![]()

CHAPTER 13

![]()

Marketing Funds Globally and Marketing Global Funds

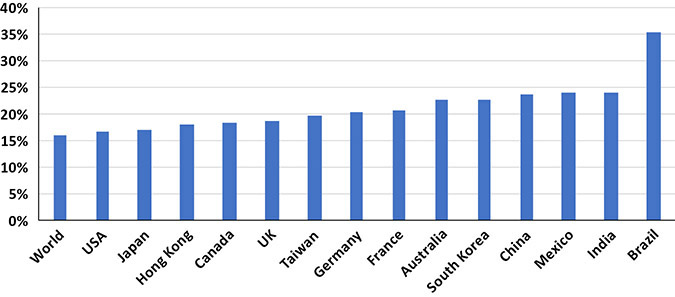

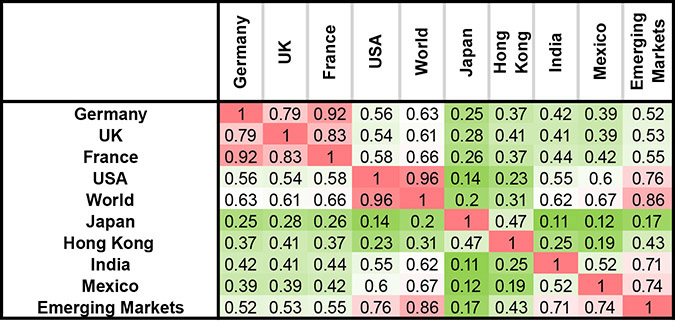

Capital is fungible, and it flows to the place of greatest return wherever in the world it might be. Risks, regulations, and diversification considerations act as barriers for the free flow of capital. For those accepting capital, the source is secondary to the need for capital. LPs allocate capital to maximize their returns within the constraints of their risk appetite, liquidity needs, and regulatory constraints. Empirical evidence bears testimony to the risk reduction benefit of global diversification. Even for the United States, which enjoys the lowest volatility of returns for any single country (see Figure 13.1), there is value in global diversification as it lowers overall portfolio volatility, irrespective of the higher returns sought by such portfolios (see Figure 13.2).

FIGURE 13.1 Volatility of returns by market

Source: Authors’ analysis using InvestSpy Calculator using Performance for country ETFs by iShares

FIGURE 13.2 Correlation Matrix for Stock Market Returns by Country (February 3, 2012–December 27, 2019)

Source: Authors’ analysis using InvestSpy Calculator

Data: Performance for iShares benchmark ETFs by country/market

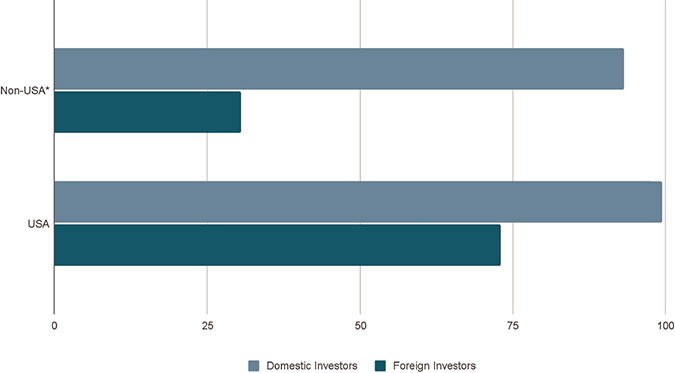

Yet most LPs are likely to exhibit a preference for their home country (see Figure 13.3). They, like most people, show signs of familiarity bias.1, 2 LPs are more familiar with the investment options and risks at home. Investing in another country, on the other hand, necessitates learning about a region that might be quite different from their own, with its own peculiar opportunities, risks, regulatory regimes, and systemic issues. Most GPs also could be deterred by the cost of opening a local office abroad. At the minimum, these factors serve as a barrier to optimal exposure, if not a barrier to entry, to foreign investments.

