CHAPTER 8

Using Trusts in Your Estate Plan

In Chapter 7, we reviewed the key elements that should be considered in all wills. At what point should you consider more complex estate planning? Additional planning is appropriate if you feel it is desirable to maintain some control over your property after you die. In this situation, establishing one or more trusts under your will may be advisable. Also, if you are married and the total of your and your spouse's estates (including life insurance death benefits) exceeds the applicable exclusion amount, you need to consider a more complex will. As you recall from the previous chapter, two important tax strategies may be available to you.

The first strategy, available only if you are married to a U.S. citizen, is called the unlimited marital deduction (or simply the marital deduction). Under federal tax laws, you may give an unlimited amount of assets to your spouse without incurring gift or estate taxes. These gifts can be made during your lifetime or at your death. This means that Bill Gates, reportedly one of the richest people in the world, could give or leave his entire fortune to his wife and the estate would not owe a dime of federal estate taxes. However, when she dies, taxes would be due. The marital deduction is available to legally married same-sex couples now that the Supreme Court declared Section 3 of the Defense of Marriage Act unconstitutional. We discuss strategies associated with the marital deduction later in this chapter.

The second strategy relates to the applicable exclusion amount. This section of the law allows you to give a certain amount of your assets to someone other than your spouse, either during your lifetime or at your death, free of federal gift or estate taxes. This “other” amount can be a trust called the credit shelter trust.

The Credit Shelter Trust Will

The purpose of the credit shelter trust will is to take advantage of the applicable exclusion amount and thus reduce the estate taxes that will be due when you and your spouse both die. Your credit shelter trust will can be set up for the specific purpose of benefiting your spouse and/or anyone else you desire. For example, for 2014 you could avoid federal estate taxes on up to $5,340,000 by placing that amount in your credit shelter trust as directed by your will (see Chapter 3, Table 3.1). Both you and your spouse can each use this exclusion, so if you plan well, the two of you could have combined estates of up to $10,680,000 in 2014 and owe no federal estate taxes. The applicable gift tax exclusion amount is $5,340,000 (indexed for inflation annually).

Case Study

It is the year 2014. Frank and Sally are married and have one child, Jan. Their combined estates equal $10,340,000. They remember from an estate planning seminar they attended that married couples may transfer $10,680,000 tax free because of portability. Sally owns $5,340,000 in her name and Frank owns $5,340,000 in his name. They currently have simple wills in which they leave all their assets to each other upon their death. Their current tax situation is as follows:

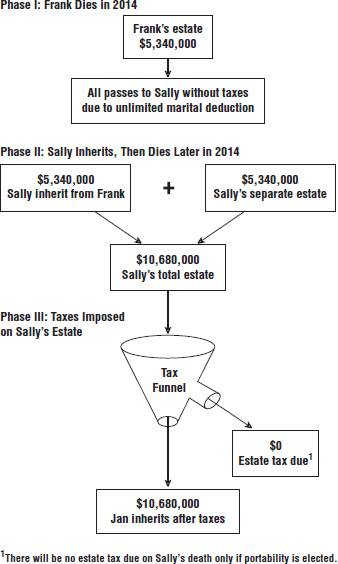

Possibly Ineffective Estate Plan Frank has a simple will and dies leaving an estate of $5,340,000 outright to Sally (see Figure 8.1) Frank's gross estate $5,340,000 Less unlimited marital deduction −$5,340,000 Taxable estate $0 Estate tax at Frank's death $0 Assets passing to Sally $5,340,000 Sally's gross estate: Sally's separate estate $5,340,000 Received from Frank's estate +$5,340,000 $10,680,000 Tentative Tax Calculation at Sally's Death Federal tax on $10,680,000 (per table) $4,217,800 Less unified credit (per table, includes DSUE amount) −$4,217,800 Estate tax at Sally's death $0 Net estate available for heirs $10,680,000 If Frank and Sally both die in 2014, they would not owe any estate tax due to portability. However, to elect portability, an estate tax return must be filed, which can be expensive. Furthermore, the deceased spouse's unused exclusion (DSUE) amount is not indexed for inflation, so that if the assets appreciate between the death of the first spouse and the death of the second spouse, then estate tax will be due on the amount of appreciation. For instance, if the assets appreciate to $13 million by the time the second spouse dies, then there would be approximately $928,000 of estate tax due. By utilizing a credit shelter trust will, there is greater certainty of a tax-efficient outcome:

