Statistics chronicling high-profile IT project failures abound in the literature and the press with some pundits suggesting that upwards of 66 percent of all IT initiatives prove unsuccessful in some measure. Although not all technology endeavors are outright failures of course, many exceed the predefined budget, lag woefully behind schedule, or are eventually rolled out with far fewer functions and features than originally suggested.[30] Histrionics and assaulting headlines aside, the stakes are incredibly high in this game as organizations spend billions of dollars on technology projects promising greater efficiency, business insights, and strategic effectiveness, all prerequisites to performing with any degree of success on today's global stage.

Although myriad reasons exist for IT project problems, a key contributor to the quagmire of murky results CIOs often find themselves trudging reluctantly through is a lack of alignment between the organization's strategy and the portfolio of initiatives pursued by IT departments struggling to keep up with user demands as discussed in the first three chapters. Information capital, the domain of the CIO, and a vital raw material to organizational success in the so-called "new economy" is only valuable in the context of strategy, and thus IT spending must align with the organization's stated strategic direction.[31] Should, for example, a company be pursuing a strategy of customer intimacy, attempting to create longterm bonds with its clientele by offering total solutions and unmatched customer service, its IT projects must be consistent with this overall direction if it hopes to derive value from its efforts. Investing heavily in customer relationship management (CRM) software would make strategic sense in this context because the resulting data may yield numerous insights to be used in fostering stronger bonds with current customers and attracting new shoppers to the company's value proposition (see Chapter 6). Conversely, an expensive and technologically challenging investment in software and systems to promote quality may deliver incremental improvements, but will eventually prove to be inconsistent with the company's customer intimacy strategy and lead to questionable longterm benefits, ultimately driving the wedge between IT and executive and line staff deeper.

To overcome this challenge, many IT groups are discovering the power of performance management, and particularly the Balanced Scorecard concept, as a means of demonstrating IT's alignment with overall firm strategy and clearly communicating the value of information technology in delivering the company's value proposition to all stakeholders, including customers, employees, boards, and regulators alike. These tools help IT organizations critically evaluate and ultimately execute their own strategies, ensuring they line up with corporate direction as discussed in Chapters 1 and 2 through the use of objectives and measures that can be tracked over time. This provides quick and valuable feedback that allows IT leaders to make necessary course corrections in their pursuit of alignment with corporate strategy. The pages ahead introduce the Balanced Scorecard system and describe how to use this powerful tool to drive efficiency, effectiveness, and strategic alignment throughout your IT organization. The chapter begins with a discussion of what has led to the prominence of the Balanced Scorecard and then describes the fundamentals of the system itself and a concise step-by-step guide of how to build a Balanced Scorecard for the IT organization. The chapter concludes with a case study of one IT group that effectively harnessed the Balanced Scorecard with a presentation of how they did it, what results they achieved, and the challenges they encountered along the way.

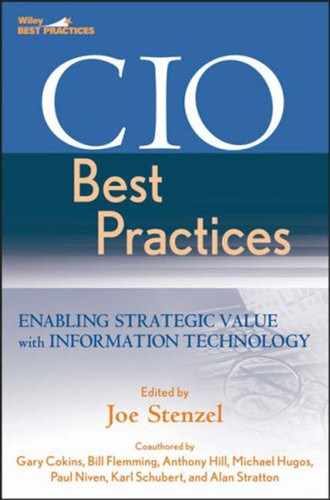

Born from a research study conducted in 1990, the Balanced Scorecard has since become a critical business tool for thousands of organizations around the globe. In fact, recent estimates suggest a whopping 60 percent of the Fortune 1000 has a Balanced Scorecard in place.[32] Further evidence of the ubiquity of the Balanced Scorecard is provided by The Hackett Group, which discovered in 2002 that 96 percent of the nearly 2, 000 global companies it surveyed had either implemented or planned to implement the tool.[33] Before discussing the structure of the Balanced Scorecard, let's examine its origins and attempt to determine just why it has become such a universally accepted methodology.

Three fundamental factors affect every organization, at times in gamechanging ways: (1) a reliance on financial measures of performance to gauge success, (2) the rise of value-creating intangible assets, and (3) the difficulty of executing strategy, all of which impact today's IT departments. While separate and distinct factors, the trio is bound together by the inspiring ability of the Balanced Scorecard to overcome and maximize them to their fullest potential.

As long as business organizations have existed, the traditional method of measurement has been financial. Bookkeeping records used to facilitate financial transactions can literally be traced back thousands of years. At the turn of the twentieth century financial measurement innovations were critical to the success of the early industrial giants like General Motors. That should not come as a surprise because the financial metrics of the time were the perfect complement to the machine-like nature of the corporate entities and management philosophy of the day. Competition was ruled by scope and economies of scale with financial measures providing the yardsticks of success.

In the twenty-first century, however, many are questioning our almost exclusive reliance on financial measures of performance. Perhaps these measures are better served as a means of reporting on the stewardship of funds entrusted to management's care rather than charting the future direction of the organization. And as everyone knows, stewardship is an increasingly vital issue in light of the many corporate scandals witnessed over the past several years, and the surge of shareholder value and job losses left in their wake. Here are some of the criticisms levied against the overabundant use of financial measures:

Not consistent with today's business realities. Today's organizational valuecreating activities are not captured in the tangible, fixed assets of the firm. Instead, value rests in the ideas of people scattered throughout the firm, in customer and supplier relationships, in databases of key information supplied by IT, and cultures capable of innovation and quality. Traditional financial measures were designed to compare previous periods based on internal standards of performance. These metrics are of little assistance in providing early indications of customer, quality, or employee problems, or opportunities. The rise of intangible assets is discussed in the next section of this chapter and again in the final chapter of this book (see Chapter 8, p. 342).

Driving by rear view mirror. Financial measures provide an excellent review of past performance and events in the organization. They represent a coherent articulation and summary of activities of the firm in prior periods. However, this detailed financial view has no predictive power for the future. Experience shows that great financial results in one month, quarter, or even year are in no way indicative of future financial performance. Even so called "great" companies, those that once graced the covers of business magazines and were the envy of their peer groups, can fall victim to this unfortunate scenario. Witness the vaunted Fortune 500 list; two-thirds of the companies compiling the inaugural list in 1954 had either vanished or were no longer large enough to maintain their presence on the list's 40th anniversary.[34]

Tend to reinforce functional silos: Financial statements in organizations are normally prepared by functional area: individual department statements are prepared and rolled up into the business unit's numbers, which are ultimately compiled as part of the overall organizational picture. This approach is inconsistent with today's organization in which much of the work is cross-functional in nature. Today we see teams comprised of many functional areas coming together to solve pressing problems and create value in never imagined ways. Regardless ofindustry or type of organization, teamwork has emerged as a musthave characteristic of winning enterprises in today's business environment. As an example, consider these three fields of endeavor: heart surgery, Wall Street research analysis, and basketball as played by the well-compensated superstars of the National Basketball Association (NBA). At first glance they appear to have absolutely nothing in common however, studies reveal that success in all three is markedly improved through the use of teamwork: surgeon interactions with other medical professionals (anesthesiologists, nurses, and technicians) is the strongest indicator of patient success on the operating table. When it comes to Wall Street "stars" it is not the individual analysts and their erudite calculations that spell success, but the teaming of analyst and firm. Even in the NBA researchers have found that teams on which players stay together longer win more games.[35] Our traditional financial measurement systems have no way to calculate the true value or cost of these relationships.

