CHAPTER 11

![]()

CURRENT LIABILITIES AND PAYROLL ACCOUNTING

OVERVIEW

Initially, the resources (assets) of a business have to come from an entity outside of the particular organization. Two main sources of resources are creditor sources (liabilities) and owner's sources (owner's equity). In this chapter, we begin our in-depth discussion of liabilities.

Due to the nature of some business activities, an entity will commonly receive goods and services and not pay for them until days or weeks later. Therefore, at a specific point in time, such as a balance sheet date, we may find that a business has obligations for merchandise received from suppliers (accounts payable), for money it has borrowed (notes payable), for interest incurred (interest payable), for sales tax charged to customers which has not yet been remitted to the government (sales taxes payable), for salaries and wages (salaries and wages payable), and for amounts due to government agencies in connection with employee compensation (Federal Income Tax Withholdings Payable, FICA Taxes Payable, Federal Unemployment Taxes Payable, and State Unemployment Taxes Payable). Such payables are reported as current (short-term) liabilities because they will fall due within the next 12 months and will require the use of current assets (cash, in most cases) to liquidate them. Accounting for current liabilities is discussed in this chapter.

SUMMARY OF LEARNING OBJECTIVES

- Explain a current liability and identify the major types of current liabilities. A current liability is a debt that a company can reasonably expect to pay (1) from existing current assets or through the creation of other current liabilities, and (2) within one year or the operating cycle, whichever is longer. The major types of current liabilities are notes payable, accounts payable, sales taxes payable, unearned revenues, and accrued liabilities such as taxes, salaries and wages, and interest payable.

- Describe the accounting for notes payable. When a promissory note is interest-bearing, the amount of assets received upon the issuance of the note is generally equal to the face value of the note. Interest expense accrues over the life of the note. At maturity, the amount paid equals the face value of the note plus accrued interest.

- Explain the accounting for other current liabilities. Companies record sales taxes payable at the time the related sales occur. The company serves as a collection agent for the taxing authority. Sales taxes are not an expense to the company. Companies initially record unearned revenues (advances from customers) in an Unearned Revenue account. As a company recognizes revenue, a transfer from unearned revenue to revenue occurs. Companies report the current maturities of long-term debt as current liabilities in the balance sheet.

- Explain the financial statement presentation and analysis of current liabilities. Companies should report the nature and amount of each current liability in the balance sheet or in schedules in the notes accompanying the financial statements. The liquidity of a company may be analyzed by computing working capital and the current ratio.

- Describe the accounting and disclosure requirements for contingent liabilities. If it is probable (likely to occur) that the contingency will happen and the amount is reasonably estimable, the company should record the liability in the accounts. However, if the contingency is only reasonably possible (it could occur), then it need be disclosed only in the notes to the financial statements. If the possibility that the contingency will happen is remote (unlikely to occur), it need not be recorded or disclosed.

- Compute and record the payroll for a pay period. The computation of the payroll involves gross earnings, payroll deductions, and net pay. In recording the payroll, companies debit Salaries and Wages Expense for gross earnings, credit individual tax and other liability accounts for payroll deductions, and credit Salaries and Wages Payable for net pay. When the payroll is paid, companies debit Salaries and Wages Payable and credit Cash.

- Describe and record employer payroll taxes. Employer payroll taxes consist of FICA, federal unemployment taxes, and state unemployment taxes. The taxes are usually accrued at the time the company records the payroll by debiting Payroll Tax Expense and crediting separate liability accounts for each type of tax.

- Discuss the objectives of internal control for payroll. The objectives of internal control for payroll are (1) to safeguard company assets against unauthorized payments of payrolls, and (2) to ensure the accuracy of the accounting records pertaining to payrolls.

- *Identify additional fringe benefits associated with employee compensation. Additional fringe benefits associated with wages are paid absences (paid vacations, sick pay benefits, and paid holidays), postretirement benefits (pensions and health care and life insurance).

*This material is discussed in the Appendix 11A in the text.

TIPS ON CHAPTER TOPICS

| TIP: | Current liabilities are also called short-term liabilities or short-term debt. Non-current liabilities are often called long-term liabilities or long-term debt. |

| TIP: | Current liabilities are obligations which come due within one year (or the company's operating cycle, if longer than a year) and whose liquidation is reasonably expected to require the use of existing resources properly classifiable as current assets, or the creation of other current liabilities. Noncurrent liabilities (or long-term liabilities) are obligations which do not meet the criteria to be classified as current. |

| TIP: | Companies often have a portion of long-term debt that is due each year. At a balance sheet date, any portion of long-term debt that is due within one year of that balance sheet date is referred to as “current maturities of long-term debt” or “current portion of long-term debt” or “long-term debt due within one year” and is classified as a current liability. |

| TIP: | A liability is recognized (recorded) when a legally binding obligation is incurred. Examples include:

(a) When cash is received. (b) When legal title to some asset other than cash is received (change in legal title usually occurs at the point that the asset is delivered to the buyer) and payment is deferred. (c) When services are received and payment is deferred. (d) As time passes (for example, interest accrues with passage of time). |

| TIP: | The amount of a liability is determined in one of three ways:

(a) By the amount of cash when cash is exchanged (for example, when money is borrowed from a bank). (b) By the negotiated or fair market value of noncash assets or services involved in a transaction. (c) By estimate. |

| TIP: | Computing the weekly, biweekly, or monthly payroll involves four basic steps:

