loss in trades that were closed out at a profit. This is also known as the maximum adverse excursion plot.

Inserting an initial condition should have two effects. (1) It should reduce the maximum intraday drawdown, since some potentially large losing trades will be cut off. (2) It should also reduce the number of profitable trades and the total paper profit, since the same stop will also cut off some potentially profitable trades. Some calculations will show if we can verify these expectations.

The results of these calculations are shown in Table 4.3, which can be compared to the results in Table 4.2. The markets and test periods are identical in both tables. Adding a $1,000 stop reduces total paper profits by 21.5 percent, from $1,386,747 to $1,088,804. Similarly, the number of winning trades fell to 689 from 810, or by 17.6 percent. As expected, the average maximum drawdown and its standard deviation also decreased, showing the desired smoothing effect due to the initial stop. The reduction was about 18.5 percent in the draw down, and 40 percent in the standard deviation. Thus, adding a hard dollar initial money management stop had the desired effect of reducing drawdown and smoothing out the variation in system performance. There was also a resultant reduction in total returns.

Figure 4.11 Cumulative frequency of maximum favorable excursion of 65sma-3cc system. Note that horizontal scale is not linear.

We chose the $1,000 initial money management stop from the MFE plot. Calculations for a $500 stop result in an even greater reduction in profits, drawdown, and volatility.

We can continue this line of thought by looking at the U.S. bond and deutsche mark markets. Our analysis of 777 profitable trades showed that once the drawdown exceeded –$1,750, few trades ended with a profit. Hence, the initial stop is varied from $250 to $1,750 in the following tests to look at the effect on the total number of profitable trades. As the initial money management stop increases, the number of profitable trades increases and then levels off (see Figure 4.12). This shows that the initial stop acts as a filter, and as the stop widens, it allows more trades to pass through. Eventually, the filter is too big, and does not cut off any trades. This allows the number of profitable trades to level off.

Table 4.3 Effect of adding a $1,000 initial money management stop to the 65sma-3cc system.

We have so far placed our stop using a dollar figure without accounting for market volatility. However, whereas in the coffee market, a $1,000 stop may seem too tight, in the corn market it may seen too wide. Thus, in some markets, a given stop will work like a stop near the left edge of Figure 4.12, and, conversely, in other markets, the same dollar stop will work like a stop on the right side of the figure.

Figure 4.12 Effect of initial money management stop on number of profitable trades. As the stop tightens, fewer and fewer profitable trades survive. The upper line is for the deutsche mark and the lower line is for the U.S. bond market.

We can get around this problem by using a volatility-based initial money management stop. For our calculations, we can set an initial money management stop as a multiple of the 15-day SMA of the daily true range for measuring volatility. We use the same continuous contracts as in Table 4.2 to test the U.S. bond market with volatility-based stops ranging from 0.25 to 3.0 times the 15-day SMA of the daily true range.

Figure 4.13 shows that a stop set at less than 1.25 times the average volatility is too tight. Once the stop increases past 2.00, the paper profit increases and the drawdown increases. The drawdown is minimized at a 1.50 stop. This means there is a balance between being too tight or too loose. The same behavior can be seen very nicely in the live hogs market (see Figure 4.14).

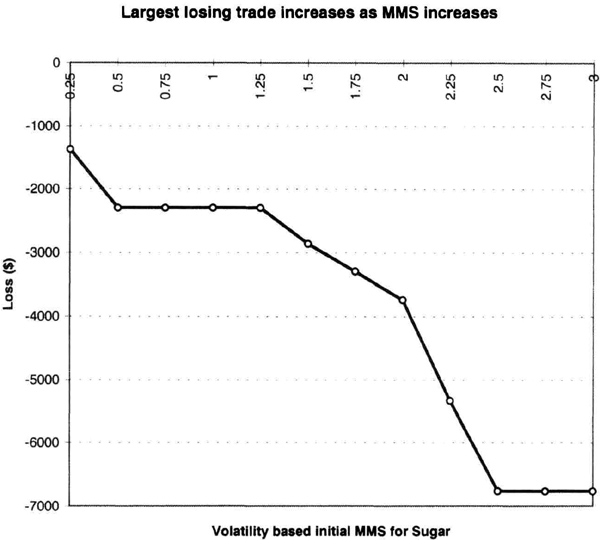

As might be expected, when we increase the money-management stop, the largest losing trade will probably increase. This happens because our stop is farther and farther away from the entry price. The sugar market shows this nicely (see Figure 4.15) when tested over the same period as Table 4.1. Other calculations (not shown) show that the largest winning trade is affected only a little by the initial stop, since these trades usually are profitable from the very beginning. You may set a volatility-based stop or a hard-dollar stop with equivalent results. You may have to set a different dollar stop for each market, although you could use the same volatility stop across all markets. Note that with a volatility stop, the actual dollar amount changes over time, and hence you must ensure that this stop is within your overall hard-dollar limits for risk control.

Figure 4.13 The profits (upper line) increase as the initial money management stop is loosened. Eventually, the stop is too wide and profits begin to level off. The lower line is the maximum intraday drawdown. Data are for the U.S. bond market.

You should note some limits on how the initial money-management stop can be tested. In most cases, the amount of the stop must be larger than the daily trading range. The software cannot determine if your stop could have been hit intraday if the stop is smaller than the daily trading range. Unless you have intraday data, you cannot test the effect of, say, a $250 stop using daily data.

In summary, adding an initial money-management stop is useful from a risk-control point of view because it reduces the largest losing trade and the maximum drawdown. But, it also cuts off some winning trades, and hence total profits are lower over the long term. You may add a dollar stop or a volatility-based stop, but both must follow sound guidelines.

Figure 4.14 The profits (upper line) increase as the initial money management stop is loosened. The lower line is the maximum intraday drawdown. Data are for the live hogs market.

Adding Filter to the 65sma-3cc System

So far, we have let the trading system generate pure signals without trying to filter the signals in any way. As we have seen, this system will generate many short-lived or “false” signals when a market is in a consolidation region. A filter is simply a set of rules that will try to refine the entry signals. By design, this system is always in the market. Remember that we do not have a specific exit strategy, and the long entry signal is also the short exit, and vice versa. At this stage, the goal of the filter is only to reduce some of the signals in a congestion area.

