The minimal risk asset – safe, low-risk returns

Buy government bonds in your base currency if credit quality is high

This chapter is about finding the lowest-risk investment as the base on which a riskier portfolio can potentially be built. Your choice depends on currency: for a sterling-denominated investor, short-term UK govenment bonds are a good choice. As discussed previously, there is probably no genuine riskless security in the world today, but the probability that the UK government will default is very low; thus minimal risk.

By comparison, a US-based investor buying short-term UK government bonds would have the same security of getting his principal back, but would incur currency risk as the GBP/USD exchange rate fluctuations add risk. So if, for example, the UK bond promised to pay the investor £101 a year hence for a £100 investment today, both investors are equally certain of receiving £101, but while the £101 would always be £101, the US dollar value of that amount could fluctuate quite a bit and is thus more risky. The US investor would therefore be better served by owning short-term US government bonds that are of similar credit quality to the UK government bonds where his returns would be independent of currency risk.

If your base investment currency is one where the government credit is of the highest quality, those government bonds will generally be a great choice for your minimal risk investment. While most investor’s base currency is obvious (sterling for UK investors, dollars for US ones, etc.), and currency risk is a risk you would rather avoid, your base currency can also be a mix of currencies. It is essentially the currency that you think you will one day need the money in. So while I may live in the UK and probably have the majority of my future expenses here, I also spend a lot of time (and money) in Denmark, the eurozone and the US. Also, I may have future expenses for my children’s education outside the UK, or my wife and I might live or retire abroad one day. By having my base currency as a mix of several currencies, albeit dominated by sterling, I will better match my future cash needs and leave myself less at risk of being caught out by a falling currency with potential expenses in other currencies.

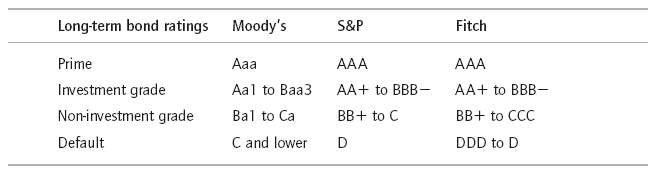

Today there are three major credit agencies that rank the creditworthiness of bonds, namely Moody’s, Standard & Poor’s and Fitch. Here is how those agencies rate long-term bonds.

The credit agencies were widely discredited after 2008 when they wrongly gave high ratings to all sorts of sub-prime garbage, but in general they give you a good indication of the credit quality of a country’s bonds.

Credit ratings change frequently. As you consider adding your minimal risk asset, you can see the latest credit ratings on Wikipedia by searching for ‘List of countries by credit rating’. If the government credit of your base currency is listed here as AAA you have an easy choice for your minimal risk asset. With the adverse environment of government debt and deficits in recent years, the list of AAA-rated countries from all agencies has shortened. That said, if your home base currency offers AA or higher-rated bonds then it would be sufficient to accept those as your minimal risk asset. If we only accepted bonds with the highest rating, at the time of writing that would exclude bonds from major economies like the US, Japan and France, which is neither practical nor desirable for many investors (the UK was also recently downgraded from the top rating by Moody’s and Fitch). While there is obviously a reason for these countries losing the highest rating it is worth noting that the financial markets trade the bonds at real yields that are among the most creditworthy in the world in any currency.

