CHAPTER 7

![]()

ACCOUNTING INFORMATION SYSTEMS

OVERVIEW

As transactions increase in number, so do the recordings and postings required to account for business activities. To deal with transactions the accountant employs (1) special journals to efficiently organize and expedite the recording and posting process for transactions which occur frequently and (2) subsidiary ledgers to free the general ledger of details. A business may have a computerized accounting system or it may rely on a manual system. The steps in the accounting cycle remain the same whether or not the system is automated.

SUMMARY OF LEARNING OBJECTIVES

- Identify the basic concepts of an accounting information system. The basic principles in developing an accounting information system are cost effectiveness, useful output, and flexibility. Most companies use a computerized accounting system. Smaller companies use entry-level software such as QuickBooks or Sage50. Larger companies use custom-made software packages which often integrate all aspects of the organization.

- Describe the nature and purpose of a subsidiary ledger. A subsidiary ledger is a group of accounts with a common characteristic. It facilitates the recording process by freeing the general ledger from details of individual balances.

- Explain how companies use special journals in journalizing. Companies use special journals to group similar types of transactions. In a special journal, generally only one line is used to record a complete transaction.

TIPS ON CHAPTER TOPICS

| TIP: | It is sometimes confusing for a beginning accounting student to differentiate between subsidiary ledgers and special journals. It may help to think about how special journals are used to record similar transactions in a common place (such as all sales on account are recorded in the sales journal); thus, special journals are used in the recording process. All transactions affect accounts. Subsidiary ledgers are used to group similar accounts in a common place (such as an account receivable for each customer is included in the accounts receivable ledger); thus, subsidiary ledgers are used in the posting process. |

| TIP: | The cash payments journal is often called the cash disbursements journal. |

EXERCISE 7-1

Purpose: (L.O. 2) This exercise will test your understanding of the postings that appear in a subsidiary ledger.

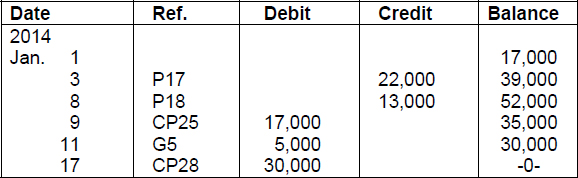

Presented below is the account for the vendor, Kitchen Plastics Company, as it appears in the accounts payable subsidiary ledger of Great Value Hardware.

KITCHEN PLASTICS COMPANY

Instructions

Explain each amount reflected in this subsidiary account.

SOLUTION TO EXERCISE 7-1

| Jan. | 1 | The account started the period with a beginning balance of $17,000. This balance was the result of unpaid purchases from the prior period. |

| Jan. | 3 | A posting of $22,000 from page 17 of the purchases journal (P17) indicates that purchases of $22,000 were made on credit. |

| Jan. | 8 | A posting of $13,000 from page 18 of the purchases journal (P18) indicates that purchases of $13,000 were made on credit. |

| Jan. | 9 | A posting of $17,000 from page 25 of the cash payments journal (CP25) indicates that a cash payment of $17,000 was made to Kitchen Plastics on account. |

| Jan. | 11 | A debit posting of $5,000 from page 5 of the general journal (G5) probably stems from a purchase return or allowance. |

| Jan. | 17 | A posting of $30,000 from page 28 of the cash payments journal (CP28) indicates that a cash payment of $30,000 was made to the vendor on account. |

| TIP: | Think about the normal balance of an account payable—credit balance. Think about common reasons for increases (credits) and for decreases (debits). Identify the source of each posting by the abbreviation in the Ref. column. The transactions being posted should then be fairly evident. |

| TIP: | In addition to having subsidiary ledgers for accounts receivable and accounts payable, it is not uncommon for a business to also use control accounts and subsidiary ledgers for other accounts such as inventory (when a perpetual system is used), equipment, and selling and administrative expenses. |

EXERCISE 7-2

Purpose: (L.O. 3) This exercise will help you identify the journal in which to record specific transactions.

A list of abbreviations and a list of transactions (in random order) follow:

Instructions

For each transaction, indicate the journal in which it would be recorded.

Transactions

SOLUTION TO EXERCISE 7-2

- CR

- CP

- GJ

- CR

- CP

- GJ

- CP

- CP

- GJ

- S

- P

- CP

- GJ

- CP

- GJ

- GJ

- GJ

- GJ

- GJ

- CP

- CP

- CP

- GJ

- CP

- GJ

- GJ

- CP

- CP

- CP

- CR

- CP

- CR

- S

- P

- CR

- CR

Approach and Explanation: Keep in mind that a special journal is used to record similar types of transactions, such as all sales of merchandise or all cash receipts. Write down a brief description of the types of transactions to be recorded in each of the journals used in this exercise. They are:

Sales journal—all sales of merchandise on account.

Cash receipts journal—all receipts of cash (including cash sales).

Purchases journal—all purchases of merchandise on account.

Cash payments (disbursements) journal—all payments of cash (including cash purchases).

General journal—all transactions that do not appropriately fit in a special journal (including adjustments and closing entries).

Identify the transactions that involve sales of merchandise on credit (items 10 and 33). They go in the sales journal. Identify the transactions that involve purchases of merchandise on account (items 11 and 34). They go in the purchases journal. Identify the transactions that involve the receipt of cash (items 1, 4, 30, 32, 35, and 36). They are to be recorded in the cash receipts journal.

Identify the transactions that involve a cash payment (items 2, 5, 7, 8, 12, 14, 20, 21, 22, 24, 27, 28, 29, and 31). They go in the cash payments journal. Identify the transactions that do not fit those first four categories (items 3, 6, 9, 13, 15, 16, 17, 18, 19, 23, 25, and 26). They go in the general journal. (Notice that items 3, 16, 18, 19 and 23 are adjusting entries and item 25 involves closing entries.)

EXERCISE 7-3

Purpose: (L.O. 3) This exercise reviews general ledger accounts and postings to them from special journals.

A list of abbreviations and a list of postings to general ledger accounts (in random order) follow:

Instructions

For each of the postings to the general ledger accounts listed below, indicate the most common source of the posting. Use the appropriate abbreviations to indicate your answer for each. (Assume all purchases of inventory and sales are made on account.)

