CHAPTER 4

Investment Strategies for Maximizing Estate Growth

Traditional investment philosophy suggests that as you get older you should invest more conservatively. Not long ago, commonly accepted wisdom employed the following investment allocation formula as a rule of thumb: 100 minus your age equals the percentage of stocks you should have in your portfolio. This means that a 70-year-old would have only a 30 percent allocation to stocks. While this strategy should reduce portfolio volatility, it also significantly reduces the long-term growth potential of your holdings. We believe this “old-age” way of approaching investing is out of touch with today's world. Advances in medicine and biotechnology have allowed scientists to better understand the aging process and develop methods for enhancing longevity. Some scientists now believe the average 50-year-old will live to age 120. Talk about a need for growth in your portfolio! One of retirees' greatest fears is that they will outlive their financial resources and become dependent on their children (or the government) for their financial support. In order to address the need for a portfolio that could provide significant long-term growth and income for retirees, coauthor Welch developed the Growth Strategy with a Safety Net®, which today represents one of the best solutions for the possibility of living too long. Here's how it works.

The goals of the Growth Strategy with a Safety Net® are as follows:

- Protect your retirement income from stock market fluctuations.

- Maximize your retirement cash flow.

- Produce an ever-increasing income stream that will more than offset the ravages of inflation.

- Provide for significant portfolio growth, ultimately providing a legacy for your heirs or favorite charitable organizations.

Sound impossible? Well, read on!

Growth Strategy with a Safety Net®

First, you determine how much annual cash flow you need and multiply that number by the number of years that you want to protect your income. Be sure your annual withdrawal rate does not exceed your risk tolerance (see the section on withdrawal rates later in this chapter). Use the following scale:

- Conservative: 10 years or more

- Moderate: 5–10 years

- Aggressive: 2–5 years

Next, add an amount of money that represents a generous emergency fund. Your total here will be invested as follows:

- Emergency fund plus your first year's income need is invested in a money market account. To find the highest money market yields, go to the Resource Center at www.welchgroup.com; click on “Links,” then “Highest Money Market Yields.”

- The money that represents your remaining cash flow “safety net” will be invested in a bond ladder using bonds maturing every 12 months. This completes your safety net.

- Implement your growth strategy by investing the balance of your money in a diversified portfolio of stocks or stock mutual funds. Periodically, you will sell a portion of your appreciated stocks and use the proceeds to replenish your bond ladder.

In a year when stocks do poorly, you postpone sales and wait for the market to recover. Historically, one to three years is sufficient time for this to occur.

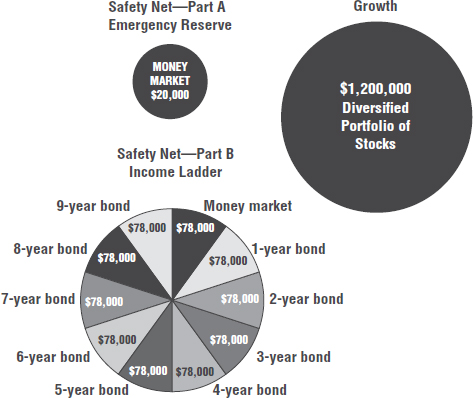

For example, assume you have $2 million available to meet your retirement income needs. You decide that a $20,000 emergency reserve account should be sufficient to cover any unforeseen financial emergencies and that initially you would like to draw $78,000 per year (a 3.9 percent withdrawal rate) from your investment portfolio in addition to your other income sources, which include Social Security and pension from your employer. You consider yourself a conservative investor and therefore decide to protect this income for 10 years. Table 4.1 outlines how your safety net is set up initially.