Figure 4.15 Largest losing trade for sugar using the 65sma- 3cc trading system increases as the volatility-based initial money management stop increases.

You can design many types of filters. Here we use a momentum-based filter using the range action verification index discussed earlier. The RAVI is the absolute percentage difference between the 7-day and 65-day simple moving averages of the daily close. This means that when the market is in a congestion or consolidation phase, the short (7-day) and long (65-day) moving averages tend to be close together. Conversely, when the markets are trending, these averages are far apart.

You can also use Wilder’s ADX (average directional index) as a filter for trending or nontrending markets. Specifically, if the ADX is declining, and/or below 20, then you can assume that the market is consolidating or entering a congestion phase. You could also use the x-day high-low range, or other momentum oscillators, to diagnose market conditions. Remember that any indicator you use, including the RAVI, will not work perfectly every time.

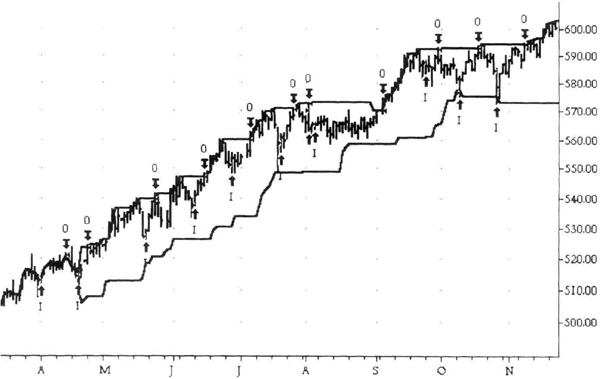

First, let us briefly review the performance of 65sma-3cc trading system in consolidating markets. As prices begin to trade in a narrow range, without a definite direction, the longer moving average (65sma) flattens out. Prices oscillate on either side of this average. Hence, you can get a succession of long and short signals as the market posts three consecutive closes above or below the 65sma.

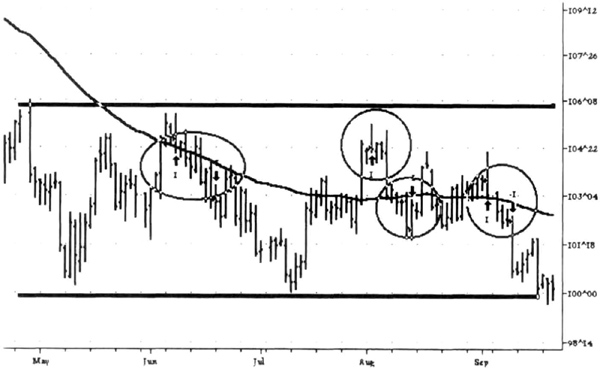

Figure 4.16 The 65sma-3cc trading system generated several entry signals as the U.S. bond market consolidated after its now-famous bear market tumble. The circled areas show the six signals—three long entries and three short entries—in this broad consolidation region.

In some sense, this becomes a self-correcting process, because the entry signals are not very far apart in price. Hence, even though you will have several losing trades in succession, the amount of the losses will be relatively small. You can imagine that in some cases the market will trade within a broad trading range, with sharp, but quick moves in both directions. The U.S. bond market has a tendency to form such consolidations. This is a worst-case scenario for the 65sma-3cc system because you will get short-lived entry signals but incur relatively large losses, since the market is making choppy moves that quickly span the trading range. Some examples of such market action follow.

Figure 4.16 shows the September 1994 U.S. bond contract consolidating after its now-famous bear market. Observe the six “false” signals from the system. Since the market was in a broad trading range, and prices were moving about on either side of the average, the false signals are inevitable given our definition of the trading system. This is a good illustration of a general principle: Whatever conditions you define, markets can always find ways to trigger false signals.

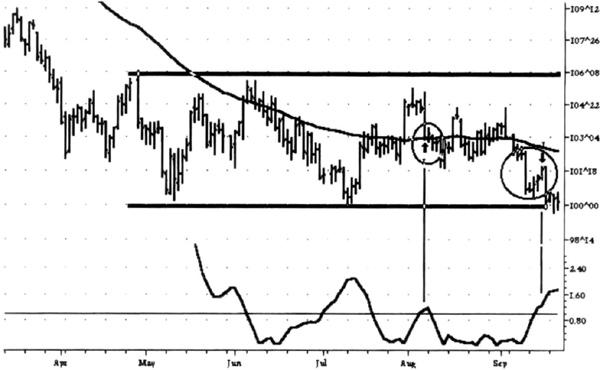

Figure 4.17 Adding a RAVI filter with barrier equal to 1.0 eliminates four of the six false trades in this broad congestion region. Notice that the 65sma-3cc model is fired only if RAVI is greater than 1 in both remaining instances.

Figure 4.17 shows the results of the same trading system with a filter. Now there are only two trades in the congestion region. The RAVI is plotted under the prices, so you can see that the signals occurred in regions where the RAVI was greater than 1. Since the model was already short coming into the picture, the first trade is a buy. The filtered model could generate a buy signal only if RAVI was greater than one and there were three consecutive closes above the 65sma.

A tight consolidation region developed immediately after the buy signal, dropping the RAVI below 1. Hence, this filtered out the next two signals, a sell and then a buy. Similarly, it also filtered out a buy signal and a sell signal in June. The last sell signal occurred when the RAVI climbed above 1 and there were three consecutive closes below the 65sma. Thus, we used the level of the RAVI to filter out some whipsaw signals.

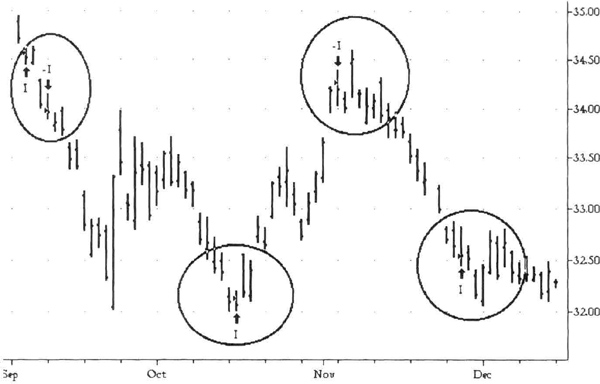

What should be the barrier value for the RAVI to filter out signals? There is no perfect answer to this question; you will have to pick a value using one method or another. Raising the RAVI barrier to 1.5 from 1 will filter out even more trades. As Figure 4.18 shows, this model would have been short from the previous October 1993, all the way down and through two major consolidation areas, for a per contract profit of $13,696. Notice how the RAVI rose strongly above I when the trend gathered strength, peaking just before the start of the lower consolidation phase.