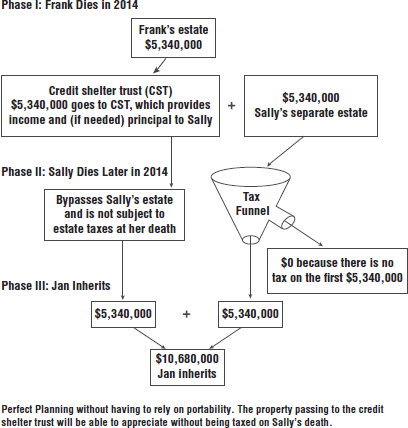

Effective Estate Plan Frank has a credit shelter trust will and dies in 2014 with an estate of $5,340,000 (see Figure 8.2) Frank's gross estate $5,340,000 Assets passing directly to Sally −$0 Assets passing to credit shelter trust −$5,340,000 Taxable estate $5,340,000 Estate tax $2,081,000 Less unified credit −$2,081,000 Net tax at Frank's death $0 Sally's own separate estate $5,340,000 Frank's assets passing directly to Sally $0 Sally's gross estate $5,340,000 Less unlimited marital deduction −$0 Sally's taxable estate $5,340,000 Tentative tax calculation on Sally's death $2,081,000 Less unified credit −$2,081,000 Estate tax at Sally's death $0 Value of assets in credit shelter trust (appreciation of $2,320,000) $7,660,000 Tax on assets held in credit shelter trust $0 Net estate available to heirs $13,000,000

FIGURE 8.1 Simple Will

FIGURE 8.2 Credit Shelter Trust Will

By utilizing a credit shelter trust will, we were able to eliminate Frank and Sally's potential federal estate tax liability that would result from strictly relying on portability. Because Frank's assets passed to the credit shelter trust, the appreciation escaped estate tax on Sally's death and we were able to preserve the maximum amount of assets for their heirs. Portability would require filing with the IRS an estate tax return and would not shield appreciating assets from estate tax—only the amount of the decedent's unused exclusion in the year he or she dies. In addition, this portability benefit could be lost if the surviving spouse remarried and the new spouse also dies. Utilizing the credit shelter structure outlined earlier allows the appreciation to be shielded from estate tax. You can also meet other goals including providing professional management of assets and protecting your assets from the potential future creditors of your surviving spouse. Note that the credit shelter trust will often is structured to provide your surviving spouse with all the income from the trust as well as the principal for certain specific reasons. Legally, these reasons are referred to as ascertainable standards and include distributions for health, maintenance, education, and support. This definition is sufficiently broad to cover most reasonable requests for additional money. In addition, the law permits what is referred to as the “five and five power.” If you choose to include this language in your trust, it would permit your spouse to take a distribution from the trust each year equal to 5 percent of its total value or $5,000, whichever is greater. Your surviving spouse can also serve as the trustee or cotrustee of the trust.

In working with clients, we sometimes recommend a provision that we call the remarriage provision. Some clients are primarily concerned with their surviving spouse's income needs only as long as he or she remains unmarried. If the surviving spouse remarries, the clients would prefer that the assets from their credit shelter trust benefit their children or some other beneficiary. To resolve this issue, a provision is included that states that if the surviving spouse remarries, his or her benefits under the credit shelter trust shall cease. Several years ago, we observed an interesting twist involving this remarriage provision. In this particular case, the surviving spouse remarried, thus forfeiting her interest in her deceased husband's credit shelter trust. Her second marriage failed within two months. Instead of getting a divorce, she got an annulment, which in effect revived her status as a surviving spouse, as well as her interest in the credit shelter trust!

Another provision to consider as part of your credit shelter trust will is the income sprinkling provision. This provision allows the trustee to pay trust income to trust beneficiaries other than the surviving spouse, typically the children. If the assets left to the surviving spouse outside of the credit shelter trust, when added to the surviving spouse's own assets, are expected to be more than sufficient for his or her lifestyle needs, then providing an income sprinkling provision will help reduce the size of the surviving spouse's estate when he or she dies. If you require the credit shelter trust to pay only the surviving spouse all of the trust income, you will effectively increase the estate taxes paid by the surviving spouse's estate and reduce the inheritance received by your heirs. This is because your surviving spouse, not needing the trust income, will stack it up in his or her estate, and it will only be taxed later. Not only is the income taxed, but the growth on the income is taxed as well. This sprinkling provision can be an effective tool that allows your trustee to distribute income to your family members who have the greatest needs. Note that if this sprinkling provision is used, your spouse can be a cotrustee but cannot be a sole trustee.

