| 5 | The Profit and Loss Statement |

Profitability … or the lack thereof!

Record companies use profit and loss (P&L) statements to both predict the success of a record prior to its release as well as analyze a project as it nears the end of its lifecycle. To understand the “math,” let’s look at all the components of a P&L, recognizing the financial significance of every line item.

SRLP …suggested retail list price

The suggested retail list price (SRLP) is set by the record label and is based on cost of the recording project, the artist’s status, genre of music, competitive landscape, and what the market will bear. Although the royalty models are changing, many labels still pay artist royalties based on the SRLP. The SRLP has a correlating wholesale price, which is usually structured by the distribution company.

This line item is the wholesale price. The card price is the dollar figure that is set by the distribution company that sells the product. For fair trade practices, wholesale card prices are published entities that are the basis of further financial negotiations between seller and buyer. The chapter on retail shows an actual published rate card of wholesale prices.

Music product regularly receives a discount, which is set by the label and is administered via the distributor. (In some situations, it can be specified by the artist’s contract.) In mainstream music, the discount is applied to the wholesale price. In some genres of music such as Christian music, discounts are applied to the retail price, and negotiations are then based on retail prices. But the majority of music is sold on wholesale pricing strategies.

Discounts are based on many variables. If a label has a really hot artist that is a big seller, and demand at the consumer level is high, a discount may not be offered, since most retailers will buy the product at full price. To entice retailers to purchase a new artist, record labels will offer discounts, which will increase the margin and profitability at the store level. Fair trade practices require that labels and their distributors offer the same discount on the same release to all retail purchasers. But the discount can be changed based on the marketing elements that the retailer may offer.

For example, a label has a new artist and is offering a 5% discount. This discount will increase the potential profitability of the retailer. If the retailer agrees to include this new artist on a “new artist” end cap for an additional 5%, then the discount will be increased to 10%, adding to the potential profitability of the retailer.

Gross sales refers to the wholesale price (value) of the product with the reduction of the discount included. It usually reflects the number of records shipped minus returns. Remember that music retailing is basically a consignment business and that stores can return product back to the distributor and label and receive a credit for this unsold product.

Depending on the relationship between the label and distributor, the distribution fee is based on sales after the discount. Meaning, it is in the distributor’s best interest to keep discounts as low as possible to help increase their profitability. This fee is a percentage of sales and varies greatly by the distributor. The conglomerates that own both the labels and distributor often charge between 14%–16%. Independent distributors structure deals with indie labels and artists that range between 18%–30%, depending on the services being offered.

Once again, the gross sales figure is determined on shipped minus returned product, being NET. Net units are multiplied by the per unit price, after discounts and distribution fees are deducted.

The industry averages about 20% returns, meaning that for every 100 records in the marketplace, 20 will be returned. To protect their business, record labels insure against returns by “reserving” a percentage of sales. Record labels “reserve” 20% of sales by pocketing these funds in an escrow account. Not until the life of the record has run the majority of its cycle will the reserve be adjusted. In some cases, a record may only have a 5% return in its lifecycle. The record company will then adjust the profitability statement to reflect such a low return, and royalties will then be distributed. In other cases, a record may have a 30% return, which adversely affects the company’s overall profitability, since they expected they had sold 10% more of a particular release then previously accounted.

Net sales after return reserve

Basically, net sales after return reserve is the computed net sales minus the 20% reserve deduction.

Labels incur returns on records shipped into the marketplace. For accounting purposes, the profit and loss statement reflects these returns within the overall equation. The returns reserve line item is usually computed at the end of the lifecycle of the release. A label will calculate what actual returns occurred and plug this adjusted number into the P&L, determining the ultimate profitability of the project. But labels will use P&Ls as predictor equations to determine potential profitability of a future project and will plug return reserve standard into the overall equation, helping to evaluate a project’s future.

The total net sales is the adjusted sales number deducting discounts, distribution fees, and returns.

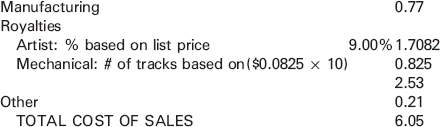

The cost of sales are costs associated with making the actual product, including the pressing of the disc, printing of paper inserts, marketing stickers on the outside of the product, all-in royalties and mechanical royalties, and inventory obsolescence. In accounting terms, these are the variable costs since the amount varies based on the number of units produced.

