CHAPTER 9

![]()

ACCOUNTING FOR RECEIVABLES

OVERVIEW

Receivables are claims that are expected to be collected in cash. Three major types of receivables are usually recognized; they are accounts, notes, and other receivables. Receivables can be (a) held until they are collected, (b) sold before they are collected, or (c) held and never collected. Many businesses grant credit to customers; hence, they have accounts receivable. They know that, when making sales “on account,” a risk exists because some accounts will never be collected. However, the cost of these bad debts is more than offset by the profit from the extra sales made because of the attraction of granting credit. The collections department may make many attempts to collect an account before “writing-off” a bad debtor. Frequently an account is deemed to be uncollectible a year or more after the date of the credit sale. In this chapter, we will discuss the allowance method of accounting for bad debts. The allowance method permits the accountant to estimate the amount of bad debts expense that should be matched with revenues rather than waiting to book expense at the time of an actual write-off.

SUMMARY OF LEARNING OBJECTIVES

- Identity the different types of receivables. Receivables are frequently classified as (1) accounts, (2) notes, and (3) other. Accounts receivable are amounts customers owe on account. Notes receivable are claims for which lenders issue formal instruments of credit as proof of the debt. Other receivables include nontrade receivables such as interest receivable, loans to company officers, advances to employees, and income taxes refundable.

- Explain how companies recognize accounts receivable. Companies record accounts receivable when they provide a service on account or at the point of sale of merchandise on account. Accounts receivable balances are reduced by sales returns and allowances. Cash discounts also reduce the amount received on accounts receivable. When interest is charged on a past due receivable, the company adds this interest to the accounts receivable balance and recognizes it as interest revenue.

- Distinguish between the methods and bases companies use to value accounts receivable. There are two methods of accounting for uncollectible accounts: the allowance method and the direct write-off method. The allowance method is required for financial reporting purposes when bad debts are material (significant) in size. Companies may use either the percentage-of-sales or the percentage-of-receivables basis to estimate uncollectible accounts using the allowance method. The percentage-of-sales basis emphasizes the expense recognition (matching) principle. The percentage-of-receivables basis emphasizes the cash realizable value of the accounts receivable. An aging schedule is often used with this basis.

- Describe the entries to record the disposition of accounts receivable. When a company collects an account receivable, it credits Accounts Receivable. When a company (factors) an account receivable, a service charge is assessed which reduces the amount of cash collected.

- Compute the maturity date of and interest on notes receivable. For a note stated in months, the maturity date is found by counting the months from the date of issue. For a note stated in days, the number of days is counted, omitting the issue date and counting the due date. The formula for computing interest is Face value × Interest rate × Time.

- Explain how companies recognize notes receivable. Companies record notes receivable at face value. In some cases, it is necessary to record accrued interest prior to maturity. In this case, companies debit Interest Receivable and credit Interest Revenue.

- Describe how companies value notes receivable. As with accounts receivable, companies report notes receivable at their cash (net) realizable value. The notes receivable allowance account is the Allowance for Doubtful Accounts. The computation and estimations involved in valuing notes receivables at cash realizable value, and in recording the proper amount of bad debt expense and related allowance, are similar to those involved in accounting for accounts receivable.

- Describe the entries to record the disposition of notes receivable. Notes can be held to maturity. At that time the face value plus accrued interest is due, and the note is removed from the accounts. In many cases, the holder of the note speeds up the conversion to cash by selling the receivable to another party (a factor). In some situations, the maker of the note dishonors the note (defaults), in which case the company transfers the note and accrued interest to an account receivable or writes off the note.

- Explain the statement presentation and analysis of receivables. Companies should identify in the balance sheet or in the notes to the financial statements each major type of receivable. Companies report short-term receivables as current assets. They report the gross amount of receivables and the allowance for doubtful accounts. They report bad debt expense and service charge expense in the multiple-step income statement as operating (selling) expenses. Interest revenue appears as other revenue in the nonoperating section of the income statement. Managers and investors evaluate accounts receivable for liquidity by computing a turnover ratio and an average collection period.

