Chapter 1

The World's Biggest Mobile Economy

What is the most celebrated Chinese holiday globally, by the Chinese and by everyone else? Here's a hint: It's not the Spring Festival, also known as the Chinese New Year. It is November 11, known as Singles’ Day. Not only is it the largest online shopping day each year in China, but it is also the largest in the world in terms of the total value of transactions.

Started by China's e-commerce giant Alibaba in 2009, the November 11 holiday has become an annual 24-hour online shopping extravaganza. (See the “Singles’ Day” box.) It is the single most important day each year for online vendors to target young, tech-savvy consumers who are accustomed to buying online and using their mobile phone wallets to pay for almost all goods, services and entertainment.

In 2015, during the run up to the shopping holiday, Alibaba hosted a gala celebration titled Double-11 Night Carnival. The four-hour TV variety show was directed by a top Chinese film director, Feng Xiao-Gang, and held at the Water Cube, a landmark structure built for the 2008 Beijing Olympics. Aired on the satellite channel Hunan TV, the variety program was also streamed on China's major video streaming site Youku Tudou, which was acquired by Alibaba only days before the Carnival.

Just like China's annual Spring Festival variety show carried by the state television network CCTV, the 2015 celebration included an 11.11 countdown, “to celebrate the potential for limitless innovation that technology has provided for all of us”, according to Alibaba's promotional statement. To ensure the 2015 holiday was a “Global Shopping Festival”, during the televised extravaganza Alibaba's founder, Jack Ma, rang the opening bell for the New York Stock Exchange remotely from the Water Cube, while the program featured western celebrities including the actor Daniel Craig, who played James Bond in the latest 007 film Spectre, as well as the singer Adam Lambert.

Employing China's social networks, Jack Ma had announced prior to the event that even the US President would appear at the Carnival. And as the celebration reached its climax, actor Kevin Spacey appeared as his character in the web TV series House of Cards, US President Frank Underwood. Thanks to the explosive growth of video streaming sites in China, House of Cards and Kevin Spacey are both famous in China. From an Oval Office set, Kevin Spacey addressed Chinese shoppers in a two-minute video. In his trademark Southern drawl, President Underwood expressed his disappointment that the White House firewalls blocked him from shopping online to take advantage of the “amazing deals” on that day.

This November 11 online shopping event in 2015 illustrates several important trends of China's e-commerce in the mobile internet age.

First of all, while e-commerce has disrupted retailers world-wide, its boom in China is unprecedented both in terms of pace and scale. In 2013, China overtook the US as the world's biggest e-commerce market. Today, this annual shopping festival generates more sales than “Black Friday” and “Cyber Monday” in the US combined. On the basis of gross merchandise volume (GMV), Alibaba is now the largest online and mobile commerce company in the world.

For the 2015 Singles’ Day, Alibaba Group announced that $14.3 billion GMV was transacted on its online marketplaces, an increase of 60% from 2014, making the 2015 GlobalShopping Festival the largest shopping day in history. It is worth noting that the GMV numbers in recent years have enjoyed steadily increasing growth (see Table 1.1). Also, the actual number of shoppers is increasing as additional buyers from smaller Chinese cities are using e-commerce, primarily through Alibaba's marketplaces every year. Although their purchases are smaller than those placed by buyers from first-tier cities, such as Shanghai and Beijing, they are an important driver for growth in the future.

Table 1.1 Singles’ Day gross merchandise volume (GMV) growth 2012–2015

| Year | GMV ($) | Year-on-year growth |

| 2012 | 3.3 billion | – |

| 2013 | 5.9 billion | 80% |

| 2014 | 9.3 billion | 58% |

| 2015 | 14.3 billion | 60% |

(Data Source: Alibaba)

Second, Chinese customers are migrating to the mobile internet rapidly. Because China has the largest smartphone user population in the world, the trend of “going mobile” has taken off with greater speed than anywhere else in the world. As the wired infrastructure has not yet fully covered the country, for many people in China, especially in rural areas, their first internet experience is often mobile instead of PC-based – from the moment they start using a smartphone. Since 2014, the number of people in China who surf the internet via mobile devices has exceeded the number of people doing so via their computer, with smartphones becoming the primary device of access for Chinese internet users.

On Singles’ Day 2014, 43% of all transactions through Alibaba were made through mobile devices, up sharply from 2013 (21%). Even more remarkable, in 2015 Alibaba's consumers made the majority of orders (68.7% of total GMV) through mobile channels. The total mobile GMV was approximately $9.8 billion, an increase of 158% from 2014. In fact, 2015’s mobile GMV alone exceeded the total GMV in 2014.

Third, this latest shopping festival has also highlighted Chinese consumers’ strong demand for international products. In 2015, Alibaba specifically made “globalization” a critical priority for the group's strategy, and it was committed to making the 2015 shopping festival “a truly and unprecedentedly global shopping experience for consumers”.

According to Alibaba, more than 16,000 international brands, including Burberry, Apple, and Uniqlo, took part in the 2015 sale. During the Carnival TV show, western brands such as Columbia, Levi's, Budweiser and Corona bought time slots for advertisements. Buyers and sellers from 232 countries and regions participated. 33% of the total buyers made purchases from international brands or merchants, with the United States, Japan, South Korea, Germany and Australia as the top countries selling to Chinese consumers.

Finally, the inaugural Carnival show in 2015 illustrates the seamless fusion of online shopping and mobile entertainment. The main use of mobile internet in China is skewed towards fun and entertainment. Moving to align with this trend, Alibaba has recently been establishing its own movie and television production subsidiaries, launching a film crowdfunding financial product, and fully acquiring the online streaming video site Youku Tudou. The movie unit of Alibaba made its first direct Hollywood film investment in Paramount Pictures and actor Tom Cruise's blockbuster Mission: Impossible — Rogue Nation.

