CHAPTER 17 Investments

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Identify the three categories of debt securities and describe the accounting and reporting treatment for each category.

- Understand the procedures for discount and premium amortization on bond investments.

- Identify the categories of equity securities and describe the accounting and reporting treatment for each category.

- Explain the equity method of accounting and compare it to the fair value method for equity securities.

- Describe the accounting for the fair value option and for impairments of debt and equity investments.

- Describe the reporting of reclassification adjustments and the accounting for transfers between categories.

What to Do?

A few years ago, a bank reported an $87.3 million write-down on its mortgage-backed securities for the third quarter of 2008. However, the bank stated that it expected its actual losses to be only $44,000. The loss of $44,000 was equal to a modest loss on a condo foreclosure. The bank's regulator found “the accounting result absurd.” And the bank regulator was right, as the bank, in the third quarter of 2009, raised its credit-loss estimate by $263.1 million, quite a difference from its original loss estimate of $44,000.

The discussion above highlights the challenge of valuing financial assets such as loans, derivatives, and other debt investments. The fundamental question that arose out of the example above and, more significantly, the recent financial crisis is: Should financial instruments be valued at amortized cost, fair value, or some other measure(s)? As one writer noted, the opinion that fair value accounting weakens financial and economic stability has persisted among many regulators and politicians. But some investors and others believe that fair value is the right answer because it is more transparent information. OK, so what to do?

Well, the FASB originally issued a proposal to account for just about all financial assets at fair value with gains and losses recorded in income (amortized cost would be disclosed for some financial assets). The FASB indicated this approach will provide the most relevant and transparent information about financial assets. In contrast, the IASB issued a new standard on financial assets (IFRS 9) that uses a mixed-attribute approach. Some of the financial assets are valued at amortized cost and others at fair value.

Interestingly, the European Union refused to consider adopting the requirements of IFRS 9, arguing that it contained too much fair value information. Nevertheless, the standard was issued and other countries that follow IFRS will have to implement the new standard in 2015. At the same time, as soon as the FASB issues its new standard, the IASB has indicated that it may revisit the valuation issue once again. Thus, the early reaction to IFRS 9 indicates that, unfortunately, once again politics is raising its ugly head on an accounting issue. Some European regulators have suggested that the IASB's future funding may even depend on the IASB putting more limits on the use of fair value.

![]() CONCEPTUAL FOCUS

CONCEPTUAL FOCUS

- See the Underlying Concepts on pages 954, 955, and 957.

- Read the Evolving Issues on pages 968 and 975 for a discussion of the fair value controversy, and proposed classification and measurement model for financial instruments.

![]() INTERNATIONAL FOCUS

INTERNATIONAL FOCUS

- See the International Perspectives on pages 952, 953, 966, 968, 987, 989, and 995.

- Read the IFRS Insights on pages 1026–1039 for a discussion of:

- Accounting for financial assets

- Debt investments

- Equity investments

- Impairments

Now, let's go back to the FASB. Recently, the FASB dropped its plan to value loans at fair value and permits amortized cost accounting for these loans. This decision means banks will continue to value loans as they do today. This reversal is a big victory for the banking industry, which argued that the fair value approach would hurt lending and provide unnecessary volatility in their financial results. As a consequence, the FASB is moving much closer to the IASB's position. So after much discussion about what went wrong in the accounting for financial instruments during the financial crises, it looks like we are headed back to most of the same measurement rules that occurred before the financial collapse of 2008. We deem that unfortunate.

Sources: Adapted from Jonathan Weil, “Suing Wall Street Banks Never Looked So Shady,” http://www.bloomberg.com/ (February 28, 2010); and Rachel Sanderson and Jennifer Hughes, “Carried Forward,” Financial Times Online (April 20, 2010).

PREVIEW OF CHAPTER 17

As indicated in the opening story, the accounting for financial assets is highly controversial. How to measure, recognize, and disclose this information is now being debated and discussed extensively. In this chapter, we address the accounting for debt and equity investments. Appendices to this chapter discuss the accounting for derivative instruments, variable-interest entities, and fair value disclosures. The content and organization of this chapter are as follows.

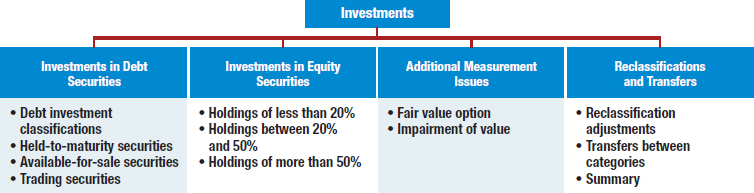

INVESTMENTS IN DEBT SECURITIES

LEARNING OBJECTIVE ![]()

Identify the three categories of debt securities and describe the accounting and reporting treatment for each category.

Companies have different motivations for investing in securities issued by other companies.1 One motivation is to earn a high rate of return. For example, companies like Coca-Cola and PepsiCo can receive interest revenue from a debt investment or dividend revenue from an equity investment. In addition, they can realize capital gains on both types of securities. Another motivation for investing (in equity securities) is to secure certain operating or financing arrangements with another company. For example, Coca-Cola and PepsiCo are able to exercise some control over bottler companies based on their significant (but not controlling) equity investments.

To provide useful information, companies account for investments based on the type of security (debt or equity) and their intent with respect to the investment. As indicated in Illustration 17-1, we organize our study of investments by type of security. Within this section, we explain the accounting for investments in debt. We address equity securities later in the chapter.

Debt securities represent a creditor relationship with another entity. Debt securities include U.S. government securities, municipal securities, corporate bonds, convertible debt, and commercial paper. Trade accounts receivable and loans receivable are not debt securities because they do not meet the definition of a security.

Debt Investment Classifications

Companies group investments in debt securities into three separate categories for accounting and reporting purposes:

![]() International Perspective

International Perspective

Under IFRS, debt investments are classified as either held-for-collection or trading.

- Held-to-maturity: Debt securities that the company has the positive intent and ability to hold to maturity.

- Trading: Debt securities bought and held primarily for sale in the near term to generate income on short-term price differences.

- Available-for-sale: Debt securities not classified as held-to-maturity or trading securities.

Illustration 17-2 identifies these categories, along with the accounting and reporting treatments required for each.

![]() International Perspective

International Perspective

Under IFRS, held-for-collection debt investments are valued at amortized cost; all other investments are measured at fair value.

Amortized cost is the acquisition cost adjusted for the amortization of discount or premium, if appropriate. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. [2]

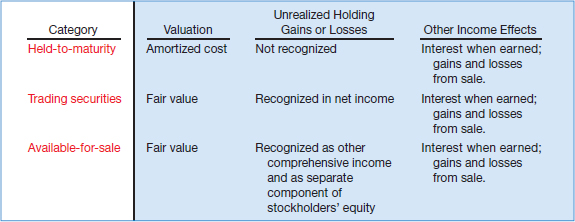

Held-to-Maturity Securities

LEARNING OBJECTIVE ![]()

Understand the procedures for discount and premium amortization on bond investments.

Only debt securities can be classified as held-to-maturity. By definition, equity securities have no maturity date. A company like Starbucks should classify a debt security as held-to-maturity only if it has both (1) the positive intent and (2) the ability to hold those securities to maturity. It should not classify a debt security as held-to-maturity if it intends to hold the security for an indefinite period of time. Likewise, if Starbucks anticipates that a sale may be necessary due to changes in interest rates, foreign currency risk, liquidity needs, or other asset-liability management reasons, it should not classify the security as held-to-maturity.2

Companies account for held-to-maturity securities at amortized cost, not fair value. If management intends to hold certain investment securities to maturity and has no plans to sell them, fair values (selling prices) are not relevant for measuring and evaluating the cash flows associated with these securities. Finally, because companies do not adjust held-to-maturity securities to fair value, these securities do not increase the volatility of either reported earnings or reported capital as do trading securities and available-for-sale securities.

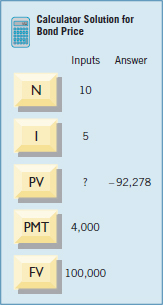

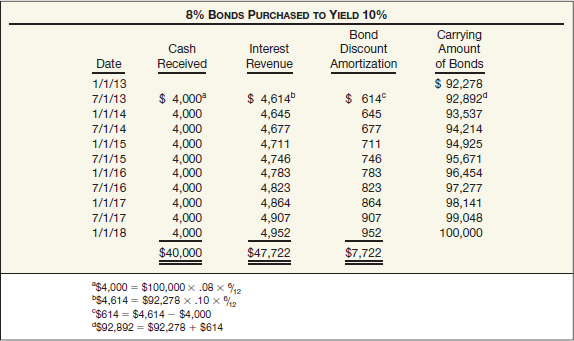

To illustrate the accounting for held-to-maturity debt securities, assume that Robinson Company purchased $100,000 of 8 percent bonds of Evermaster Corporation on January 1, 2013, at a discount, paying $92,278. The bonds mature January 1, 2018 and yield 10%. Interest is payable each July 1 and January 1. Robinson records the investment as follows.

![]()

Robinson uses a Debt Investments account to indicate the type of debt security purchased.3

![]() Underlying Concepts

Underlying Concepts

The use of some simpler method that yields results similar to the effective-interest method is an application of the materiality concept.

As indicated in Chapter 14, companies must amortize premium or discount using the effective-interest method unless some other method—such as the straight-line method—yields a similar result. They apply the effective-interest method to bond investments in a way similar to that for bonds payable. To compute interest revenue, companies compute the effective-interest rate or yield at the time of investment and apply that rate to the beginning carrying amount (book value) for each interest period. The investment carrying amount is increased by the amortized discount or decreased by the amortized premium in each period.

Illustration 17-3 shows the effect of the discount amortization on the interest revenue that Robinson records each period for its investment in Evermaster bonds.