Many of these costs are negotiable, such as the mechanical rate. Labels often receive a reduced mechanical rate on artists that are also the songwriter. Older songs as well as reissued material can often receive lower mechanical rates based on the age and inactivity of the copyrights.

Dealing with the inventory of product that does not sell into the marketplace costs money. So, labels build into the cost of goods an amount that will fund the management of an obsolete inventory. It takes manpower and resources to “scrap” a pile of CDs. This includes moving the inventory off the warehouse floor, pulling the inserts and CDs from the jewel cases (which are recycled for new releases), and breaking/melting the actual CDs into pellets, which can then be used to make new CDs.

Gross margin before recording costs

Gross Margin Before Recording Costs deducts the cost of sales from the total net sales.

Know that the recording costs are initially funded by the record label. But built into most artist contracts, recording costs are recoupable, meaning that once the release starts to make money, the record company will pay itself back prior to the artist receiving royalties.

Also included in recording costs are advances. Advances are monies fronted to the artist to assist them with living expenses. It takes time to record a record, which doesn’t allow an artist to make money elsewhere. Advances are recoupable.

Gross margin reflects gross sales minus discounts, distribution fees, returns, cost of sales, and recording costs. These are revenues made prior to marketing expenses.

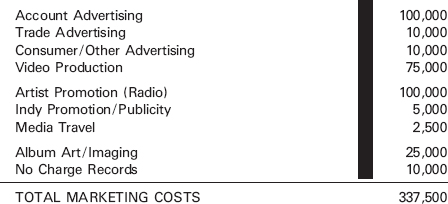

To launch an artist’s career in today’s climate, it takes a lot of money. How a company manages its marketing costs can determine the success of an album … and artist. Beyond the making of the record, marketing costs include the imaging of an artist, advertising at both trade and consumer publications, publicity, radio promotion, and usually the most expensive element of marketing is retail positioning in the stores.

Even in today’s business model, one of the most expensive marketing costs—ranking right up there with radio promotion and video—is the positioning of a record in the retail environment, known as co-op advertising. In the grocery business, this is called a slotting allowance. Ever notice that premium, name-brand items are placed in the most prominent positions within a grocery store? The same occurs in record retail. The pricing and positioning (P&P) of a record, meaning a “sale” or reduced price along with prime real estate placement in-store, can cost record labels hundreds of thousands of dollars.

Other types of account advertising include print advertising via the store’s Sunday circulars, end-cap positioning, listening stations, event marketing such as artist in-store visits, point of purchase materials placement guarantees, and more. Chapter 12 discusses the many aspects of the retail environment.

Most schools of advertising include a lesson on internal versus external advertising. Trade advertising is considered an internal promotional activity.

Trade advertising creates awareness of a new product to the decision makers of that industry by using strong imaging of the artist and release along with relevant facts such as sales and radio success, tour information, sales data, and upcoming press events.

In the record business, decision makers include music buyers for retail stores, radio stations and their programmers, talent bookers for television shows, reviewers for newspaper and consumer magazines, and talent buyers for venues. Some prominent trade magazines for the music industry include Billboard, R&R, Amusement Business, Pollstar, and Variety, to name a few.

Consumer advertising is considered external advertising since it is targeting the “end consumer.” Consumer advertising also creates awareness, but to end consumers who will purchase music. This advertising can include artist album art with imaging via print, but the actual product can be “heard” via broadcast advertising, alerting consumers as to a new release now available for purchase.

Negotiated into the recording contract, artists are usually responsible for 50% of the cost of video production. Although the record company will fund the video shoot, the record company will expect to receive recoupable pay of 50% of the overall costs from record sales, and 100% recoupable from video/DVD sales.

This line item usually covers the costs associated with introducing and promoting the artist to radio. Still a primary source for learning about new music, labels often take artists to visit with radio stations, including on-air interviews, dinners with music programmers, and Listener Appreciation events. The record company incurs this cost and it is usually not recoupable.

Independent promotion and publicity

Depending on the artist’s stature and current competitive climate, record companies will hire the services of independent promotion companies and independent publicists. In addition to the label’s efforts, these independent agents should enhance the label’s strategy by assisting in creating exposure for their artists via additional radio airplay and media. This line item is not recoupable.

