Turn on the television during market hours and there's a good chance you'll stumble across a purported expert expounding the virtues of some company's stock. Any number of reasons may be presented, but their focus will invariably be stock-specific—talk of supply and demand of securities or the importance of country and sector allocations is unlikely. That's because most investors believe investing begins and ends with picking stocks. Unfortunately, they're only half right.

As a top-down investor, you know the last step is indeed stock selection. But you also know it's the least important decision for your portfolio's overall return, and your investment process shouldn't start with it. This is especially so for emerging markets. As discussed in Chapter 5, emerging markets are concentrated. A few countries dominate the market, and a few sectors and stocks rule the country. This makes the top-down method the most logical approach because the largest companies—which often compose the majority of the country's weight—are often driven more by the economic, political, and sentiment drivers of the country than those specific to the company.

With the majority of excess return added in these higher level decisions, it's not vital to pick the "best" stocks in the universe. Rather, you want to pick stocks with a good probability of outperforming their peers. Doing so can enhance returns without jeopardizing good top-down decisions by picking risky, go-big-or-go-home stocks. Being right more often than not should create outperformance relative to your benchmark over time.

Every firm and every stock is different, and viewing them through the right lens is vital. Much like for portfolio drivers, investors need a functional, consistent, and reusable framework for analyzing securities. While by no means comprehensive, the framework provided and the questions at this chapter's end should serve as good starting points for the beginner-to-intermediate investor to help identify strategic attributes and company-specific risks. For a more thorough understanding of financial statement analysis, valuations, modeling, and other tools of security analysis, additional reading is suggested.

Security analysis is nowhere near as complicated as it may seem—but that doesn't mean it's easy. Similar to your goal in appropriately allocating to countries and sectors, you've got one basic task: Spot opportunities not currently discounted into prices. Or, put differently, know something others don't. Investors should analyze firms by taking consensus expectations for a company's estimated financial results and then assessing whether it will perform below, in line with, or above those baseline expectations. Profit opportunities arise when your expectations are different and more accurate than consensus expectations. Trading on widely known information or consensus expectations adds no value to the stock selection process. Doing so is really no different than trading on a coin flip.

The top-down method offers two ways to spot such opportunities. First, accurately predict high-level, macro themes affecting a group of companies—these are your portfolio drivers as outlined in Chapter 6. Second, find firms that will benefit most if those high-level themes and drivers play out. This is done by finding firms with competitive advantages (we'll explain this concept more in a bit).

Analyzing a stock against its peer group can be summarized as a five-step process:

These five steps provide a consistent framework for analyzing firms in their peer groups. While these steps are far from a full stock analysis, they provide the basics necessary to begin making better stock selections.

The first step is to understand what the business does, how it generates its earnings, and what drives those earnings. Here are a few tips to help in the process.

Industry overview: Begin any analysis with a basic understanding of the firm's industry, including its drivers and risks. You should be familiar with how current economic trends affect the industry.

Company description: Obtain a business description of the company, including an understanding of the products and services within each business segment. Browse the firm's website and financial statements/reports to gain an overview of the company and how it presents itself.

Corporate history: An understanding of firm history may reveal its growth strategy or clues to its true core competencies. Analyze the firm's history since its inception and over the last several years. Ask questions like: Has it been an industry leader for decades, or is it a relative newcomer? Has it switched strategies or businesses often in the past?

Business segments: Break down company revenues and earnings by business segment and geography to determine how and where it makes its money. Find out what drives results in each business and geographic segment. Begin thinking about how each of these business segments fits into your high-level themes.

Recent news/press releases: Read all recently released news about the stock, including press releases. Do an Internet search and see what comes up. Look for any significant announcements regarding company operations. What is the media's opinion of the firm? Is it a bellwether to the industry or a minor player?

Markets and customers: Identify main customers and the markets it operates in. Determine whether the firm has any particularly large single customer or a concentrated customer base.