By integrating the shopping event with a televised show, Alibaba successfully created a continuous feedback loop of online consumption of both merchandise and entertainment. The Carnival show kept people up until midnight, when the sales began. During the program, online viewers were prompted to check their smartphones periodically, as discount coupons were distributed through their mobile shopping apps. Viewers could also play along with the game show portion of the event. When the hosts of the show greeted “Mr. Bond” and asked viewers to “support 007”, consumers were guided to online ticketing services for the latest James Bond film Spectre.

However, it would be premature to conclude from this event that e-commerce is taking over entirely from traditional retailers in China. In mid-2015, just a few months before the online shopping festival, Alibaba spent $4.6 billion to acquire a stake in Suning Commerce Group, one of the largest retailers in China. At the time of the transaction, Suning had a network of more than 1,600 outlets spread across 289 cities in China, selling electronics, appliances, and other products. The two companies announced a partnership in online sales and offline logistics by breaking the information wall for products, services and memberships between the online and offline channels.

Not to be outdone, in August 2015 JD.com, Alibaba's primary e-commerce rival in China, also bought a 10% stake in Yonghui Superstores – another major domestic supermarket – for $700 million. Founded in 1998, Yonghui Superstores ran 364 supermarkets on the Chinese mainland, with ambitious expansion plans for hundreds more in the coming years. Similar to Alibaba, JD.com also aimed to leverage Yonghui's existing networks of bricks-and-mortar stores to boost its supply chain and diversify its offline offerings.

The marriage between the e-commerce giants (Alibaba and JD.com) and traditional retailers (Suning and Yonghui) illustrates a new retailing model that fully integrates online and offline channels, which is frequently referred to as “omni-channel”. To enhance the digital consumers’ experience, the internet firms strive to use both online and offline touch-points to cover the full search, decision and purchase journey, including researching and comparing prices online, trying products at offline shops, paying online or at an offline outlet, and arranging delivery online for pick-ups at physical shops.

In fact, one of the two key themes of the Alibaba 2015 shopping festival is offline-to-online (O2O) (the other being globalization as mentioned previously). Approximately 100,000 brick-and-mortar stores in China, such as Suning and Intime (another Alibaba-invested retailer), will establish strategic O2O collaboration agreements with Alibaba Group, which in turn will cover marketing, customer management, post-sales management, logistics, and more, for the physical stores.

Interestingly, this new “omni-channel” trend provides some answers to the debate on the future of the e-commerce model as represented by the competition between JD.com and Alibaba. Alibaba operates the largest marketplaces for e-commerce, while JD.com is the largest online retailer in China. Alibaba is more akin to a combination of eBay and PayPal, and its marketplace serves as a platform to connect buyers and sellers and provides services like online payments. JD.com is more like Amazon which deals with inventory, sales and distribution directly. Their growing integration with traditional offline retailers, however, makes their business models increasingly similar to one other.

Of course, the online shopping extravaganza is but one example of the explosive growth of China's digital economy. For China, the years 2014 to 2015 were the most important inflection point in the history of the internet, as the Chinese internet population officially entered into the age of mobile internet and multi-screens (smartphones, tablets, personal computers and more). During this incredible period of change, the mobile internet in China has given rise to a dynamic tech sector, thriving social networks and the world's largest digitally-connected middle income class.

At the same time, the integration of e-commerce with offline retailing is a case in point for the “Internet Plus” strategy promoted by China's central government. In his public speeches, President Xi Jinping emphasized that innovation, economic restructuring and consumption should be among the top priorities of China's next stage of growth (the 13th Five-Year Plan for 2016–2020). The “Internet Plus” action plan seeks to drive economic growth by integration of internet technologies with manufacturing and business. The term “Plus” is a reference to the internet as an enabler of new developments and higher efficiency, as in the case of the new “omni-channel” retailing model above.

Urbanization, Mobile Users and Information Consumption

Delivering the government work report in March 2016, Premier Li Keqiang noted that China's development is at a critical stage and new growth poles should be created through incessant innovation to transition to a “new economy”. This was the first time the term “new economy” has ever been mentioned in the government work report. Meanwhile, the government's 13th Five-Year Plan (2016–2020) placed strong emphasis on household consumption and industrial innovation as the economy's new growth engines.

As background, after decades of staggering growth, China has entered into a stage of moderate growth and has put more emphasis on the sustainable quality of growth in the future. In the 35 years between 1978 and 2013, annual growth of the economy averaged close to 10%, and over 11.5% between 2003 and 2007. That growth rate slowed to 7.4% in 2014, and it dropped further to 6.9% in 2015 as the government focused more on the transformation of the economic model than on a high GDP growth rate per se. For the upcoming five years (2016–2020), the 13th Five-Year Plan set an “above 6.5 percent” average growth target.

The new administration has referred to the moderate growth in the new era as “the new normal”. The new economic model is a consumer-driven growth model, where China shifts the balance of its economy away from government-led investment and import-export business and towards domestic household consumption. To achieve this goal, Premier Li Keqiang has written that “urbanization has the greatest potential for boosting domestic demand”. In China's urbanization plan, the central government aims to boost domestic consumption by increasing the proportion of urban residents to 60% by 2020 (approximately 800 million people).

