CHAPTER 12

![]()

ACCOUNTING FOR PARTNERSHIPS

OVERVIEW

There are three forms of business organization: proprietorship, partnership, and corporation. Accounting for the revenues, expenses, assets, and liabilities is the same for all three forms of business organization; however, these three forms differ in accounting for owners' equity. Thus far in this book, we have been referring to a sole proprietorship when our discussions involved owner's equity. Accounting for owners' equity of a corporation will be discussed in Chapters 13 and 14. In this chapter, we will examine accounting for owners' equity in a partnership. The procedures are the same ones that are used in accounting for a proprietorship—with the exception that separate capital and drawing accounts must be maintained for each partner.

SUMMARY OF LEARNING OBJECTIVES

- Identify the characteristics of the partnership form of business organization. The principal characteristics of a partnership are: (a) association of individuals, (b) mutual agency, (c) limited life, (d) unlimited liability, and (e) co-ownership of property.

- Explain the accounting entries for the formation of a partnership. When formed, a partnership records each partner's initial investment at the fair market value of the invested assets at the date of their transfer to the partnership.

- Identify the bases for dividing net income or net loss. Partnerships divide net income or net loss on the basis of the income ratio, which may be (a) a fixed ratio, (b) a ratio based on beginning or average capital balances, (c) salaries to partners and the remainder on a fixed ratio, (d) interest on partners' capital and the remainder on a fixed ratio, and (e) salaries to partners, interest on partners' capital, and the remainder on a fixed ratio.

- Describe the form and content of partnership financial statements. The financial statements of a partnership are similar to those of a proprietorship. The principal differences are as follows: (a) The partnership shows the division of net income on the income statement. (b) The owners' equity statement is called a partners' capital statement. (c) The partnership reports each partner's capital on the balance sheet.

- Explain the effects of the entries to record the liquidation of a partnership. When a partnership is liquidated, it is necessary to record the (a) sale of noncash assets, (b) allocation of the gain or loss on realization, (c) payment of partnership liabilities, and (d) distribution of cash to the partners on the basis of their capital balances.

- *Explain the effects of the entries when a new partner is admitted. The entry to record the admittance of a new partner by purchase of a partner's interest affects only partners' capital accounts. The entries to record the admittance by investment of assets in the partnership (a) increases both net assets and total capital and (b) may result in recognition of a bonus to either the old partners or the new partner.

- *Describe the effects of the entries when a partner withdraws from the firm. The entry to record a withdrawal from the firm when the partners pay from their personal assets affects only partners' capital accounts. The entry to record a withdrawal when payment is made from partnership assets (a) decreases net assets and total capital and (b) may result in recognizing a bonus either to the retiring partner or the remaining partners.

*This material is discussed in Appendix 12A in the text.

TIPS ON CHAPTER TOPICS

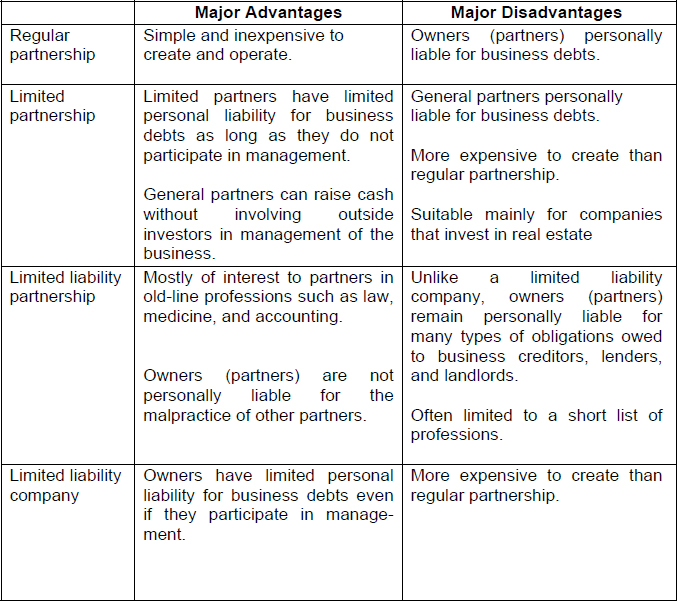

ILLUSTRATION 12-1

DIFFERENT FORMS OF ORGANIZATIONS WITH PARTNERSHIP

CHARACTERISTICS (L.O. 1)

Source: www.nolo.com--ownership structures (accessed June 2010).

EXERCISE 12-1

Purpose: (L.O. 1) This exercise will review the advantages and disadvantages of the partnership form of business organization.

Groucho, Harpo, and Marko are making plans to enter into a new business together. They come to you for advice as to whether they should form a corporation or operate as a partnership.

Instructions

(a) List and briefly describe the advantages of the partnership form over the corporate form of business organization.

(b) List and briefly describe the disadvantages of the partnership form over the corporate form of business organization.

SOLUTION TO EXERCISE 12-1

(a) The advantages of the partnership form as compared to a corporation include:

- A partnership is more easily formed. A partnership is created by a contract expressing the voluntary agreement of two or more individuals. (The agreement should be written and is referred to as the partnership agreement or articles of co-partnership.) There is much more effort and “red tape” involved in forming a corporation.

- A partnership has more freedom from governmental regulations and restrictions. For example, a partnership is not a taxable entity; it files only an information tax return, and the partners pick up their share of business income on their personal income tax returns. A corporation is a taxable entity. Income of a corporation is taxed once at the corporate level and again as owners receive dividends which must be reported as income on their personal income tax returns.

- There is more ease of decision making with a partnership. Decisions can be made quickly by a partnership on substantive matters affecting the firm, whereas in a corporation, formal meetings with the board of directors are often needed.

(b) The disadvantages of the partnership form as compared to a corporation include:

- Mutual agency exists in a partnership. Mutual agency means that each partner acts on behalf of the partnership when engaging in partnership business. The act of any partner is binding on all other partners, even when partners act beyond the scope of their authority, so long as the act appears to be appropriate for the partnership. In a corporation, an owner's (stockholder's) acts are not binding on the organization if the owner's acts are beyond the scope of the individual's authority.

- A partnership has a limited life. A partnership may be ended voluntarily at any time through the acceptance of a new partner into the firm or the withdrawal of an old partner. A partnership may be ended involuntarily by the death or incapacity of a partner. The life of a corporation is unlimited.