Competition: Find the main competitors and how market share compares with other industry players. Is the industry highly segmented? Assess the industry's competitive landscape. Keep in mind the biggest competitors can sometimes lurk in different industries—sometimes even in different sectors! Get a feel for how the firm stacks up—is it an industry leader or a minor player? Does market share matter in that industry?

After gaining a sound grasp of firm operations, the next step is identifying strategic attributes consistent with higher level portfolio themes. Also known as competitive or comparative advantages, strategic attributes are unique features allowing firms to outperform their industry or sector. Since industry peers are generally affected by the same high-level drivers, strong strategic attributes are the edge in creating superior performance. Examples of strategic attributes include:

High relative market share

Low-cost production

Superior sales relationships/distribution

Economic sensitivity

Vertical integration

Strong management/business strategy

Geographic diversity or advantage

Consolidator

Strong balance sheet

Niche market exposure

Pure play

Potential takeover target

Proprietary technologies

Strong brand name

First mover advantage

Portfolio drivers help determine which kind of strategic attributes are likely to face head- or tailwinds. After all, not all strategic attributes will benefit a firm in all environments. For example, while higher operating leverage might help a firm boost earnings when an industry is booming, it would have the opposite effect in a down cycle. Access to iron ore reserves for a steel producer was an important strategic attribute from 2003 to 2007 due to the rising cost of raw materials (see Chapter 6). When iron ore prices decline, however, iron ore operations will create a drag on company earnings growth relative to other producers. Thus, it's essential to pick strategic attributes consistent with higher level portfolio themes.

A strategic attribute is also only effective to the extent management recognizes and takes advantage of it. Execution is key. For example, if a firm's strategic attribute is technological expertise, it should focus its effort on research and development to maintain that edge. If its strategic attribute is low-cost production relative to its peer group, it should capitalize by potentially lowering prices or expanding production (assuming the new production is also low cost) to gain market share.

Identifying strategic attributes may require thorough research of the firm's financial statements, website, news stories, history, and discussions with customers, suppliers, competitors, or management. Don't skimp on this step—be diligent and thorough in finding strategic attributes. It may feel like an arduous task at times, but it's also among the most important in security selection.

Once you've gained a thorough understanding of the business, earnings drivers, and strategic attributes, the next step is analyzing firm performance both fundamentally and in the stock market.

Emerging market financial information can be notoriously difficult to find. Reporting standards are simply not as rigorous and standardized as the developed world—countries often don't require regular filings, if at all. All is not lost, however. Most reasonably sized emerging market firms have listings on developed market exchanges. If a company lists on a US exchange, for example, it is required to file a 20-F—a condensed version of the 10-K filing, which is required annually for all US companies. These filings and more can be found online at the Securities and Exchange Commission's (SEC) EDGAR database http://www.sec.gov/). In addition, as companies expand globally, they are increasingly cognizant of investors' desire to have detailed information on their financial results. As such, many companies have begun to post this information to their websites.

If you can't find information, ignore the company. Every once in a while, you may lose out on a winner, but it's simply not worth the added risk. If filings are available, analyze performance in recent quarters/years. Not all earnings results are created equal. Understanding what drives results gives clues to what will drive future performance. Ask things like:

What are recent revenue trends? Earnings? Margins? Which business segments are seeing rising or falling sales?

Is the firm growing its business organically, because of acquisitions, or some other reason?

How sustainable is their strategy?

Are earnings growing because of strong demand or because of cost cutting?

Are they using tax loopholes and one-time items?

What is management's strategy to grow the business for the future?

What is the financial health of the company?

Next, evaluate stock performance. Check the company's chart for the last few years and try to determine what has driven performance. Explain any big up or down moves and identify any significant news events. If the stock price has trended steadily downward despite consistently beating earnings estimates, there may be a force driving the whole industry downward. Likewise, if the company's stock soared despite reporting tepid earnings growth or prospects, there may be some force driving the industry higher, like takeover speculation. Or stocks can simply move in sympathy with the broader market. Whatever it is, make sure you know and understand.