Figure 4.18 Increasing the RAVI filter barrier to 1.5 eliminates even more trades.

These figures illustrate that you can use a filter to reduce the number of trades from a trend-following model. You can use different filters, and for a given filter you can use different barrier levels. Note that this system still is in the market at all times: either long or short.

By now, the effects of adding a filter should be clear: (1) We filter out some false signals; (2) we can reduce the maximum intraday drawdowns; (3) we can improve the profit factor of a system, i.e., the ratio of gross profit to gross loss over the test period; (4) the average trade usually increases; and (5) the length of the average winning trade increases. Our results will depend on how we choose the filter and its barrier level.

These comments can be supported with more data. Table 4.4 shows the results of calculations for adding a 0.5 percent RAVI filter to the 65sma-3cc model with a $1,000 initial stop and $100 deducted for slippage and commissions for 14 arbitrarily selected markets. These markets are a broad basket of softs, grains, metals, energies, currencies, and index and interest rate contracts. You can compare them to Table 4.2 for an estimate of their performance without stops or filters.

Table 4.4 Effect of adding a filter of RAVI = 0.5 to the 65sma-3cc system; filtering reduces the number of trades.

Table 4.5 shows the effect of the 0.5 percent RAVI filter on the dollar value of the average trade. The filtered system has a higher average trade, reflecting the improved quality of the entries.

Tables 4.4 and 4.5 show that as you filter a trading system, the number of trades decreases, the average trade increases, and the profit factor improves. These results are sensitive to the filtering rules. You can choose to filter a system many different ways. For example, you can use the ADX instead of the RAVI. Again, you have to make trade-offs in every choice you make.

In summary, we took the 65sma-3cc trend following system and tested its performance over 20 years of data and 23 markets. Then, we analyzed the winning and losing trades to select an initial money management stop. We filtered the system to reduce the number of signals. We used a “one-way” model, which does not allow back-to-back long or short trades. The main advantage of using a one-way model for testing is that it allows an apples-to-apples comparison of changes in trading strategy. You do not need this restriction for actual trading.

We have not tried to manage the equity curve in each of our analyses; the system was allowed to run to maximize profits. However, this system was always in the market. If we add a neutral zone, the system will not be always in the market. We can also consider adding one or more exit rules to get a smoother equity curve. With a bit of luck, the exit strategy will also create a neutral zone.

Table 4.5 Adding a filter increases the average trade.

Adding Exit Rules to the 65sma-3cc System

Selecting general and powerful exit rules is a difficult challenge in system design because the markets exhibit many different price patterns. One form of exit that is particularly easy to implement is the initial money-management stop. If the stop is hit, you exit the trade, no questions asked. However, taking profits is another matter, since you must design reentry rules should the trade continue on after meeting your exit criteria.

In the 65sma-3cc system, the approach of using entry rules as exit rules does catch long trends, but at the cost of wide swings in account equity. Hence, including exit rules tends to smooth out the equity curve. If possible, you should trade multiple contracts in each market, assigning one or more contracts to each exit rule. This allows you the luxury of not having only one “best” exit strategy.

As an alternative to the entry-triggers-exits approach, you can consider many exit strategies. One simple rule is to use a fixed-dollar trailing stop. In this case, you will set a stop, say, $1,500 away from the point of highest equity in the trade. Instead of a fixed-dollar stop, you can use a volatility-based stop, which sets a stop some multiple of the true-range away from the point of highest trade equity. Yet another exit strategy is to use a time-based stop, such as the price extremes of the last n-days. Another effective exit strategy is to exit on the close of the n-th day in the trade. For example, you could exit on the close of the fifth day in the trade. This approach works nicely if you can trade multiple contracts, and arrange to close trade from say the fifth through the twenty-fifth day in the trade.

Table 4.6 Effect of adding an exit on number of days in the market.

If you use exit strategies without an effective reentry strategy, you will miss significant moves. Hence, it makes little sense to use a trend-following strategy and then to cut off trades with a sensitive exit strategy. Exit strategies offer many opportunities for discretionary approaches. Hence, if you wish to use discretion, exit strategies are a good place to focus your attention.

An example of the effect of adding a 14-day exit to our 65sma-3cc model run with a 0.5 percent RAVI filter and a $1,000 initial money-management stop is shown in Table 4.6. The trailing exit closes out a trade if prices exceed the previous 14-day range. For example, if long, we would exit a trade tomorrow on the open if today’s close is lower than the lowest low of the last 14 days. This is a trend-following exit that should get you out near the end of a major trend, with the criterion being a 14-day reversal in prices.

Adding an exit condition decreased the days in market by 45 percent on average. At the same time, you can confirm that the profitability and maximum drawdown decreased also. Any investments you make in money market instruments during the time that the system is out of the market will add to your total return. Thus, as you make the model more restrictive, the overall profitability is restricted also. Your choice in this case is governed by your preference for a smooth equity curve versus growth in equity.

Channel Breakout–Pullback Pattern

This section discusses a trading system based on a pattern observed in mature markets, that is, markets with a large volume of institutional activity. In these markets, the big players have a tendency to fade market moves. Thus, they will resist advances and support declines. For example, when a market makes a new 20-day high, many big players will short it heavily, and push the market back into the previous consolidation. If the fundamental forces underlying the market are strong, the up trend will resume after a brief consolidation. A trading system that trades the long side only, by going long during the pull-back after new 20-day highs, is called the channel breakout–pullback (CB-PB) system.

We begin with a few examples of how the CB-PB system works, and show the actual code used for the tests. Next, we test the basic CB-PB entry strategy across 22 markets to illustrate the general validity of the idea. Then, we discuss three different exit strategies to show how you can convert the same entry strategy into vastly different trading systems. These systems vary from a short-term system, which is in the market for 7 to 9 days, to a long-term trend-following system. We will also explore the effect of using a $1,500 “close” initial stop versus a $5,000 “wide” stop. The analysis focuses on the following mature markets: coffee, Eurodollar, Japanese yen, Swiss franc, S&P-500, 10-year T-Note, and the U.S. bond.