TABLE 4.1 Initial Safety Net

| $ 20,000 | Emergency reserves invested in a money market account |

| $ 78,000 | First year's income need invested in a money market account |

| $ 78,000 | Bond maturing end of year 1 |

| $ 78,000 | Bond maturing end of year 2 |

| $ 78,000 | Bond maturing end of year 3 |

| $ 78,000 | Bond maturing end of year 4 |

| $ 78,000 | Bond maturing end of year 5 |

| $ 78,000 | Bond maturing end of year 6 |

| $ 78,000 | Bond maturing end of year 7 |

| $ 78,000 | Bond maturing end of year 8 |

| $ 78,000 | Bond maturing end of year 9 |

| $800,000 | Safety net total (40% of portfolio) |

Each month you draw $6,500 from your money market account along with Social Security and pension to cover your normal living expenses. If you have a financial emergency, you have an additional $20,000 available in your money market emergency reserve account. Having your safety net in place guarantees that your income needs will be met for a total of 10 years. Note that the interest earnings on your bonds can be either added to your money market account to provide an increasing income stream or reinvested as part of your growth strategy.

The balance of your portfolio ($1,200,000) is invested in a diversified portfolio of stocks or stock mutual funds and will provide you with needed long-term growth. In years when the stock market does well, you will sell $78,000 worth of stocks and buy another bond that matures in 10 years to replace the $78,000 that you spent during the previous year. If the market does poorly in a given year, you will postpone selling stocks until there is a market recovery. You can take comfort in knowing that your income is totally secure for the next 9 years no matter what happens to the stock market. Figure 4.1 provides a visual illustration of what the Growth Strategy with a Safety Net® looks like.

FIGURE 4.1 Growth Strategy with a Safety Net®

In an unprecedented historical occurrence, we have had two generational bear markets within a single decade: one that lasted from 2000 to 2003 and one that began in 2008 and ended in March of 2009. Both saw stock market indices drop more than 50 percent from the market peak to the market trough. In both cases, the stock market made a full recovery within approximately 5 years of the market bottom. It's instructive to put these two generational bear markets in the context of the only bear market that was worse—the Great Depression of 1929. More typically, you'll have a bear market, defined as a 20 percent decline within a 12-month period, once every 3 to 10 years (a full market cycle). The typical bear market lasts only about 14 months before recovery begins. Having a 5- to 10-year safety net should be more than sufficient to get you through a bear market while allocating enough money to growth investments (stocks or stock mutual funds) to allow your portfolio the opportunity to grow and offset the ongoing ravages of inflation.

This strategy allows you to allocate a large portion of your money in the stock market, where it can grow, while your income is protected during periods of poor market performance. We should add that this strategy is relatively tax efficient for taxable accounts because you have a portion of your portfolio producing taxable income in the form of interest (your safety net) and a portion of your portfolio whose distributions are subject to the lower long-term capital gains tax (the growth portion). Table 4.2 illustrates the power of this strategy over time. Not only are you maximizing your current income, but the potential growth of your stock portfolio allows both your income and portfolio values to rise over time.

TABLE 4.2 Growth Strategy with a Safety Net®

| Year | Beginning

Balance |

Annual

Withdrawals |

Cumulative

Withdrawals |

Growth at

5.6%a |

Ending

Capital Account |

Withdrawn

Rate |

| 1 | 2,000,000 | 80,000 | 80,000 | 107,520 | 2,027,520 | 4.00% |

| 5 | 2,112,373 | 84,495 | 411,161 | 113,561 | 2,141,439 | 4.00% |

| 10 | 2,261,759 | 90,470 | 851,398 | 121,592 | 2,292,881 | 4.00% |

| 15 | 2,421,710 | 96,868 | 1,322,769 | 130,191 | 2,455,033 | 4.00% |

| 20 | 2,592,972 | 103,719 | 1,827,475 | 139,398 | 2,628,652 | 4.00% |

| 25 | 2,776,346 | 111,054 | 2,367,874 | 149,256 | 2,814,549 | 4.00% |

| 30 | 2,972,688 | 118,908 | 2,946,490 | 159,812 | 3,013,593 | 4.00% |

| 35 | 3,182,916 | 127,317 | 3,566,025 | 171,114 | 3,226,713 | 4.00% |

| 40 | 3,408,010 | 136,320 | 4,229,374 | 183,215 | 3,454,904 | 4.00% |

| 45 | 3,649,023 | 145,961 | 4,939,634 | 196,171 | 3,699,234 | 4.00% |

| 50 | 3,907,081 | 156,283 | 5,700,123 | 210,045 | 3,960,842 | 4.00% |

| 55 | 4,183,388 | 167,336 | 6,514,394 | 224,899 | 4,240,952 | 4.00% |

| 60 | 4,479,236 | 176,169 | 7,386,250 | 240,804 | 4,540,870 | 4.00% |

a Assumptions: 5.6% blended rate of return (ROR) using a 60% stocks/40% bonds & money market asset allocation and assuming an 8% ROR on stocks; 2% ROR on bonds.