What makes this ambitious program unique is the government's parallel effort to promote information-related consumption as a related new growth engine. In late 2013, China's State Council issued a blueprint to officially promote “information consumption” – a term that includes both “consumption based on information technology” (such as e-retailing and online banking services) and “quality information products for consumption” (such as movies and online videos). For example, as shown by the shopping sprees on Singles’ Days in recent years, the rapid expansion of the middle class and the exponential growth of the e-retailing industry have created an important catalyst for consumption growth in China.

To help implement this, the central government launched a “Broadband China” strategy in 2013 to significantly improve the country's information infrastructure, which equates internet networks with traditional forms of public infrastructure, such as highways and high-speed rail services. Also in 2013, the Ministry of Industry and Information Technology (MIIT) officially granted fourth-generation (4G) mobile technology licenses to three domestic telecommunication operators, marking the beginning of China's 4G era. The 4G network coverage is expected to include all the cities in the country within a short period of time. With such an infrastructure in place, China will see the development of “smart cities”, with much improved Wi-Fi coverage in public places, FTTH (fiber-to-the-home) capability, HD cable subscription and so on, each of which will drive development and consumption.

According to the official data from the China Internet Network Information Center (CNNIC), by the end of 2015 China had 688 million internet users (just above 50% of the total population), which was by far the world's biggest internet population. While the internet-enabled business and innovation are set to play a major role in fueling China's economic growth, it also has profound implications for society, such as how people relate to and communicate with each other. One dramatic example of the internet gaining familiarity and popularity in China is a recent phenomenon known as “human flesh search”. (See the “Renrou Sousuo” box.) Many similar new terms created by the internet culture in China will be examined in the following chapters in the context of their related business areas.

Since the beginning of the 21st century, a large proportion of the Chinese population has stopped using landline phones entirely and moved to using mobile phones. The fact that usage of landlines was not as pervasive as in Western economies meant that for many the transition did not involve a migration from fixed-line phones at all, but was a transition to mobile phones directly. With their advanced and ever increasing technological capabilities, smartphones are also replacing personal computers (PCs). For many people in China, especially in rural areas, their first internet experience is often mobile instead of one connected with a PC – indeed, their first online experience is the moment they start using a smartphone.

In other words, the Chinese population has transitioned directly into a mobile-first mobile-only era. Focusing on a niche passed up on by premium brands like Apple and Samsung, the Chinese brands like Xiaomi, Huawi and Lenovo have mainly offered low price, high performance devices, which have played well into the general Chinese population's desire to own a smartphone and to access the internet, but at an accessible point of entry. It is worth noting the three domestic brands are neck-and-neck in terms of their sales volume in China, and they are now competing directly for the No. 3 position in the global market (just behind Apple and Samsung, the two undisputed market leaders).

The spread of low-cost mobile phones quickly reached all parts of this geographically vast country, and the large screens strongly preferred by Chinese customers from the outset, a trend driven by the mobile-only tendency noted above, made them great platforms for various types of transactions. For example, the lack of a developed credit card system in China means that mobile payment is the “first” and “only” non-cash payment experience for many users. Also, the Chinese users have adopted social network technologies comfortably. For them, the smartphone has not only become an extension of their daily routine, but also an indispensable link with the rest of society.

As a result, the percentage of mobile internet users (as a subset of all internet users) has risen steadily, a trend that has accelerated in recent years (see Figure 1.1). According to CNNIC's data, in mid-2014 more than 500 million people in China reported gaining access to the internet with mobile devices, exceeding for the first time the percentage who reported using computers to go online. By the end of 2015, China had the world's largest mobile internet user population of 620 million, representing more than 90% of the total internet population.

Figure 1.1 The Steady Increase of Mobile Internet User Percentage (2007–2015)

(Data Source: CNNIC, December 2015)

In summary, China's mobile infrastructure has developed with remarkable speed, marked by the exceptionally rapid penetration of internet access, the uptake of smartphones by users and the spread of digital social networks. In addition to the unrivalled internet user population size, what also makes the market unique is the fact that China is the largest “mobile-first” and “mobile-only” market in the world. Backed by a huge middle class that is digitally connected, there are enormous opportunities on the horizon as China shifts towards a model of economic growth that is based on productivity, innovation and consumption.

More importantly, the development of the mobile internet has helped China develop more “smart cities” and a “shared economy” at a time the public goods and services supplied by all levels of government are stretched by the country's large population and fast growth. The mobile infrastructure also creates a new social infrastructure that is helping bridge the digital divide in China, allowing more Chinese people to benefit from the digital economic boom, enabling megacities to execute on their urbanization policies, and narrowing the income gap between cities and less developed areas.

For example, with daily subway commuters exceeding 10 million, the Beijing municipality increased subway fares to cut passenger numbers in 2014, which created substantial controversy. In an optimistic scenario for the future, more e-commerce and e-business opportunities may involve more Chinese people in the growing economy, while reducing the number of commuters, and therefore traffic. In healthcare, advanced communication technologies enable China's first-tier hospitals, via regional health-information networks, to make high quality treatment available to lower-tier hospitals by linking patients to medical specialists elsewhere.

During the 2016 Mobile World Congress (MWC) in Barcelona, the GSMA (the representative body of the world mobile industry) published its findings, which showed that when compared to developed markets, China is more advanced in terms of consumer uptake of mobile data services. The transition from fixed line to mobile internet (from voice-centric to data-centric services) is happening all over the world, but China is leading the field with a strong uptake of mobile data services, such as “gaming, apps and video”.

For example, there were 73% of Chinese mobile users accessing social media over their phones, compared to only 43% in the UK, where just 40% of mobile users have IP messaging apps, compared to 81% in China. GSMA concluded that “the ability to access a wide array of mobile data services in China – enabled by the country's rapid rollout of 4G networks and supported by strong local content players – is creating demand- and supply-side drivers”. Indeed, with a 4G network capable of handling faster data-heavy applications than before, mobile service sectors such as video streaming and internet movies are making big leaps, and China's mobile netizens are becoming more sophisticated. The next section will introduce the internet giants BAT (Baidu, Alibaba and Tencent), their mobile apps and the Chinese customers that the internet firms seek to cover seamlessly.