Postings to General Ledger Accounts

SOLUTION TO EXERCISE 7-3

*The answer depends on whether the entity makes most purchases of supplies for cash (entered in the cash payments journal) or on credit (entered in the general journal). Some companies expand their purchases journal to provide columns to record credit purchases of items other than merchandise inventory.

**The answer depends on whether the entity makes most sales on credit (entered in the sales journal) or for cash (entered in the cash receipts journal).

Approach and Explanation: Briefly describe the columns typically found in each of the special journals listed. Match them up with the postings in this exercise. The remainder of the postings have to come from the general journal (items 9, 12, 14, 16, 19, and 20).

| TIP: | Keep in mind that posting to a given account describes one-half of the dual effect of one transaction. For example, a posting “Debits to Advertising Expense” describes an increase in advertising expense. The most common transaction increasing advertising expense is the payment for advertising services. All cash payments are recorded in the cash payments journal. Therefore, the most common source of the posting of debits to the Advertising Expense account is the cash payments journal. For a second example, a posting “Credits to Interest Revenue” describes an increase in interest revenue. Although the Interest Revenue account can be increased at the end of a period because of an adjusting entry in the general journal to record accrued interest (revenue that has been earned but not received), the most common reason for having an increase in Interest Revenue is the collection of interest during a period. All cash collections are recorded in the cash receipts journal. |

| TIP: | Remember that all transactions involving a receipt of cash go in the cash receipts journal, and all transactions involving a payment of cash go in the cash payments journal. |

EXERCISE 7-4

Purpose: (L.O. 2, 3) This exercise will discuss why a business employs special journals and subsidiary ledgers.

Up until this point, we have assumed that all transactions are recorded in the general journal and posted to the general ledger. In this chapter, we find that even small businesses can expedite the recording process by the use of special journals and subsidiary ledgers.

Instructions

(a) Explain the advantages of using special journals.

(b) Explain the advantages of using subsidiary ledgers.

SOLUTION TO EXERCISE 7-4

(a) The main advantages of using special journals are that they:

(1) Permit greater division of labor by allowing several individuals to record entries in different journals at the same time. For example, one employee may be responsible for journalizing all cash receipts, and another for journalizing all credit sales.

(2) Reduce the time necessary to record and post transactions by eliminating the need to repeatedly write out account titles in the general journal and by dramatically cutting down on the number of postings required to the general ledger. Monthly postings to some accounts may be substituted for daily postings.

(b) The advantages of using subsidiary ledgers are that they:

(1) Show transactions affecting one customer or one creditor in a single account, thus providing necessary up-to-date information on specific account balances.

(2) Free the general ledger of excessive details. As a result, a trial balance of the general ledger does not contain a vast number of individual account balances.

(3) Help locate errors in individual accounts by reducing the number of accounts combined in one ledger and by using controlling accounts.

(4) Make possible a division of labor in posting by having one employee post to the general ledger and a different employee(s) post to the subsidiary ledgers.

| TIP: | A company may employ any number of special journals. A special journal can be designed to record any type of transaction that occurs frequently. The four special journals typically found in a merchandising entity are discussed in this chapter: sales journal, cash receipts journal, single-column purchases journal, and the cash payments journal. If a company finds it frequently has a transaction that is not recorded in one of these journals, it can design another special journal. For example, frequent sales returns for credit against the customers' account receivable balances would indicate the usefulness of designing a sales returns journal. Amounts in the one column would get posted as debits to Sales Returns and credits to Accounts Receivable and amounts in a second column would get posted as debits to Merchandise Inventory and credits to Cost of Goods Sold. Each return would also be individually posted to the customer's account in the accounts receivable subsidiary ledger and to the appropriate perpetual inventory records. |