Note: Historical long-term returns for stocks ranged between 9% and 11%. Historical returns for intermediate-term high-quality bonds have averaged 4.5% to 5.5%. Rates used in this example reflect more conservative return estimates based on the current interest rate stock return environment.

Table 4.3 profiles the volatility and return characteristics of conservative, moderate, and aggressive portfolios based on the Growth Strategy with a Safety Net®. It should be noted that while the one-year risk associated with investing in stocks or stock mutual funds is relatively high, that risk profile decreases substantially over time. The basis of the Growth Strategy with a Safety Net® is allowing time for the market to recover. Table 4.3 indicates how market volatility dissipates over time.

TABLE 4.3 Retirement Portfolio Equity (Stock) Allocation Guidelines Based on Growth Strategy with a Safety Net®

| Conservative | Moderate | Aggressive | |

| One-year downside riska | −17% | −22% | −29% |

| 10-year downside riska | 2% | 1% | 0% |

| 20-year downside riska | 6% | 6% | 6% |

| Expected returns (10 years+)b | 8.0% | 8.5% | 9.1% |

| Investment Mix: | |||

| Equities (stocks) | 60% | 70% | 85% |

| Fixed income (CDs, bonds, money market)c | 40% | 30% | 15% |

a One-year, 10-year, and 20-year downside risks are based on historical returns from 1946 to 2013.

b Return assumptions are based as follows:

- Equities 9.8%

- Fixed Income 5.4%

Returns are approximated and based on annualized returns for large cap stocks (equities) and intermediate-term government bonds from 1926 to 2013 (2013 Ibbotson® Stocks, Bonds, Bills, and Inflation® [SBBI®] Classic Yearbook).

c The fixed income portion of the portfolio should be based on the Growth Strategy with a Safety Net®. See pages 33–37.

Note: These portfolios are for postretirement investment accounts and should be used only as general guidelines. Asset allocation models might yield different risk objectives versus Growth Strategy with a Safety Net® allocations. Consult with your financial adviser. Investment results are not guaranteed. Risks and returns are targets only. Statistics are based on historical data indicating possible calendar year losses for equities of 37% and losses for fixed income of 5%.

As your retirement date approaches, you should begin to build your safety net ahead of time. For example, let's assume you plan to retire in seven years and you have decided that you want to protect six years' worth of your income (safety net). Continuing with our example in Table 4.1, the next year you would sell $78,000 worth of stocks (assuming the market is up!) and buy a bond that matures just before your retirement date. This will fund your first year's income. The following year, you will do the same thing: sell $78,000 of stocks and buy a bond that matures in five years. Using this strategy, by the time you retire, your safety net will be fully in place, and you will have maximized the growth potential of your investments until the time you need to begin drawing on them for your retirement income.

Withdrawal Rates

At this point it is important that you understand both the concept and the importance of the withdrawal rate (sometimes referred to as the withdrawal factor) as it relates to your portfolio.

Your withdrawal rate is equal to the percentage of dollars you are taking from your portfolio on an annual basis. For example, if you have $1 million in your investment portfolio and you take out $50,000 in a given year, your withdrawal rate is 5 percent ($50,000 ÷ $1,000,000). If your withdrawal rate is too high, you run the risk of depleting your investment account. Based on our experience, an appropriate withdrawal rate scale is as follows:

- Conservative: 4 percent or less

- Moderate: 5 percent

- Aggressive: 6 percent or more

This scale is sometimes adjusted for age and health factors. For example, a 9 percent withdrawal rate might not be considered aggressive for someone who is 95 years old and in ill health. But for our purposes, we'll use the scale described above. How you determine the appropriate withdrawal rate for you will be based on your particular circumstances and risk tolerance.