- Each partner has unlimited liability. Each partner is personally and individually liable for all partnership liabilities. Creditors' claims attach first to partnership assets and then to the personal resources of any partner, irrespective of that partner's equity in the partnership. Some states allow limited partnerships in which the liability of a limited partner is limited to that partner's equity in the partnership. However, there must always be at least one partner with unlimited liability, often referred to as the general partner.

| TIP: | It is often harder for a partnership to raise money than it is for a corporation. Also, depending on the articles of co-partnership, it may be more difficult to transfer ownership of the business when the partnership form is used rather than the corporate form. |

EXERCISE 12-2

Purpose: (L.O. 2) This exercise will illustrate the accounting involved when three individuals pool their assets to form a partnership.

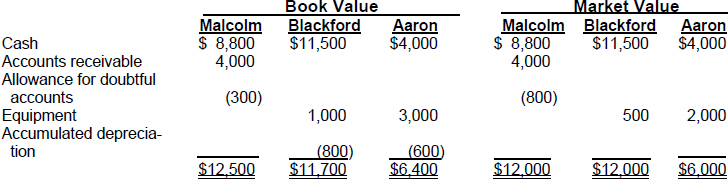

Malcolm, Blackford, and Aaron combine their proprietorships to start a new partnership named Pet Specialists. The partners invest the following assets in the business:

Instructions

Prepare the journal entries to record the investments of Malcolm, Blackford, and Aaron.

SOLUTION TO EXERCISE 12-2

| TIP: | Notice the accounting treatment of the equipment invested by Blackford. Neither the original cost ($1,000) nor its book value ($200) on Blackford's books is recorded by the partnership. The equipment is recorded on the partnership's books at its fair market value ($500) at the acquisition date, which is consistent with the cost principle.

Since the equipment has not been used by the partnership, there can be no accumulated depreciation when the asset is initially acquired by the partnership entity. In contrast, the gross claims on customers represented by Malcolm's accounts receivable ($4,000) are carried to the partnership, and the Allowance for Doubtful Accounts is established at $800 to arrive at a cash (net) realizable value of $3,200. |

| TIP: | Appropriate liability accounts are credited for any debts assumed by the partnership. |

| TIP: | Care must be taken to ensure that appropriate valuation of assets is made when the partners invest them. Otherwise, when disposition is later made of the assets, improper allocation of gains and losses may result. (This is because the gains and losses would then be allocated among the partners according to their income ratio rather than being reflected in the capital account of the partner who contributed the asset.) |

EXERCISE 12-3

Purpose: (L.O. 4) This exercise will test your knowledge of the reasons for changes in the balance of a partner's capital account.

A partner's capital account balance can change for several reasons.

Instructions

In the T-account below, insert each code letter on the appropriate side of the account to indicate how each of the following items would be reflected in a partner's capital account.

(a) Balance at beginning of the period.

(b) Additional investment of assets in partnership by the partner.

(c) Partner's share of net income for the period.

(d) Partner's drawings for the period.

(e) A disinvestment by the partner.

(f) Balance at end of the period.

SOLUTION TO EXERCISE 12-3

| TIP: | As in a proprietorship, changes in capital may result from four causes: additional capital investment, results of operations (net income or net loss), drawings, and capital disinvestment. |

EXERCISE 12-4

Purpose: (L.O. 4) This exercise illustrates the entries involved with closing the Income Summary and Drawings accounts in a partnership business.

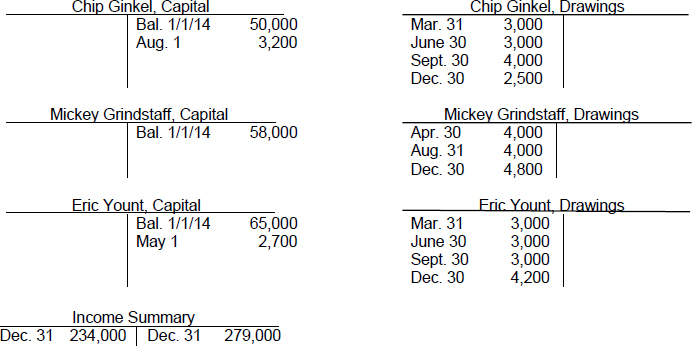

The following selected accounts appear in the ledger of the Wizzard Services Company. The business is owned by three partners named Ginkel, Grindstaff, and Yount. The amounts shown appear at December 31, 2014, after all revenue and expense accounts have been closed, but before any other closing entries have been prepared. The partners share all profits and losses equally.

Instructions

(a) Record the remaining necessary closing entries in general journal form.

(b) Post the entries to the ledger accounts.

(c) Calculate the balances of the capital accounts that will appear in the owners' equity section of the balance sheet at December 31, 2014.

(d) Prepare the partners' capital statement for the year ended December 31, 2014.

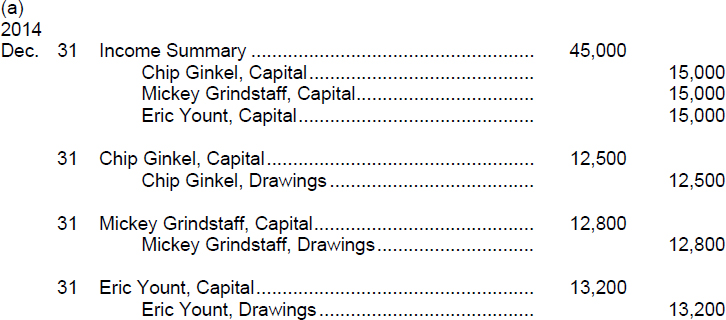

SOLUTION TO EXERCISE 12-4

| TIP: | The function of a partners' capital statement is to explain the changes in each partner's capital account and in total partnership capital during the year. As in a proprietorship, changes in capital may result from four causes: additional capital investment, net income or net loss, drawings, and capital disinvestment. |