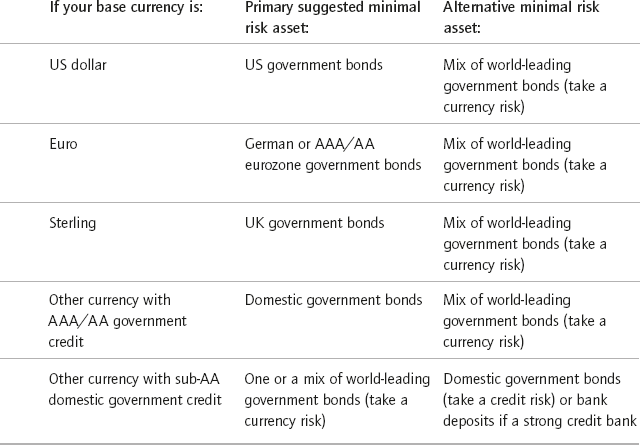

If your base currency is one without a highly rated bond available, you face a tougher choice. For all their undoubted economic successes over the past decades countries like Brazil, Mexico and India do not have highly rated government bonds (all approximately BBB-rated at the time of writing). As a Brazilian you could buy Brazilian short-term government bonds which would not be minimal risk or highly rated government bonds in one or a couple of foreign currencies, although this would involve a currency risk. Depending on the credit rating of your base currency government you may choose to take the credit risk of the domestic government bonds instead of taking the currency risk of highly rated foreign bonds, or perhaps even keep money in cash deposits in the local bank if that is considered a superior credit option to domestic government bonds (see the box on pages 49–53).

Older people in certain parts of the world, including Brazil, undoubtedly remember times of domestic economic turmoil and the thought of buying local government bonds as their minimal risk asset will seem like heresy. And they are right. These investors do not have essentially risk-free bonds in their local currency, however far the government has come. Perhaps one day the credits of these governments and many like them will grow in esteem to the point that they become the lowest-risk bonds in the world, but not today. In the past, many investors with a less-creditworthy domestic government essentially made their base investment currency the US dollar and would buy US government bonds for their base currency.

While the lower credit ratings of some government bonds mean that the bonds yield more, this is not a good reason to have them as your minimal risk or safe asset. As discussed in the next chapter, if you want to add returns to your portfolio you can do so by adding broad exposures of equities that have the added benefit of both being geographically diversified and adding expected returns.

Perhaps diversify even the very low risk that your domestic government fails

Investing in sub-AA credit ratings is a question of degrees. Some investors would be happy to invest in their BBB-rated local currency government bonds whereas others would rather invest abroad with currency risk than have an AA domestic-rated government bond. The choice partly depends on your situation and sensitivity to currency risk versus domestic credit risk. For those inclined to accept sub-AA domestic government bonds as their minimal risk asset I would encourage you to think about what else would happen in your portfolio if your domestic government defaulted. In most cases, a domestic government default would have a catastrophic effect on your portfolio and general life.

If you had diversified some of the domestic risk away by having your minimal risk asset as highly rated foreign bonds, such as German/UK/US government bonds, then you would at least have some respite when the domestic calamity hit. Also, some investors consider that having all your minimal risk assets invested in the bonds of just one government, however creditworthy, is a bad idea. Those investors argue that while the government bonds of Britain or Germany are highly rated today there is always some risk that they could fail, perhaps even spectacularly and quickly.1 Because of this eventuality investors should diversify their minimal risk asset into a couple of different, highly rated government bonds, even if this means taking a currency risk for those bonds that are not in your base currency. My view is that if you are invested in government bonds that are among the most highly rated in the world the probability of a sudden default is so low that for practical purposes it is a risk you could feel safe taking.

Here are some recommendations for minimal risk assets depending on your base currency:

So your minimal or ‘safe’ asset is not necessarily your domestic government bond. Consider a Spanish investor who is after the lowest risk asset, and does not want to take a currency risk. This investor should not be buying Spanish government bonds that are quite lowly rated, but instead should buy German government bonds that are also euro denominated. If this investor did not want the minimal risk to be the bonds of just one government he could diversify by either adding other euro-denominated government bonds or accept the currency risk with highly rated non-euro government bonds.

In most countries there are domestic bonds related to the sovereign issuer, such as government-guaranteed regional, city or municipal bonds. Those and similar bonds could be reasonable alternatives as minimal risk assets, particularly if there are tax advantages to investing in them. However, make sure that the guarantee is bulletproof even in distress. If you get a superior yield from these alternative bonds compared to the standard government bonds, you are probably taking additional credit risk. Also be careful in thinking that adding these kinds of bonds provide you with additional safety; they are typically a poor diversifier of risk as they tie back to the same creditworthiness as the domestic government bonds.

Matching time horizon

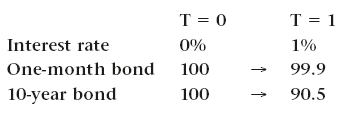

In the discussion above, short-term bonds are the minimal risk asset. This is because longer-term bonds have greater interest risk (the fluctuation in the value of the bond as a result of fluctuations in the interest rate). Consider the example of a one-month zero-coupon bond and a 10-year zero-coupon bond that trade at 100 (zero-coupon bonds don’t pay interest, only the principal back at maturity). Now suppose annual interest rates go from zero to 1% suddenly. What happens to the value of the bonds?