Prioritizing Your Investment Dollars

How do you maximize the power of your estate accumulation program? We have already seen how retirees can use the Growth Strategy with a Safety Net® to increase their retirement income while maintaining long-term growth. You can also significantly magnify the power of your estate accumulation program by choosing the best investment environment. The investment environment relates to whether the investment is a retirement account like a 401(k), traditional individual retirement account (IRA), or Roth IRA; a tax-deferred account such as an annuity; or a personal investment account. Each environment has its advantages and disadvantages, but some are better than others, particularly for accumulating money for your estate and retirement. By prioritizing where your investment dollars go, you can significantly enhance your long-term accumulation results. Let's begin with a review of your best options.

Retirement Planning: Choosing the Best Investment Environments

Under most circumstances, the best strategy for accumulating money for your retirement is through a qualified retirement plan. This may seem obvious, but you would be surprised at how often we find that people fail to understand this. For example, a new client was very concerned about saving for retirement. Every month he contributed 6 percent of his salary to a 401(k) plan, 50 percent of which was being matched by his employer. The plan allowed him to contribute up to 15 percent of his pay. When asked why he was not investing more money in his 401(k), he said he could not afford to contribute more. It turned out that he was paying several hundred dollars each month toward a whole life insurance policy. Through some rearranging of his life insurance, he was able to maintain the insurance policy without further premium payments and divert the insurance premiums into his 401(k). Not only would those life insurance premium dollars grow faster in his 401(k), but he got a tax deduction to boot! This is actually an easy mistake to make. To avoid it, you must review where all your investment dollars are going. To get the most benefit, invest the maximum allowable into tax deductible retirement plans before you invest any money in personal investment programs. This is a very important concept. Look at the dramatic differences depicted in Table 4.4.

TABLE 4.4 The Power of Retirement Plan Investing

| Compare: $1,000 per month invested on a pretax basis in a retirement plan vs.

paying the income tax on $1,000 per month and investing personally. |

||

| Retirement | vs. | Personal |

| $1,000 per month | $650 per montha | |

| × 25 years | × 25 years | |

| @10% | @9.8%b | |

| $1,337,890 | $840,422 | |

| Approximately 60% more!! | ||

a A 35% marginal tax bracket assumed. If your marginal tax bracket is higher (state income taxes, Medicare taxes, etc.), the results of investing personally worsen and vice versa.

b Assumes annual tax load of 0.20% related to taxes on dividends, etc.

Note: Retirement plan distributions will be subject to ordinary income taxes. Distributions from the personal investment program will likely be primarily subject to long-term capital gains taxes. (Federal maximum rate of 20% for taxpayers who earn more than $406,750 if single or $457,600 if married filing jointly). If held until death, the personal account would receive a stepped-up cost basis and income taxes would be avoided. If the retirement plan were held until death, a beneficiary (under certain circumstances) could continue to defer a large portion of the gain.

Retirement Plans

The power of retirement plans is created through one or more of the following:

- Tax deductibility of contributions

- Tax-deferred growth

- Tax-free growth (Roth IRA)

If your employer provides a contributory retirement plan such as a 401(k) plan, funding it should be your first priority, especially if the employer provides a matching contribution. If you are self-employed, you should consider starting your own retirement plan. You have numerous options available to you, including the Simplified Employee Pension Plan (SEP), single-person 401(k), profit-sharing plan, Savings Incentive Match Plan for Employees (SIMPLE), or defined benefit plan, as well as a number of variations. If you have employees, they must be included in your plan. Which one is best for you will depend on your specific circumstances. You'll need the help of a professional adviser to assist you in setting up one of these plans to make certain you maximize the benefits to you and that you follow the complex plan regulations.

Roth IRAs also require special consideration. With a Roth IRA, you don't receive an income tax deduction for your contribution, but your withdrawals are tax free. Typically, a Roth IRA is the best choice if your income tax bracket is relatively low. Note that certain restrictions apply to tax-free withdrawals for Roth IRAs. Although contributions are not tax deductible, earnings are tax-deferred, and withdrawals are tax-free under the following circumstances:

- Withdrawals are made at least five years after the Roth IRA was established and you are at least age 591/2.