ILLUSTRATION 17-3 Schedule of Interest Revenue and Bond Discount Amortization—Effective-Interest Method

Robinson records the receipt of the first semiannual interest payment on July 1, 2013 (using the data in Illustration 17-3), as follows.

Because Robinson is on a calendar-year basis, it accrues interest and amortizes the discount at December 31, 2013, as follows.

Again, Illustration 17-3 shows the interest and amortization amounts.

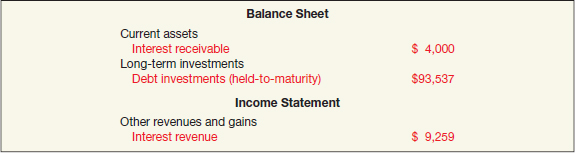

Robinson reports its investment in Evermaster bonds in its December 31, 2013, financial statements, as follows.

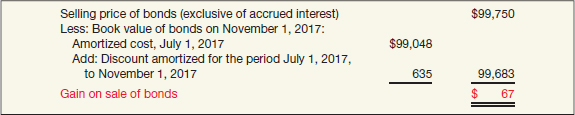

Sometimes, a company sells a held-to-maturity debt security so close to its maturity date that a change in the market interest rate would not significantly affect the security's fair value. Such a sale may be considered a sale at maturity and would not call into question the company's original intent to hold the investment to maturity. Let's assume, as an example, that Robinson Company sells its investment in Evermaster bonds on November 1, 2017, at 99¾ plus accrued interest. The discount amortization from July 1, 2017, to November 1, 2017, is $635 (![]() × $952). Robinson records this discount amortization as follows.

× $952). Robinson records this discount amortization as follows.

![]()

Illustration 17-5 shows the computation of the realized gain on the sale.

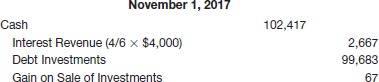

Robinson records the sale of the bonds as:

The credit to Interest Revenue represents accrued interest for four months, for which the purchaser pays cash. The debit to Cash represents the selling price of the bonds plus accrued interest ($99,750 + $2,667). The credit to Debt Investments represents the book value of the bonds on the date of sale. The credit to Gain on Sale of Investments represents the excess of the selling price over the book value of the bonds.

Available-for-Sale Securities

![]() Underlying Concepts

Underlying Concepts

Recognizing unrealized gains and losses is an application of the concept of comprehensive income.

Companies like Amazon.com report available-for-sale securities at fair value. It records the unrealized gains and losses related to changes in the fair value of available-for-sale debt securities in an unrealized holding gain or loss account. Amazon adds (subtracts) this amount to other comprehensive income for the period. Other comprehensive income is then added to (subtracted from) accumulated other comprehensive income, which is shown as a separate component of stockholders' equity until realized. Thus, companies report available-for-sale securities at fair value on the balance sheet but do not report changes in fair value as part of net income until after selling the security. This approach reduces the volatility of net income.

Example: Single Security

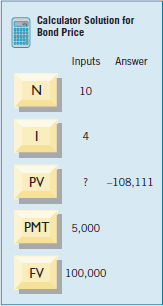

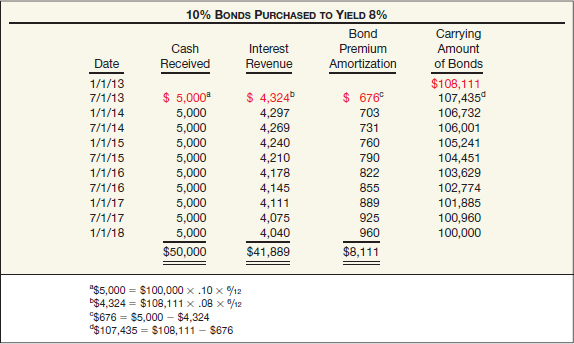

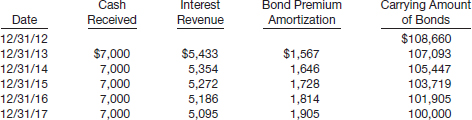

To illustrate the accounting for available-for-sale securities, assume that Graff Corporation purchases $100,000, 10 percent, five-year bonds on January 1, 2013, with interest payable on July 1 and January 1. The bonds sell for $108,111, which results in a bond premium of $8,111 and an effective-interest rate of 8 percent.

Graff records the purchase of the bonds as follows.

![]()

Illustration 17-6 discloses the effect of the premium amortization on the interest revenue Graff records each period using the effective-interest method.

ILLUSTRATION 17-6 Schedule of Interest Revenue and Bond Premium Amortization—Effective-Interest Method

The entry to record interest revenue on July 1, 2013, is as follows.

At December 31, 2013, Graff makes the following entry to recognize interest revenue.

As a result, Graff reports revenue for 2013 of $8,621 ($4,324 + $4,297).

To apply the fair value method to these debt investments, assume that at year-end the fair value of the bonds is $105,000 and that the carrying amount of the investments is $106,732. Comparing this fair value with the carrying amount (amortized cost) of the bonds at December 31, 2013, Graff recognizes an unrealized holding loss of $1,732 ($106,732 − $105,000). It reports this loss as other comprehensive income. Graff makes the following entry.

![]()

![]() Underlying Concepts

Underlying Concepts

Companies report some debt securities at fair value not only because the information is relevant but also because it is representationally faithful.

Graff uses a valuation account instead of crediting the Debt Investments account. The use of the Fair Value Adjustment (available-for-sale) account enables the company to maintain a record of its amortized cost. Because the adjustment account has a credit balance in this case, Graff subtracts it from the balance of the Debt Investments account to determine fair value. Graff reports this fair value amount on the balance sheet. At each reporting date, Graff reports the bonds at fair value with an adjustment to the Unrealized Holding Gain or Loss—Equity account.

Example: Portfolio of Securities

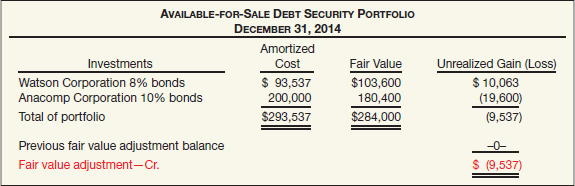

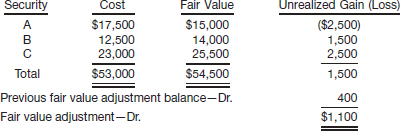

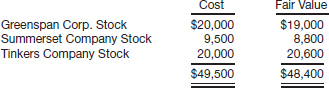

To illustrate the accounting for a portfolio of securities, assume that Webb Corporation has two debt securities classified as available-for-sale. Illustration 17-7 identifies the amortized cost, fair value, and the amount of the unrealized gain or loss.

The fair value of Webb's available-for-sale portfolio totals $284,000. The gross unrealized gains are $10,063, and the gross unrealized losses are $19,600, resulting in a net unrealized loss of $9,537. That is, the fair value of available-for-sale securities is $9,537 lower than its amortized cost. Webb makes an adjusting entry to a valuation allowance to record the decrease in value and to record the loss as follows.

![]()

Webb reports the unrealized holding loss of $9,537 as other comprehensive income and a reduction of stockholders' equity. Recall that companies exclude from net income any unrealized holding gains and losses related to available-for-sale securities.

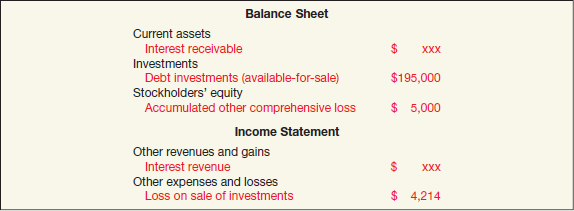

Sale of Available-for-Sale Securities

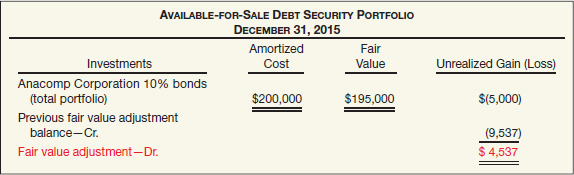

If a company sells bonds carried as investments in available-for-sale securities before the maturity date, it must make entries to remove from the Debt Investments account the amortized cost of bonds sold. To illustrate, assume that Webb Corporation sold the Watson bonds (from Illustration 17-7) on July 1, 2015, for $90,000, at which time it had an amortized cost of $94,214. Illustration 17-8 (on page 958) shows the computation of the realized loss.

Webb records the sale of the Watson bonds as follows.

Webb reports this realized loss in the “Other expenses and losses” section of the income statement.4 Assuming no other purchases and sales of bonds in 2015, Webb on December 31, 2015, prepares the information shown in Illustration 17-9.

Webb has an unrealized holding loss of $5,000. However, the Fair Value Adjustment (available-for-sale) account already has a credit balance of $9,537. To reduce the adjustment account balance to $5,000, Webb debits it for $4,537, as follows.

![]()

Financial Statement Presentation

Webb's December 31, 2015, balance sheet and the 2015 income statement include the following items and amounts (the Anacomp bonds are long-term investments but are not intended to be held to maturity).

Some favor including the unrealized holding gain or loss in net income rather than showing it as other comprehensive income.5 However, some companies, particularly financial institutions, note that recognizing gains and losses on assets, but not liabilities, introduces substantial volatility in net income. They argue that hedges often exist between assets and liabilities so that gains in assets are offset by losses in liabilities, and vice versa. In short, to recognize gains and losses only on the asset side is unfair and not representative of the economic activities of the company.

This argument convinced the FASB. As a result, companies do not include in net income these unrealized gains and losses. [3] However, even this approach solves only some of the problems because volatility of capital still results. This is of concern to financial institutions because regulators restrict financial institutions' operations based on their level of capital. However, companies can still manage their net income by engaging in gains trading (i.e., selling the winners and holding the losers).