EXERCISE 12-5

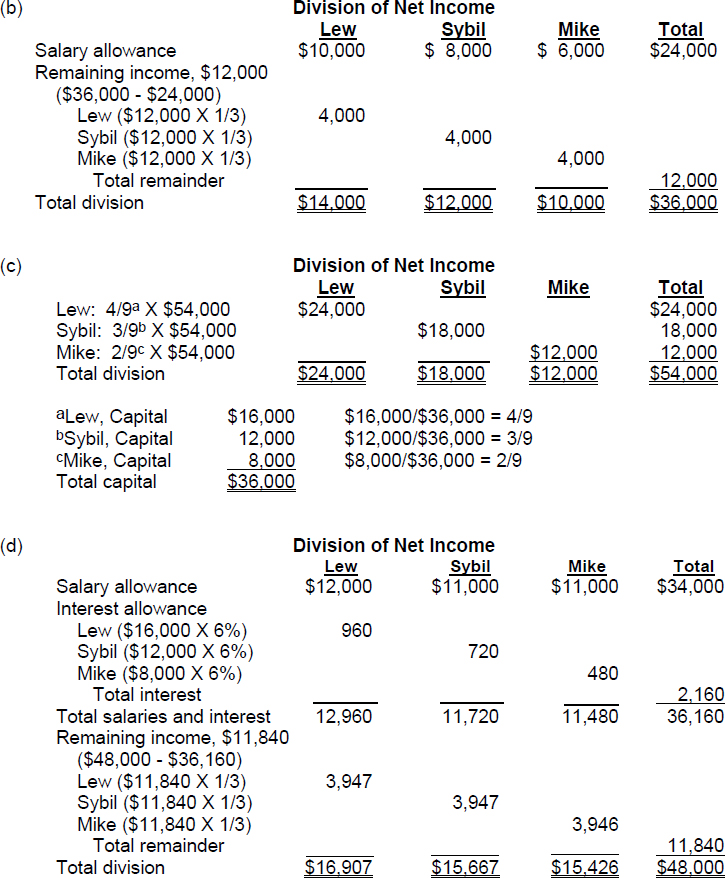

Purpose: (L.O. 3) This exercise will give your practice in allocating partnership net income (or net loss) among partners under various arrangements.

The following balances pertain to the partnership equity accounts of the Haveard Vegetable Market at January 1, 2014:

Instructions

Compute the division of partnership net income (or net loss) in each of the independent situations described below.

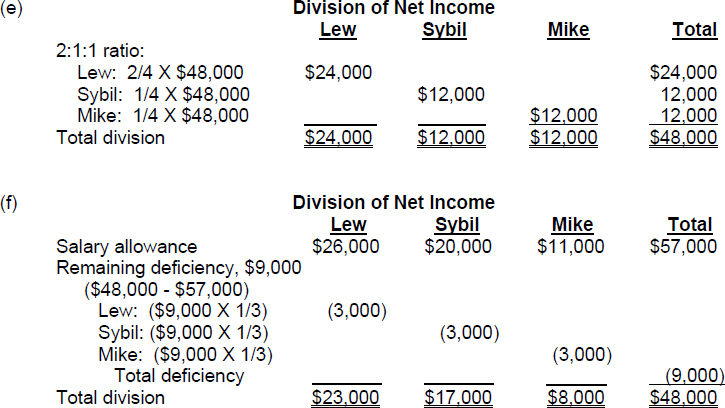

(a) Net income is $36,000. No written agreement on profit distribution exists.

(b) Net income is $36,000. Salaries are $10,000 to Lew, $8,000 to Sybil, and $6,000 to Mike. Any remaining profits are shared equally.

(c) Net income is $54,000. Net income is divided on the basis of relative beginning capital account balances.

(d) Net income is $48,000. Salaries are $12,000 to Lew, $11,000 to Sybil and $11,000 to Mike. Interest of 6% on beginning capital account balances is to be allocated. Any remaining income is to be divided equally.

(e) Net income is $48,000 and is to be divided on a 2:1:1 ratio (2/4 to Lew, 1/4 to Sybil, and 1/4 to Mike).

(f) Net income is $48,000. Salaries are $26,000 to Lew, $20,000 to Sybil and $11,000 to Mike. The remainder is to be divided equally.

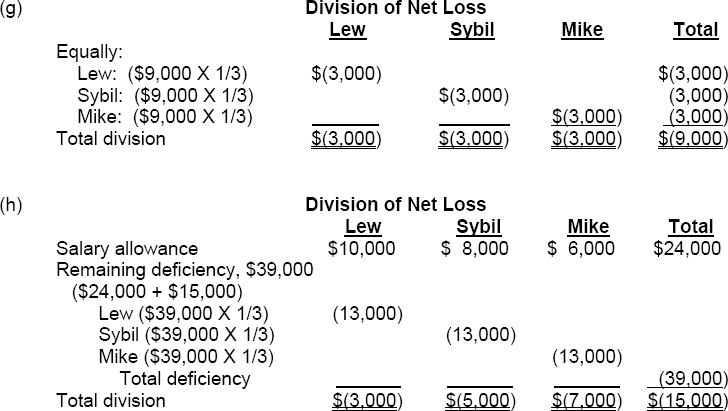

(g) Net loss is $9,000 and is to be divided equally.

(h) Net loss is $15,000. Salaries are $10,000 to Lew, $8,000 to Sybil, and $6,000 to Mike. The remainder is divided equally.

SOLUTION TO EXERCISE 12-5

Approach: Allocate salary allowances, then interest allowances, and then apportion the remainder using the appropriate ratio.

| TIP: | Interest on partnership capital is determined by multiplying the appropriate interest rate by the balance in the individual partner's capital account. Usually, the balance at the beginning of the period is used. |

| TIP: | If the salary and interest allocations exceed the total profits to be divided, the resulting negative figure (deficiency) must be divided among the partners, thereby reducing the net amounts to be credited to the partners' capital accounts in the process of closing the Income Summary account. |

EXERCISE 12-6

Purpose: (L.O. 5) This exercise will test your ability to compute both the cash to be received by each partner and the entries to be made when a partnership is dissolved.

