07

Cash Flow Management

All accountants and bank managers (although I should probably use their preferred title of ‘relationship managers’ these days) love cash flow forecasts. The reason they like them so much is that they know cash flow forecasts are the most accurate way to predict the future financial health of the business, both in the short and medium term. Accountants know, from their experience in dealing with insolvency, that most businesses fail when they simply run out of cash. The popular misconception is that businesses are forced to close because they failed to make a profit or to find sufficient customers. The truth is that the majority are forced into liquidation because they could no longer meet their financial obligations when they fell due and the bank’s goodwill had been exhausted.

Cash Flow Forecast – A Definition

The cash flow forecast is a rolling statement of all of the cash inflows and outflows for the practice which predicts the month end cash balance for a number of months ahead. This is one of the most important reports for an architect to monitor in order to get a view of when a cash shortage problem may be approaching.

You will commonly hear the directors of a recently declared insolvent company make comments such as: ‘If only that major customer had paid us on time then we would have survived’. I often refer to the quarterly VAT payment as the ‘dreaded VAT payment’ – which gets that name because it is often the final straw. It is the last large payment that simply cannot be met, and which pushes the business that has been teetering on the brink of its overdraft limit for the last few months over the edge. As a number of professional football clubs have discovered in recent years it is often the VAT department of HMRC that initiates winding-up procedures.

The cash flow forecast is one of the key documents that the bank will want to see regularly in support of its overdraft facilities, and it is important to ensure that it is as accurate as possible. The bank will look back and review the accuracy of the cash flow forecasts that they have been given in the past. They understand that these were forecasts and will not expect them to be entirely accurate. However, if they can see that the forecasts are consistently very inaccurate, they will begin to have doubts about the competence of the management team, and the practice’s ability to manage its own financial affairs.

If the bank feels uncomfortable, it may be unwilling to renew the overdraft facility when it falls due, which could have serious financial consequences. It is worth remembering that bank overdrafts are repayable on demand, which means that the bank does have a right to ask the practice for the entire amount outstanding on the overdraft to be paid back within a few days.

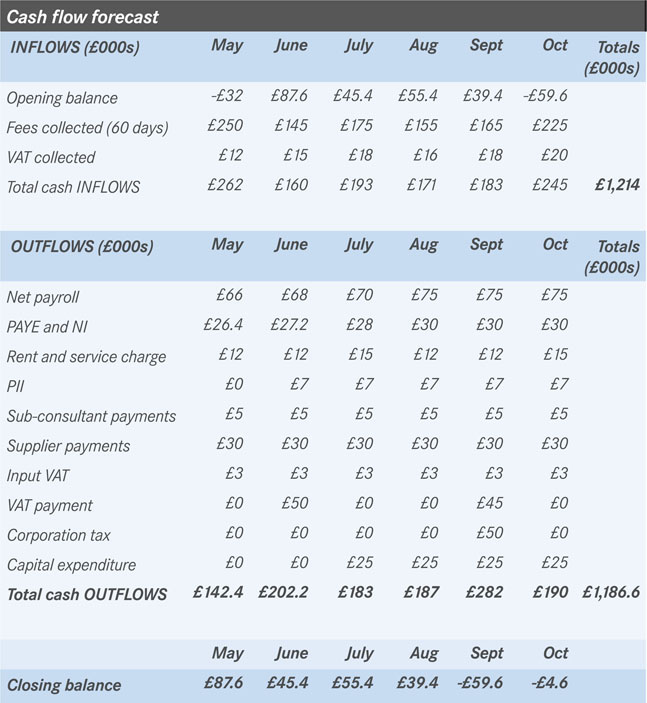

The chart opposite shows a typical cash flow forecast.

The cash flow forecast is the most important tool available for predicting the continuing financial health of the practice. Like many financial reports, it is most easily read from the bottom up. The row at the foot of the page shows the predicted final (closing) bank balance the end of each month. This shows at a glance if there is going to be a cash flow problem and when it is likely to arise.

In common with the captive and possible fees and resources spreadsheets, the cash flow forecast is a rolling forecast – in the example above, it is a rolling six-month forecast. This means that the forecast is revised each month and in so doing the first month is removed and a new month is added on the end.

Each practice will have to establish a suitable forecast period to suit its needs. For smaller practices it is like to be up to 6 months, whereas larger practices may well be able to work meaningfully with a 12 or 18 month forecast.