The one-month bond declines a little in value to reflect an interest rate of 1%, while the 10-year bond declines to a value of around 90.5 to reflect the higher interest rate. Clearly something that can go from 100 to 90.5 fairly quickly (rate changes are rarely that dramatic) is riskier, even if your chance of eventually being paid in full has not changed.

However, in reality the time horizon for most investors exceeds the maturity of the short-term bond. Someone who is interested in maintaining a position in the minimal risk asset for five years will be taking an interest rate risk over that five-year time horizon whether buying new three-month bonds every three months, or buying a five-year bond and keeping it to maturity.

But if the time horizon is such that you think five-year bonds make sense, you shouldn’t necessarily just buy the five-year bond and hold it to maturity. A year hence, your bond would only have four years to maturity and therefore no longer match your time horizon.

The best way to address this issue is not for you to constantly buy and sell bonds to get the right maturity profile (here you would sell the now four-year bond and buy another five-year bond), but to buy the bonds through a product like an exchange-traded fund or investment fund that trades the bonds for you. (These ‘access products’ will be discussed in detail later.) Such funds will offer products like ‘Germany 5–7 years (to maturity) government bonds’, ‘UK 10–12 year government bonds’, etc. Buying one or a couple of these products to match your desired minimal risk asset and maturity profile is a cheap and low-hassle way to ensure you have the right minimal risk asset in your profile.

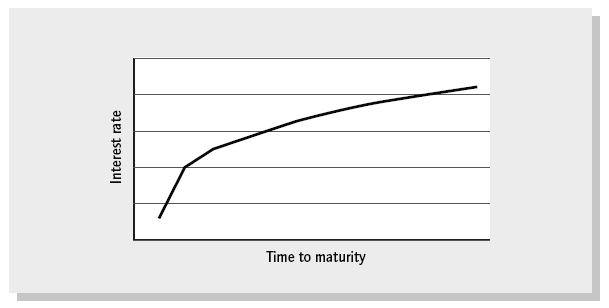

So investors with a longer time horizon should therefore buy longer-maturing minimal-risk bonds. As a reward for taking the interest rate risk associated with the longer-term bonds they typically yield more than the short-term bonds, as illustrated in Figure 4.1.2

So if you need a product that will not lose money over the next year, pick short-term bonds to match that profile. However, if you – like most people – are after a product that will provide a secure investment further into the future, pick longer-term bonds and accept the attendant interest-rate risk.

You should therefore consider the time horizon of your portfolio and select the maturity of your minimal risk bonds accordingly. If you are matching needs far in the future (like your retirement spending) there is certainly merit in adding long-term bonds or even inflation-protected bonds (see below) to your portfolio. Long-term bonds compensate investors for interest-rate risks by offering higher yields and you have the further benefit of matching the timing of your assets and needs.

Another good alternative is to mix the maturities of your minimal risk assets. You may have some assets that you won’t need for decades, and others you think will be needed in 5–7 years. In that case, there is nothing wrong with picking a couple of different products with different maturities to match that profile.

Inflation-protected bonds

Normally when people quote a bond yield they refer to the nominal yield. The nominal yield consists of the real yield plus inflation. (So if a bond offers a 2% yield then that simply means that you get £2 for a £100 bond; if you assume inflation at 1%, then the real yield would be 1%.) So as an investor, in most bonds you have an inflation risk on top of the interest rate risk. To address this inflation concern several governments have started issuing inflation-protected bonds where the buyer is promised a real return. The inflation-indexed bonds work by linking the principal to an inflation index like the consumer price index (in the US) or the retail price index (in the UK). As those indices go up with inflation, so does the amount you are owed by the government.

The market has grown explosively since the British government started issuing these bonds in 1981, but are still not nearly as widespread as the regular bonds: there are currently about $1.5 trillion outstanding compared to world government bonds of over $40 trillion. These bonds are an interesting development and provide investors with a way to avoid the inflation risk inherent in the bond markets, and I would recommend UK and US investors in particular to consider them.