(a) Determining the amount of employee compensation. (b) Calculating deductions from employee compensation. (c) Calculating employer tax liabilities based on employee compensation. (d) Maintaining proper employee payroll records. |

EXERCISE 11-1

Purpose: (L.O. 1) This exercise tests your ability to distinguish between current and noncurrent (long-term) liabilities.

| ______ 1. | Obligation to supplier for merchandise purchased on credit. (Terms 2/10, n/30). |

| ______ 2. | Note payable to bank maturing 90 days after balance sheet date. |

| ______ 3. | Note payable due January 1, 2017. |

| ______ 4. | Property taxes payable. |

| ______ 5. | Interest payable on note payable. |

| ______ 6. | Sales taxes payable. |

| ______ 7. | Portion of mortgage obligation due in years 2016 through 2020. |

| ______ 8. | Revenue received in advance, to be earned over the next six months. |

| ______ 9. | Salaries and wages payable. |

| ______ 10. | Rent payable. |

| ______ 11. | Short-term notes payable. |

| ______ 12. | Pension obligations maturing in ten years. |

| ______ 13. | Installment loan payments due three months after the balance sheet date. |

| ______ 14. | Installment loan payments due more than one year after the balance sheet date. |

| ______ 15. | Portion of mortgage obligation due within a year after the December 31, 2014 balance sheet date. |

| _______ 16. | Note payable maturing March 1, 2015. |

Instructions:

Indicate whether each of the above items would be reported as a current liability (CL) or a long-term liability (LT) on a balance sheet prepared at December 31, 2014.

Approach: Review the definition of a current liability. Analyze each situation above and determine if the liability will fall due within a year (or operating cycle) of the balance sheet date and whether it will require the use of current assets or the incurrence of another current liability to liquidate. If so, it is current; if not, it is long-term.

SOLUTION TO EXERCISE 11-1

- C

- C

- LT

- C

- C

- C

- LT

- C

- C

- C

- C

- LT

- C

- LT

- C

- C

EXERCISE 11-2

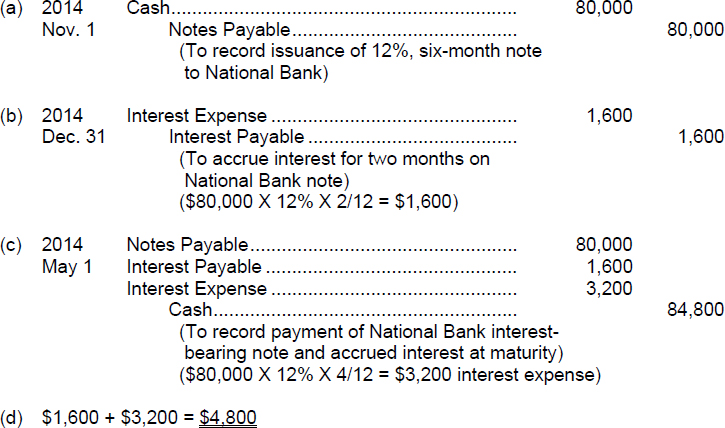

Purpose: (L.O. 2) This exercise will review the journal entries involved for an interest-bearing note payable.

On November 1, 2014, Bono Company borrowed $80,000 from National Bank and signed a note stipulating that $80,000 was to be repaid in 6 months with interest at 12%. Bono Company adjusts its accounts and prepares financial statements annually on December 31. (Reversing entries are not used.)

Instructions

(a) Prepare the journal entry on November 1, 2014, to record the loan.

(b) Prepare the adjusting entry on December 31, 2014.

(c) Prepare the journal entry at maturity (May 1, 2015).

(d) Determine the total financing cost (interest expense) for the six-month period.

SOLUTION TO EXERCISE 11-2

| TIP: | Interest rates are stated on an annual basis (per annum) unless otherwise indicated. Thus, the 12% rate in this exercise is an annual rate. |

EXERCISE 11-3

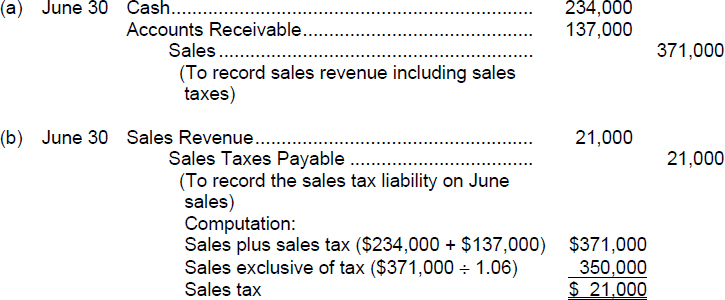

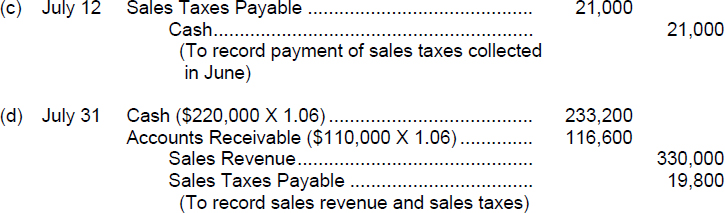

Purpose: (L.O. 3) This exercise will provide an example of the proper accounting for an obligation to an agency of the state government—unremitted sales taxes.

