CHAPTER 5

![]()

ACCOUNTING FOR MERCHANDISING OPERATIONS

OVERVIEW

A service entity performs services for its customers to earn service revenue. A merchandising entity sells products to its customers to earn sales revenue. Both types of entities incur expenses in generating revenue. Thus, both must match expenses incurred with revenues earned. This chapter will acquaint you with the income statement for a merchandising entity. The major differences between the income statement for a service type firm and the income statement for a merchandising firm lie with the data reported for net sales revenue and cost of goods sold expense for the merchandiser. Both the single-step and the multiple-step formats for the income statement are discussed in this chapter.

A merchandiser must account for the purchase and sale of its inventory items. The perpetual system is discussed in this chapter and the periodic system is explained in an appendix to this chapter.

SUMMARY OF LEARNING OBJECTIVES

- Identify the differences between service and merchandising companies. Because of the presence of inventory, a merchandising company has sales revenue, cost of goods sold, and gross profit. To account for inventory, a merchandising company must choose between a perpetual inventory system and a periodic inventory system.

- Explain the recording of purchases under a perpetual inventory system. The company debits the Inventory account for all purchases of merchandise, freight-in and other costs, and credits it for purchase discounts and purchase returns and allowances.

- Explain the recording of sales revenues under a perpetual inventory system. When a merchandising company sells inventory, it debits Accounts Receivable (or Cash), and credits Sales Revenue for the selling price of the merchandise. At the same time, it debits Cost of Goods Sold and credits Inventory for the cost of the inventory items sold. Sales Returns and Allowances and Sales Discounts are debited.

- Explain the steps in the accounting cycle for a merchandising company. Each of the required steps in the accounting cycle for a service company applies to a merchandising company. A worksheet is again an optional step. Under a perpetual inventory system, the company must adjust the Inventory account to agree with the physical count.

- Distinguish between a multiple-step and a single-step income statement. A multiple-step income statement shows numerous steps in determining net income, including nonoperating activities sections. A single-step income statement classifies all data under two categories, revenues or expenses, and determines net income in one step.

- *Prepare a worksheet for a merchandising company. The steps in preparing a worksheet for a merchandising company are the same as for a service company. The unique accounts for a merchandiser are Inventory, Sales Revenue, Sales Returns and Allowances, Sales Discounts, and Cost of Goods Sold.

- **Explain the reporting of purchases and sales of inventory under a periodic inventory system. In recording purchases under a periodic system, companies must use entries for (a) cash and credit purchases, (b) purchase returns and allowances, (c) purchase discounts, and (d) freight costs. In recording sales, companies must make entries for (a) cash and credit sales, (b) sales returns and allowances, and (c) sales discounts.

*This material is covered in Appendix 5A in the text.

**This material is covered in Appendix 5B in the text.

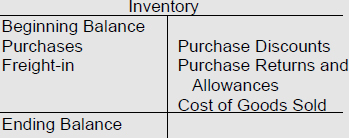

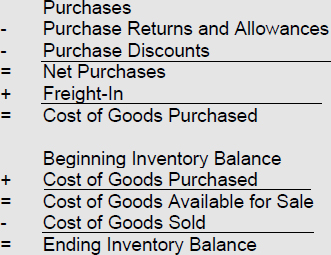

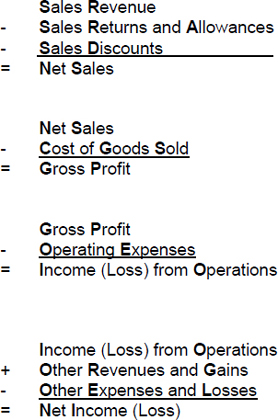

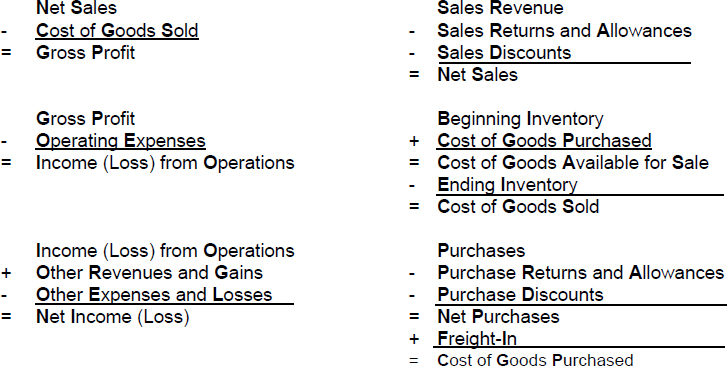

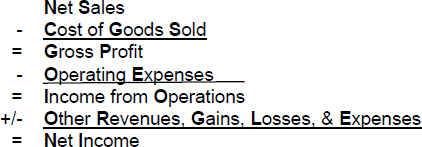

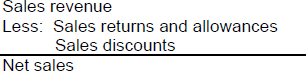

ILLUSTRATION 5-1

COMPUTATION MODELS FOR COMPONENTS OF

A MULTIPLE-STEP INCOME STATEMENT (L.O. 1, 5, 7)

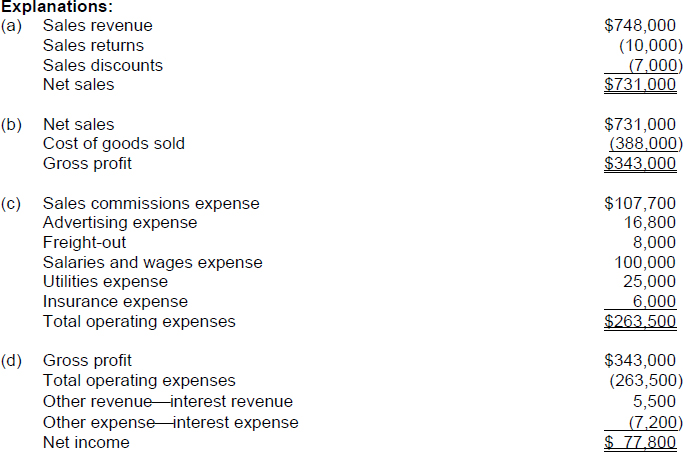

EXERCISE 5-1

Purpose: (L.O. 1) This exercise will help you to identify the relationships among the components involved in measuring net income for a merchandising company.

The following information applies to The Sports Shop for 2014:

| Sales revenue | $748,000 |

| Sales returns | 10,000 |

| Sales discounts | 7,000 |

| Cost of goods sold | 388,000 |

| Sales commissions expense | 107,700 |

| Advertising expense | 16,800 |

| Salaries and wages expense | 100,000 |

| Utilities expense | 25,000 |

| Insurance expense | 6,000 |

| Freight-out | 8,000 |

| Interest revenue | 5,500 |

| Interest expense | 7,200 |

Instructions

(a) Compute net sales for 2014.

(b) Compute gross profit for 2014.

(c) Compute total operating expenses for 2014.

(d) Compute net income for 2014.

SOLUTION TO EXERCISE 5-1

Approach for parts (a), (b) and (d): Write down the elements of the computations for net sales, gross profit, and net income. Refer to Illustration 5-1. Enter the data given and solve.

Approach for part (c): Examine the items not used to compute net sales and gross profit. Identify the items that are operating expenses and think about whether they are involved with the selling function (selling expenses such as salaries for the sales force, sales commissions, advertising, freight-out, and depreciation of sales counters, showroom, and store equipment) or not (administrative expenses such as officer salaries, rent, and insurance). Nonoperating items are other revenues, gains, other expenses, and losses.

| TIP: | Some companies subdivide the operating expenses into the subclassifications of selling expenses and administrative expenses. Administrative expenses are often called general and administrative expenses. (However, for homework purposes, do not do this subdivision unless specifically instructed to do so). Selling expenses include expenses associated with the making of sales, such as salaries for the sales force, sales commissions, advertising, freight delivery, and depreciation of sales counters, showroom, and store equipment. General and administrative expenses include expenses relating to general operating activities such as rent, officer salaries, personnel management, insurance, accounting, and store security. |