TIPS ON CHAPTER TOPICS

| TIP: | Trade accounts receivable result from the sale of products or services to customers. Nontrade accounts receivable (amounts that are due from nontrade customers who do not buy goods or services in the normal course of the company's main business activity) should be listed separately on the balance sheet from the trade accounts receivable balance. |

| TIP: | Notice how the subjects of this chapter affect the balance sheet and the income statement. The balance of the Accounts Receivable account and its contra account—Allowance for Doubtful Accounts—are reported in the current asset section of the balance sheet. The balance of Notes Receivable (assuming the notes are due within one year of the balance sheet date) is also classified in the current asset section of the balance sheet. The balance of Bad Debt Expense is usually reported in the operating expense section of the multiple-step income statement. |

| TIP: | Assets such as current receivables and inventories should never be reported at more than their net (cash) realizable value. Thus, if some uncollectible accounts are expected, receivables are reduced by these uncollectible amounts when presented on the balance sheet. |

| TIP: | The carrying value (or book value or carrying amount) of accounts receivable is equal to the balance of the Accounts Receivable account less the balance of the related valuation account (Allowance for Doubtful Accounts). |

| TIP: | In the event that a customer's account has a credit balance on the balance sheet date, it should be classified as a current liability and not be offset against other accounts receivable with debit balances. |

| TIP: | Even though special journals were discussed in a prior chapter, simplicity requires that the general journal be used to illustrate all journal entries in the remainder of the book. |

ILLUSTRATION 9-1

ENTRIES FOR THE ALLOWANCE METHOD (L.O.3)

EXERCISE 9-1

Purpose: (L.O. 3) This exercise will identify the two approaches of applying the allowance method of accounting for uncollectible accounts receivable.

Howell's Department Store offers a store credit card for the convenience of its customers. Even though the store follows up on delinquent accounts, past experience indicates that a predictable amount of credit sales will ultimately result in uncollectible accounts. Howell uses the allowance method of accounting for uncollectible accounts. Bad debts are a material amount.

Instructions

(a) Describe the two methods available for determining the amount of the adjusting entry to record bad debt expense and to adjust the allowance account. Also discuss the emphasis of each method.

(b) Explain why the direct write-off method is not a generally accepted accounting method for Howell's Department Store.

SOLUTION TO EXERCISE 9-1

(a) When using the allowance method of accounting for bad debts, there are two methods available for determining the amount of the adjusting entry to record bad debts expense and to adjust the allowance account. They are:

(1) The percentage-of-sales basis: This method focuses on estimating bad debts expense. The average percentage relationship between actual bad debt losses and net credit sales (or total credit sales) of the period is used to determine the amount of expense for the period. This method focuses on the matching of current bad debts expense with revenues of the current period and thus emphasizes the income statement. The amount of bad debts expense is simply calculated and recorded; a by-product of this approach is the increase in the allowance account.

(2) The percentage-of-receivables basis: This method focuses on estimating the cash (net) realizable value of the current receivables and thus emphasizes the balance sheet. It only incidentally measures bad debts expense; the expense reported may not be the best figure to match with the amount of credit sales of the current period. If this method is to be used, the aging technique is preferable to the use of a simple percentage times total accounts receivable. An aging analysis takes into consideration the age of a receivable. The older the age, the lower the probability of collection.

(b) Under the direct write-off method, bad debt losses are not estimated and no allowance account is used. No entry regarding bad debts is made until a specific account has definitely been established as uncollectible. Then the loss is recorded by a debit to Bad Debt Expense and a credit to Accounts Receivable.

When the direct write-off method is used, Accounts Receivable will be reported at its gross amount and bad debt expense is often recorded in a period different from the period in which the revenue was recorded. Thus, no attempt is made to match bad debt expense to sales revenues in the income statement or to show the cash (net) realizable value of the accounts receivable in the balance sheet. Consequently, unless bad debt losses are insignificant, the direct write-off method is not acceptable for financial reporting purposes. Howell's bad debts are material (significant) in amount so the allowance method must be used for financial reporting purposes. The direct write-off method is, however, used for tax purposes.

EXERCISE 9-2

Purpose: (L.O. 3) This exercise will review the two bases for determining the dollar amount of the adjusting entry to recognize bad debt expense and to adjust the Allowance for Doubtful Accounts account.

The trial balance before adjustment at December 31, 2014 for the Liz Company shows the following balances:

Instructions

Using the data above, give the journal entries to record each of the following cases (each situation is independent):

(a) The company expects bad debts to be 1 3/4% of net credit sales.