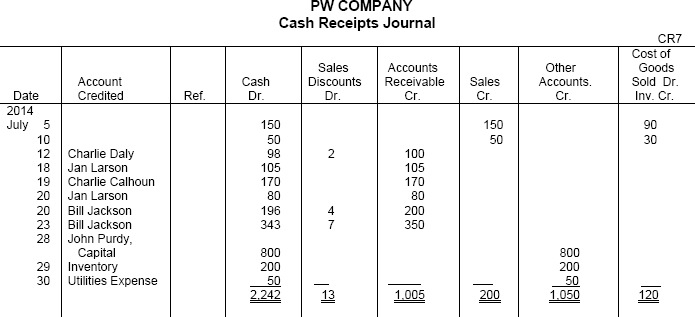

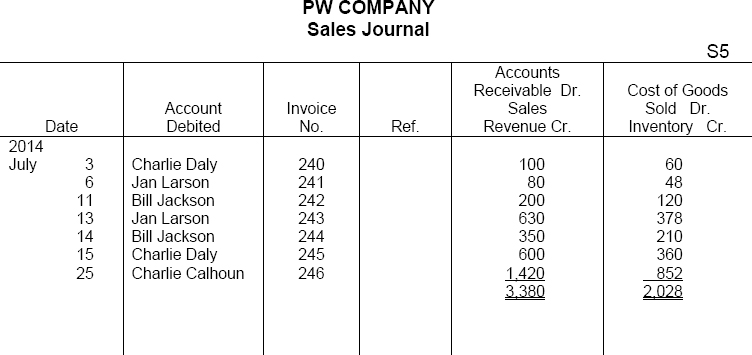

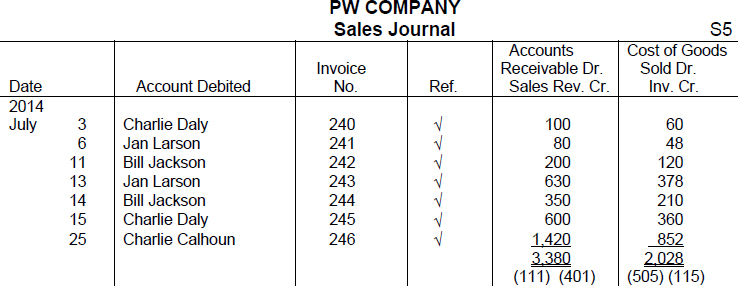

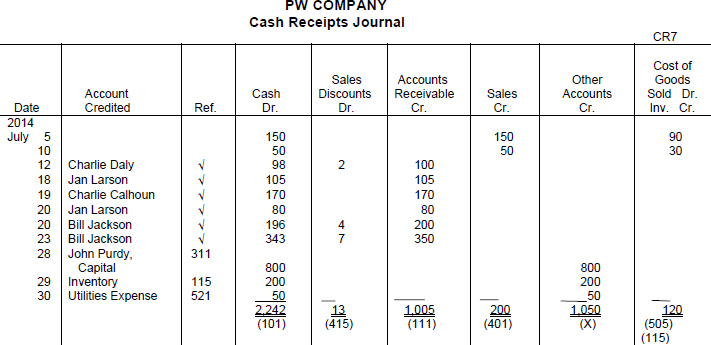

EXERCISE 7-5

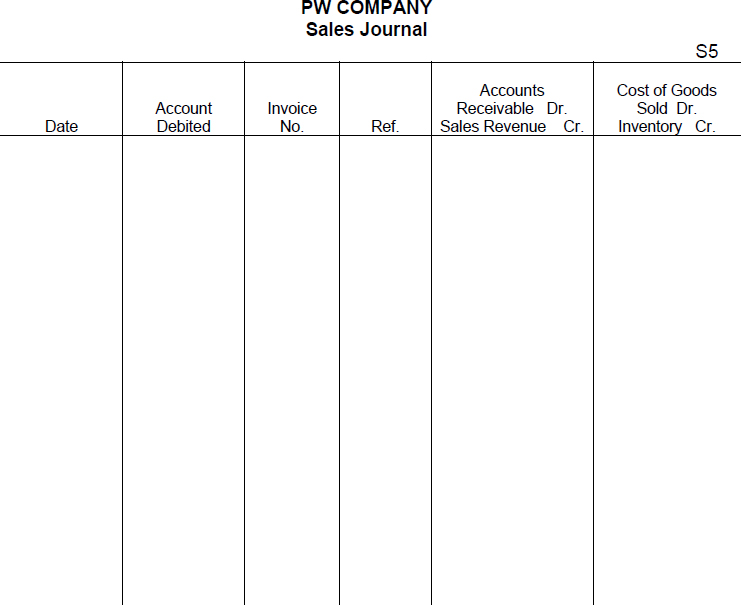

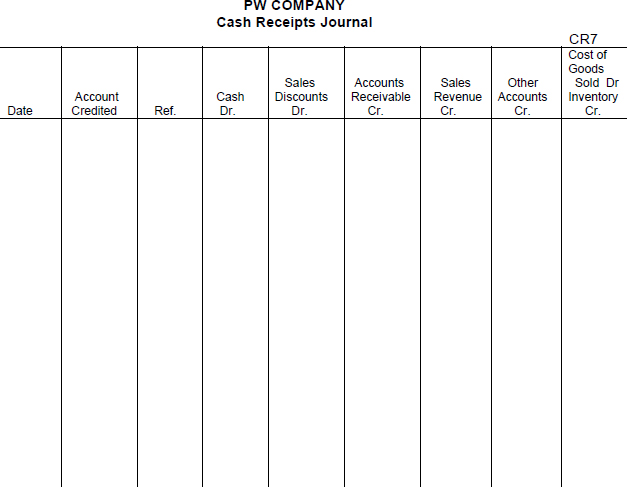

Purpose: (L.O. 3) This exercise will allow you to practice recording transactions in the sales journal and the cash receipts journal.

PW Company's chart of accounts includes the following selected accounts:

| 101 | Cash |

| 111 | Accounts Receivable |

| 115 | Inventory |

| 211 | Accounts Payable |

| 311 | Owner's Capital |

| 401 | Sales Revenue |

| 415 | Sales Discounts |

| 416 | Sales Returns & Allowances |

| 505 | Cost of Goods Sold |

| 521 | Utilities Expense |

PW Company has four customers. The following balances appeared in PW Company's accounts receivable subsidiary ledger at July 1, 2014:

A list of selected transactions for July 2014 for PW Company follows. The sales journal and the cash receipts journal follow that list.

Transactions

Instructions

(a) Journalize the transactions above in the sales journal and the cash receipts journal.

(b) Foot and crossfoot the two journals at July 31, 2014.

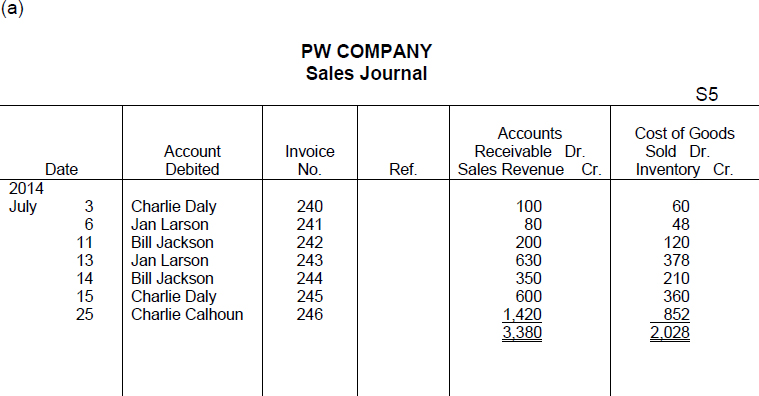

SOLUTION TO EXERCISE 7-5

(b) To foot a journal means to sum each column in the journal. Thus, adding the amounts in the columns in the sales journal constitutes footing the journal. There are six individual columns of figures to be added to foot the cash receipts journal. To crossfoot a journal means to prove the equality of the debits and credits recorded therein. Because the columns in the sales journal are posted both as debits and credits, there is nothing to crossfoot. In the cash receipts journal, the totals of the debit columns are added together ($2,242 + $13 + $120 = $2,375) and are compared to the sum of the totals of the credit columns ($1,005 + $200 + $1,050 + $120 = $2,375). Because the two grand totals equal, the journal is said to crossfoot.

