Chapter 6 Study Questions

What is entrepreneurship?

What is special about small business entrepreneurship?

How do entrepreneurs start and finance new ventures?

Chances are you are already heavily involved in what many are now calling the new "app economy." Those tiny programs that fuel our fun and productivity on smartphones and devices such as the iPad have already created an annual market exceeding $1 billion, and growing fast. The money is made selling the apps, selling products through the apps, and selling advertising space within the apps.

Among the app players that have made it big is Zynga, the brainchild of Marc Pincus.[352] Zynga's revenues jumped to $150+ million in just three years. Pincus is self-described as having one part the DNA of an entrepreneur and a second part the DNA of a competitive gamer. The company's mission is to connect the world through online games such as its wildly popular FarmVille. And the connection has been made; some 120 million people play Zynga games each day.

Like its apps, Zynga isn't the typical business. Perhaps it's the Google influence, or perhaps it's Pincus's instincts; or maybe it's both. His firm operates with a fun culture that is heavy on the creativity side and very light on the corporate control side. Chefs cook two meals a day for Zynga's employees—why waste time going out for food?

A masseuse is on staff—who needs stress? And then there are the keg parties and poker tournaments—remember, it's a company that is based on having fun! And, yes, you can bring your pet to work.

As for Pincus, he's the guy in jeans and loose shirt—one among other casually dressed staffers. But don't let appearances fool you; he's all business. There's a lot at stake as the app economy grows bigger and more competitive every day. Zynga faces competition from the likes of Playfish and Playdom, and from the thousands of app programmers around the world. For now, Pincus is betting on Zynga's internal culture where freedom inspires teams of employees to work a tremendous number of hours together while creating what they each hope will be the next best fun app that everyone is clamoring to download.

Zynga is building a foundation for success based on a fun and flexible corporate culture. Don't you wonder if this could be the model for more organizations, not just those in the tech industries? And let's not forget another side of this story; there are thousands of people out there creating apps—on their own time and using their own creativity. Opportunities for entrepreneurship are everywhere; you just have to recognize them.

The many complex challenges of work and everyday living in our uncertain times call significantly upon one's capacities for self-management. It's an ability to use an objective understanding of one's strengths and weaknesses to continuously improve and adapt to meet life's challenges. Self-management is an essential skill that asks you to dig deep and continually learn from experience. After all, how are you going to take the best advantage of what experience offers, including possible entrepreneurship, if you don't know yourself well enough?

Think of it this way. In order to be strong in self-management you must have the ability to understand yourself individually and in the social context, to assess personal strengths and weaknesses, to exercise initiative, to accept responsibility for accomplishments, to work well with others, and to adapt by continually learning from experience in the quest for self-improvement.

Some self-management ideas are shown in the box. These and other foundations for career success are within everyone's grasp. But the motivation and the effort required to succeed must come from within. Only you can make the commitment to take charge of your destiny and become a self-manager.

According to author and consultant Steven Covey, you can move your career forward by (1) behaving like an entrepreneur, (2) seeking feedback on your performance continually, (3) setting up your own mentoring systems, (4) getting comfortable with teamwork, (5) taking risks to gain experience and learn new skills, (6) being a problem solver, and (7) keeping your life in balance.[353]

One of the best ways check your capacity for self-management is to examine how you approach college, your academic courses, and the rich variety of development opportunities available on and off campus. Test yourself. What activities are you involved in? How well do you balance them with academic and personal responsibilities? Do you miss deadlines or turn in assignments pulled together at the last minute? Do you accept poor or mediocre performance? Do you learn from mistakes? Take advantage of the end-of-chapter Self-Assessment feature to further reflect on your Entrepreneurship Orientation.

Visual Chapter Overview

6 Enterpreneurship, Social Enterprise, and New Ventures

Study Question 1 | Study Question 2 | Study Question 3 |

|---|---|---|

Nature of Enterpreneurship | Entrepreneurship and Small Business | New Venture Creation |

|

|

|

Learning Check 1 | Learning Check 2 | Learning Check 3 |

Need a job? Why not create one? That's what Jennifer Wright did after the financial crisis shut down her work as a credit analyst. While back at school in an MBA program she tweaked a friend's idea for a better pizza box and entered it in a b-school entrepreneurship competition. The "green box" as she calls it breaks into plates and a storage container before it goes for recycling. She says the feedback was "so incredibly positive I felt I'd be crazy not to pursue this."

Retired, feeling a bit old, and want to do more? Not to worry; people aged 55-64 are the most entrepreneurially active in the U.S. Realizing that he needed "someplace to go and something to do" after retirement, Art Koff, now 74, started RetireBrains.com. It's a Job board for retirees and gets thousands of hits a day. It also employs 7 people and keeps Koff as busy as he wants to be.

Struggling with work-life balance as a mother? You might find flexibility and opportunity in entrepreneurship. Denise Devine was a financial executive with Campbell Soup Co. Now she has her own line of fiber-rich juice drinks for kids. Called mompreneurs, women like Devine find opportunity in market niches for healthier products they spot as moms. Says Devine: "As entrepreneurs we're working harder than we did, but we're doing it on our own schedules."[354]

Female, thinking about starting a small business, but don't have the money? Get creative and reach out. You might find help with organizations like Count-Me-In. Started by co-founders Nell Merlino and Irish Burnett, it offers "microcredit" loans of $500 to $10,000 to help women start and expand small businesses. Borrowers qualify by a unique credit scoring system that doesn't hold against them things such as a divorce, time off to raise a family, or age—all things that might discourage conventional lenders. Merlino says: "Women own 38% of all businesses in this country, but still have far less access to capital than men because of today's process."[355]

Think about it. These examples should be inspiring. In fact, this is really a chapter of examples. The goal is not only to inform, but to also get you thinking about starting your own business, becoming your own boss, and making your own special contribution to society. What about it? Can we count you in to join the world of entrepreneurship and small business management?

