| 11 | Distribution |

Music distributors are a vital conduit in getting physical music product from record labels’ creative hands into the brick-and-mortar retail environment. Recognize that as the marketplace shifts to a digital environment, distribution companies are re-evaluating their value in the food chain and continually developing sales models that reflect direct sales opportunities to music consumers. Whatever the sales channel, distribution companies think of themselves as extensions of the record labels that they represent.

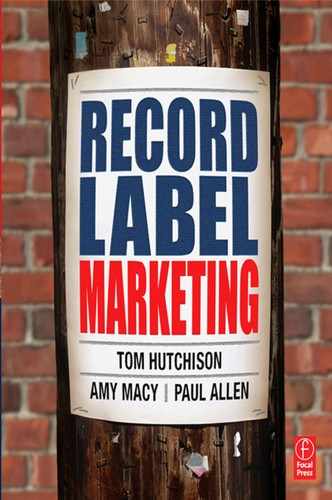

Prior to the current business model, most individual records labels hired their own sales and distribution teams, with sales representatives calling on individual stores to sell music. It took many reps to cover retail, as Figure 11.1 shows. This model shows nine points of contact, where each label meets with each retailer. As retailers became chains, and as economics of the business evolved, record labels combined sales and distribution forces to take advantage of economies of scale, which eventually evolved into the current business model.

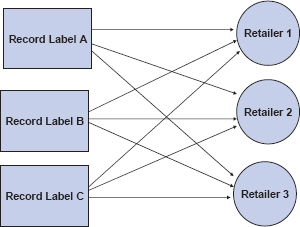

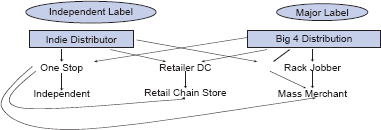

Figure 11.2 includes the distribution function, and shows the points of contact reduced to six. In today’s business model, record label sales executives communicate with distribution as their primary conduit to the marketplace, but labels also have ongoing relationships with retailers. Depending on the importance of the retailer, the label rep will often visit the retailer with their distribution partner so that significant releases and marketing plans can be communicated directly from the label to the retailer. And as deals are struck, both orders and marketing plans can then be implemented by the distributor.

![]() Figure 11.1 Direct contact concept

Figure 11.1 Direct contact concept

![]() Figure 11.2 Distribution-centered concept

Figure 11.2 Distribution-centered concept

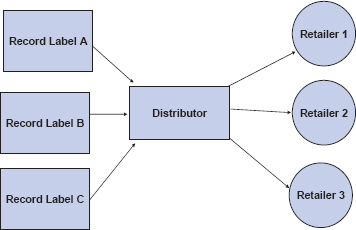

Three out of the Big 4 conglomerates (major labels) share profit centers that are vertically integrated, creating efficiencies in producing product for the marketplace. To take full advantage of being vertically integrated, labels looking for songs would tap their “owned” publishing company. (Each of the major labels has a publishing company. If they only recorded songs that were published by their sister company, more of the money would stay in-house.) Once recorded, the records would be manufactured at the “owned” plant. In-turn, the pressed CDs would then be sold and distributed into retail—with the money being “paid” for each of the functions staying within the family of the music conglomerate.

![]() Figure 11.3 Vertical integration of conglomerates

Figure 11.3 Vertical integration of conglomerates

![]() Figure 11.4 The distribution pathway

Figure 11.4 The distribution pathway

In addition to the Big 4 companies, there are many independent music distributors that are contracted by independent labels to do the same job. Ideally, the distribution function is not only to place music into retailers, but also to assist in the sell-through of the product throughout its lifecycle.

Once in the distributor’s hands, music is then marketed and sold into retail. Varying retailers acquire their music from different sources. Most mass merchants are serviced by rack jobbers, who maintain the store’s music department including inventory management, as well as marketing of music to consumers. Retail chain stores are usually their own buying entities, with company-managed purchasing offices and distribution centers. Many independent music stores are not large enough to open an account directly with the many distributors, but instead work from a one-stop’s inventory as if it were their own. (One-stops are wholesalers who carry releases by a variety of labels for smaller retailers who, for one reason or another, do not deal directly with the major distributors.) Know that retail chain stores and mass merchants will on occasion use one-stops to do “fill-in” business, which is when a store runs out of a specific title and the one-stop supplies that inventory. (Retail is discussed in detail in another chapter.)