Record labels will fund the costs associated with travel for an artist who is doing a media event. Media travel is usually an isolated event where an artist is doing a television talk show or an awards event. Again, an expense to the label and not recoupable.

The imaging of an artist can take time … and money. Most artists receive some type of grooming, if not just a polishing of what the artist already represents. Professionals trained at artist imaging are hired to create a “look” that is unique and defining. Such professionals as hair and make-up artists, clothing specialists, even movement/dance professionals are often required to give an artist a specific shine. As a part of the team, photographers are hired to shoot cover artwork as well as press images for publicity use. And then a designer is hired to create the overall album art concept, from artist image use, album title treatment, booklet layout, and so forth. All of these efforts are expenses to the label and not usually recoupable.

A marketing tool often used by labels is the actual CD. No charge records are those CDs that are used for promotional use such as giveaways on the radio, or in-store play copies for record retailers. The value of these records and their use must be accounted for, and are not recoupable.

From the gross margin, a label would subtract the marketing costs including account advertising, trade and consumer advertising, video production, artist promotion, independent promotion and publicity, media travel, album art, and no charge records to determine the release’s contribution to a record company’s overhead.

Note the percentages given within the spreadsheet. The total net sales percentage reflects 100% of money generated by the sale of the project. Each line item subheading also reflects a percentage, causing each department to consider how much is being spent as a reflection of the project as a whole. Although the contribution to overhead may be a large number, its percentage of the whole determines how effective and efficient the project was managed.

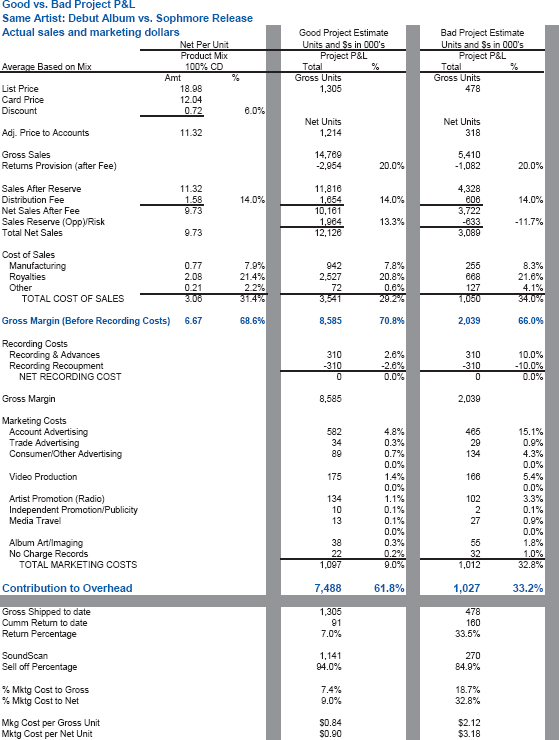

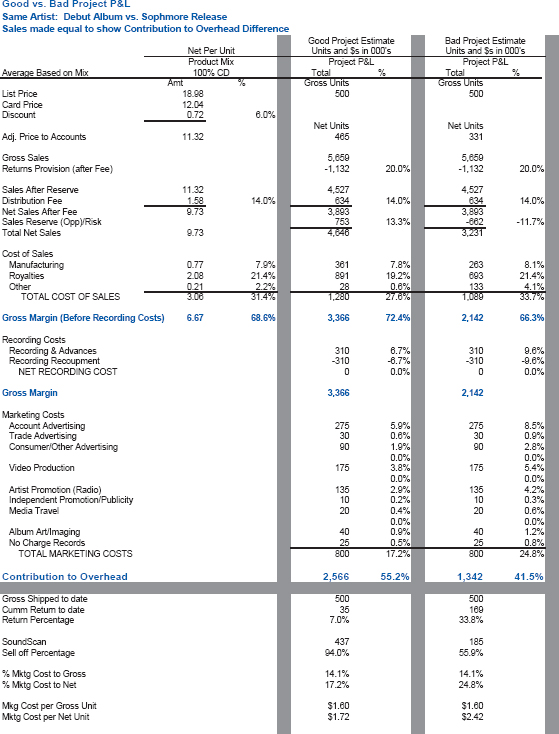

Contribution to overhead: example of two different projects

Example:

Looking at the numbers, Project B made more money for the company, but as for efficiency, Project A was a more effective release since the company did a better job at managing its expenses.