EXERCISE 7-6

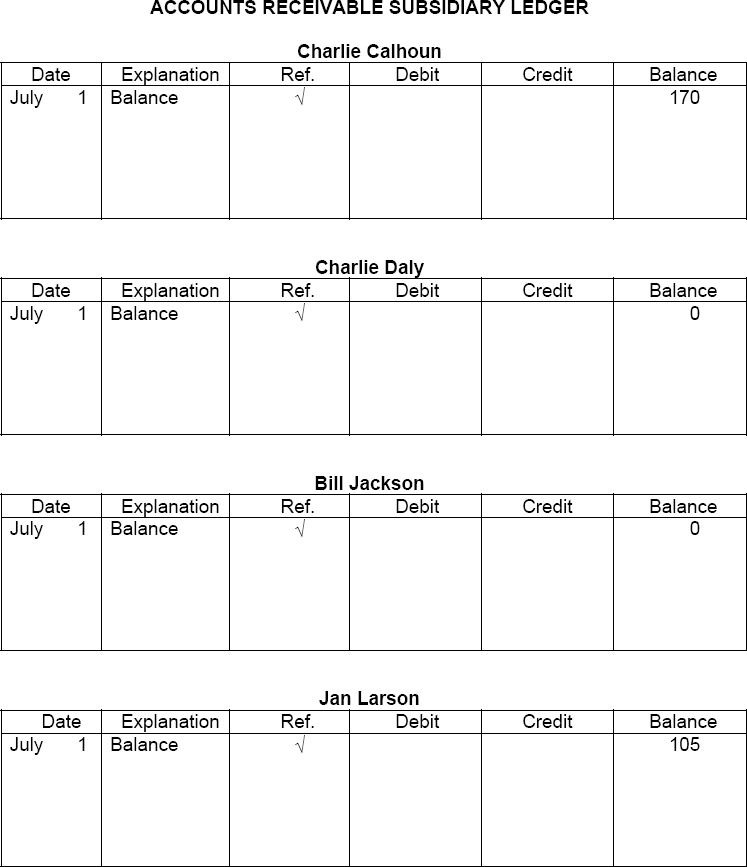

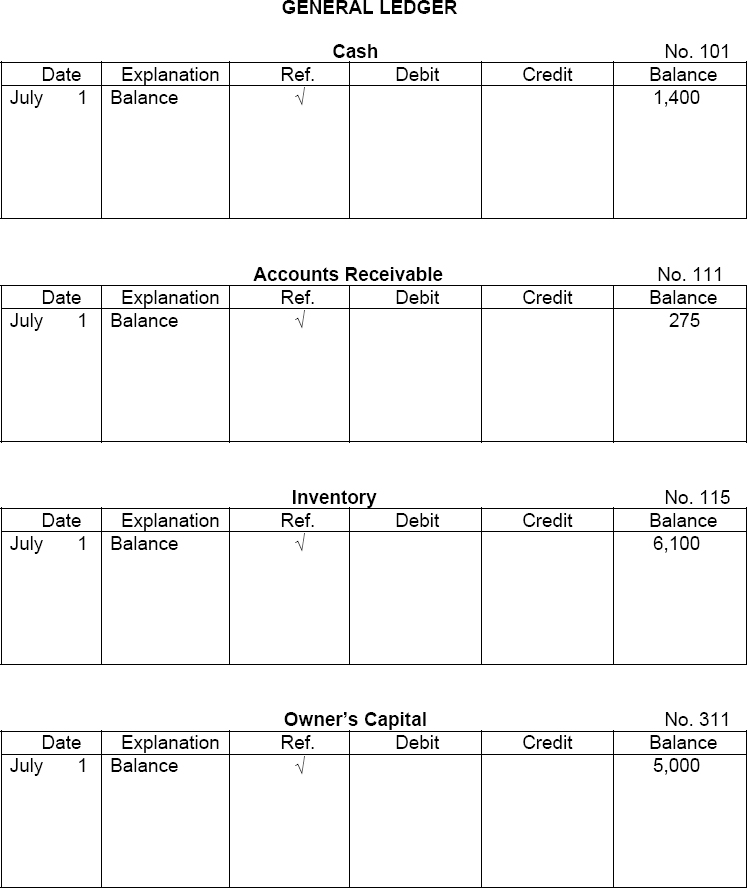

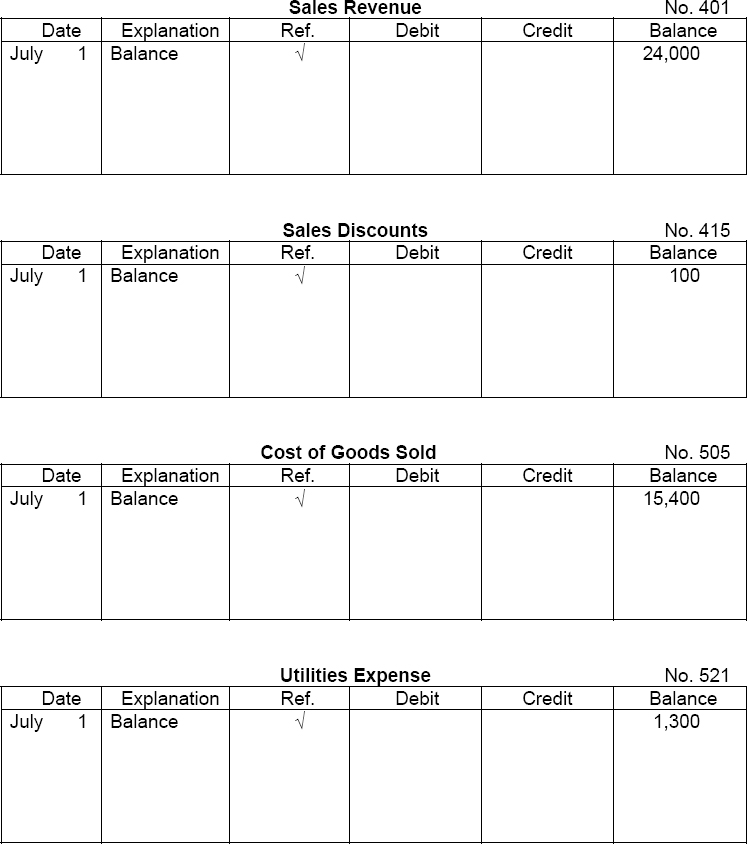

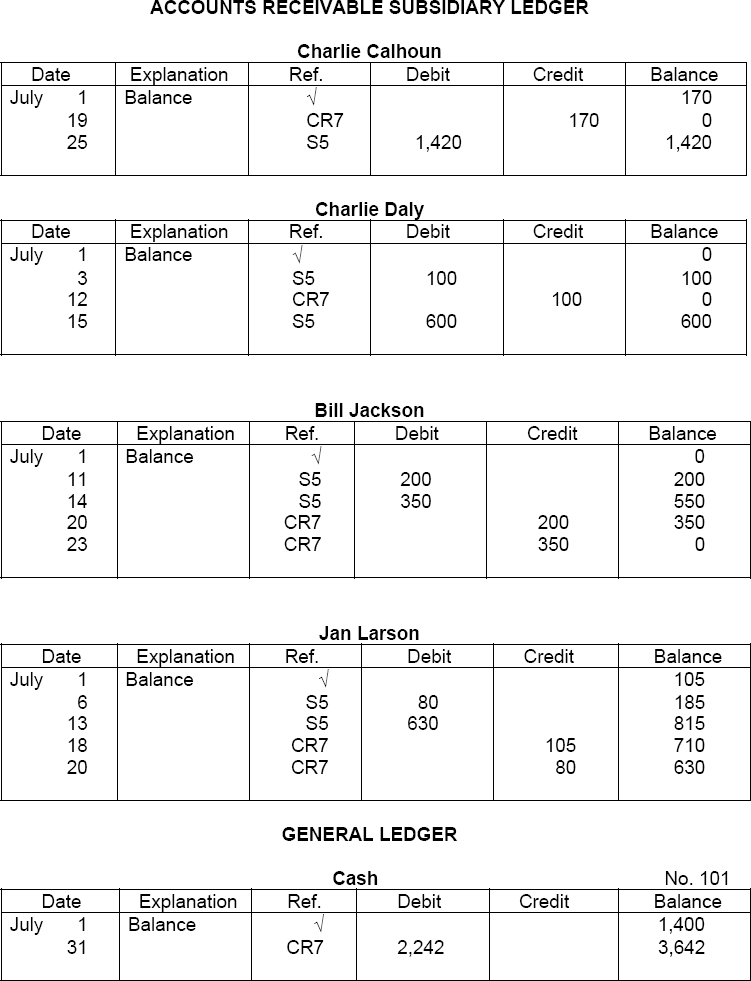

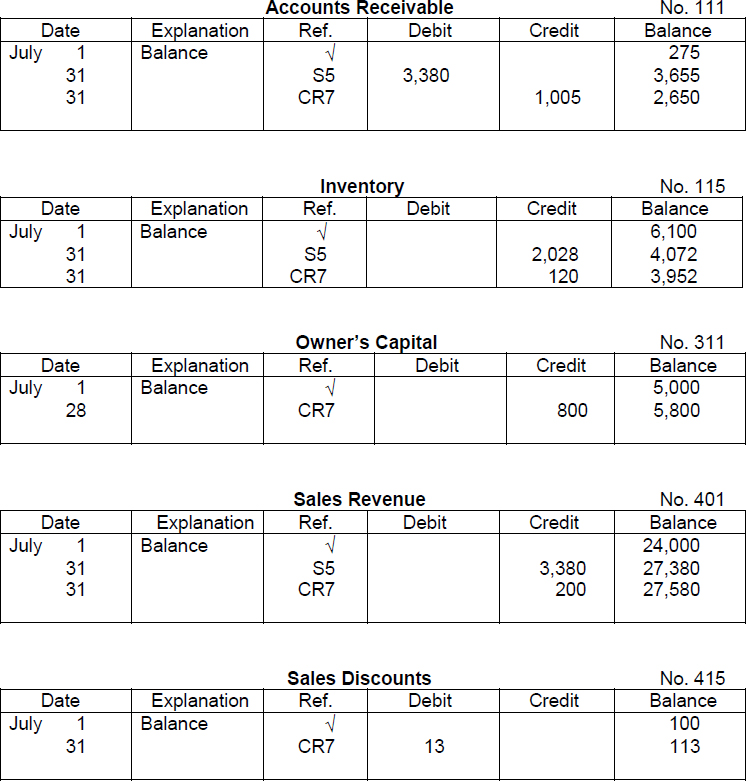

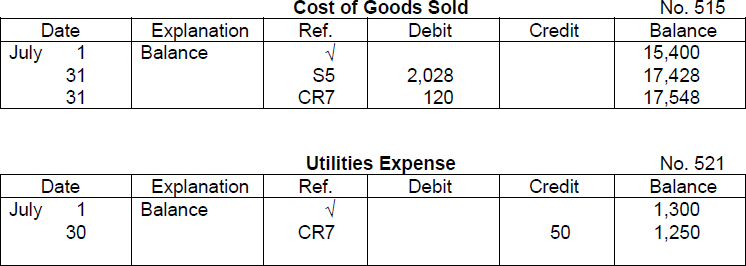

Purpose: (L.O. 2, 3) This exercise illustrates the relationship of the accounts receivable subsidiary ledger to the Accounts Receivable control account in the general ledger.

PW Company has four customer accounts in its accounts receivable ledger. The following balances appeared in that subsidiary ledger at July 1, 2014:

The cash receipts journal and the sales journal for July are reproduced below (from the Solution to Exercise 7-5).

The accounts receivable subsidiary ledger and selected accounts from the general ledger appear below. Some accounts have a balance at July 1, 2014 as shown.

(a) Post the transactions to both the general ledger and the subsidiary ledger accounts. (Show the appropriate cross references in both the journals and the ledgers.)