Cash flow forecast

This is the classic report prepared by finance people all over the world and the bank manager’s favourite. It shows the amount of money that is predicted to flow in and out of the practice and the projected bank balance at the end of each month.

Using Longer-Term Cash Flow Forecasts to Assess the Business Viability

The example cash flow forecast shown above is a model based on normal operating conditions. If the practice is considering approaching the bank about financing a major new project (such as the purchase of new premises or the acquisition of another practice) it will need to produce cash flow forecast extended up to two or even three years in support of the application.

In addition, for end-of-year accounting purposes accountants and auditors may require some long-term cash flow forecasts to support a ‘going concern’ assumption for the business. Once the practice is large enough to require a formal audit, the accountants will need to produce accounts to which they are prepared to sign a declaration that the accounts that they have prepared show a ‘true and fair view’ of the financial position of the business. As a part of this process the accountants will take a view on the ability of the business to keep operating in its current form and the long-term cash flow forecast will be a key report that will enable them to do this.

It is interesting to check the total value of inflows against the total value of outflows over the course of the forecast period to get a sense of overall liquidity.

In the example, total inflows for the six months are £1.214 million, whereas total outflows are expected to be £1.187 million, indicating a potentially balanced position across the period. As this forecast is directly linked to the fee forecast described in Chapter 6 it will tend to follow a similar pattern. Most cash flow forecasts show an improving position over the next quarter or two, and then a rapid deterioration six months or so later. This reflects the uncertainty of future fees and the financial ‘cliff edge’ effect that all practices tend to face in the medium term.

Cash flow is often described as the lifeblood of the business. It is useful to think of cash in these terms: something that needs to keep circulating in order to keep each part of the practice healthy.

Equally – although it is not usually a problem that many architecture practices have – it is also not a good idea to sit on a large cash pile for too long. Money needs to flow and to be used creatively, rather than just be left to accumulate in the bank account. This is especially true in the current ultra-low interest rate environment.

It is worth looking at this forecast in some detail.

Cash Inflows

The top section of the cash flow chart shows the money that is coming into the practice, of which the largest element is the collection of fees from clients. For this you need to make an honest and realistic assumption about how quickly the fees are being paid. Most practices will have standard payment terms of 30 days, but that does not mean this will actually be achieved. Therefore, you need to work with the reality of the situation based on experience, which you can do by calculation of the average ‘debtor days’ as shown above.

Worked Example: Calculating ‘Debtor Days’

For example, say the annual gross fee income (including VAT) is £200,000, and the average amount due from clients at the month end is £33,000:

This means that on average it takes 60 days to collect the fees that are invoiced.

Equally, you can perform a similar calculation for ‘creditor days’ (i.e. how long does it take on average to pay your suppliers).

If the average amount due is £15,000 and the annual gross cost of overheads is £100,000, then

These examples represent a balanced scenario, in which the practice is being paid at a broadly similar rate to the speed with which it is settling the bills with suppliers. At SEH, we set target debtor and creditor days as a part of our annual budget process and monitor the ongoing trends on a monthly basis as part of our KPI package.

These calculations become the working assumptions to be used for cash flow purposes.

Using these values, you can fill in the fees collected row in the cash flow spreadsheet by taking the figures from the captive fees forecast and entering them into the anticipated cash flow two months later. This means that fees invoiced in January are assumed to be collected in March, and so on.

It is good practice for the cash flow forecast to show the key assumptions as a footnote, so that anyone looking at it can make a judgement about the reasonableness of the assumptions and thus the reliability of the cash flow built on those assumptions.

Accounting for VAT

The cash flow forecast needs to account for all the money going in and out of the practice, so it must allow for the effects of VAT. Assuming that your clients are all UK-based and VAT registered, you will need to add 20 per cent to the fees collected as an inflow of cash. You also need to estimate how much VAT you pay to your suppliers and enter that figure as a cash outflow. Then you need to plan to pay HMRC the net VAT, usually on a quarterly basis (where net VAT is simply the VAT you have collected from customers minus the VAT you have paid out to suppliers in the most recent three-month reporting period, i.e. net VAT = output VAT – input VAT). It is important to be prepared for this relatively large payment.