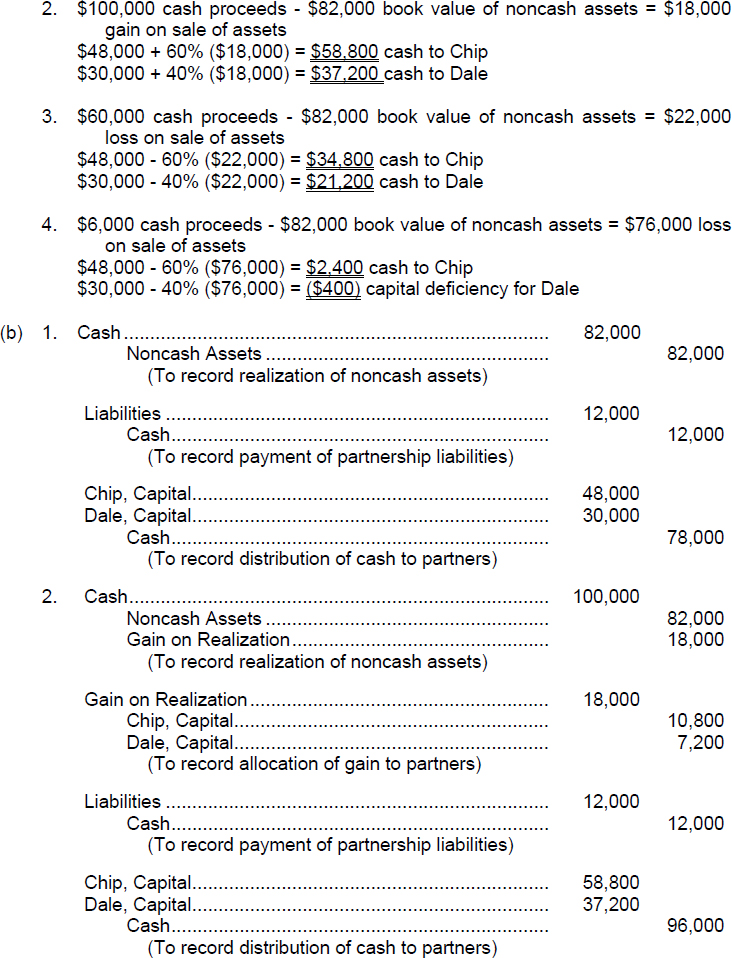

Chip and Dale are partners who share profits and losses in a 60%:40% ratio, respectively. Before liquidation of the noncash assets, the following amounts pertain to the partnership:

Instructions

(a) Compute the amount of cash that each partner will receive under the following independent situations:

- The noncash assets are sold for $82,000 cash, the liabilities are paid, and the remaining cash is distributed to the partners.

- The noncash assets are sold for $100,000 cash, the liabilities are paid, and the remaining cash is distributed to the partners.

- The noncash assets are sold for $60,000 cash, the liabilities are paid, and the remaining cash is distributed to the partners.

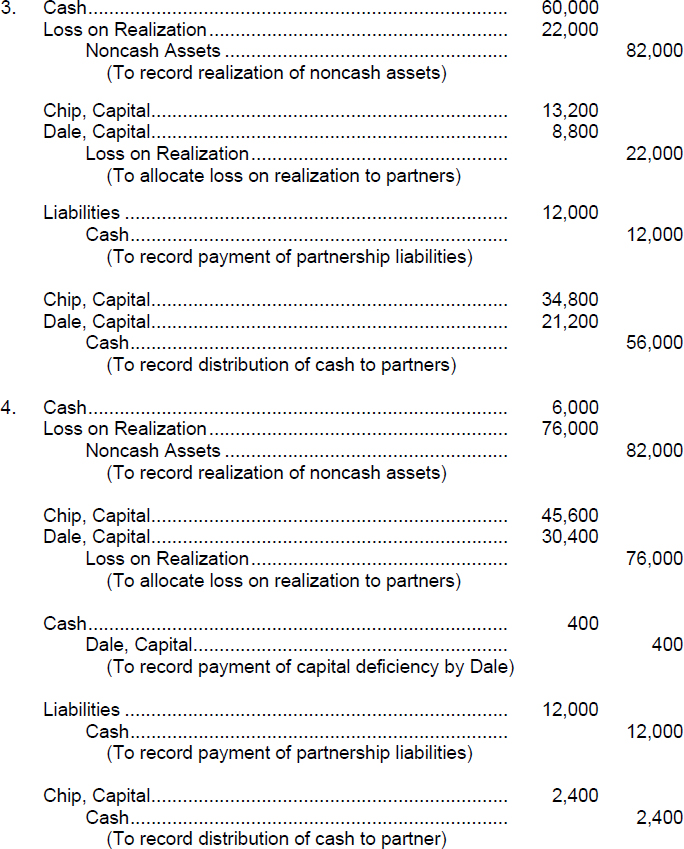

- The noncash assets are sold for $6,000 cash, Dale makes payment of his capital deficiency, the liabilities are paid, and the remaining cash is distributed.

(b) Prepare the journal entries for the partnership books for the dissolution of the partnership under each of the situations listed in (a) above.

| TIP: | In a real-life business, there would be separate accounts for each noncash asset and each type of liability. These items were combined in this exercise to simplify the solution and to highlight the main points being illustrated. |

| TIP: | Total liabilities ($12,000) can be determined by deducting total owners' equity ($48,000 + $30,000 = $78,000) from total assets ($90,000). |

SOLUTION TO EXERCISE 12-6

| TIP: | If Dale had not made payment for his capital deficiency, the last three entries would have been as follows:

|

Approach and Explanation: The liquidation of a partnership entails performing the following steps in order:

- Sell noncash assets for cash and recognize a gain or loss on realization.

- Allocate the gain or loss on realization to the partners using their income ratio.

- Pay partnership liabilities in cash.

- Distribute the remaining cash to partners on the basis of their capital balances.

In liquidation of a partnership, the sale of noncash assets for cash is called realization, and the difference between the book value of the assets and the cash proceeds is called the gain or loss on realization.

When gains and losses on realization are divided among the partners, the capital accounts of all partners may have credit (normal) balances in their capital accounts (a situation called no capital deficiency) or one (or more) partner(s) may end up with a debit (negative) balance instead of a normal credit balance (a situation referred to as a capital deficiency). When a capital deficiency occurs, that partner must contribute the amount of his (her) negative balance to the partnership. If a partner is unable to pay the amount owed to the partnership, the partners with credit balances must absorb the loss. The loss is allocated on the basis of the income ratio that exists between the partners with credit balances.

Notice that assumption 1 resulted in no gain or loss on realization. Assumption 2 resulted in a gain on realization. Assumption 3 resulted in a loss on realization. Assumption 4 resulted in a loss on realization and a capital deficiency.

*ILLUSTRATION 12-2

ADMISSION OF A NEW PARTNER IN A

BONUS SITUATION (L.O. 6)

A bonus to old partners results when the new partner's capital credit on the date of admittance is less than his or her investment in the firm. A bonus to a new partner results when the new partner's capital credit is greater than his or her investment of net assets in the firm. The procedure for determining the new partner's capital credit and the bonus is as follows:

- Determine the total capital of the new partnership by adding the new partner's investment to the total capital of the old partnership.

- Determine the new partner's capital credit by multiplying the total capital of the new partnership by the new partner's ownership interest.

- Determine the amount of bonus by comparing the new partner's capital credit with the new partner's investment.

- Allocate the bonus to the old partners on the basis of their income ratio or allocate the bonus to the new partner, whichever is appropriate.