During the month of June, Chelsea's Boutique had cash sales of $234,000 and credit sales of $137,000, both of which include the 6% sales tax that must be remitted to the state by July 15. Sales taxes on June sales were lumped with the sales price and recorded as a credit to the Sales Revenue account.

During the month of July, Chelsea's Boutique set up a new cash register that rings up sales and the 6% sales tax separately. The register totals for July were cash sales of $220,000 and credit sales of $110,000. The related sales tax is not due to be paid until August 15.

Instructions

(a) Prepare the journal entry to record June's sales at June 30 (assuming the total sales for June are recorded at June 30).

(b) Prepare the adjusting entry that should be recorded to fairly present the financial statements at June 30.

(c) Prepare the journal entry to record the remittance of the sales taxes on July 12.

(d) Prepare the journal entry to record July's sales at July 31.

SOLUTION TO EXERCISE 11-3

EXERCISE 11-4

Purpose: (L.O. 3) This exercise will illustrate the accounting for unearned revenue.

Soap Opera Summarized is published by Viewer Publishers. Subscriptions to the magazine are sold for a one-year, two-year, or three-year period. Cash receipts from subscribers are credited to Unearned Subscription Revenue, and this account had a balance of $3,000,000 at December 31, 2014, before adjustment. Outstanding subscriptions at December 31, 2014, expire as follows:

Instructions

(a) Prepare the journal entry to adjust the Unearned Subscription Revenue account at December 31, 2014.

(b) Explain how relevant amounts will be reported on the annual financial statements prepared at the end of 2014.

SOLUTION TO EXERCISE 11-4

(b) Subscription revenue of $1,700,000 will appear on the income statement for the year ending December 31, 2014.

Unearned subscription revenue of $600,000 will appear as a current liability on the December 31, 2014, balance sheet because Viewer Publishers has an obligation to deliver magazines (or refund $600,000) to subscribers within one year of the balance sheet date because of revenues collected in advance.

Unearned subscription revenue of $700,000 will appear as a long-term liability on the December 31, 2014, balance sheet because of collections from customers for services to be performed in periods beyond one year from the balance sheet date.

Approach and Explanation: Draw a T-account. Enter the information given. Solve for the missing link.

A magazine company often collects cash from subscribers before it provides magazines to them. Thus, at the point of receipt of cash, the company has an obligation to publish and deliver magazines for a number of months that follow the cash receipts.

Revenue is to be recognized in the period services are performed. If cash collections of $3,000,000 have been received and credited to the unearned revenue account during the period and the only unearned amount at the end of the period is $1,300,000, $1,700,000 must be removed from the liability account (unearned revenue) and transferred to an earned revenue account.

| TIP: | Synonymous terms for unearned revenue are deferred revenue, revenue collected in advance, and revenue received in advance. Unearned revenue is a liability until the point in time when the revenue is earned or a refund is made. |

EXERCISE 11-5

Purpose: (L.O. 5) This exercise will test your ability to properly account for situations involving contingent liabilities.

As the accountant for the Blow-Dry Manufacturing Company you are to analyze the following situations in preparing the balance sheet at December 31, 2014:

- The Blow-Dry Manufacturing Company grants a six-month warranty on each of the hair dryers it sells. Based on past experience, it is estimated that 3% of all hair dryers sold are returned; it costs the company an average of $4.40 to satisfy the warranty obligation for each unit returned. The company sold 77,000 hair dryers in the last half of 2014 and has spent $3,000 for warranty work on those units.

- The Speedy-Dry Manufacturing Company has filed a lawsuit for $100,000 in damages against the Blow-Dry Manufacturing Company for infringement of patent rights. Legal counsel for Blow-Dry states that it is reasonably possible, but not likely, that there will be an unfavorable outcome of the case because the Blow-Dry Company has good evidence to support its position.

- The Internal Revenue Service is currently auditing a tax return of the Blow-Dry Company for a prior year. It is remotely possible that the IRS may disallow a deduction of $4,200 on the tax return.

- The Blow-Dry Company is a defendant in a lawsuit. A former executive filed suit on November 7, 2014 based on his claim that the Blow-Dry Company did not comply with a written promise to pay him a $50,000 bonus for 2013. The company did not make the bonus payment because the executive resigned the last week of December 2013. Legal counsel for the company states that the written agreement will probably be held to apply even though the executive resigned. The suit is expected to be settled early in 2015.

Instructions

Explain how to account for each of the situations. Should a liability be included on the face of the balance sheet at December 31, 2014 or should there only be disclosure in the notes accompanying the financial statements or should the item not be recorded or disclosed? Justify your answer.

SOLUTION TO EXERCISE 11-5

- Blow-Dry Manufacturing should include an estimated warranty liability in the current liability section of the balance sheet for $7,164 [(77,000 × 3% × $4.40) − $3,000]. Based on past experience, it is probable the company will have to expend goods and services to satisfy the warranty and the cost to do so is estimable.

- Blow-Dry Manufacturing should only disclose this contingent liability by a note to accompany the financial statements. It is only reasonably possible that a liability exists at the balance sheet date due to the patent infringement lawsuit.

- Blow-Dry Manufacturing Company need not disclose the IRS audit in the notes or include it in the body of the statements. It is only remotely possible that Blow-Dry will owe tax for the deduction in question.

- Blow-Dry Company should include a $50,000 liability in the current liability section of the balance sheet. It appears probable that Blow-Dry will lose the suit and the amount is estimable. A journal entry should be made to accrue the loss to the current period (2014). The entry will include a debit to Loss from Lawsuit and a credit to Lawsuit Payable for $50,000.