While on the subject of VAT, it is worth mentioning the potential attractions of HMRC’s Flat Rate Scheme (FRS). This can work well for professional service firms such as architects where all, or the vast majority, of the work is for UK-based VAT registered clients, and the practice does not incur a large amount of input VAT (i.e. payments of VAT to its own suppliers). The FRS is attractive because it is much simpler to administer than the normal quarterly accounting for all income and expenses, and can also result in a small ‘profit’ for the practice. At the time of writing, the FRS percentage applicable to architects is 14.5 per cent. It is worth exploring with your accountant whether the FRS would work well in your particular circumstances.

Worked Example: FRS Calculation

| Value of sales invoiced in the three-month period | £100,000 |

| VAT added to sales (at 20%) | £20,000 |

| Total | £120,000 |

| Apply the FRS percentage to the total: | |

| 14.5% of £120,000 = | £17,400 |

That is the figure to be paid across to HMRC.

Note that the practice has, of course, collected £20,000 of output VAT from its clients, and has therefore made a gain of £2,600.

In this simplified method no input tax is claimed, so this ‘gain’ is the allowance for the VAT that has been paid to suppliers in the period but not claimed.

There is even an additional first year incentive whereby the rate used is reduced by 1 per cent – which gives the small business an even greater ‘profit’.

Cash Outflows

The first thing that you will notice on the cash flow forecast spreadsheet above is that there are many more rows in the outflows section than there are in the inflow sections. As with the rest of our lives, there always seem to be many more ways to spend money than there are ways to earn it!

Even in the simple example forecast there are a number of lines which represent groups of expenses. It is essential to ensure that all of the many types of practice expenditure are included somewhere in the cash flow, perhaps by working through the detailed Profit and Loss account on a line by line basis. It could also be useful to pore over old bank statements to look for items that have been missed or which only arise occasionally (e.g. annual subscriptions or insurance renewals). I like to keep a rolling comparison of my monthly cash flow forecast with the actual cash flow achieved. This is a good feedback mechanism that can help to improve the accuracy of the cash flow forecast process for the future.

The largest single regular cash outflow is likely to be the payroll. The associated PAYE income tax and NI contributions are deducted from salaries and have to be paid across to HMRC by the middle of the following month. The total payroll figure for any given month is split over two months, with the net pay (i.e. after tax deductions) going out in the first month and the PAYE and NI deductions relating to it being paid to HMRC in the following month. In the normal course of events this makes little difference, because the total outflows are much the same from month to month. However, it’s important to model the effects of the annual pay review and the payment of any irregular bonuses.

It is important to identify separately all significant single items of expenditure, such as the PII premium, which may have to be paid in a single instalment or perhaps be spread over a number of months (as it is in the example above).

It also helpful to identify the payments that need to be made to the members of the design team for which the architect is acting as lead consultant for invoicing and payment purposes. These can be significant amounts and can have a serious impact on the overall cash flow position, especially if the architect has to pay the consultant before having collected the equivalent funds from the client. This can represent a significant risk for which the architect receives little if any reward.

Finally, you need to ensure that you include those items of capital expenditure that were identified in the capital budget. This can require large sums to be spent at a particular point in time. The cash flow forecast may suggest that you should consider entering into suitable finance arrangements (e.g. leasing for the purchase of computer equipment) if outright purchase would seem to be straining the cash flow unduly.

Accounting for Taxation

The payment of income tax and corporation tax are the other significant items to be included in the list of cash outflows. For partnerships or LLPs there will be self-assessment income tax payments to be made in January and July of each year. For companies, there will be a single annual corporation tax payment, of approximately 20 per cent of profits, to be made to HMRC within nine months and a day of the end of the company’s financial year.

Summary

- Cash is the lifeblood of any business. It represents the flow of energy through the body of the practice. It needs to be kept moving and it needs to be constantly refreshed.

- The cash flow forecast is one the most important financial control reports.

- If the bank has provided finance in the form of an overdraft or loan it will certainly expect to see the cash flow forecast at regular intervals.

- Periodic payments such as income tax and VAT are often the straw that breaks the camel’s back. The practice may be just managing to keep its head above water from month to month in financial terms when a large tax bill comes along which simply cannot be paid.

- As well as the day-to-day income and expenses, cash flow forecasts need to take account of other items such as capital expenditure on cars, computer equipment and furniture, which can require large amounts of cash to be found at a particular point in the year and can throw the whole cash flow plan adrift.