Solar Grid Parity and its Impact on the Grid

Abstract

Market forces, rather than subsidies, will drive a much more diverse mix of PV-based prosumers. Further cost reductions for PV and its urban locational flexibility means its spread to commercial and industrial usages is likely to be particularly rapid, as it will be for urban fringe and remote rural regions where grid connection is uneconomic. For many prosumers in the commercial sector reliance on the grid will be limited, as daylight PV power generation matches power demand. However as renewables reach a critical proportion of energy generation, concentrated solar power or other solutions will be needed for system reliability. In the long run the uptake of corporate prosumers will be an increasingly important variable in grid management as will purchasing power agreements with utilities.

Keywords

1. Introduction

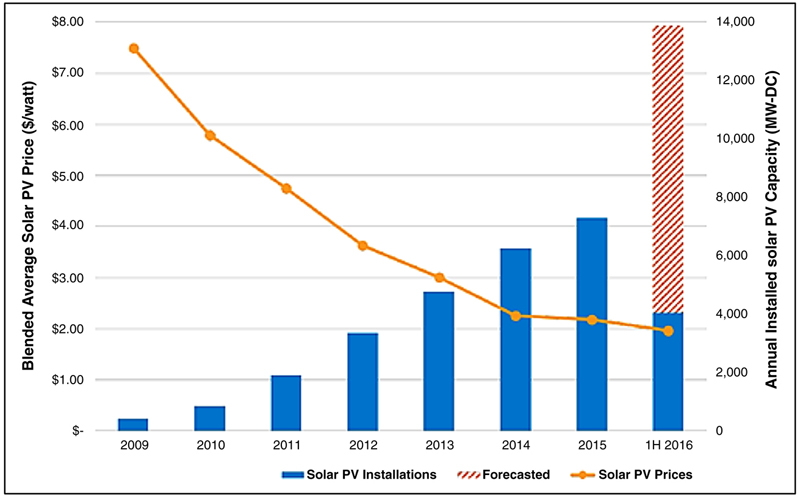

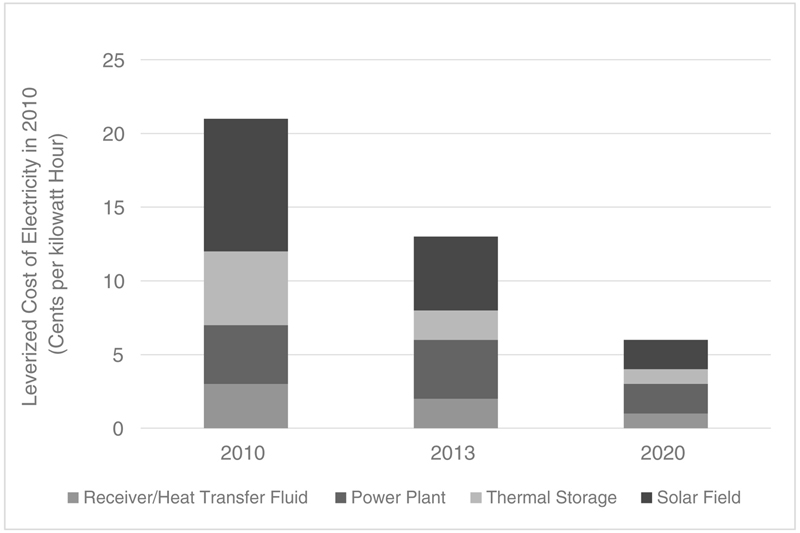

2. The solar energy cost watershed

Table 19.1

Levelized Cost Of Electricity (LCOE) Estimates for Selected Generation Technologies (C/kWh)

| Item | California (C/kWh) | Massachusetts (C/kWh) |

| Utility-scale PV | 10.5 | 15.8 |

| Residential-scale PV | 19.2 | 28.7 |

| Utility-scale CSP | 14.1 | 33.1 |

| Average over 22 US regions | Maximum (C/kWh) | Minimum (C/kWh) |

| Utility-scale PV | 10.1 | 20.1 |

| Utility-scale CSP | 17.7 | 38.8 |

| Onshore wind | 7.1 | 9.0 |

| Gas combined cycle | 6.1 | 7.6 |

| Conventional coal | 8.7 | 11.4 |

| Conventional gas turbine | 10.6 | 14.9 |

Source: MIT Energy Initiative (2015) and Energy Information Agency (2014).