Ways at looking at project efficiency and effectiveness

Record labels look at the “numbers” in many ways to determine how well they are performing. By “spinning” these figures, a company should analyze where spending is less effective, thus causing the overall project to be less profitable.

Gross Ships — Cumulative Returns = Net Shipment

Cumulative Returns/Gross Ships = Return Percentage

Example:

500,000 units — 35,000 returns = 465,000 units Net Shipment

35,000 units / 500,000 units = 7% return

Again, industry standards reflect an approximate 20% return percentage. Generally, a record that returns more than 20% is not performing at the market average. A couple of decisions could have affected this percentage. The record company over-sold the project and caused the returns, or the record company did not promote and have a hit with the project, thus causing returns. In any case, the record company needs to determine what occurred to ensure that it doesn’t happen again.

If a project under performs a market dramatically, such as a lifetime return average of 5%, the project could be considered a great success, minimizing return costs as well as manufacturing costs. But the company should also be sensitive to the fact that they may have undersold the project, thus not realizing the full sales potential of the project too. Again, further analysis is vital to the overall success of future projects and the company.

SoundScan is an information system that tracks sales of music and music video products throughout the United States and Canada. Sales data using UPC bar codes from point-of-sale cash registers is collected weekly from over 19,000 retail, mass merchant and non-traditional (on-line stores, venues, and so on etc.) outlets. Weekly data is compiled and made available every Wednesday. Now branded with the Nielsen name, SoundScan is the sales source for the Billboard music charts, major newspaper, magazine, TV, MTV and VH1 charts. Chapter 6 is dedicated to SoundScan, its analysis and impact on the industry.

To evaluate inventory, record companies can use a simple equation to know how many units remain in the marketplace:

Net Shipments — SoundScan Sales = Remaining Inventory

SoundScan Sales/Net Shipments = Sell Off Percentage

Example:

465,000 Net Ships – 437,000 units SoundScanned = 28,000 units

437,000 SoundScan/465,000 Net Ships = 94% Sell Off

If this project is a steady seller, quietly moving units every week, a record company could use SoundScan weekly sales to determine how many weeks of inventory are left in the marketplace. If this project sold 2,000 each week:

28,000 remaining inventory/2,000 SoundScan each week = 14 weeks of inventory left

Knowing inventory levels and keeping aware of sales is critical to the success of a project. A record company does not want to run out of records, which is called can’t fill. If it’s not on the retailer’s shelves, it cannot be purchased.

Isolating marketing costs and analyzing their effectiveness in selling records is best reflected in the following equations:

Percentage of Marketing Cost to Gross: Marketing Costs/Gross Sales × 100 = %

Percentage of Marketing Cost to Net: Marketing Costs/Net Sales × 100 = %

Example:

$800,000 Marketing Costs/$4,238,000 Gross Sales = 18.9%

$800,000 Marketing Costs/$3,402,000 Net Sales = 23.5%

The lower the percentage reflects, the better performing project. Keeping marketing costs in check and knowing when to stop “fueling the fire” is usually a great determiner of seasoned record labels.

Marketing Costs per Gross Unit:

Marketing Costs/Gross Shipments = Cost per unit

Marketing Costs per Net Unit:

Marketing Costs/Net Shipments = Cost per unit

Example:

$800,000/500,000 units Gross Shipped = $1.60

$800,000/465,000 units Net Shipped = $1.72

In all of these equations, the “real” picture is best drawn when using Net Shipments, since that is the ultimate number of units in the marketplace.

Record companies can use the profit and loss statement as a predictor of success. Often, labels will “run the numbers” to see how profitable, or not, a potential release could be. By using the spreadsheet and plugging in forecasted numbers, including shipments, cost of sales, recording costs (or the acquisition of a master), and marketing costs, the equation will help a label evaluate and determine whether a project is worth releasing.

Small considerations can dramatically affect the contribution to overhead. List price, discounts, number of pages in the CD booklet, royalties—both artist and mechanical, and the various marketing line items can either make a project profitable or not.

When does a record “break even” in covering the costs that it took to make the project, and when does it start to turn a profit? Depending on the equation, record companies look at this value in several ways.