Most distribution companies have three primary roles: The sale of the music, the physical distribution of the music, and the marketing of the music. Reflecting the marketplace, most distribution companies have similar business structures to that of their customers—the retailers. Often times, the national staff is separated into two divisions: Sales and marketing. The sales division is responsible for assisting labels in setting sales goals, determining and setting deal information, and soliciting and taking orders of the product from retail. Additionally, the sales administration department should provide and analyze sales data and trends, and readily share this information with the labels that they distribute.

The marketing division assists labels in the implementation of artists’ marketing plans along with adding synergistic components that will enhance sales. For instance, the marketing plan for a holiday release may include a contest at the store level. Distribution marketing personnel would be charged with implementing this sort of activity. But the distribution company may be selling holiday releases from other labels that they represent. The distribution company may create a holiday product display that would feature all the records that fit the theme, adding to the exposure of the individual title.

The physical warehousing of a music product is a huge job. The major conglomerates have very sophisticated inventory management systems where music and its related products are stored. Once a retailer has placed an order, it is the distributor’s job to pick, pack, and ship this product to its designated location. These sophisticated systems are automated so that manual picking of product is reduced, and that accuracy of the order placed is enhanced. Shipping is usually managed through third-party transportation companies.

As retailers manage their inventories, they can return music product for a credit. This process is tedious, not only making sure that the retailer receives accurate credit for product returned, but the music itself has to be retrofitted by removing stickers and price tags of the retailer, re-shrink wrapping, and then returning into inventory.

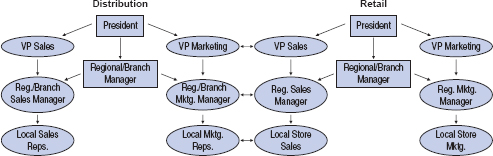

Conglomerate distribution company structure as it relates to national retail accounts

Although there are many variations and nuances to these structures as determined by each distribution company, the basic communication chart applies. At each level, the companies are communicating with each other. At the national level, very complex business transactions are being discussed, including terms of business as well as national sales and marketing strategies that would affect both entities company-wide. As mandated by the national staff, the regional/branch level is to formulate marketing strategies, either as extensions of label/artist plans, or that of a distribution focus. At the local level, implementation of all these plans is the spotlight. But by design, these business structures are in place to create the best possible communication at every level, with an eye on maximizing sales.

![]() Figure 11.5 Conglomerate distribution company structure

Figure 11.5 Conglomerate distribution company structure

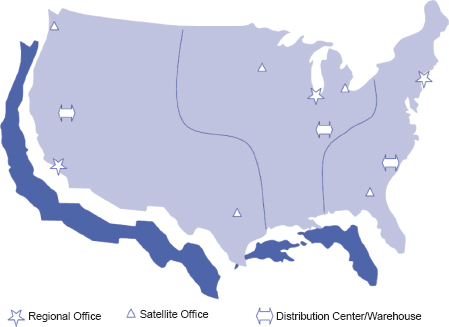

To optimize communication along with service, distributors need to be close to retailers. Many of the major conglomerates have structured their companies nationally to accommodate the service element of their business. Most distributors have regional territories of management containing core offices and distribution centers. Each region contains satellite offices, getting one step closer to actual retail stores. As reflected in the structure chart in Figure 11.6, field personnel are on the front line, reporting to satellite offices, who then report to the regional core offices.

This map shows basic regions for a major distributor with satellite offices and distribution centers (DC). Core regional offices are located in Los Angeles,Chicago, and New York. Regions are naturally eastern, central, and western, with regional offices including Atlanta, Detroit, Minneapolis, Dallas, and Seattle. The distribution centers are centrally located within each region. In this example, the DCs are located in Sparks, NV, Indianapolis, IN, and Duncan, SC. No destination is more than a two-day drive from the DC, making product delivery timely.

![]() Figure 11.6 U.S. map of distributor locations

Figure 11.6 U.S. map of distributor locations

Although the core regional offices are centrally located, these offices are primarily marketing teams, executing plans derived by both the labels that they represent and the distribution company. To be clear, over 80% of the music business is purchased and sold through ten retailers. The locations of these buying offices are key sales sites, and designated distribution personnel are placed near these retailers so that daily, personal interaction can occur. These locations and retailers are shown in Table 11.1.