Note: Numbers are current cost estimates for specified locations in Southern California and Central Massachusetts. The EIA numbers are maximum and minimum 2019 costs across 22 US regions. CSP, Concentrated solar power; PV, photovoltaic.

2.1. Solar Energy Grid Parity

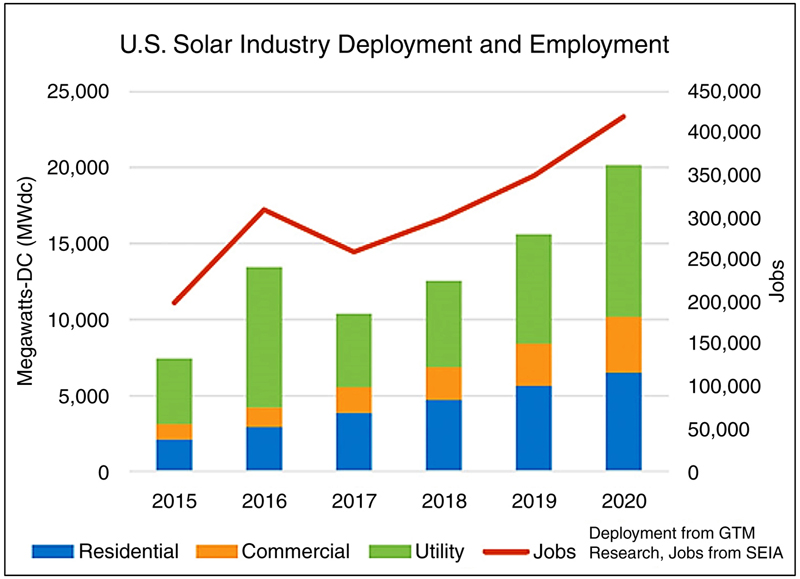

2.2. Drivers of Solar Power Uptake: USA and Australia

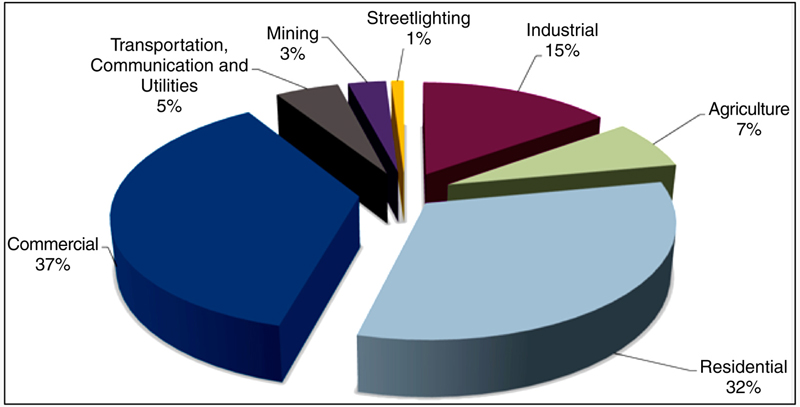

Note: The left to right order of the legend for power-use sectors is replicated in the figure’s bar charts from bottom to top. (Source: Solar Energy Industries Association/Gtm Research (2016).)