Sacrifice long-term thinking. Many change programs feature severe costcutting measures that may have a very positive impact on the organization's short-term financial statements. However, these cost reduction efforts often target the long-term value-creating activities of the firm such as research and development, associate development, and customer relationship management. This focus on short-term gains at the expense of long-term value creation may lead to sub-optimization of the organization's resources. Interestingly, an emerging body of evidence is beginning to suggest that cost-cutting interventions such as downsizing frequently fail to deliver the promised financial rewards nd in fact sabotage value. University of Colorado Business School professor Wayne Cascio documented that downsizing not only hurts workers who are laid off, but destroys value in the long term. He found that, all else being equal, downsizing never improved profits or stock market returns.[36]

Financial measures are not relevant to many levels of the organization. Financial reports by their very nature are abstractions. Abstraction in this context is defined as moving to another level leaving certain characteristics out. When we roll up financial statements throughout the organization that is exactly what we are doing—compiling information at a higher and higher level until it is almost unrecognizable and useless in the decision making of most managers and employees. Employees at all levels of the organization need performance data they can act on. This information must be imbued with relevance for their day-to-day activities.

Given the limitations of financial measures, should we even consider saving a space for them in our Balanced Scorecard? With their inherent focus on short-term results, often at the expense of long-term valuecreating activities, are they relevant in today's environment? I believe the answer is yes for a number of reasons. As the name implies, the Balanced Scorecard is just that: balanced. An undue focus on any particular area of measurement often leads to poor overall results. Precedents in the business world support this position. In the 1980s the focus was on productivity improvement, whereas in the 1990s quality became fashionable and seemingly essential to an organization's success. In keeping with the principle of hat gets measured gets done, many businesses saw tremendous improvements in productivity and quality. What they didn't necessarily see was a corresponding improvement in financial results, and in fact some companies with the best quality in their industry failed to remain in business. Financial metrics will remain an important tool for organizations because they ultimately determine whether improvements in customer satisfaction, quality, innovation, and employee training are leading to improved financial performance, whether that is judged by cost containment (often used by support functions such as IT), revenue growth, or ultimately, shareholder value.

What a difference fifty years can make. Writing in the Harvard Business Review back in 1957, Harvard professor Malcolm P. McNair had this to say about organizations paying excess attention to their people: "Too much emphasis on human relations encourages people to feel sorry for themselves, makes it easier for them to slough off responsibility, to find excuses for failure, to act like children."[37] Can you imagine the reaction business leaders would have to this quote if it were uttered today? What was your reaction? If you are like most you would probably completely disagree with McNair's pessimistic view and instead assert the now prevailing notion that an organization's people or its "human capital" represent the critical enabler in the new economy. Harvard Business Review editor Thomas Stewart captures the essence of this notion succinctly and powerfully when he says, "The most important of all are "soft" assets such as skills, capabilities, expertise, cultures, loyalties, and so on. These are the knowledge assets—intellectual capital—and they determine success or failure."[38]

Consulting organizations offer a compelling example of creating value from intangible rather than physical assets. Consultants don't rely heavily on tangible assets, instead they provide value for clients by drawing on relationships with subject matter experts throughout the firm and knowledge from past client experiences to provide innovative solutions. A client engagement I was involved with provides an example: the client encountered a problem loading data for their new performance measurement software. Automatic data interfaces for the software (pulling data directly from source systems throughout their locations) would have required significant human and financial resources to build, and this was not considered a viable option. The alternative of manual data entry was also deemed unacceptable because it would prove a time-consuming and non-value-added activity for system administrators. Our team was tasked with finding an innovative and cost-effective solution.

We convened a team of experts on various subjects: the scorecard software program, the Balanced Scorecard methodology, desktop applications such as MS Access and MS Excel, and client data sources. The newly formed team brainstormed various approaches that would satisfy the criteria of cost efficiency and very limited manual data entry efforts. In the end we determined our best approach was to build a new data entry tool in Excel. Data owners would enter their individual data in the spreadsheet, and e-mail it to the system administrator who would then automatically upload the information into the software. The spreadsheets were custom designed to contain only those measures for which each owner was accountable. This solution ensured that both the innovative and costeffective criteria were satisfied. The new system cost very little to develop and implement and eliminated manual data entry for system administrators. It wasn't the physical assets that led to this innovative solution to a client's needs, but instead the skillful combination of an array of knowledge held by the individual team members.

This kind of situation is happening in organizations around the globe in the transition from an economy based on physical assets to one almost fully dependent on intellectual assets. While this switch is evident to anyone working in today's business world, it is also borne out by research findings of the Brookings Institute. Take a look at Exhibit 5.1, which illustrates the transition in value from tangible to intangible assets. Speaking on National Public Radio's Morning Edition, Ms. Margaret Blair of the Brookings Institute suggests that tangible assets have continued to tumble in value:

If you just look at the physical assets of the companies, the things that you can measure with ordinary accounting techniques, these things now account for less than one-fourth of the value of the corporate sector. Another way of putting this is that something like 75% of the sources of value inside corporations is not being measured or reported on their books.[39]

If you happen to be employed in the public sector you may have noticed Ms. Blair uses the term "corporations". Believe me, your organizations are being affected every bit as much as your corporate counterparts. The challenges represented by this switch are not going unnoticed in Washington. David M. Walker, Comptroller General of the United States said in a February, 2001 testimony to the U.S. Senate that "human capital management is a pervasive challenge in the federal government. At many agencies human capital shortfalls have contributed to serious problems and risks."[40]

In his President's Management Agenda, U.S. President George W. Bush echoes Walker's comments and adds that "We must have a government that thinks differently, so we need to recruit talented and imaginative people to public service."[41] In yet another demonstration of the importance of intangible assets, companies are opening the purse strings for intellectual investments. On second thought, opening the purse strings is a bit like saying World War II was a little skirmish, considering the fact that American companies spend a staggering 36 percent of their revenue each year on human capital related investments.[42]

This transition in value creation from physical to intangible assets has major implications for measurement systems. The financial measurements that characterize existing methods of tabulation were perfectly appropriate for a world dominated by physical assets. Transactions affecting property, plant, and equipment could be recorded and reflected in an organization's General Ledger. However, the new economy with its premium on intangible value-creating mechanisms demands more from our performance measurement systems. Today's system must have the capabilities to identify, describe, monitor, and fully harness the intangible assets driving organizational success. The Balanced Scorecard provides a voice of strength and clarity to intangible assets, allowing organizations to benefit fully from their astronomical potential.

Could there possibly exist a more passionately discussed and debated subject on the business landscape than strategy? While military strategy has been with us for millennia and continues to influence our thinking—witness the ever-popular Art of War by Sun Tzu—business strategy is a relatively new phenomenon with its greatest contributions arriving in the twentieth century. Despite its brief tenure the topic has spawned hundreds of books, thousands of scholarly articles, and countless gurus each espousing their version of the Holy Grail of strategy.

Strategy is not a subject that can be unraveled by its academic and practical threads to reveal the one right method or version of the truth. Every reader of this book, if appropriately prodded, could undoubtedly produce a coherent and cogent definition of strategy. Ultimately we all cherish that spirit of discovery and rightly applaud our diversity of ideas, but practically speaking, it makes the study of strategy a frustrating one. Fortunately for all of us the one thing that pundits from every strategy corner do agree on is the fact that strategy execution or implementation is far more important than strategy formation.