(b) Liz performs an aging analysis at December 31, 2014 which indicates an estimate of $6,000 uncollectible accounts.

SOLUTION TO EXERCISE 9-2

Explanation

(a) The percentage-of-net-credit-sales approach to applying the allowance method of accounting for bad debts focuses on determining an appropriate expense figure. The existing balance in the allowance account is not relevant in the computation.

(b) An aging analysis provides the best estimate of the net realizable value of accounts receivable. By using the results of the aging to adjust the allowance account, the amount reported for net receivables on the balance sheet is the cash (net) realizable value of accounts receivable. It is important to notice that the balance of the allowance account before adjustment is a determinant in the adjustment required. The following T-account reflects the facts used to determine the necessary adjustment.

EXERCISE 9-3

Purpose: (L.O. 4) This exercise will illustrate the journal entries related to credit card sales.

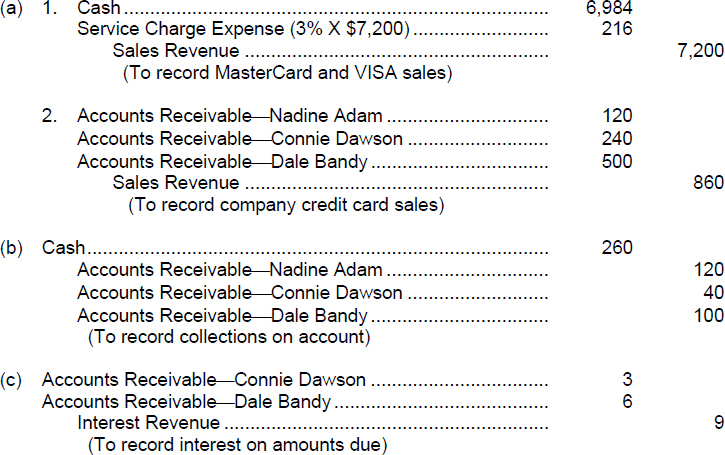

Bubba's Bed & Bath Shop accepts MasterCard, VISA, and its own Bubba's Bed & Bath Shop (BB&BS) credit cards. MasterCard and VISA sales slips are deposited in the bank daily; the bank charges a 3% fee. The following transactions occurred on May 3, 2014.

- Made sales of $7,200 to customers who presented MasterCard and VISA cards.

- Made sales to the following who used their BB&BS cards:

- Nadine Adam, $120

- Connie Dawson, $240

- Dale Bandy, $500

Instructions

(a) Prepare the journal entries to record the transactions above for Bubba's Bed and Bath Shop.

(b) Prepare the journal entry to record collections of $120, $40, and $100 from Nadine Adam, Connie Dawson, and Dale Bandy, respectively.

(c) Prepare the journal entry to record interest charged to customer accounts at the rate of 1.5% per month as follows: Connie Dawson, $3; Dale Bandy, $6.

SOLUTION TO EXERCISE 9-3

EXERCISE 9-4

Purpose: (L.O. 4) This exercise will illustrate the factoring of accounts receivable.

The Tuscawilla Tailgate Company often factors its accounts receivable. On May 1, 2014, the company factored $250,000 of customer accounts receivable to Fagan Factors, Inc. which charged a 3% service charge.

Instructions

(a) Prepare the journal entry to record the sale of the accounts receivable to the factor.

(b) Explain how the service charge will affect Tuscawilla Tailgates' financial statements.

SOLUTION TO EXERCISE 9-4

(b) The service charge expense incurred should be reported as a selling expense (operating expense) on the income statement because the company often sells its receivables. If receivables were sold infrequently, the service charge expense may be classified in the Other Expenses and Losses section of the income statement.

EXERCISE 9-5

Purpose: (L.O. 6) This exercise reviews the journal entries for various transactions involving notes receivable.