3. The rise of distributed commercial/solar

4. The shaping of PPAs by PV uptake

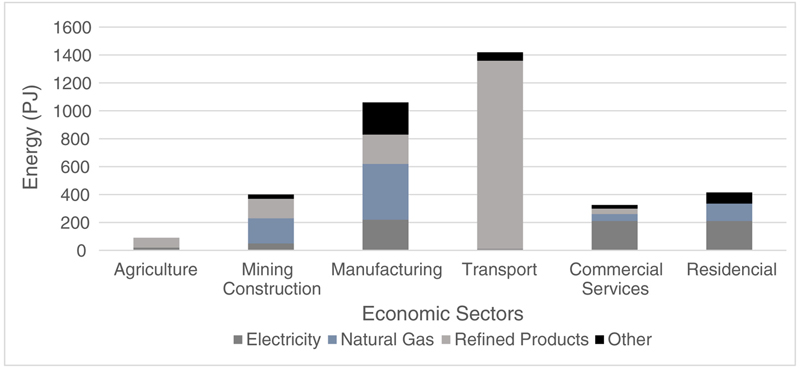

5. Commercial solar uptake: Australia

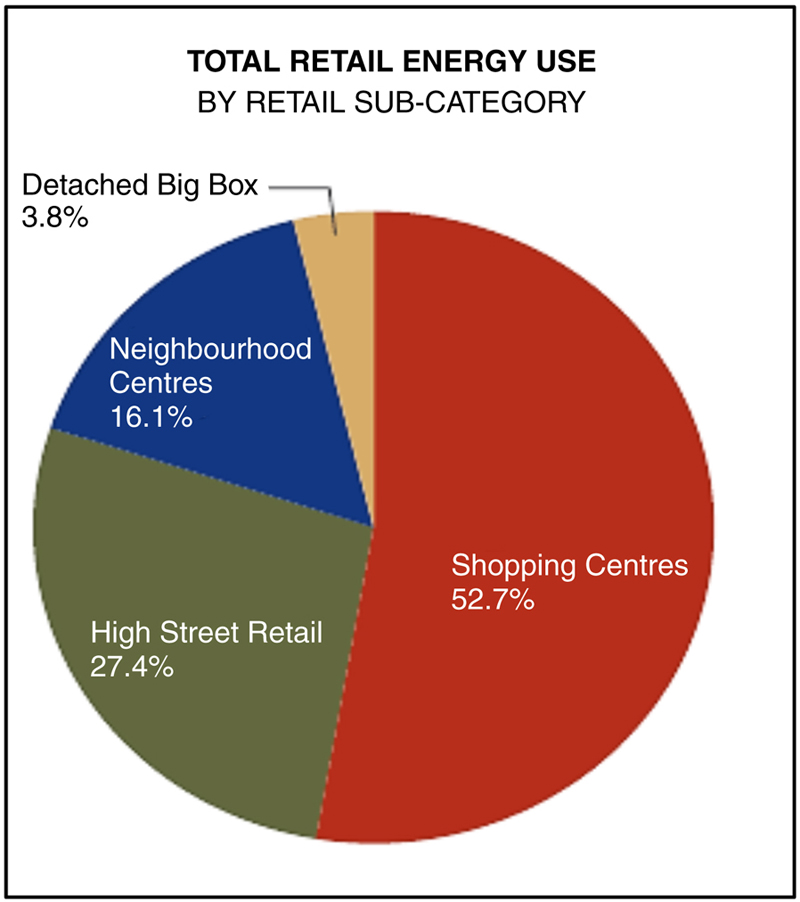

Note: The left to right order of the types of energy listed in the figure’s legend are replicated on chart’s bars from bottom to top. (Source: Zero Carbon Australia Buildings Plan (2013).)