The term entrepreneurship describes strategic thinking and risk-taking behavior that results in the creation of new opportunities. H. Wayne Huizenga, who started Waste Management with just $5,000 and once owned the Miami Dolphins says: "An important part of being an entrepreneur is a gut instinct that allows you to believe in your heart that something will work even though everyone else says it will not.[356]

• Entrepreneurship is risktaking behavior that results in new opportunities.

A classic entrepreneur is a risk-taking individual who takes action to pursue opportunities others fail to recognize, or may even view as problems or threats. Some people become serial entrepreneurs in that they start and run new ventures over and over again, moving from one interest and opportunity to the next. We find such entrepreneurs both in business and nonprofit settings.

• A classic entrepreneur is someone willing to pursue opportunities in situations others view as problems or threats.

• A serial entrepreneur starts and runs businesses and nonprofits over and over again, moving from one interest and opportunity to the next.

On the business side, H. Wayne Huizenga, mentioned earlier, is a serial entrepreneur who made his fortune founding and selling businesses like Blockbuster Entertainment, Waste Management, and AutoNation. A member of the Entrepreneurs' Hall of Fame, he describes being an entrepreneur this way: "We're looking for something where we can make something happen: an industry where the competition is asleep, hasn't taken advantage. It's going to be hard to find another Blockbuster, but that doesn't mean you can't have three good companies growing. The point is, we're going to be busy."[357]

On the nonprofit side, Scott Beale is more of a classic entrepreneur. He quit his job with the U.S. State Department to start Atlas Corps, something he calls a "Peace Corps in reverse." The organization brings nonprofit managers from India and Colombia to the United States to volunteer for local nonprofits while improving their management skills. After a year they return to a nonprofit in their home countries. "I am just like a business entrepreneur," Beale says, "but instead of making a big paycheck I try to make a big impact."[358]

Both Huizenga and Beale show entrepreneurial skill with first-mover advantage, moving quickly to spot, exploit, and deliver a product or service to a new market or an unrecognized niche in an existing one. Here are some other business entrepreneurs who were willing to take risks and sharp enough to spot the chance for first-mover advantage. Although each is unique as an individual, they share something in common that we all might aspire to—each built a successful business from good ideas and hard work.[359]

• A first-mover advantage comes from being first to exploit a niche or enter a market.

Mary Kay Ash

After a career in sales, Mary Kay Ash "retired" to write a book that she hoped would help women compete in the male-dominated business world. Then she realized she was writing a business plan. Her retirement lasted a month and she turned the plan into Mary Kay Cosmetics. Launched with an investment of $5,000, the company now operates worldwide and has been named one of the best companies to work for in America. Mary Kay's goal from the beginning was "to help women everywhere reach their full potential."

Caterina Fake

From idea to buyout only took 16 months. That's quite a benchmark for would-be Internet entrepreneurs. Welcome to the world of Flickr, started by Caterina Fake and her husband Stewart Butterfield. They took the notion of online photo sharing and turned Flickr in real-time into an almost viral Internet phenomenon. They also built the firm in the online environment without needing start-up capital; their families, friends, and angel investors provided the necessary financing. The payoff came when Yahoo! bought them out for $30 million. Fake's latest venture is Hunch.com, a website designed to help people make decisions such as: "Should I buy that new BMW?"

Earl Graves

With a vision and a $175,000 loan, Earl Graves started Black Enterprise magazine in 1970. That success grew into the diversified business information company Earl G. Graves, Ltd., including BlackEnterprise.com. Today the business school at his college alma mater, Baltimore's Morgan State University, is named after him. Graves says: "I feel that a large part of my role as publisher of Black Enterprise is to be a catalyst for black economic development in this country."

David Thomas

Have you had your Wendy's today? A lot of people have, and there's quite a story behind it. The first Wendy's restaurant opened in Columbus, Ohio, in 1969. It's still there, although there are also about 5,000 others now operating around the world. What began as founder David Thomas's dream to own one restaurant grew into a global enterprise. He became one of the world's best-known entrepreneurs and "the world's most famous hamburger cook." But there's more to Wendy's than profits and business performance. The company strives to help its communities, with a special focus on schools and schoolchildren. An adopted child, Thomas founded the Dave Thomas Foundation for Adoption.

Is there something in your experience that could be a pathway to business or nonprofit entrepreneurship? A common image of an entrepreneur is as the founder of a new enterprise that achieves large-scale success like the ones just mentioned. But that's only part of the story. Entrepreneurs and entrepreneurship are everywhere and there is no age prerequisite to join them.

Consider the stories of two "young" entrepreneurs. At the age of 22, Richard Ludlow turned down a full-time job offer and an MBA admission to start New York's Academic Earth. It's an online location for posting and sharing faculty lectures and other educational materials. His goal is to both make a profit and help society by lowering the cost of education. While in high school Jasmine Lawrence created her own natural cosmetics after having problems with a purchased hair relaxer. Products from her firm Eden Body Works can now be found at Wal-Mart and Whole Foods.[360]

There are lots of entrepreneurs to be found in any community. Just look around. Those who take the risk of buying a local McDonald's or Subway Sandwich or Papa John's franchise, open a small retail shop selling used video games or bicycles, start a self-employed service business such as financial planning or management consulting, or establish a nonprofit organization to provide housing for the homeless or deliver hot meals to house-bound senior citizens, are entrepreneurs in their own ways.[361] Entrepreneurs are found within larger organizations as well. Called intrapreneurs, they are people who step forward and take risk to introduce a new product or process, or pursue innovations that can change the organization in significant ways.

• Intrapreneurs display entrepreneurial behavior as employees of larger firms.

Research suggests that entrepreneurs tend to share certain attitudes and personal characteristics. The general profile is of an individual who is very self-confident, determined, resilient, adaptable, and driven by excellence.[362] You should be able to identify these attributes in the prior examples.