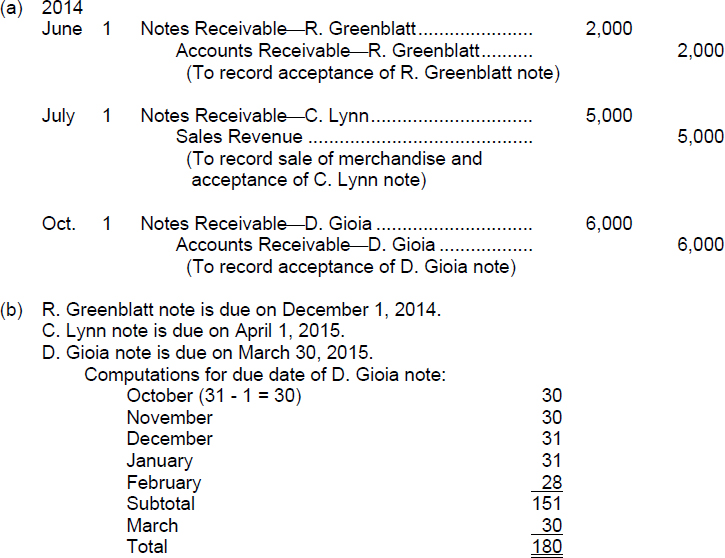

The following transactions occurred during 2014 and pertain to the Aaron Retail Company.

| June 1 | Accepted a note from R. Greenblatt in settlement of his $2,000 account. The note is due in six months and bears interest at 12%. |

| July 1 | Sold merchandise to C. Lynn for $5,000. Accepted a note due in nine months at 10%. |

| Oct. 1 | Accepted a note from D. Gioia for $6,000 in settlement of his account receivable. The 10% note is due in 180 days. |

Instructions

(a) Prepare the journal entries to record the receipt of each of the three notes.

(b) Indicate the due date of each note.

(c) Assume the first note is collected on its due date. Prepare the appropriate journal entry to record its collection.

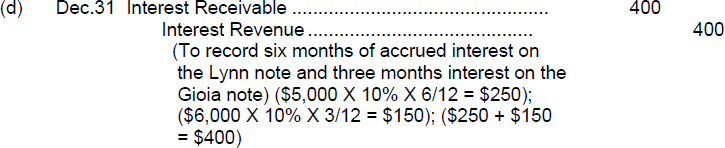

(d) Assume the accounting period ends on December 31. Prepare the appropriate adjusting entry(s) at December 31, 2014, to record accrued interest on the second and third notes.

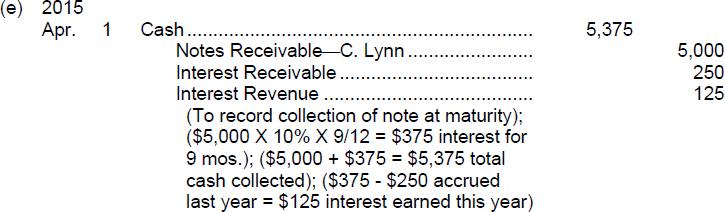

(e) Assume the second note is honored on its maturity date. Prepare the journal entry to record this transaction.

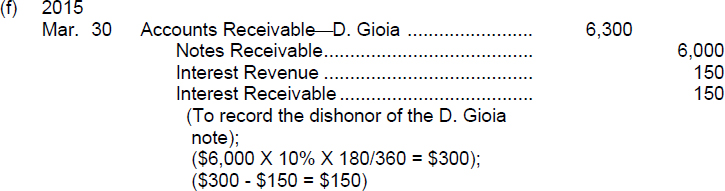

(f) Assume the third note is dishonored on its due date. Aaron expects eventual collection. Prepare the appropriate journal entry.

SOLUTION TO EXERCISE 9-5

| TIP: | When the life of a note is expressed in terms of months, the due date is found by counting the months from the date of issue. A note drawn on the last day of a month matures on the last day of a subsequent month. When the due date is stated in terms of days, it is necessary to count the exact number of days to determine the maturity date. In counting, the day the note was issued is omitted but the due date is included. |

| TIP: | The formula for computing interest on an interest-bearing note is:

|

| TIP: | An interest rate is always stated in terms of an annual basis, unless otherwise indicated. |

| TIP: | A note is said to be honored when it is paid in full at its maturity date. |

| TIP: | A dishonored note is a note that was not paid in full at its maturity date. The maker defaulted on the note. | ||||||||

| TIP: | No interest revenue would be recorded at this date if collection of the note was not expected. | ||||||||

| TIP: | Review the terminology related to notes receivable:

|

||||||||

| TIP: | Interest is always a function of time, rate, and balance. Always assume a 360-day year when computing interest (unless a 365-day year is specified). This assumption makes computations easier. |

EXERCISE 9-6

Purpose: (L.O. 9) This exercise will review the measures used to evaluate the liquidity of accounts receivable.