The threat of inflation is a real concern for a lot of savers and these new bonds offer a good way to address that concern. While you still take an interest-rate risk and should match maturities to your maturity profile, at least your inflation risk is mitigated.

In recent inflation-linked bond issues several issuers were able to issue bonds that had a negative real interest. Think about that. You lend someone money, potentially even for a very long time, and they promise to pay you back less than what you lent them in terms of what that money can buy. It may seem crazy, but that is the reality of the world we live in right now. This does not mean that these are not good bonds to own, just an illustration that interest rates are low now and the cost of owning a bond that will be extremely likely to repay you is high.

What will the minimal risk bond earn you?

Most people with even a peripheral interest in finance realise that at the time of writing, in spring 2013, interest rates are currently at or near a historical low. So investors should not expect to make a lot of money investing in the minimal risk asset in any currency. In fact, with nominal interest rates near zero, inflation means that investors in short-term government bonds will experience negative real returns. So while your £100 invested in a government bond may, with almost certainty, become £105 in five years’ time, the purchasing power of that £105 will be less than that of the £100 today. This is, of course, still better than if you had held the £100 in cash for five years – in that case the purchasing power would be even lower.

Without putting too fine a point on it, that obviously isn’t great, but there is not a lot you can do about it. If you are after securities with minimal risk then the yields are just very low right now. Instruments that offer higher returns come with more risk of not getting paid and anyone who tells you otherwise is not telling you the whole story.

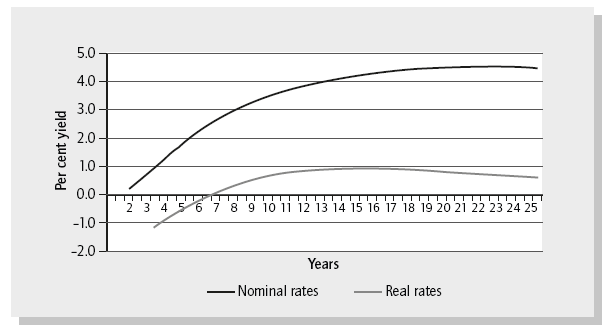

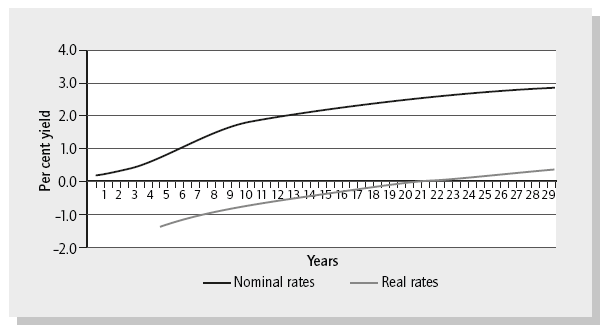

Figures 4.2 and 4.3 show what UK and US government bonds (so in £ and $) will currently earn you, by maturity, both in real and nominal terms.

Based on data from www.bankofengland.co.uk

Based on data from www.treasury.gov

While the outlook for generating very low-risk real returns is thus fairly limited (at the time of writing), these are continuously moving markets and it is worth staying on top of them as rates change. What you can see from Figure 4.2, for example, is that if you wanted to buy UK government bonds now, you could expect to earn a just under 1% real return a year for a 20-year bond. Likewise, for a five-year bond you should expect a negative return of about 0.5% a year.

What you can also see from Figures 4.2 and 4.3 is the current market expectation of future inflation (the difference between the lines). So, for example, the markets are assuming that there will be approximately 4% annual inflation in the UK for the next 25 years, but only around 2% for the next five years, suggesting higher inflation in the longer term. Inflation is bad for many things, one of which is tax. (While the benefits you get from your investments are based on real returns and the future purchasing power of your money, you pay taxes on the nominal return.)

Suppose you invest £100 for a nominal return of 2% the following year, then you could be liable for tax on your £2 gain, even if 2% annual inflation had eroded the real gain (so the purchasing power a year hence would still be £100 in today’s money even if the nominal amount had become £102). Compare that to a zero inflation rate environment with a 0% nominal/real return and your £100 would still be £100, both in real terms and nominally, at the end of the year. There would be no gains to pay taxes on.