As shown in Figure 6.1, typical personality traits and characteristics of entrepreneurs include the following.[363]

Internal locus of control: Entrepreneurs believe that they are in control of their own destiny; they are self-directing and like autonomy.

High energy level: Entrepreneurs are persistent, hardworking, and willing to exert extraordinary efforts to succeed.

High need for achievement: Entrepreneurs are motivated to accomplish challenging goals; they thrive on performance feedback.

Tolerance for ambiguity: Entrepreneurs are risk takers; they tolerate situations with high degrees of uncertainty.

Self-confidence: Entrepreneurs feel competent, believe in themselves, and are willing to make decisions.

Passion and action orientation: Entrepreneurs try to act ahead of problems; they want to get things done and not waste valuable time.

Self-reliance and desire for independence: Entrepreneurs want independence; they are self-reliant; they want to be their own bosses, not work for others.

Flexibility: Entrepreneurs are willing to admit problems and errors, and are willing to change a course of action when plans aren't working.

Entrepreneurs tend to have unique backgrounds and personal experiences.[364] Childhood experiences and family environment seem to make a difference. Evidence links entrepreneurs with parents who were entrepreneurial and self-employed. And entrepreneurs are often raised in families that encourage responsibility, initiative, and independence. Another issue is career or work history. Entrepreneurs who try one venture often go on to others. Prior work experience in the business area or industry being entered is helpful.

Entrepreneurs also tend to emerge during certain windows of career opportunity. Most start their businesses between the ages of 22 and 45, an age spread that seems to allow for risk taking. However, age shouldn't be viewed as a barrier. When Tony DeSio was 50, he founded the Mail Boxes Etc. chain. He sold it for $300 million when he was 67 and suffering heart problems. Within a year he launched PixArts, another franchise chain based on photography and art.[365]

A report in the Harvard Business Review further suggests that entrepreneurs may have unique and deeply embedded life interests. The article describes entrepreneurs as having strong interests in creative production—enjoying project initiation, working with the unknown, and finding unconventional solutions. They also have strong interests in enterprise control—finding enjoyment from running things. The combination of creative production and enterprise control is characteristic of people who want to start things and move things toward a goal.[366]

Undoubtedly, entrepreneurs seek independence and the sense of mastery that comes with success. That seems to keep driving Tony DeSio from the earlier example. When asked by a reporter what he liked most about entrepreneurship, he replied: "Being able to make decisions without having to go through layers of corporate hierarchy—just being a master of your own destiny."

To help keep things in perspective, Management Smarts 6.1 debunks some common myths about entrepreneurship.[367]

When economists speak about entrepreneurs, they differentiate between those who are driven by the quest for new opportunities and those who are driven by absolute need.[368] Those in the latter group pursue necessitybased entrepreneurship, meaning that they start new ventures because they have few or no other employment and career options. Necessity-driven entrepreneurship is one way for people, often minorities and women who have hit the "glass ceiling" in their careers or are otherwise cut off from other employment choices, to strike out on their own and gain economic independence. In the case of Anita Roddick who founded the Body Shop, she says it began because she needed "to create a livelihood for myself and my two daughters, while my husband, Gordon, was trekking across the Americas."[369]

The National Foundation for Women Business Owners (NFWBO) reports that women own more than 9 million, about 38%, of all U.S. businesses and are starting new businesses at twice the rate of the national average.[370] Among women leaving private-sector employment to work on their own, 33% said they were not being taken seriously by their prior employer and 29% said they had experienced glass ceiling issues.[371] In Women Business Owners of Color: Challenges and Accomplishments, the NFWBO points out that the glass ceiling problems motivating women of color to pursue entrepreneurship include not being recognized or valued by their employers, not being taken seriously, and seeing others promoted ahead of them.[372]

Minority entrepreneurship is one of the fastest-growing sectors of our economy.[373] Businesses created by minority entrepreneurs now employ more than 4 million U.S. workers and generate over $500 billion in annual revenues. And the trend is upward. In the last census of small businesses, those owned by African Americans had grown by 45%, by Hispanics 31%, and by Asians 24%. Small businesses owned by women also had grown by 24%.[374]

Speaking of entrepreneurship, don't forget it can play an important role in tackling social issues: housing and job training for the homeless—bringing technology to poor families—improving literacy among disadvantaged youth—making small loans to start minority-owned businesses. These examples and others like them are all targets for social entrepreneurship, a unique form of ethical entrepreneurship that seeks novel ways to solve pressing social problems.

• Necessity-based entrepreneurship takes place because other employment options don't exist.

• Social entrepreneurship is a unique form of ethical entrepreneurship that seeks new ways to solve pressing social problems.

Real People

Entrepreneurs Find Rural Setting Fuels Solar Power

When she received the Ohio Department of Development's Keys to Success Award, Michelle Greenfield said, "It's exciting. It's kind of nice to be recognized as a good business owner. The goal is not to have the award, the goal is to have a good business and do well." She and her husband Geoff certainly do have a good business; it's called Third Sun Solar Wind and Power, Ltd.

Although the company's products are timely today, they were a bit ahead of the market in the beginning. The Greenfields began by building a home that used no electricity in rural Athens County, Ohio. Using solar power. They have yet to pay an electric utility bill. As friends became interested, they helped others get into solar power. The business kept growing from there. Third Sun has been ranked by Inc. magazine as the 32nd fastest growing energy business in the United States. It is the largest provider of solar energy systems in the Midwest and has experienced a 390% growth in three years. Quite a story for an idea that began with a sustainable home!

Michelle says that they lived very frugally in their rural home, and this helped them start the business on a low budget. Soon after its birth, Third Sun moved into the Ohio University Innovation Center, a business incubator dedicated to helping local firms grow and prosper. They have also benefited fromt apping the local workforce in a university town and from having MBA students work with their firm in consulting capacities.