Baidu, Alibaba and Tencent (BAT)

While the first wave of “open and reform” policies in the 1980s and 1990s created a large working class in China, the next wave of globalized growth in the 21st century has created a middle class that is already the size of the entire US population (and it is expected to double in a few more years). Collectively, these new consumers have a significant amount of disposable income and they are also digitally connected. Mobile internet usage by this demographic is primarily focused on socializing, shopping and entertainment, due to the dominant composition of young netizens (below 39 years of age) in the internet population (see Figure 1.2).

Figure 1.2 Demographic of Chinese Internet Users

(Data Source: CNNIC, December 2015)

According to demographic data from the CNNIC, by the end of 2015, more than 75% of internet users are between the ages of 10 and 39. Close to one-third of the internet population is between the ages of 20 and 29 (29.9%). As the mobile network speeds up and smartphone technology continues improving, the younger generation of Chinese netizens have shifted their entertainment habits online in record numbers. For the majority of their time online, they play online games, watch videos, assume online personas in the virtual world and form online communities.

This digitally-connected middle class is leading a seismic change in the Chinese consumer market. Not only is this new generation of consumers extremely comfortable with mobile e-commerce, they have enjoyed unprecedented exposure and access to foreign brands, with social networks having tremendous influence on their purchasing decisions. As a result, they have high expectations both of quality and of service that did not exist in China previously. In particular, the younger demographic consists of “conspicuous consumers” who like to share their experience publicly and for whom consumption is a social experience.

A list of the most commonly used mobile apps (as of mid-2014) provides a perspective on the new generation of consumers’ preferences (see Table 1.2). The year 2014 is viewed as a “breakout” year for mobile internet in China, so the leading apps are a reflection of the important areas where internet giants have accumulated a significant number of users. The three most important areas – social network, mobile search and e-commerce, as represented by the three leading firms Tencent, Baidu and Alibaba – are discussed in detail below respectively.

Table 1.2 Top 10 most used mobile apps (June 2014)

| Ranking | App name | Monthly activeusers (million) | Sector/Company |

| 1 | 383.17 | Messaging app/Social network (Tencent) | |

| 2 | 316.69 | Messaging app/Social network (Tencent) | |

| 3 | Baidu | 136.33 | Mobile search (Baidu) |

| 4 | Mobile Taobao | 123.48 | e-Commerce (Alibaba) |

| 5 | QQ mobile browser | 113.33 | Mobile browser (Tencent) |

| 6 | Sougou Chinese character input | 106.84 | Chinese character input (Sougou) |

| 7 | 360 Phone Guardian | 94.431 | Anti-virus software (Qihoo 360) |

| 8 | QQ Music | 94.429 | Online music (Tencent) |

| 9 | Qzone | 90.61 | Social network (Tencent) |

| 10 | Baidu map | 89.10 | Map services (Baidu) |

(Data Sources: China Daily, Analysys International)

Tencent's Social Network

As mentioned previously, two key themes of China's mobile internet usage are socializing and entertainment. In the mid-2014 report by the research firm Analysys International as summarized above, China's internet giant Tencent Holdings, whose focus is online games and social networking, owns half of the country's top ten mobile applications by monthly active users. Most notably, Tencent's two popular mobile messaging apps WeChat and QQ take the top two positions in the ranking.

QQ is one of Tencent's older applications for person-to-person communication. It was one of the earliest platforms in China where users could post pictures, videos and blogs. Its strategy is to offer entry-level services for free, then charge for added features once users are hooked. Users are willing to pay for “value-added services” such as weapons and costumes for their avatars, and it has proven to be a profitable model for Tencent. It is all the more remarkable as Tencent's peers are still primarily focusing on advertising revenue in their business models.

The newer version of WeChat is now the most popular forum in China. It started off as a messaging service similar to WhatsApp, and now it has evolved into a platform of integrated apps. For instance, many people find typing Chinese characters on a smartphone screen time-consuming, so WeChat has developed strong voice capabilities and has offered free voice messaging features. Chinese users can send text, links, videos and photos to friends more cheaply and conveniently through WeChat (by way of data package charges) than through traditional texting services offered by wireless carriers (with charges per text).

What is also remarkable is that Tencent has built an entire ecosystem of interrelated services and functions that can be integrated directly within WeChat. Alongside text, video and voice messaging, WeChat users can now shop and make mobile payments, play games, book hotels or flight tickets, order a taxi and do many other things without ever leaving the app ecosystem. Because Chinese shoppers are increasingly resorting to friends’ reviews and recommendations online when they make a purchase, the WeChat platform becomes an ideal place to introduce offerings that can benefit from word-of-mouth recommendation and peer reviews, such as branded goods and experience consumption. From its humble beginnings as a messaging service, WeChat has become a full-blown, unified ecosystem for mobile commerce, content and entertainment.

Baidu's Mobile Search App

The main search engine in China, Baidu, has Google-like predominance in China's search and maps services. Today, urban residents mostly turn to their smartphones to navigate their daily lives as they commute in the cities, which explains Baidu's mobile search apps becoming the second most widely used apps after social messaging, ahead of traditional top activity e-commerce. According to Baidu, searches on smartphones have exceeded those on PCs since the second half of 2014.