- Withdrawals are made because of death or disability.

- Tax-free withdrawals of up to $10,000 are allowed to cover the expenses of purchasing your first home.

Don't forget that the spouse of an employee who participates in a company retirement plan is eligible to contribute to a Roth IRA or a traditional IRA even if that spouse has no earned income. The rules regarding the phase-out of deductibility of contributions are shown in Table 4.5.

TABLE 4.5 Phase-Out of Deductibility of Traditional IRA and Roth IRA Contributionsa

| Traditional IRA (if you are covered by a retirement plan at work) | |

| Single taxpayer and head of household | 2014 $60,000 to $70,000 |

| Married filing jointly | 2014 $96,000 to $116,000 |

| Married filing separately | 2014 $0 to $10,000 |

| Traditional IRA (if you are not covered by a retirement plan at work) | |

| Single taxpayer and head of household | 2014 Any amount |

| Married filing jointly or separately with spouse who is not covered by plan at work | 2014 Any amount |

| Married filing jointly with spouse who is covered by plan at work | 2014 $181,000 to $191,000 |

| Married filing separately with spouse who is covered by plan at work | 2014 $0 to $10,000 |

| Roth IRA | |

| Single taxpayer and head of household | 2014 $114,000 to $129,000 |

| Married filing jointly | 2014 $181,000 to $191,000 |

| Married filing separately | 2014 $0 to $10,000 |

a Phase-out is adjusted annually based on changes in the Consumer Price Index. Consult with your tax adviser for changes for 2015 or later.

Although you can contribute to both a traditional IRA and a Roth IRA, your total combined contribution cannot exceed $5,500 (plus an additional $1,000 if you are age 50 or older).

Although you can contribute to both a traditional IRA and a Roth IRA, your total combined contribution cannot exceed $5,000 (plus an additional $1,000 if you are age 50 or older).

If you are eligible for an IRA, you should invest in one. Are you better off with the deductible traditional IRA or the nondeductible Roth IRA? For many people, the Roth IRA will produce better results. However, it is not the hands-down winner. Again, you will need to do your homework or seek the aid of a financial adviser. Contributing to a Roth IRA is definitely better than contributing to a nondeductible traditional IRA, because neither contribution is deductible, but future distributions from the Roth IRA will be tax free if you follow the qualifying rules. Also, the Roth IRA is not subject to the required minimum distribution rules, which require that you to begin systematic withdrawals from retirement plans beginning after you turn age 701/2.

ROTH CONVERSIONS

The law allows you to convert your traditional IRA to a Roth IRA. If you choose to do so, you will owe ordinary income tax on the conversion for the tax year the conversion occurs. Should you convert your existing traditional IRA to a Roth IRA? There is no one right answer for everyone. What is best for you will depend on your particular circumstances. One thing that is clear is that it makes sense to convert only if you can pay the income taxes from proceeds outside of your IRA. Your financial adviser can help you run the numbers to see what is best for you, or you can do your own calculations at the Resource Center at www.welchgroup.com; click on “Links,” then “Roth Conversion Calculator.”

Retirement plans do have some disadvantages. First, if you take your money out before age 591/2, you will likely owe a 10 percent penalty in addition to ordinary income taxes on the proceeds. More important, retirement accounts (excluding Roth IRAs) convert what may have been long-term capital gains (for most taxpayers this rate will be 15 percent; for high income earners, it will be 20 percent) to ordinary income, taxed at your highest personal tax bracket. These disadvantages are typically overcome based on the value of the immediate income tax deduction and the tax deferral of income until withdrawn. It has also been our experience that we are better able to “manage” client's income taxes (and tax rates) during their retirement years allowing us to get money out of retirement plans at lower tax rates.