Approach: Think about the definition of a contingent liability and how to account for one. A contingent liability is a potential liability that may become an actual liability in the future based on the outcome of some future event. The following guidelines apply:

- If it is probable (likely) that a liability has been incurred and the amount is estimable, the liability should be recorded in the accounts. (The corresponding debit goes to an income statement account—expense or loss).

- If it is only reasonably possible (less than likely and more than remote) that a liability exists, the potential liability should simply be disclosed in the notes that accompany the financial statements. That is, the potential liability will not appear in the body of the financial statements.

- If it is only remotely possible (unlikely) that the future event will occur to substantiate a liability, the situation can be ignored. No liability is to be included in the balance sheet, and no note disclosure is required.

EXERCISE 11-6

Purpose: (L.O. 5) This exercise will provide an example of how to account for the sale of a product that includes a warranty.

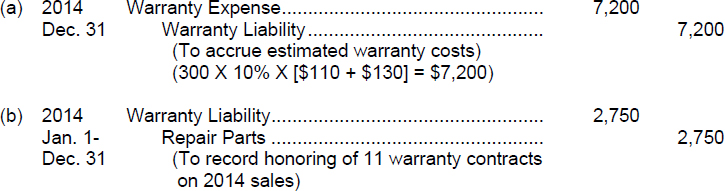

Colleen Mahla Company sells portable tables to be used for massage therapy. Each table has a built-in stereo system and carries a one-year warranty contract that requires the company to replace defective parts and to provide the necessary repair labor. During 2014, the company sold 300 tables at a unit price of $2,500. Sales occurred evenly throughout the year. The one-year warranty costs to repair defective tables are estimated to average $240 per unit. Approximately 10% of the tables sold are estimated to require warranty service. During 2014, the company's first year of operations, 11 units were submitted for warranty work at a total cost of $2,750.

Instructions

(a) Record the adjusting journal entry at the end of 2014 to accrue the estimated warranty costs on the 2014 sales.

(b) Prepare the entry to record repair costs incurred in 2014 to honor warranty contracts on 2014 sales.

(c) Explain how all of the relevant amounts would be reflected on the financial statements prepared at the end of 2014.

(d) Why are warranty costs accrued in the period of sale? Explain.

SOLUTION TO EXERCISE 11-6

| TIP: | The entry in part (b) is shown in summary form. Throughout the year, customers will bring in units for warranty service and an entry to record the performance of the warranty work will be recorded at that time. The entry in part (a) is made only once a period, in the adjusting process at the end of the period, so the entry(s) in (b) is actually recorded chronologically before the entry illustrated in (a). |

(c) Warranty expense of $7,200 is reported in the selling expense classification (which is part of operating expenses) in the income statement for the year ending December 31, 2014. The balance of $4,450 ($7,200 − $2,750) in the Warranty Liability account is to be classified as a current liability on the balance sheet at December 31, 2014.

(d) The accounting for warranty costs is based on the matching principle. To comply with this principle, the estimated cost of honoring product warranty contracts should be recognized as an expense in the period in which the sale occurs.

EXERCISE 11-7

Purpose: (L.O. 6, 7) This exercise will review the computations and journal entries relating to payroll accounting.

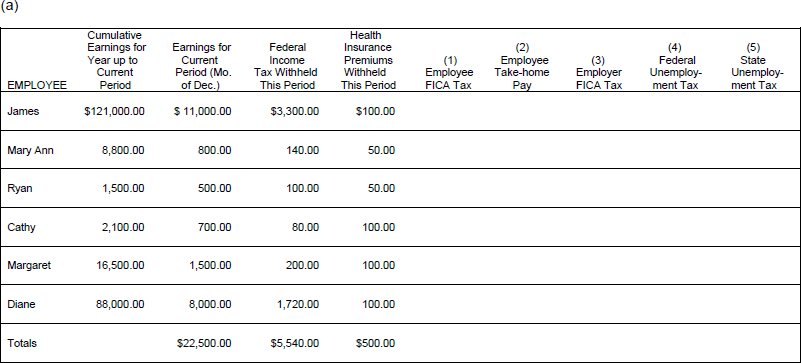

Hunt Enterprises has six salaried office employees who get paid on the last day of each month. Information about employee earnings for the current month (December 2014) and cumulative earnings for the first eleven months of 2014 appear on the next page. Data on federal income tax withholdings and health insurance withholdings is also provided.

The tax rates in effect are as follows:

FICA: 8% on gross earnings of up to $90,000

Federal unemployment taxes: 0.8% on gross earnings of up to $7,000

State unemployment taxes: 5.4% on gross earnings of up to $7,000

Instructions

(a) Compute the following items for December 2014 for each employee listed and fill in your answers on the schedule provided.

- Employee FICA tax.

- Employee's take-home pay.

- Employer FICA tax.

- Federal unemployment tax.

- State unemployment tax.