However, from the advertising income aspect, searches on mobile phones are not as profitable as those on PCs, even though the market for these is growing substantially faster. The smaller screen of smartphones means less space for ads than on standard computer screens or laptops, and advertisers are still trying to figure out new strategies for driving traffic from them, as click-through rates tend to be lower as well. However, it is still possible for revenue from searches on the mobile platforms to catch up because they provide the merchants with additional information from the users, such as the context and location of their searches.

One of the most promising business opportunities is the growth in searches for location-based services. Traditionally, searches are considered as tools to connect people to information, but in the age of the mobile platform, searches can function as a tool for connecting people with services. Among Baidu's fast-growing mobile offerings is the Baidu Mobile Maps app, which integrates maps with related information of merchant partners, so that users are able to conduct searches for services close to their location.

The best showcase of Baidu's expertise in location-based services is an interactive heat map on its website at the Spring Festival each year, which visualizes the movement of people during the one-month travel rush when millions of Chinese travel across the country for holiday family gatherings. In addition to the heat map, Baidu also releases the “Spring Festival Homecoming Tool Kit” on Baidu Maps. During the chaotic holiday travel season, the tool kit provides users with information on the cities’ weather conditions, traffic conditions, railway timetables, flight schedules and locations of holiday train tickets sales agents.

The capability for location-based searches is the key to the growth of online-to-offline (O2O) transactions like the “Homecoming Tool Kit” example. O2O can be broadly defined as the integration of offline business opportunities with the activities on the internet. In its most popular form, O2O means attracting retail customers online, and then directing them to physical stores for actual goods purchases or real-life experiences such as seeing movies, dining out, hailing taxis and so on (see Figure 1.3). For instance, Baidu's investment into and partnership with Uber, the US car-hailing mobile app company, has been critical for the latter's rapid expansion in the China market.

Figure 1.3 Location/Map Searches Are the Key to the O2O Business Model

Alibaba's e-Commerce Empire

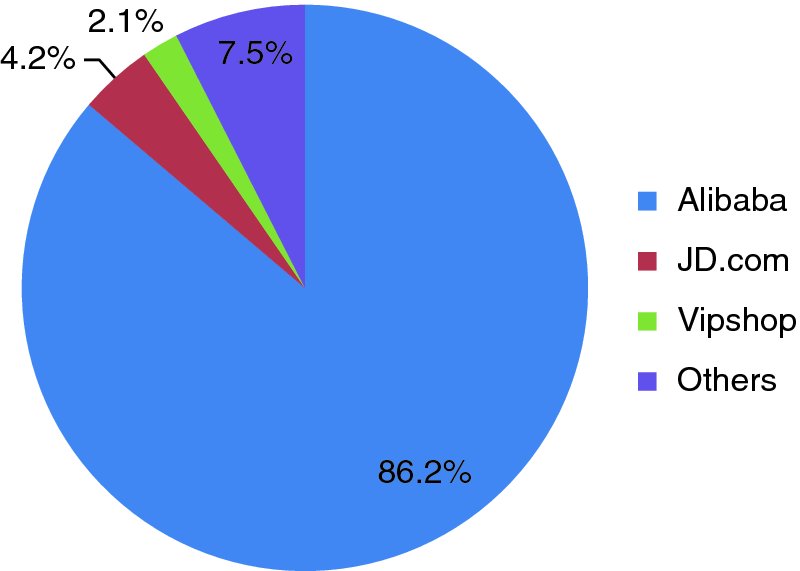

As mentioned at the beginning of this chapter, Alibaba dominates the e-commerce world through two online market-places – Taobao and Tmall (the latter is specifically intended for high-end goods and luxury brands). Its leading position is further strengthened by the widely-used online payment system Alipay, which is affiliated with Alibaba Group. So far, Alibaba's e-commerce prowess has carried the momentum into the mobile world. As Figure 1.4 shows, in 2014 Alibaba owned an overwhelming majority (86.2%) of the mobile e-retailing market. (In fact, it had an even bigger share of mobile shopping than in the overall online retail market.)

Figure 1.4 Market Share of China's Mobile Shopping Market in 2014

(Data Source: iResearch, 2015)

Mobile e-retailing enables customers to place online orders anytime and anywhere, which aligns with Chinese consumers’ desire for speed and convenience of “any time” shopping. Many of those purchases are ad hoc decisions arising from offline world advertisements, social conversations, or simply random thoughts. According to CNNIC data, in 2014 13.9% of Chinese customers purchased goods on smartphones while travelling on public transportation and another 10.6% customers did so while waiting in queues.

However, the wide usage of Tencent's social network platform such as WeChat, as well as Baidu's mobile search, indicates that popular mobile apps can potentially become primary mobile-commerce platforms in their own right. For example, in recent years Tencent has permitted merchants to set up “little WeChat stores” (“Weixin Xiaodian” in Chinese) by verified public accounts linked to the app's own payment system. Similarly, individual WeChat users can establish in-app stores to sell goods to their friends and followers. This type of “social distribution platform” based on social contacts has different dynamics from Alibaba's e-commerce empire. To maintain its leadership in mobile e-retailing, Alibaba has in turn invested aggressively in the mobile market, including social network and map services.

Competition for the Closed Loop

While the three internet giants that make up BAT come to the mobile world with different intrinsic strengths – search, e-commerce and social network respectively – all of them have an expansive vision to create a mobile world into which consumers can immerse themselves. This type of platform is expected to link every possible item or content with consumers who are looking for them, whether domestic or abroad, online or offline. The general belief is that the platform with the most users will eventually capture the biggest share, and therefore the highest profit, from the overall mobile economy in China.

