8

MARKETBUSTER CASE STUDY

ROYAL INSURANCE ITALY

IN 1994 Clive Mendes carried out a strategic review for Lloyd Italia Spa, which was at the time the largest Italian subsidiary of the British Royal Insurance Group. At the time, the Italian legislative and cultural framework was undergoing many changes, and Mendes believed that an opportunity was developing to bust the market for personal lines insurance, particularly motor (auto) insurance.

When Mendes looked at the auto insurance market, he saw a large market (30 million vehicles). Some three hundred insurance companies were offering coverage, but three large, well-known Italian “institutions” dominated: SAI, RAS, and Generali.

Distribution was predominantly by means of tied agents—self-employed agents who worked exclusively for one company. Even a medium-sized company could have several thousand of these agents, whose work arrangements varied from one-man shows to sizable organizations involving a number of subagents. This scenario is not very different from that in many European countries, with two exceptions. First, auto insurance premiums and policy conditions were set by the Italian government and, second, there was an extraordinary degree of customer dissatisfaction with the insurance service received.

Mendes knew that the European Union was about to require all European governments to “liberalize” their auto insurance markets. This would mean that individual companies would be free to set their own prices and conditions. He guessed that most Italian companies would not be ready, after many years of simply administering a government tariff, to make a rapid transition to a more advanced, personalized form of pricing. Mendes’s view was that in many cases they lacked the knowledge, the data, and the necessary in-depth statistical analyses. What’s more, there was an inherent cultural conservatism or mindset that would make it difficult for most insurers to make the needed radical changes in the short term. They would get there eventually, but in the meantime there would be a few years for a creative first-mover to bust the market and redraw the playing field.

What Mendes had in mind was creating a direct distribution company somewhat similar to Direct Line in the U.K. Direct Line was the first U.K. company to take advantage of advances in IT and in call center technology to sell auto insurance to customers over the phone as well as manage customer claims and damage repair from centralized locations. This model relies on operating efficiency to create price advantages as well as improved customer service from longer operating hours and homogenous, controlled interaction with clients. The Royal Insurance Group had also adopted this model in the U.K., setting up a direct company in 1988 called The Insurance Service (TIS) and, around the same time, a small but very successful company in Barcelona called Regal Insurance Club.

TIS operated very similarly to Direct Line. It had a fairly wide target group of customers and was focused on operating excellence as its principal strategic positioning. Regal was different. It had a narrower target market—the best drivers—and, as its name suggests, customers who qualified (for the club) with a good driving record were rewarded with excellent service and attractive prices.

Royal Insurance, however, was not simply a clone of Direct Line, nor of TIS and Regal. Royal Insurance had to succeed in a very different market. Mendes believed that it was possible to put together a recipe that would take advantage of a uniquely differentiated approach focused on the high degree of customer dissatisfaction with auto insurance in Italy. Customer research suggested that customers considered the purchase of compulsory third-party auto insurance as something akin to a tax. They strongly resented buying it, and often the experience was unpleasant and frustrating from a customer perspective. Claims were processed slowly by big, bureaucratic institutions, and customers had no voice or means of reaching decision makers except through the agents, who often didn’t have the influence they professed to have. Importantly, customers also generally tarred all insurers with the same brush. In short, insurance was a grudge purchase.

Therefore, Mendes decided that he could be successful only if the business system created happy customers who would spread the news that there was a different type of insurance company in the market—one that sold the kind of products that customers wanted to buy, at prices that were reasonable, and with a quality of service that was second to none. He also believed that if he was successful and consistent in pleasantly surprising his customers, then, in addition to spreading the word to family and friends, they would be more loyal, or at least their inherent conservatism would make them less likely to be tempted by competitors’ offers.

Thus there was a major opportunity to revolutionize the attribute map at several links in the consumption chain in the following ways:

- By reducing several dissatisfiers: purchasing, claims processing, and customer service

- By adding positive differentiators in the form of lower premiums for drivers having good risk profiles

- By offering a menu of coverage from which to choose

The challenge therefore was to design a company that would stand out from the rest by outperforming its rivals in customer satisfaction and profitability.

Business Philosophy

The Royal Insurance Italy business was founded on the following five basic principles, which Mendes and his team view as the keys to long-term success.