I have had the opportunity to sit in on a number of strategy setting workshops and have always relished the spirited debates, the "aha" moments of breathtaking clarity. The freshly minted strategy emerging from these often grueling sessions is a justifiably pride-invoking achievement; however, it is a far cry from producing the strategic document to actually living and breathing it day in and day out. To succeed in any business today that is precisely what we must do—bring the strategy to life with the unmistakable clarity necessary for everyone in the organization to act on it each and every day. Eighty-four percent of respondents in one recent poll said that competition in their industry had significantly increased in the last five years.[43] Let's face it—we have to execute not only to thrive but to simply stay alive in today's business world.

The good news is that strategy implementation has been proven to boost financial fortunes rather significantly—one study suggested a 35 percent improvement in the quality of strategy implementation for the average firm was associated with a 30 percent improvement in shareholder value.[44] Unfortunately, many organizations fall off the strategy execution track, frequently in dramatic fashion. So why does strategy execution prove so elusive for the typical enterprise? Scorecard architects Robert S. Kaplan and David P. Norton believe the answer lies in the form of four barriers that must be surmounted before strategy can be effectively executed (see Exhibit 5.2).

The Vision Barrier The vast majority of employees do not understand the organization's strategy. This situation sufficed at the turn of the twentieth century when value was derived from the most efficient use of physical assets, and employees were literally cogs in the great industrial wheel. However, in the information or knowledge age in which we currently exist, value is created from the intangible assets—the know-how, relationships, databases of rich information, and cultures existing within the organization. Sadly, the news is no better at the department level. In one recent study 52 percent of IT and business executives said IT's strategic plan is only somewhat understood or not understood at all across the company.[45] Put simply, it is difficult to expect employees, already struggling under the burdens of a Mount Everest-sized pile of priorities, to act in concert with your strategy if they don't understand it.

The People Barrier In its 2005 "Reward Programs and Incentive Compensation Survey", the Society for Human Resource Management found that 69 percent of companies offer some form of incentive compensation to their employees.[46] Like most people, I'm a fan of incentive plans because of the focus and alignment they can drive toward the achievement of a mutually beneficial goal. However, companies take many liberties when constructing these plans, and often the designs leave something to be desired. For example, it is not at all uncommon for incentive plans to link a cash award with the achievement of a short-term financial target such as quarterly earnings. In fact, in our "meet the numbers or else" culture this evil twin of the effective compensation plan springs up frequently in boardrooms across the globe. When the focus is on achieving short-term financial targets, clever employees will do whatever it takes to ensure those results are achieved. This often comes at the expense of creating long-term value for the firm. Do the words Enron or WorldCom ring a bell?

The Resource Barrier Sixty percent of organizations don't link budgets to strategy. This finding really should not come as a surprise to us because most organizations have separate processes for budgeting and strategic planning. There is one group working to forge the strategy leading the firm heroically into the future, while independently another group crafts the operating and capital budgets for the coming year. This finding is particularly relevant to CIOs who must ensure their spending supports the organization's strategy as discussed in the preceding chapter should they hope to demonstrate the alignment desired by all. Unfortunately, a recent survey conducted in part by CIO Insight found that just a tenth of respondents consider IT investment allocation decisions to be "strategic and based on explicitly strategic plans."[47]

The Management Barrier In a sad, yet humorous commentary on modern organizational life a recent poll of U.S. office workers revealed that 41 percent would rather wash their kitchen floors than attend a management meeting at their company.[48] What exactly is being said at these companies? And more importantly, if I offer to host their meetings will they do my laundry at my place? Most of the cleanliness-minded respondents of the survey would, if pressed, probably report that their management meetings are just plain boring, and in many cases that is undoubtedly an accurate assessment. With mind-numbing charts and graphs, sleep-inducing commentaries, and zero conflict, most meetings can rightly be classified as both a waste of time and, unfortunately, a huge lost opportunity.

It certainly doesn't have to be that way. With strategy forming the agenda for a management meeting new life can be pumped into an antiquated institution, instantly changing the dynamic from dull, rote presentations to stimulating debate and discussion on the factors driving the firm forward. How does your executive team spend their time during their monthly or quarterly reviews? If it is like most organizations they probably pend the majority of their time analyzing the financial results and looking for remedies to the "defects" that occur when actual results do not meet budget expectations. A focus on strategy demands that executives spend their time together moving beyond the analysis of defects to a deeper understanding of the underlying value creating or destroying mechanisms in the firm.

As the preceding discussion indicates, organizations face many hurdles in developing performance measurement systems that truly monitor the right things. What is required is a system that balances the historical accuracy of financial numbers with the drivers of future performance, while simultaneously harnessing the power of intangible assets, and of course assisting organizations in implementing their differentiating strategies. The Balanced Scorecard is the tool that answers this complex triad of challenges.

The Balanced Scorecard was developed by Robert Kaplan, an accounting professor at Harvard University, and David Norton, a consultant also from the Boston area. In 1990 Kaplan and Norton led a research study of a dozen companies exploring new methods of performance measurement. The impetus for the study was a growing belief that financial measures of performance were ineffective for the modern business enterprise for the many reasons discussed in the opening pages of this chapter. People in the study companies, along with Kaplan and Norton, were convinced that a reliance on financial measures of performance was affecting their ability to create value. The group discussed a number of possible alternatives but settled on the idea of a scorecard featuring performance measures capturing activities from throughout the organization—customer issues, internal business processes, employee activities, and of course shareholder concerns. Kaplan and Norton labeled the new tool the Balanced Scorecard and later summarized the concept in the first of several Harvard Business Review articles, "The Balanced Scorecard—Measures that Drive Performance."[49]

Over the next four years a number of organizations adopted the Balanced Scorecard and achieved immediate results. Kaplan and Norton discovered these organizations were not only using the scorecard to complement financial measures with the drivers of future performance, but were also communicating their strategies through the measures they elected for their Balanced Scorecard. As the scorecard gained prominence with organizations around the globe as a key tool in the implementation of strategy, Kaplan and Norton summarized the concept and the learning to that point in their 1996 book, The Balanced Scorecard.[50]

Since that time the Balanced Scorecard has been adopted by more than half of all Fortune 1000 organizations, and the momentum continues unabated with companies large, medium, and small taking full advantage of the tool's profound simplicity and unmistakable effectiveness. Once considered the exclusive domain of the for-profit world, the Balanced Scorecard has been translated and effectively implemented in both the nonprofit and public sectors. These organizations have learned that by slightly modifying the scorecard framework they are able to demonstrate to their constituents the value they provide and the steps being taken to fulfill their important missions. So widely accepted and effective has the scorecard been that the Harvard Business Review recently hailed it as one of the 75 most influential ideas of the twentieth century.

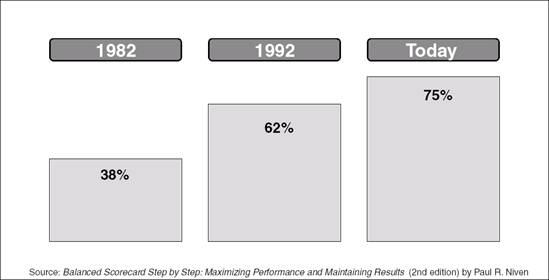

The Balanced Scorecard is a carefully selected set of quantifiable measures derived from an organization's strategy. The measures selected for each organization's scorecard represent a tool for its leaders to use in communicating to employees and external stakeholders the outcomes and performance drivers by which the organization achieves its mission and strategic objectives. Scorecard measures are contained in four distinct, yet related perspectives.