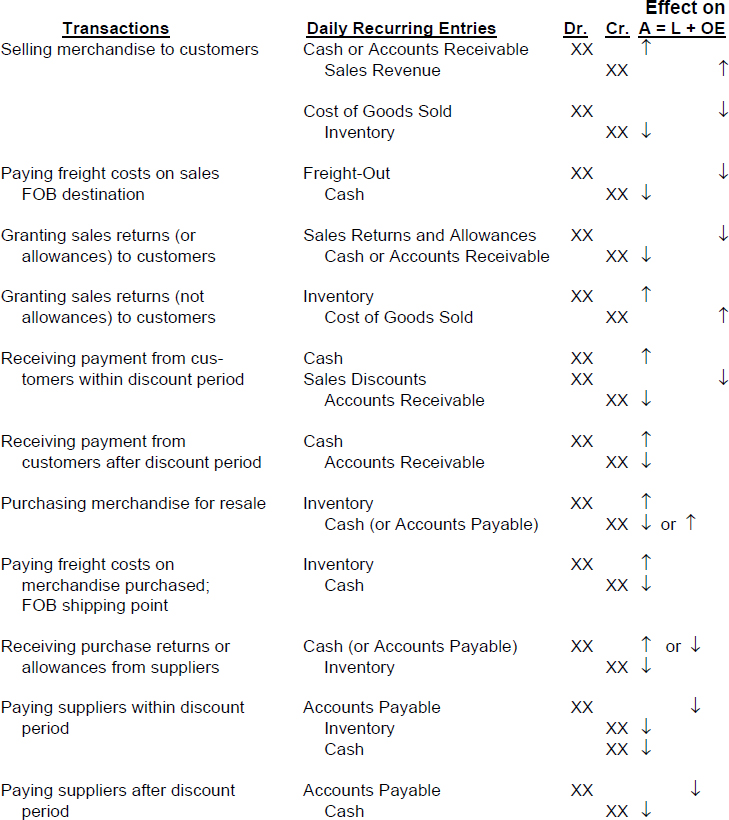

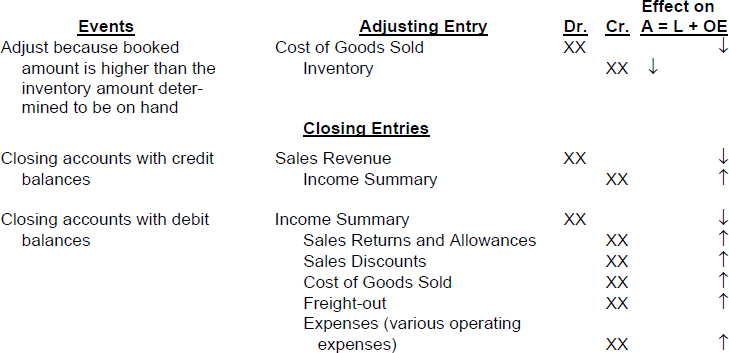

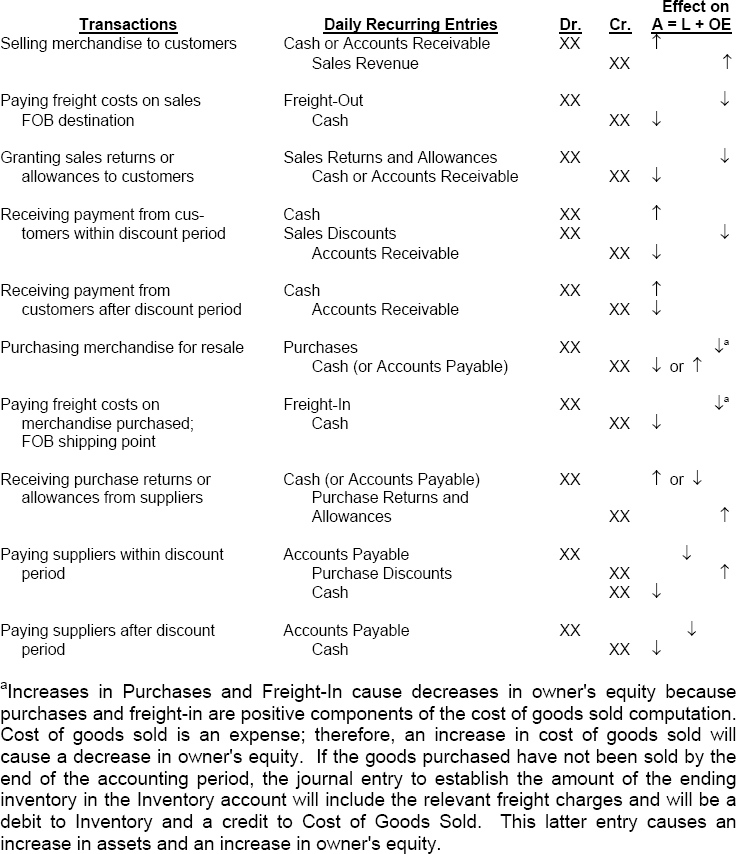

ILLUSTRATION 5-2

DAILY RECURRING AND ADJUSTING AND CLOSING ENTRIES FOR A MERCHANDISING ENTITY USING A PERPETUAL INVENTORY SYSTEM (L.O. 2, 3, 4)

The following are the typical entries for a merchandising entity employing a perpetual inventory system:

| TIP: | Notice that the first five transactions in this Illustration involve activities related to the sale of merchandise inventory; whereas, each of the second group of five transactions involves activities related to the purchase of merchandise inventory. |