This concept is often referred to as a “closed loop” (or “ecosystem”). In a closed loop, an internet firm has an important role throughout the online consumer's decision journey: generating demand, finding and comparing local merchants, moving customers from considering to making a purchase, paying and then reviewing or sharing with a friend and building loyalty. Similarly, in the O2O business, the firm delivers an end-to-end service, from taking an order to arranging for a service and collecting the payment.

Because the closed loop is so efficient, and because it drives revenues, all the internet firms – BAT and their competitors – are attempting to broaden their platforms through acquisitions and alliances with various online and offline businesses. In small and large ways, they are stepping into every possible corner of the mobile world. Compared to their peers, the BAT corporations have an enormous advantage from what economists call “network effects” – the more people use them, the more indispensable they keep getting. Their existing major networks create big data, which is also a rich source of information when these established players choose to pursue new opportunities or new market sectors.

Because of the advantages stemming from their existing platforms — the users, the data and the large amount of revenue income they generate, the BAT have extended their business development and acquisitions far beyond their core products. They're making waves in taxi-hailing, healthcare, and finance; they are creating advertisement business, building robots and connected cars and making blockbuster movies. In particular, the mobile entertainment business has strategic importance for BAT's “ecosystems”. That's because entertainment contents and services are not only an important revenue source by themselves, but also a distinguishing factor that draws users to any specific e-commerce empire and further keeps them hooked. As shown in the list above, entertainment content consumption apps are among the top ten list. (In 2015, according to other research firms’ rankings, the Tencent and Youku video apps have also joined the top ten most actively used apps.)

According to the CNNIC data by the end of 2015, 71.9% of users watched online videos on their smartphones, making smartphones the leading terminal for viewing videos, ahead of desktops or laptops (see Figure 1.5). The figure is expected to grow as Chinese mobile carriers adopt faster fourth-generation networks that are more suitable for video viewing. The young internet population is increasingly watching videos, reading books, sharing and having discussions about content on their hand-held devices while commuting on the subway or in their brief moments of spare time throughout the day. They may watch a short video or read an installment of an online novel for a few minutes while they are on the move or in between tasks.

Figure 1.5 Different Terminal Usages for Watching Online Videos

(Data Source: CNNIC, December 2014)

As one would expect, these internet giants have quickly evolved into what might be viewed as full-fledged media companies. The same has also happened in dining services, car-hailing and other sectors. Because every major firm's goal is to create a “closed loop” of its own, the companies are increasingly in competition with one another. As many players race to offer services at below cost to compete for users, the market starts to have doubts about the sustainability of such businesses. In fact, the internet firms are taking huge bets by spending heavily on subsidies because the repeat customers may not stay when the subsidies end. The many cases reviewed in this book will examine whether a profitable model will eventually arise in those markets.

Overall, the Chinese economy is going through a structural shift to more moderate, but more sustainable, growth. After becoming the second largest economy globally, its pace of expansion is slower and the course may be bumpier, but its consumption growth is undoubtedly still tracing a staggering trajectory. According to the data from China's National Bureau of Statistics, in 2015 the services sector surpassed the 50% share of GDP for the first time in history. In addition, the services sector grew at a much faster pace than primary sectors (agricultural, forestry, etc.) and secondary sectors (manufacturing, utility, natural resources, etc.).

In other words, China's expanding middle class has grown in importance as the country's traditional growth engines, such as manufacturing and exports, start to slow down. Under the new economic model, consumer spending on e-commerce platforms is meant to counterbalance the slowdown in other parts of the economy. The sophisticated and seasoned middle class shoppers – those able and willing to pay a premium for quality and to consider discretionary goods and experience consumption – are therefore emerging as the new pillar for economic growth. To some extent, internet firms like BAT, which connect and empower this huge swell of consumers, are a proxy for the prospects of Chinese consumption and the state of the Chinese economy itself.

Internet Plus in Business Sectors

China's “internet plus” strategy was unveiled in the 2015 government work report, which aimed to “integrate mobile internet, cloud computing, big data and the Internet of Things with modern manufacturing, to encourage the healthy development of e-commerce, industrial networks and internet banking, and to help internet companies increase their international presence”.

Internet plus means the mobile economy is more than simply expanding the ubiquity of e-commerce through mobile platforms. On the surface, internet plus means incorporating today's mobile technology into the traditional industries to provide better consumer communication and transaction services. Chinese companies are thus investing heavily in internet infrastructures, such as cloud computing, wireless communications, new digital platforms, big data analytics and more. Many companies are looking to the internet for a new set of tools to engineer productivity improvements. As a result, consumers will benefit from lower prices and transaction costs, as well as better goods and services.

The more profound implication of Internet plus is growth and innovation by way of incremental consumption demand and new business models where traditional industries use the internet to run key aspects of their business. In other words, internet plus is more about “internet thinking” than “internet using”. As mobile internet is leading the fourth industrial revolution globally, the “creative destruction” of traditional industry sectors is happening in all markets. Driven by the largest mobile internet population worldwide, the speed and scale of this transformation in China is unparalleled: immature industries such as retail and logistics leapfrog straight from the early industrial age to the internet one, and the growth and positive spillovers go beyond the consumer goods sector to services, entertainment, media, finance and other traditional industry sectors.

As illustrated by the Alibaba/Suning alliance and the JD.com/Yonghui investment, in order to fully serve and monetize digital consumers, the retail industry needs to use internet tools to get even closer to them and adopt more flexible business models. The traditional retailers need to move away from the perception that e-commerce is merely another sales channel for their products, as it is critical for customers to get the same products, services and shopping experience in every channel where they choose to make purchases. The new trend is for retailers to provide a “seamless omni-channel shopping experience” by integrating their online and offline channels, instead of having separate systems to sell products online and offline.