What do the numbers mean? WHAT IS FAIR VALUE?

In the fall of 2000, Wall Street brokerage firm Morgan Stanley told investors that rumors of big losses in its bond portfolio were “greatly exaggerated.” As it turns out, Morgan Stanley also was exaggerating.

As a result, the SEC accused Morgan Stanley of violating securities laws by overstating the value of certain bonds by $75 million. The SEC said the overvaluations stemmed more from wishful thinking than reality, which violated generally accepted accounting principles. “In effect, Morgan Stanley valued its positions at the price at which it thought a willing buyer and seller should enter into an exchange, rather than at a price at which a willing buyer and a willing seller would enter into a current exchange,” the SEC wrote.

Especially egregious, stated one accounting expert, were the SEC's findings that Morgan Stanley in some instances used its own more optimistic assumptions as a substitute for external pricing sources. “What that is saying is: ‘Fair value is what you want the value to be. Pick a number …’ That's especially troublesome.”

As indicated in the opening story, both the FASB and the IASB are assessing what is fair and what isn't when it comes to assigning valuations. Concerns over the issue caught fire after the collapses of Enron Corp. and other energy traders that abused the wide discretion given them under fair value accounting. Investors have expressed similar worries about some financial companies, which use internal—and subjectively designed—mathematical models to come up with valuations when market quotes aren't available. Similar concerns have been raised when companies revalue their debt obligations when they apply the fair value option.

Sources: Adapted from Susanne Craig and Jonathan Weil, “SEC Targets Morgan Stanley Values,” Wall Street Journal (November 8, 2004), p. C3; Floyd Norris, “Distortions in Baffling Financial Statements,” The New York Times (November 10, 2011); and Marie Leone, “The Fair Value Deadbeat Debate Returns,” CFO.com (June 25, 2009).

Trading Securities

Companies hold trading securities with the intention of selling them in a short period of time. “Trading” in this context means frequent buying and selling. Companies thus use trading securities to generate profits from short-term differences in price. Companies generally hold these securities for less than three months, some for merely days or hours.

Companies report trading securities at fair value, with unrealized holding gains and losses reported as part of net income. Similar to held-to-maturity or available-for-sale investments, companies are required to amortize any discount or premium. A holding gain or loss is the net change in the fair value of a security from one period to another, exclusive of dividend or interest revenue recognized but not received. In short, the FASB says to adjust the trading securities to fair value, at each reporting date. In addition, companies report the change in value as part of net income, not other comprehensive income.

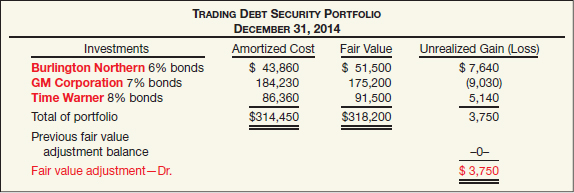

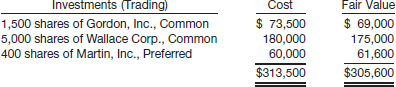

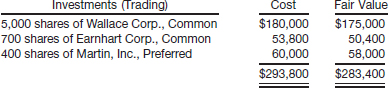

To illustrate, assume that on December 31, 2014, Western Publishing Corporation determined its trading securities portfolio to be as shown in Illustration 17-11. (Assume that 2014 is the first year that Western Publishing held trading securities.) At the date of acquisition, Western Publishing recorded these trading securities at cost, including brokerage commissions and taxes, in the account entitled Debt Investments. This is the first valuation of this recently purchased portfolio.

The total cost of Western Publishing's trading portfolio is $314,450. The gross unrealized gains are $12,780 ($7,640 + $5,140), and the gross unrealized losses are $9,030, resulting in a net unrealized gain of $3,750. The fair value of trading securities is $3,750 greater than its cost.

At December 31, Western Publishing makes an adjusting entry to a valuation allowance, referred to as Fair Value Adjustment (trading), to record the increase in value and to record the unrealized holding gain.

![]()

Because the Fair Value Adjustment account balance is a debit, Western Publishing adds it to the cost of the Debt Investments account to arrive at a fair value for the trading securities. Western Publishing reports this fair value amount on the balance sheet.

As with other debt investments, when a trading investment is sold, the Debt Investments account is reduced by the amount of the amortized cost of the bonds. Any realized gain or loss is recorded in the “Other expenses and losses” section of the income statement. The Fair Value Adjustment account is then adjusted at year-end for the unrealized gains or losses on the remaining securities in the trading investment portfolio.

When securities are actively traded, the FASB believes that the investments should be reported at fair value on the balance sheet. In addition, changes in fair value (unrealized gains and losses) should be reported in income. Such reporting on trading securities provides more relevant information to existing and prospective stockholders.

INVESTMENTS IN EQUITY SECURITIES

LEARNING OBJECTIVE ![]()

Identify the categories of equity securities and describe the accounting and reporting treatment for each category.

Equity securities represent ownership interests such as common, preferred, or other capital stock. They also include rights to acquire or dispose of ownership interests at an agreed-upon or determinable price, such as in warrants, rights, and call or put options. Companies do not treat convertible debt securities as equity securities. Nor do they treat as equity securities redeemable preferred stock (which must be redeemed for common stock). The cost of equity securities includes the purchase price of the security plus broker's commissions and other fees incidental to the purchase.

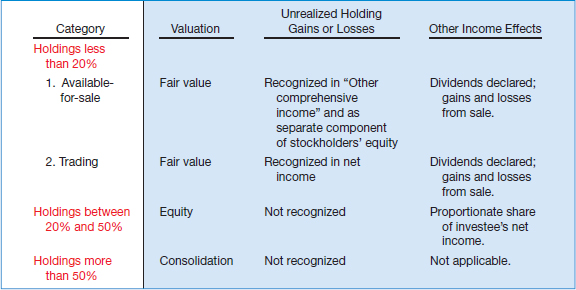

The degree to which one corporation (investor) acquires an interest in the common stock of another corporation (investee) generally determines the accounting treatment for the investment subsequent to acquisition. The classification of such investments depends on the percentage of the investee voting stock that is held by the investor:

- Holdings of less than 20 percent (fair value method)—investor has passive interest.

- Holdings between 20 percent and 50 percent (equity method)—investor has significant influence.

- Holdings of more than 50 percent (consolidated statements)—investor has controlling interest.

Illustration 17-12 lists these levels of interest or influence and the corresponding valuation and reporting method that companies must apply to the investment.

The accounting and reporting for equity securities therefore depend on the level of influence and the type of security involved, as shown in Illustration 17-13.

Holdings of Less Than 20%

When an investor has an interest of less than 20 percent, it is presumed that the investor has little or no influence over the investee. In such cases, if market prices are available subsequent to acquisition, the company values and reports the investment using the fair value method.6 The fair value method requires that companies classify equity securities at acquisition as available-for-sale securities or trading securities. Because equity securities have no maturity date, companies cannot classify them as held-to-maturity.

Available-for-Sale Securities

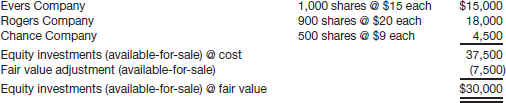

Upon acquisition, companies record available-for-sale securities at cost.7 To illustrate, assume that on November 3, 2014, Republic Corporation purchased common stock of three companies, each investment representing less than a 20 percent interest.

Republic records these investments as follows.

![]()

On December 6, 2014, Republic receives a cash dividend of $4,200 on its investment in the common stock of Campbell Soup Co. It records the cash dividend as follows.

![]()

All three of the investee companies reported net income for the year, but only Campbell Soup declared and paid a dividend to Republic. But, recall that when an investor owns less than 20 percent of the common stock of another corporation, it is presumed that the investor has relatively little influence on the investee. As a result, net income of the investee is not a proper basis for recognizing income from the investment by the investor. Why? Because the increased net assets resulting from profitable operations may be permanently retained for use in the investee's business. Therefore, the investor recognizes net income only when the investee declares cash dividends.

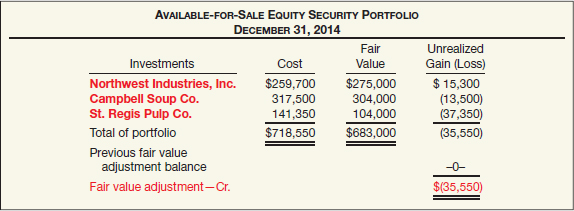

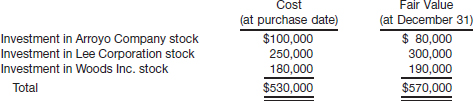

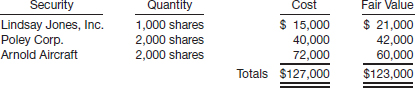

At December 31, 2014, Republic's available-for-sale equity security portfolio has the cost and fair value shown in Illustration 17-14.

ILLUSTRATION 17-14 Computation of Fair Value Adjustment—Available-for-Sale Equity Security Portfolio (2014)

For Republic's available-for-sale equity securities portfolio, the gross unrealized gains are $15,300, and the gross unrealized losses are $50,850 ($13,500 + $37,350), resulting in a net unrealized loss of $35,550. The fair value of the available-for-sale securities portfolio is below cost by $35,550.

As with available-for-sale debt securities, Republic records the net unrealized gains and losses related to changes in the fair value of available-for-sale equity securities in an Unrealized Holding Gain or Loss—Equity account. Republic reports this amount as a part of other comprehensive income and as a component of other accumulated comprehensive income (reported in stockholders' equity) until realized. In this case, Republic prepares an adjusting entry debiting the Unrealized Holding Gain or Loss—Equity account and crediting the Fair Value Adjustment account to record the decrease in fair value and to record the loss as follows.