As the company grew, Geoff focused on technical issues while Michelle spent most of her time on the business and managerial ones. She's now the CEO and, though primarily concerned with strategic issues as the firm grows, still keeps involved by helping the firm's 21 employees with other aspects of the business. "I do a lot of marketing," she says. "I do speaking engagements ... I serve on the Board of Directors of Green Energy Ohio."

Michelle says that the name "Third Sun ..." was chosen to represent a "third son" for the couple, one requiring lots of nurturing in order to help it grow big and strong. Even now, with a growing customer base, she says that the company is still in an "adolescent" stage where it still needs lots of attention, although the challenges of running the business at this stage are different from those in the start-up phase.

Social entrepreneurs that take risks to find new ways to solve social problems share many characteristics with other entrepreneurs. But, they are driven by a social mission and pursue innovations that help make lives better for people who are disadvantaged.[375] You can think of these problems as the likes of poverty, illiteracy, poor health, and even social oppression. Fast Company magazine tries to spot and honor social entrepreneurs that run organizations with "innovative thinking that can transform lives and change the world." Here are some recent winners on its prestigious annual Honor Roll of Social Enterprises of the Year.[376]

• A social entrepreneur takes risks to find new ways to solve pressing social problems.

Chip Ransler and Manoj Sinha—tackled the lack of power faced by many of India's poor villagers. As University of Virginia business students, they realized that 350 million people without reliable electricity lived in India's rice-growing regions. Noting that tons of rice husks were being discarded with every harvest, Ransler and Sinha started Husk Power Systems to create biogas from the husks and use the gas to fuel small power plants.

Neal Keny-Guyer—tackled the crowded field of microfinance in Indonesia, where more than 50,000 micro lenders serve 50 million people. But with as many as 110 million Indonesians struggling to live on $2 per day, Keny-Guyer's organization Mercy Corps bought a local bank that was in trouble and restructured it to serve as a banker for micro lenders. The goal was to boost the impact of microfinance in Indonesia by supporting it with topflight financial tools and technology, as well as capital.

Rose Donna and Joel Selanikio—tackled public health problems in Sub-Saharan Africa. Realizing that developing nations are often bogged down in the paperwork of public health, they created software to make the process quicker and more efficient, while increasing the reliability of the resulting databases. The UN, the World Health Organization, and the Vodafone Foundation are now helping their firm, DataDyne, move the program into 22 other African nations.

When you think social entrepreneurship, don't neglect what is happening in your community. Lots of social entrepreneurship takes place without much notice, flying under the radar so to speak. Attention most often goes to business entrepreneurs making lots of money, or trying to do so. But you can find many examples of people who have made the commitment to social entrepreneurship. Deborah Sardone is one. As the owner of a housekeeping service in Texas, she noticed that her clients with cancer really struggled with everyday household chores. This realization prompted her to start Cleaning for a Reason. It's a nonprofit that builds networks of linkages with cleaning firms around the country that are willing to offer free home cleaning to cancer patients.[377]

Note

✓Learning Check

Study Question 1

What is entrepreneurship?

Be sure you can ✓ define entrepreneurship and differentiate between classic and serial entrepreneurs ✓ list key personal characteristics of entrepreneurs ✓ explain the influence of background and experience on entrepreneurs ✓ define social entrepreneurship ✓ define necessity-based entrepreneurship ✓ discuss motivations for entrepreneurship by women and minorities

The U.S. Small Business Administration (SBA) defines a small business as one that has 500 or fewer employees, is independently owned and operated, and does not dominate its industry. Almost 99% of American businesses meet this definition, and some 87% of them employ fewer than 20 persons. Small businesses in the United States employ some 52% of private workers, provide 51% of private-sector output, receive 35% of federal government contract dollars, and provide as many as 7 out of every 10 new jobs in the economy.[378] Their importance was center stage when President Barack Obama used the following words to proclaim National Small Business Week in 2009, a time of major economic turmoil for America and the world.[379]

• A small business has fewer than 500 employees, is independently owned and operated, and does not dominate its industry.

Small businesses are the lifeblood of cities and towns across the country. Over the last decade, small businesses created 70 percent of new jobs, and they are responsible for half of all jobs in the private sector. They also help enhance the lives of our citizens by improving our quality of life and creating personal wealth. Small businesses will lead the way to prosperity, particularly in today's challenging economic environment.

There are many reasons why entrepreneurs launch their own small businesses. One study reports the following motivations: number 1—wanting to be your own boss and control your future; number 2—going to work for a family-owned business; and number 3—seeking to fulfill a dream.[380] The publication of a Gallup-Healthways Well-Being Index provides additional incentive to start your own business. It show that self-employed business and store owners outrank working adults in 10 other occupations—including professional, manager/executive, and sales, on such factors as job satisfaction and emotional and physical health.[381]

Roger the Plumber Enjoys Being in Control

His name really is Roger, and the company really is Roger the Plumber. The 14-person firm in Overland Park, Kansas, was founded by Roger Peugeot, and he has seen all the ups and downs of small business ownership—from growth to staff cutbacks. Yet he's happy, saying "I'm still excited to get up and go to work every day. Even when things get tough I'm still in control." Peugeot is one of many self-employed business owners that outranked 10 other occupational groups in a Gallup survey of job satisfaction and overall quality of life.

Once a decision is made to go the small business route, the most common ways to get involved are to start one, buy an existing one, or buy and run a franchise —where a business owner sells to another the right to operate the same business in another location. A franchise such as Subway, Quiznos, or Domino's Pizza runs under the original owner's business name and guidance. In return, the franchise parent receives a share of income or a flat fee from the franchisee.

• A franchise is when one business owner sells to another the right to operate the same business in another location.