Some companies offer earnings calls announcing recent results. If available, these are typically posted on the investor relations section of a firm's website. They are invaluable—read as many as you can get your hands on. You'll begin to notice similar trends and events affecting the industry. Take note of these so you can distinguish between issues that are company-specific or industry-wide.

Emerging markets individually can be riskier than developed markets. This is well known. But the risks aren't terribly different from those in developed markets—it's the degree that varies. For example, there is a greater propensity for stock ownership to be concentrated in emerging markets. One individual, or even the government, owning a majority of shares is common.

There are two main types of risks in security analysis: stock-specific risk and systematic risk (also known as non–stock specific risk). Both can be equally important to performance.

Stock-specific risks, as the name suggests, are issues affecting the company in isolation. These are mainly risks affecting a firm's business operations or future operations. Some company-specific risks are discussed in detail in the annual reports, or regulatory filings, but one can't rely solely on firms self-identifying risk factors. You must see what analysts are saying about them and identify all risks for yourself. Other examples include:

Stock ownership concentration (insider or institutional)

Customer concentration

Sole suppliers

Excessive leverage or lack of access to financing

Obsolete products

Poor operational track record

High cost of products versus competitors

Latest filings

Qualified audit opinions

Hedging activities

Pension or benefit underfunding risk

Regulatory or legal (pending litigation)

Pending corporate actions

Executive departures

Regional, political/governmental risk

Systematic risks include macroeconomic or geopolitical events out of a company's control—many of the potential drivers discussed in Chapter 6. While these risks may affect a broad set of firms, they will have varying effects on each. Some examples include:

Commodity prices

Industry cost inflation

Economic activity

Labor scarcity

Strained supply chain

Legislation affecting taxes, royalties, or subsidies

Geopolitical risks

Capital expenditures

Interest rates

Currency

Weather

Identifying stock-specific risks helps an investor evaluate the relative risk and reward potential of firms within a peer group. Identifying systematic risks helps you make informed decisions about which sub-industries and countries to overweight or underweight.

If you don't feel strongly about any company in a peer group within a sub-industry you wish to overweight, you could pick the company with the least stock-specific risk. This would help to achieve the goal of picking firms with the greatest probability of outperforming their peer group and still performing in line with your higher level themes and drivers.

Valuations can be tricky. They are tools used to evaluate market sentiment and expectations for firms. But they are not a foolproof way to see if a stock is "cheap" or "expensive." Valuations are primarily used to compare firms against their peer group (or peer average) or a company's valuation relative to its own history. As mentioned earlier, stocks move not on the expected, but on the unexpected. We aim to try and gauge what the consensus expects for a company's future performance and then assess whether that company will perform below, in line with, or above expectations.

Valuations provide little information by themselves in predicting future stock performance. Just because one company's P/E is 20 while another's is 10 doesn't mean you should buy the one at 10 because it's "cheaper." There's likely a reason why one company has a different valuation than another, including such things as strategic attributes, earnings expectations, sentiment, stock-specific risks, and management's reputation. The main usefulness of valuations is explaining why a company's valuation differs from its peers and determining if it's justified.

There are many different valuation metrics investors use in security analysis. Some of the most popular include:

Once you've compiled the valuations for a peer group, try to estimate why there are relative differences and if they're justified. Is a company's relatively low valuation due to stock-specific risk or low confidence from investors? Is the company's forward P/E relatively high because consensus is wildly optimistic about the stock? A firm's higher valuation may be entirely justified, for example, if it has a growth rate greater than its peers. A lower valuation may be warranted for a company facing a challenging operating environment in which it is losing market share. Seeing valuations in this way will help to differentiate firms and spot potential opportunities or risks.