In addition to consumer goods, the growth in “experience” consumption, such as movie going, dining out, taxi-bookings and so on, is at the core of the O2O trends in China. However, even among the internet giants, no single player dominates in every area of the mobile linkages relating to the O2O market. If Baidu is understood to be the best link for people and information (search), Alibaba for people and goods (e-commerce), Tencent for people and people (social network), then O2O is the link between people and service, which requires the utilization of all three of the above connectors. That makes the competition in the O2O market extremely fierce and its outcome critical to each of the players involved.

Going forward, the Chinese economy will see internet business penetrate deeper into numerous traditional industries. Among other things, the examples above demonstrate that the new value creation from the mobile internet can come from the following areas:

- Introduction of new competition. The internet lowers barriers to entry dramatically, making it possible for start-ups to launch quickly, scale up and compete. It gives entrepreneurs access to low-cost resources to start new businesses.

- Reduced transaction costs. The internet allows companies, consumers, researchers and the public sector to communicate and collaborate instantly. It facilitates productivity gains from e-commerce, crowdsourcing and internet-enabled supply chain management. It also allows manufacturers to connect directly with consumers, cutting out middlemen.

- The use of big data analytics. For instance, big data can lead to cost-efficient analysis of the credit risks of lending to small businesses and individuals. It also allows e-retailers to deliver personalized recommendations to consumers based on their past purchases.

- The ability to meet long-tail demand. For example, marketplaces like Alibaba have aggregated all the brands and offerings so that customers have a lot more choices online than they would in physical markets. In the fresh food sector, cross-border e-commerce provides customers with access to foreign offerings directly.

- The incorporation of social networks into purchase decisions. The information flow on social networks makes consumers more informed and active.

- Enhanced transparency, competition and efficiency can lower prices and improve the quality of products. The internet also empowers consumers to compare offerings from a wide range of companies easily.

In addition to business model transformation, internet plus has also stimulated “shared economy” applications that have led to broad social benefits. For example, as is the case in many cities worldwide, the demand for cross-town transportation is at the heart of an urban lifestyle in modern China. Although more individuals are buying cars, the demand for taxi services is steadily increasing as the population in many cities has exploded due to swift urbanization. The main issue is that demand is distributed unevenly because there are too few taxis during rush hour. Meanwhile, four-fifths of China's private vehicles reportedly remain idle for long periods of time, as the lack of parking spots in downtown areas forces most car owners to leave their cars at home – an enormous waste of resources.

As such, the mobile apps offered by the US car-service and pooling company Uber and its homegrown rival Didi Kuaidi (backed by Alibaba and Tencent) have been widely embraced by Chinese urban residents. These apps use the mobile internet to match demand and supply in real time, reducing information asymmetry between passengers and drivers. In fact, Uber's rapid growth in China so far might be the best performance by a US tech company in the country for a long time. The internet transformation of traditional industries and services like taxi apps is anything but trivial. It could ultimately make many modes of urban transportation cheaper, more flexible and more widely accessible to people across the income spectrum.

What's even more interesting is the fact that Uber's service has taken off in China much faster than it did in the US. For example, Uber's top three most popular cities worldwide – Guangzhou, Hangzhou and Chengdu – are all in China. The main reason, of course, is the large urban population and the high concentration of city residents. There are approximately 200 cities in China with more than a million people. As the growing Chinese economy brings personal wealth to more people, the Chinese urban residents have generated a strong, new demand for goods and services, and the cities need to adopt “shared economy” models as a result of their scale, density and simply because of the sheer rapidity of the transition. The related business implication is profound: new mobile applications can receive market feedback and achieve meaningful scale more quickly in China than elsewhere, because new technology based on “human infrastructure” tends to spread faster in China – this is because of the size of the mobile user market.

In that context, China is perhaps the best lab and market for “shared economy” applications. The mobile internet and smartphones have created a new social coordinating mechanism, and what the market sees is a seemingly endless potential to put goods and labor that are less than fully utilized to productive use. In the case of Uber and Didi Kuaidi, repurposing a fleet of idle private vehicles as taxis both cuts resource idleness and alleviates the shortage of rush hour taxis greatly. These mobile applications will help to create a more inclusive model of urbanization and economic growth because IT innovations intrinsically emphasize sharing over ownership. When more people are integrated into this new form of growth, everyone will get a piece of a smarter pie.

Innovated in China

The period of 2014 to 2015 was a time of inflection for the global competition between Chinese and US tech players. The blockbuster IPOs of China's two largest e-commerce companies, Alibaba and JD, were more than a showcase of the mobile internet boom and economic model transformation in the Chinese market. Their US listings – Alibaba at the NY stock exchange and JD at the Nasdaq exchange – also shook overseas capital markets as well as the global virtual world.

What is really interesting is that the challenges that Chinese companies now face in overseas markets are very much the same as those encountered by US companies such as Amazon and eBay when they ventured into China. More than a decade ago, those American tech firms were similarly intrigued by the Chinese market's large user base and fast market growth. Yet the cultural, language, political and technological elements turned out to be more complex than they expected. As a result, they swiftly retreated and chose instead to focus primarily on the North American and European market in the past few years.

The difference, I believe, is that for Chinese firms overseas expansion is a must instead of an option. While there is always more growth to be found within China, the fastest-growing market in the world will inevitably slow down, and the Chinese top tech companies must search and find their next billion customers in order to expand. And it is not only about expansion, any company that is strictly local within the context of a global economy is vulnerable either to competition or to takeover by a larger global player. For companies today, and this is not only true for Chinese companies of course, expansion into new markets is a question of survival. Their journey to the foreign markets is full of challenges, but with their overseas listing and significant foreign share ownership, one would expect Alibaba, Tencent and other Chinese companies to manage cultural differences better than the US firms did in China a decade ago.