The channel breakout-pullback pattern is for long trades only. The assumptions underlying this system are:

- The market will begin an uptrend after the consolidation ends, because it has recently made a new 20-day high.

- The entry during the consolidation is a low-risk entry point.

- Exits could be placed at the nearby 20-day high, by using trailing stops, or by exiting after x-days in the trade.

The reality is that markets may have an extended consolidation after making a new 20-day high, or could even make new 20-day lows. Hence, a bias to the long side may be correct only 50 to 70 percent of the time. It is also difficult to find consistent exits, since the markets do not follow the same script every time. Hence, another difficulty with the CB-PB system is finding a consistent exit strategy. A third area of difficulty is where to place the initial stop. If the market rolls over and starts a new downtrend, then an initial stop is critical for risk management and loss control, whether it is a simple-dollar stop or a volatility-based stop.

The first example of the CB-PB pattern uses the March 1995 deutsche mark contract. Figure 4.19 shows the daily bars and, superimposed on the bars, the 20-bar trading range. The 20-day range lines have a 13-tick barrier added to both the lines to filter out some false breakouts. The chart shows that the deutsche mark broke above its 20-day range in December 1995 and then consolidated for 7 days before moving higher. Upon moving higher, it made a higher high, and consolidated again.

Figure 4.19 The deutsche mark pulls back after making a new 20-day high. The goal is to buy after the pullback. The 20-day price channel is shown for visual reference.

Ideally, we would like to buy some time during the pullback, but we do not know how long the pullback will last. Hence, the problem is how to specify that a pullback has occurred. During the pullback, markets often also make new 5-day lows. Hence, we can define this breakout and pullback long entry rule as follows: the market must make a new 20-day high, and then define a 5-day low in the next 7 days. Once it forms a 5-day low, buy on the open the next trading day. These choices are arbitrary, and you can experiment with these numbers. For example, we can buy on the close instead of on the open after the market forms a 5-day low following a 20-day high.

We now need an exit condition to evaluate this entry rule. To keep it simple, we will exit on the close of the n-th day in the trade, with n = 5 for short-term systems and n = 50 for intermediate systems. Again, these numerical values are arbitrary. You may try other values, such as a 3-day low instead of a 5-day low.

Using the Omega Research TradeStation Power Editor™, the rule appears, in part, as:

Input: Xdays (14);

If Highest Bar(High, 20)[1] < 7 and Low < Lowest

(Low, 5)[1]

then buy tomorrow on the open;

If BarsSinceEntry = Xdays then exitlong at the close;

The first line defines “Xdays” as an input-variable with a default value of 14 days. You can change this value during testing. The Highest Bar function returns the number of bars (trading days) since the 20-day highest high. The second line first checks if 7 or fewer days have elapsed since the new 20-day high. Then, it checks if today’s low is lower than the previous 5-day low (i.e., a new 5-day low). If both conditions are true, then you can buy tomorrow on the open. By default, this system will buy one contract. The third line is the exit condition, which says that if today is the x-th day since entry, then exit the long trade at the market on the close. This system will fill the long trade at the opening price of the entry day, and at the closing price of the exit day.

There is a quirk in how the Highest Bar function works. The function counts 20 days back from the day it is testing. Hence, the function will occasionally give a signal that does not work off the highest high as intended. Hence, to accurately pick off the highest high of the last 20 days, the rule should say Highest Bar(High,27)[1]. However, the difference in the results over the long run is insignificant.

Figure 4.20 shows that the March 1995 deutsche mark chart with a 14-day exit worked well. The first breakout occurred on December 28, 1994, and the pullback entry occurred on January 9, 1995, at the open of 64.11, which was the exact low of the ensuing 14 days. The exit was on the close of January 30, 1995, at 66.52, for a profit of $2,913, after allowing $100 for slippage and commissions. The next entry occurred on February 1, 1995, on the open at 65.65. The low of the trade occurred four days later at 65.07, for a 58-tick risk of $725. The exit was on the close of February 23, 1995, at 68.19. The nominal profit was $3,075.

Figure 4.20 The CP-PB strategy gave good trades with low-risk entry points.

Thus, the CB-PB system generated low-risk entries into an emerging up trend in the March 1995 deutsche mark contract. The exit on the 14th day was a lucky choice for this chart. You could use a number based on your individual preference just as well.

Note here that we specified a generic entry pattern with no specific assumptions about DM price patterns. The exit was again arbitrary. Of course, if you had exited on the fifth-day close instead of the fourteenth-day close, the profits would have been smaller. Note that the CB-PB pattern offers a relatively low-risk entry method. You can use it as a short-term system or a long-term system by simply varying the exit strategy.

So far, the exit strategy has been trend-following in nature, with some variation based on the actual day of the exit. For example, we could vary the exit from 5 days to 50 days and get completely different results. However, we will never make the “perfect” choice of x days. We can anticipate market action in a different way that does not use time as the exit signal. Instead, we will use a price we already know. Since we are buying a pullback, it is plausible to assume that the market will retest the recent 20-day high. Hence, we can write an exit signal that buys the pullback and exits the retest of the recent high. Here is how we would write the new system variation in TradeStation™:

If Highest Bar(High, 20)[1] < 7 and Low < Lowest

(Low, 5)[1]

then buy tomorrow on the open;

Exitlong at highest(h, 20)[1] limit;

The first line of the CB-PB rule is exactly the same as before. The second line specifies a long exit for tomorrow with a limit order at the most recent 20-day high. This turned out to be the “perfect” model for the December 1995 S&P-500 contract. There were 12 winning trades in a row, with a total profit of $50,000 (see Figure 4.21).

The noteworthy feature here is that we started with the DM contract, using very general price patterns, and arrived at an intriguing short-term system, which performs particularly well in choppy up-trends. We made no contract-specific assumptions, and captured a general market behavior that we can expect to see in every market in the future. The CB-PB entry with an exit at a recent high works well in consolidations.

Another exit strategy involves a trailing stop, but one that will not cut off long trends prematurely. Hence, we will exit at the lowest low of the last 40 days. This will convert CB-PB into a long-term trend-following system.

Figure 4.21 The CP-PB model with exit at the recent 20-day high using limit orders produced 12 winning trades in a row for a nominal profit of $50,000.