In terms of small business startups, serial entrepreneur Steven Blank calls them temporary organizations that are trying "to discover a profitable, scalable business model." In other words, a startup is just that—a "start;" it's a new venture that the entrepreneur is hoping will take shape and prove successful as things move forward. Blank advises that the early goals of a startup should be to move fast and create a "minimum viable product" that will attract customers, and that can be further developed and made more sophisticated over time. He gives the example of Facebook which started with simple message sharing and keeps growing by moving into ever-more complex features. He also favors what are now being called lean startups. They take maximum advantage of things like opensource software and free Web services, while staying small and striving to keep all operations as simple as possible.[382]

• A startup is a new and temporary venture that is trying to discover a profitable business model for future success.

• Lean startups use things like open-source software, while staying small and striving to keep operations as simple as possible.

Today there are major opportunities in Internet entrepreneurship that makes direct use of the Internet to pursue entrepreneurial activities. The Interactive Advertising Bureau estimates that Internet-related businesses provide some three million jobs in the U.S. economy.[383] And although firms like Amazon.com, Yahoo!, Google, and Netflix may jump to mind, the role of smaller Internet businesses is also significant. Just take a look at the action on eBay and imagine how many people are now running small trading businesses from their homes.

• Internet entrepreneurship is the use of the Internet to pursue an entrepreneurial venture.

In our age of open-source software and ever-expanding access to high-speed broadband connections, the opportunities to pursue Internet-based entrepreneurship continue to grow. Some of the proven business models include the following.

• Internet entrepreneurship through the advertising model creates a website attractive to visitors, and then advertisers pay to be displayed on it.

• Internet entrepreneurship through the subscription model creates a website offering value that visitors are willing to pay to view.

Advertising model —this is the great Google play; you build a website that is attractive to visitors, and then advertisers pay you to be displayed on the site and become known to its visitors.

Subscription model —this is the New York Times online play; you offer something of value that visitors to your website are willing to pay to view.

Intermediary model —this is the eBay play; you build a website that brings buyers and sellers together, and collect a fee or commission for the service.

Transaction model —this is the Amazon.com play; you sell something through a website that customers are willing to buy.

• Internet entrepreneurship through the intermediary model creates a website that collects a fee for bringing buyers and sellers together.

• Internet entrepreneurship through the transaction model creates a website to sell something that customers are willing to buy.

The Small Business Administration states that some 85% of small firms are already conducting business over the Internet.[384] For some, the old ways of operating from a bricks-and-mortar retail establishment have given way to entirely online business activities. That's what happened to Rod Spencer and his S&S Sportscards store in Worthington, Ohio. He closed his store, not because business was bad; it was really good. But the nature of the business was shifting into cyberspace. When sales over the Internet became much greater than in-store sales, Spencer decided to follow the world of e-commerce. He now works from his own home with a computer and high-speed Internet connection. This saves the cost of renting retail space and hiring store employees. "I can do less business overall," he says, "to make a higher profit."[385]

In the little town of Utica, Ohio, there is a small child's desk in the corner of the president's office at Velvet Ice Cream Company. Its purpose is to help grow the next generation of leadership for the firm. "That's the way Dad did it," says Luconda Dager, the current head of the firm. "He exposed us all to the business at an early age." She and her two sisters, now both vice presidents, started working at the firm when they were 13 years old. And when it came time for Joseph Dager to retire and pass the business on to the next generation, he said: "It is very special for me to pass the baton to my oldest daughter. Luconda has been with us for 15 years. She understands and breathes the ice cream business, and there is no one better suited for this position.[386]

Velvet Ice Cream is the classic family business, one owned and financially controlled by family members. The Family Firm Institute reports that family businesses account for 78% of new jobs created in the United States and provide 60% of the nation's employment.[387] These family businesses must solve the same problems of other small or large businesses—meeting the challenges of strategy, competitive advantage, and operational excellence. When everything goes right, as in the Velvet Ice Cream case, the family firm is almost an ideal situation—everyone working together, sharing values and a common goal, and knowing that what they do benefits the family. But it doesn't always work out this way—or stay this way, as a business changes hands over successive generations. Indeed, family businesses often face quite unique problems.

• A family business is owned and controlled by members of a family.

DiFara's Pizza Is a Lesson in Love

In a small shop and at the postretirement age of 70+, Dominick DeMarco pursues his quest of making the perfect pizza. He makes all the pizzas, doesn't even start until he has an order, and grinds fresh Parmigiano Reggiano flown in from his native village in Italy. One newspaper reporter describes a DiFara's pizza as "a masterpiece, challenging my expectations every moment ... I sighed, wondering how pizza could be so good." The difference is Dominick. "He flies in his cheese because he loves it," the reporter says." He stretches dough only after it's ordered because he loves it. He does not run a restaurant—he makes pizza because he loves it."

Research Brief

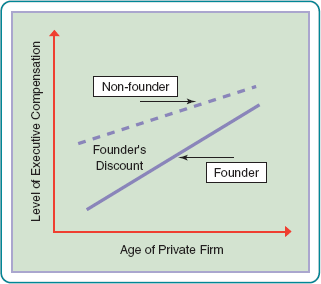

Do Founders of New Ventures Take Less Compensation than Other Senior Managers in Their Firms?

"Yes, but," says Noam Wasserman in an article published in the Academy of Management Journal. Wasserman examines two theories that might explain the founders' approaches to compensation. Stewardship theory argues that founders are likely to act as "stewards" of the firms they create, derive more psychic rewards from their roles in the enterprise, and, thus, take less monetary compensation. Agency theory argues that nonfounders are "agents" hired by founders to work in their behalf; agency costs are incurred because the interests of the founders and agents may diverge. Incentive compensation is one way of reducing those agency costs.

Wasserman hypothesized that founders will act more like stewards and nonfounder executives more like agents. He used data from 1,238 executives in 528 private companies to test his ideas. Of the executives, 41% were company founders. His results confirmed his hypotheses with an interesting twist. He found that founders and executives holding higher amounts of equity in a private firm earn less monetary compensation. In some cases (above 50%) founders even earned less than or equal to other executives reporting to them. He describes this as a "founder's discount" where they essentially "pay to be founders" and take more soft compensation in the form of psychic rewards.