FIGURE 13.3 Share of investors’ portfolios in issuers’ currencies

Source: https://www.nber.org/reporter/2021number1/global-capital-allocation-project

The United States is an outlier in that it attracts global investors despite the home-country bias of foreign LPs. America is seen as a safe haven for capital, with its adherence to the rule of law and democratic government with checks and balances, stable financial and banking system, the world’s most popular reserve currency, a largely free market economy, and a plethora of investment opportunities. Such a unique confluence of beneficial factors for investors is rarely seen elsewhere in the world.

Other countries, especially developing economies, install high barriers to entry with constraining regulations for foreign investors and capital controls. In this context, how are GPs to seek capital from foreign LPs? It is a burning issue for many, especially emerging GPs who cannot afford to invest their limited marketing budget chasing after low probability targets.

CULTURE MEETS STRATEGY

Understanding culture is a key aspect of global marketing, and marketing alternatives is no exception. When US LPs meet with foreign GPs, cultural dynamics can be the deciding factor in who gets an allocation. For example, GPs from countries with a culture of hierarchy often assume the same hierarchy exists at LP firms, which can be a grave mistake. They fail to understand that in organizations with flat structures, the decisions are rarely top-down and are often bottom-up, with decision makers acting as judges and enablers instead of pushing their decisions down the chain. Without this cultural context, their actions, even in trivial social or office settings, might alienate a potential investor.

In 2008, a US institutional investor was on a due-diligence trip to Asia. During a meeting with a well-known GP, the US team observed the manager’s unhealthy team dynamics. The portfolio manager displayed his sense of entitlement when he grabbed a cup of water that the head of investor relations poured for himself, without any acknowledgment or thank you. Such entitled behavior was the last nail in the coffin, and the US team walked away.

American GPs could fall into the same trap. You will be well served to understand the cultural context of the foreign LP’s due-diligence meetings. In the United States, it is a good practice to address the presentation to everyone at the meeting, even if the decision maker is the focus of the pitch. Ensure everyone in the room feels important, because people you might least expect could be pivotal to the decision.

On the other hand, the egalitarian approach might not work in regions where hierarchy is part of the culture. The GP could offend foreign LPs who feel they were not treated with enough respect. In addition to honing their pitch, GPs and marketers also should learn to read the room to see how the rest of the foreign team treats the decision maker. If they are deferential, focus your pitch on that person.

Take another example: punctuality. Some cultures have a more casual attitude toward punctuality, while others see it as a mark of professionalism. Find out what the cultural norm is and adapt. Employing a “buffer time” when investors expect meetings to start and end on time, or vice versa, could end up in disaster. GPs with buffer-time expectations will learn a costly lesson where punctuality is obligatory.

While one can find LPs worldwide, there are regions where investors in global funds tend to congregate. The United States is an obvious one, as it is the largest market for alternatives and has a fairly large number of LPs with holdings abroad, who understand the value and risk of investing in assets overseen by foreign GPs. Canada is another such region, with its huge concentration of large pension and sovereign wealth funds; Europe is a region of LP concentration with its wealth management, and SFOs and MFOs. The Middle East has the world’s largest concentration of sovereign wealth funds; Asia is also home to sovereign wealth funds and large family offices. Australia–New Zealand are known for their superannuation funds.

With such opportunities around the globe, where should a GP focus? Since time and resources are practical constraints, prioritize the home market for your marketing efforts, and then regions where there is a high probability of complementary strategy and check size. Only after excelling at these markets—handling operations well and backed by the right resources—should GPs look at other regions. Remember to prioritize the list of LPs you could solicit, provide the right resources to ensure your efforts can succeed, and persist with the effort. It is bound to take more time, effort, and resources than you expected to get a check from even an interested LP—and not every interested prospect turns out to be an investor in the fund.

UPCOMING REGIONS

Some regions are developing their own concentration of LPs in alternatives. Latin America has a large number of pension funds that can take long-term investment risks, since they are catering to a rapidly growing younger demographic. Many developing countries are witnessing a huge explosion of high net worth and ultra-high net worth individuals. Countries where financial system regulations ban foreign investments or make their compliance requirements onerous are also changing their rules due to demand for diversification.

This large market will open up opportunities for global asset managers. However, they tend to favor well-known and larger funds because they are more familiar. For US GPs not in that camp, solutions include partnering with a well-known local name for a cobranded feeder fund, procuring a publicly disclosed investment from a large local investor, establishing a local office (an expensive option that may pay off if it can generate investments and fundraises), or hiring a well-connected and respected placement agent.