Disclaimers

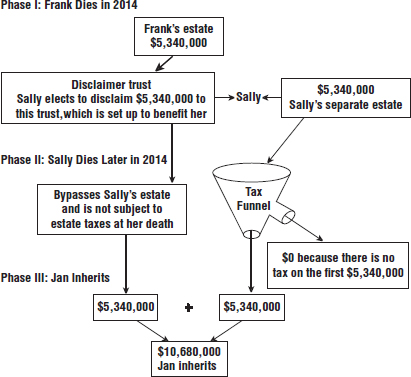

A disclaimer is the refusal to accept property that has been given to you either by gift or through someone's will. It may sound strange that anyone would refuse an inheritance, but there can be very good reasons for doing so. The most typical reason is to avoid or at least postpone estate taxes. Let's say that you are single and in your will you leave all your estate to your sister if she survives you; otherwise, you leave everything to her children. When you die, your sister is elderly and has a large estate of her own. She has no need for your money, so if she does receive it, it will be added to her estate and taxed at her death. Instead, she disclaims it. In the eyes of the law it is as if she has predeceased you, which means that under the terms of your will, it passes to her children. It will be a long time before they are likely to have to pay estate taxes on your money. Note that disclaimers are not all-or-nothing. Your sister could have disclaimed only a portion of your estate. She could even have disclaimed specific items of your estate. A disclaimer is often used in conjunction with a credit shelter trust and is called a disclaimer credit shelter trust will (or simply a disclaimer trust will). Essentially, a disclaimer credit shelter trust will is a simple will that allows the surviving heir(s) the option to convert to a trust-type will in order to reduce future estate taxes.

We revisit our first example with Frank, Sally, and their daughter, Jan. Suppose that when Frank and Sally first wrote their wills, they had a much smaller estate. They were, however, optimistic about their financial future, and they wanted their will to reflect that optimism. To accommodate them, their attorney prepared their will with disclaimers in mind. Frank's will was set up so that if Sally disclaimed any portion, that portion would go into a credit shelter trust that was set up to provide Sally with income (and principal for certain reasons). Sally now has the option of accepting the bequest from Frank or disclaiming the assets, which will be sent to the disclaimer credit shelter trust. This strategy allows her to do postmortem planning. If it is tax beneficial to do so, she disclaims the appropriate amount of money to a trust that is set up to benefit her. Graphically, the disclaimer credit shelter trust will is depicted in Figure 8.3.

FIGURE 8.3 Simple Will with Disclaimer Credit Shelter Trust Option

Certain criteria must be met for the disclaimed property to bypass the disclaiming heir's estate for estate tax purposes. First, the disclaimer must be irrevocable and unqualified. Second, it must be in writing. Third, you must not have accepted any interest in or received any benefit from the disclaimed property. Fourth, you must disclaim the property within nine months from the time you were eligible to receive it. Finally, you must have no say as to whom the disclaimed property goes.

Marital Trusts

Marital trusts will generally fall into one of three types: the general power of appointment trust, the qualified terminable interest property (QTIP) trust, and the qualified domestic trust (QDOT). The purpose of each is to allow you to exercise some control over how your assets will be handled after your death. Which trust you choose will depend on the degree of control you wish to exercise.