The etymology of the word "perspective" is from the Latin perspectus: "to look through" or "see clearly", which is precisely what companies aim to do with a Balanced Scorecard—examine their strategy and make it clearer through the lens of different viewpoints. To be effective, any strategy must contain descriptions of financial aspirations, markets served, processes to be conquered, and of course the people who steadily and skillfully guide the ship to success. Thus, when measuring progress it makes little sense to ocus on just one aspect of the strategy when in fact as Leonardo da Vinci reminds us "Everything is connected to everything else."[51] An accurate picture of strategy execution must be painted in the full palette of perspectives that comprise it, therefore when developing a Balanced Scorecard companies typically use the following four: Customer, Internal Processes, Employee Learning and Growth, and Financial. Now let's take a brief tour of those four perspectives, examining what the CIO might find at the corporate level of the company as well as what measures IT leaders may use to populate their own scorecard (see Exhibit 5.3).

Customer Perspective When choosing measures for the Customer perspective of the scorecard organizations must answer three critical questions: (1) who are our target customers, (2) what is our value proposition in serving them, and (3) what do our customers expect or demand from us? Sounds simple enough, but each of these questions offers many challenges. Most organizations state that they do in fact have a target customer audience, yet their actions reveal an "all things to all customers" strategy. As strategy guru Michael Porter has taught, this lack of focus prevents an organization from differentiating itself from competitors. Choosing an appropriate value proposition poses no less of a challenge to most firms. Many will choose one of three "disciplines" articulated by Treacy and Wiersema in "The Discipline of Market Leaders":[52]

Operational Excellence. Organizations pursuing an operational excellence discipline focus on low price, convenience, and often "no frills." Wal-Mart provides a great representation of an operationally excellent company.

Product Leadership. Product leaders push the envelope of their firm's products. Constantly innovating, they strive to offer simply the best product in the market. Sony is an example of a product leader in the field of electronics.

Customer Intimacy. Doing whatever it takes to provide solutions for unique customer's needs help define the customer intimate company. They don't look for one-time transactions but instead focus on long-term relationship building through their deep knowledge of customer needs. In the retail industry Nordstrom epitomizes the customer intimate organization.

Regardless of the value discipline chosen, at the corporate level the Customer perspective normally includes measures widely used today: customer satisfaction, customer loyalty, market share, and customer acquisition, for example. Equally as important, the organization must develop the performance drivers that lead to improvement in these "lagging" indicators of customer success. Doing so greatly enhances the chances of answering the third question for this perspective: what do our customers expect or demand from us?

IT organizations must follow a similar path when developing their Customer perspective, beginning with a discussion of "Who is the Customer?" Most frequently the answer is business units and other departments utilizing IT's many and varied offerings. While customers vary in their expectations and demands, many require the IT function to provide high-quality, reliable services at a reasonable cost. In other words, they expect all applications supported by IT to be "always on" just as Chapter 1 describes: "The thankless task is to make sure the systems infrastructure needed by an organization is operating correctly and efficiently 24 hours a day, seven days a week." Quality and reliability, therefore, are popular measures on many IT Scorecard Customer perspectives.

In addition to supplying reliable service, customers increasingly expect IT to make significant contributions to business unit success through the provision of analytics and innovative technology solutions necessary to tackle complex marketplace challenges.[53] Measuring these contributions are very likely to highlight the important role IT plays in overall corporate strategy execution.

Internal Process Perspective The Internal Process perspective of the scorecard identifies the key processes the firm must excel at in order to continue adding value for customers, and ultimately shareholders. Each of the customer disciplines outlined in the Customer perspective description entails the efficient operation of specific internal processes in order to serve customers and fulfill value propositions. The task in this perspective is to identify those processes and develop the best possible objectives and measures with which to track progress. To satisfy customer and shareholder expectations executives often have to identify entirely new internal processes rather than focusing efforts on the incremental improvement of existing activities. Product development, production, manufacturing, delivery, and post-sale service may be represented in this perspective.

Once again, IT organizations follow a similar route in developing measures for their own scorecard. The challenge lies in determining which internal processes the organization must excel at in order to meet the outcomes described in the Customer perspective. For example, if you include a measure of reliability in the Customer perspective, you must then ask, "What drives reliability from a process standpoint?" Regular maintenance of all systems may be considered an essential process for any IT organization and one that contributes significantly to its ability to supply reliable service for end users. Therefore, you may choose to measure maintenance in your Internal Process perspective.

When developing measures for this perspective it is also important to look beyond the day-to-day challenges that keep the IT organization hopping from 9 to 5, or 8 to 6, or even 7 to 7, and consider the differentiating processes that elevate its status as a strategic player in the company and ultimately highlight the critical part the IT organization plays in overall company success. This may be facilitated, for example, by reaching out to business unit leaders, forging partnerships, embedding IT personnel in different units to learn the challenges on the ground, and using the information and knowledge gleaned to produce innovative solutions well beyond the current scope of operations. This new "imperative" to work with other parts of the organization has been stated mildly, especially when compared with the words of Gartner Inc. Vice President Bill Kirwin who warns, "Any CIO who isn't mingling with the business units to learn how IT can support various initiatives is going to be toast."[54]

Employee Learning and Growth Perspective If a CIO wants to achieve ambitious results for internal processes, customers, and ultimately shareholders where are these gains found? The objectives and measures in the Employee Learning and Growth perspective are really the enablers of the other three perspectives. In essence they are the foundation upon which this entire house of a Balanced Scorecard is built. The CIO who identifies objectives, measures, and related initiatives in the Customer and Internal Process perspective can be certain of discovering some gaps between IT's desired direction and current organizational infrastructure of employee skills (human capital), information systems (informational capital), and the environment required to maintain success (organizational capital). The objectives and measures the CIO designs in this perspective help close that gap and ensure sustainable performance for the future.

Employee skills, employee satisfaction, availability of information, and alignment could all have a place in this perspective. Many organizations I've worked with struggle in the development of Learning and Growth measures. It is normally the last perspective to be developed, and perhaps the teams are intellectually drained from their earlier efforts of developing new strategic measures, or they simply consider this perspective "soft stuff" best left to the Human Resources group. No matter how valid the rationale seems, this perspective cannot be overlooked in the development process. As mentioned earlier, the measures developed in the Learning and Growth perspective are really the enablers of all other measures on the IT scorecard. Think of them as the roots of a tree that ultimately run through the trunk of internal processes to the branches of customer results, and finally to the leaves of financial returns.

When creating this perspective, IT organizations should utilize the three areas of capital discussed previously: human, information, and organizational. Human capital relates to the mix of skills and talents required by IT personnel in meeting the strategic requirements of the organization's users. Does your team have the skills and talents required to make the strategic contribution expected of you? Of course, IT has its own information requirements, and they should be measured and monitored under the heading of information capital. Finally, and perhaps most importantly, the IT organization must ensure that its culture is in alignment with the needs of its user community. An insular, silo-based culture will not be effective, or tolerated, in organizations that thrive on information sharing and a customer service ethic.