Wasserman also found an interesting pattern in the data. As private firms grow in size, compensation for all executives increases. And as it does, the "founder's discount" becomes smaller.

You Be the Researcher

Would you have predicted that founders will take less monetary compensation from their new ventures? It might seem likely since they own most of the assets and will thus profit more in the long run, especially if the company is sold. They should also be highly motivated to work hard and make these financial gains and firm success possible. Suppose founders gave more equity to other executives and lower-level employees? Is it possible that we would find that private firms where ownership is shared widely among employees have lower compensation but also tend to grow and prosper in contrast to others?

Reference: Noam Wasserman, "Stewards, Agents and the Founder Discount: Executive Compensation in New Ventures,"Academy of Management Journal, vol. 49 (2006), pp. 960–76.

"Okay, Dad, so he's your brother. But does that mean we have to put up with inferior work and an erratic schedule that we would never tolerate from anyone else in the business?"[388] This complaint introduces a problem that can all too often set the stage for failure in a family business—the family business feud. Simply put, members of the controlling family get into disagreements about work responsibilities, business strategy, operating approaches, finances, or other matters. The example is of an intergenerational problem, but the feud can be between spouses, among siblings, or between parents and children. It really doesn't matter. Unless family disagreements are resolved to the benefit of the business itself, the firm will have difficulty surviving in a highly competitive environment.

• A family business feud occurs when family members have major disagreements over how the business should be run.

Another common problem faced by family businesses is the succession problem —transferring leadership from one generation to the next. A survey of small and midsized family businesses indicated that 66% planned on keeping the business within the family.[389] But the management question is: how will the assets be distributed, and who will run the business when the current head leaves? Although this problem is not specific to the small firm, it is very important in the family business context. A family business that has been in operation for some time is often a source of both business momentum and financial wealth. Ideally, both are maintained in the succession process. But data on succession are eye-opening. About 30% of family firms survive to the second generation; only 12% survive to the third; and only 3% are expected to survive beyond that.[390]

• The succession problem is the issue of who will run the business when the current head leaves.

Business advisers recommend having a succession plan —a formal statement that describes how the leadership transition and related financial matters will be handled when the time for changeover arrives. A succession plan should include at least procedures for choosing or designating the firm's new leadership, legal aspects of any ownership transfer, and financial and estate plans relating to the transfer. This plan should be shared and understood among all affected by it. And, the chosen successor should be prepared through experience and training to perform in the new role when the time comes.

• A succession plan describes how the leadership transition and related financial matters will be handled.

Small businesses have a high failure rate—one high enough to be intimidating. The SBA reports that as many as 60 to 80% of new businesses fail in their first five years of operation.[391] Part of this is a "counting" issue—the government counts as a "failure" any business that closes, whether it is because of the death or retirement of an owner, sale to someone else, or inability to earn a profit.[392] Nevertheless, the fact remains that a lot of small business startups don't make it. As shown in Figure 6.2, most of the failures are the result of insufficient financing, and bad judgment and management mistakes of several types.[393]

Insufficient financing— not having enough money available to maintain operations while still building the business and gaining access to customers and markets.

Lack of experience —not having sufficient know-how to run a business in the chosen market or geographical area.

Lack of expertise —not having expertise in the essentials of business operations, including finance, purchasing, selling, and production.

Lack of strategy and strategic leadership —not taking the time to craft a vision and mission, nor to formulate and properly implement a strategy.

Poor financial control —not keeping track of the numbers, and failure to control business finances and use existing monies to best advantage.

Growing too fast —not taking the time to consolidate a position, fine-tune the organization, and systematically meet the challenges of growth.

Lack of commitment —not devoting enough time to the requirements of running a competitive business.

Ethical failure —falling prey to the temptations of fraud, deception, and embezzlement.

Individuals who start small businesses face a variety of challenges. Even though the prospect of being part of a new venture is exciting, the realities of working through complex problems during setup and the early life of the business can be especially daunting. Fortunately, there is often some assistance available to help entrepreneurs and owners of small businesses get started.

One way that start-up difficulties can be managed is through participation in a business incubator. These are special facilities that offer space, shared administrative services, and management advice at reduced costs with the goal of helping new businesses become healthy enough to survive on their own. Some incubators are focused on specific business areas such as technology, light manufacturing, or professional services; some are located in rural areas, while others are urban based; some focus only on socially responsible businesses.

• Business incubators offer space, shared services, and advice to help get small businesses started.

Regardless of their focus or location, business incubators share the common goal of increasing the survival rates for new start-ups. They want to help build new businesses that will create new jobs and expand economic opportunities in their local communities. An example is Y Combinator, an incubator located in Mountain View, California. It was founded by Paul Graham with a focus on Web start-ups, and supports about 10 start-ups at any given time. The entrepreneurs get offices, regular meetings with Graham and other business experts, and access to potential investors. They also receive $15,000 grants in exchange for the incubator taking a 6% ownership stake. Y Combinator hopes to capture a significant return on such investments as the new businesses succeed.[394]

Another source of assistance for small business development is the U.S. Small Business Administration. Because small business plays such a significant role in the economy, the SBA works with state and local agencies as well as the private sector to support a network of over 1,100 Small Business Development Centers (SBDCs) nationwide.[395] These SBDCs offer guidance to entrepreneurs and small business owners, actual and prospective, on how to set up and manage business operations. They are often associated with colleges and universities, and some give students a chance to work as consultants with small businesses at the same time that they pursue their academic programs.

• Small Business Development Centers founded with support from the U.S. Small Business Administration provide advice to new and existing small businesses.

Note

✓Learning Check

Study Question 2

What is special about small business entrepreneurship?