If Highest Bar(High, 20)[1] < 7 and Low < Lowest

<Low. 5)[1]

then buy tomorrow on the open;

exitlong at lowest(low, 40)[1] - 1 point stop;

The CB-PB entry rule remains intact. The second line exits on a stop set one tick below the trailing 40-bar (trading days) low. You can see that this will become a trend-following exit. Our initial stop will close out our trade should the market head lower. The trailing stop at the 40-bar low will keep us in the trade through minor consolidations.

Notice how we took an intuitive understanding of a market pattern and adapted it to three different exit philosophies to meet specific trading preferences. Remember you could use it as a short term system by exiting at the recent high. You could exit on the close of the n-th day in the trade, for short- or intermediate-term trading. Or you could use a trailing stop. Each exit produces a trading system with different characteristics off the same entry signal. These are the types of modifications you should consider as you look at trading systems. Figure 4.22 from the March 1995 U.S. bond market will help you visualize the three exit strategies.

Now let us take a closer look at the entry signal, to see if it is any better than a random entry system. Following the suggestion of Le Beau and Lucas (see bibliography), we will try to isolate the effect of this CB-PB entry signal.

Figure 4.22 The CB-PB gave a low risk entry into the new trend for the March 1995 U.S. bond contract.

We test the CB-PB entry signal with exit on the close of the n-th day (n = 5, 10, 15, and 20), without stops and assuming no slippage or commission costs. Le Beau and Lucas suggest that if the entry signal is performing better than a random system, it should result in at least 55 percent profitable trades over a range of markets. They tested only 6 years of data and 6 markets to measure a signal’s ability to perform better than random. Here we use 22 markets and continuous contracts using all available data from January 1, 1975, through July 10, 1995. This should be a severe test of this entry signal, and our goal is to check if it is consistently profitable more than 55 percent of the time.

Table 4.7 shows that about 55 percent of all CB-PB entries were profitable. Hence, you can be reasonably confident that the CB-PB entry signal provides better than random entries. You can now marry this entry signal to a variety of risk control and exit strategies to fashion a trading system that fits your trading mentality.

The first exit strategy is simply to exit on the close of the n-th day in the trade. You are making the working assumption that the market is going to trend after the entry signal. Hence, consider now the CB-PB entry using continuous contracts, $1,500 initial stop, and allowing $100 for commissions and slippage. As discussed at the beginning of this section, we are focusing on “mature” markets. Let us consider the case when we exit the long trade on the close of the fifth day. The test uses all available data from January 1, 1975, through July 10, 1995.

Table 4.7 Percent winning trades for CB-PB entry signal calculated over all available data from January 1, 1975, through July 10, 1995.

The results of exiting on the fifth day of the trade are not impressive (see Table 4.8). Since we are buying the markets during a consolidation, most of them have not done much in the 5 days after entry. Hence, we should consider holding on to the long trade for a little while longer.

Consider what happens if we hold the long position for 50 days, exiting on the close. The conditions for the test are identical to those for Table 4.8. Table 4.9 shows there is a dramatic improvement in performance with n = 50 days. The average profit per market has increased three-fold, and the profit factor is up 46 percent. Thus, our basic assumption that the market will trend after the consolidation seems to work well about 39 percent of the time on these markets. Thus, we have converted our anemic short-term system into an interesting intermediate term system by exiting on the close of the fiftieth day.

We have previously stated that the initial stop should depend on market volatility. For example, the $1,500 stop may be “too close” given the volatility of the S&P-500 market. For the CB-PB system with exit on the 50th day using a $5,000 initial stop instead of the $1,500 initial stop, the profits dropped for all markets in Table 4.9 except S&P-500. Profits for S&P-500 increased to $141,840 on just 55 trades with 56 percent winners, a $2,579 average trade. The maximum drawdown was –$24,795, with the profit factor increasing to 2.29 from 1.62. Hence, the initial stop will influence overall system performance.

Table 4.8 CB-PB long trades with exit on the 5th day using $1,500 initial stop, tested on all available data from January 1, 1975, through July 10, 1995.

Table 4.9 CB-PB long trades with exit on the fiftieth day, using $1,500 initial stop, tested on all available data from January 1, 1975, through July 10, 1995.

Table 4.10 CB-PB long trades with exit on a trailing stop at the 40-day low, using $1,500 initial stop, tested on all available data from January 1, 1975, through July 10, 1995.

We can continue to explore the long-term nature of this entry by using a trailing stop. We know from Table 4.9 that we should use a trailing stop that will allow trends to develop. Hence, let us arbitrarily specify an exit on the lowest low of the last 40 days; this should convert the intermediate system into a long-term trading system. As before, we will use $1,500 initial stop and allow $100 slippage and commissions.

Table 4.10 shows the long-term performance of this entry with a profit factor of nearly 3 and an average trade of $1,082. The ratio of net profits to drawdown is more than 4.5. These numbers suggest that you can take the same entry and make it into a strong long-term trend-following system.

Let us now take the CB-PB entry and attach it to an exit at the recent 20-day high. It is reasonable to assume that the market will retest the recent 20-day highs as part of the backing and filling during the consolidation. Table 4.11 summarizes the test results using a $1,500 initial stop and a $100 allowance for slippage and commissions.

The CB-PB system with an exit at the recent 20-day high was interesting only on the Eurodollar, S&P-500, 10-year T-note, and U.S. bond markets. The large proportion of winning trades makes this exit particularly attractive. Notice that the length of the average winning trade was only 9 days.

You can develop other variations of this strategy. For example, one of the design features of the CB-PB system is that we want a low risk entry point into long trades. Hence, you can use a multicontract trading strategy to improve performance. Another approach would be to add a filter to reduce the number of trades.

Thus, the CB-PB system has a flexible entry to suit many trading styles. The CB-PB strategy is more profitable with an intermediate to long-term trading strategy. A short-term approach worked on a few active markets. Note also how we can develop different systems from the same entry signal by changing the exit strategy.

Table 4.11 CB-PB long trades with exit at the recent 20-day highs on a limit, using $1,500 initial stop, tested on all available data from January 1, 1975, through July 10, 1995.