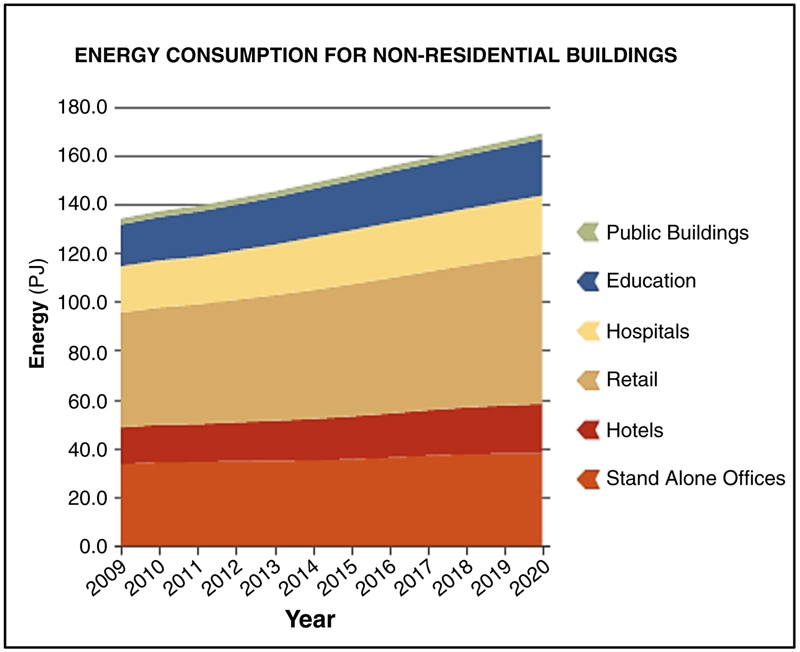

Note: The bottom to top order of the figure’s legend showing building types is replicated in the figure’s levels from the bottom up. (Source: Zero Carbon Australia Buildings Plan (2013).)

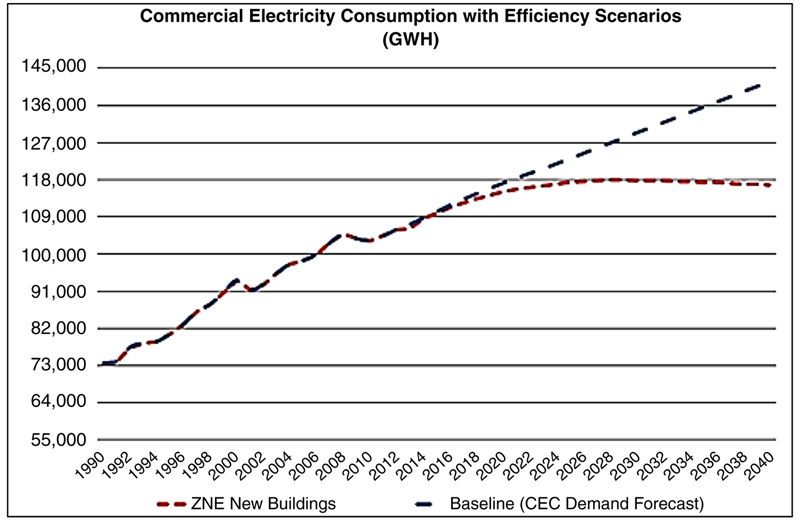

6. Commercial PV uptake: California

Note: This represents an approximate assessment of the effect of ZNE for all projected future new construction, which is projected to require some six new 500-MW power plants to meet load. (Source: Fogel (2015).)