![]()

On January 23, 2015, Republic sold all of its Northwest Industries, Inc. common stock receiving net proceeds of $287,220. Illustration 17-15 shows the computation of the realized gain on the sale.

Republic records the sale as follows.

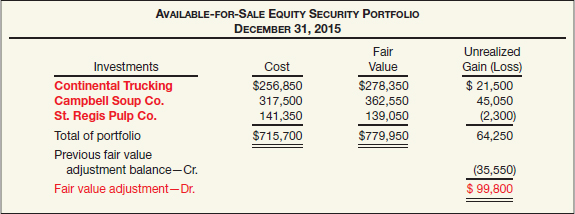

In addition, assume that on February 10, 2015, Republic purchased 20,000 shares of Continental Trucking at a market price of $12.75 per share plus brokerage commissions of $1,850 (total cost, $256,850).

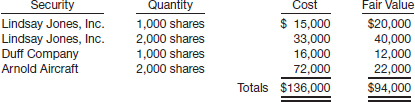

Illustration 17-16 lists Republic's portfolio of available-for-sale securities, as of December 31, 2015.

ILLUSTRATION 17-16 Computation of Fair Value Adjustment—Available-for-Sale Equity Security Portfolio (2015)

At December 31, 2015, the fair value of Republic's available-for-sale equity securities portfolio exceeds cost by $64,250 (unrealized gain). The Fair Value Adjustment account had a credit balance of $35,550 at December 31, 2015. To adjust its December 31, 2015, available-for-sale portfolio to fair value, the company debits the Fair Value Adjustment account for $99,800 ($35,550 + $64,250). Republic records this adjustment as follows.

![]()

Trading Securities

The accounting entries to record trading equity securities are the same as for available-for-sale equity securities, except for recording the unrealized holding gain or loss. For trading equity securities, companies report the unrealized holding gain or loss as part of net income. Thus, the account titled Unrealized Holding Gain or Loss—Income is used.

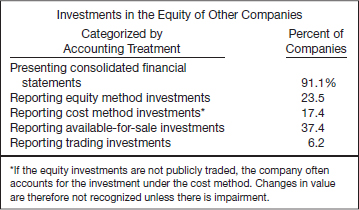

What do the numbers mean? MORE DISCLOSURE, PLEASE

How to account for investment securities is a particularly sensitive area, given the large amounts of equity investments involved. And presently companies report investments in equity securities at cost, equity, fair value, and full consolidation, depending on the circumstances. As a recent SEC study noted, “there are so many different accounting treatments for investments that it raises the question of whether they are all needed.”

Presented in the right-hand column is an estimate of the percentage of companies on the major exchanges that have investments in the equity of other entities.

As the table indicates, many companies have equity investments of some type. These investments can be substantial. For example, the total amount of equity-method investments appearing on company balance sheets is approximately $403 billion, and the amount shown in the income statements in any one year for all companies is approximately $38 billion.

Source: “Report and Recommendations Pursuant to Section 401(c) of the Sarbanes-Oxley Act of 2002 on Arrangements with Off-Balance Sheet Implications, Special Purpose Entities, and Transparency of Filings by Issuers,” United States Securities and Exchange Commission—Office of Chief Accountant, Office of Economic Analyses, Division of Corporation Finance (June 2005), pp. 36–39.

Holdings Between 20% and 50%

LEARNING OBJECTIVE ![]()

Explain the equity method of accounting and compare it to the fair value method for equity securities.

An investor corporation may hold an interest of less than 50 percent in an investee corporation and thus not possess legal control. However, an investment in voting stock of less than 50 percent can still give the investor the ability to exercise significant influence over the operating and financial policies of the investee company. [4] Significant influence may be indicated in several ways. Examples include representation on the board of directors, participation in policy-making processes, material intercompany transactions, interchange of managerial personnel, or technological dependency.

Another important consideration is the extent of ownership by an investor in relation to the concentration of other shareholdings. To achieve a reasonable degree of uniformity in application of the “significant influence” criterion, the profession concluded that an investment (direct or indirect) of 20 percent or more of the voting stock of an investee should lead to a presumption that in the absence of evidence to the contrary, an investor has the ability to exercise significant influence over an investee.8

In instances of “significant influence” (generally an investment of 20 percent or more), the investor must account for the investment using the equity method.

Equity Method

Under the equity method, the investor and the investee acknowledge a substantive economic relationship. The company originally records the investment at the cost of the shares acquired but subsequently adjusts the amount each period for changes in the investee's net assets. That is, the investor's proportionate share of the earnings (losses) of the investee periodically increases (decreases) the investment's carrying amount. All cash dividends received by the investor from the investee also decrease the investment's carrying amount. The equity method recognizes that investee's earnings increase investee's net assets, and that investee's losses and dividends decrease these net assets.

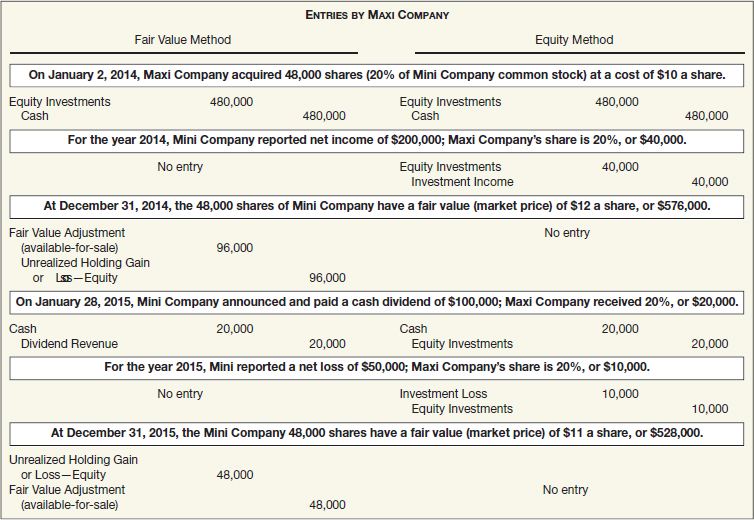

To illustrate the equity method and compare it with the fair value method, assume that Maxi Company purchases a 20 percent interest in Mini Company. To apply the fair value method in this example, assume that Maxi does not have the ability to exercise significant influence, and classifies the securities as available-for-sale. Where this example applies the equity method, assume that the 20 percent interest permits Maxi to exercise significant influence. Illustration 17-17 shows the entries.

Note that under the fair value method, Maxi reports as revenue only the cash dividends received from Mini. The earning of net income by Mini (the investee) is not considered a proper basis for recognition of income from the investment by Maxi (the investor). Why? Mini may permanently retain in the business any increased net assets resulting from its profitable operation. Therefore, Maxi only recognizes revenue when it receives dividends from Mini.

![]() International Perspective

International Perspective

IFRS has similar accounting rules for significant influence equity investments.

Under the equity method, Maxi reports as revenue its share of the net income reported by Mini. Maxi records the cash dividends received from Mini as a decrease in the investment carrying value. As a result, Maxi records its share of the net income of Mini in the year when it is recognized. With significant influence, Maxi can ensure that Mini will pay dividends, if desired, on any net asset increases resulting from net income. To wait until receiving a dividend ignores the fact that Maxi is better off if the investee has earned income.

Using dividends as a basis for recognizing income poses an additional problem. For example, assume that the investee reports a net loss. However, the investor exerts influence to force a dividend payment from the investee. In this case, the investor reports income, even though the investee is experiencing a loss. In other words, using dividends as a basis for recognizing income fails to report properly the economics of the situation.

For some companies, equity accounting can be a real pain to the bottom line. For example, Amazon.com, the pioneer of Internet retailing, at one time struggled to turn a profit. Furthermore, some of Amazon's equity investments had resulted in Amazon's earnings performance going from bad to worse. At one time, Amazon disclosed equity stakes in such companies as Altera International, Basis Technology, Drugstore.com, and Eziba.com. These equity investees reported losses that made Amazon's already bad bottom line even worse, accounting for up to 22 percent of its reported loss in one year alone.

Investee Losses Exceed Carrying Amount. If an investor's share of the investee's losses exceeds the carrying amount of the investment, should the investor recognize additional losses? Ordinarily, the investor should discontinue applying the equity method and not recognize additional losses.

If the investor's potential loss is not limited to the amount of its original investment (by guarantee of the investee's obligations or other commitment to provide further financial support) or if imminent return to profitable operations by the investee appears to be assured, the investor should recognize additional losses. [6]

Holdings of More Than 50%

When one corporation acquires a voting interest of more than 50 percent in another corporation, it is said to have a controlling interest. In such a relationship, the investor corporation is referred to as the parent and the investee corporation as the subsidiary. Companies present the investment in the common stock of the subsidiary as a long-term investment on the separate financial statements of the parent.

![]() International Perspective

International Perspective

In contrast to U.S. firms, financial statements of non-U.S. companies often include both consolidated (group) statements and parent company financial statements.

When the parent treats the investment as a subsidiary, the parent generally prepares consolidated financial statements. Consolidated financial statements treat the parent and subsidiary corporations as a single economic entity. (Advanced accounting courses extensively discuss the subject of when and how to prepare consolidated financial statements.) Whether or not consolidated financial statements are prepared, the parent company generally accounts for the investment in the subsidiary using the equity method as explained in the previous section of this chapter.

What do the numbers mean? WHO'S IN CONTROL HERE?

Molson Coors Brewing Company owns 42 percent of the MillerCoors' brewing venture operating in the United States and Puerto Rico. As part of the agreement, Molson helps the MillerCoors unit produce and sell its products in the U.S. and Puerto Rican markets. Lenovo Group owns a significant percentage (45 percent) of the shares of Beijing Lenovo Parasaga Information Technology Co. (which develops and distributes computer software). Beijing Lenovo is important to Lenovo because it develops and sells the software that is used with Lenovo computers. In return, Beijing Lenovo depends on Lenovo to provide the products that make its software and services valuable, as well as perform significant customer and market support. Indeed, it can be said that to some extent Lenovo controls Beijing Lenovo, which would likely not exist without the support of Lenovo.