Without marketing costs, a number can be derived simply by dividing the total fixed costs by price, using wholesale dollars.

Break-even point

![]()

Break even with costs listed

![]()

Break-even example

Example:

![]()

a (card price of SRLP $18:98) b (based on total cost of sales) c (Distr: Fee)

BE = 75,581 units without marketing costs

Cost of sales

Cost of Sales

Adding marketing costs changes the outcome of the equation dramatically:

A label has to derive predicted/budgeted marketing costs to add to the equation. Most seasoned labels have an idea as to how much each activity may cost to launch a record. Using the following dollars, check-out the break even analysis:

Marketing costs

Marketing Costs

Break-even example with marketing costs

Example:

![]()

a (card price of SRLP $18:98) b (based on total cost of sales) c (Distr: Fee)

Clearly, the job of the profit and loss statement is multifaceted. It can be used as a predictor of success (or not), as well as an evaluation tool of existing projects. Not a part of the equation is the overhead that it takes to operate the business, such as building expenses, salaries, supplies, and so on. But lessons learned from this type of analysis should aid record labels as to the better allocation of funds and resources.

PROFIT AND LOSS STATEMENT

Record companies use Profit and Loss Statements to both predict the success of a record prior to its release as well as analyze a project as it nears the end of its lifecycle. To understand the “math,” let’s look at all the components of a P&L, recognizing the financial significance of every line item.

SRLP – Suggested Retail List Price

This price is set by the record label and is based on artist status, genre of music, competitive landscape, and what the market will bear. The SRLP is the monetary base from which artist royalties are paid, and it sets the wholesale price.

CARD PRICE

This is the wholesale price that is determined by the SRLP. The term “card price” is the dollar figure that is set by the distribution company that sells the product.

STANDARD DISCOUNT

Music product regularly receives a discount, which is set by the label and is administered via the distributor. In mainstream music, the discount is applied to the wholesale price.

GROSS SALES

This term refers to the wholesale price of the product with the reduction of the discount included. Gross sales usually reflect the number of records shipped minus returns. Remember that music retailing is basically a consignment business and that stores can return product back to the distributor and label and receive a credit for this unsold product.

DISTRIBUTION FEE

Depending on the relationship between the label and distributor, this fee is based on sales after the discount. This fee is a percentage of sales and varies greatly on the distributor. The conglomerates that own both the labels and distributor often charge between 14%-16%.

GROSS SALES AFTER FEE

This figure is determined on shipped minus returned product, being NET. Net units are multiplied by the per unit price, after discounts and distribution fees are deducted.

RETURN PROVISION

The industry averages about 20% returns, meaning that for every 100 records in the marketplace, 20 will be returned. To protect their business, record labels insure against returns by “reserving” a percentage of sales–20%–by pocketing these funds in an untouchable account.

NET SALES AFTER RETURN RESERVE

Computed net sales minus the 20% reserve deduction.

RETURNS RESERVE OPP/(RISK)

This item is usually computed at the end of the lifecycle of the release. A label can calculate what actual returns occurred and plug this adjusted number into the P&L, determining the ultimate profitability of the project.

TOTAL NET SALES

Adjusted sales number deducting discounts, distribution fees, and returns.

COST OF SALES

Costs associated with making the actual product, including the pressing of the disc, printing of paper inserts, marketing stickers on the outside of the product, all-in royalties and mechanical royalties, and inventory obsolescence. These are the variable costs–based on the number of units produced.

GROSS MARGIN BEFORE RECORDING COSTS

Subtracting Cost of Sales from the Total Net Sales generates a dollar figure.

RECORDING COSTS

Recording costs are initially funded by the record label. But built into most artist contracts, recording costs are recoupable, meaning that once the release starts to make money, the record company will pay itself back prior to the artist receiving royalties. Also included in recording costs are advances.

GROSS MARGIN

Gross Sales – Discount, Distribution, Returns, Cost of Sales, and Recording Costs. Monies that are made prior to marketing costs.

MARKETING COSTS

Beyond the making of the record, marketing costs include the imaging of an artist, advertising at both trade and consumer publications, publicity, radio promotion, and usually the most expensive element of marketing is retail positioning in the stores.