- If the new partner's capital credit exceeds the new partner's investment, the bonus is allocated to the new partner, which means the capital account balances of the old partners should be decreased by their respective portion of the bonus allocation. This decrease is based on the income ratio of the old partners before admission of the new partner.

- If the partner's capital credit is less than the new partner's investment, the bonus is allocated to the old partners, which means the capital account balances of the old partners will be increased by their respective portion of the bonus allocation. This increase is also based on the income ratio of the old partners before admission of the new partner.

*EXERCISE 12-7

Purpose: (L.O. 6) This exercise will test your knowledge of the various situations in which a new partner is admitted to a partnership.

The following represent various arrangements (situations) which may be present when a new partner is admitted to a partnership:

- A new partner is admitted by purchasing all or part of the interest of an existing partner or partners.

- A new partner is admitted by investment and no bonus is granted.

- A new partner is admitted by investment and a bonus is granted to the old partners.

- A new partner is admitted by investment and a bonus is granted to the new partner.

Instructions

The above are descriptions of situations involving the admission of a new partner to a partnership. For each of the statements, identify the arrangement or arrangements to which the statement would apply by using the appropriate code letter(s). There may be more than one answer for each of them.

SOLUTION TO EXERCISE 12-7

Approach: Review Illustration 12-2 for a description of situations involving a bonus.

Explanation:

Situation a: A new partner is admitted by purchasing all or part of the interest of an existing partner or partners.

- When a new partner purchases an interest from one of the established partners, the appropriate amount of interest in the business is transferred from the existing partner's capital account to the new partner's capital account. Thus, there is no change in the total assets or total owners' equity of the business. (The exact amount paid by the new partner is determined by the new partner and the old partner and does not appear on the partnership's books.)

- When an old partner sells his partnership interest (or a portion of it), he records the sale on his personal books by a debit to Cash for the sales price, and a credit to the asset, Interest in Partnership, for his book value of the interest. If the situation warrants, he may also record a debit to Loss on Sale of Investment or a credit to Gain on Sale of Investment for the difference between his book value and the sales price.

- When a new partner purchases the interest (or a portion thereof) of an existing partner, all partners must agree on a new manner in which to divide partnership profits and losses. If they do not reach a mutual agreement, the law assumes that they share equally.

Situation b: A new partner is admitted by investment and no bonus is granted.

- When a new partner is admitted to the business by investment (rather than by purchase of an existing interest), the new partner contributes assets (cash and/or noncash) to the partnership. Thus, the total assets and total owners' equity of the partnership are increased through the creation of a capital interest for the new partner.

- If the increase in the total amount of owners' equity is equal to the value of the assets that the new partner invests in the partnership and if the new partner is to receive credit for that exact amount, there is no bonus payment involved. The entry on the partnership's books is a simple debit to Cash (or other assets contributed by the new partner) and a credit to the new owner's capital for the fair market value of the assets contributed.

Situation c: A new partner is admitted by investment and a bonus is granted to the old partners.

- At the time a new partner is being admitted by investment, the fair market values of old partnership assets such as land and buildings may be higher than their book values or unrecorded goodwill may exist and, therefore, the new partner is willing to pay a bonus to the old partners in order to become a partner.

- A bonus payment is made to the old partners when their capital accounts are credited with a portion of the amount that would normally be credited to the capital account of the new partner.

- When a new partner is admitted by investment and a bonus payment to the old partners is recognized, the following events occur:

(a) The increase in assets is equal to the cash and noncash assets invested by the new partner.

(b) The increase in total owners' equity is equal to the cash and noncash assets invested by the new partner less any liabilities assumed by the partnership.

(c) The new partner's capital account is credited with an amount less than the net amount of cash and noncash assets the new partner invested.

(d) The bonus to the old partners is allocated to them on the basis of their income ratio before the admission of the new partner.

Situation d: A new partner is admitted by investment and a bonus is granted to the new partner.

- At the time a new partner is being admitted by investment, the fair market values of old partnership assets may be lower than their books values or the new partner may have some special expertise for which the old partners are willing to pay a bonus to the new partner.

- A bonus payment is made to the new partner when the new partner's capital account is credited with amounts transferred from the capital accounts of the old partners.

- When a new partner is admitted by investment and a bonus payment to the new partner is recognized, the following events occur:

(a) The increase in assets is equal to the cash and noncash assets invested by the new partner.

(b) The increase in total owners' equity is equal to the amount of cash and noncash assets invested by the new partner less any liabilities assumed by the partnership.

(c) The new partner's capital account is credited with an amount more than the amount of cash and noncash assets the new partner invested.

(d) The bonus to the new partner results in a decrease in the capital balances of the old partners based on their income ratio before the admission of the new partner.

*EXERCISE 12-8

Purpose: (L.O. 6) This exercise will give you practice in recording the entry for the admittance of a new partner, given different agreements for admittance.

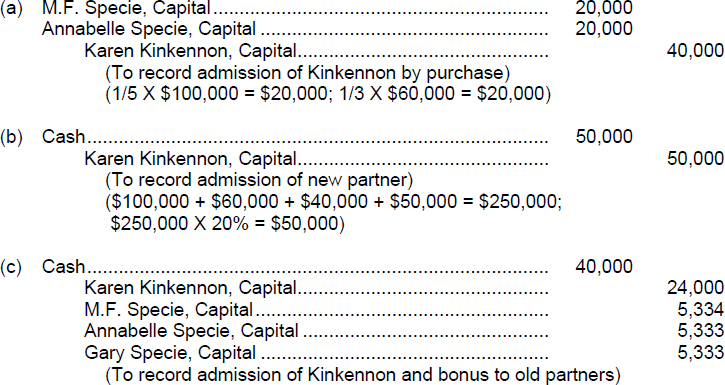

M.F. Specie, his wife Annabelle, and their son, Gary, are partners in a family business. They have respective capital account balances of $100,000, $60,000, and $40,000. They share profits and losses equally.

Instructions

Prepare the journal entry to record Karen Kinkennon's admittance to the partnership under each of the following independent assumptions:

(a) Karen acquires a 20% interest in the partnership by purchasing one-fifth of M.F.'s investment and one-third of Annabelle's interest. Karen pays cash of $25,000 to M.F. and $25,000 to Annabelle. The new partnership of M.F., Annabelle, Gary, and Karen will share profits and losses by the ratio of 2:1:1:1.

(b) Karen acquires a 20% interest in the partnership for a $50,000 cash investment. No bonus is recognized. The new partnership will share profits and losses equally.