Be sure you can ✓ give the SBA definition of small business ✓ illustrate opportunities for entrepreneurship on the Internet ✓ discuss the succession problem in family-owned businesses and possible ways to deal with it ✓ list several reasons why many small businesses fail ✓ explain how business incubators work and how both they and SBDCs can help new small businesses

Whether your interest is low-tech or high-tech, online or offline, opportunities for new ventures are always there for the true entrepreneur. To begin, you need good ideas and the courage to give them a chance. But then you must also be prepared to meet and master the test of strategy and competitive advantage. Can you identify a market niche on a new market that is being missed by other established firms? Can you generate first-mover advantage by exploiting a niche or entering a market before competitors? These are among the questions that entrepreneurs must ask and answer in the process of beginning a new venture.

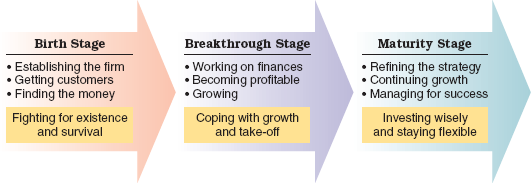

Figure 6.3 describes the stages common to the life cycles of entrepreneurial companies. It shows the relatively predictable progression from birth to breakthrough to maturity.

The firm begins with the birth stage —where the entrepreneur struggles to get the new venture established and survive long enough to test the viability of the underlying business model in the marketplace. The firm then passes into the breakthrough stage —where the business model begins to work well, growth is experienced, and the complexity of managing the business operation expands significantly. Next comes the maturity stage —where the entrepreneur experiences the advantages of market success and financial stability, while also facing the continuing management challenge of remaining competitive in a changing environment.

Entrepreneurs often deal with substantial control and management dilemmas when their firms experience growth, including possible diversification or global expansion. They encounter a variation of the succession problem described earlier for family businesses. This time, the problem is transitioning from entrepreneurial leadership to professional strategic leadership. Entrepreneurial leadership brings the venture into being and sees it through the early stages of life. Professional strategic leadership manages and leads the venture into maturity as an everevolving and perhaps still-growing corporate enterprise. If the entrepreneur is incapable of meeting or unwilling to meet the firm's strategic leadership needs, continued business survival and success may well depend on the business being sold, or management control being passed to professionals.

When people start new businesses or even launch new units within existing ones, they can benefit from a good business plan. This plan describes the details needed to obtain start-up financing and operate a new business.[396] Banks and other financiers want to see a business plan before they loan money or invest in a new venture; senior managers want to see a business plan before they allocate scarce organizational resources to support a new entrepreneurial project. And, there's good reason for this.

• A business plan describes the direction for a new business and the financing needed to operate it.

The detailed thinking required to prepare a business plan can contribute to the success of the new initiative. It forces the entrepreneur to think through important issues and challenges before starting out. Says Ed Federkeil, who founded a small business called California Custom Sport Trucks: "It gives you direction instead of haphazardly sticking your key in the door every day and saying—'What are we going to do?'"[397] More thoughts on why you need a business plan are presented in Management Smarts 6.2.

Although there is no single template, it is generally agreed that a good business plan includes an executive summary, covers certain business fundamentals, is well organized with headings and easy to read, and runs no more than about 20 pages in length. Here is a sample business plan outline.[398]

Executive summary —overview of the business purpose and highlight of key elements of the plan.

Industry analysis —nature of the industry, including economic trends, important legal or regulatory issues, and potential risks.

Company description —mission, owners, and legal form.

Products and services description —major goods or services, with competitive uniqueness.

Market description —size of market, competitor strengths and weaknesses, fiveyear sales goals.

Marketing strategy —product characteristics, distribution, promotion, pricing, and market research.

Operations description —manufacturing or service methods, supplies and suppliers, and control procedures.

Staffing description —management and staffing skills needed and available, compensation, and human resource systems.

Financial projection —cash flow projections for one to five years, breakeven points, and phased investment capital.

Capital needs —amount of funds needed to run the business, amount available, and amount requested from new sources.

Milestones —a timetable of dates showing when key stages of the new venture will be completed.

One of the important choices that must be made in starting a new venture is the legal form of ownership. There are a number of alternatives, and the choice among them requires careful consideration of their respective advantages and disadvantages.

A sole proprietorship is simply an individual or a married couple pursuing business for a profit. This does not involve incorporation. One does business, for example, under a personal name—such as "Tiaña Lopez Designs." A sole proprietorship is simple to start, run, and terminate, and it is the most common form of small business ownership in the United States. However, the business owner is personally liable for business debts and claims.

• A sole proprietorship is an individual pursuing business for a profit.

A partnership is formed when two or more people agree to contribute resources to start and operate a business together. It is usually backed by a legal and written partnership agreement. Business partners agree on the contribution of resources and skills to the new venture, and on the sharing of profits and losses. The simplest and most common form is a general partnership where the partners share management responsibilities. A limited partnership consists of a general partner and one or more "limited" partners who do not participate in day-to-day business management. They share in the profits, but their losses are limited to the amount of their investment. A limited liability partnership, common among professionals such as accountants and attorneys, limits the liability of one partner for the negligence of another.

• A partnership is when two or more people agree to contribute resources to start and operate a business together.

Real Ethics

TOMS Walks Pathways to Philanthropy

Would you buy shoes just because they're also pledged to philanthropy? Blake Mycoskie, founder of TOMS Shoes, wants you to. Back in 2002 he was participating with his sister in the reality TV show The Amazing Race. It whetted his appetite for travel and he visited Argentina in 2006. There he came face-to-face with lots of young children without shoes, and he had a revelation: he would return home and start a sustainable business that would help address the problem.

Blake launched TOMS (short he says for "better tomorrow") to sell shoes made in a classic Argentinean style. But there's a twist–for each pair of shoes it sells, TOMS donates a pair to needy children. Blake calls this One for One, a "movement" that involves "people making everyday choices that improve the lives of children."