As you have learned, because a company like Lenovo owns less than 50 percent of the shares, it does not consolidate Beijing Lenovo but instead accounts for its investment using the equity method. Under the equity method, Lenovo reports a single income item for its profits from Beijing Lenovo and only the net amount of its investment in the statement of financial position. Equity method accounting gives Lenovo a pristine statement of financial position and income statement, by separating the assets and liabilities and the profit margins of the related companies from its laptop-computer businesses.

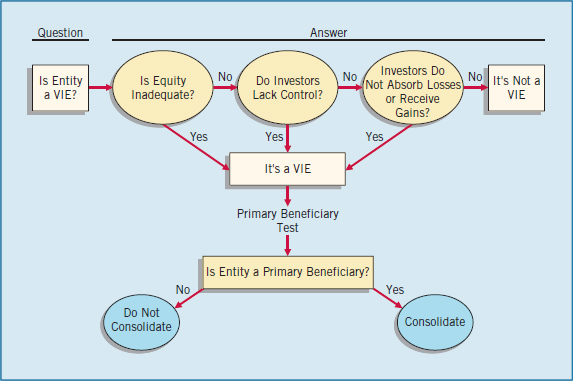

Some are critical of equity method accounting. They argue that some investees, like Beijing Lenovo, should be consolidated. The FASB has issued rules to consider other factors, in addition to voting interests, when determining whether an entity should be consolidated. We discuss these rules in Appendix 17B. The FASB has tightened up consolidation rules, so that companies will be more likely to consolidate more of their 20–50-percent-owned investments. Consolidation of entities, such as MillerCoors and Beijing Lenovo, is warranted if Molson and Lenovo effectively control their equity method investments.

ADDITIONAL MEASUREMENT ISSUES

Fair Value Option

LEARNING OBJECTIVE ![]()

Describe the accounting for the fair value option and for impairments of debt and equity investments.

As indicated in earlier chapters, companies have the option to report most financial instruments at fair value, with all gains and losses related to changes in fair value reported in the income statement. This option is applied on an instrument-by-instrument basis. The fair value option is generally available only at the time a company first purchases the financial asset or incurs a financial liability. If a company chooses to use the fair value option, it must measure this instrument at fair value until the company no longer has ownership.

For example, assume that Abbott Laboratories purchased debt securities in 2014 that it classified as held-to-maturity. Abbott does not choose to report this security using the fair value option. In 2015, Abbott buys another held-to-maturity debt security. Abbott decides to report this security using the fair value option. Once it chooses the fair value option for the security bought in 2015, the decision is irrevocable (may not be changed). In addition, Abbott does not have the option to value the held-to-maturity security purchased in 2014 at fair value in 2015 or in subsequent periods.

Many support the use of the fair value option as a step closer to total fair value reporting for financial instruments. They believe this treatment leads to an improvement in financial reporting. Others argue that the fair value option is confusing. A company can choose from period to period whether to use the fair value option for any new investment in a financial instrument. By permitting an instrument-by-instrument approach, companies are able to report some financial instruments at fair value but not others. To illustrate the accounting issues related to the fair value option, we discuss two different situations.

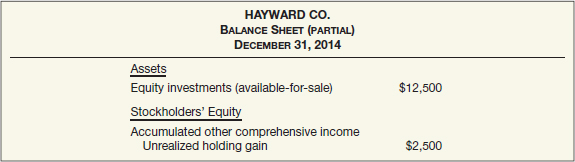

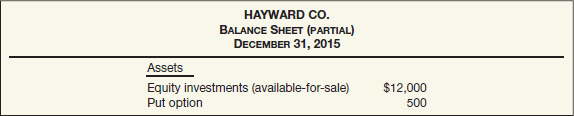

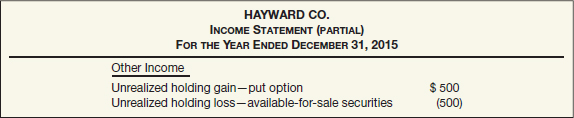

Available-for-Sale Securities

Available-for-sale securities are presently reported at fair value, with any unrealized gains and losses recorded as part of other comprehensive income. Assume that Hardy Company purchases stock in Fielder Company during 2014 that it classifies as available-for-sale. At December 31, 2014, the cost of this security is $100,000; its fair value at December 31, 2014, is $125,000. If Hardy chooses the fair value option to account for the Fielder Company stock, it makes the following entry at December 31, 2014.

![]()

In this situation, Hardy uses an account titled Equity Investments to record the change in fair value at December 31. It does not use a Fair Value Adjustment account because the accounting for a fair value option is on an investment-by-investment basis rather than on a portfolio basis. Because Hardy selected the fair value option, the unrealized gain or loss is recorded as part of net income. Hardy must continue to use the fair value method to record this investment until it no longer has ownership of the security.

Equity Method Investments

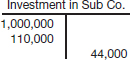

Companies may also use the fair value option for investments that otherwise follow the equity method of accounting. To illustrate, assume that Durham Company holds a 28 percent stake in Suppan Inc. Durham purchased the investment in 2014 for $930,000. At December 31, 2014, the fair value of the investment is $900,000. Durham elects to report the investment in Suppan using the fair value option. The entry to record this investment is as follows.

![]()

In contrast to equity method accounting, if the fair value option is chosen, Durham does not report its pro rata share of the income or loss from Suppan. In addition, any dividend payments are credited to Dividend Revenue and therefore do not reduce the Equity Investments account.

![]() International Perspective

International Perspective

IFRS does not allow the use of the fair value option for equity method investments. The FASB is considering a proposal to converge to IFRS in this area.

One major advantage of using the fair value option for this type of investment is that it addresses confusion about the equity method of accounting. In other words, what exactly does the one-line consolidation related to the equity method of accounting on the balance sheet tell investors? Many believe it does not provide information about liquidity or solvency, nor does it provide an indication of the worth of the company.

Evolving Issue FAIR VALUE CONTROVERSY

Evolving Issue FAIR VALUE CONTROVERSY

The reporting of investment securities is controversial. Some believe that all securities should be reported at fair value. Others believe they all should be stated at amortized cost. Still others favor the present approach. Here are some of the major unresolved issues:

- Measurement based on intent. Companies classify debt securities as held-to-maturity, available-for-sale, or trading. As a result, companies can report three identical debt securities in three different ways in the financial statements. Some argue such treatment is confusing. Furthermore, the held-to-maturity category relies on intent, a subjective evaluation. What is not subjective is the fair value of the debt instrument. In other words, the three classifications are subjective, resulting in arbitrary classifications.

- Gains trading. Companies can classify certain debt securities as held-to-maturity and therefore report them at amortized cost. Companies can classify other debt and equity securities as available-for-sale and report them at fair value, with the unrealized gain or loss reported as other comprehensive income. In either case, a company can become involved in “gains trading” (also referred to as “cherry picking,” “snacking,” or “sell the best and keep the rest”). In gains trading, companies sell their “winners,” reporting the gains in income, and hold on to the losers.

- Liabilities not fairly valued. Many argue that if companies report investment securities at fair value, they also should report liabilities at fair value. Why? By recognizing changes in value on only one side of the balance sheet (the asset side), a high degree of volatility can occur in the income and stockholders' equity amounts. Further, financial institutions are involved in asset and liability management (not just asset management). Viewing only one side may lead managers to make uneconomic decisions as a result of the accounting. The fair value option may address this concern to some extent. However, there is debate on the usefulness of fair value estimates for liabilities.

Impairment of Value

A company should evaluate every investment, at each reporting date, to determine if it has suffered impairment—a loss in value that is other than temporary. For example, if an investee experiences a bankruptcy or a significant liquidity crisis, the investor may suffer a permanent loss. If the decline is judged to be other than temporary, a company writes down the cost basis of the individual security to a new cost basis. The company accounts for the write-down as a realized loss. Therefore, it includes the amount in net income.

For debt securities, a company uses the impairment test to determine whether “it is probable that the investor will be unable to collect all amounts due according to the contractual terms.”

For equity securities, the guideline is less precise. Any time realizable value is lower than the carrying amount of the investment, a company must consider an impairment. Factors involved include the length of time and the extent to which the fair value has been less than cost, the financial condition and near-term prospects of the issuer, and the intent and ability of the investor company to retain its investment to allow for any anticipated recovery in fair value.

To illustrate an impairment, assume that Strickler Company holds available-for-sale bond securities with a par value and amortized cost of $1 million. The fair value of these securities is $800,000. Strickler has previously reported an unrealized loss on these securities of $200,000 as part of other comprehensive income. In evaluating the securities, Strickler now determines that it probably will not collect all amounts due. In this case, it reports the unrealized loss of $200,000 as a loss on impairment of $200,000. Strickler includes this amount in income, with the bonds stated at their new cost basis. It records this impairment as follows.

![]()

The new cost basis of the investment in debt securities is $800,000. Strickler includes subsequent increases and decreases in the fair value of impaired available-for-sale securities as other comprehensive income.9

Companies base impairment for debt and equity securities on a fair value test. This test differs slightly from the impairment test for loans that we discuss in Appendix 7B. The FASB rejected the discounted cash flow alternative for securities because of the availability of market price information.10

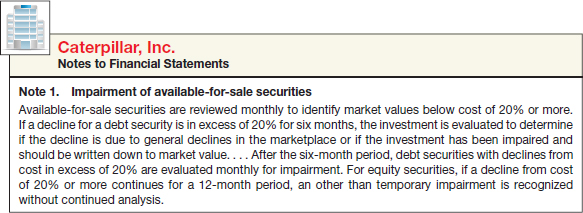

An example of the criteria used by Caterpillar to assess impairment is provided in Illustration 17-18.