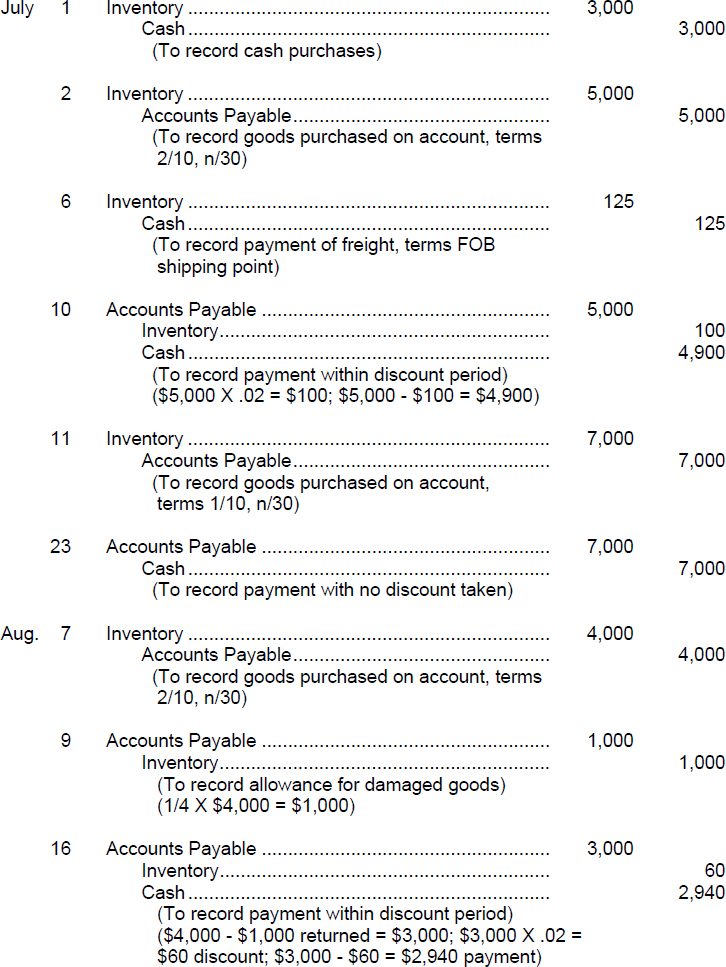

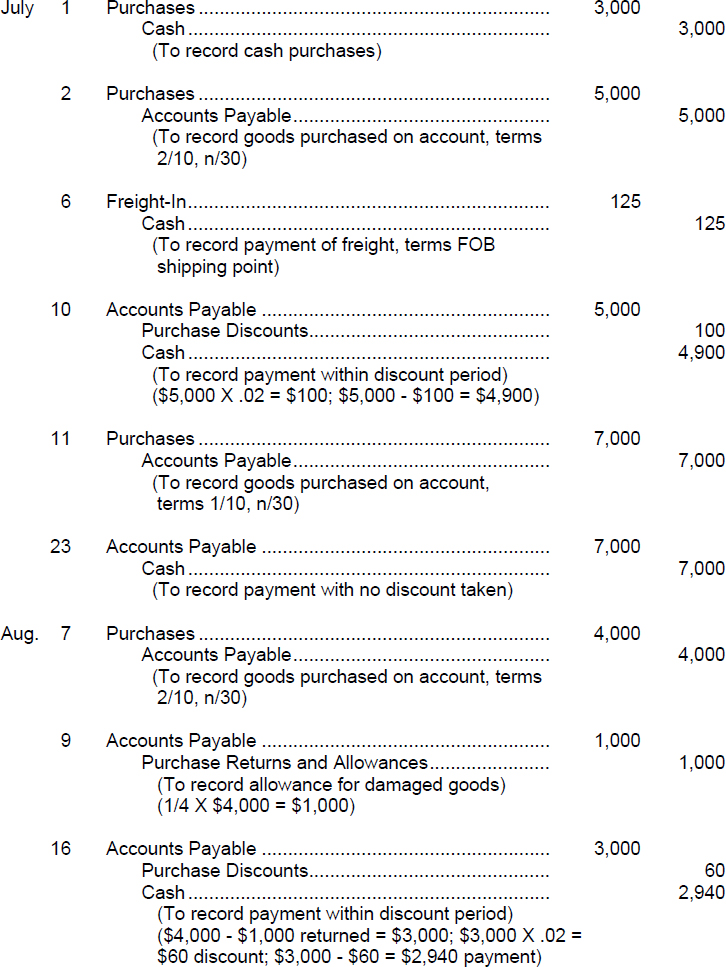

EXERCISE 5-2

Purpose: (L.O. 2) This exercise reviews the journal entries to record purchases of merchandise inventory under a perpetual inventory system.

A list of transactions for the Luke Bryan Memorabilia Sales Company appears below. A perpetual inventory system is used.

| July 1 | Purchased merchandise from Oliver Company for $3,000 cash. |

| 2 | Purchased merchandise from Yearwood Company, $5,000, FOB shipping point, terms 2/10, n/30. |

| 6 | Paid freight on July 2 purchase, $125. |

| 10 | Paid Yearwood Company the amount owed. |

| 11 | Purchased merchandise from McBride Company, $7,000, FOB destination, terms 1/10, n/30. |

| 23 | Paid McBride Company the amount owed. |

| Aug. 7 | Purchased merchandise from Dun Company, $4,000, FOB destination, terms 2/10, n/30. |

| 9 | Returned one-fourth of the merchandise acquired in the August 7 transaction to Dun Company because of detected defects. |

| 16 | Paid Dun Company the balance owed. |

Instructions

Prepare the journal entries to record these transactions on the books of the Luke Bryan Memorabilia Sales Company.

SOLUTION TO EXERCISE 5-2

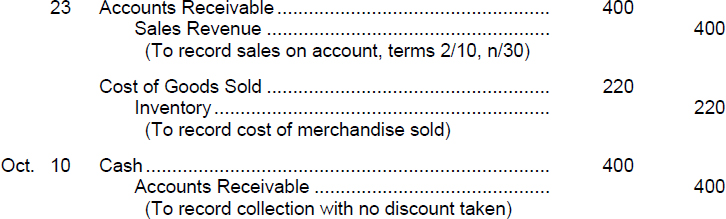

EXERCISE 5-3

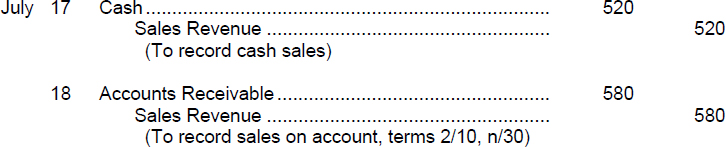

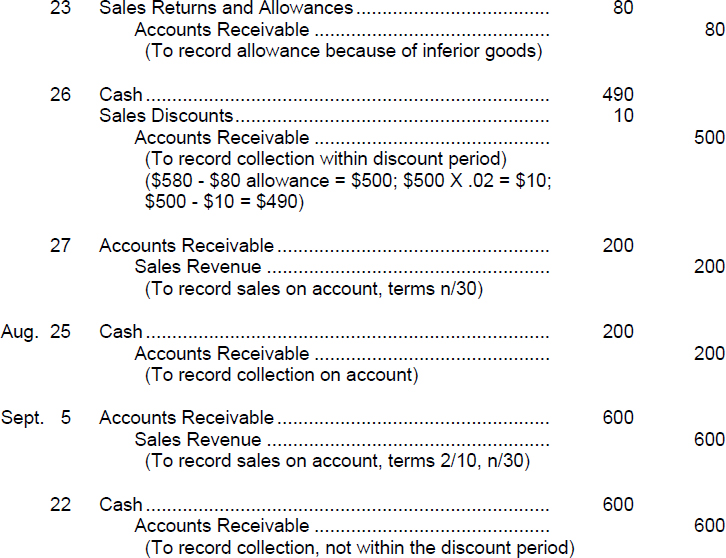

Purpose: (L.O. 3) This exercise reviews the journal entries to record sales of merchandise inventory under a perpetual inventory system.

A list of transactions for the Luke Bryan Memorabilia Sales Company appears below. A perpetual inventory system is used.

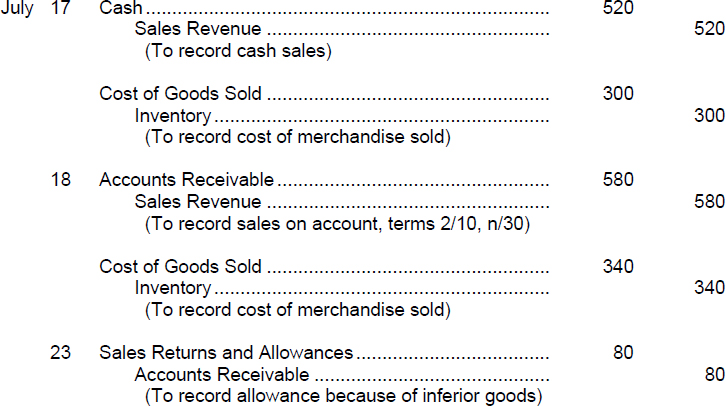

| July 17 | Sold merchandise with a cost of $300 to Eric Nelson for $520 cash. |

| 18 | Sold merchandise with a cost of $340 to Guy Sellars for $580, terms 2/10, n/30. |

| 23 | Issued a credit memo for $80 to Guy Sellars because of a sales allowance granted to him due to the inferior quality of goods sold to him on July 18. |

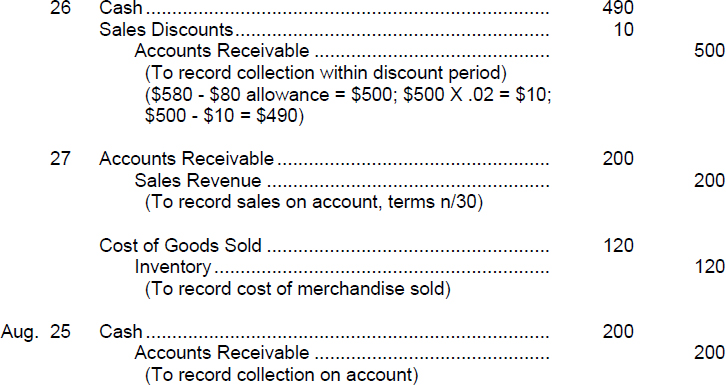

| 26 | Received payment from Guy Sellars for amount due for sale of July 18. |

| 27 | Sold merchandise to Jason Zahner, $200, terms n/30. The merchandise cost $120. |

| Aug. 25 | Received payment in full from Jason Zahner. |

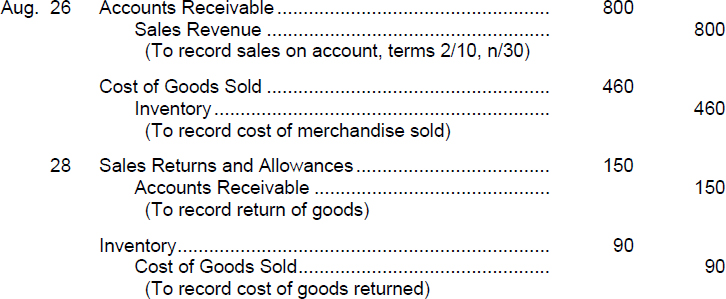

| 26 | Sold merchandise with a cost of $460 to Michele Blackburn for $800, terms 2/10, n/30. |

| 28 | Issued a credit memo for $150 to Michele Blackburn because she returned a portion of the goods sold to her on Aug. 26; the returned merchandise had a cost of $90. |