The TOMS business model can be described as caring capitalism, or profits with principles. Two other names associated with this approach are Ben & Jerry's Ice Cream and Tom's of Maine. But each of these firms was sold to a global enterprise–Unilever for Ben & Jerry's and Colgate-Palmolive for Tom's of Maine. The expectation was that the corporate buyers wouldn't compromise on the founder's core values and social goals. Who knows what the future holds for TOMS if it grows to the point where corporate buyers loom.

You Decide

What about it? Is the TOMS business model one that others should adopt? Is it ethical to link personal philanthropic goals with the products that your business sells? And if an entrepreneurial firm is founded on a caring capitalism model, is it ethical for a future buyer to reduce or limit the emphasis on social benefits?

A corporation, commonly identified by the "Inc." designation in a name, is a legal entity that is chartered by the state and exists separately from its owners. The corporation can be for-profit, such as Microsoft, Inc., or nonprofit, such as Count-Me-In, Inc.—a firm featured early in the chapter for helping women entrepreneurs get started with small loans. The corporate form offers two major advantages: (1) it grants the organization certain legal rights (e.g., to engage in contracts), and (2) the corporation becomes responsible for its own liabilities. This separates the owners from personal liability and gives the firm a life of its own that can extend beyond that of its owners. The disadvantage of incorporation rests largely with the cost of incorporating and the complexity of the documentation required to operate as an incorporated business.

• A corporation is a legal entity that exists separately from its owners.

Recently, the limited liability corporation, or LLC, has gained popularity. A limited liability corporation combines the advantages of the other forms—sole proprietorship, partnership, and corporation. For liability purposes, it functions like a corporation and protects the assets of owners against claims made against the company. For tax purposes, it functions as a partnership in the case of multiple owners and as a sole proprietorship in the case of a single owner.

• A limited liability corporation is a hybrid business form combining the advantages of the sole proprietorship, partnership, and corporation.

Have you seen the reality TV show Shark Tank ? It pits entrepreneurs against potential investors called "sharks." The entrepreneurs present their ideas, and the sharks, people with money to invest, debate the worthwhileness of investing in their businesses. Brian Duggan went on the show to pitch his Element Bars, a custom energy bar he developed as an MBA student. He tried to get a bank loan, but failed. But the sharks were impressed and gave him $150,000 in return for 30% ownership in his business.[399]

While being part of a reality TV show isn't common, Brian Duggan's situation is characteristic of that faced by entrepreneurs. Starting a new venture takes money, and that money must often be raised. Realistically speaking, the cost of setting up a new business or expanding an existing one can easily exceed the amount a wouldbe entrepreneur has available from personal sources. Initial start-up financing might come from personal bank accounts and credit cards. Very soon, however, the chances are much more money will be needed to sustain and grow the business. There are two major ways an entrepreneur can obtain such outside financing for a new venture.

Debt financing involves going into debt by borrowing money from another person, bank, or financial institution. This loan must be paid back over time, with interest. It also requires collateral that pledges business assets or personal assets, such as a home, to secure the loan in case of default. The lack of availability of debt financing became a big issue during the recent financial crisis, and the problem hit entrepreneurs and small business owners especially hard. Andy Shallal, for example, owns a successful bookstore in the Washington, D.C., area. He employs 40 people and wanted to expand to other locations. But even with this track record he couldn't get a bank loan for the expansion without pledging his home as collateral, something he didn't want to do. Shallal says: "I want to have a loan that's really a business loan that's going to use my business as collateral. And I was told no, in these economic times it's very difficult for banks to give money this way."[400]

• Debt financing involves borrowing money that must be repaid over time, with interest.

Equity financing is an alternative to debt financing. It involves giving ownership shares in the business to outsiders in return for their cash investments. This money does not need to be paid back. It is an investment, and the investor assumes the risk for potential gains and losses. The equity investor gains some proportionate ownership control in return for taking that risk.

• Equity financing involves exchanging ownership shares for outside investment monies.

Equity financing is usually obtained from venture capitalists, companies and individuals that make investments in new ventures in return for an equity stake in the business. Most venture capitalists tend to focus on relatively large investments of $1 million or more, and they usually take a management role, such as a board of director's seat, in order to oversee business growth. The hope is that a fast-growing firm will gain a solid market base and be either sold at a profit to another firm or become a candidate for an initial public offering. This IPO is when shares of stock in the business are first sold to the public and begin trading on a stock exchange. When an IPO is successful and the share prices are bid up by the market, the original investments of the venture capitalist and entrepreneur rise in value. The quest for such return on investment is the business model of the venture capitalist.

• Venture capitalists make large investments in new ventures in return for an equity stake in the business.

• An initial public offering, or IPO, is an initial selling of shares of stock to the public at large.

When large amounts of venture capital aren't available to the entrepreneur, another financing option is the angel investor. This is a wealthy individual who is willing to make a personal investment in return for equity in a new venture. Angel investors are especially common and helpful in the very early start-up stage. Their presence can raise investor confidence and help attract additional venture funding that would otherwise not be available. For example, when Liz Cobb wanted to start her sales compensation firm, Incentive Systems, she contacted 15 to 20 venture capital firms. She was interviewed by 10 and turned down by all of them. After she located $250,000 from two angel investors, the venture capital firms got interested again. She was able to obtain her first $2 million in financing and has since built the firm into a 70-plus employee business.[401]

• An angel investor is a wealthy individual willing to invest in a new venture in return for equity in a new venture.

Note

✓Learning Check

Study Question 3

How do entrepreneurs start and finance new ventures?

Be sure you can ✓ explain the concept of first-mover advantage ✓ illustrate the life cycle of an entrepreneurial firm ✓ identify the major elements in a business plan differentiate sole proprietorship, partnership, and corporation ✓ differentiate debt financing and equity financing ✓ explain the roles of venture capitalists and angel investors in new venture financing