RECLASSIFICATIONS AND TRANSFERS

Reclassification Adjustments

LEARNING OBJECTIVE ![]()

Describe the reporting of reclassification adjustments and the accounting for transfers between categories.

As we indicated in Chapter 4, companies report changes in unrealized holding gains and losses related to available-for-sale securities as part of other comprehensive income. Companies may display the components of other comprehensive income in one of two ways: (1) in a combined statement of income and comprehensive income, or (2) in a separate statement of comprehensive income that begins with net income.

The reporting of changes in unrealized gains or losses in comprehensive income is straightforward unless a company sells securities during the year. In that case, double-counting results when the company reports realized gains or losses as part of net income but also shows the amounts as part of other comprehensive income in the current period or in previous periods.

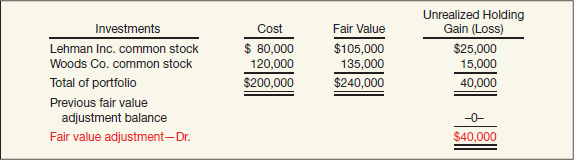

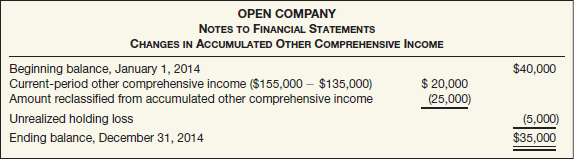

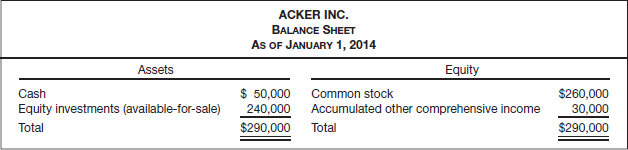

To ensure that gains and losses are not counted twice when a sale occurs, a reclassification adjustment is necessary. To illustrate, assume that Open Company has the following two available-for-sale securities in its portfolio at the end of 2013 (its first year of operations).

The entry to record the unrealized holding gain in 2013 is as follows.

![]()

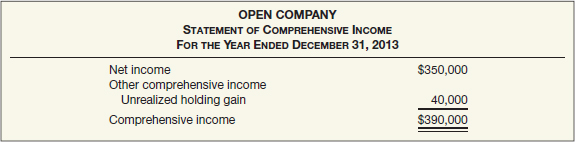

If Open Company reports net income in 2013 of $350,000, it presents a statement of comprehensive income as follows.

At December 31, 2013, Open Company reports on its balance sheet equity investments of $240,000 (cost $200,000 plus fair value adjustment of $40,000) and accumulated other comprehensive income in stockholders' equity of $40,000. The entry to transfer the unrealized holding gain—equity to accumulated other comprehensive income is as follows.

![]()

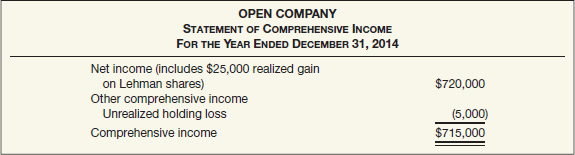

In 2014, Open Company sells its Lehman Inc. common stock for $105,000 and realizes a gain on the sale of $25,000 ($105,000 − $80,000). The journal entry to record this transaction is as follows.

![]()

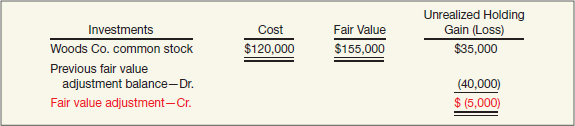

At the end of 2014, the fair value of the Woods Co. common stock increased an additional $20,000 ($155,000 − $135,000), to $155,000. Illustration 17-21 shows the computation of the change in the Fair Value Adjustment account (based on only the Woods Co. investment).

The entry to record the unrealized holding gain in 2014 is as follows.

![]()

If we assume that Open Company reports net income of $720,000 in 2014, including the realized sale on the Lehman stock, its income statement is presented as shown in Illustration 17-22.

At December 31, 2014, Open Company reports on its balance sheet equity investments of $155,000 (cost $120,000 plus a fair value adjustment of $35,000) and accumulated other comprehensive income in stockholders' equity of $35,000 ($40,000 − $5,000). The entry to transfer the unrealized holding loss—equity to accumulated other comprehensive income is as follows.

![]()

In 2013, Open included the unrealized gain on the Lehman Co. common stock in comprehensive income. In 2014, Open sold the stock. It reported the realized gain ($25,000) in net income, which increased comprehensive income again. To avoid double-counting this gain, Open makes a reclassification adjustment to eliminate the realized gain from the computation of comprehensive income in 2014.

This reclassification adjustment may be made in the income statement, in accumulated other comprehensive income or in a note to the financial statements. The FASB prefers to show the reclassification amount in accumulated other comprehensive income in the notes to the financial statements.11 For Open Company, this presentation is as shown in Illustration 17-23.

Comprehensive Example

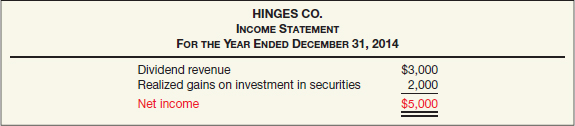

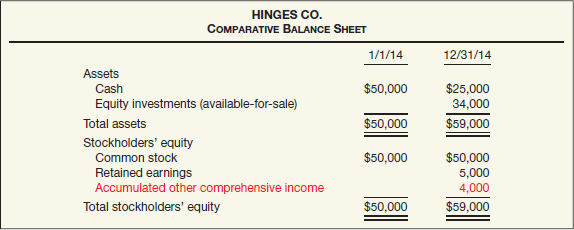

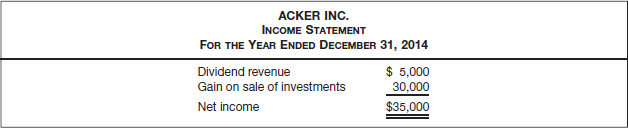

To provide a single-period example of the reporting of investment securities and related gain or loss on available-for-sale securities, assume that on January 1, 2014, Hinges Co. had cash and common stock of $50,000.12 At that date, the company had no other asset, liability, or equity balance. On January 2, Hinges purchased for cash $50,000 of equity securities classified as available-for-sale. On June 30, Hinges sold part of the available-for-sale security portfolio, realizing a gain as shown in Illustration 17-24.

Hinges did not purchase or sell any other securities during 2014. It received $3,000 in dividends during the year. At December 31, 2014, the remaining portfolio is as shown in Illustration 17-25.

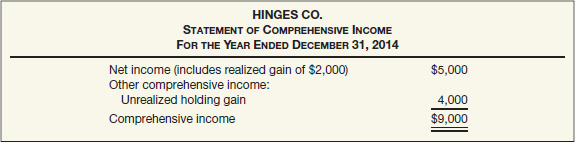

Illustration 17-26 shows the company's income statement for 2014.

The company reports its change in the unrealized holding gain in a statement of comprehensive income as follows.

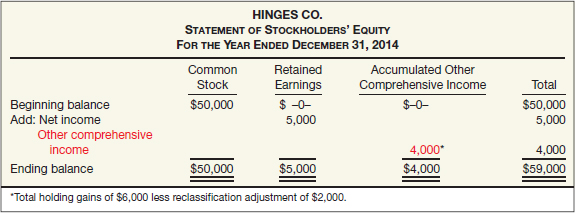

Its statement of stockholders' equity appears in Illustration 17-28.

The comparative balance sheet is shown below in Illustration 17-29.

This example indicates how an unrealized gain or loss on available-for-sale securities affects all the financial statements. Note that a company must disclose the components that comprise accumulated other comprehensive income.

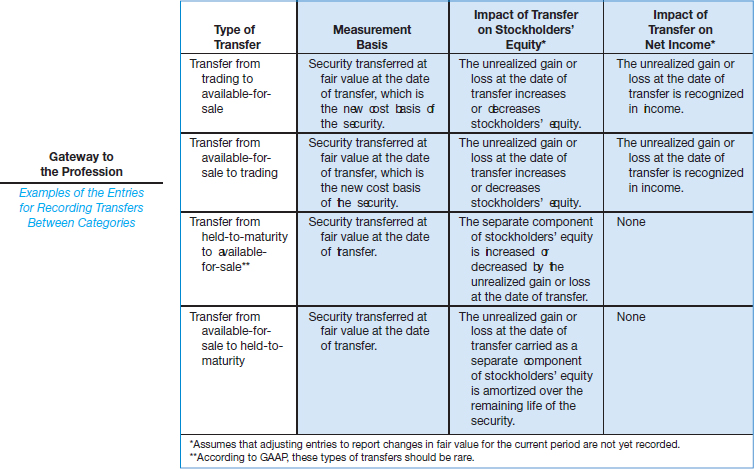

Transfers Between Categories

Companies account for transfers between any of the categories at fair value. Thus, if a company transfers available-for-sale securities to held-to-maturity investments, it records the new investments (held-to-maturity) at the date of transfer at fair value in the new category. Similarly, if it transfers held-to-maturity investments to available-for-sale investments, it records the new investments (available-for-sale) at fair value. This fair value rule assures that a company cannot omit recognition of fair value simply by transferring securities to the held-to-maturity category. Illustration 17-30 summarizes the accounting treatment for transfers.