An ADX Burst Trend-Seeking System

We have assumed that the market was about to trend in both the 65sma-3cc and the CB-PB systems, although we did not actually verify that the market was trending because it is difficult to measure trendiness consistently. As was shown in the discussion in Chapter 3 on the range action verification index, market momentum is often a good measure of trendiness. Unfortunately, a certain amount of smoothing is essential to minimize noise in the indicator, and this smoothing usually causes undesirable lags in indicator response.

Figure 4.23 shows the March 1993 U.S. T-bond contract trending upward nicely from December 1992 through March 1993. The indicator under the daily bars is the 18-day average directional index. ADX measures the amount of activity outside the previous bar over a given period; a strong trend usually leads to a rising ADX line. An ADX reading above 20 is considered to indicate a trend, but the ADX is a lagging indicator, and there is little significance to any particular indicator value.

ADX is closely related to double-smoothed absolute momentum, and hence will often have quirky lags. The ADX will often seem to be late in signaling a trend, and choppy markets will not follow through in the original direction that caused the ADX to rise. In fact, the market can reverse strongly, and the ADX will keep on rising.

Figure 4.23 A rising 18-day ADX can be a good indicator of a trending market.

During a strong trend, as markets make big daily moves in the direction of the trend, the daily ADX momentum can “pop” over 1.0 point, an ADX “burst.” Figure 4.24 shows the March 1993 U.S. bond contract with the histogram of the ADX burst superimposed on the 18-day ADX line. As the trend accelerates, the daily ADX changes are more than 1, and you can see relatively large bars associated with this ADX burst activity. Now you can build a trading system using this idea as shown in Figure 4.25, where the entries are circled.

Obviously, the ADX burst indicates accelerating momentum. So, here the design philosophy has changed to begin with a check that increases the odds of success of a trend-following strategy. Notice that the ADX burst is itself triggering the trade, and that the ADX is not acting as a filter. For reference, you can look up a similar system in Lucas and Le Beau (see bibliography for reference). Our goal is to take the trade in the direction of the short-term trend. If the 3-day SMA is greater than the 12-day SMA, then the trend is up, and vice versa. Table 4.12 shows the results using a simple 20-day exit strategy and allowing $100 for slippage and commissions, over all available data from Janury 1, 1975, through July 10, 1995.

The rather large profit factor suggests that the entries are effective in identifying profitable trades, so that an ADX burst is a good entry into strong trends. The profit factor is overestimated here to some degree because we are using continuous contract data. The results can be improved with multiple contracts, and you can try a variety of other exit strategies.

Figure 4.24 The histogram of ADX burst momentum shows daily changes greater than 1.

Figure 4.25 A trading system triggered by ADX burst with daily momentum changes more than 1.

Table 4.12 ADX burst system performance with $5,000 initial stop.

If you compare the number of trades here to that for the 65sma-3cc system, you will find that you have fewer entries, suggesting that the ADX burst is working as both a trade filter and a trigger. For example, this system was in the market about 3 5 to 45 percent of the time, indicating it has a rather large “neutral zone.” A trading system with a neutral zone is out of the market unless it rises above stiff entry barriers. The 65sma-3cc system is always in the market, and is a reversal-type system, whereas the ADX burst system steps aside 55 to 65 percent of the time.

We used a wide initial stop of $5,000 in these calculations to isolate the performance of the system. Table 4.13 includes performance data on selected markets with an initial stop of $1,500. The performance with the two different initial stops was generally similar.

One of the quirks of the ADX burst system is that it will often get in late, near the tops or bottoms of short but swift moves (see Figure 4.26). Such moves fire its entry signals, but the capricious market fails to follow through with a trend in the advertised direction. Hence, you should always trade a system such as this one with a preplaced stop loss order.

Table 4.13 ADX burst system performance with a $1,500 initial stop.

In summary, the ADX burst system provides entries into strong trends. It tests well across many markets and over long time periods. The system has a large neutral zone, so it is in the market only 35 to 45 percent of the time. It differs from the 65sma-3cc system, which is always in the market, and does not have a trend filter. You can use it to enter trades or increase the position in those markets. You can derive other variations using different values of the ADX burst, the look-back period for the burst calculations, and other exit strategies.

Figure 4.26 The June 1990 U.S. bond contract sells off beyond a trading range to make a new low with good momentum. The system kicks in with a short. The bond market soon reverses, to get back into the prior consolidation region.

A Trend-Antitrend Trading System

In this section we explore the trend-antitrend (T-AT) system, designed to switch automatically between an antitrend mode and a trend-following mode. You will like this system if you aggressively like to fade the market, but do not mind reversing into a with-the-trend position if needed. This system shows you that trend following is not the only way to trade the markets. Many institutions and money managers, with their deep pockets, big positions, excellent execution, and low costs, usually assume the market is ranging. These sophisticated souls will be selling new highs and buying new lows. Of course, the difference is in the trading time frames: They are in and out a dozen times, before most of us are warming up to the trade.

The challenge in this type of system is to find a consistent basis to define when to trade with the trend and when to fade it. Markets will often make new 25-day highs or lows, but without strong momentum. This can be interpreted to mean that the market is likely to reverse, so we should try to sell the highs and buy the lows. However, if the market then goes on to make news highs or lows with increasing momentum, we must immediately reverse into a trend-following position.

For this system, we will use the 18-day ADX to measure market trendiness, and an 18-day SMA of the ADX as the reference. If the ADX is above its own 18-day SMA, then the market is trending, and we will buy new highs, and sell new lows. Conversely, if the ADX is below its 18-day SMA, we will sell new highs, and buy new lows. Since we will be going against the short-term trend, we must use an initial risk control stop, or the losses will be unbearable.

We must also decide how to enter the trade. For simplicity, we will enter on the open of the next trading day. We can use the usual 20-day exit to check on the trend-following aspects. Again, for simplicity, we will test this system without specific exits, so that the entries also serve as the exit for the opposite position.

You can see how this trading system works in Figure 4.27 from the September 1993 U.S. bond contract. The market formed a base during a congestion phase, and then rallied strongly, experiencing one brief sideways period. Observe how the model readily fades new highs, and then quickly reverses in the direction of the trend. This system picked off the top and bottom cleanly during the consolidation in April and May. It was long coming into the rally off the May bottom. It hiccuped twice, in June and August, but quickly returned to the underlying long trend.