Magnify the Power of Your Retirement Plan Tenfold

Receiving an immediate tax deduction and tax-deferred growth are two powerful reasons for using retirement plans in your investment program. Is there a way to magnify these results? Under certain circumstances, the answer is most definitely yes. The determining factor is who you designate as your beneficiary. For many reasons, your primary beneficiary should usually be your spouse. However, we often find that people either leave their contingent beneficiary blank or they name their estate. This can be a big mistake. Let's assume that you have named your spouse as your primary beneficiary and you leave your contingent beneficiary blank. If your wife dies before you do, your retirement plan assets will automatically go to your estate and be distributed according to the terms specified in your will. Let's assume your will leaves everything to your children. Because your estate is the beneficiary, the income taxes on your retirement plan assets must be paid by December 31 of the fifth year following the year of your death. In other words, the advantage of tax deferral ends five years after you die. We'll refer to this as Option 1. If, however, you had named your children as the contingent beneficiary, they would have the option to continue deferring the majority of the retirement plan assets over their own lifetime. This is Option 2. Under these circumstances, to receive the maximum tax benefit, the law requires that your children begin mandatory distributions prior to December 31 of the calendar year following the year of death. However, the mandatory distributions are based on their life expectancy. This results in a reduced mandatory (taxable) distribution, thus allowing for a substantial continuation of tax deferral. There are two very important points here that you and your beneficiaries should be aware of. First, Option 2 is by far the best income tax strategy for the beneficiaries since it will allow them to stretch the income taxes over their respective lifetimes. In order to qualify for Option 2, the beneficiaries must begin taking the mandatory distributions by the deadline. Second, if there is more than one beneficiary, they must elect to “separate” the inherited IRA in order to use their own life expectancy for the calculation of the mandatory distribution. If they fail to do this, the life expectancy of the oldest beneficiary will be used. This is clearly a disadvantage for younger beneficiaries. It is also important to note that if you do not name an individual or individuals as your beneficiary, Option 1 is the only option your heirs will have. Let's look at two examples.

For our first example, assume that you are age 45 and you are the named beneficiary under your father's IRA in the amount of $200,000. He dies and you elect to receive only the minimum required distributions. Based on IRS life expectancy tables, your life expectancy is 38.8 more years (see Appendix C for IRS Life Expectancy Table). By dividing 38.8 into $200,000 you determine that your mandatory withdrawal for the first year is $5,155 or about 2.6 percent. If you actually earned, say, 6 percent, this means that you were able to continue to defer all of your $200,000 plus a portion of your earnings. Note that you must recalculate your required minimum distribution each year since your life expectancy changes each year. Over 38.8 years (your life expectancy according to the IRS), the combination of your mandatory withdrawals plus the remaining portfolio value exceeds $1 million!

For our second example, let's assume your father uses this strategy, naming your 25-year-old son (instead of you) as the beneficiary. Your son's life expectancy is 58.2 years. Your father dies and your son now elects to take minimum distributions (first year = $3,436) while deferring any additional growth. If the account earns an average of 7 percent per year, the account value would have grown to almost $1 million by the time he reaches age 65. This is in addition to the $737,000 in mandatory distributions that he took out over that time period! This strategy allows you to leverage a modest retirement account into a million-dollar financial asset.

Personal Investment Accounts

By now you know that you should invest the maximum amount allowable into your retirement plan(s) before you invest any money personally for your retirement. The main advantage of a personal investment program is that you have access to your money without penalties if you should need it. Doing so may trigger income taxes, but for investments held for more than 12 months, you will be taxed at the more favorable long-term capital gains rate (for most taxpayers, taxed at 15 percent federal rate; for high income taxpayers, taxed at 20 percent). Dividends paid on stocks of public corporations are also typically taxed at a favorable federal tax rate of 15 percent (20 percent for taxpayers subject to the highest marginal tax rate). This more favorable tax treatment of corporate dividends provides an incentive for investors to invest in dividend-paying stocks.