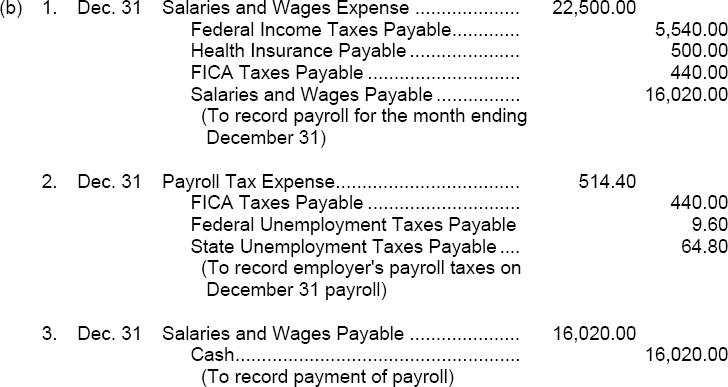

(b) Prepare the journal entries to record:

- The December 31, 2014 payroll.

- The payroll tax expense associated with the December 31, 2014 payroll.

- The payment of the December 31, 2014, payroll.

(c) Explain how the balances of the payable accounts will be reported on the financial statements.

| TIP: | Fixed amounts of compensation paid per week, month, or even per year, regardless of the number of hours worked during the designated period, are referred to as salaries. When an employee is paid a certain amount per hour, per day, or per unit, the compensation is referred to as wages. The wage rate multiplied by actual employee activity equals the amount of an employee's earnings for the period. |

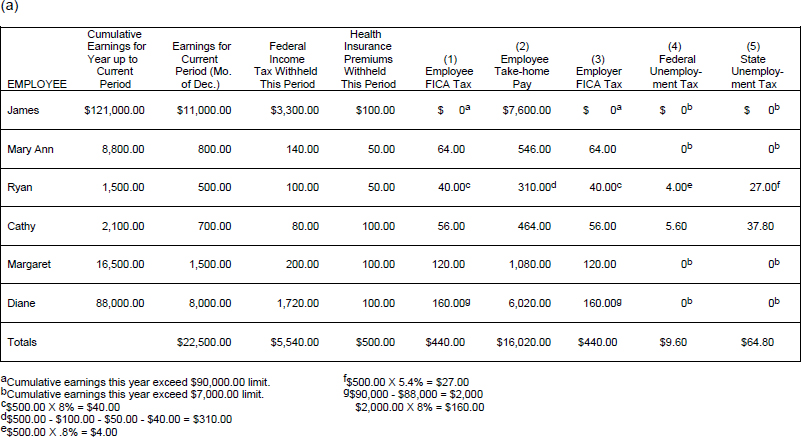

SOLUTION TO EXERCISE 11-7

(c) At December 31, 2014, the balances in Federal Income Taxes Payable, Health Insurance Payable, FICA Taxes Payable, Federal Unemployment Taxes Payable, and State Unemployment Taxes Payable will be classified in the current liability section of the balance sheet because they are all obligations that become due shortly after the balance sheet date and will require the use of current assets to liquidate them.

Explanation:

- An amount equal to 8% of an employee's gross earnings is withheld from the employee's paycheck and is remitted to the federal government for FICA taxes. This represents the employee's share of the FICA tax.

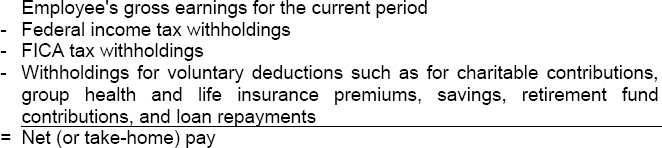

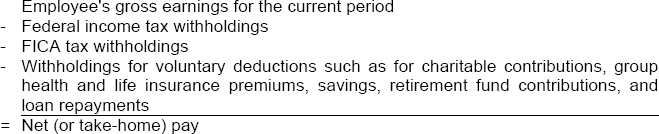

- An employee's net pay (or take-home pay) is calculated by the following:

- The employer must also bear a portion of the FICA tax. The FICA tax applies on earnings up to a certain level ($90,000 in this exercise). The employee, James, had surpassed this level prior to December so no FICA taxes are due on him for December. The employee Diane has only $2,000 ($90,000 − $88,000) of her December pay subject to the FICA tax because her December earnings put her cumulative earnings over the $90,000 threshold.

- The employer must bear the federal unemployment tax which is .8% on the employee's first $7,000 of gross earnings from that employer for the current year. Only Ryan and Cathy are still subject to that tax in this exercise.

- The employer must bear the state unemployment tax which is 5.4% on the employee's first $7,000 of gross earnings from that employer for the current year. Only the earnings of Ryan and Cathy are still subject to that tax in this exercise.

| TIP: | State income tax withholdings are treated in the same manner as the federal income tax withholdings. Voluntary deductions for union dues, charitable contributions, and the like are handled in the same manner as the health insurance premiums above. |

| TIP: | The tax rate and earnings base for the FICA tax that are used in this exercise do not represent what is currently in effect. The rate and base for this tax changes so frequently that an assumed rate and base are used here for simplicity. The same can be said for the tax rate and earnings base for the unemployment taxes. The Medicare portion of the FICA tax typically has a higher earnings base than the Social Security portion; that has been ignored in this exercise. |

EXERCISE 11-8

Purpose: (L.O. 1 thru 9) This exercise will quiz you about terminology used in this chapter.

A list of accounting terms with which you should be familiar appears below:

| Bonus | Payroll deductions |

| Contingent liability | Payroll register |

| Current ratio | *Pension plan |

| Employee earnings record | *Postretirement benefits |

| Federal unemployment taxes | Salaries |

| Fees | Statement of earnings |

| FICA taxes | State unemployment taxes |

| Full-disclosure principle | Wage and Tax Statement (Form W-2) |

| Gross earnings | Wages |

| Net pay | Working capital |

| Notes payable |

Instructions

For each item below, enter in the blank the term that is described.