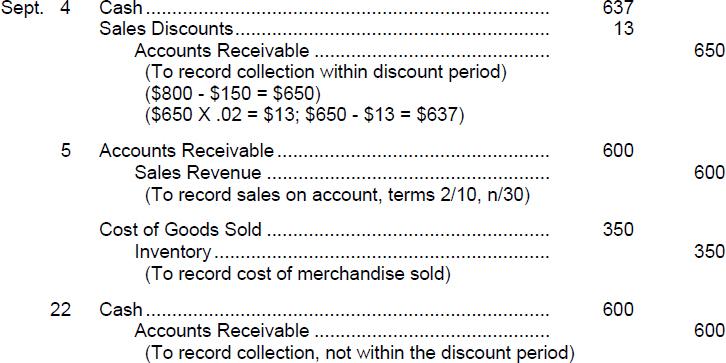

| Sept. 4 | Collected balance of account from Michele Blackburn. |

| 5 | Sold merchandise to Andrea Brotherly, $600, terms 2/10, n/30. The merchandise cost $350. |

| 22 | Received payment from Andrea Brotherly for amount due for sale of Sept. 5. |

| 23 | Sold merchandise costing $220 to Herman Ichner for $400, terms 2/10, n/30. |

| Oct. 10 | Received payment from Herman Ichner for sale of September 23. |

Instructions

Prepare the journal entries to record these transactions on the books of the Luke Bryan Memorabilia Sales Company.

SOLUTION TO EXERCISE 5-3

| TIP: | There is no entry affecting Inventory because there was no return of merchandise; there was a sales allowance granted. |

| TIP: | This entry assumes the goods returned were still in good condition. |

| TIP: | The amount was collected after the end of discount period so no discount is allowed. |

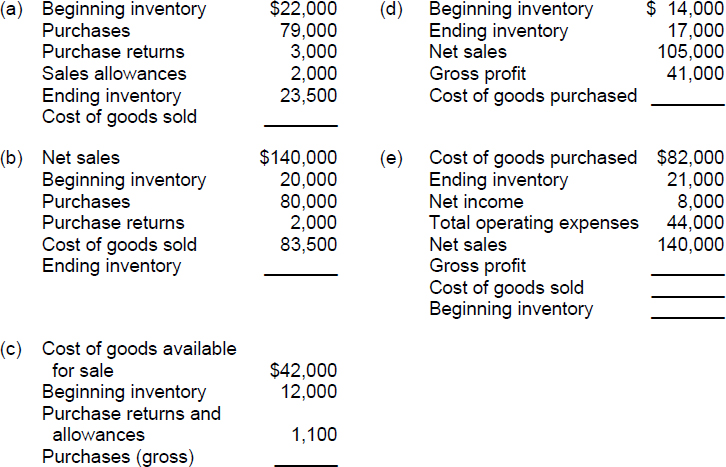

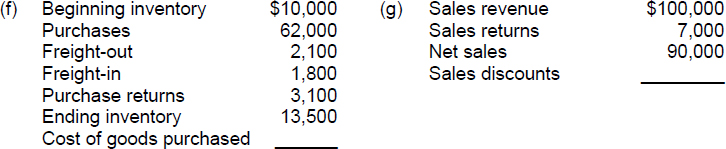

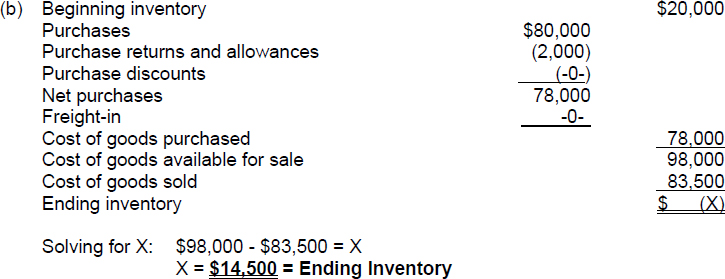

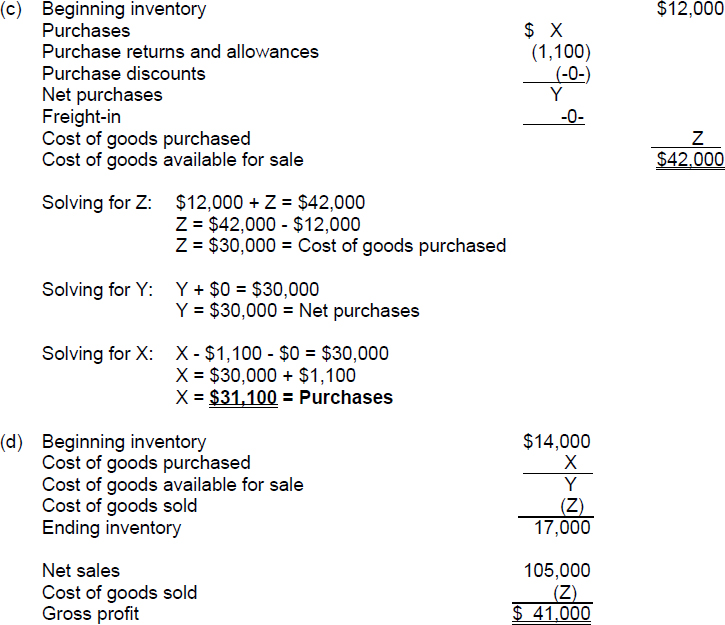

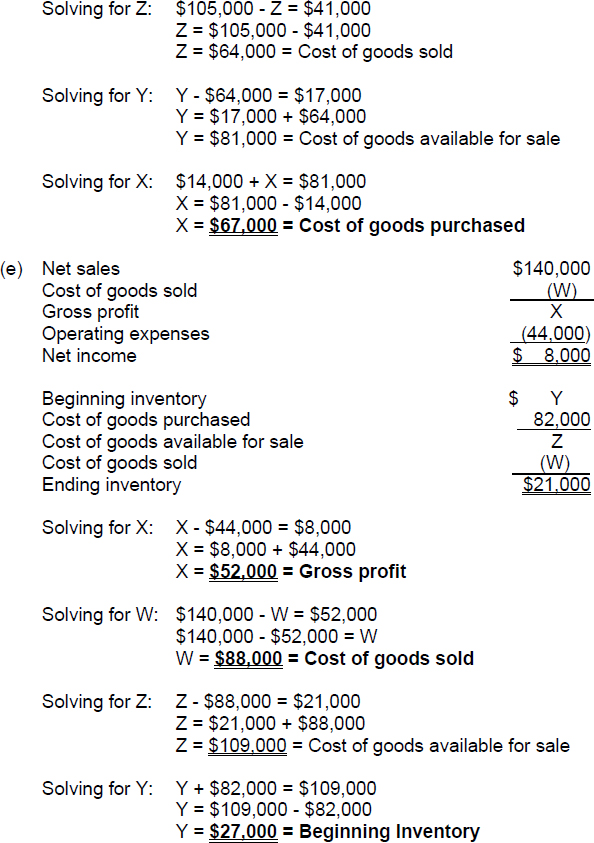

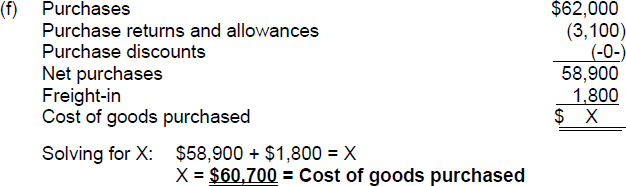

EXERCISE 5-4

Purpose: (L.O. 1, 2, 3, *7) This exercise reviews the elements of the net sales, cost of goods sold, gross profit, total operating expenses, and net income computations for a merchandising company.