Figure 4.27 The trend-antitrend system in action on the September 1993 U.S. bond contract. Notice how it picked off turning points nicely during the consolidation. It detected two turning points during the uptrend, but quickly reversed to follow the up move.

As Figure 4.27 shows, the T-AT system caught some turning points very well. This system will also see turning points that turn out to be insignificant, and, of course, there will be some turning points that it will not notice at all. The drawback of the T-AT system is the potential for significant loss as it switches fruitlessly between its anti-trend and trend-following modes.

The usual T-AT system worked beautifully on the December 1985 deutsche mark contract (see Figure 4.28). The DM was defining a broad consolidation region after a down trend. Note how the T-AT system quickly reversed to long in September after a premature short signal. The subsequent market turns were timed flawlessly. This is quite remarkable for a mechanical system using a single trend-checking rule.

You must use good risk control with this system, since the market could move against the position in a vicious countermove. The June 1995 deutsche mark contract provides a good illustration of this (see Figure 4.29). The T-AT system signaled a perfect short trade within a day of the actual contract high. Then, it correctly picked off the bottom of the quick sell off. However, it rolled over to short during the brief congestion and then was short through the volatile countermove in late May. Trend-antitrend trading requires great faith in the system and rigid risk control, with the added benefit that the risk/reward ratio can be excellent.

Figure 4.28 The T-AT system picked off turning points flawlessly in this December 1985 deutsche mark contract. Notice how it quickly returned to a trend-following mode in September, as the market drifted lower.

Figure 4.29 The June 1995 deutsche mark contract illustrates how the T-AT system can get trapped by a volatile countermove.

The June 1995 deutsche mark contract also illustrates the difficulty of using a heavily smoothed ADX indicator in volatile markets. The same smoothing that desensitizes ADX works against it if the market is choppy and thin.

Another quirk of the T-AT system is that it will often be slow in signaling a countermove if the market is drifting slowly, as the December 1993 cotton contract was doing near the summer top. T-AT logic correctly picked the first low (see Figure 4.30), but had to sit through the ensuing double bottom in November before the trend turned up. Once again, we have the hiccup at the start of the trend, with the system quickly reversing into the intermediate trend.

Let us briefly explore how this system was actually written, using the Power Editor from Omega Research’s TradeStation™ software. There is only one input variable, the length of the breakout period, currently set to 25 bars (days). The antitrend entry at a new 25-day high is written as follows: if today’s high was the highest high of the previous 25 days, but the 18-day ADX was below its 18-day SMA, then sell tomorrow at the market on the open. The countertrend buy signal is also similar.

Figure 4.30 The T-AT system was slow to respond to the market drift in the summer for the December 1993 cotton contract. It correctly picked the first dip of the eventual double bottom.

If high > highest (H.25)[1] and ADX(18) < average (adx(18), 18) then sell tomorrow on the open. If low < lowest (L, 25)[1] and ADX(18) < average (adx(18), 18) then buy tomorrow on the open.

This approach gives a symmetric long and short sell order on an antitrend basis. Let us assume you have a long position near a potential bottom. However, the market bounces up for a few days, and then reverses to begin a strong downtrend. In this situation, you want the system to switch to a short trend-following position only if it is long to begin with. Similarly, a new 25-day high with rising momentum is your signal to switch to a long position if you were short to begin with. Thus, the trend-following entries are similar to the antitrend entries, but you should first test if the system is short or long.

If MARKETPOSITION(0) = 1 and low < lowest(L.25)[1] and

ADX(l8) >

average(ADX(18), 18) then sell tomorrow on the open.

If MARKETPOSITION(0) = −1 and high > highest(H, 25)[1]

and ADX(18) >

average(ADX(18), 18) then buy tomorrow on the open.

Here MARKETPOSITION is a special built-in function that returns 1 if the system is long, and −1 if the system is short. Once again, we have the symmetric conditions for long reentry. If we sell a new 25-day high, but the market makes new 25-day highs with increasing momentum, then the T-AT system switches to long. A similar condition holds for the short reentry.

By design, the T-AT system first tries the antitrend entry, and with-the-trend positions occur on reentry. Therefore, you should remember that this system will lose money as it hunts for a reentry market condition. Of course, if the resulting trend is a long one, then the loss at reentry will seem minor.

If you like this approach, you can try a number of variations. You could enter not on the open, but on the close or beyond the previous day’s high or low. You could also use a more sensitive reentry, as just a new 25-day high or low, not requiring the additional ADX conditions.

Table 4.14 shows the results of long-term testing on all available data from January 1, 1975 through July 10, 1995 with a $5,000 stop and allowing $100 for slippage and commissions. Only markets with positive results are included, since this strategy requires active markets.

Table 4.14 points out the strengths and weaknesses of the T-AT system. First, it does not work on all markets, and second, it generates a lot of trades. Hence, this is an expensive system to run, as shown by the drawdown numbers. The initial stop had to be rather wide, at $5,000, to allow a cushion for the antitrend component to work. However, the profit factor is healthy, as is the average trade. Hence, on mature and active markets, the T-AT system seems to work quite well. The strategy requires excellent risk control and good discipline to implement. You can now develop other variations of this system, adapting it to your trading preferences.

Figure 4.31 presents a frequency distribution of 1,311 trades generated by the T-AT system. This distribution is broader than the distribution for the 65sma-3cc system (see Figure 4.5). It also shows a spike near the $5,000 initial stop. Like the 65sma-3cc distribution, it also shows a spike for trades with big profits. Figure 4.32 shows this distribution normalized and compared to a fitted normal distribution. It is immediately clear that the T-AT trade distribution has “fat” tails compared to the normal distribution. Thus, the probability of a trade far from the center is much greater than the corresponding normal distribution. The tail on the profits side is fatter than on the losing side, suggesting that the entries are working well. Observe how the initial stop cuts off losing trades. However, there is no such cutoff on the profit side, as seen by the spike at the right edge of the distribution. This is the TOPS COLA principle introduced in Chapter 1 applied to a trading system in practice.

In summary, the T-AT system illustrates how to develop a system that automatically adjusts to market conditions. It differs from the 65sma-3cc system in that its initial stance is to take an antitrend position; the 65sma-3cc system always takes a position with the trend. A reversal condition switches the T-AT system from antitrend to a trend-following mode. The objective reversal condition assures entry in the direction of a major trend, thus allowing you to take advantage of all market conditions.