The most expensive marketing cost is the positioning of a record in the retail environment. The pricing and positioning of a record (P&P), meaning a “sale” or reduced price along with prime real estate placement in store, can cost record labels hundreds of thousands of dollars. Other types of account advertising includes print advertising via the store’s Sunday circulars, end cap positioning, listening stations, event marketing such as artist in-store visits, point of purchase materials placement guarantees, and more.

Advertising

Trade advertising is considered an internal promotional activity. Trade advertising creates awareness of a new product to the decision-makers of that industry by using strong imaging of the artist and release along with relevant facts such a sales and radio success, tour information, sales data, etc.

Video Production

Negotiated into the recording contract, artists are usually responsible for 50% of the cost of video production.

Artist Promotion

Usually covers the costs associated with introducing and promoting the artist to radio. Labels often take artists to visit with radio stations, including on-air interviews, dinners with music programmers, and Listener Appreciation events. The record company incurs this cost and is usually not recoupable.

Independent Promotion and Publicity

Record companies will hire the services of independent promotion companies and independent publicists. They assist in creating exposure for their artists via additional radio airplay and media. This line item is not recoupable.

Media Travel

Record labels will fund the costs associated with travel for an artist who is doing a media event. This is an expense to the label and not recoupable.

Album Art

Photographers are hired shoot cover artwork as well as press images for publicity use. And then a designer is hired to create the overall album art concept, from artist image use, album title treatment, booklet layout, etc. All of these efforts are expenses to the label and not usually recoupable.

No Charge Records

A marketing tool often used by labels is the actual CD. No Charge Records are those CDs that are used for promotional use such as give-aways on the radio, or instore play copies for record retailers. The value of these records and their use must be accounted for, and are not recoupable.

CONTRIBUTION TO OVERHEAD

From the Gross Margin, a label would subtract the marketing costs including Account Advertising, Trade and Consumer Advertising, Video Production, Artist Promotion, Independent Promotion and Publicity, Media Travel, Album Art, and No Charge Records to determine the release’s contribution to record company’s overhead.

Note the percentages given within the spreadsheet. The total net sales percentage reflects 100% of money generated by the sale of the project. Each line item subheading also reflects a percentage, causing each department to consider how much is being spent as a reflection of the project as a whole. Although the Contribution to Overhead may be a large number, its percentage of the whole determines how effective and efficient the project was managed.

![]() Figure 5.1 The profit and loss summary

Figure 5.1 The profit and loss summary

![]() Figure 5.2 Example P&L worksheet: actual sales and marketing dollars

Figure 5.2 Example P&L worksheet: actual sales and marketing dollars

![]() Figure 5.3 Sales made equal to show contribution to overhead difference (return % varies)

Figure 5.3 Sales made equal to show contribution to overhead difference (return % varies)

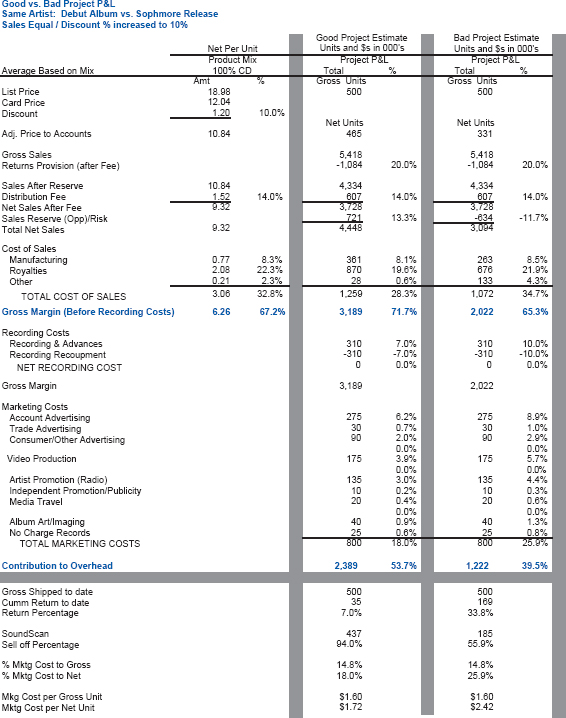

![]() Figure 5.4 Discount increased to 10%, return percentage varies

Figure 5.4 Discount increased to 10%, return percentage varies