The management of M. F. Specie Company is analyzing the entity's recent financial statements to determine the efficiency of the company's credit policies for customers. The following information is extracted from the statements:

| Sales revenue | $930,000 |

| Sales returns | 30,000 |

| Accounts receivable, 12/31/14 | 85,000 |

| Accounts receivable, 12/31/13 | 60,000 |

Instructions

- Assuming all sales are credit sales (on account), compute the receivables turnover for 2014.

- Assuming the company's policy is to require payment within 30 days of invoicing a customer and invoices are sent within two days of a sale, explain whether the company's average collection period suggests that the company has weak or strong controls surrounding its credit-granting activity.

SOLUTION TO EXERCISE 9-6

2. The average collection period of 29.41 days when compared to the typical 32 days between a sale date and the payment due date suggests that the company has adequate to strong controls surrounding its credit-granting activity.

The average number of days to collect an account receivable is computed as follows:

| TIP: | A ratio is an expression of the relationship of one item (or group of items) to a second item (or group of items). It is determined by dividing the first item (amount) by the second item (amount). The relationship may be expressed either as a percentage, a rate, or a simple proportion.

For example: If A is $100,000 and B is $25,000 the ratio of A to B can be expressed in several ways, such as the following:

The way in which the ratio is expressed depends on the particular ratio. If it is the current ratio, it would likely be expressed as a proportion (4:1 or 4 to 1) or as a rate (4 times). If it is the debt to stockholders' equity ratio, it would likely be expressed as a percentage (400%). |

||||||||

| TIP: | In this chapter we look at the financial ratio used to assess the liquidity of receivables--the receivables turnover ratio. In Chapter 6 we looked at the financial ratio used to assess the liquidity of inventory—the inventory turnover ratio. In the remaining chapters of this book, be alert for discussions of other financial ratios. | ||||||||

| TIP: | The average collection period is not very meaningful until it is compared with the company's credit terms. | ||||||||

| TIP: | The denominator of a turnover ratio (such as for receivables) always involves an average balance. That average can be determined by adding the balance at the end of the period to the balance at the beginning of the period and dividing by 2. However, if seasonal variances are significant, the annual average should be determined by adding together the balances at the end of each month and dividing by 12. |

EXERCISE 9-7

Purpose: (L.O. 1 thru 9) This exercise will quiz you about terminology used in this chapter.

A list of accounting terms with which you should be familiar appears below.

| Accounts receivable | Maker |

| Accounts receivable turnover | Notes receivable |

| Aging the accounts receivable | Other receivables |

| Allowance method | Payee |

| Average collection period | Percentage-of-receivables basis |

| Bad Debts Expense | Percentage-of-sales basis |

| Cash (net) realizable value | Promissory note |

| Direct write-off method | Receivables |

| Dishonored (defaulted) note | Trade receivables |

| Factor |

Instructions

For each item below, enter in the blank the term that is described.

- _____________________Amounts due from individuals and other companies.

- _____________________Amounts owed by customers on account.

- _____________________Written promise from another party (as evidenced by a formal instrument) for an amount to be received from them.

- _____________________Various forms of nontrade receivables, such as interest receivable and income taxes refundable.

- _____________________The analysis of customer balances by the length of time they have been unpaid.

- _____________________Management establishes a percentage relationship between the expected losses from uncollectible accounts and the amount of receivables.

- _____________________Management establishes a percentage relationship between expected losses from uncollectible accounts and the amount of credit sales.

- _____________________The net amount expected to be received in cash.

- _____________________A written promise to pay a specified amount of money on demand or at a definite time.

- _____________________The party in a promissory note who is making the promise to pay.

- _____________________The party to whom payment of a promissory note to be made.

- _____________________A note that is not paid in full at maturity.

- _____________________A finance company or bank that buys receivables from businesses and then collects the payments directly from the customers.

- _____________________Notes and accounts receivable that result from sales transactions.

- _____________________A measure of the liquidity of accounts receivables, computed by dividing net credit sales by average net accounts receivables.