While BAT and other Chinese firms are expanding globally to find growth in overseas markets, the internet companies in Silicon Valley such as Uber and Linkedin, are also focusing on China as the single largest market for growth after the US. Although the last decade saw Chinese and US firms establishing themselves in two isolated home markets, respectively, competition between them is set to heat up. In addition to fighting more directly in each other's territory, the Chinese and US tech players are also facing each other in other global markets, especially in the emerging markets in Asia and Africa.

Going forward, the Chinese market is poised to be a trend-setter, rather than a trend-follower, in next-generation mobile devices and services. Its unique strength is its unrivalled internet user population size, because data in the digital era is becoming a significant asset. With a population of approximately 1.4 billion and nearly 700 million internet users in China, the data in China's consumer market is primed for surging growth. It is the oil of the information economy and the foundation of upcoming Chinese-designed products and new business models.

Similarly important, and what makes the market unique, is the fact that China is also the largest “mobile-first” and “mobile-only” market in the world. Therefore, from the application side, China's market has evolved in a very different way from the Western equivalent, moving much more aggressively into mobile. A ride-sharing mobile app is a product which best represents the direction of mobile internet development in China: one can post the information of other shared resources on a PC, but one cannot carry a PC while hailing a taxi on the street. Nor can the driver install a PC in the car. As illustrated in the Uber China case, new mobile applications can potentially achieve significant scale more quickly in China than elsewhere.

Furthermore, with government endorsement in the background, a dynamic ecosystem of entrepreneurs and start-ups is being built up organically. The network of established internet firms and their seasoned entrepreneurs, endless eager talent, abundant angel investors and venture capital, and a sophisticated manufacturing system are collectively making China one of the most interesting centers of innovations in the world (see Figure 1.6). This innovation ecosystem is centered on a network of “graduated entrepreneurs” from established internet firms such as BAT. This development resembles the multiplying effect seen in the Silicon Valley ecosystem in the last few decades, where the generation of entrepreneurs spawned by Intel, Netscape, Google and Paypal have created waves of start-ups.

Figure 1.6 China's Innovation Ecosystem

Not that long ago, China's tech industry was known primarily for low-cost, cheap knock-offs and copied internet business models. Fast forward to today and Chinese companies are moving to the forefront of global technology innovation. They can no longer be easily benchmarked against their Western counterparts. Alibaba at the very beginning might have been thought of as “China's eBay”, but now Alibaba is more of a mix of Amazon, eBay, PayPal and Netflix. Although Xiaomi is often referred to as the “mini Apple”, its business model is that of an “internet company” instead of a “smartphone company”, and its product offering has expanded into many different smart device categories.

As will be seen throughout the book, Chinese tech companies have already proven their mettle by catching up to global rivals in the smartphone and fourth-generation (4G) technology development process. They are now joining a fiercely competitive global race to become the first company to offer fifth-generation (5G) wireless networks and products to global customers. Many Chinese firms are moving aggressively into the future of an ultimate multi-device and hyper-connected world. For instance, Chinese players have invested heavily in the internet-connected and electric cars, which are considered to be the next key terminal for mobile internet after the smartphones.

Most remarkably, the new innovation ecosystem in China is creating more tech start-ups that cannot simply be described as the Chinese version of US firms. The new generation companies are more innovative in terms of products and technologies calibrated to local market needs, more willing to accept outside investors and have a more global outlook from the very beginning. (See Table 1.3 for China's top ten highest valued start-ups.) Their high valuation not only reflects their enviable scale in the world's largest mobile commerce market, but also illustrates the investors’ optimism in the special business models or product features that they are pioneering.

Table 1.3 China's top ten highest valued start-ups (as of January 2016)

| Company name | Valuation ($ bn) | Latest funding (valuation date) | Business description | |

| 1 | Xiaomi | 45 | December 2014 | Leading manufacturer of smartphones and smart devices |

| 2 | Ant Financial | 45 | July 2015 | Internet finance company covering mobile payment, cash management and wealth management |

| 3 | Meituan/Dianping | 18 | January 2016 | China's Groupon and Yelp, covering both group buying and consumer reviews |

| 4 | Didi Kuaidi | 15 | July 2015 | Dominant taxi-hailing app, Uber's biggest rival in China |

| 5 | Lufax | 9.6 | March 2015 | Internet finance, one of the largest peer-to-peer (P2P) online lenders |

| 6 | DJI Innovations | 8.0 | May 2015 | The world's largest consumer drone maker by revenue |

| 7 | Zhong An Online | 8.0 | June 2015 | China's first online-only insurer |

| 8 | Meizu | 6.0 | February 2015 | Smartphone and internet service company backed by Alibaba |

| 9 | LeTV Mobile | 5.5 | November 2015 | Smartphone unit of LeTV, the internet and video conglomerate |

| 10 | Ele.me | 3.0 | August 2015 | Online food delivery service for universities, offices and others |

(Data Sources: Disclosures from fund-raising rounds; Approximate valuations)

Therefore, the innovation happening in the Chinese market is of strategic value to the leading tech firms in Silicon Valley as well as the global tech industry. Backed by the emerging ecosystem of entrepreneurship in China, Chinese tech and internet firms are very likely going to become a source of unique features, products and business models. There are also opportunities to cultivate cross-pollinated innovations between China and Silicon Valley, as well as other centers of entrepreneurial excellence. The story of China is rapidly transforming from the old “Made in China” to the new “Innovated in China”.