Still, the primary disadvantage of investing personally is the imposition of current taxation. For equities, the use of dividend-paying stocks or holding appreciated securities for long-term capital gains tax treatment will help reduce your tax bite. For fixed-income investments, you can invest in municipal bonds. The interest income from these bonds is not subject to federal income taxes, including the 3.8 percent surtax on investment income, and in certain cases is not subject to state, city, or county taxes, either. However, you should use some caution here. We often find that people who have bought municipal securities are in a relatively low tax bracket. They would have been better off, after taxes, having bought taxable securities. Remember, it's the net jingle in your pocket that counts. The formula for comparing taxable versus tax-free investments is as follows:

For example, if you are in the 28 percent federal tax bracket and you want to compare a tax-free bond yielding 3.0 percent to a taxable bond of similar quality and maturity yielding 4.5 percent, your calculation would be as follows:

From this example, obviously the taxable bond yielding 4.5 percent is preferable. Go to the Resource Center at www.welchgroup.com; click on “Links,” then “Tax Equivalent Yield Converter” for a financial calculator that can help you compare the net return on municipal versus taxable bonds.

It should be noted that all tax-free bonds are not entirely tax-free. Certain types of municipal bonds are subject to the alternative minimum tax. The Internal Revenue Service rules require you to first calculate your income taxes the usual way and then recalculate them the alternate way, which includes the interest income from certain municipal bonds. If the alternate method creates a larger tax, then that is the tax you must pay. To avoid this potential problem you must either buy municipal bonds that are not subject to the alternative minimum tax or make certain that you will not be subject to the tax. Your tax adviser can help you determine the best course for you.

Tax-Deferred Investment Programs

Tax-deferred investment programs fall into two main categories: tax-deferred annuities and cash value life insurance. The obvious advantage to these programs is having your money grow without being subjected to current income taxes. However, the disadvantages are also significant. Let's start by looking at annuities. Annuities have four main disadvantages:

- High expenses. Many annuities have relatively high expenses associated with their purchase. Annual expenses for annuities can exceed 2 percent. Portions of these premiums are used to cover mortality charges in the event you choose to have your account converted into a life income. Almost no one does, so this is a waste of money. Other expenses include commissions, policy fees, and a variety of other one-time and annual charges.

- Potentially higher taxes on withdrawals. An annuity converts what may have been long-term capital gains, which are taxed at a maximum federal tax rate of 20 percent, into ordinary income, for which federal tax rates can be as high as 39.6 percent. For example, if you bought a stock index fund, held it for 20 years, and then took your money out, your gains could be taxed at a maximum federal rate of 20 percent assuming your modified adjusted gross income in 2014 is equal to or more than $406,750 if single or $457,600 if married filing jointly (15 percent for taxpayers below these thresholds). If, however, you bought a variable annuity and through the annuity invested in a similar stock index fund, when you take your money out 20 years later the gain will be subject to ordinary income tax rates. Table 4.6 illustrates in dollar terms the disadvantages of annuities outlined here. Even worse, when you begin withdrawing money from your annuity after age 591/2, you will be taxed on a last-in, first-out basis unless you annuitize your payments. This means that you will pay ordinary income taxes on all distributions until you have withdrawn all of your profits. Once all profits have been withdrawn, all future withdrawals would be a return to cost basis and be tax free.

- Limited investment choices. Another major disadvantage of annuities is limited investment choices. Many have two dozen or fewer choices. Some have many more, but that's still limiting compared to being able to choose among the entire universe of over 10,000 mutual funds. By way of analogy, let's assume that you and I each have $100 million to buy a baseball team (never mind that this amount wouldn't even buy us a minor league team!). There are 20 teams in the league, and I give you first choice. Once you choose your team, you are stuck with it for the season. Now it's my turn. But instead of choosing a team, I get to choose individual players! Which option would you rather have?

- Potential tax penalties. The final disadvantage of annuities is that if you had to take your money out before age 591/2, you would incur a 10 percent penalty in addition to ordinary income taxes. There are cases in which annuities make sense, but they are rare. If someone is trying to sell you one, consult your financial adviser (one who doesn't sell products!) before signing on the dotted line.