Customer Satisfaction. This belief is ingrained in the company’s psyche. All processes, products, and activities are built from the customers’ perspective and incorporate their views and priorities. The company obtains this information directly from customers by means of feedback processes such as questionnaires, focus groups, a “customer charter” (discussed in a moment), and an attention to customer relations throughout the organization. This has resulted in delivery of prize-winning customer satisfaction and consistently high customer-retention levels of more than 90 percent.

Operational Excellence. Similarly, Mendes believed that he could sustain his initial success by pursuing levels of operational efficiency that were better than the norm. Operational excellence means getting things right the first time and getting things done as quickly as possible at the lowest required level of competence in the organization and with maximum automation. Over the years the firm has redesigned the way it does things. Wherever possible, the preference is to make step changes in quality rather than incremental improvement.

Personal Responsibility. Royal employs people who enjoy taking responsibility for doing a good job and for developing themselves and others while being passionate about providing solutions to customers’ needs. Royal’s leaders (formal and otherwise) set the example to support this ideal, and the rewards and recognition systems have been recast to ensure that successes are recorded, rewarded, and celebrated. With the exception of a few technical positions and some outstanding people, the company’s preference is to choose managers and staff from outside the insurance industry.

Image Management. Royal Italy was aware of the importance of its brand as an instrument for influencing its key constituents: customers, distributors, staff, and society. It has kept careful control of its image and has actively used every medium to ensure the consistency of its message, including advertising, promotions, public relations, public affairs, and customer relations management. The name Royal Insurance was chosen because customer tests showed that it had positive connotations of service, quality, and tradition—attributes that the company thought it would need to convince customers of its seriousness as well as to develop its own institutional image power to match that of the large Italian insurers.

“Knowing Our Business.” The business philosophy of Royal Insurance is supported by a highly sophisticated data management system that covers everything from technical knowledge to understanding customers as well as understanding and influencing the market environment.

Making a MarketBusting Move

Capitalizing on the opportunity to bust the market via exploitation of a shift in industry dynamics, Mendes and his team put together a six-pronged marketbusting program to capitalize on the regulatory changes by the Italian government:

- Radical resegmentation at the purchase link

- Radical changes in the service link

- Revolutionized pricing

- Radical new distribution links

- A radical attack on the awareness link of the consumption chain

- A major attack on key metrics

Radical Resegmentation at the Purchase Link

Royal Insurance radically resegmented the market to capture a prime target market of private car drivers who are over thirty-five, have a proven good driving record, and drive cars for social or commuting purposes. Royal Insurance did not cover commercial vehicles or fleets.

With this target market in mind, Mendes and his team assembled products that have the following compelling attributes.

Personalized and modular products: The customer chooses the desired coverage, limits, and so on. Products are simple but offer wide coverage with no hidden clauses or compulsory deductibles. Unlike rival offers, which tend to be “standard products,” coverage is modular, and customers can tailor policies to their own needs.

To quote Mendes, “Customers are smart and rational in their choices but emotional in their affiliations, and if you involve them they will become your allies and your champions.”

Transparent products: Royal Insurance policies were the first in Italy to be written in plain Italian, doing away with complex, legal language.

Meritocracy: Prices vary so that good drivers pay less than those who are not so careful.

Radical Changes in the Service Link

Royal Insurance became the only insurance company in Italy and the first in Europe to offer its customers a customer charter (“Carta dei Diritti”), which contains a written promise of the service standards customers can expect. The standards, which relate to access to services, claims performance, and privacy, are extremely challenging. For example, the company promises inspection of accident damage within forty-eight hours, payment of refunds within three working days, and payments of claims within seven days.

This innovative written promise was introduced to underline the company’s commitment to customers in the form of guaranteed service standards but also served to focus internal attention on the key quality and efficiency indicators. Furthermore, it serves as a rallying point for staff, who take pride in the unrivaled quality of their work.

The seriousness of the “Carta dei Diritti” is demonstrated by a financial penalty that is paid to a customer as an apology when the promised standards of service are not delivered. Royal Insurance’s performance in maintaining service standards is audited annually by a group comprising Price Waterhouse Coopers and randomly selected customers, who have access to any information they ask for. This is an important formal and symbolically powerful moment of interaction with customer representatives. It also helps keep the service standards relevant to customers, maintains internal company performance at the most efficient level, and makes it difficult for competitors to imitate the Royal Insurance approach. In the spirit of transparency, the results of the audit are published in the major national newspapers, and a copy is mailed to each customer.