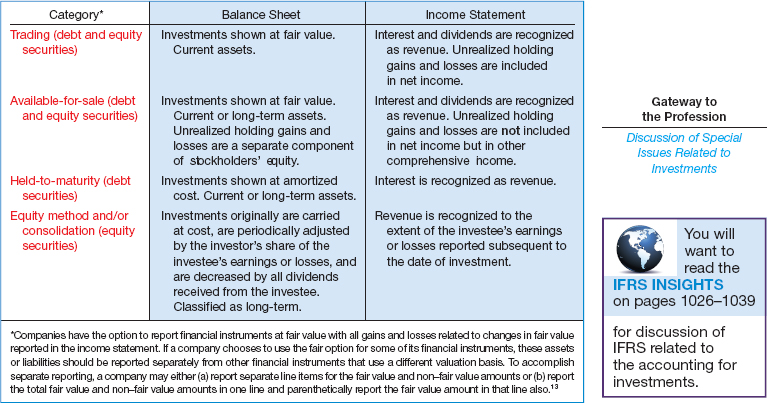

Summary of Reporting Treatment of Securities

Illustration 17-31 summarizes the major debt and equity securities and their reporting treatment.

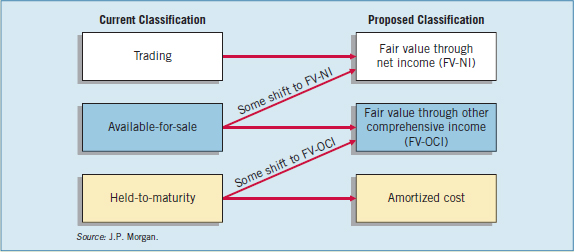

Evolving Issue CLASSIFICATION AND MEASUREMENT—THE LONG ROAD

As discussed in the opening story, the FASB and IASB have been on divergent approaches to financial instrument classification and measurement. These differences have narrowed recently with the decision to permit a “Fair Value through Other Comprehensive Income” category for some debt instruments. The following table summarizes the agreed-upon approach in comparison to current GAAP.

As indicated, under the new model, there will still be three “buckets” although the proportions of financial instruments within the new classifications will change. For example, the FV-NI category will likely be larger than the current trading category because publicly traded companies will likely be required to classify all equity securities (both marketable and nonmarketable) in FV-NI. Currently, companies are able to classify some equities in the available-for-sale category if particular criteria are met. To the extent a company has traditionally classified a large portion of its equity securities in the available-for-sale category, more equity instruments accounted for in the FV-NI category could create more net income volatility than under current GAAP.

The FV-OCI category may be larger or smaller than a company's current available-for-sale category. On the one hand, equities will no longer be eligible for classification in this category, which will make it smaller. On the other hand, some instruments that are currently classified as held-to-maturity will not be eligible for amortized cost classification and instead will end up being moved into the FV-OCI category.

For most companies, the amortized cost category generally will be smaller than the current held-to-maturity category because securities will no longer be eligible for classification in this category. Our expectation is that most of the instruments that will no longer meet the eligibility criteria for amortized cost accounting will likely move to the FV-OCI category.

The FASB is expected to issue a revised proposal in 2013. The IASB has specified that a revised IFRS 9 will be effective for annual periods beginning on or after January 1, 2015.

Source: Adapted from D. Mott, “FASB and IASB Come Together on the Classification and Measurement of Debt Instruments,” Global Equity Research—Accounting Issues, J.P. Morgan (25 May 2012).

KEY TERMS

amortized cost, 953

available-for-sale securities, 952

consolidated financial statements, 966

controlling interest, 966

debt securities, 952

effective-interest method, 954

equity method, 965

equity securities, 960

exchange for noncash consideration, 962(n)

fair value, 953

Fair Value Adjustment, 957

fair value method, 961

gains trading, 959

held-to-maturity securities, 952

holding gain or loss, 959

impairment, 969

investee, 961

investor, 961

parent, 966

reclassification adjustment, 970

security, 952(n)

significant influence, 964

subsidiary, 966

trading securities, 952

SUMMARY OF LEARNING OBJECTIVES

![]() Identify the three categories of debt securities and describe the accounting and reporting treatment for each category. (1) Carry and report held-to-maturity debt securities at amortized cost. (2) Value trading debt securities for reporting purposes at fair value, with unrealized holding gains or losses included in net income. (3) Value available-for-sale debt securities for reporting purposes at fair value, with unrealized holding gains or losses reported as other comprehensive income and as a separate component of stockholders' equity.

Identify the three categories of debt securities and describe the accounting and reporting treatment for each category. (1) Carry and report held-to-maturity debt securities at amortized cost. (2) Value trading debt securities for reporting purposes at fair value, with unrealized holding gains or losses included in net income. (3) Value available-for-sale debt securities for reporting purposes at fair value, with unrealized holding gains or losses reported as other comprehensive income and as a separate component of stockholders' equity.

![]() Understand the procedures for discount and premium amortization on bond investments. Similar to bonds payable, companies should amortize discount or premium on bond investments using the effective-interest method. They apply the effective-interest rate or yield to the beginning carrying value of the investment for each interest period in order to compute interest revenue.

Understand the procedures for discount and premium amortization on bond investments. Similar to bonds payable, companies should amortize discount or premium on bond investments using the effective-interest method. They apply the effective-interest rate or yield to the beginning carrying value of the investment for each interest period in order to compute interest revenue.

![]() Identify the categories of equity securities and describe the accounting and reporting treatment for each category. The degree to which one corporation (investor) acquires an interest in the common stock of another corporation (investee) generally determines the accounting treatment for the investment. Long-term investments by one corporation in the common stock of another can be classified according to the percentage of the voting stock of the investee held by the investor.

Identify the categories of equity securities and describe the accounting and reporting treatment for each category. The degree to which one corporation (investor) acquires an interest in the common stock of another corporation (investee) generally determines the accounting treatment for the investment. Long-term investments by one corporation in the common stock of another can be classified according to the percentage of the voting stock of the investee held by the investor.

![]() Explain the equity method of accounting and compare it to the fair value method for equity securities. Under the equity method, the investor and the investee acknowledge a substantive economic relationship. The company originally records the investment at cost but subsequently adjusts the amount each period for changes in the net assets of the investee. That is, the investor's proportionate share of the earnings (losses) of the investee periodically increases (decreases) the investment's carrying amount. All dividends received by the investor from the investee decrease the investment's carrying amount. Under the fair value method, a company reports the equity investment at fair value each reporting period irrespective of the investee's earnings or dividends paid to it. A company applies the equity method to investment holdings between 20 percent and 50 percent of ownership. It applies the fair value method to holdings below 20 percent.

Explain the equity method of accounting and compare it to the fair value method for equity securities. Under the equity method, the investor and the investee acknowledge a substantive economic relationship. The company originally records the investment at cost but subsequently adjusts the amount each period for changes in the net assets of the investee. That is, the investor's proportionate share of the earnings (losses) of the investee periodically increases (decreases) the investment's carrying amount. All dividends received by the investor from the investee decrease the investment's carrying amount. Under the fair value method, a company reports the equity investment at fair value each reporting period irrespective of the investee's earnings or dividends paid to it. A company applies the equity method to investment holdings between 20 percent and 50 percent of ownership. It applies the fair value method to holdings below 20 percent.

![]() Describe the accounting for the fair value option and for impairments of debt and equity investments. Companies have the option to report most financial instruments at fair value, with all gains and losses related to changes in fair value reported in the income statement. This option is applied on an instrument-by-instrument basis. The fair value option is generally available only at the time a company first purchases the financial asset or incurs a financial liability. If a company chooses to use the fair value option, it must measure this instrument at fair value until the company no longer has ownership.

Describe the accounting for the fair value option and for impairments of debt and equity investments. Companies have the option to report most financial instruments at fair value, with all gains and losses related to changes in fair value reported in the income statement. This option is applied on an instrument-by-instrument basis. The fair value option is generally available only at the time a company first purchases the financial asset or incurs a financial liability. If a company chooses to use the fair value option, it must measure this instrument at fair value until the company no longer has ownership.

Impairments of debt and equity securities are losses in value that are determined to be other than temporary, are based on a fair value test, and are charged to income.

![]() Describe the reporting of reclassification adjustments and the accounting for transfers between categories. A company needs a reclassification adjustment when it reports realized gains or losses as part of net income but also shows the amounts as part of other comprehensive income in the current or in previous periods. Companies should report unrealized holding gains or losses related to available-for-sale securities in other comprehensive income and the aggregate balance as accumulated comprehensive income on the balance sheet.

Describe the reporting of reclassification adjustments and the accounting for transfers between categories. A company needs a reclassification adjustment when it reports realized gains or losses as part of net income but also shows the amounts as part of other comprehensive income in the current or in previous periods. Companies should report unrealized holding gains or losses related to available-for-sale securities in other comprehensive income and the aggregate balance as accumulated comprehensive income on the balance sheet.

Transfers of securities between categories of investments should be accounted for at fair value, with unrealized holding gains or losses treated in accordance with the nature of the transfer.

APPENDIX 17A ACCOUNTING FOR DERIVATIVE INSTRUMENTS

LEARNING OBJECTIVE ![]()

Describe the uses of and accounting for derivatives.

Until the early 1970s, most financial managers worked in a cozy, if unthrilling, world. Since then, constant change caused by volatile markets, new technology, and deregulation has increased the risks to businesses. In response, the financial community developed products to manage these risks.

These products—called derivative financial instruments or simply derivatives—are useful for managing risk. Companies use the fair values or cash flows of these instruments to offset the changes in fair values or cash flows of the at-risk assets. The development of powerful computing and communication technology has aided the growth in derivative use. This technology provides new ways to analyze information about markets as well as the power to process high volumes of payments.

DEFINING DERIVATIVES

In order to understand derivatives, consider the following examples.

Example 1—Forward Contract. Assume that a company like Dell believes that the price of Google's stock will increase substantially in the next 3 months. Unfortunately, it does not have the cash resources to purchase the stock today. Dell therefore enters into a contract with a broker for delivery of 10,000 shares of Google stock in 3 months at the price of $110 per share.