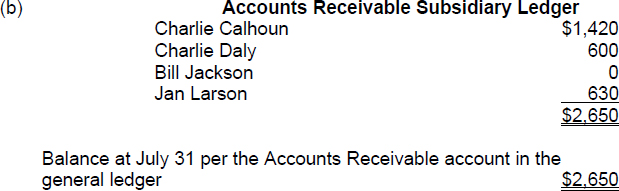

(b) Prove the agreement of the subsidiary ledger and its control account.

(c) Explain how an accountant unfamiliar with a company could examine your work and determine the following:

- What accounts are to receive postings from the sales journal?

- Have the postings been completed to the general ledger accounts?

- Have the postings been completed to the subsidiary ledger accounts?

- What was the source of the $50 credit to the Utilities Expense account on July 30?

| TIP: | If you wish to more closely simulate a real life situation, you will post the transactions in chronological order. If you post all of the transactions in the sales journal before you post the transactions in the cash receipts journal, you should end up with the correct ending balances, but your postings will appear in an order different than the order shown in the solution presented below. |

| TIP: | All credit sales are recorded in the sales journal, and all cash sales are recorded in the cash receipts journal so all sales transactions for July have been entered in the appropriate journals. However, a number of other transactions are not reflected because they appear in the purchases journal, the cash payments journal, and the general journal and are, therefore, not included in this exercise. |

SOLUTION TO EXERCISE 7-6

| TIP: | Practically all states, and cities require a sales tax be charged on items sold, which the company must remit to the state or city. In this case, it is desirable to add an additional credit column to the sales journal for sales tax payable. Sales tax payable is posted in total at the end of the month, similar to sales. Accounting for sales taxes is not illustrated in this exercise. |

| TIP: | The accounts listed above all have a single balance column. Therefore, the balance is assumed to be a normal balance for that type of account (debit versus credit) unless the balance is in brackets ( ) or is circled or is printed in red ink, in which case the balance is an abnormal one. |

| TIP: | Total debits do not equal total credits in the general ledger accounts shown because only selected accounts are being illustrated in this exercise. |

| TIP: | Examine the “Account Credited” column of the cash receipts journal. Notice that a subsidiary ledger account title is entered in that column whenever the entry involves an account receivable. Whereas, a general ledger account title is entered in that column whenever the entry involves an account that is not the subject of a special column (and an amount is entered in the “Other Accounts” column). No account title is entered in the “Account Credited” column if neither of the foregoing apply. |

| TIP: | In this exercise, the balance of the Inventory account continues to decrease throughout the entire month because there was no information about inventory acquisitions during the month. Typically, purchases are made regularly in order to keep a sufficient inventory level to accommodate customers. |

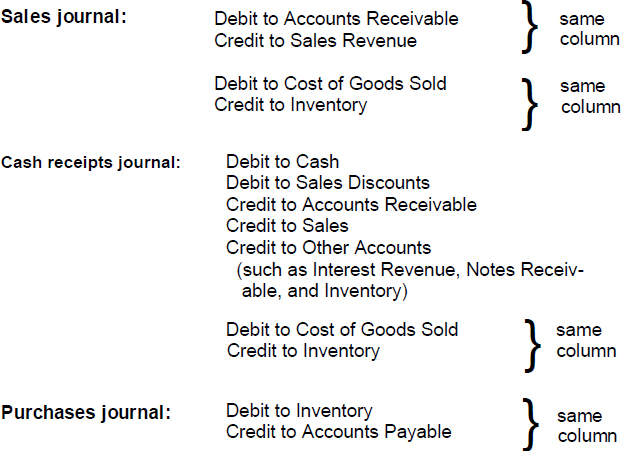

(c) 1. The accounts to receive postings from the sales journal can be determined by reading the two money column headings in that journal: (1) Accounts Receivable Dr. and Sales Revenue Cr., and (2) Cost of Goods Sold Dr. and Inventory Cr.

2. An independent reviewer can readily see that the postings have been completed to the general ledger accounts because the relevant general ledger account numbers appear in parentheses below the totals of the money columns in the special journals. For example, the account numbers 111 (Accounts Receivable) and 401 (Sales Revenue) appear below the total of the first money column in the sales journal because that total was posted to both the Accounts Receivable account and the Sales Revenue account in the general ledger. The account numbers 505 (Cost of Goods Sold) and 115 (Inventory) appear below the second money column in the sales journal. The account number 101 (Cash) appears below the “Cash” column of the cash receipts journal, and so forth.

The transactions recorded in the cash receipts journal which affect accounts other than the accounts for which there are special money columns have been posted to those other accounts as can be determined by the relevant account numbers appearing in the Ref. column (311 for Owner's Capital, 115 for Inventory, and 521 for Utilities Expense).

3. The completion of a posting to a subsidiary account is indicated by a “![]() ” in the Ref. column of a special journal. All postings have been completed from the sales journal because there is a

” in the Ref. column of a special journal. All postings have been completed from the sales journal because there is a ![]() in the Ref. column on every used line. All postings have been completed from the cash receipts journal because a “

in the Ref. column on every used line. All postings have been completed from the cash receipts journal because a “![]() ” appears in the Ref. column on every line that contains a subsidiary ledger account title in the Account Credited column.

” appears in the Ref. column on every line that contains a subsidiary ledger account title in the Account Credited column.

4. The source of the $50 credit to the Utilities Expense account on July 30 can be determined by looking in the Ref. column in the general ledger account for Utilities Expense. The posting for $50 on July 30 came from CR7 which stands for page 7 of the cash receipts journal.

EXERCISE 7-7

Purpose: (L.O. 3) This exercise will allow you to practice recording transactions in the purchases journal and the cash payments journal.