Instructions

Compute the missing amounts for each of the independent situations below.

| TIP: | Be careful to distinguish between purchase allowances and sales allowances. Sales allowances are reductions in sales prices allowed to customers. Purchase allowances are reductions in the purchase prices of merchandise from suppliers. Sales allowances are a contra revenue item; purchase allowances reduce the balance of the Inventory account (when the perpetual system is used to record inventory purchases). Likewise, be careful to distinguish between (a) sales returns and purchase returns, and (b) sales discounts and purchase discounts. Returns and discounts processed for customers are related to sales; returns and discounts honored by suppliers of merchandise inventory are related to purchases. |

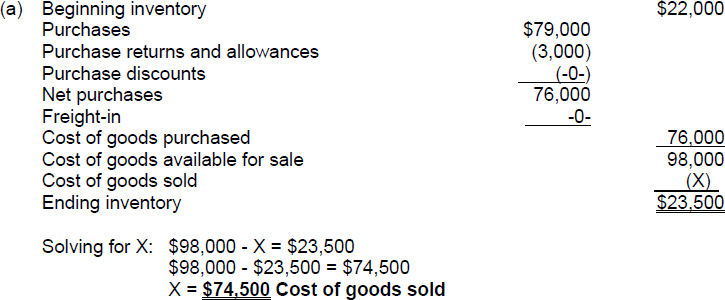

SOLUTION TO EXERCISE 5-4

Approach: Use the computation models in Illustration 5-1 and the data that flows through the Inventory account. Fill in the information given. Solve for the unknown.

| TIP: | Sales allowances have no impact on the balance of the Inventory account, the cost of merchandise purchased, or the cost of goods sold computation. |

| TIP: | Net sales is irrelevant information for the question at hand. |

| TIP: | The beginning and ending inventory amounts have no effect on the computation of the cost of goods purchased. Freight-out is a selling expense and, therefore, does not affect the computation of the cost of goods purchased. |

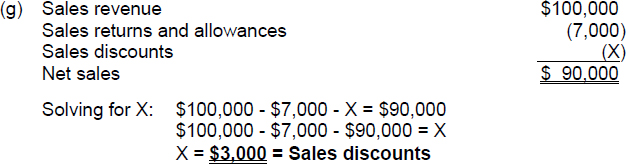

EXERCISE 5-5

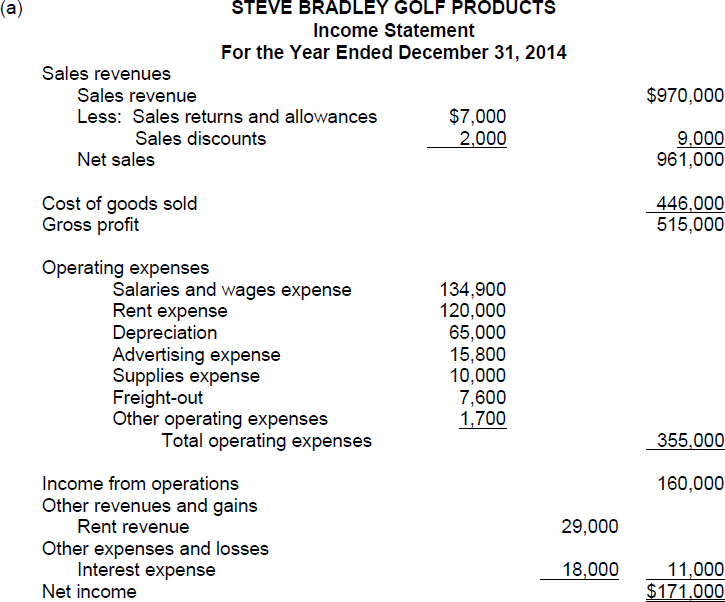

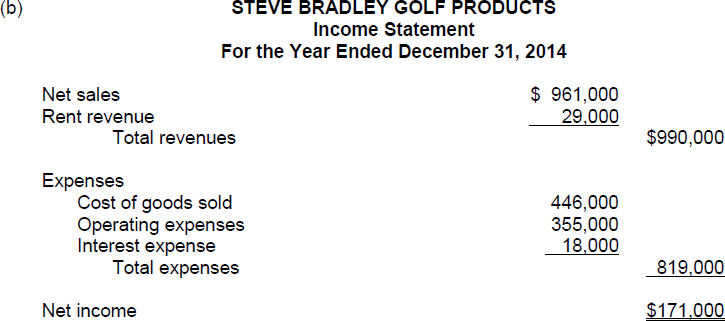

Purpose: (L.O. 5) This exercise will allow you to practice preparing an income statement and to contrast the multiple-step format and the single-step format for this statement.

The accountant for Steve Bradley Golf Products has compiled the following information from the company's records as a basis for an income statement for the year ended December 31, 2014.

| Rent revenue | $ 29,000 |

| Interest expense | 18,000 |

| Salaries and wages expense | 134,900 |

| Supplies expense | 10,000 |

| Other operating expenses | 1,700 |

| Sales revenue | 970,000 |

| Freight-out | 7,600 |

| Advertising expense | 15,800 |

| Depreciation expense | 65,000 |

| Sales returns and allowances | 7,000 |

| Rent expense | 120,000 |

| Cost of goods sold | 446,000 |

| Sales discounts | 2,000 |

| Owner's Drawings | 85,000 |

(a) Prepare a multiple-step income statement.

(b) Prepare a single-step income statement.

SOLUTION TO EXERCISE 5-5

| TIP: | A merchandising business has various types of expenses. Common expense categories are as follows: (1) cost of goods sold, (2) selling, (3) administrative, (4) interest, and (5) income taxes. Collectively, selling expenses and administrative expenses are usually called operating expenses; they may be separately displayed or combined for one line item as illustrated above. Refer to the multiple-step income statement [part (a) above]. Notice where each of these types of expenses appear on a multiple-step income statement. (Income tax expense will be illustrated in a later chapter.) |

| TIP: | Nonoperating activities consist of (1) revenues and expenses that result from secondary or auxiliary operations and (2) gains and losses that are unrelated to the company's operations. The results of nonoperating activities are shown in two sections on a multiple-step income statement: Other Revenues and Gains and Other Expenses and Losses. Items classified in the Other Revenues and Gains section of a multiple-step income statement include rent revenue, investment revenues (interest revenue and dividend revenue), unusual inflows (such as prizes received), and gains on the sale of assets not classified as inventory. Items classified in the Other Expenses and Losses section of a multiple-step income statement include financing expenses (interest expense), unusual outflows (such as casualty losses and litigation losses), and losses on the sale or abandonment of assets not classified as inventory (such as loss on the sale of property, plant and equipment). |

| TIP: | The term revenue is a gross concept and the term income is usually used as a net concept. Thus, net income results after expenses are offset against revenues. Sometimes the word income is used interchangeably with revenue in describing other types of revenues (such as interest income and rental income); it is best, however, if the term “revenue” instead of “income” is used in those contexts. |

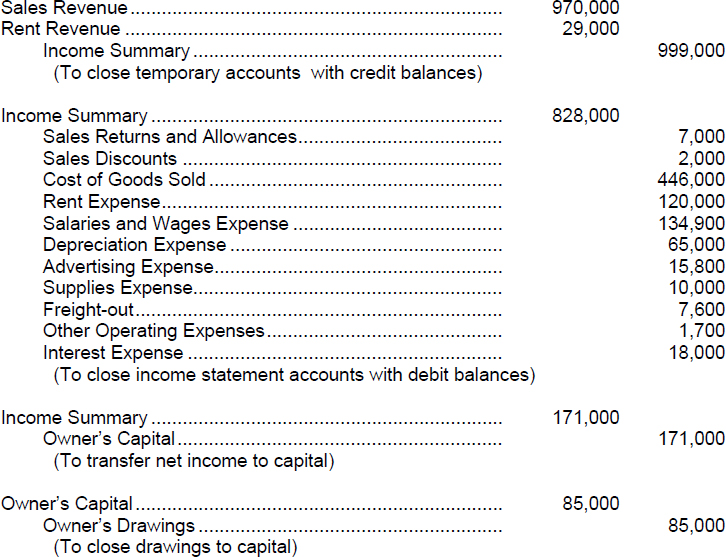

EXERCISE 5-6

Purpose: (L.O. 4) This exercise will review closing entries for a merchandising enterprise.

Closing entries are recorded at the end of an accounting period to prepare the temporary accounts for the subsequent accounting period. For example, assume the calendar year is the accounting period for a company. At the end of 2014, the Sales Revenue account balance is closed so that the Sales Revenue account begins the year of 2015 with a zero balance. Therefore, at the end of 2015, the balance in the Sales Revenue account will reflect only sales that took place in that single year (2015).

Closing entries also update the balance of the Owner's Capital account.

Instructions

Refer to the facts in Exercise 5-5 and its Solution. Prepare the closing entries for Steve Bradley Golf Products for the year ending December 31, 2014.

