Expenses

In this chapter we are going to look at the cost of your portfolio. There are too few people from the world of finance that are interested in emphasising the importance of low fees to investors. They are, after all, the ones making money from those same fees. I have nothing to sell you, other than the book you have already bought.

Fees are always important in finance, but even more so for the rational investor. Since we don’t think we’ll be able to outperform the market, we are not asking anyone to be particularly clever about investing. We just want someone to replicate the market. As a result, we can expect to pay very little for it. It’s worth repeating a lesson from earlier (see Figure 13.1).

Inertia is a powerful force. It either makes us leave our investments where they are or makes us buy the well-known active funds, like so many others. Most investors are aware of the extra costs, but often don’t seem to react – please don’t let that be you. It seems paradoxical to me that many investors spend endless hours comparing the prices of laptops or holidays when hours spent researching better and cheaper financial products could far outweigh savings made elsewhere.

An expensive, active choice

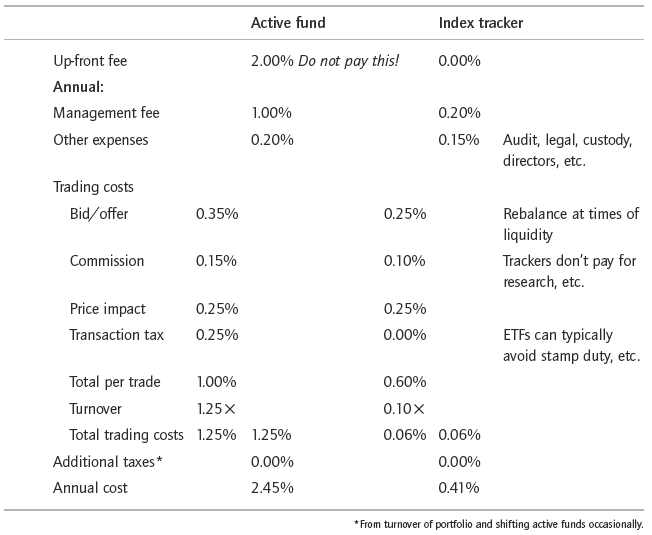

Let’s compare the costs of investing in a passive, index-tracking product to that of a typical active fund tracking the same index:

While thankfully many investors can avoid the increasingly rare up-front fees, in simple terms you can save about 2% a year by investing in an index-tracking fund compared to an active fund (some funds have exit fees too, but those are increasingly rare).

If the annual saving does not seem like a lot to you, consider the power of compounding returns.

Let’s assume that you are a frugal investor who diligently put aside 10% of £50,000 income from the age of 25 to 67 that you put into equities. (Assume income will go up with inflation but to simplify this is an average over the time span – most 25-year-olds don’t make £50,000.) How much of a difference should you expect from the allocation to an index-tracking product as opposed to an active fund?

Let’s further assume the following nominal cumulative returns before fees (ignoring taxes for now):

| Minimal risk rate | 0.50% |

| Equity risk premium | 4.50% |

| Annual inflation | 2.00% |

| 7.00% |

It is worth reiterating the key point that we should not expect the active manager to outperform the index before fees. Obviously some managers will do so, but in aggregate the active managers perform in line with the index before fees. It is because of their significant trading, management and other fees that the outperformance is so stark compared to index-tracking products.

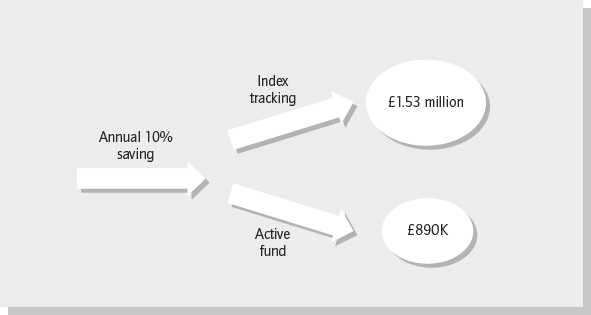

So where does this leave you? As you get ready to retire at age 67 the difference in the savings pot is staggering. You are left better off by £643,000 simply by investing with an index fund as opposed to an active manager (see Figure 13.2).

This is calculated by simply taking the annual savings each year (so £50,000 × 10% = £5,000 in the first year, etc.) and either investing it in the index tracker or the active manager with a return of 7% a year before fees.