- _____________________A potential liability that may become an actual liability in the future.

- _____________________Employee pay that is based on a fixed amount per month or per year rather than an hourly rate.

- _____________________Amounts paid to employees based on a rate per hour or on a piece-work basis.

- _____________________Compensation to management and other personnel based on factors such as increased sales or the amount of net income.

- _____________________Total compensation earned by an employee. Sometimes called gross pay.

- _____________________Deductions from gross earnings to determine the amount of a paycheck.

- _____________________A payroll record that accumulates the gross earnings, deductions, and net pay by employee for each pay period.

- _____________________Gross earnings less payroll deductions. Sometimes called take-home pay.

- _____________________Requires that companies disclose all circumstances and events that would make a difference to financial statement users.

- _____________________Taxes imposed on the employer by the federal government that provide benefits for a limited time period to employees who lose their jobs through no fault of their own; the taxing authority is the federal government.

- ___________________Taxes designed to provide workers with supplemental retirement, employment disability, and medical benefits.

- _____________________A cumulative record of each employee's gross earnings, deductions, and net pay during the year.

- _____________________Taxes imposed on the employer by states that provide benefits to employees who lose their jobs; the taxing authority is a state government.

- _____________________A form showing gross earnings, FICA taxes withheld, and income taxes withheld which is prepared annually by an employer for each employee.

- _____________________A document attached to a paycheck that indicates the employee's gross earnings, payroll deductions, and net pay.

- _____________________An agreement whereby an employer provides benefits to employees after they retire.

- _____________________Payments by an employer to retired employees for health care, life insurance, and pensions.

- _____________________A measure of a company's liquidity; computed as current assets minus current liabilities.

- _____________________A measure of a company's liquidity; computed by dividing current assets by current liabilities.

- _____________________Obligations in the form of written promissory notes.

- ______________________Payments made for the services of professionals.

SOLUTION TO EXERCISE 11-8

- Contingent liability

- Salaries

- Wages

- Bonus

- Gross earnings

- Payroll deductions

- Payroll register

- Net pay

- Full-disclosure principle

- Federal unemployment taxes

- FICA taxes

- Employee earnings record

- State unemployment taxes

- Wage and Tax Statement (Form W-2)

- Statement of earnings

- *Pension plan

- *Postretirement benefits

- Working capital

- Current ratio

- Notes payable

- Fees

ANALYSIS OF MULTIPLE-CHOICE TYPE QUESTIONS

- (L.O. 1) A current liability is an obligation that:

- was paid during the current period.

- will be reported as an expense within the year or operating cycle that follows the balance sheet date, whichever is longer.

- will be converted to a long-term liability within the next year.

- is expected to require the use of current assets or the creation of another current liability to liquidate it.

Approach and Explanation: Before you read the answer selections, write down the definition for current liability. Compare each answer selection with your definition. A current liability is an obligation which will come due within one year and whose liquidation is reasonably expected to require the use of existing resources properly classifiable as current assets or the creation of other current liabilities. (Solution = d.)

- (L.O. 1) Included in Jurassick Company's liability accounts at December 31, 2014, was the following:

12% note payable issued in 2011 for cash and due in May 2015 $200,000 Sales taxes payable 16,000 Interest payable 11,000 Federal income tax withholdings 6,000 How much of the above should be included in the current liability section of Jurassick's balance sheet at December 31, 2014?

- $27,000.

- $33,000.

- $227,000.

- $233,000.

Explanation: All of the obligations will become due within a year of the balance sheet date and will require the use of current assets to liquidate them ($200,000 + $16,000 + $11,000 + $6,000 = $233,000). (Solution = d.)

- (L.O. 1) John Craig Clothiers has an obligation coming due on July 1, 2015, which will be settled by transferring assets which are properly classified as a long-term investment. The obligation should be classified on the company's December 31, 2014 balance sheet as:

- a current liability.

- a long-term liability.

- a contra current liability item.

- a contra current asset item.

Approach and Explanation: Write down the definition of current liability and determine if the obligation described meets the criteria contained in that definition. A current liability is an obligation which will come due within a year of the balance sheet date and is expected to require the use of assets properly classifiable as current assets or the creation of other current liabilities to liquidate it. The obligation described in the question is coming due within a year of the balance sheet date, but a noncurrent asset will be used to settle the debt; thus the obligation is properly classifiable as a long-term liability. (Solution = b.)

- (L.O. 1, 3) Which of the following should be reported as a current liability at December 31, 2014?

- Revenue received in advance to be earned in 2015.

- Installment loan payments due after December 31, 2015.

- Pension obligations estimated to mature in ten years.

- Note payable due in 2016.

Approach and Explanation: Define current liability. A current liability is an obligation that comes due within one year of the balance sheet date (and thus will be paid within one year) and is expected to require the use of current assets or the incurrence of another current liability to liquidate it. Analyze each answer selection to see if it meets the definition. Revenue received in advance represents an obligation to perform services or to deliver goods or to provide a refund to the customer. If the revenue will be earned in the period that immediately follows the balance sheet date, it is a current liability; if it will be earned beyond that one year mark, it is to be classified as a long-term liability. Selections “b”, “c”, and “d”, are all incorrect because they do not meet the definition. (Solution = a.)

- (L.O. 2) Which of the following is true regarding a situation where the accounting period ends on a date that does not coincide with an interest payment date for a note payable that is outstanding?