TABLE 4.6 Comparison of Personal Investment vs. Variable Annuity

| Assume: Investor A invests in an S&P 500 index fund. | ||

| Investor B also invests in an S&P 500 index fund but uses a variable annuity. | ||

| Investor A without

Variable Annuity |

Investor B with

Variable Annuity |

|

| Account Growth for 30 Years: | ||

| After-tax contribution | $10,000 | $10,000 |

| Growth factora | ×16.52 | ×10.06 |

| Account value in 30 years | $165,200 | $100,600 |

| Tax Effect upon Sale in 30 Years: | ||

| Account value | $165,200 | $100,600 |

| Less capital gains taxb | −20,124 | −0 |

| Less ordinary income tax | −0 | −35,219 |

| Net to investor | $145,076 | $65,381 |

| Advantage to investor | $79,695 | |

a The growth factor for both index funds is based on 10% average annual return net of fund manager cost. The growth factor for the index fund that is held personally is reduced by the estimated income tax loads of 0.20% (i.e., tax on annual dividend distributions). The growth factor for variable annuity is reduced by the estimated average annual expenses associated with annuity products (2.0%).

b For index fund, reinvested dividends increase the cost basis.

Note: If both investors held their accounts until death, Investor A's heirs would receive a “stepped-up” cost basis and avoid all income taxes. Investor B's heirs would eventually be required to pay ordinary income taxes on all gains.

For retirees, annuities can provide a guaranteed income stream. You'll want to pay close attention to the credit quality of the insurance company you invest with since you'll be counting on them to make payments to you (and perhaps your spouse) as long as you live. Consider “spreading your risks” by investing with multiple insurance companies.

Life Insurance

Life insurance is a complex product and therefore is often confusing to the buying public. Let's see if we can demystify it a bit. All financial products, including life insurance, are a matter of mathematics. When you buy a cash value life insurance policy, your money (called premiums) goes to the insurance company. A portion of your premium is used to cover the risk of your dying prematurely. This is known as the mortality charge. You can think of it as the term insurance charge. Another portion goes to cover the insurance company's overhead, including agents' commissions. The remaining portion is invested by the insurance company for your benefit. The insurance companies have managed to secure some preferential tax treatment. First, the earnings in a cash value policy are tax-deferred until withdrawn. If you do withdraw part of your money, it is taxed on a first-in, first-out (FIFO) basis. This means that you pay no taxes until you have withdrawn all the money you contributed. If you never take your money out and die while the insurance is in force, your investment gains are never subject to income taxes. While dying is not our idea of a good investment strategy, we are always happy to avoid taxes.

As an investment, the disadvantages of cash value life insurance center around two issues: potentially high expenses and limited investment choices. Commissions and expenses can easily consume your first year's entire premium. Many contracts take 10 years or longer to break even (meaning your cash value is equal to what you've paid in premiums). Some policies are more competitive than this, but all contain high expenses when compared with direct investments into mutual funds, stocks, or bonds.

As with annuities, your investment options are extremely limited. We should add that cash value life insurance does have an important and appropriate place in estate planning, which we will discuss in Chapter 10. But if you are using it primarily as an investment vehicle, you can likely find better alternatives.

To summarize, if you have only a limited amount of money to invest, you will increase the power of your retirement investment program by prioritizing how those dollars are used. First, you want to invest through retirement plans to the maximum amount that the law allows before you invest any money in personal investment accounts. Additionally, you should consider your alternatives carefully before investing in tax-deferred vehicles such as annuities or cash value life insurance.

Some Final Thoughts on Investing

With each passing year our financial markets become more and more complex. Many of our long-held beliefs about what is safe versus what is risky have been shattered. We have witnessed the failure or near failure of some of the largest and oldest financial institutions in America. Formerly esteemed corporate executives have been exposed as nothing more than greedy people with mediocre talent whose focus was on producing quarterly results to impress Wall Street (and line their own pocketbook) at the expense of sound business decisions.

Now, more than ever, designing and monitoring a portfolio that is responsive to the financial markets we now find ourselves dealing with is more important than ever. If you don't have the time or inclination to do it properly, we recommend that you seek the assistance of a professional. If you would like assistance locating an adviser near you, contact one of us and we'll be happy to assist you. Our contact information is located in Appendix A.

In this chapter we have discussed the importance of investing for long-term growth and choosing the best investment environment for maximizing estate accumulation. In the next chapter, you will learn just how large an estate you will need in order to secure your financial future for as long as you live along with the best strategies for creating the retirement of your dreams.