Figure 13.2 Result of investing with an index fund as opposed to an active fund

Adjusting the £643,000 for inflation, the saving is still around £280,000 in today’s money. If you had managed to avoid paying the up-front charges your active fund investment would have been greater by about £23,000 at age 67, hitting home the advantage of avoiding this initial charge, if possible. If you had avoided the up-front charge and there had only been a 1.5% annual difference in costs, the difference in savings at retirement would still amount to £494,000. If you think you have a great edge in the market and think you could easily make up this 1.5% or 2% annual cost difference, then good luck to you. If not, then the sooner you shift out of the expensive investment products and into cheap index-tracking products the better off you will be.

Think about that. By not giving money to an active manager who probably was not able to outperform anyhow you saved £280,000 in today’s money over your investing life. Just imagine the difference in quality of life that kind of money would make in retirement or for your relatives after you are gone. Suppose now that you are an institution administrating assets for a large number of customers – the cumulative savings from shifting assets into the index-tracking products can quickly become truly astounding.

Conversely, consider the 85–90% of investors who invest in active managers as opposed to index-tracking funds either directly or via their pension funds. Over the long run only a very small percentage of those investors will be lucky enough to invest with active managers that will give better returns after fees. The rest have simply paid a staggering amount of money to the financial industry over their investment lives. To put things in perspective, next time you see a finance person driving a Porsche or jetting off to a holiday home in Spain just consider that these additional and unnecessary fees for just one saver over his or her investing life could buy at least seven Porsches. And paradoxically this is money paid to the finance industry from a saver who would typically not be able to afford a Porsche.

If you know all of the above and are still happily paying the fees then at least stop complaining about people in finance making too much money and driving fancy cars.

You are obviously not forced to choose only between an active manager or an index tracker. As many do, you could manage your own portfolio with individual security selection. The decision whether or not to do this goes back to the question of having an edge in the first place. If you don’t have an edge you know that this ‘do-it-yourself’ approach is a loser’s game for you as you will not be able to pick a superior portfolio to that of the market, and will end up buying the market index trackers as this is far less hassle and more cost efficient.

Patience

The problem with the focus on fees is that we don’t receive instant gratification. There is no stock that doubles next month. To really notice the additional profit we gain from being clever about expenses takes years or even decades. The key to reaping the most savings is to have the patience to wait for the compounding impact of the lower expenses to take effect. I compare it to making money while you sleep; lower fees make a little bit of money all the time.

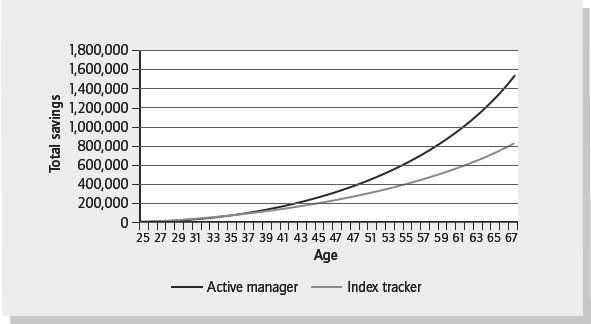

Consider Figure 13.3 that illustrates the aggregate savings of the saver mentioned above. In the early years you can barely tell the difference between the active and index tracking investments. In the later years the benefits are apparent, but obviously only exist for the investor who maintained the discipline of lower fees.

Saving 2% or more a year in fees may sound like a lot, but are we going to notice that amid the noise of the investment markets? The index tracker performs slightly better than the average active fund – outperformance coming from the lower fees. Meanwhile the active fund performance will be all over the map, with the best performers screaming the loudest about how their special angle or edge ensured the greatest performance. We might be tempted to believe the manager and abandon our boring and average index-tracking strategy, but please don’t unless you can clearly explain to yourself why you have an edge. Chances are you don’t and you will be wealthier in the long run from acknowledging this.

Figure 13.3 The importance of sticking with it: your aggregate savings

Believing in an edge can be expensive

Once the CFO of a mid-sized European insurance company proudly showed me around his internal investment group. We came to a large open-plan floor and he showed me analysts that were actively trading securities in individual stock markets, with the team being divided geographically. There were perhaps 25 of them in total, with a trader who would pass on the orders to brokers around the world. When I asked the CFO, ‘Do you think these guys have an edge in the markets’, he looked at me like I had just asked him a nonsense question, like how long to cook a chicken.