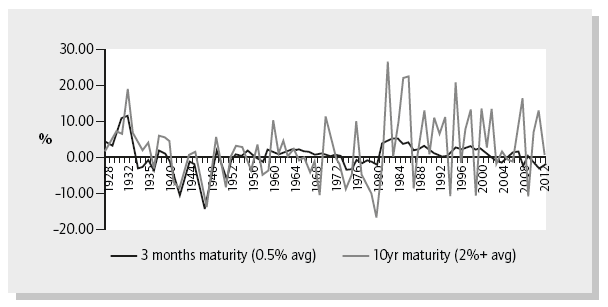

If the charts above give you the sense that the returns you get in any one year from owning UK or US government bonds is stable, reconsider. Figure 4.4 shows the annual return from holding short-term (sub one year) and long-term (more than 10 years) US bonds since around the Depression. What you can see is that the annual returns move around a fair deal for both, but far more for the long-term bonds. This is because those bonds will move in value far more as the interest rate or inflation fluctuates.

It can be hard to do an objective, like-for-like comparison of historical and current returns as the market view of the creditworthiness of government credit has not been constant, but Figure 4.4 suggests that the returns from longer-maturity bonds are not without risk. If your investment horizon for the minimal risk asset was approximately 10 years and you had gained access to the government bonds through an ETF or index fund, your annual fluctuations would have looked roughly like Figure 4.4. It will probably be a surprise that something that is considered as safe as US government bonds can fluctuate as much as the chart suggests.

Based on Bureau of Labor Statistics and Federal Reserve St. Louis

There are a few points to note from the charts above:

- Real return expectations from the minimal risk asset are currently near an historic low.

- Returns from these minimal risk assets have fluctuated quite a bit, because of changes in inflation and real interest rates, and can reasonably be expected to do so in the future.

- You can generally expect higher returns from investing in longer-dated bonds. If that matches your investment horizon then hold your minimum risk bond portfolio through a suggested access product like an ETF or index fund. But note that particularly for longer-dated bonds the yearly fluctuations in value can be significant.

In the interest of keeping things simple in the following examples, I have assumed a real return of 0.5% a year from the minimal risk asset. As you can see in Figure 4.4 while that is too high for current short-term bonds, it is more reasonable for longer-term bonds and in line with historical returns from short-term bonds.

Do not believe your cash is safe in the bank!

Although interest rates are quite low, many investors still hold large deposits in cash at their financial institutions without considering the credit risk. I would caution against blindly doing this.

About 120 countries in the world have a system whereby the state guarantees deposits with financial institutions up to a certain amount in cases of default. While this varies by country it means that the first £85,000 (in the UK) or €100,000 (in many EU countries) of deposits with a bank is guaranteed by the government. The guarantees are in place to lend confidence to the financial system and avoid runs on the banks. Without a bank guarantee we would be general creditors to the bank and have to gauge bank credit risk, something most depositors are not equipped to do. (Of course, if you have your money with a bank deemed ‘too big to fail’ the bank won’t fail without the government also failing.)

If you hold cash deposits with one or more financial institutions in excess of the deposit insurance then you are a general creditor of that institution in the event that it fails. This means that if you have £200,000 in deposits with a bank and the credit insurance is only for £85,000, the last £115,000 is not covered.

A good friend of mine sold his successful IT business a while ago for a very large cash amount. He was never really that interested in finance, and just left the money in an account with his financial institution while he took some time off. This was a large, double-digit, million-dollar amount and the financial institution was the insurance company AIG. He got concerned when one morning he read in the Financial Times about all the issues with AIG and how it could potentially go bust. When my friend contacted AIG there was initially some confusion about the kind of account he held and for a while my friend thought his money with AIG was going to be lost in the general abyss of a spectacular financial collapse. In the end, he along with all the other creditors of AIG kept his money, but the experience certainly put the statement that an investment is ‘as good as money in the bank’ in perspective.