SOLUTION TO EXERCISE 5-6

| TIP: | The closing process for a merchandiser includes the following:

(1) entry to (a) debit Sales Revenue for its ending balance, debit any other revenue or gain accounts for their ending balances, and (b) credit Income Summary. This entry closes the temporary account(s) with credit balance(s). (2) entry to (a) credit contra sales items (Sales Returns and Allowances and Sales Discounts) for their ending balances, (b) credit operating expense accounts for their ending balances, and (c) credit interest expense and any other expense or loss accounts for their ending balances, and (d) debit Income Summary. (3) entry to close the balance of the Income Summary account to the Owner's Capital account. (4) entry to credit the Owner's Drawing account for its ending balance and debit the Owner's Capital account. This entry closes the Owner's Drawing account to the Owner's Capital account. |

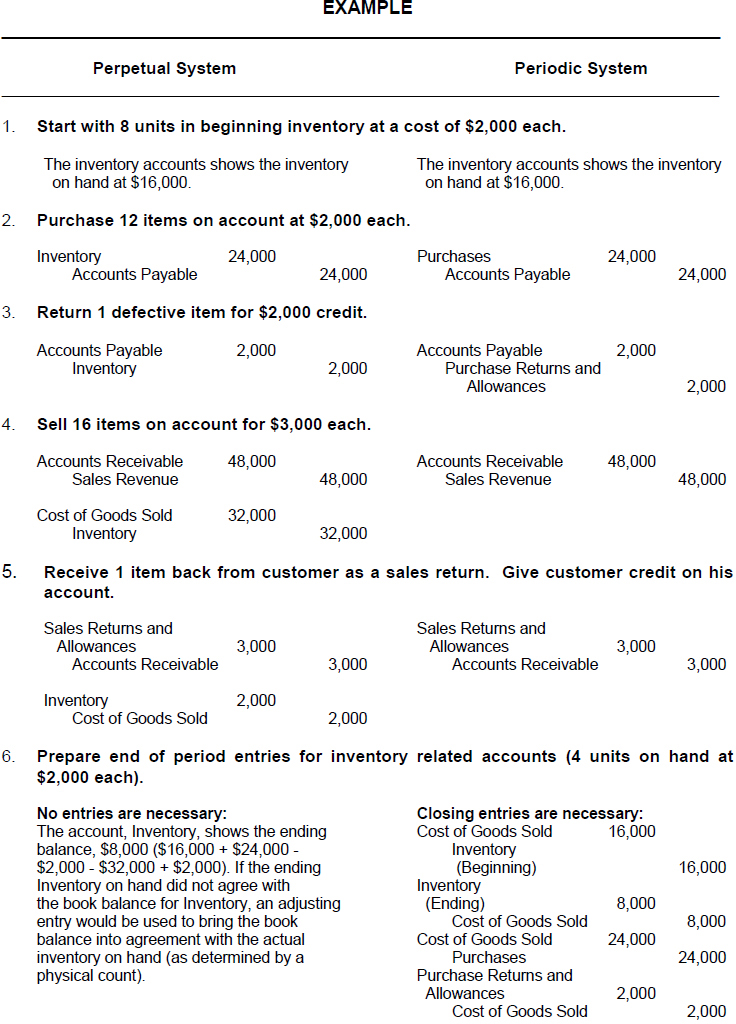

**ILLUSTRATION 5-3

COMPUTATION MODELS FOR COMPONENTS OF A MULTIPLE-STEP INCOME STATEMENT WHEN THE PERIODIC INVENTORY SYSTEM IS USED (L.O. **7)

ILLUSTRATION 5-4

PERPETUAL VS. PERIODIC INVENTORY SYSTEMS (L.O. 2, 3, **7)

| Features of A Perpetual System | Features of A Periodic System |

|

|

| TIP: | When the perpetual system is used, purchases of merchandise inventory are charged to the Inventory account (a real or permanent account). When the periodic system is used, four temporary (nominal) accounts are used to record the net cost of purchases (Purchases, Purchase Returns and Allowances, Purchase Discounts, and Freight-In); the balances in these temporary accounts must be closed (reduced to zero at the end of the accounting period) so that information about the cost of goods sold in the next accounting period can be properly accumulated. |

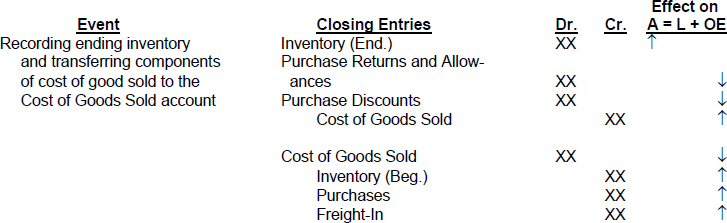

**ILLUSTRATION 5-5

DAILY RECURRING AND CLOSING ENTRIES FOR A MERCHANDISING ENTITY USING A PERIODIC INVENTORY SYSTEM (L.O. **7)

| TIP: | Compare Illustration 5-5 (entries for a periodic system) with Illustration 5-2 (entries for a perpetual system). Note the differences and think about the reasons for the differences. |

*EXERCISE 5-7

Purpose: (L.O. 7) This exercise reviews the journal entries to record purchases of merchandise inventory under a periodic inventory system.

A list of transactions for the Randy Travis Sales Company appears below. A periodic inventory system is used.

| July 1 | Purchased merchandise from Oliver Company for $3,000 cash. |

| 2 | Purchased merchandise from Yearwood Company, $5,000, FOB shipping point, terms 2/10, n/30. |

| 6 | Paid freight on July 2 purchase, $125. |

| 10 | Paid Yearwood Company the amount owed. |

| 11 | Purchased merchandise from McBride Company, $7,000, FOB destination, terms 1/10, n/30. |

| 23 | Paid McBride Company the amount owed. |

| Aug. 7 | Purchased merchandise from Dun Company, $4,000, FOB destination, terms 2/10, n/30. |

| 9 | Returned one-fourth of the merchandise acquired in the August 7 transaction to Dun Company because of detected defects. |

| 16 | Paid Dun Company the balance owed. |

Instructions

Prepare the journal entries to record these transactions on the books of the Randy Travis Sales Company.

SOLUTION TO EXERCISE 5-7

*EXERCISE 5-8

Purpose: (L.O. 7) This exercise reviews the journal entries to record sales of merchandise inventory under a periodic inventory system.

A list of transactions for the Randy Travis Sales Company appears below. A periodic inventory system is used.

| July 17 | Sold merchandise with a cost of $300 to Eric Nelson for cash, $520. |

| 18 | Sold merchandise with a cost of $340 to Guy Sellars for $580, terms 2/10, n/30. |

| 23 | Issued a credit memo for $80 to Guy Sellars because of a sales allowance granted to him due to the inferior quality of goods sold to him on July 18. |

| 26 | Received payment from Guy Sellars for amount due for sale of July 18. |

| 27 | Sold merchandise to Jason Zahner, $200, terms n/30. The merchandise cost $120. |

| Aug. 25 | Received payment in full from Jason Zahner. |

| Sept. 5 | Sold merchandise to Andrea Brotherly, $600, terms 2/10, n/30. The merchandise cost $350. |

| 22 | Received payment from Andrea Brotherly for amount due for sale of Sept. 5. |

Instructions

Prepare the journal entries to record these transactions on the books of the Randy Travis Sales Company.