MARKETING ACROSS COUNTRIES

Marketing in multiple countries comes with a set of unique challenges, compared to a purely local marketing effort. One primary issue is the plethora of regulations in each region. The lack of common regulations or even a common construct for GPs to follow makes it very difficult to navigate. There is a concerted effort to align some regulations, including a push toward allowing retail investors entry into alternatives, mandating enhanced disclosures, and standardizing reporting requirements by asset class.

While the intention is noble, even the act of sharing information with interested investors in a different region may be subject to local regulations. That means GPs should pay special attention to the legal and regulatory disclosures required by each country. Failure to include obligatory information in the marketing materials can have serious consequences for the manager due to noncompliance.

In addition, GPs must keep on top of the changes in regulations where the fund is being marketed. It is crucial for GPs to ensure necessary filings are made prior to marketing the fund and to seek the advice of counsel to abide by the regulations of each country. The marketing should only start when you can ensure there are processes and procedures to comply with applicable regulations, maintain filings, and fulfill reporting requirements as required in each of the countries where the fund intends to market.

Hiring legal counsel in each geographical area is an impractical task if there will be no real marketing impact from a country. It is better for the fund to prioritize its marketing efforts, as without prioritization the chances of success are limited. Remember that in many countries, even if the investor is interested in committing to the fund, they need permission to invest from their local regulator. This can consume a lot of time, budget, and resources during the fundraise for both private equity and hedge funds.

Importantly, fund performance in a new locale will differ from past experiences. Currency fluctuations can significantly impact an investor with a foreign stake. If there is reporting or tax payment required based on the fund’s performance in the local currency, this may have significant unintended consequences as well. For example, in the late 2000s, wealthy Indian-Americans invested in rupee-denominated fixed-income products in India. The currency depreciated significantly during the time and investors experienced a loss, yet investors were forced to pay taxes on their interest income. They had to wait until the investment matured and they were able to repatriate the principal back to the United States to realize the losses, even as they paid phantom taxes in the prior years.

It is not necessarily a GP’s responsibility to educate LPs about a region and its associated macroeconomic or investment issues, but the GP could make efforts to do so. Educating an LP about a foreign market might not be a good use of limited time in an introductory meeting.

Does this advice hold true for emerging market GPs? One common mistake they make when pitching to US investors is to spend significant time talking about macro issues. This is painfully evident when GPs from most developing economies start their fund pitch with a country primer (even for large nations like China, India, and Brazil). Managers should send the fund materials in advance, including a section on macroeconomic, regulatory, and other investment-related topics prior to the meeting for LPs to read.

There are exceptions to the rule. For example, it is the LP’s first foray into the foreign market, and there is a need to make them feel comfortable with that country’s macroeconomic, political, or investment risks. If the LP is sophisticated and interested in speaking with the GP, it is reasonable to assume there is a familiarity with the investment landscape—or they would spend time learning about it before meeting. It is easier to do a quick recap if it becomes evident during talks that the LP could benefit from learning about this market, rather than wasting time up front.

Creating a pipeline of foreign prospects and marketing to them will be more expensive and time-consuming than targeting domestic investors. Different time zones alone make it difficult for timely communication. In addition to cultural barriers, lack of on-the-ground resources and the necessity of travel add to the cost, inefficiency, and time consumed. However, there are some solutions to mitigate some of these issues: hiring a good placement agent may not only be an effective and efficient way to get access to these investors, it might also be a government requirement to use local registered advisors or brokers. Another solution is to aggregate meetings, such as holding country-specific conferences. These events are a great way to meet specific investor types or investors from a specific region.

CONCLUSION

Raising funds in a country other than the country of domicile of the fund is time intensive and represents additional operational and fundraising challenges. These challenges require a thoughtful consideration that leverages internal resources and identifies key service providers who can facilitate the process and ensure a fund is not undertaking undue risks. Given the plethora of investors across the globe, it would be beneficial to prioritize the effort to focus on investors with limited investment friction. Diversifying the investor base will be beneficial to both fund investors and the fund manager in the long run.