On a much smaller scale, I had some cash in a lesser-known bank in excess of the government credit guarantee. I had agreed to put most of the money on time deposits where I would get a slightly higher interest rate of 2.5%. Coincidentally I discovered that the bank bonds were trading in the market at a yield of approximately 5% a year. In simple terms, the market was telling me that I was taking a credit risk on the non-government guaranteed portion of my deposit that the market estimated at 5% a year, but getting paid 2.5% for it. Not a great idea!

Who backs the deposit insurance?

The deposit insurance scheme is only as good as the institution that has granted this guarantee. If you were holding cash with a Greek bank and relied on the deposit insurance protection from the Greek government you would clearly not be as secure as with the same guarantee from the German government.

In the recent bailout of Cyprus, the restructuring that was initially suggested involved depositors both above and below the guaranteed amount taking a cut in their deposits (in the end, only larger depositors had part of their holdings confiscated), suggesting that bank depositors in that country were indirectly exposed to the creditworthiness of that government in addition to that of the bank holding their money.

Local banks fare horribly if the government defaults; the banks are tied strongly to the local economy, which is suffering. On top of facing a poor economic climate, the banks will have lost a lot on their holding of government bonds. The correlation between the troubles of your government and your bank is thus very high, and the protection you were hoping for may be absent as a result. This is bad news, particularly as your bank and government default may well happen at the same time as other things in your life are being negatively affected by the same economic factors; you may have lost your job, your house may decline in value, and so on. It is exactly in that circumstance that you want the diversification of investments and assets that the rational portfolio provides.

A way to address the potential lack of security of your cash in the bank is to buy securities like AAA/AA government bonds or other investment securities that closely resemble cash (such as money market funds, etc.). Importantly, securities like these still belong to you even in the case of a bank default, and while the process of moving that security to another financial institution could be cumbersome, you are no longer a creditor to a failed bank, which gives you far greater security in a calamity.

While investments like stocks and bonds held in custody at a bank still belong to you if the bank goes bust, you should be careful about holding too many assets at risky banks. Once an institution defaults, the process of finding out who exactly owns what can take time. There have even been cases where the segregation between client assets and bank assets have been less firm than it legally should be, rendering it even harder to regain the investments that are legitimately yours, in the face of bank creditors claiming that the same assets belong to them.

Also, in a future bailout like the ones we have seen in Southern Europe it may be that not only your cash is confiscated, but that institutions find a way to take some of your securities as well. It’s all a mess worth avoiding, so unless there is a compelling reason not to do so I would encourage you to place your cash and investment assets with very credible banks.

Particularly pre–2008, some less-known banks offered very generous interest rates on deposits compared to the more conservative traditional banks (these turned out to not be so conservative either, but that’s another story). In the UK, the Icelandic banks in particular were guilty of this, but there were many others. (The rate differential provided the potential for profits from the perspective of the depositor at the expense of the soundness of the banking system.) If the depositor guarantee was indeed iron clad (i.e. the government would not try to get out of the depositor guarantee under any circumstances) then depositors were incentivised to withdraw cash deposits from the more conservative high street banks and deposit the money with the bank that offered higher deposit interest rates. If the gun-slinging bank went bust (like some did later) the government would ensure the depositor would not suffer. If the gun-slinging bank stayed in business, the depositor would benefit from higher rates.

A couple of years ago I was approached by someone who was planning to start a bank. His pitch did not involve great new markets or interesting products, but rather what he called an ‘arbitrage’ on the credit insurance of the government. His arbitrage involved offering customers extremely high deposit rates, but only up to the amount of the government deposit insurance, and thus attract sizeable deposits. He would use the deposits to offer loans to renewable energy investments that also had government guaranteed rates of return, while capturing a spread for the bank (and himself presumably) in the middle. He claimed that his scheme was entirely legal and within banking regulations (I suggested he double checked this). I don’t know if this man was able to start his bank, but it gives a good picture of the kind of thinking that can drive some of the more gun-slinging banks out there. Also, it shows how important it is for governments to get bank regulation right in the face of the many people who constantly try to game the system. It is not an easy task.