- No adjusting entry is required. The interest expense will be recorded in the period it is paid.

- An adjusting entry is required and it contains a debit to Interest Expense and a credit to Interest Payable.

- An adjusting entry is required and it contains a debit to Note Payable and a credit to Interest Expense.

- An adjusting entry is required and it contains a debit to Income Summary and a credit to Interest Expense.

Explanation: An adjusting entry is required to properly match the interest expense with the time period for which the interest was incurred. Interest is payment for use of someone else's money. The cost of that use should be matched with the period to which the interest pertains. (Solution = b.)

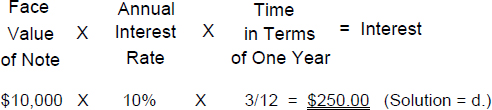

- (L.O. 2) A note payable dated October 1, 2014 has a face value of $10,000, an interest rate stipulated at 10%, and a maturity date of April 1, 2015. Interest expense (pertaining to this note) to appear on the income statement for the year ending December 31, 2014 amounts to:

- $0.

- $125.00.

- $166.67.

- $250.00.

Approach and Explanation: Write down the formula for computing interest. Plug in the amounts given and solve.

- (L.O. 3) McGuire Company sells a product on credit for $200. The sale is subject to a 5% state sales tax which is not included in the $200. The entry to record the sale would include a:

- debit to Accounts Receivable for $200.

- credit to Sales for $210.

- credit to Sales Taxes Payable for $10.

- debit to Sales Taxes for $10.

Approach and Explanation: Before looking at the alternative answers, prepare the journal entry on paper (or mentally). Then find the solution that agrees with your entry. The entry is:

The sales tax is levied by the state government. The company making the sale acts as an agent for the state government as it collects the tax and remits it to the taxing authority. (Solution = c.)

- (L.O. 4) The current ratio is calculated by dividing:

- current assets by total liabilities.

- current assets by current liabilities.

- quick assets by current liabilities.

- total assets by total liabilities.

Approach and Explanation: Write down the formula for the current ratio before you read the answer selections. Choose the answer that matches the formula.

- (L.O. 4) Which of the following items would not be used in calculating the current ratio?

- Accounts payable.

- Inventory.

- Accounts receivable.

- Furniture purchased during the current period.

Approach and Explanation: Think about the current ratio and write down the formula to compute it. Then read the answer selections and determine which selection does not fit into the formula. The current ratio is determined by dividing total current assets by total current liabilities at a point in time. Answer selection “d” would be classified under the property, plant, and equipment classification and would therefore not be included in the calculation of the working capital ratio. (Solution = d.)

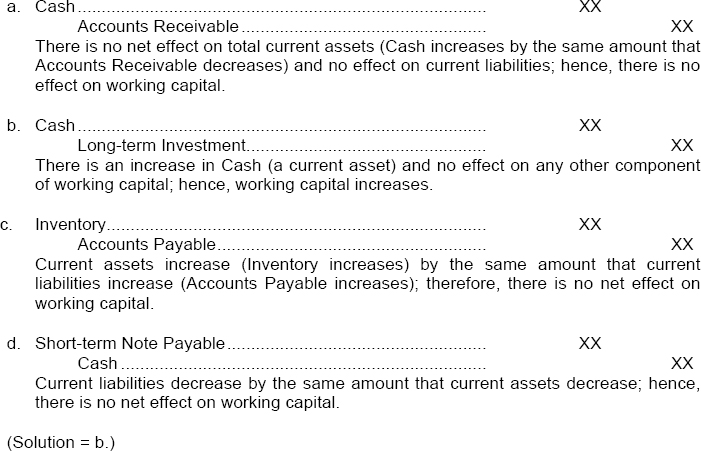

- (L.O. 4) Which of the following will increase the amount of working capital?

- Collection of accounts receivable.

- Sale of a long-term investment at book value.

- Purchase of inventory on account.

- Payment of a short-term note payable.

Approach: Write down the formula for determining working capital. Write down the journal entry for each transaction mentioned. Analyze the accounts in each entry to determine the effect on the elements of the working capital computation.

Working Capital = Current Assets − Current Liabilities

- (L.O. 5) A company has a contingency. If it is probable that an actual liability exists at the balance sheet date, but the amount is not reasonably estimable, the contingent liability should be:

- ignored and not disclosed.

- reported on the face of the balance sheet without an amount.

- disclosed only in the notes accompanying the financial statements.

- reported only in the following period.

Approach and Explanation: Briefly review in your mind the guidelines for reporting contingent liabilities:

If it is probable that a loss will occur and the amount is estimable, accrue the loss and report the liability on the face of the balance sheet.

If it is only reasonably possible a loss will occur, or if it is probable but not estimable, disclose only in the notes.

If the loss is remotely possible, it need not be disclosed or accrued.

(Solution = c.)

TIP: In the context of accounting for contingencies, probable means “likely;” remotely possible means “not likely”; reasonably possible means “less than likely and more than remote.” - (L.O. 5) An example of a contingent liability is:

- Sales taxes payable.

- Accrued salaries.

- Property taxes payable.

- A pending lawsuit.

Approach and Explanation: Mentally define contingent liability and think of examples before you read the alternative answer selections. A contingent liability is a situation involving uncertainty as to possible loss or expense that will ultimately be resolved when one or more future events occur or fail to occur. Examples are pending or threatened lawsuits, pending IRS audits, and product warranties. Accrued salaries result in an actual liability. Sales taxes payable and property taxes payable are both actual liabilities if they exist at a balance sheet date. (Solution = d.)