SOLUTION TO EXERCISE 5-8

| TIP: | When the periodic inventory system is used, withdrawals from inventory are not recorded as cost of goods sold until the end of the accounting period. |

| TIP: | The amount was collected after the end of discount period so no discount is allowed. |

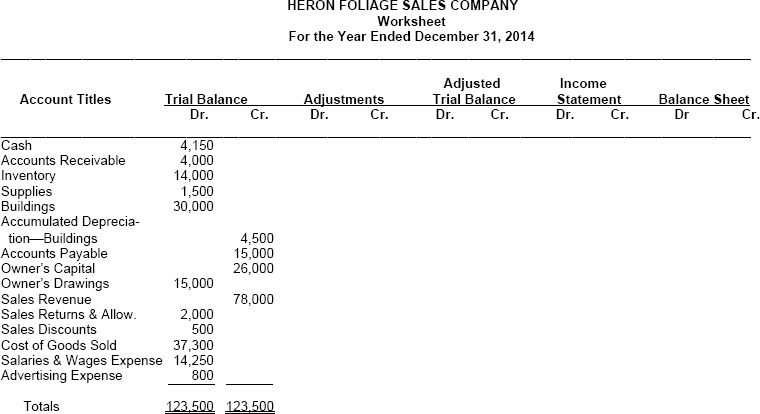

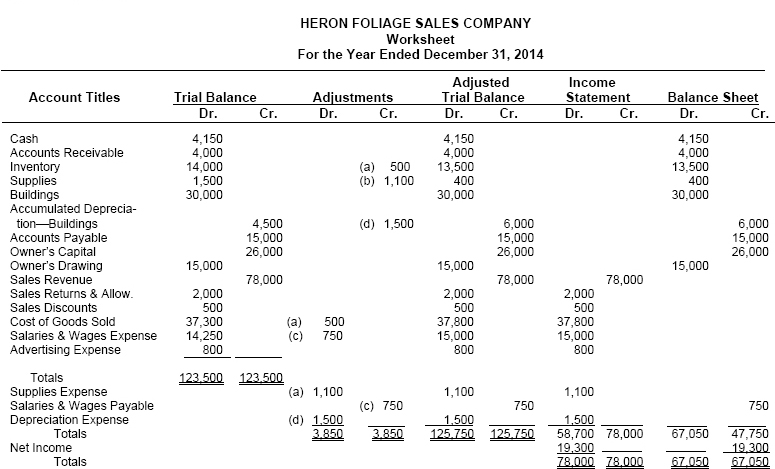

**EXERCISE 5-9

Purpose: (L.O. 6) This exercise will give you practice in completing a worksheet for a business engaged in merchandising activity.

The trial balance of the Heron Foliage Sales Company at December 31, 2014, has already been entered on the worksheet on the following page.

Adjustment data:

- The physical count of inventory reveals there is only $13,500 on hand.

- A count of supplies shows $400 to be on hand.

- Accrued salaries at year end amount to $750.

- Depreciation on the building amounts to $1,500 for the year.

Instructions

Complete the worksheet for the Heron Foliage Sales Company for the year ended December 31, 2014.

SOLUTION TO 5-9

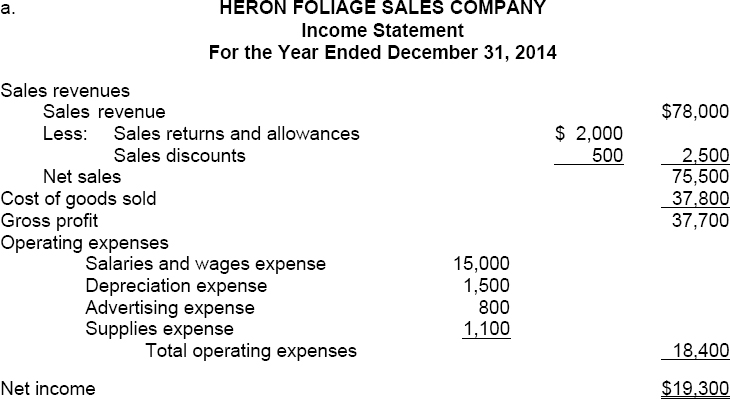

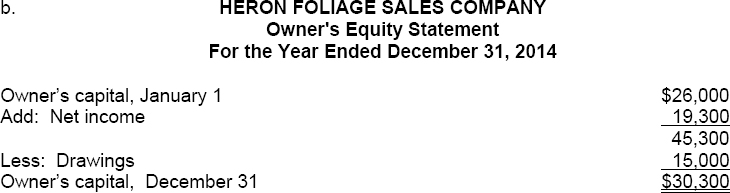

**EXERCISE 5-10

Purpose: (L.O. 5, 6) This exercise will give you practice in preparing a multiple-step income statement from a worksheet for a merchandising company.

A worksheet is a tool to organize accounting data to be reported in external financial statements.

Instructions

Refer to the worksheet in the Solution for Exercise 5-9 above.

- Prepare a multiple-step income statement for Heron Foliage Sales Company for the year ended December 31, 2014.

- Prepare an owner's equity statement for Heron Foliage Sales Company for the year ended December 31, 2014.

SOLUTION TO EXERCISE 5-10

EXERCISE 5-11

Purpose: (L.O. 1 thru 5) This exercise will quiz you about terminology used in this chapter.

A list of accounting terms with which you should be familiar appear below.

| Contra revenue account | Other revenues and gains |

| Cost of goods sold | Periodic inventory system |

| FOB destination | Perpetual inventory system |

| FOB shipping point | Purchase allowance |

| Gross profit | Purchase discount |

| Gross profit rate | Purchase invoice |

| Income from operations | Purchase return |

| Multiple-step income statement | Sales discount |

| Net sales | Sales invoice |

| Nonoperating activities | Sales returns and allowances |

| Operating expenses | Sales revenue (sales) |

| Other expenses and losses | Single-step income statement |

Instructions

For each item below, enter in the blank the term that is described.

- _____________________Freight terms indicating that the seller places the goods free on board to the buyer's place of business, and the seller pays the freight costs.

- _____________________Freight terms indicating that the seller places the goods free on board the carrier, and the buyer pays the freight costs.

- _____________________The primary source of revenue in a merchandising company.

- ___________________Sales revenue less sales returns and allowances and less sales discounts.

- ___________________The total cost of merchandise sold during the period. A synonymous term is cost of sales.

- ____________________The excess of net sales over the cost of goods sold. A synonymous term is gross margin.

- _____________________Expenses incurred in the process of earning sales revenues.

- _____________________A nonoperating section of the income statement that shows expenses from auxiliary operations and losses unrelated to the company's operations.

- _____________________A nonoperating activities section of the income statement that shows revenues from auxiliary operations and gains unrelated to the company's operations.

- _____________________Income from a company's principal operating activity, determined by subtracting cost of goods sold and operating expenses from net sales.

- _____________________An income statement that shows several steps in determining net income.

- _____________________An income statement that shows only one step in determining net income.

- _____________________An inventory system under which the company does not keep detailed inventory records throughout the accounting period, but determines the cost of goods sold only at the end of an accounting period.

- ___________________An inventory system under which the company keeps detailed records of the cost of each inventory purchase and sale and the records continuously show the quantity and cost of the inventory that should be on hand.

- _____________________A reduction given by a seller for prompt payment of a credit sale.

- _____________________A document that supports each credit sale.

- _____________________A document that supports each credit purchase.

- _____________________A cash discount claimed by a buyer for prompt payment of a balance due.

- _____________________An account that is offset against a revenue account on the income statement.

- _____________________Gross profit expressed as a percentage, by dividing the amount of gross profit by net sales.

- _____________________Various revenues, expenses, gains, and losses that are unrelated to a company's main line of operations.

- _____________________A return of goods by the buyer to the seller for a cash or credit refund.

- _____________________A deduction (from buyer's viewpoint) made to the selling price of merchandise, granted by the seller so that the buyer will keep the merchandise.

- _____________________Purchase returns and allowances from the seller's perspective. (See purchase returns and purchase allowances.)

SOLUTION TO EXERCISE 5-11

- FOB destination

- FOB shipping point

- Sales revenue

- Net sales

- Cost of goods sold

- Gross profit

- Operating expenses

- Other expenses and losses

- Other revenues and gains

- Income from operations

- Multiple-step income statement

- Single-step income statement

- Periodic inventory system

- Perpetual inventory system

- Sales discounts

- Sales invoices

- Purchase invoice

- Purchase discount

- Contra revenue account

- Gross profit rate

- Nonoperating activities

- Purchase return

- Purchase allowance

- Sales returns and allowances

ANALYSIS OF MULTIPLE-CHOICE TYPE QUESTIONS

- (L.O. 1) Which of the following formulas will yield the net income figure for a merchandising firm?

- Gross profit minus cost of goods sold.

- Net sales minus cost of goods sold.

- Gross profit minus operating expenses.

- Net sales minus operating expenses.

Approach and Explanation: Before you look at the alternative answers, write down the components in the net income computation. Abbreviations for these components will suffice.

Then take each answer selection and see if it describes your model. (Solution = c.)

- (L.O. 3) The balance in the Sales Discounts account is to be reported on the income statement as a(n):

- contra account to Sales Revenue.

- expense account.

- reduction of the cost of goods sold.

- addition to Sales Revenue.

Approach and Explanation: Write down a sketch of the portion of the income statement that includes sales discounts.