Financial Perspective Financial measures are a critical component of the Balanced Scorecard, especially in the for-profit world. The objectives and measures in this perspective tell whether strategy execution—which is detailed through objectives and measures chosen in the other perspectives— are leading to improved bottom-line results. The IT organization ould focus all its energy and capabilities on improving customer satisfaction, quality, on-time delivery, or any number of things, but they are of limited value without an indication of their effect on the company's financial returns. Typical examples of financial indicators include profitability, revenue growth, and asset utilization.

Most IT organizations use the Financial perspective to shine a penetrating light on their budgets, ensuring they balance effectiveness with efficiency. This perspective is particularly relevant in an era when some Fortune 100 company IT budgets rival the gross domestic product of small nations! Of course I'm being facetious, but the underlying message remains resonant—IT must avoid the perception of chasing every new technology and instead focus on assisting their customers reach their business goals while doing so with an unrelenting focus on best overall cost. Exhibit 5.3 outlines the typical structure of the Balanced Scorecard as it was originally conceived with profit-seeking enterprises in mind.

From time to time my phone rings with a request to help "turnaround" a troubled Balanced Scorecard implementation, and recently I received just such a call. Challenges in executing the Balanced Scorecard can stem from any number of sources, but in this large nonprofit the culprit was a distinct lack of planning. The agency was as unprepared from a planning standpoint as it was enthusiastic about the scorecard. Unfortunately the interest and exuberance they felt for the tool failed to compensate for their lack of organization. Virtually every meeting was slowed to a merciless crawl with discussions of process questions. Team members and other stakeholders were naturally curious about the next steps in the process, but the leaders of the scorecard implementation had barely thought through the current meeting let alone the entire implementation journey.[55] This lack of planning significantly slowed what could otherwise have been a very swift and successful implementation.

As with any major initiative, the CIO needs a carefully crafted development plan to produce an effective Balanced Scorecard. Every organization is different when it comes to planning and executing significant change efforts. Some feel a highly detailed plan that encompasses thousands of lines in Microsoft Project is the only way to capture all the necessary elements of the work. I recall arriving at the offices of one new client, barely completing introductions to the scorecard team, and having a phonebook-sized plan thrust upon my lap. Others use less formal means, outlining only the most critical tasks and tracking them on MS Excel or Word documents.

This section outlines the key steps in developing a Balanced Scorecard for the IT organization based on experience and research. Keep in mind that this presentation appears in summary form; I've written three books to capture the entire process. Therefore, please use this as an initial guide to help stimulate your Balanced Scorecard thinking.

Before beginning the work of building a Balanced Scorecard, the CIO must lay the groundwork for the implementation ahead. The planning phase includes the following steps.

Step 1—Develop a Guiding Rationale for the IT Balanced Scorecard Creating a Balanced Scorecard because it "seems right" or "a colleague had good luck with it" almost always leads to an ineffective implementation. As with any other initiative, invest time, energy, and resources into adopting a Balanced Scorecard according to a guiding rationale and a legitimate business reason. Launching a new program that requires significant employee support for success without a compelling business reason is sure to invite disaster if your employees are already busy contending with the attendant IT firefighting and stress-inducing challenges that arise in their day-to-day work. "The voice created by the failure to communicate is soon filled with poison, drivel, and misrepresentation."[56] Establish a valid reason for embarking on this trail, and communicate that rallying cry relentlessly to win the support of an often change-fatigued employee base.

Step 2—Secure Executive Sponsorship In his book Jack, Straight from the Gut, former General Electric CEO Jack Welch points to an undeniable truth of organizational life. "To make initiatives work it took passionate, all-consuming commitment from the top . . . Every leadership action must demonstrate total commitment to the initiative."[57] To break through the attention and commitment barriers that weary IT organization employees experience in the blizzard of change blowing relentlessly around them, the project must, repeat must, have an executive sponsor who believes in the value of the Balanced Scorecard who is willing to ceaselessly champion the cause both up and down the chain of command.

Step 3—Form and Train Your Balanced Scorecard Team A robust Balanced Scorecard is best created by the hearts and minds of a small group of people committed to a common purpose. Forget the Lone Ranger, the CIO needs a group of bright people willing to engage in the spirited debate necessary to create a scorecard that truly shines a light on IT's strategic contribution as exemplified by the leadership principles listed in Chapters 1 or 3. With the team formed, don't neglect to invest in some upfront training on this concept, which admittedly appears simple at first glance, but is replete with nuances and subtleties, the attention to which often separates the winners in this game from the losers.

Step 4—Formulate Your Implementation Plan As information technology experts, CIOs are very familiar with the importance of planning. Create an implementation plan for the IT organization's Balanced Scorecard initiative and monitor major milestones to ensure it remains on track. When it comes to timing for a Balanced Scorecard implementation, every organization will be somewhat different depending upon urgency, availability of resources, and overcoming the inevitable logistical challenges; however, the CIO can expect to have a draft Balanced Scorecard constructed within four weeks.

Step 5—Develop a Communication Strategy and Plan for Your Balanced Scorecard Implementation Professor and author John Kotter has said, "Without credible communication, and a lot of it, employees' hearts and minds are never captured."[58] To their detriment, most organizations fail to heed this valuable advice and their change efforts are the worse for it. These challenges must be met head-on during the implementation efforts if the CIO expects the IT organization employees to begin using this tool to make real business decisions. A carefully constructed communication strategy and plan proves to be a great ally in the struggle to enlighten all employees and win support throughout the Balanced Scorecard development process. A document the size of a Manhattan phone book isn't necessary here, simply focus on the basics: What are our communication objectives (key messages), who are our target audiences, what are their requirements, and how will we communicate (mechanisms, timing, and so on)?

Consider the steps presented in this section as a framework for development of a Balanced Scorecard for the IT organization. One of the many benefits of the scorecard, one that has greatly contributed to its longevity and unabated growth, is its flexibility in adapting to the constraints of every organization. Take advantage of that flexibility when constructing your plan.

Step One: Gather and Distribute Background Material The Balanced Scorecard is a tool that describes strategy. In order to fulfill this promise your team must have ample access to background material on the IT organization's mission, vision, values, strategy, and employee core competencies. Of course, because IT focuses on supplying services to other departments within the company it is important to gather information regarding user needs and business plans.

Step Two: Provide Balanced Scorecard Education At this point in the process the development team has been steeped in the fundamentals of the Balanced Scorecard, but the tool still represents a great black hole to much of the IT organization. Plug this gap early and effectively with a comprehensive scorecard training session designed to outline the challenges that led to the selection of the scorecard, fundamental principles of the model, success stories, and how you plan to guide the implementation. Invite as many people as can comfortably fit into a venue for this first training session; this is no time to practice "education snobbery". Winning the commitment of every employee, thus informing them of what this tool is all about, represents a vital early step on this journey.

Step Three: Develop or Confirm Mission, Values, Vision, and Strategy Based on the information gathered in Step One, generate a consensus of where the IT organization rests in terms of these critical items. If missing one or all of these scorecard "raw materials", go back, work with the leadership team, and develop them.

Step Four: Develop Your Strategy Map A well-grounded executive understanding of strategy mapping is critical to Balanced Scorecard success. The Harvard Business Review has cited the Balanced Scorecard as one of the 75 most influential business ideas of the twentieth century. So how does a management tool ascend to such a lofty position when literally hundreds of others are relegated to has-been and flavor of the month status? First and foremost, the Balanced Scorecard has been proven to generate results for thousands of organizations in private, public, and nonprofit fields of endeavor, and this efficacy would seem a prerequisite of any tool destined to reach the pantheon of business systems.