E & Y Company's chart of accounts includes the following selected accounts:

| 101 | Cash |

| 111 | Accounts Receivable |

| 115 | Inventory |

| 131 | Prepaid Insurance |

| 140 | Supplies |

| 150 | Equipment |

| 211 | Accounts Payable |

| 311 | Owner's Capital |

| 401 | Sales Revenue |

| 415 | Sales Discounts |

| 416 | Sales Returns |

| 505 | Cost of Goods Sold |

| 521 | Utilities Expense |

| 522 | Advertising Expense |

| 523 | Rent Expense |

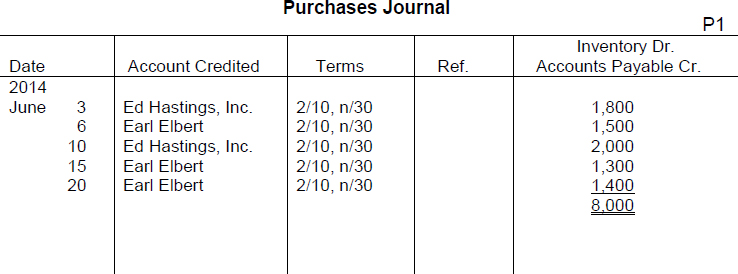

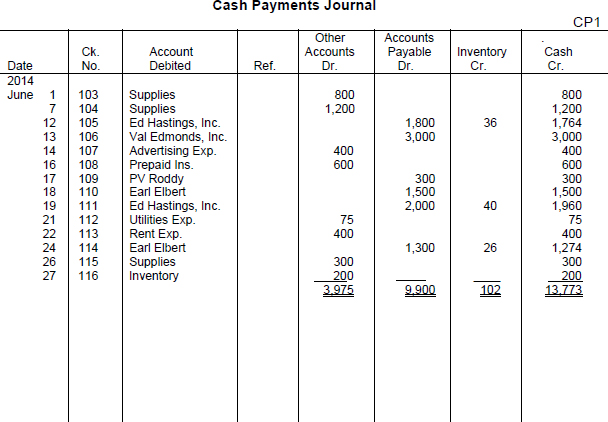

A list of selected transactions for June 2014 for E & Y Company appears below. The purchases journal and the cash payments journal follow that list.

| June | 1 | Purchased supplies, check no. 103, $800. |

| 3 | Purchased merchandise on account from Ed Hastings, Inc., invoice no. 1272, terms 2/10, n/30, $1,800. | |

| 4 | Purchased equipment on credit from Val Edmonds, Inc., $3,000. | |

| 5 | Purchased supplies on account from PV Roddy, $300. | |

| 6 | Purchased merchandise on account from Earl Elbert, invoice no. 1521, terms 2/10, n/30, $1,500. | |

| 7 | Purchased supplies, check no. 104, $1,200. | |

| 10 | Purchased merchandise on account from Ed Hastings, Inc., invoice no. 1490, terms 2/10, n/30, $2,000. | |

| 12 | Paid Ed Hastings, Inc. for invoice no. 1272, $1,800 less 2% discount, check no. 105, $1,764. | |

| 13 | Paid Val Edmonds, Inc., $3,000 on account, check no. 106. | |

| 14 | Paid an advertising agency for ads to appear in June, check no. 107, $400. | |

| 15 | Purchased merchandise on account from Earl Elbert, invoice no. 1706, terms 2/10, n/30, $1,300. | |

| 16 | Paid premium due on a one-year insurance policy, check no. 108, $600. | |

| 17 | Paid PV Roddy on account, $300, check no. 109. | |

| 18 | Issued check no. 110 for $1,500 to Earl Elbert for payment on account. | |

| 19 | Paid Ed Hastings, Inc., in full for invoice no. 1490, $1,960, check no. 111. | |

| 20 | Purchased merchandise on account, from Earl Elbert, invoice no. 1811, terms 2/10, n/30, $1,400. | |

| 21 | Paid $75 for utilities, check no. 112. | |

| 22 | Paid $400 for rent for June, check no. 113. | |

| 23 | Purchased supplies on account from PV Roddy, $420. | |

| 24 | Paid Earl Elbert for invoice no. 1706, $1,300 less 2% discount, check no. 114, $1,274. | |

| 26 | Purchased supplies for cash, check no. 115, $300. | |

| 27 | Purchased merchandise for cash, $200, check no. 116. |

(a) Journalize the transactions above in the single-column purchases journal and the cash payments journal provided.

(b) Identify any transactions which must be recorded in a journal other than these two special journals.

(c) Foot and crossfoot the two special journals at June 30, 2014.

SOLUTION TO EXERCISE 7-7

| TIP: | The cash payments journal is often called the cash disbursements journal. |

(b) Transactions which must be recorded in other journals are:

| TIP: | Some companies expand the purchases journal to include all types of purchases on account. Instead of one column for purchases of merchandise on credit (requiring postings to both Inventory and Accounts Payable), a multiple-column format is used. The multiple-column format usually includes a credit column for accounts payable and debit columns for purchases of merchandise, purchases of office supplies, purchases of store supplies, and other accounts. A special column can be added for purchases of equipment if the activity warrants it. |

| TIP: | The general journal is used to record transactions that do not occur with enough frequency to warrant the creation of a special journal. |

(c) Footing is accomplished by adding the amounts of each column and inserting the totals at the bottom of the respective columns. There is nothing to crossfoot in a single-column journal because there is only one column. The cash payments journal is crossfooted by summing the totals of the debit columns ($3,975 +$9,900 = $13,875) and comparing that sum with the sum of the totals of the credit columns ($102 + $13,773 = $13,875). The two sums are equal so the journal crossfoots. This means the equality of the debits and credits entered in that journal has been proven.

EXERCISE 7-8

Purpose: (L.O. 1 thru 3) This exercise will quiz you about terminology used in this chapter.

A list of accounting terms with which you should be familiar appear below.

| Accounting information system | Manual accounting system |

| Accounts payable (creditors') subsidiary ledger | Purchases journal |

| Accounts receivable (customers') subsidiary ledger | Sales journal |

| Cash payments (cash disbursements) journal | Special journal |

| Cash receipts journal | Subsidiary ledger |

| Control account |

Instructions

For each item below, enter in the blank the term that is described.

- _______________________A journal that records similar types of transactions, such as all credit sales.

- _______________________A special journal used to record all sales of merchandise on account (on credit).

- _______________________A special journal that records all cash received.

- _______________________A special journal that records all purchases of merchandise on account (on credit).

- _______________________A special journal that records all cash paid.

- _______________________A group of accounts with a common characteristic.

- _______________________A subsidiary ledger that contains accounts with individual creditors.

- _______________________A subsidiary ledger that contains individual customer accounts.