Then examine each answer solution to see if it describes what you know about sales discounts. The items which are deducted from sales are called contra revenue items; they are contra type valuation accounts. They are not to be called expenses even though they have debit balances and reduce net income in the same fashion as expense accounts. (Solution = a.)

- (L.O. 3) The purchaser is responsible for the transportation charges on goods that are sold and shipped on terms of:

- FOB destination.

- FOB shipping point.

- FOB common carrier.

- FOB buyer.

Approach and Explanation: Before you look at the alternative answers, write down the two shipping terms and describe who bears the freight cost:

The question asks for the terms where the purchaser bears the cost, which is FOB shipping point. Look for that answer. (Solution = b.)

TIP: FOB buyer is another name for FOB destination. FOB common carrier is a nonsense type answer selection. - (L.O. 2) The following amounts relate to the current year for the Ira Company:

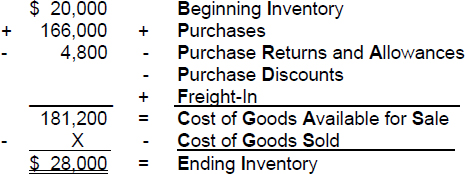

Beginning inventory $ 20,000 Ending inventory 28,000 Purchases 166,000 Purchase returns 4,800 Freight-out 6,000 The amount of cost of goods sold for the period is:

- $169,200.

- $162,800.

- $153,200.

- $147,200.

Approach and Explanation: Write down the components of the cost of goods sold. Enter the amounts given and solve for the unknown.

Solving for Cost of Goods Sold: $181,200 − $28,000 = X; X = $153,200 (Solution = c.)

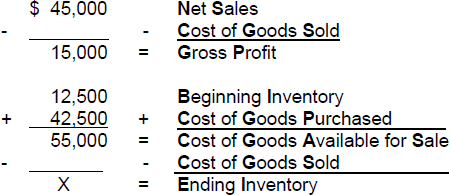

TIP: Freight-out is classified as a selling expense, not a component of cost of goods sold. - (L.O. 1, 2) The following amounts relate to the Crown Sales Company:

Beginning inventory $12,500 Purchases 42,500 Net sales 45,000 Gross profit 15,000 The amount of ending inventory is:

- $40,000.

- $25,000.

- $30,000.

- $15,000.

Approach and Explanation: Write down the models for the net sales and cost of goods sold computations. Fill in the amounts given.

Solving for Cost of Goods Sold: $45,000 − $15,000 = $30,000 Cost of Goods Sold. $55,000 − $30,000 Cost of Goods Sold = X. Solving for X: $55,000 − $30,000 = $25,000 Ending Inventory. (Solution = b.)

- (L.O. 2) Abraham Company sold a product to Walsh Company. Abraham finds reason to prepare a credit memorandum related to the sale to Walsh. Abraham will record the credit memorandum by a credit to:

- Accounts Receivable.

- Sales Returns and Allowances.

- Purchase Returns and Allowances.

- Accounts Payable.

Explanation: A credit memorandum is prepared by a seller to grant a customer a sales return or allowance. This document informs a customer that a credit has been made to the customer's account receivable for a return or allowance. The document is recorded on the seller's (Abraham) books by a debit to Sales Returns and Allowances and a credit to Accounts Receivable. This credit reduces the balance of the Accounts Receivable account. There is an accompanying entry to record the return of the goods to the Inventory account and a reduction of the Cost of Goods Sold account on the seller's books. The credit memorandum is recorded on the buyer's (Walsh) books by a debit to Accounts Payable and a credit to Inventory. (Solution = a.)

- (L.O. 3) The following information pertains to the Boot Sales Company:

Sales revenue $100,000 Sales returns and allowances 4,500 Sales discounts 500 Purchase returns 2,000 Transportation-out 3,200 The amount of net sales for the period is:

- $100,000.

- $95,000.

- $93,000.

- $89,800.

Approach and Explanation: Write down the computation model for net sales. Enter the data given and solve for the unknown.

TIP: Purchase returns are a contra-purchases (therefore contra cost of goods sold) item, not a contra-sales item. Transportation-out (or freight-out) is a selling expense, not a contra-sales item, for classification purposes. - (L.O. 5) Which of the following is not included in the operating expenses section of a multiple-step income statement?

- Advertising expense.

- Cost of goods sold.

- Freight-out.

- Supplies expense.

Approach and Explanation: Operating expenses include those costs incurred in the generation of sales revenue and are deducted from gross profit to determine income from operations. Cost of goods sold is the total cost of the merchandise sold during the period and is deducted from net sales to determine gross profit. Therefore, cost of goods sold is not a part of operating expenses. (Solution = b.)

- (L.O. 5) Which of the following will not appear on a single-step income statement?

- Net sales.

- Cost of goods sold.

- Gain on disposal of plant assets.

- Gross profit.

Approach and Explanation: Write down an outline of the major parts of the single-step income statement: Revenues minus Expenses = Net income (loss). The revenues section includes all forms of revenues and gains. The expense section includes all forms of expenses and losses. Notice there is no subtotal for Gross profit. Therefore, Gross pofit does not appear on the single-step income statement. (Solution = d).

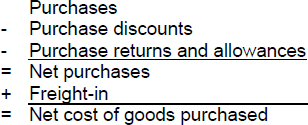

- (L.O. 1, 2, 3) The net cost of goods purchased is affected by:

- Sales returns.

- Purchase discounts.

- Freight-out.

- Sales allowances.

Explanation: The net cost of goods purchased is computed as follows:

Sales returns and sales allowances reduce net sales revenue. Freight-out is classified as an operating expense. (Solution = b.)

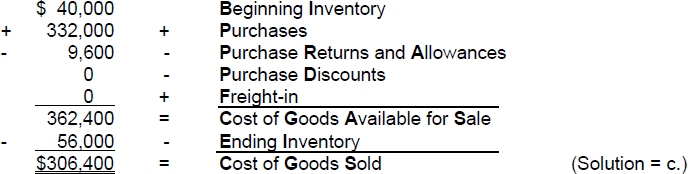

- (L.O. 1, 2) The following amounts relate to the current year for the Rod Buckley Company:

Beginning inventory $ 40,000 Ending inventory 56,000 Purchases 332,000 Purchase returns 9,600 Freight-out 12,000 The amount of cost of goods sold for the period is:

- $338,400.

- $325,600.

- $306,400.

- $294,400.

Approach and Explanation: Write down the computation model for cost of goods sold. Enter the amounts given and solve for the unknown.

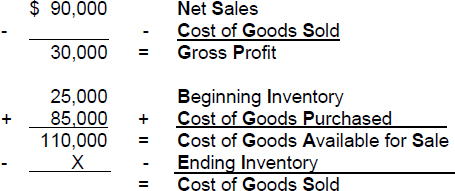

TIP: Freight-out is classified as a selling expense, not a component of cost of goods sold. - (L.O. 1, 3) The following amounts relate to the Rachael Avery's Sales Company:

Beginning inventory $25,000 Purchases 85,000 Net sales 90,000 Gross profit 30,000 The amount of ending inventory is:

- $80,000.

- $50,000.

- $60,000.

- $30,000.

Approach and Explanation: Write down the models for the net sales and cost of goods sold computations. Fill in the amounts given.

Solving for Cost of Goods Sold: $90,000 − $30,000 = $60,000 Cost of Goods Sold. $110,000 − X = $60,000 Cost of Goods Sold. Solving for X: $110,000 − $60,000 = X = $50,000 Ending Inventory. (Solution = b.)

- *(L.O. 7) The accountant for the Orion Sales Company is preparing the income statement for 2015 and the balance sheet at December 31, 2015. Orion uses the periodic inventory system. The January 1, 2015 merchandise inventory balance will appear:

- only as an asset on the balance sheet.

- only in the cost of goods sold section of the income statement.

- as a deduction in the cost of goods sold section of the income statement and as a current asset on the balance sheet.

- as an addition in the cost of goods sold section of the income statement and as a current asset on the balance sheet.

Explanation: The January 1, 2015 inventory amount is the beginning inventory figure. Beginning inventory is a component of the cost of goods available for sale for the period which is a component of cost of goods sold. (Solution = b.)

| TIP: | If the question asked about the December 31, 2015 merchandise inventory balance (ending inventory) rather than the beginning inventory balance, the correct answer would have been “c” (as a deduction in computing cost of sales and as a current asset). |