The CFO made some comment to me that instead of caring only about edge, by actively trading stocks the analysts were able to create the kind of risk profile that suited their overall investment objective. I thought that they would be better off combining equity indices with a broad bond portfolio in proportions that suited their risk profile. And then there was the issue of costs. Even excluding the Bloomberg terminals, office space, real-time price feeds, bid/offer spreads, commissions, risk of fraud, research costs and so on, in total these guys cost the company millions every year in salary, bonuses and expenses. Was that worth it? I thought not – I didn’t think they had an edge. In fact in the financial models I built for this insurance company I built in an expectation that they would underperform the equity indices by 1.5% a year in their equity exposure (but I doubt they made the same assumption internally). They should not have spent the large resources actively trading in the market, but realise that they were without an edge and have an index-tracking portfolio as a result. Over time this would serve them and their shareholders better.

In another case I visited a commodity firm with large and fluctuating euro/dollar exchange exposures. There was a small team of traders in charge of hedging the company’s currency exposure. Fair enough. But instead of thinking about what kind of exposure the company wanted and implementing it these guys had effectively set up a small trading operation where they were actively trading multiple currencies, depending on their views of the market. This made no sense to me. The euro/dollar foreign exchange market is one of the most liquid markets in the world, and anyone with a real edge in this market has a fantastic opportunity to realise great riches from it. It just seemed to me that the three or four traders at this commodity firm did not possess this edge and would be better off not playing those markets.

In both the company examples above it seems that the shareholders would be better off without the implicit assumption of an edge. Unfortunately in far too many cases, trading decisions are made on the basis of how things have always been done or perhaps as a result of someone who was given some leeway to trade, only to have things mushroom from there.1 Instead these companies and many like them would have been far better off if they had started with a basic question: ‘Do we have an edge, and if so why, where, and how can we best exploit it?’

Where are we heading?

In my view, expenses in connection with investing will be a major point of debate over the next decade, as awareness and dissemination of information increases further in the investment management industry.

Particularly in the 1970s and 1980s the mutual fund industry grew explosively. The benefits of diversification espoused by academic portfolio theory also became wider known, even if not necessarily in technical terms. When I was attending classes on financial theory in the early 1990s, mutual fund investing was discussed in great detail as a great tool for the private investor.

As the mutual fund industry grew so did the index-tracking industry. The index-tracking firms were not generally as widely known as the mutual funds, probably in large part because their low fees did not leave a lot of room for general marketing expense. They were led by Vanguard and the legendary John Bogle.

The growth in the index trackers was a natural extension of the disaggregation that the finance industry had moved slowly towards for decades. Disaggregation is perhaps too big a term and I’m sure that nobody had a grand plan, but the basic idea was that you paid for what you got. If you only wanted market exposure as defined by the creation of some index, you only paid for that, with the simplicity of the product continuously pushing down its costs. Unless you wanted to, you didn’t have to pay for a supposed star mutual fund manager at the same time or the friendly advice from your local broker. And doing it all yourself was not only time consuming, but the cost and information disadvantages compared to professional investors meant that it was increasingly a bad choice. Those things are certainly still available, but so is the bare-bone version of only buying the index.

Index-tracking investments consist of approximately only 15% of stock-market investing so there is a lot of room to grow. This continued growth will benefit investors at the expense of the financial industry as the aggregate fees will decrease.2

I hope a future development in the world of index tracking will be a focus on lowering the costs of this essentially commodity product. There is today far too great a disparity between the charges imposed by index-tracking providers (like index funds, ETFs, etc.) and some are simply too expensive. Vanguard is at the forefront of an extreme focus on costs and that firm’s massive size suggests investors are receptive to the improvements. Competitors including iShares have responded to the challenge and lowered fees, leading to an encouraging industry trend. A rational portfolio should be driving a Volvo, not a Porsche. Taking cost reductions further, investors could be offered the chance of investing in a white-label index3 instead of a more well-established index like S&P or MSCI, and thus save the licence fees. In one of those moves that cause great ripples in the world of index investing, but hardly noticed elsewhere, Vanguard recently changed some of their products to track a FTSE index instead of an MSCI one to save money on licence fees. This kind of cost focus among the product providers ultimately benefits customers.

1 In my view there are many cases where it is in the employees’ but not the company’s interest to have these kinds of trading operations. The employee may get a bonus or share of the profit if there are gains, but will not share in the losses.

2 There is clearly an upper limit on indexing. If there was only index investing there would not be an efficient market with prices reflecting the future prospect of individual securities. However, I think index tracking could more than triple and still be very far from this point.

3 A white-label product is one that is produced by one company, which is then rebranded by others.