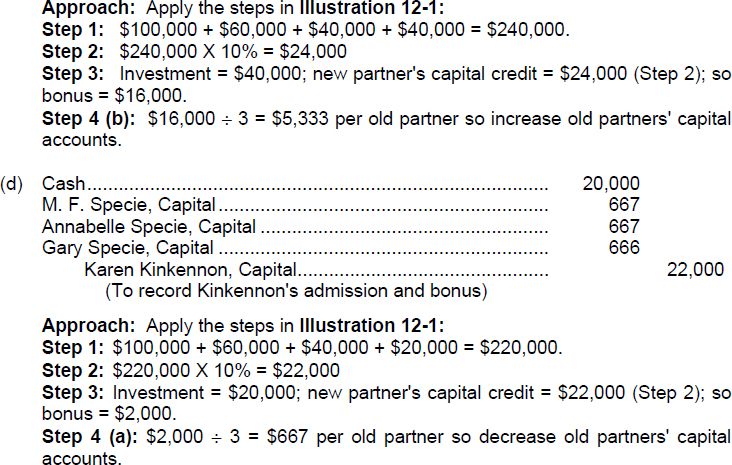

(c) Karen acquires a 10% interest in the partnership for a $40,000 investment. A bonus is granted to the old partners. The new partnership of M.F., Annabelle, Gary, and Karen will share profits and losses equally.

(d) Karen acquires a 10% interest in the partnership for a $20,000 investment. A bonus is granted to the new partner. The new partnership of M.F., Annabelle, Gary, and Karen will share profits and losses equally.

SOLUTION TO EXERCISE 12-8

*EXERCISE 12-9

Purpose: (L.O. 7) This exercise will illustrate the accounting for the withdrawal of a partner under different assumptions.

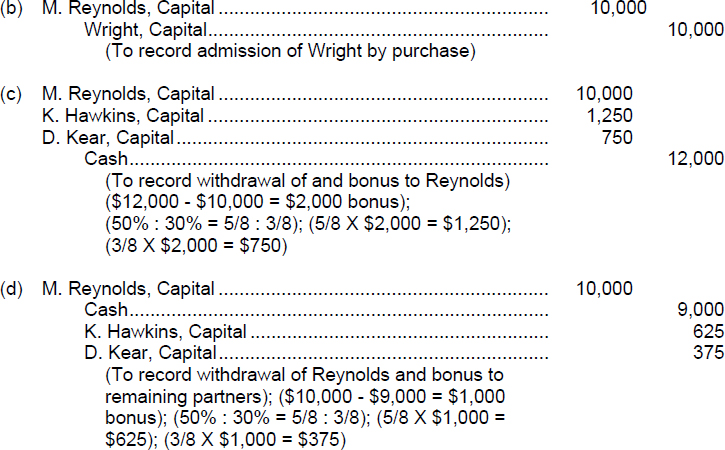

On December 31, 2014, the capital account balances and income-sharing percentages in Wiley Books, a partnership, are as follows:

Instructions

Prepare the journal entry on the partnership books to record the withdrawal of Reynolds under each of the following assumptions:

(a) Each of the remaining partners agrees to pay $6,500 in cash from personal funds to purchase Reynolds' ownership equity. Each receives 50% of Reynolds' partnership interest.

(b) Joe Wright agrees to purchase Reynolds' ownership interest for $14,000 cash.

(c) Reynolds is paid $12,000 from partnership assets and a bonus to the retiring partner is recognized.

(d) Reynolds is paid $9,000 from partnership assets, and bonuses to the remaining partners are recorded.

SOLUTION TO EXERCISE 12-9

| TIP: | The withdrawal of a partner when payment is made from partners' personal assets is the direct opposite of admitting a new partner who purchases a partner's interest. Payment to the retiring partner is made directly from the remaining partners' personal assets. Partnership assets are not involved in any way, and total capital does not change. Thus, the effect on the partnership is limited to a realignment of the partners' capital balances. The amount paid for the retiring partner's interest does not impact the journal entry on the partnership books. |

Approach and Explanation: When a partner withdraws, determine whether partnership assets are affected or not affected. In assumption (a), the retiring partner is bought out by the other partners, but the other partners use their personal assets rather than partnership assets to accomplish the buyout. Therefore, only capital accounts are affected in the journal entry to record assumption (a), and the amount of assets received by the retiring partner is not reflected on the partnership books. In assumption (b), two individuals (the retiring partner and an outsider named Wright) make a deal that again does not affect the partnership's assets. Only the capital accounts on the partnership's books are affected when a new partner purchases an old partner's ownership interest. In assumptions (c) and (d), partnership assets are used to payoff the withdrawing partner. If the amount of partnership assets being distributed to the retiring partner differs from the balance of that partner's capital account before withdrawal, there is a bonus situation and the procedure for determining and allocating the bonus as follows:

- Determine the amount of the bonus by comparing the assets disbursed to the retiring partner with the retiring partner's capital account balance.

-

(a) If the amount of assets distributed exceed the retiring partner's capital account balance, the excess is a bonus to the retiring partner. The bonus is deducted from the remaining partners' capital balances on the basis of their income ratio.

(b) If the amount of assets distributed is less than the retiring partner's capital account balance, the difference is a bonus to the remaining partners and will be allocated (credited) to the capital accounts of the remaining partners on the basis of their income ratio.

Assumption (c) is an example of a bonus paid to the retiring partner and assumption (d) is an example of a bonus paid to the remaining partners.

A bonus may be paid to a retiring partner when (1) the fair market values of partnership assets are more than their book values; (2) there is unrecorded goodwill resulting from the partnership's superior earnings record; or (3) the remaining partners are anxious to remove the withdrawing partner from the firm.

A retiring partner may give a bonus to the remaining partners when (1) partnership assets have book values in excess of their fair market values; (2) the partnership has a poor earnings record; or (3) the withdrawing partner is anxious to leave the partnership.

EXERCISE 12-10

Purpose: (L.O. 1 thru 7) This exercise will quiz you about terminology used in this chapter.

A list of accounting terms with which you should be familiar appears below:

*Admission by investment

*Admission by purchase of an interest

Capital deficiency

General partner

Income ratio

Limited liability company

Limited liability partnership

Limited partners

Limited partnership

No capital deficiency

Partners' capital statement

Partnership

Partnership agreement

Partnership dissolution

Partnership liquidation

Schedule of cash payments

*Withdrawal by payment from partners' personal assets

*Withdrawal by payment from partnership assets

Instructions

For each item below, enter in the blank the term that is described.

- ____________________An association of two or more persons to carry on as co-owners of a business for profit.