Dig a little deeper, however, to find another equally compelling rationale for the Balanced Scorecard's continued growth—its adaptability. Perhaps evolution is a more suitable description. Brought into the world by Kaplan and Norton as a methodology to tame the power of financial metrics run amok, the Balanced Scorecard soon evolved into a system capable of bridging short-term leadership action with long-term strategy through links to such processes and budgeting and compensation. This discovery heralded a new chapter in its life and beckoned thousands of additional organizations to heed the call. But quite possibly the most powerful evolutionary leap in the Balanced Scorecard's life has been from measurement system to strategy communication device through the advent of the strategy map.

The subtitle of Kaplan and Norton's first Balanced Scorecard book is "Translating Strategy Into Action," which is exactly what is accomplished by creating performance measures to track the execution of a game plan for success. But creating effective performance measures that serve as true barometers of strategy and performance is tough sledding. Just imagine opening the three-ring binder housing most companies' 50-page business strategy with the task of translating the contents into a coherent set of measures that indicate whether or not they've actually taken the proverbial hill. Even if it's a two-page strategy pamphlet the chore is an onerous one because even the most well-conceived and carefully crafted strategies are bound to contain at least a portion of ambiguous terms like "customer service" or "product development." Early Balanced Scorecard adopters faced this challenge and found themselves instinctively spanning the strategy/measures chasm with a discussion of objectives, or what needed to be done well in order to implement the essence of the strategy. So instead of beginning with "How do we measure this strategy?" they uncorked the process by asking themselves "What do we need to do well in order to execute?"

Parsing the task in this way allows users to add a necessary layer of granularity to the strategy, ultimately rendering the job of measures creation significantly simpler. For example, if the strategy devoted a section to new product development, stressing the need to bring new products to market at a faster rate than competitors, this narrative was translated into the simple objective of "Accelerate new product development," which may be accurately measured by the new product development life cycle.

As with any groundbreaking business tool the Balanced Scorecard has a lexicon all its own, and this discussion distinguishes the meaning of two key terms: objective and measure. This is a critical distinction and one the CIO must master to create a scorecard that both accurately describes the IT organization's game plan and brings it to life for those charged with the responsibility of executing it on a day-to-day basis—your employees.

An objective is a succinct statement, normally beginning with a verb, describing what the IT organization must do well in each of the four perspectives in order to implement its plan. Examples vary widely but could include "Reduce costs", "Improve service delivery time", "Enhance reliability", and "Close our skills gap". Strategy maps are comprised entirely of objectives. Tracking success in achieving the objective is the domain of the measure, a (typically) quantitative device used to monitor progress.

For those who grapple with an issue best by first defining it, try this for a strategy map: a one-page graphical representation of what the IT organization must do well in each of the four perspectives to successfully execute its game plan. Strategy maps do not take any measurements, no tallying of results here, instead the IT organization is communicating to all its audiences, internal and external, what it must do well to achieve its ultimate goals. This fulfills the description of the strategy map as a powerful communication tool, signaling to everyone within the enterprise what must occur to beat the almost overwhelming odds of strategy execution.

So why use the term "map"? Why not a more mundane term such as "strategy sheet" or "must do" list? A map guides us on our journey, detailing the pathways to get us from point A to point B, ultimately leading us to our chosen destination. So it is with a strategy map—defining causal pathways that weave through the four perspectives, which lead to the implementation of the IT organization's strategy. An example strategy map of a fictitious company is displayed in Exhibit 5.4.

Using the raw materials previously captured—mission, vision, strategy, user expectations—the IT organization's scorecard development team starts to build a strategy map for the entire IT organization that describes what it must do well in each of the four perspectives in order to succeed.

Step Four (a): Gather Employee Feedback Ultimately, the CIO expects the IT organization's Balanced Scorecard to provide information that allows all IT employees to understand how their day-to-day actions link to the organization's strategic plan. Therefore, the CIO polls IT employees to ensure they feel the strategy map has captured the critical elements of value to the whole IT organization.

Step Five: Develop Performance Measures Returning to the ancestral homeland of the Balanced Scorecard, which was created many years ago as a measurement system, the IT organization's scorecard development team translates each of the objectives on the strategy map into metrics that can be tracked to provide insight into the execution of IT strategy and establish accountability throughout the organization.

Step Five (a): Gather Employee Feedback This represents an optional step. While the CIO desires employee feedback at every turn of the scorecard wheel, the appropriate managers must eventually own the highestlevel performance measures, and one would expect their "stickiness factor" to be off the charts if they have not had the chance to participate. Consider using this opportunity to explain to IT staff members precisely why the particular measures were chosen.

Step Six: Establish Targets and Prioritize Initiatives Without a target for each measure, the CIO and measurement managers have no way of knowing whether improvement efforts are yielding acceptable results. The data from the IT scorecard metrics provides the IT organization with only half the picture. A target gives meaning to measure results by affording a point of comparison. Additionally, all measures should be accompanied by initiatives designed to bring the targets to fruition. An initiative may be a specific action, project, or plan that supports the achievement of the target.

Step Seven: Gather Data for Your First Balanced Scorecard Report Dare to be bold and proclaim that within 60 days of developing your performance measures the IT organization will conduct its first meeting with its scorecard at the helm. This requires gathering the data necessary to supply that initial report. You may be thinking, "We'll never have all the data!" And you are probably correct, because most new scorecard adopters are missing at least a portion of the data for performance metrics as they ramp up their reporting efforts. However, don't let that stop you from the many significant benefits that can accrue from discussing the measures you do have: focus, alignment, and improved resource allocation decisions to name but a few. Please refer to the discussion in Chapters 1 and 3, about team building, and Chapter 8, for the return on such an investment.

Step Eight: Hold Your First Balanced Scorecard Meeting Those rockin' Granddads and elder statesmen of music royalty, the Rolling Stones, recently made a stop on their world tour here in San Diego, and I would love to have seen them in action. But as the concert date loomed ever closer did I take any action? No, I just kept saying to myself, "I'd love to see them." Earth to Paul: buy a ticket! There was absolutely nothing in the way of me wailing my heart out to "Satisfaction" with the exception of that tiniest of details—that for some reason I let the opportunity slip away. Some scorecard implementing organizations make the same mistake by talking a great game about the alignment and focus they are going to derive from the tool, but they fail to achieve it because they simply refuse to place the scorecard at the center of their management meeting and reporting agenda. Repeat after me: "To execute strategy, we must discuss strategy." Getting to the first Balanced Scorecard report should be the CIO's number one priority in the initial stages of the IT organization's scorecard implementation. Unlike me with the Stones (knowing them, they will probably be touring for another 20 years), CIOs don't have the luxury of time, so make reporting a high priority on your list.

Step Nine: Develop the Ongoing Balanced Scorecard Implementation Plan The preceding steps will get the CIO and the IT organization from point zero to the development of a Balanced Scorecard measurement tool. The word measurement is stressed here because you can do so much more with your scorecard—install the system as the cornerstone of the IT organization's management processes such as budgeting, compensation, and professional development.