Table 4.14 Long-term performance of T-AT system over all available data from January 1, 1975 through July 10, 1995 with $5,000 stop and $100 for slippage and commissions.

Figure 4.31 Frequency distribution of T-AT trades showing a spike at the $5,000 initial stop and at trades with profit greater than $8,000.

Gold-Bond lntermarket System

This section develops intermarket trading systems for trading negatively or positively correlated markets. We begin with a quick review of the difficulties of formulating intermarket models. The gold-bond system is illustrated for negatively correlated markets and tested on other market combinations also. An example of using three markets for intermarket analysis is then given. Lastly, the gold-bond system is modified for positively correlated markets. This section will convince you that it is possible to develop interesting intermarket systems. You may have greater confidence in such systems because they contain a weak form of cause-and-effect relationships. Hence, they are often a good addition to your analytical tool set.

Figure 4.32 T-AT frequency distribution normalized and compared to a fitted normal distribution.

Many analysts have recognized intermarket relationships, which imply some form of weak cause-and-effect relationship. For example, bond prices decline when inflation is rising, and rising gold prices suggest potentially higher inflation. Therefore, we expect gold prices and bond prices to move in opposite directions (see Figure 4.33). You can also measure inflation with the prices of industrial metals such copper or aluminum. The idea is that increasing economic activity will raise the price of copper, and herald a rise in inflation. Therefore, we expect copper prices and bond prices to move in opposite directions (see Figure 4.34).

Other intermarket relationships occur with positive correlation. This means that the prices of some commodities rise and fall together. For example, rising crude oil prices suggest potential inflation, and we should expect gold prices to rise. You can use the currency markets as another good example of correlated markets. Exchange rates reflect long-term fundamental forces in the economy such as inflation and interest rates. Thus, we expect the U.S. dollar to decline at approximately the same time against other foreign currencies such as the Japanese yen and the deutsche mark. Thus, we should expect that Japanese yen and deutsche mark prices are correlated, and we should be able to generate buy or sell signals for one market from the other.

Figure 4.33 Bond (top) and gold (bottom) prices generally, but not always, move opposite one another. Thus, intermarket relationships are often imperfect.

Figure 4.34 The general inverse relationship between weekly bond (top) and copper (bottom) prices.

There are several difficulties involved with exploiting intermarket relationships. First, weak intermarket cause-and-effect relationships have time lags. Thus, the price of copper may rise for several months before bond prices begin to fall. This difference in the timing of peaks and troughs among related markets is called a time lag. The problem is that the time lags are neither constant nor consistent.

A second difficulty is that each market has its supply and demand forces, which will often distort the usual intermarket relationships. For example, we would expect copper and gold prices to move up or down at about the same time. However, there have been periods when gold and copper prices have moved in opposite directions (Figure 4.35). Thus, any systems built on intermarket forces will not be correct all the time.

A third problem is the internal technical condition of each market. Each market can become “overbought” or “oversold” at different times. The usual intermarket trends are broad trends, which could unfold over many months. Hence very short term trends in the markets can move opposite the cause-and effect relationship. Such movements can complicate your entry signals because they can trigger a risk control exit without changing the underlying trend.

Figure 4.35 An example of copper and gold prices moving in opposite directions in late 1994-early 1995.

All these issues influence the precise form of relationship you select for your system. You must also decide if you want to relate two markets or more than two markets.

The gold-bond system, which assumes that bond prices move in the opposite direction of gold prices, is a simple but effective example of how to construct an intermarket trading system. The system assumes that rising gold prices signal potential inflation and thus influence the bond market. We will use a dual moving-average crossover system, using arbitrary 10-day and 50-day simple moving averages to build the system. Here are the rules:

- If the 10-day SMA of gold crosses above the 50-day SMA, then sell the T-bond futures tomorrow on the open.

- Conversely, if the 10-day SMA gold crosses under the 50-day SMA, then buy the T-bond futures tomorrow on the open.

These rules say that an upside crossover of the moving averages signals rising gold prices and therefore predicts falling bond prices. Here we have not used any filters for the emerging trend in the gold market, but you could certainly use the ADX indicator. To use the ADX filter, simply require that the 14-day ADX be rising, and determine the direction of the short-term trend by comparing the 3-day SMA to the 20-day SMA. The specific rules for the ADX-filtered system are as follows:

- If the 14-day ADX is greater than its value 14 days ago, and if the 3-day SMA is below the 20-day SMA of the daily gold closes, then buy the bond futures on tomorrow’s open.

- Similarly, if the 14-day ADX is above its value 14 days ago, and the 3-day SMA is above the 20-day SMA of daily gold closes, then sell the bond futures on tomorrow’s open.

We tested both of these models on U.S. bond and Comex Gold continuous contracts from August 23, 1977, through July 1, 1995, with an initial $5,000 money management stop and $100 allowed for slippage and commissions. As discussed above, the short-term trends in the markets can be a problem for trade entry. The results are summarized in Table 4.15.

These results suggest that there is indeed a broad inverse relationship between gold and bond prices. However, from a trading perspective, only about half the signals are profitable. The filtered gold-bond system was significantly more profitable than the dual moving average crossover system, with about half the maximum drawdown. The gold-bond system could function as a filter to check whether the “trading environment” favors rising bond prices.

Table 4.15 Results of testing the gold-bond systems, August 21, 1977 through July 10, 1995.

We know that there are lags between the price movements among markets. Since a hint of inflation can move many other markets, we should check out the basic gold-bond system on other market combinations, such as the soybeans-bond, copper-bond and deutsche mark-bond combinations. The grain markets often signal inflation, and the soybeans market is used as a proxy for those markets. The copper market follows strength in the industrial sector and is a leading indicator of inflation. Lastly, interest rates signal broad forces in the economy that also influence the currency markets, such as the deutsche mark. We used the gold-bond system for negatively correlated markets with the same $5,000 initial stop, one contract per trade, and $100 for slippage and commissions, and tried to generate buy and sell signals for the bond market from the markets indicating inflation.

The data in Table 4.16 confirm that changing trends in markets heralding inflation can be used to trade the bond market. Of all the combinations tested, the copper market seems to provide the best indication. In every case, only about half of the signals were profitable. Thus, these systems follow the well-known principle of economic forecasting: if you must forecast, forecast often.