Bentonville, AR |

Wal-Mart |

Minneapolis |

Best Buy, Target, and Musicland |

Detroit |

Kmart |

Albany |

Transworld |

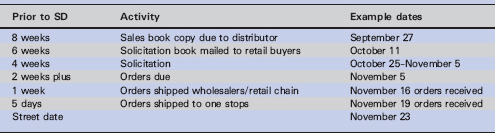

The communication regarding a new release begins months prior to the street date. Although there are varying deadlines within each distribution company, the ideal timeline is pivotal on the actual street date of a specific release. For most releases, street dates occur on Tuesdays. Working backwards in time, to have product on the shelves by a specific Tuesday, product has to ship to retailer’s distribution centers approximately one week prior to street date. To process the orders generated by retail, distributors need the orders one week prior to shipping. The sales process of specific titles occurs during a period called solicitation. All titles streeting on a particular date are placed in a solicitation book, where details of the release are described. The solicitation page, also known as Sales Book Copy, usually includes the following information:

![]() Artist/Title

Artist/Title

![]() Street Date

Street Date

![]() File under category—where to place record in the store

File under category—where to place record in the store

![]() Information/History regarding the artist and release

Information/History regarding the artist and release

![]() Single(s) and radio promotion plan

Single(s) and radio promotion plan

![]() Video(s) and video promotion plan

Video(s) and video promotion plan

![]() Internet Marketing

Internet Marketing

![]() Publicity Activities

Publicity Activities

![]() Consumer Advertising

Consumer Advertising

![]() Tour and Promotional Dates

Tour and Promotional Dates

![]() Available POP

Available POP

![]() Bar Code

Bar Code

This information is also available online on the business-to-business (B2B) sites established for the retail buyers.

Table 11.2 shows the actual timeline for labels to be included in the solicitation process.

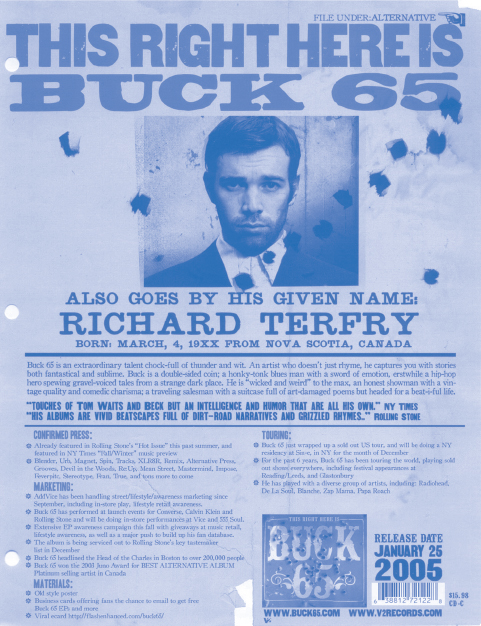

One sheet – the solicitation page

On the website, MusicDish Industry e-journal, Christopher Knab of ForeFront Media and Music describes a one sheet as:

“A Distributor One Sheet is a marketing document created by a record label to summarize, in marketing terms, the credentials of an artist or band. The One Sheet also summarizes the promotion and marketing plans and sales tactics that the label has developed to sell the record. It includes interesting facts about an act’s fan base and target audience. The label uses it to help convince a distributor to carry and promote a new release” (Knab, C., 2001).

The one sheet typically includes the album logo and artwork, a description of the market, street date, contact info, track listings, accomplishments, and marketing points. The one sheet is designed to pitch to buyers at retail and distribution. The product bar code is also included to assist in the buy-plugging the actual release into the inventory code system.

![]() Figure 11.7 One sheet for Buck 65 (Source: V2 Records)

Figure 11.7 One sheet for Buck 65 (Source: V2 Records)

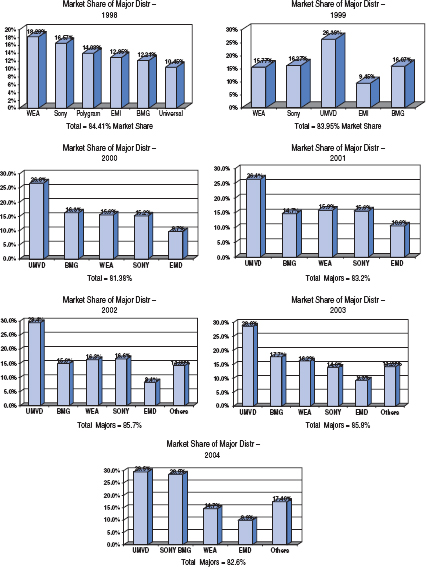

Consolidation and market share

As consolidation continues, the Big 4 just keep getting bigger. Looking at market share data generated by over-the-counter sales of SoundScan, one can view how large these entities have become over time. Note that the piece of the Big 4 pie fluctuates, with independents representing the remaining market share.