I feel like a pessimist in writing about the dangers of cash deposits. It is certainly the case that in more than 99% of cases the thought behind the term ‘safe as money in the bank’ or ‘cash is king’ means exactly that; that it is entirely safe. My logic is based more on how things fit together and trying to avoid several bad things happening at the same time. If you consider the unlikely scenario of the bank where you hold most deposits going out of business, that scenario probably involves a lot of things that are also not good for your investing life. Regardless of what your risk profile is as an investor, you should be sure that you get properly compensated for the risks you are taking, and that you think about what happens in a calamity. The risk to your cash deposits in the case of a bank default is no different.

Summary

- Cash deposits are not entirely without risk. Don’t hold cash in excess of that which is guaranteed by the government at one bank, and do worry about which government has issued the deposit insurance on your cash.

- By holding investment securities like government bonds (or products like ETFs for government) instead of cash with a financial institution, you are often in a far better situation to recover these securities in the event of a bank failure.

Buying the minimal risk asset

Because of costs in trading bonds most investors in short-term bonds have to accept that the bonds in their portfolios will not be super short term,3 and that you will be taking a little bit of interest rate risk as a result. The most liquid short-term bond implementation products like ETFs or index funds that represent the underlying bonds have average maturities of 1–3 years. The slight interest rate risk that comes from holding bonds with 1–3 year maturities is a reasonable compromise between the theoretical minimal risk product and one we can actually buy in the real world. For most investors with longer-term investment horizons other implementation products typically have different ranges of maturities like 5–7 years, 7–10 years, etc. to suit your preferences.

How much of the minimal risk asset you should have in your portfolio and what maturities it should have depends on your circumstances and attitudes towards risk. If you are extremely risk averse you could have your entire portfolio in short-term minimal risk assets, but you could not expect much in terms of returns with that. I will revert to what sample portfolios look like when you start introducing more risk, but the availability of the minimal risk asset is of critical importance to all investment decisions:

- You can use the minimal risk asset as part of your portfolio to adjust the risk profile. In the simple scenario where you can only choose between the minimal risk asset and a broad equity portfolio, you could weigh the balance of those two according to the desired risk. The minimal risk bonds would have very little risk, whereas the equities would have the market risk. How much risk you want in your portfolio would be an allocation choice between the two (we will later add other government and corporate bonds).4

- For some investors, the minimal risk asset is their optimal portfolio. If you are unwilling to take any risk whatsoever with your investments and willing to accept that this means low expected returns, this is it.

Summary

- If your base currency has government bonds of the highest credit quality (£, $, €, etc.) then those should be your choice as the minimal risk asset.

- If your base currency does not offer minimal risk alternatives you have the choice of lower-rated domestic bonds where you take a credit risk, or higher-rated foreign ones where you take a currency risk. Keep in mind that a domestic default will probably happen at the same time as other problems in your portfolio, and the domestic currency would probably devalue, rendering the foreign currency denominated bonds worth more in local currency terms.

- If you want no risk at all you should buy short-term bonds. If you have a longer investment horizon, then match the investment horizon with the maturity of your minimal risk bond portfolio. You will have to accept interest rate risk even if you avoid inflation risk by buying inflation-adjusted bonds.

1 For those who don’t think government bonds can default I would encourage you to read This Time is Different: Eight Centuries of Financial Folly by Carmen Reinhart and Kenneth Rogoff (Princeton University Press, 2011). The authors make a mockery of the belief that governments rarely default and that we are somehow now protected from the catastrophic financial events of the past.

2 There are cases where the yield curve is reversed and shorter-term bonds yield more than longer-term ones, but these cases are less frequent.

3 Imagine the scenario where you want to hold one-month government bonds. Tomorrow the bonds are no longer one-month to maturity, but 29 days. Is this ok? How about 2 days hence? How much you are willing for the maturity to deviate from exactly 30 days is up to you, but in reality there is a trading and administrative cost associated with trading bonds. It would simply not be feasible to stay at exactly 30 days to maturity at all times.

4 Certain corporate bonds trade with lower risk premiums than many governments. The view is that these corporates are lower credit risk than many governments – not hard to believe – and although they do not have the ability to print money, nor do governments in the eurozone. The reason I believe that you should not consider these bonds as the minimal risk asset is more practical. Compared to government bonds, the amount of corporate bonds outstanding for any one company is minuscule and you would probably not be able to trade them as cheaply and liquidly as government bonds.