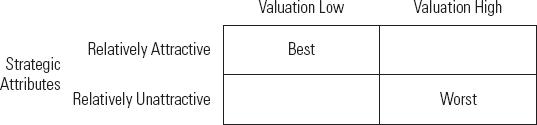

Valuations should be used in combination with previous analysis of a company's fundamentals, strategic attributes, and risks. For example, Figure 7.1 is a grid showing how an investor could combine an analysis of strategic attributions and valuations to help pick firms.

Stocks with relatively low valuations but attractive strategic attributes may be underappreciated by the market (as shown in Figure 7.1). Stocks with relatively high valuations but no discernible strategic attributes may be overvalued by the market. Either way, use valuations appropriately and in the context of a larger investment opinion about a stock, not as a panacea for true value.

While this chapter's framework can be used to analyze any firm, there are additional factors related to emerging markets stocks that should be considered. The following section provides some of the most important factors and questions to consider when researching firms in the category. Answers to these questions should help distinguish between firms within a peer group and help identify strategic attributes and stock-specific risks. While there are countless other questions and factors that could and should be asked, these should serve as a good starting point.

Revenues and Earnings Breakdown: Most firms produce more than a single product. The more diversified the revenue, the less exposed the firm is to fluctuations in a single product or end market. Its product mix will also determine what has the greatest affect on the firm's future earnings and performance. How are the firm's revenues and earnings divided between products? How does this compare to competitors? Is it more concentrated or diversified?

Geographic Breakdown and Geopolitical Risk: Regional prices and volumes demanded can vary dramatically between home and export markets. Thus, regional diversification can mitigate risks of big changes in any one market. For globally priced goods, a breakdown of regional production will help identify political and social risks to production, while a breakdown of regional consumption will identify the primary drivers.

Where are most of the firm's current and future planned production sites? Are they in politically stable or unstable countries? What percentage of production comes from politically unstable regions? Do they have a solid history of operating in foreign territories? Has the company historically had good or troubled relations with governments in the region? Are labor unions historically strong or weak in those regions? Do tariffs, subsidies, or price caps exist? Is the firm beholden to trade problems with other regions? For regionally priced goods, how quickly is the product's end market growing in its regions of operation?

While a firm with relatively high exposure to a geopolitically unstable region may face higher risks of government intervention or production disruption, the potential additions to production growth may warrant these risks and are not always inherent negatives.

Government Control: Emerging market governments play a larger role in firms. Companies are often partially or entirely government-owned and may be subject to unique taxes, royalties, subsidies, or price controls. Dividend policies may also be set in the interest of balancing budgets rather than future earnings. Depending on the circumstances, government ownership can work for or against a company, but you'll want to know its impact.

Some questions to ask: Are the firm's shares owned or controlled by a government? If so, to what degree? Does the government play an active role in firm decisions and policies? If so, has it ever made decisions in conflict with the interests of shareholders? Does the firm secure free market pricing for its product or does the government set pricing? Has the company historically been given special treatment or favored over other producers for contracts, loans, or taxes?

Competition and Barriers to Entry: What is the competitive landscape of the firm's peers? Does it compete against government-owned firms? Does the firm operate in a region or industry with significant barriers to entry? Barriers to entry may include dominant market share, capital intensity, patents, proprietary technology, a concentrated industry, and difficulty in obtaining regulatory or environmental permits. High barriers to entry typically provide pricing power and reduce competition.

Supply/Demand Environment: For globally priced goods, what is the product's supply/demand environment around the world? And for regionally priced goods, what is it within the firm's countries of operation? Have prices recently been affected by changes or expectations of changes in the supply/demand equation? Both supply- and demand-side factors will have a great influence on prices, which can be volatile.

Cost Structure: Emerging market firms tend to have notably different cost structures. Because firms often lack productivity-enhancing technology, labor costs are higher as a percent of revenue. These factors differ markedly across countries and sectors. What factors are driving the firm's production costs? What are the firm's production costs relative to its peers? What is the firm's strategy to mitigate industry cost inflation? Does its plan differ from competitors? If it's a low-cost producer compared to peers, does it have a strategy to take advantage of that? If it's a high-cost producer, does it have a strategy to change that?