- ____________________A written contract expressing the voluntary agreement of two or more individuals in a partnership.

- ____________________Admission of a partner in a personal transaction between one or more existing partners and the new partner; does not change total partnership assets or total capital.

- ____________________Admission of a partner by investing assets in the partnership, causing both partnership net assets and total capital to increase.

- ____________________The basis for dividing net income and net loss in a partnership.

- ____________________The owners' equity statement for a partnership which shows the changes in each partner's capital balance and in total partnership capital during the year.

- ____________________A debit balance in a partner's capital account after allocation of gain or loss on realization.

- ____________________All partners have credit balances after allocation of gain or loss on realization.

- ____________________A change in partners, due to withdrawal or admission, which does not necessarily terminate the business.

- ____________________Withdrawal of a partner in a personal transaction between partners; does not change total partnership assets or total capital.

- ____________________Withdrawal of a partner in a transaction involving the partnership, causing both partnership net assets and total capital to decrease.

- ____________________A schedule showing the distribution of cash to the partners in the liquidation of a partnership. (Sometimes called a safe cash payments schedule).

- ____________________An event that ends both the legal and economic life of a partnership.

- ____________________A partner who has unlimited liability for the debts of the firm.

- ____________________Partners whose liability for the debts of the firm is limited to their investment in the firm.

- ____________________A partnership in which one or more general partners have unlimited liability and one or more partners have limited liability for the obligations of the firm.

- ____________________A partnership of professionals in which partners are given limited liability and the public is protected from malpractice by insurance carried by the partnership.

- ____________________A form of business organization, usually classified as a partnership and usually with limited life, in which partners, who are called members, have limited liability.

SOLUTION TO EXERCISE 12-10

- Partnership

- Partnership agreement

- *Admission by purchase of an interest

- *Admission by investment

- Income ratio

- Partners' capital statement

- Capital deficiency

- No capital deficiency

- Partnership dissolution

- *Withdrawal by payment from partners' personal assets

- *Withdrawal by payment from partnership assets

- Schedule of cash payments

- Partnership liquidation

- General partner

- Limited partners

- Limited partnership

- Limited liability partnership

- Limited liability company

*This material is covered in the Appendix to Chapter 12 in the text.

ANALYSIS OF MULTIPLE-CHOICE TYPE QUESTIONS

- (L.O. 1) A limited partnership is a partnership in which:

- one or more, but not all, of the partners assume a limited liability in the operations of the business.

- creditors cannot claim the personal assets of any of the partners.

- all partners invest a limited amount of assets.

- profit distributions to partners are limited to a set sum.

Approach and Explanation: Mentally define limited partnership before you read the answer selections. Some states allow limited partnerships in which the liability of a partner is limited to the partner's equity in the partnership. However, there must always be at least one partner with unlimited liability, often referred to as the general partner. (Solution = a.)

- (L.O. 1) Which of the following is not a characteristic of the partnership form of business organization?

- Unlimited liability of general partners.

- Mutual agency relationship of owners.

- Limited life.

- Separate taxable entity.

Explanation: A partnership is not a taxable entity. However, a partnership is required to file an information tax return showing partnership net income and each partner's share. The partners then pick up their share of the business income on their personal tax returns and pay taxes at personal tax rates. Taxes are due on a partner's share of the partnership income, regardless of the amount of the partner's withdrawals from the business during the year. (Solution = d.)

- (L.O. 4) The following items may be reflected in a partner's capital account:

- The partner's investments in the business.

- The partner's share of business profits.

- The partner's share of business losses.

- The partner's drawings.

- The partner's disinvestments.

Which of the above items (by reference numbers) are reflected as credits in the partner's capital account?

- 1, 2, and 5.

- 2 and 5.

- 1 and 2.

- 3, 4, and 5.

- none of the above.

Approach and Explanation: Draw a T-account and enter the items above. Notice the credits are for the items that cause increases in a partner's capital account. (Solution = c.)

- (L.O. 2) In starting a partnership, the noncash assets contributed to the business by the partners should be recorded on the business books at:

- the fair market values.

- the amounts the assets originally cost the individual partners.

- proportional amounts that correspond to the income-sharing agreement.

- the amount at which the assets were reported on the partner's old books (the partner's book value).

Explanation: Each partner's initial investment in a partnership should be recorded at the fair market value of the assets at the date of their transfer to the partnership. (Solution = a.)

- (L.O. 3) Salaries allocated to the owners of a partnership are:

- recorded as an operating expense and reported on the income statement.

- always equal for each general partner within the partnership.

- never allowed for limited partners.

- used only as a means of computing a partner's share of the business income and do not get reported as an expense.

Explanation: Partners' salaries are not an expense on the partnership's books; they are used only as a means of determining a partner's share of partnership net income or net loss. (Solution = d.)

- (L.O. 3) When salary and interest allocations to partners are provided for in a partnership income-sharing agreement, these allocations:

- must also be made in determining the amount of net loss that is to be allocated to each partner.

- are reported as expenses on the income statement of the business.

- need not be made if they exceed the amount of net income for the period.

- must be paid in cash.

Explanation: Salary and interest allowances for partners are used in the determination of a partner's share of partnership profits and losses. They are not expenses in determining partnership net income or net loss. (Solution = a.)

- (L.O. 4) Mike invested $80,000 in a partnership named M & J Printers at the beginning of 2013. Mike and his partner Jane share profits and losses equally. The business reported net income of $22,000 and $28,000 for the year 2013 and 2014, respectively. Mike's drawings totaled $10,000 and $16,000 for 2013 and 2014, respectively. What is the balance of Mike's capital account to be reported on the partnership's balance sheet at the end of 2014?

- $131,000.

- $105,000.

- $104,000.

- $79,000.

Approach and Explanation: Draw a T-account for Mike's capital account. Enter the data given.

- (L.O. 3) Partners Steve, Bev, and Connie are to share partnership income in a 3 : 1 : 1 ratio. If the net income of the partnership for one year is $90,000, Steve's share amounts to:

- $67,500.

- $54,000.

- $30,000.

- $27,000.

Approach and Explanation: Add the items in the ratio: 3 + 1 + 1 = 5. Use the five as the denominator of three fractions and the 3, 1, and 1 as numerators. Thus, the fractions are 3/5, 1/5, and 1/5 for Steve, Bev, and Connie, respectively.

3/5 × $90,000 = $54,000 for Steve's share (Solution = b.)