Dell has entered into a forward contract, a type of derivative. As a result of the contract, Dell has received the right to receive 10,000 shares of Google stock in 3 months. Further, it has an obligation to pay $110 per share at that time. What is the benefit of this derivative contract? Dell can buy Google stock today and take delivery in 3 months. If the price goes up, as it expects, Dell profits. If the price goes down, Dell loses.

Example 2—Option Contract. Now suppose that Dell needs 2 weeks to decide whether to purchase Google stock. It therefore enters into a different type of contract, one that gives it the right to purchase Google stock at its current price any time within the next 2 weeks. As part of the contract, the broker charges $3,000 for holding the contract open for 2 weeks at a set price.

Dell has now entered into an option contract, another type of derivative. As a result of this contract, it has received the right but not the obligation to purchase this stock. If the price of the Google stock increases in the next 2 weeks, Dell exercises its option. In this case, the cost of the stock is the price of the stock stated in the contract, plus the cost of the option contract. If the price does not increase, Dell does not exercise the contract but still incurs the cost for the option.

The forward contract and the option contract both involve a future delivery of stock. The value of the contract relies on the underlying asset—the Google stock. Thus, these financial instruments are known as derivatives because they derive their value from values of other assets (e.g., stocks, bonds, or commodities). Or, put another way, their value relates to a market-determined indicator (e.g., stock price, interest rates, or the Standard and Poor's 500 stock composite index).

In this appendix, we discuss the accounting for three different types of derivatives:

- Financial forwards or financial futures.

- Options.

- Swaps.

WHO USES DERIVATIVES, AND WHY?

Whether to protect for changes in interest rates, the weather, stock prices, oil prices, or foreign currencies, derivative contracts help to smooth the fluctuations caused by various types of risks. A company that wants to ensure against certain types of business risks often uses derivative contracts to achieve this objective.14

Producers and Consumers

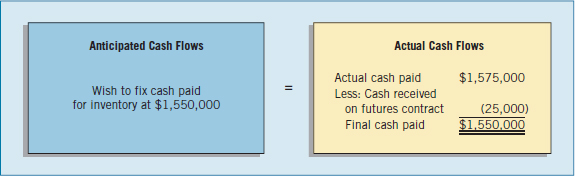

To illustrate, assume that Heartland Ag is a large producer of potatoes for the consumer market. The present price for potatoes is excellent. Unfortunately, Heartland needs two months to harvest its potatoes and deliver them to the market. Because Heartland expects the price of potatoes to drop in the coming months, it signs a forward contract. It agrees to sell its potatoes today at the current market price for delivery in 2 months.

Who would buy this contract? Suppose on the other side of the contract is McDonald's Corporation. McDonald's wants to have potatoes (for French fries) in 2 months and believes that prices will increase. McDonald's is therefore agreeable to accepting delivery in 2 months at current prices. It knows that it will need potatoes in 2 months and that it can make an acceptable profit at this price level.

In this situation, if the price of potatoes increases before delivery, Heartland loses and McDonald's wins. Conversely, if the price decreases, Heartland wins and McDonald's loses. However, the objective is not to gamble on the outcome. Regardless of which way the price moves, both Heartland and McDonald's have received a price at which they obtain an acceptable profit. In this case, although Heartland is a producer and McDonald's is a consumer, both companies are hedgers. They both hedge their positions to ensure an acceptable financial result.

Commodity prices are volatile. They depend on weather, crop production, and general economic conditions. For the producer and the consumer to plan effectively, it makes good sense to lock in specific future revenues or costs in order to run their businesses successfully.

Speculators and Arbitrageurs

In some cases, instead of McDonald's taking a position in the forward contract, a speculator may purchase the contract from Heartland. The speculator bets that the price of potatoes will rise, thereby increasing the value of the forward contract. The speculator, who may be in the market for only a few hours, will then sell the forward contract to another speculator or to a company like McDonald's.

Arbitrageurs also use derivatives. These market players attempt to exploit inefficiencies in markets. They seek to lock in profits by simultaneously entering into transactions in two or more markets. For example, an arbitrageur might trade in a futures contract. At the same time, the arbitrageur will also trade in the commodity underlying the futures contract, hoping to achieve small price gains on the difference between the two. Markets rely on speculators and arbitrageurs to keep the market liquid on a daily basis.

In these illustrations, we explained why Heartland (the producer) and McDonald's (the consumer) would become involved in a derivative contract. Consider other types of situations that companies face.

- Airlines, like Delta, Southwest, and United, are affected by changes in the price of jet fuel.

- Financial institutions, such as Citigroup, Bankers Trust, and BMO Harris, are involved in borrowing and lending funds that are affected by changes in interest rates.

- Multinational corporations, like Cisco Systems, Coca-Cola, and General Electric, are subject to changes in foreign exchange rates.

In fact, most corporations are involved in some form of derivatives transactions. Companies give these reasons (in their annual reports) as to why they use derivatives:

- ExxonMobil uses derivatives to hedge its exposure to fluctuations in interest rates, foreign currency exchange rates, and hydrocarbon prices.

- Caterpillar uses derivatives to manage foreign currency exchange rates, interest rates, and commodity price exposure.

- Johnson & Johnson uses derivatives to manage the impact of interest rate and foreign exchange rate changes on earnings and cash flows.

Many corporations use derivatives extensively and successfully. However, derivatives can be dangerous. All parties involved must understand the risks and rewards associated with these contracts.15

BASIC PRINCIPLES IN ACCOUNTING FOR DERIVATIVES

The FASB concluded that derivatives such as forwards and options are assets and liabilities. It also concluded that companies should report them in the balance sheet at fair value.16 The Board believes that fair value will provide statement users the best information about derivatives. Relying on some other basis of valuation for derivatives, such as historical cost, does not make sense. Why? Because many derivatives have a historical cost of zero. Furthermore, the markets for derivatives, and the assets upon which derivatives' values rely, are well developed. As a result, the Board believes that companies can determine reliable fair value amounts for derivatives.17

On the income statement, a company should recognize any unrealized gain or loss in income, if it uses the derivative for speculation purposes. If using the derivative for hedging purposes, the accounting for any gain or loss depends on the type of hedge used. We discuss the accounting for hedged transactions later in the appendix.

In summary, companies follow these guidelines in accounting for derivatives.

- Recognize derivatives in the financial statements as assets and liabilities.

- Report derivatives at fair value.

- Recognize gains and losses resulting from speculation in derivatives immediately in income.

- Report gains and losses resulting from hedge transactions differently, depending on the type of hedge.

Example of Derivative Financial Instrument—Speculation

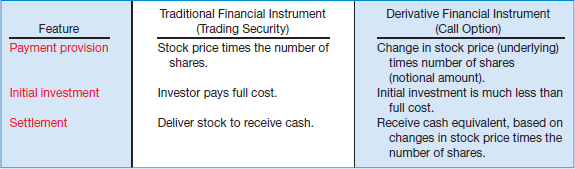

To illustrate the measurement and reporting of a derivative for speculative purposes, we examine a derivative whose value depends on the market price of Laredo Inc. common stock. A company can realize a gain from the increase in the value of the Laredo shares with the use of a derivative, such as a call option.18 A call option gives the holder the right, but not the obligation, to buy shares at a preset price. This price is often referred to as the strike price or the exercise price.

For example, assume a company enters into a call option contract with Baird Investment Co., which gives it the option to purchase Laredo stock at $100 per share.19 If the price of Laredo stock increases above $100, the company can exercise this option and purchase the shares for $100 per share. If Laredo's stock never increases above $100 per share, the call option is worthless.

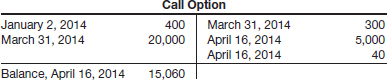

Accounting Entries. To illustrate the accounting for a call option, assume that the company purchases a call option contract on January 2, 2014, when Laredo shares are trading at $100 per share. The contract gives it the option to purchase 1,000 shares (referred to as the notional amount) of Laredo stock at an option price of $100 per share. The option expires on April 30, 2014. The company purchases the call option for $400 and makes the following entry.

![]()

This payment is referred to as the option premium. It is generally much less than the cost of purchasing the shares directly. The option premium consists of two amounts: (1) intrinsic value and (2) time value. Illustration 17A-1 shows the formula to compute the option premium.

Intrinsic value is the difference between the market price and the preset strike price at any point in time. It represents the amount realized by the option holder, if exercising the option immediately. On January 2, 2014, the intrinsic value is zero because the market price equals the preset strike price.

Time value refers to the option's value over and above its intrinsic value. Time value reflects the possibility that the option has a fair value greater than zero. How? Because there is some expectation that the price of Laredo shares will increase above the strike price during the option term. As indicated, the time value for the option is $400.20

The following additional data are available with respect to the call option.

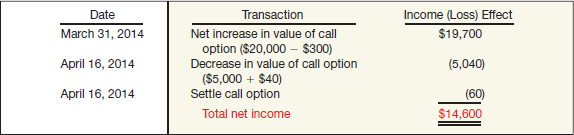

As indicated, on March 31, 2014, the price of Laredo shares increases to $120 per share. The intrinsic value of the call option contract is now $20,000. That is, the company can exercise the call option and purchase 1,000 shares from Baird Investment for $100 per share. It can then sell the shares in the market for $120 per share. This gives the company a gain of $20,000 ($120,000 − $100,000) on the option contract.21 It records the increase in the intrinsic value of the option as follows.

![]()

A market appraisal indicates that the time value of the option at March 31, 2014, is $100.22 The company records this change in value of the option as follows.

![]()

At March 31, 2014, the company reports the call option in its balance sheet at fair value of $20,100.23 The unrealized holding gain increases net income for the period. The loss on the time value of the option decreases net income.