General Power of Appointment Trust

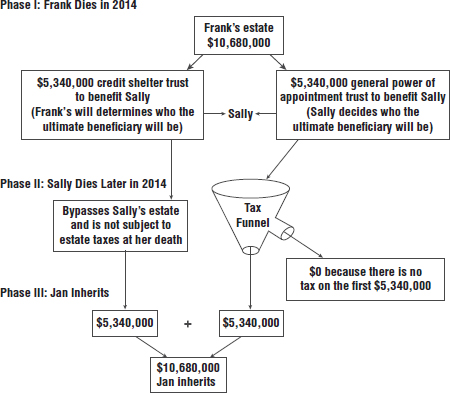

There may be situations in which it is not desirable to leave assets outright to your spouse. For example, if your spouse has little experience in managing money, you may want to remove that burden from him or her by establishing a trust run by a professional money manager. The general power of appointment trust allows you to place certain controls on the assets that you leave to your spouse while continuing to qualify those assets for the unlimited marital deduction. For this trust to qualify for the unlimited marital deduction and therefore not be taxed at your death, your spouse must receive all the income from the trust at least annually. Also, as the name implies, your spouse must be given a general power of appointment that allows him or her to determine which person(s) or organization(s) receives the trust property at his or her death. Other than these two requirements, the trust can be very flexible or very restrictive. You can give your spouse the power to terminate the trust, although most trusts of this type are irrevocable. You can give the trustee the power to distribute principal at his or her discretion. This makes certain that there will be access to trust principal for appropriate needs. At the opposite end of the spectrum, you can structure the trust so that your spouse receives only the income during his or her lifetime. As with the credit shelter trust and disclaimer trust, you can appoint your spouse as the trustee or the cotrustee, or you can have someone else serve as trustee. Often, the general power of appointment trust is used in conjunction with the credit shelter trust and graphically looks as depicted in Figure 8.4.

FIGURE 8.4 Two-Trust Will Utilizing a General Power of Appointment Trust and a Credit Shelter Trust

Notice that the use of the marital trust does not affect estate taxes. At your spouse's death, all the assets in the marital trust plus any of your spouse's separate property will be included in his or her estate for federal estate tax purposes. A disadvantage of the general power of appointment trust is that it is your spouse, not you, who determines who will eventually receive your property. If you would like to place more restrictions on the assets you leave your spouse, consider the benefits of the QTIP trust.

The Qualified Terminable Interest Property Trust

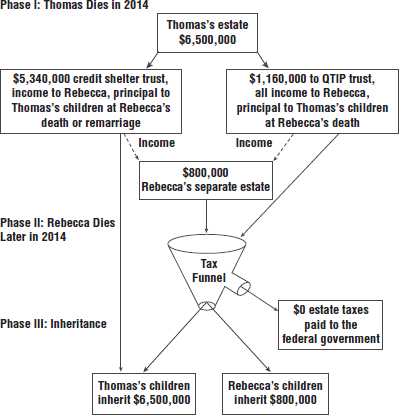

Under a QTIP trust, you decide who will ultimately receive your property at your spouse's death. This determination is specifically indicated in your will. As with the general power of appointment trust, to qualify for the marital deduction, your spouse must receive all the income from the trust at least annually. People often use QTIP trusts in cases of second marriages. Consider this example: Thomas and Rebecca recently married. They both have children from prior marriages and both have brought assets into the marriage. Thomas's total estate is $6,500,000, and Rebecca's assets total $800,000. Their goals are twofold. When the first of them dies, they would like their assets to be available as a source of income for the surviving spouse during that spouse's lifetime. At that spouse's death, they want to make certain that their assets go to their children. Their attorney recommends a QTIP trust. Under the provisions of the QTIP trust, if Thomas dies first, his assets would go into the trust and pay Rebecca all the income, at least annually, as long as she lives and no person has a power to appoint any part of the property to any person other than Rebecca. Because Rebecca is receiving all the income annually, and no person other than Rebecca can benefit from the property while she is alive, Thomas's property passing into the trust qualifies for the unlimited marital deduction upon an election by his executor and thereby avoids taxation at his death. The trust does not give Rebecca a general power of appointment and states that at her death the trust assets go to his children. Rebecca's will is a mirror of Thomas's will. As a result of this planning, both of their goals have been met. The surviving spouse has the income from the deceased spouse's estate, and the deceased spouse is certain that his or her estate eventually passes to his or her children.

The QTIP trust is an important planning technique. Think of what might happen without the QTIP trust. Thomas dies and leaves all of his assets to Rebecca with the presumption that she will take care of his children. Rebecca remarries and over time loses touch with Thomas's children. Her will already leaves all of her property to her children. When Rebecca dies, Thomas's children receive nothing. Alternatively, if Thomas dies without a will, the laws of intestacy in his state of residence direct that one-half of his property passes to Rebecca and the other half passes to his children. Rebecca later leaves her portion to her children. As with the marital trust, the QTIP trust is often used in conjunction with the credit shelter trust. Graphically, this planning strategy is depicted in Figure 8.5.