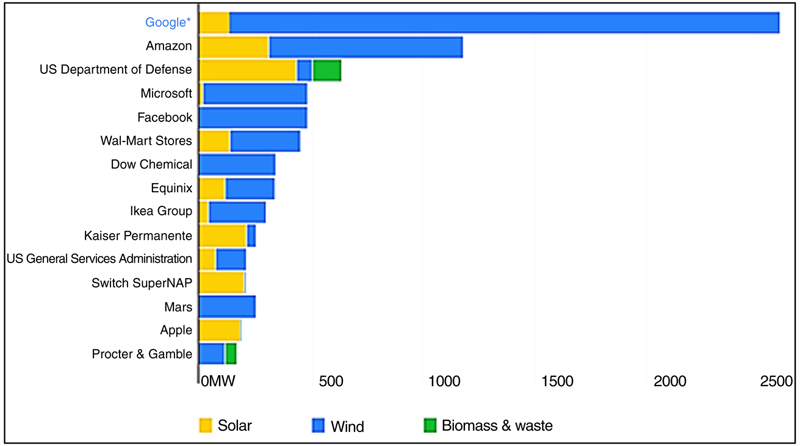

7. Financing and management of large-scale corporate uptake of PV solar

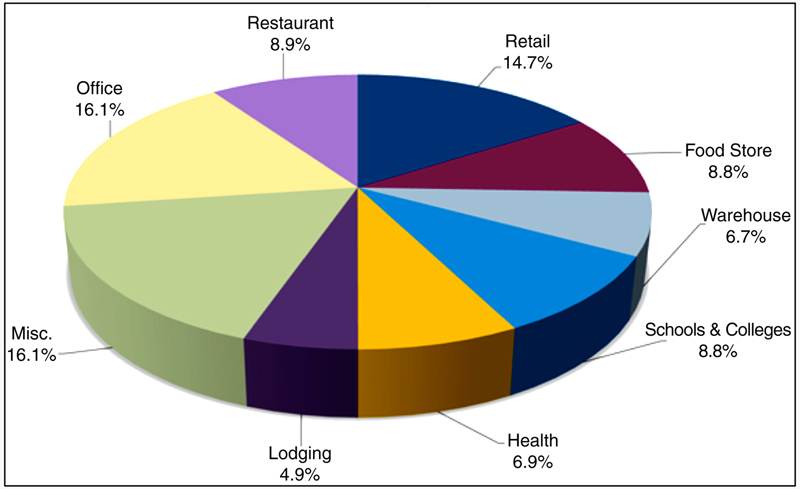

Note: The left to right order of the figure’s legend listing power sources is replicated in the figure’s bars from left to right. Biomass and waste are represented by the bar’s third segment for the US Department of Defense and Proctor and Gamble. (Source: Bloomberg New Energy Finance (2015).)

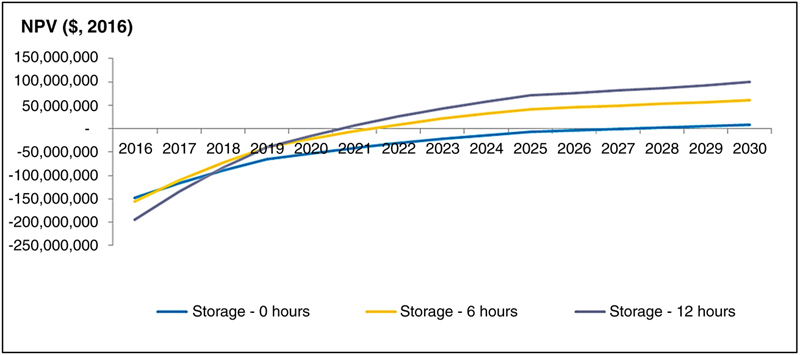

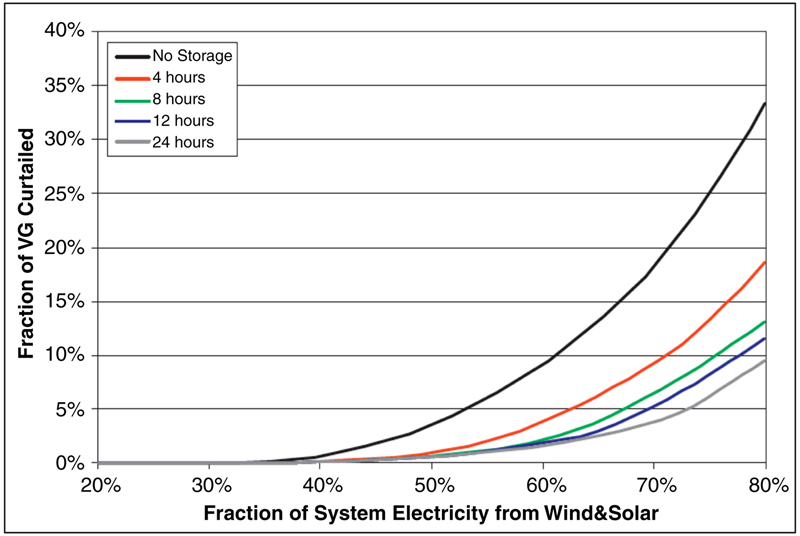

8. The future of a PV/wind-dominated power supply

Note: The left to right order of the legend’s listing of different types of power generation systems are replicated on chart’s bars from bottom to top. (Source: US Department of Energy (2016).)

Note: The legend’s top to down order for storage hours is replicated in the same order by trend lines on the figure from left to right. (Source: Denholm and Hand (2011).)

9. Community-based microgrids