Under the leadership of CIO Bill Mao, the information services (IS) department's team of 35 employees and 10 contractors provides the Orange County (California) Transportation Agency (OTCA) with a broad portfolio of services including data management, business support, security, and technical services. That list of offerings probably sounds familiar, but as many CIOs know, prioritizing staff workloads and determining IS success while attempting to remain in alignment with overall organizational strategy is a tremendous challenge. To help overcome those potential barriers OCTA IS introduced the Balanced Scorecard in 2003, with the following objectives for the implementation:

Align stakeholders, sponsors, leaders, and employees to do the right things for the organization.

Make strategy the job of all IS employees through a personal contribution to strategic implementation.

Translate the IS strategy to operational terms so that everyone understands it and demonstrates how they contribute.

Provide reliable data for business cases to negotiate budgets (up or down), prioritize work, and allocate resources.

Ensure rewards and positive reinforcement continually occur.

Tie employee compensation to performance as defined and measured within the IS BSC.

Provide IS management and staff a common context in which to make daily decisions, both individually and as a group, with a similar pace and congruent results in mind.

Help all employees focus on the future and not dwell on the past.

Achieving such ambitious objectives would require a dedicated executive sponsor willing to freely share one's time, expertise, and guidance. CIO Bill Mao immediately assumed the role and developed strong relationships with other OCTA stakeholders including the Director of Finance and Administration, the Director of Operations, and the Assistant Chief Executive Officer. Forging close bonds with these stakeholders proved to be a critical advantage for the initiative because two of the three had personal experience with the Balanced Scorecard and demonstrated advocacy for the implementation from the earliest stages.

In keeping with the discussion of scorecard "raw materials" earlier in the chapter, the IS group began their efforts by developing a mission, vision, and strategic themes for the department, each of which would serve as pillars for the scorecard work to follow. The mission statement reads:

Through teamwork, provide leadership, guidance, and support for information and communication technologies within the Authority. Our goal is to add value and provide business solutions that satisfy our customers.

The IS vision builds on the mission and focuses on what is necessary for IS to ensure success in the challenging environment they face:

Success: driven by customers, fueled by innovation, achieved through partnerships.

It would certainly be difficult to argue with the choices inherent in the vision statement, as success truly is driven by customers; understanding their needs and providing them with the tools they require to drive the organization's strategy. Similarly, innovative new technologies and solutions are more necessary than ever. And finally, it is only through building bridges with users by forming partnerships and alliances that establish true alignment in this or any organization. With the mission and vision statements in place the group turned their attention to the development of "strategic themes", which they defined as broad directional priorities used to steer the overall IS ship. Four such themes were created:

Have a Business/Customer focus

Keep pace with technology

Work smarter

Always "on"

With the necessary scorecard building blocks in place, two teams were created for the work to follow: a leadership team comprised of IS managers would provide overall guidance and approve all scorecard materials, and a core team consisting of six representatives from the various IS disciplines was responsible for creating the department's strategy map and Balanced Scorecard of measures. Job number one was Balanced Scorecard training for both newly minted teams, and with the assistance of outside consultants the groups were provided with a curriculum of strategy and scorecardrelated concepts including BSC background and fundamentals, developing strategy maps and measures, and managing with the BSC system.

The Balanced Scorecard is primarily an agent of change within an organization; a change in the way it measures, in the way it manages, and if utilized effectively, a change in results. As we all know, change can prove to be painfully difficult, so it should come as no surprise that despite the careful foundation poured for the BSC by IS leadership, both core team members and employees were initially hesitant to jump on board. As Scorecard Coordinator Annette Hess explains,

Employees were very resistant and reluctant. The BSC was initially perceived as just another flavor of the month that would disappear off the radar in due time. When people realized it was not going away any time soon they began to resist it. Reactions were mixed but mostly staff felt they did not have time for it, they were too busy as it was and this was just another chore piled on top.[59]

For some, only proof in the form of results would help sway their sentiments. But for many, simply learning more about the scorecard itself and why IS was launching the initiative proved to be an effective antidote to reluctance and resistance. The IS team communicated to staff in a number of ways: updates and discussions occurred in general department meetings, PowerPoint presentations were delivered, and posters were placed throughout the department highlighting specific aspects of the IS Balanced Scorecard.

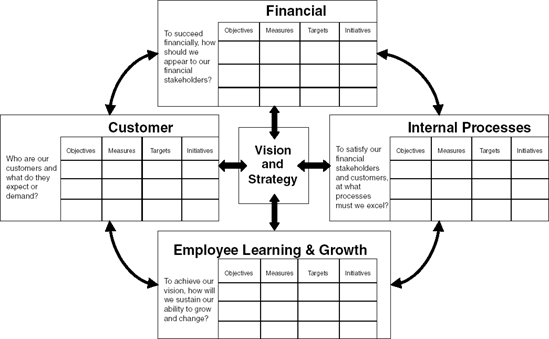

Exhibit 5.5 shows the IS department's strategy map of key objectives. The first thing that stands out about their map is that they don't use the four standard Balanced Scorecard perspectives previously discussed. In place of a Financial perspective they've chosen to use the label "Mission" and include within it their overall objectives of increasing OCTA value, increasing customer satisfaction, and getting more bang for their buck. Although the standard scorecard monikers have proven effective for many organizations around the globe, they may not match the language many organizations use on a day-to-day basis. To enhance understanding and acceptance of the scorecard, be sure and use perspective titles that fit your IT organization's culture and represent the language spoken by your teams.

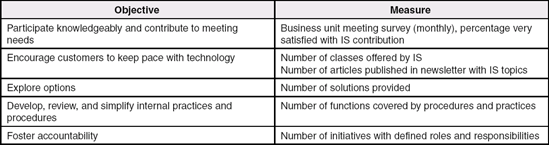

The IS department also decided to use their four strategic themes as headings with objectives appearing in each of the perspectives telling a strategic story related to the particular themes. For example, under the theme of "Business/Customer focus" in the Internal Process perspective they place the objective "Understand customers' business needs." The team feels that if they are able to do this it will positively influence the objective of "Participate knowledgeably and contribute to meeting needs" as shown in the Customer perspective. Participating knowledgeably in turn drives customer satisfaction in the Mission perspective, which in turn increases OCTA's value, their overarching objective.

These "theme stories" as they came to be known throughout the IS department turned out to be a critical enabler of the scorecard's success. Managers have noted the value of the stories in explaining the organization's strategic direction with their employees, making the linkages among objectives plain for all to see, understand, and most important, act upon.

Using this system of cause and effect among the objectives allows the leadership team to critically examine results in light of the hypotheses represented within the map. "But," you say, "Why are there no one-to-one direct upward arrows extending from the Employee Learning and Growth perspective?" As discussed earlier, objectives in this perspective are typically seen as enablers, and each could potentially impact every objective in all remaining perspectives. For example, "Communicate and collaborate" is critical to the success of any organization, OCTA IS included, and impacts the success of every objective comprising the map. Drawing arrows from Communicate and collaborate to all objectives above would simply confuse readers and dramatically diminish the strategy map's power as a communication tool.

An important lesson to draw from the OCTA IS strategy map is the simple language employed throughout the document. As all CIOs know, working in technology provides nearly limitless opportunities to pepper one's speech and written communication with acronyms and phrases that can leave the rest of us technology neophytes scratching our heads in utter confusion. This team recognized the importance of communicating effectively to all stakeholders: managers, employees, senior leaders outside of IS, and outside vendors. Consequently, IS worked diligently to create a map that is at once readable and powerful in its elegant simplicity.