- _____________________An account in the general ledger that controls a subsidiary ledger.

- _______________________A system that collects and processes data, and communicates financial information to interested parties.

- _______________________A system in which someone performs each of the steps in the accounting cycle by hand.

SOLUTION TO EXERCISE 7-8

- Special journal

- Sales journal

- Cash receipts journal

- Purchases journal

- Cash payments (cash disbursements) journal

- Subsidiary ledger

- Accounts payable (creditors') subsidiary ledger

- Accounts receivable (customers') subsidiary ledger

- Control account

- Accounting information system

- Manual accounting system

ANALYSIS OF MULTIPLE-CHOICE TYPE QUESTIONS

- (L.O. 1) Which of the following is not a principle of accounting information system development?

- Automation.

- Cost awareness.

- Useful output.

- Flexibility.

Approach and Explanation: List the principles that should be followed in designing and developing an accounting system. Identify the answer selection not in your list. Not all entities need automated (or computerized) systems. Some entities find a manual system more appropriate. For any entity, however, the following principles should be followed in designing and developing an efficient and effective accounting information system:

- Cost awareness—the benefits obtained from the information collected and disseminated must outweigh the cost of providing it.

- Useful output—to be useful, information must be understandable, relevant, reliable, timely, and accurate.

- Flexibility—the system should be able to accommodate a variety of users and changing information needs.

(Solution = a.)

- (L.O. 2) A general ledger account which summarizes the collection of related accounts appearing in a subsidiary ledger is called a:

- contra account.

- control account.

- summary account.

- subsidiary ledger account.

Explanation: The subsidiary ledger reduces the number of accounts that otherwise would appear in the general ledger. The details about an item (such as accounts receivable or accounts payable or equipment, for example) are removed from the general ledger and are replaced by a single account (control account) which summarizes the detail. The details are then grouped and called a subsidiary ledger. A control account is often called the controlling account. (Solution = b.)

- (L.O. 3) Each of the following likely appears as a column heading in the cash receipts journal except:

Approach and Explanation: Think about the purpose of the cash receipts journal—to record all transactions involving a receipt of cash. A receipt of cash is recorded by a debit to Cash; therefore, the rest of the entry involves a credit to a noncash account. The credit is (1) to Sales Revenue for a cash sale of merchandise, or (2) to Accounts Receivable for a collection on a customer's account, or (3) to some other account (such as Equipment for a sale of equipment or Interest Revenue for interest earned on money loaned to others).

If a merchandiser offers a cash discount on sales for timely payment of the customer's account, the collection of the account receivable within the discount period results in recording a debit to Sales Discounts (a contra sales account). Thus, a special column in the cash receipts journal for Sales Discounts Dr. is needed to accommodate the recording of this frequent transaction. Debits are made to the Sales Revenue account only to (1) correct erroneous credit entries to the same account, and (2) close the balance of the Sales Revenue account to Income Summary at the end of the period. Therefore, “Sales Dr.” does not appear as a column heading in any special journal. (Solution = b.)

- (L.O. 3) A checkmark entered in the “Ref.” column of a single-column purchases journal indicates that the entry:

- is not to be posted to any ledger.

- has been posted to the general ledger.

- has been posted to the appropriate subsidiary ledger.

- has been posted to the general ledger and to the appropriate subsidiary ledger.

Explanation: Answer selection “a” is incorrect because all transactions recorded in any journal must be posted to the general ledger and all transactions recorded in a single-column purchases journal must also be posted to a subsidiary ledger—the accounts payable ledger. Answer selection “b” is incorrect because the transactions recorded in the single-column purchases journal are posted to the general ledger in total at the end of the month, and the completion of that posting is indicated by placing the general ledger account numbers for Inventory and Accounts Payable beneath the total of the single-money column. Answer selection “d” is incorrect because a checkmark appears by an individual transaction, and purchases are not posted individually to the general ledger. A checkmark is placed in the Ref. column when the posting has been made to the suppliers' (accounts payable) subsidiary ledger. Postings are to be made to the subsidiary ledger on a daily basis. (Solution = c.)

- (L.O. 3) When special journals are used, the return of merchandise to a supplier for credit is usually recorded in the:

- Sales journal.

- Purchases journal.

- Cash receipts journal.

- Cash payments journal.

- General journal.

Approach and Explanation: List the four special journals discussed in this chapter and briefly describe their function. Also describe the general journal's function.

- Sales journal—all sales of merchandise on account.

- Cash receipts journal—all receipts of cash (including cash sales).

- Purchases journal—all purchases of merchandise on account.

- Cash payments journal—all payments of cash (including cash purchases).

- General journal—all transactions that do not appropriately fit in a special journal (including adjustments and closing entries).

The transaction described does not fit the description of any of the four special journals. Thus, it goes into the general journal. (Solution = e.)

- (L.O. 3) When special journals are used, the payment to a supplier for merchandise which had previously been purchased on account is usually recorded in the:

- Sales journal.

- Purchases journal.

- Cash receipts journal.

- Cash disbursements journal.

- General journal.

Approach and Explanation: Mentally review the types of journals and their functions. All cash payments are recorded in the cash payments journal which is often called the cash disbursements journal. (Solution = d.)

- (L.O. 3) When special journals are used, the most likely source of a debit posting to the Accounts Receivable account in the general ledger is the:

- Sales journal.

- Purchases journal.

- Cash receipts journal.

- Cash payments journal.

- General journal.

Approach and Explanation: Identify the most common reason for debits to Accounts Receivable—sales on account (on credit). Mentally review the special journals and the transactions recorded therein. All sales on account are recorded in the sales journal. (Solution = a.)

- (L.O. 3) When special journals are used, the most likely source of a credit posting to an expense account in the general ledger is the:

- Sales journal.

- Purchases journal.

- Cash receipts journal.

- Cash payments journal.

- General journal.

Explanation: The most common reason for a credit to an expense account is a closing entry at the end of the period or possibly from an adjusting entry or a correction. All of these items are recorded in the general journal. (A cash refund for an item previously recorded as an expense would cause a credit posting and would be recorded in the cash receipts journal; however, this would not be as common as adjusting or closing entries.) (Solution = e.)