FIGURE 8.5 Two-Trust Will Utilizing a QTIP Trust and a Credit Shelter Trust

Figure 8.5 shows that at Rebecca's death in 2014, the assets from the QTIP trust ($1,160,000), which will go to Thomas's children, plus Rebecca's own separate assets ($800,000), which will go to her children, are added together for estate tax purposes. The result is that Rebecca's estate owes no federal estate taxes. However, if Thomas and Rebecca's combined estates exceed $10,680,000, some estate taxes are due at the death of the last to die. It is important to consider whether these taxes will come from Thomas's assets (the QTIP) or from Rebecca's assets. The law provides that any additional taxes caused by a QTIP trust shall be paid from the QTIP trust unless directed otherwise by the surviving spouse. You need to take special care here. Boilerplate language in many wills provides that all estate taxes are to be paid from the residuary estate. This oversight could result in all estate taxes of Rebecca's estate being paid from her children's share. To resolve this problem, both Thomas and Rebecca should have provisions in their wills requiring that any taxes caused by a QTIP trust will be paid from the QTIP trust assets.

Qualified Domestic Trust

If your spouse is not a U.S. citizen, you are not eligible for the unlimited marital deduction. (Congress reasoned that a non–U.S. citizen spouse might leave the United States in order to avoid U.S. taxes.) Currently, the maximum that you can transfer to a non–U.S. citizen spouse free of gift tax is $145,000 in 2014 (as indexed for inflation). In order to resolve this potentially unfair treatment, Congress passed a law allowing an unlimited marital deduction for property that is transferred to a QDOT. Requirements of a QDOT include the following:

- All income from the trust must be paid to the surviving spouse at least annually.

- The trust must be irrevocable.

- Certain IRS regulations must be included in the trust agreement that have the effect of ensuring that trust assets will not escape U.S. taxes.

- Generally, at least one of your trustees must be either a U.S. citizen or a U.S. corporation at all times. Be sure that your trust document has language that assures this result.

Certain foreign countries do not recognize either trusts or noncitizen trustees that, in effect, would prohibit you from establishing a QDOT. To address this problem, Congress has provided for the Treasury Department to make exceptions under certain conditions. If this is the case for you, consult with an attorney who specializes in such matters.

Spendthrift Trust

A spendthrift trust, originally intended as a way to protect people who tend to squander their money, is appropriate under numerous circumstances. Essentially, this trust provides the trustee with very strict guidelines as to how much and under what conditions money can be distributed to your beneficiary(s). The language in the trust forbids using the trust assets or the trust income as collateral or pledge for any type of loan. If a lender accepts any interest in the trust as a pledge, that pledge is not valid even if the loan is provable. The trustee can simply refuse to disperse funds to the creditor, and the creditor will have no recourse against the trust or trustee. Spendthrift trusts are normally set up for the lifetime of the beneficiary(s). Another circumstance where a spendthrift trust can prove useful is where a beneficiary, due to his or her profession, is a likely candidate for a lawsuit. The classic examples would include the doctor or commercial building contractor. Say your daughter is a physician and is concerned about being subject to a large malpractice judgment. Instead of giving your daughter her inheritance outright, you give it to her by way of a spendthrift trust. By doing so, those assets will be protected from creditors. However, in most states, it is not possible for you to receive this creditor protection by placing your own assets in a spendthrift trust. A spendthrift trust is also appropriate if you have a beneficiary who is incompetent.

Standby Trust

If you were to become incompetent because of an accident or sickness, who would handle your financial affairs? Would you want them to have specific instructions? If you don't know the answer to the first question, and/or you answer “yes” to the second question, then you might want to consider a standby trust (sometimes referred to as an unfunded revocable trust or living trust). This trust will state who your trustee will be and outline instructions for how trust assets are to be handled. The trust would remain unfunded until there is a triggering event, such as your incompetency. Your standby trust will be used in conjunction with a durable power of attorney that has specific language allowing your assets to be transferred to your trust under the conditions that you specify.

Other Trusts

With the exception of the standby trust just discussed, all the trusts that we have reviewed in this chapter have been testamentary trusts. That is, they are trusts that you created under your will. Inter vivos trusts are trusts that you create during your lifetime and can also be an important part of your estate-planning arsenal. They include the revocable living trust, the irrevocable insurance trust, the 2503(c) trust—which is sometimes referred to as the qualified minors trust—and various charitable trusts.

In Chapter 9, we discuss the details of the revocable living trust. Irrevocable insurance trusts are covered in Chapter 10, and the 2503(c) trust is discussed in Chapter 11. Charitable trusts are covered in Chapter 12.