![]() Figure 11.8 Market share of major distributors (Data Source: Nielsen SoundScan)

Figure 11.8 Market share of major distributors (Data Source: Nielsen SoundScan)

Since over 90% of music is still purchased through brick-and-mortar stores, the primary function for music distributors continues to be that of physical distribution of CDs into physical stores. But to reflect the burgeoning downloading trends, most of the major distributors have sites where consumers can buy tracks and albums directly from the conglomerate. These sites usually promote and sell music from their represented labels only, which makes it difficult for consumers to experience one-stop shopping.

In-turn, within most conglomerate families resides a department that licenses music to third-parties, which are legal downloading sites such as iTunes® and Napster™. These licensing departments are critical to the future of distribution, positioning them as gatekeepers for the growing downloading environment. At these third-party sites, consumers can purchase from the many sources of music, clearly beyond that of one conglomerate. Currently, the wholesale price of a digital track is approximately $0.68 a license.

Revenues from a 99-cent download

As consumership of music continues to evolve, so does that of distribution of music. Current trends reveal that younger consumers look to purchase tracks, making the classic album less attractive to this buyer. The digital download arena is where these consumers are satiating their needs. And yet, 90% of music is still purchased in the classic brick-and-mortar environment, making the need for physical distribution a continuing viable business entity.

|

Table 11.3 Revenues from a 99-cent download |

|

Participant |

Revenue |

Label |

47 cents |

Distribution affiliate |

10 cents |

Artist |

7 cents |

Producer |

3 cents |

Music publisher |

8 cents |

Service provider |

17 cents |

Credit card fees |

5 cents |

Bandwidth costs |

2 cents |

|

99 cents |

Source: Brian Garrity. |

|

Several distribution companies are exploring ways to add value to the conglomerate equation. Creating distribution-specific marketing campaigns with nonentertainment product lines helps validate distribution’s existence, while hopefully enhancing the bottom line. Marketing efforts such as on-pack CDs with cereal, greeting card promotions, and ringtone services add to the branding of the participating artists, while increasing overall revenue through licensing and/or sales of primary items.

The ultimate value for today’s distribution companies is that of consolidator. Distributors can consolidate labels to create leverage points within retail. To gain positioning in the retail environment, one must have marketing muscle, and by using the collective power of the label’s talent, the entire company can raise its market share by coattailing on the larger releases in the family.

Big 4 – These are the four music conglomerates that maintain a collective 85% market share of record sales. They are Universal, Sony/BMG, Warner, and EMI.

Economies of scale – Producing in large volume often generates economies of scale—the per-unit cost of something goes down with volume. Fixed-costs are spread over more units lowering the average cost per unit and offering a competitive price and margin advantage.

Fill-in – One-stop music distributors supply product to mass merchants and retailers who have run out of a specific title by “filling in” the hole of inventory for that release.

Mass merchants – Very large retail chains that sell a variety of goods and depend on volume sales. Wal-Mart and Target are examples.

One stop – A wholesaler who carries releases by a variety of labels for sale to small retail stores.

Rack jobbers – Companies that supply records, compact discs and other items to department stores, discount chains and other outlets and service (rack) their record departments with the right music mix.

Sales Book – Distribution companies compile all their releases for a specific street date into a “sales book,” which contains one-sheets for each title that outlines the marketing efforts.

Sell-through – Once a title has been released, labels and distributors want to minimize returns and “sell-through” as much inventory as possible.

Solicitation period – The sales process of specific titles occurs during a period called solicitation. All titles streeting on a particular date are placed in a solicitation book, where details of the release are described.

Vertical integration – The expansion of a business by acquiring or developing businesses engaged in earlier or later stages of marketing a product.

Bibliography

Knab, C. (2001). http://www.musicdish.com/mag/index.php3?id=3357. The distributor one sheet. (3–25–2001).

Weatherson, Jim, President of Ventura Distribution and former Executive Vice President of Universal Music Distribution, from personal interview, July 2004.

Garrity, Brian. “Seeking Profits at 99 ¢”, Billboard, July 12, 2003.