Revolutionized Pricing

Royal Insurance introduced a number of revolutionary pricing policies.

Personalized meritocratic prices: By asking a series of questions about a customer’s lifestyle and driving style, the company can statistically estimate his or her propensity to have an accident. There are several million possible price combinations, meaning that prices can be accurately correlated to each customer. Each driver pays more or less depending on his or her risk profile.

Pricing innovations: An innovative “no claims discount” enables good drivers to reach the lowest price after only five years instead of the fourteen years of claims-free driving offered by most other companies.

Segmentation and selectivity: At the heart of the business is a state-of-the-art executive information system, based on SAS technology, that lets the company easily and quickly monitor the performance of the portfolio. Royal Insurance can forecast accurately and intervene rapidly to take advantage of positive market developments as well as take any needed corrective action in a timely manner. The company can change prices in a matter of a few hours.

Radical New Distribution Links

Royal Insurance added radically new distribution links.

Call center: Royal Insurance was one of the first insurance companies in Italy to distribute its products by call center. The call center, which employs about three hundred fifty (FTE) people, has been the source of about 68 percent of the firm’s business to date. The call center is the only one in Italy to be open seven days per week with extended operating hours. Staff members work in shifts to service business needs.

Internet: Mendes realized that the Internet would be a powerful new distribution channel, and so Royal Insurance has had a Web presence since 1996. It has developed the Internet site over the years and has been actively selling on the Web using an automatic process since 1999. Currently 40 percent of new business comes from this source, and the proportion is growing, with obvious cost-saving advantages and greater satisfaction for customers. Royal Insurance is a recognized industry leader in e-business.

Partner system: In 1998, Royal Insurance developed an extranet (called Partner System) that is used to service business partners. Partnerships are not core to Royal’s business, but this B2B tool has enabled it to gain additional business from nontraditional partners that have been attracted to Royal by its reputation for quality. These partners include several banks, a supermarket chain, and car manufacturers.

A Radical Attack on the Awareness Link

Royal Insurance speaks directly to its customers through various advertising media (print, television, posters, the Internet, and so on). It overtly employs a message of trust in its customers and emphasizes the “intellectual equality” of the contracting parties; in other words, customers are mature and are capable of choosing according to their needs.

Frequent communications are also a feature of Royal Insurance’s customer relations system. In addition to an annual letter reminding customers of the need to renew their policies—an approach typical of relationships with most insurance companies—Royal Insurance uses many other opportunities, such as birthdays, to communicate with customers. So when renewal time comes around, Royal is fresh in the customer’s mind. The style of the communication is novel and sophisticated, and as exciting as it is possible to be with an insurance product.

As we mentioned earlier, in the spirit of transparency the results of the Price Waterhouse Cooper audit are published in the major national newspapers and a copy is mailed to each customer. In this way, Royal Insurance has been successful in establishing a brand image of both innovation and traditional seriousness, together with a reputation for customer focus.

A Major Attack on Key Metrics

Many people think that the source of advantage in direct insurance is a lower-cost administrative structure. As a result, the basic business model Mendes developed is not necessarily obvious.

The technical business proposition is as follows: By controlling the quality of driver insured—and therefore excluding from the portfolio drivers who are statistically more likely to have accidents— Royal Insurance can offer good drivers high-quality service at a lower price than they would pay elsewhere, while still receiving from these drivers a higher contribution to its profit. (In rough terms, the usual 20/80 rule applies: Some 20 percent of people cause 80 percent of accidents.) Royal Insurance applies the basic principle that each customer pays for the risk that he or she represents.

The company manages the quality of its portfolio principally by means of a performance management system developed in-house. This system provides management information, advanced statistical analysis, decision support, planning and forecasting, and customer relationship management (CRM) functionality. This state-of-the-art system gives Royal Insurance important competitive advantages in pricing, portfolio management, and market positioning.

This combination of good price and high-quality service creates a “virtuous spiral” effect, with fast growth and high retention levels repaying the initial investment in a relatively short time. The result is that it was possible to create an important, profitable, low-cost-base personal lines insurer in the space of a few years. The direct relationship and the intimate knowledge of the customer base enable cross-selling and up-selling from this platform and permit various kinds of future vertical or horizontal integration.