- (L.O. 5) Warranty costs are accrued in the period of sale to comply with the:

- expense recognition principle.

- revenue recognition principle.

- cost principle.

- concept of conservatism.

Explanation: Revenues are recognized in the period they are earned to comply with the revenue recognition principle. Then the expense recognition principle dictates that all costs incurred in generating the revenue recognized should be reported in the same time period as the revenue. Therefore, warranty costs are to be matched with the revenue from the sale of the product under warranty. (Solution = a.)

- (L.O. 5) A contingent loss which is judged to be reasonably possible and estimable should be:

Explanation: A contingent loss that is probable and estimable is to be accrued. A contingent loss that is reasonably possible should be disclosed, but it should not be accrued. A contingent loss that is remotely possible can be ignored. (Solution = c.)

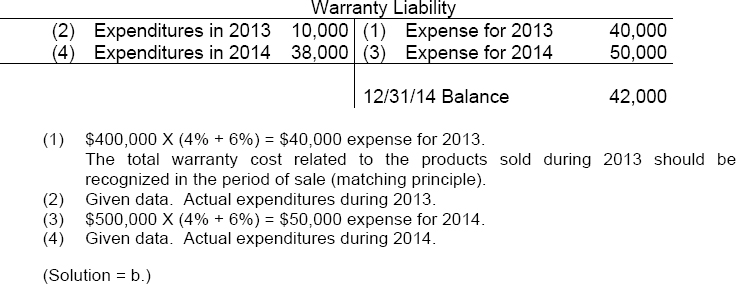

- (L.O. 5) D. Scott Corporation provides a two-year warranty with the sale of its product. Scott estimates that warranty costs will equal 4% of the selling price the first year after sale and 6% of the selling price the second year after the sale. The following data are available:

The balance of the warranty liability at December 31, 2014 should be:

- $12,000.

- $42.000.

- $44,000.

- $50,000.

Approach and Explanation: Draw a T-account for the liability and enter the amounts that would be reflected in the account and determine its balance.

TIP: Because some items are sold near the end of the year and the warranty is for two years, a portion of the warranty liability should be classified as a current liability (the amount pertaining to the actual expenditures estimated to occur in 2015) and the remainder as a long-term liability. - (L.O. 6) An employee's net pay is determined by gross earnings minus amounts for income tax withholdings,

- employee's portion of FICA taxes, and unemployment taxes.

- employee's and employer's portion of FICA taxes, and unemployment taxes.

- employee's portion of FICA taxes, unemployment taxes, and any voluntary deductions.

- employee's portion of FICA taxes, and any voluntary deductions.

Approach and Explanation: Before you read the answer selections, write down the model for the net pay (take-home pay) computation. Then find the answer selection that agrees with your model.

(Solution = d.)

- (L.O. 7) Which group of items would be recorded in the Payroll Tax Expense account?

- Employer's share of FICA taxes, federal unemployment tax, state unemployment tax.

- Federal and state income tax withholdings, all FICA taxes, federal unemployment tax, state unemployment tax.

- Federal and state income tax withholdings, employer's share of FICA taxes, federal and state unemployment taxes, union dues.

- Employer's share of FICA, federal and state unemployment taxes, union dues, insurance premiums, contributions to charitable organizations.

Approach and Explanation: Think of the payroll taxes the employer must bear; they are the ones recorded in the Payroll Tax Expense account. Payroll taxes borne by the employer include the employer's share of FICA tax and all unemployment taxes (both federal and state). Taxes withheld from an employee's payroll check (employee's share of FICA and income tax withholdings) represent a portion of the employee's total earnings (gross pay); therefore, they are in effect charged (debited) to a wages and salaries expense account. (Solution = a.)

- (L.O. 7) Which group of items represents a cost burden for the employer rather than the employee?

- Federal income tax withholdings, employer's portion of FICA tax, state unemployment tax.

- Employer's portion of FICA tax, state unemployment tax, federal unemployment tax.

- Employer's and employee's portions of FICA tax, federal unemployment tax, state unemployment tax.

- Federal income tax withholdings, state income tax withholdings, employer's share of FICA taxes, federal unemployment tax, state unemployment tax.

Explanation: The items to be borne by the employer include the employer's share of FICA tax and all unemployment taxes (both state and federal). Items which must be borne by an employee include the employee's share of FICA tax, federal income tax withholdings, state income tax withholdings, city income tax withholdings, and voluntary deductions. (Solution = b.)

- (L.O. 6) Deductions from an employee's earnings may include:

- withholdings for federal and state income tax.

- FICA tax.

- union dues.

- amounts for purchase of savings bonds for employee.

- all of the above.

Explanation: See Explanation to Question 18 above. (Solution = e.)

- *(L.O. 9) A 401(k) plan is often referred to as a:

- defined-contribution plan.

- defined-benefit plan.

- post-retirement care plan.

- post-retirement living plan.

Explanation: A 401(k) plan is often referred to as a defined-contribution type pension plan. In a defined-contribution plan, the plan defines the contribution that an employer will make but not the benefit that the employee will receive at retirement. The other type of pension plan is a defined-benefit plan in which the employer agrees to pay a defined amount to retirees, based on employees meeting certain eligibility standards. (Solution = a.)