Perhaps my favorite objective, a wonderful exemplar of this simplicity principle, is "Get off the 3rd floor." Assuming you don't work for this organization, what do you think that means? I'm sure many of you are thinking to yourself, "It means get out and speak with our customers, build relationships, and learn more about their needs." Exactly! This is the kind of language you should be using in such a document, which is at its core a communication vehicle, signaling to all stakeholders the critical objectives of the IT organization's success. OCTA's Scorecard Coordinator Annette Hess suggests that keeping the map easy to understand and resonant with the department's culture is a key to success in this process: "You should keep the map current and simple; make it yours. Don't try to mimic other companies just to say you have one."[60]

Each objective on the strategy map is translated into one or more performance measures demonstrating how the organization will gauge its success on that particular item. Although I can't share all of the IS team's measures in this chapter, a sample has been provided in Exhibit 5.6.

With a strategy map and measures in place the IS leadership team continued their scorecard education efforts by introducing all employees to these new tools for executing strategy. In group sessions, facilitators walked participants through the map and measures explaining why IS was focusing on the themes appearing on the map and how the objectives and measures related to the ultimate fulfillment of the promise inherent in each. The sessions also served to steep employees in the new language and terminology of the Balanced Scorecard system.

According to IS leadership, the greatest benefit from implementing the Balanced Scorecard has been increased employee knowledge of how they are able to personally contribute to the department's strategy. Through discussions of scorecard results and the ongoing communication campaign launched by the leadership team, employees not only recognize their vital link in the chain of events leading to improved customer satisfaction but are offering ideas and suggestions as to specific actions everyone can take to increase OCTA's value—their overarching mission objective. Stakeholders outside of IS have also taken notice of the changes and the department is viewed as providing value-added service to the entire organization.

Though the IS Balanced Scorecard can be deemed a success it has not been without challenges, the type which plague many such change-oriented initiatives. A barrier erected at the outset of the implementation was the fact that the BSC was not being developed at higher levels of the OCTA organization, thus employees were concerned they were "going it alone" without the necessary support of senior executives throughout the organization. The ceaseless efforts of the executive sponsor, CIO Bill Mao, and the support of other directors within OCTA were, and will continue to be, necessary to reassure employees this is not a flavor of the month offering but instead represents a fundamental shift in the way the department does business.

In hindsight the leadership team believes it would have proven beneficial to dedicate more time and resources to the initiative at the outset, getting the program up, running, and self-sustaining in a shorter period of time. In the early days of the initiative much of the work fell upon the shoulders of the Balanced Scorecard Coordinator, which not only significantly increased her already considerable workload but did little to generate buy-in and support for the tool from the wider employee base. Establishing theme and objective owners has improved the scorecard's prospects significantly by spreading the work across a number of individuals and in the process enhancing knowledge of, and commitment to, the process itself.

As with any major change, initiative challenges remain as the IS department continues its journey with the Balanced Scorecard system, but the indicators thus far are very positive: enhanced knowledge of strategy, increased alignment with overall OCTA goals, and an unrelenting focus on key performance measures all combining to make the IS team a key contributor to OCTA's ongoing success.

[Note to readers. Much of this chapter is drawn directly from Mr. Niven's book: Balanced Scorecard Step by Step: Maximizing Performance and Maintaining Results (2nd Edition), Wiley 2006. He has updated the work with an emphasis on the role of the BSC for the IT organization.]

[30] Accessed at http://www.computerworld.com/managmenttopics/management/story/0, 10801, 109087, 00.html. March 6, 2006.

[31] See, David P. Norton, "Creating Strategic Alignment and Readiness for IT," Balanced Scorecard Report, September-October 2002: 1-5.

[32] From the presentation delivered by Robert S. Kaplan, "Creating Strategy-Focused Public Sector Organizations," September, 2004.

[33] David P. Norton and Randall H. Russell, "Translate the Strategy Into Operational Terms," Balanced Scorecard Report, May-June 2005: 1-5.

[34] Thomas A. Stewart, "Intellectual Capital, (New York, NY, Currency, 1999) xxi.

[35] Scott Thurm, "Teamwork Raises Everyone's Game," The Wall Street Journal, November 7, 2005: B8.

[36] Lauri Bassi and Daniel McMurrer, "Are Employee Skills a Cost or an Asset," Business Ethics, Fall 2004.

[37] Malcolm P. McNair, "What Price Human Relations?" Harvard Business Review (1957).

[38] Quoted in 11th Annual Worldwide Luminary Series: Leading to Greatness" participant workbook, November 2, 2005.

[39] Interview on National Public Radio's Morning Edition October 27, 2000.

[40] Testimony by David M. Walker, Comptroller General of the United States, before the Subcommittee on Oversight of Government, Management, Restructuring, and the District of Columbia Committee on Governmental Affairs, U.S. Senate.

[41] Found at: www.whitehouse.gov/omb/budget/fy2002/mgmt.pdf.

[42] Haig R. Nalbantian, Richard A. Guzzo, Dave Kieffer, and Jay Doherty, Play To Your Strengths (New York: McGraw-Hill, 2004).

[43] McKinsey Quarterly Global Survey of Business Executives, November 2004.

[44] Brian E. Becker, Mark A. Huselid, and Dave Ulrich, The HR Scorecard, (Boston: Harvard Business School Press, 2001).

[45] From the Strategic Alignment Research Study, "Communication Gap," 2002. Study Sponsored by CIO Insight Magazine and the Balanced Scorecard Collaborative.

[46] Reported in: Synygy Magazine, Fall 2005.

[47] From the Strategic Alignment Research Study, "Communication Gap," 2002. Study Sponsored by CIO Insight Magazine and the Balanced Scorecard Collaborative.

[48] Julia Neyman and Julie Snider, "USA Today Snapshots," USA Today, November 15, 2004.

[49] Robert S. Kaplan and David P. Norton, "The Balanced Scorecard—Measures that Drive Performance," Harvard Business Review, January-February 1992: 71-79.

[50] Robert S. Kaplan and David P. Norton, The Balanced Scorecard (Boston: Harvard Business School Press, 1996).

[51] Michael J. Gelb, How to Think Like Leonardo da Vinci (New York: Random House, 2004).

[52] Michael Treacy and Fred Wiersema, The Discipline of Market Leaders (Reading, MA, Perseus Books, 1995).

[53] Robert S. Kaplan and David P. Norton, Alignment (Boston: Harvard Business School Press, 2006) 146.

[54] Tad Leahy, "The Elusive IT Balanced Scorecard," Business Finance, August 2003. Article accessed at www.businessfinancemag.com/magazine/archives.

[55] Paul R. Niven, Balanced Scorecard Diagnostics: Maintaining Maximum Performance (New York: John Wiley & Sons, 2005) 58.

[56] Quoted in: Kerry Patterson, Joseph Grenny, Ron McMillan, and Al Switzler, Crucial Conversations (New York: McGraw-Hill, 2002).

[57] Jack Welch with John A. Byrne, Jack: Straight From The Gut (New York: Warner Business, 2001).

[58] John P. Kotter, Leading Change, (Boston: Harvard Business School Press, 1996).

[59] From a correspondence with the author dated May 16, 2006.

[60] See note 30 above.