In combination, the strategies lead to a powerful key metrics business model that not only generates passionately loyal policy-holder revenue but also reduces key cost metrics in the following ways:

Correct risk selection Reduces technical costs Operating excellence Reduces operating costs Information access and management Reduces operating costs Culture of empowerment Reduces operating costs Image management Reduces acquisition costs Outstanding service Reduces retention costs

From the perspective of the customer and staff member, the system is simple and straightforward, even if data-processing and data-mining complexities lurk behind the scenes. It is this data technology that renders the business simple. Royal Insurance built scalable call center, claims-handling, and Internet environments to service the processes required by the relatively simple Royal Insurance formula.

Results

The results were, as expected, low growth in the initial years as the new concept established itself. This was followed by ever-increasing customer acceptance, retention in the range of 90 percent, declining costs, and an exceptionally high quality portfolio: nonvolatile loss ratios in the low 80 percent range in what is considered a difficult market, with an average compulsory-motor-loss ratio (a measure of costs) in excess of 110 percent.

The original plan was to build a portfolio of 100,000 policies by the end of 2001; the actual result was 250,000 by that point, and about 280,000 customers by the end of August 2002, of whom about one-quarter were recruited from the Internet. This placed Royal Insurance in a leading position in the direct market and prepared it well to continue its rapid growth. At launch the company employed forty-five persons, a number that has grown to five hundred at the company’s headquarters in Milan.

Royal Insurance is a two-time winner of the Databank BICSI award for customer satisfaction and is the recognized industry leader in this area. It was also awarded the first Databank prize for excellence in e-business in February 2002.

The success of Royal Insurance has had an important effect on how auto insurance is transacted in Italy. A number of local and foreign companies entered the direct market, such as Linear (Gruppo Unipol, based in Italy); Lloyd 1885; RAS (based in Germany and Italy); and Allstate (from the United States). In addition, the direct and traditional markets have reacted by making changes to pricing structures, moving to personalized tariffs (in which prices for insurance vary by individual), and modifying no-claims discount mechanisms.

Overall, the insurance market has become aware of the importance of retaining valuable customers and the need for satisfying customers. Some traditional companies (such as AXA, based in France) began using call centers and direct techniques to service their agency networks. Others, such as Italy’s Cattolica, have reorganized their claims-handling structures to mimic those of Royal Insurance.

Several companies have introduced customer charters or published service standards. The Italian legislature (which initially found it difficult to accept some of the Royal Insurance innovations) has passed laws that embody concepts, such as the “risk profile,” that Royal Insurance introduced into the market.

Thus we see that a truly successful marketbuster will inevitably provoke a competitive response, and the continued success of Royal Insurance will depend, as in many other cases in this book, on the capacity of Royal’s new parent company not to rest on its laurels but instead to either continuously and entrepreneurially innovate (as we suggest in our first book) or to begin looking for a follow-on marketbuster.

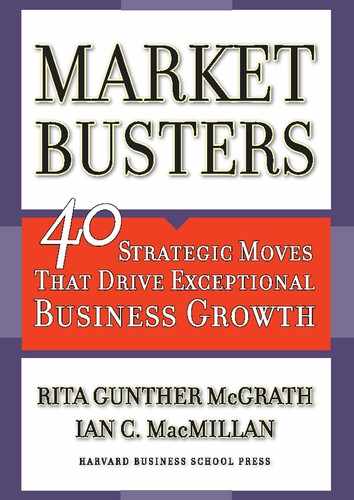

Table 8-1 outlines the threats faced by Mendes when he began the company.

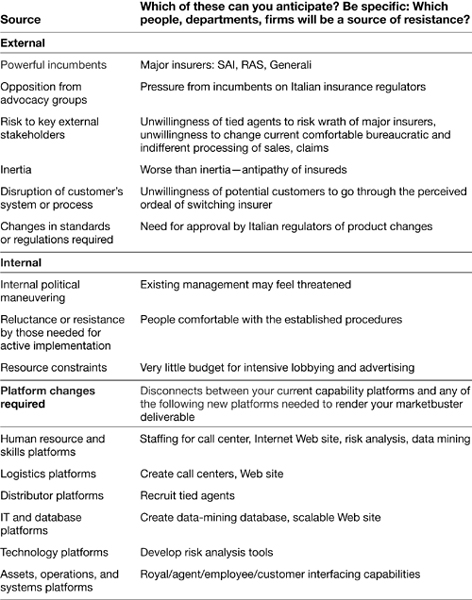

As you can see, Mendes was facing a formidable task. In a way, this is why no one else in the industry was mobilizing for change and why, after he overcame these forces, he could expect his marketbusting move to run for some time. Table 8-2 shows the forces Mendes was able to marshal.