Infrastructure: Emerging markets infrastructure varies across countries and is generally inferior to developed markets. Does the firm face infrastructure burdens relative to its peers? For example, does it have consistent access to electricity and power? Does it have easy access to its supply chain?

Transportation: Transportation costs are particularly important for bulk goods (with lower value-to-weight ratios) where transportation makes up a greater percentage of overall costs. How does the firm deliver its product to consumers? How far away are its consumers? What impact will rising or falling transportation costs have on it compared to competitors? Are there any transportation bottlenecks? If so, does it have a plan to address them? How has the firm responded to such bottlenecks in the past?

Legislative Risks: Are there any legislative risks? These can include royalties, windfall taxes, environmental legislation, price caps, labor laws, subsidies, tariffs, and the nationalization of assets. How thoroughly are laws enforced?

Technology and Innovation: Does the firm possess any proprietary technologies or patents giving it a competitive edge? Does it have a history of innovation? Is its end market dynamic, requiring the consistent release of new products, or do they specialize in more mature markets?

Regulation: How are the firm's operations affected by regulation? Does the firm currently operate in a favorable regulatory environment? How might that change? What is the firm's history with gaining regulatory approval for its products? Firms with highly regulated assets are exposed to regulatory risks, but they may also have more stable returns.

Market Share: Dominant market share often provides greater pricing power, especially for regionally priced goods. Because there are fewer companies competing in emerging market industries, dominant share levels differ from developed markets. For example, a company with a 20 percent share would likely have dominant share in the developed world but be an average-sized player in emerging markets.

Some questions to ask: What is the firm's market share in each of its business segments relative to its competitors? How fragmented are the consumers in its end markets? Does the firm have pricing power for its products and services? For regionally priced products, how do its prices and raw material costs compare to competitors?

Margins: Are margins growing or shrinking? Has the company historically offset higher costs with higher prices? How do its margins compare to peers? High margins in a vacuum tell you little since some industries historically hold higher margins than others, and it's usually well-known and taken into account in share prices.

Cash-Flow Use: How is the firm spending its cash flow? To what degree is it buying back shares, paying dividends, spending on capital expenditures, or paying down debt? Depending on industry conditions, investors may prefer a firm rewarding shareholders with dividends and share buybacks over one taking on risky new production plans.

Balance Sheet: Does the firm have the financial ability to make large acquisitions to fuel growth? Does the firm's balance sheet allow it to take on additional leverage? Debt isn't necessarily a bad thing—many firms generate an excellent return on borrowed funds. In either case, it's vital to understand the capital structure of a firm.

Interest Rates: Interest rates vary widely across countries and industries. How sensitive is the firm's operations to interest rates? Are rising or falling rates good or bad for the firm's operations and share price? Firms with greater leverage tend to be more affected by interest rate movements due to changes in interest expense.

Currency: Currency risk arises when a company sells it goods or services to a foreign country. How much of the company's revenues are denominated in foreign currency? What are the risks in that foreign country? Is the company hedged?

Employee Relations: What is the company's relationship with its workforce? Is it heavily unionized? Generous pension benefits? Lifetime employment? Can a company freely hire or fire workers based on the country's employment laws? Labor laws can have a dramatic impact on the operating environment (like Black Economic Empowerment (BEE) in Chapter 4).

Security Availability: Last, but certainly not least, can you actually purchase the security through your broker? Is an ADR available?

Chapter Recap

The top-down investment methodology first identifies and analyzes high-level portfolio drivers affecting broad categories of stocks. These drivers help determine portfolio country, sector, and style weights.

Quantitative factor screening helps narrow the list of potential portfolio holdings based on characteristics such as valuations, liquidity, and solvency.

Stock selection is the last step in the top-down process. Stock selection attempts to find companies possessing strategic attributes consistent with higher level portfolio drivers.

Stock selection also attempts to find companies with the greatest probability of outperforming their peers.