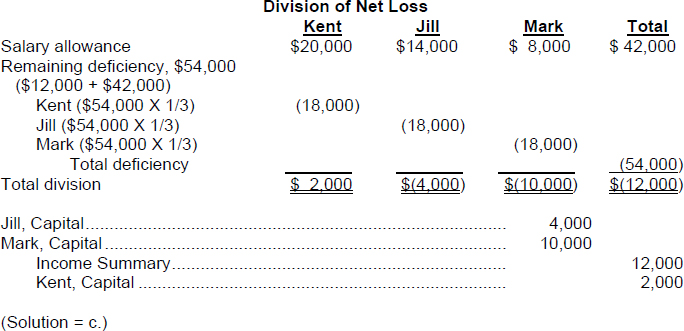

- (L.O. 3) Partners Kent, Jill, and Mark have the following income-sharing agreement for their partnership: $20,000 Salary allowance for Kent; $14,000 Salary allowance for Jill; $8,000 Salary allowance for Mark. Remaining profits and losses are to be divided equally. If the results of operations for 2014 show a net loss of $12,000, the journal entry to close the Income Summary account will include a:

- debit to Kent, Capital for $4,000.

- credit to Mark, Capital for $10,000.

- credit to Kent, Capital for $2,000.

- debit to Income Summary for $12,000.

Approach and Explanation: Compute each partner's share of the net loss and prepare the journal entry to close the Income Summary account.

- (L.O. 5) Diane and Emmett are partners in the D & E Store. Daniel is being admitted as a new partner by the purchase of part of the interests of the existing partners. Which of the following is true?

- The balances of the old partners' capital accounts will change by the same amount.

- The total assets of the partnership are increased by this transaction.

- The total amount of owner's equity of the partnership is not changed by this transaction.

- The capital account for Diane will increase in amount.

Explanation: Admission of a new partner by having the new partner purchase an interest of one or more of the existing partners results in no change in total assets and no change in total owners' equity of the partnership. The capital account for Diane will decrease in amount. The capital accounts of the old partners may or may not decrease by the same amount, depending on what portion of the partners' interests is purchased by the new partner. (Solution = c.)

- (L.O. 5) Samantha is being admitted as a new partner into a partnership business. If the increase in total owners' equity is equal to the fair market value of the assets that Samantha invests in the partnership and Samantha's capital account is credited for an amount less than the value of the new assets contributed, the arrangement for Samantha's admittance is by:

- purchase of all or part of the interest of an existing partner or partners.

- investment and no bonus is granted.

- investment and a bonus is granted to the old partners.

- investment and a bonus is granted to the new partner.

Explanation: The excess of the fair market value of the assets contributed over the new partner's capital credit is a bonus that is granted to the old partners. It should be allocated to them by their respective income ratios. (Solution = c.)

- (L.O. 5) If a bonus is granted to a new partner upon admittance to a partnership, this bonus will result in a(an):

- increase in the capital accounts of the old partners.

- decrease in the capital accounts of the old partners.

- operating expense to be reported on the income statement of the partnership.

- amount to be recorded in the new partner's drawing account.

Explanation: A bonus is granted to a new partner when the new partner's capital credit exceeds the new partner's investment. Thus, in the entry to record the new partner's admittance, the credit to the new partner's capital account is greater than the debit(s) to assets. The remaining debits needed to balance the entry come from decreases in the capital accounts of the old partners. The bonus to the new partner is allocated to the old partners (as a reduction in their equity) based on the income-sharing ratio before admission of the new partner. (Solution = b.)

- *(L.O. 7) The following balances exist at December 31, 2014, for the Food Court, a partnership.

The partners share profits in a ratio of 3 : 2 : 1. In the process of liquidating the partnership in January 2015, the noncash assets are sold for $50,000 cash. Assuming any resulting capital deficiency is allocated to the remaining partners, the amount of cash to be distributed to B. Bean amounts to:

- $12,500.

- $15,000.

- $25,000.

- $27,500.

Approach and Explanation: Work through the steps in the liquidation process:

- Sell noncash assets for cash and recognize a gain or loss on realization.

$50,000 cash proceeds − $110,000 book value = $60,000 loss on realization

- Allocate the gain or loss on realization to the partners using their income ratio.

3 : 2 : 1 = 3/6 : 2/6 : 1/6

$60,000 × 3/6 = $30,000 loss allocated to B. Bean; $60,000 × 2/6 = $20,000 loss allocated to H. Burger; $60,000 × 1/6 = $10,000 loss allocated to I. Lamb.

The resulting $10,000 deficiency for H. Burger is allocated to the remaining partners by their respective ratios (3 : 1 means 3/4 of $10,000 is allocated to B. Bean and 1/4 of $10,000 is allocated to I. Lamb). The capital accounts would then reflect the following:

- Pay partnership liabilities in cash. The Cash account will then reflect the following:

- Distribute the remaining cash to partners on the basis of their capital balances.

$12,500 to B. Bean and $27,500 to I. Lamb

(Solution = a.)

- *(L.O. 7) In the process of dissolving a partnership, any cash that remains after the noncash assets have been liquidated and all liabilities have been paid is distributed to the partners:

- in accordance with their income ratio.

- in proportion to the relative amount of time the partners have devoted to the business.

- according to the remaining balances in their respective capital accounts.

- in proportion to their relative original investments in the partnership.

Explanation: The balance of a partner's capital account represents that partner's claim against partnership assets. Thus, in liquidation, a partner receives assets equal to the balance of that partner's capital account. Be careful not to confuse this issue with the question of how to allocate gains and losses on realization which is part of the liquidation process. When the noncash assets are sold (converted to cash), they are usually exchanged for an amount of cash unequal to their book (carrying) values. Thus, gains and losses on realization are recognized. These gains and losses are allocated to the partners' capital accounts based on their income ratio. The resulting balances in the partners' capital accounts dictate the amount of cash due each partner. (Solution = c.)

- *(L.O. 7) In the process of dissolving a partnership, if the allocation of the losses from liquidation of the noncash assets results in a debit balance in the capital account of one partner, this indicates that:

- an error was made in the recording process.

- creditors will not be paid the full amounts due them.

- the partner with the debit balance should contribute cash to the partnership equal in amount to the negative balance.

- an amount of cash equal to the debit balance is owed to that partner by the partnership.

Explanation: The debit balance in the partner's capital account is called a capital deficiency. That partner should pay the partnership the amount of the capital deficiency. In the event of nonpayment, however, the capital deficiency is eliminated by reductions of the capital accounts of the remaining partners (in the proportion of their respective income ratios). (Solution = c.)