In addition to the DRAT table, we look at Mendes’s kite challenges in table 8-3.

Because Mendes was creating an entirely new organization, he really didn’t have an existing kite to work with, and that gave him considerable latitude to create an organization that could uniquely deliver this strategy. Normally, we would encourage you to start from where you are, think about where you need to go, and specify the gaps so that they become extremely operational for you and your team. This approach should show you how, by focusing on the essentials and avoiding unnecessary details, you can provide the selected champions with an integrated kite that frames the challenges they need to overcome to develop a plan having all the requisite details. In the example in table 8-3, notice that each cell of the table has three to six core drivers that integrate action across the entire kite.

TABLE 8-1

DRAT Table, Royal Insurance

TABLE 8-2

How Royal Insurance Might Cope with DRAT Challenges

TABLE 8-3

Marketbusting Kite for Royal Insurance

We have found that it can take as little as three to four hours to develop the first-cut frame you need for your new kite.

Remember that your kite analysis is meant to focus you on developing a set of core, consistent themes that integrate and align coordinated marketbusting action in your operation. After you have developed these core themes, you can readily identify the obstacles to moving from the current kite to the marketbusting kite. Then you can appoint champions to begin making detailed plans to overcome the obstacles and jointly begin taking coordinated action to effect the marketbusting transition.

Epilogue

In January 2002, Direct Line bought Royal Insurance from Royal & Sun Alliance for slightly less than 20 million euros. As a result of the deal, Direct Line ended up with three hundred thousand subscribers in Italy.

Royal Insurance can rightly take credit for busting a major European insurance market, capitalizing on not just one but several of the marketbusting lenses we have presented in this book.

Taking Your Next Step

Well, there you have it: five lenses, forty moves, and a set of implementation issues to bear in mind as you strive to create exceptional growth in profits and profitability. Now what? Here are a few suggestions:

- Make marketbusting a part of your conversation and your management meetings, and devote at least some of your time to it every week. Set aside some time explicitly for getting away from today’s business to think about the future. A simple way to do this? Make a weekly “date” with yourself, and put it in your calendar, with the commitment to think about marketbusting (by which we mean dramatic growth, not the word itself). When you have regular meetings with colleagues, put a marketbusting topic somewhere near the beginning of the agenda. Even if you don’t spend much time on it at every meeting, the fact that it is there will keep the topic alive and show that you care about it.

- Test some of the tools we’ve described here to identify opportunities for marketbusting. Do you see big changes afoot in your regulatory environment, as Mendes did? Consider looking at industry dynamics as a key trigger. Do you think that customers’ experiences could be improved? Consumption chain analysis comes to mind. Do you believe that there is an opportunity to radically differentiate your products and services from the competition? Try attribute mapping. Do you think you can win by developing really different ways of operating from those of the competition? Key metrics is a natural. And if you can see your way to capitalize on the confluence of tectonic moves in the marketplace, it could represent a significant opportunity.

- As your business rhythm dictates, begin to plan how you might construct a marketbuster. Use discovery-driven planning to make the concepts crisp.1 Then work your way through your kite and DRAT tables—not to fall into analysis paralysis, but to make sure you’ve given the most essential elements some thought in a comprehensive way.

- As you move into execution mode, don’t be afraid to redirect the initiative as new information comes in. Try to keep your moves modest and low risk until you have reduced the most significant uncertainties you face. This strategy is a component of “real options” reasoning.2

- For easy reference, we’ve included in the appendix the provocative questions sprinkled throughout this book.

As we bring this book to a close, we thank you for sharing the results of a journey we have been on for the past three years. We appreciate your interest and attention. Even better, we’d love to hear from you. What worked? What didn’t? What did you learn? And what would others benefit from hearing about? What more would you like to learn about yourself? These are the issues that keep our research engaging, exciting, and, we hope, useful.

We wish you luck!