- _____________________The average amount of time that a receivable is outstanding, calculated by dividing 365 days by the accounts receivable turnover.

- _____________________An expense account used to record the cost of uncollectible receivables.

- ______________________A method of accounting for bad debts that involves expensing accounts at the time they are determined to be uncollectible.

- ______________________A method of accounting for bad debts that involves estimating uncollectible accounts at the end of each period.

SOLUTION TO EXERCISE 9-7

- Receivables

- Accounts receivable

- Notes receivable

- Other receivables

- Aging the accounts receivable

- Percentage-of-receivables basis

- Percentage-of-sales basis

- Cash (net) realizable value

- Promissory note

- Maker

- Payee

- Dishonored (defaulted) note

- Factor

- Trade receivables

- Accounts receivable turnover

- Average collection period

- Bad Debts Expense

- Direct write-off method

- Allowance method

ANALYSIS OF MULTIPLE-CHOICE TYPE QUESTIONS

- (L.O. 3) The journal entry to record the write-off of an individual customer's account receivable using the allowance method involves a debit to:

- Allowance for Doubtful Accounts and a credit to Accounts Receivable.

- Bad Debt Expense and a credit to Accounts Receivable.

- Accounts Receivable and a credit to Allowance for Doubtful Accounts.

- Bad Debt Expense and a credit to Allowance for Doubtful Accounts.

Approach and Explanation: Write down the journal entry to record the write-off of an individual customer's account:

Find the answer selection that describes this entry. Answer selection “d” describes the journal entry to record bad debts expense and to adjust the allowance account. (Solution = a.)

- (L.O. 3) The balances of the Accounts Receivable account and Allowance for Doubtful Accounts account, before adjustment, are $60,000 and $1,200 respectively. Bad debt expense for the period is estimated to be $3,100. What amount should be reported for net accounts receivable on the balance sheet?

- $58,100.

- $58,800.

- $56,900.

- $55,700.

Approach and Explanation: One approach is to draw T-accounts, enter the balances before adjustment, reflect in the accounts the entry to record bad debt expense, balance the accounts, and deduct the balance of the contra account from the balance of the Accounts Receivable account to determine net accounts receivable at the balance sheet date.

$60,000 Accounts receivable − $4,300 Allowance = $55,700 Net accounts receivable. (Solution = d.)

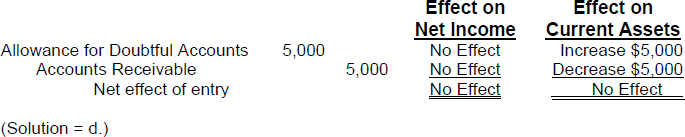

- (L.O. 3) The journal entry to record uncollectible accounts expense using the allowance method will:

- reduce net income and total current assets.

- reduce net income but will not affect total current assets.

- not affect net income but will reduce total current assets.

- not affect net income or total current assets.

Approach and Explanation: Before you read all of the answer choices, write down the journal entry to record bad debt expense (uncollectible accounts expense is synonymous to bad debt expense). Analyze both parts of the entry (one part at a time) to determine the impact on (1) net income and (2) current assets.

The amount used in the entry can be any assumed amount since no amount was specified. (Solution = a.)

- (L.O. 3) The journal entry to write off an individual customer's account receivable using the allowance method will:

- reduce net income and total current assets.

- reduce net income but will not affect total current assets.

- not affect net income but will reduce total current assets.

- not affect net income or total current assets.

Approach and Explanation: Write down the journal entry to write off an individual customer's account. Analyze each part of the entry to determine its impact on (1) net income and (2) current assets. Summarize the effects and locate the correct answer selection. Assume any amount you want for the entry since no amount was specified in the question.

- (L.O. 3) The balance of the Allowance for Doubtful Accounts account represents the:

- total amount of uncollectible accounts written off to date.

- amount of credit sales made this period that has not been collected.

- amount of cash that has been set aside in a special fund to make up for bad debt losses.

- portion of total accounts receivable that is not expected to be converted to cash.

Approach and Explanation: Think about what prompts entries to the valuation (allowance) account for accounts receivable. The allowance is increased when the provision for bad debt (expense) is recorded. The allowance is decreased when an individual account is ultimately deemed to be uncollectible. The provision is recorded because some yet unidentified portion of receivables arising from credit sales will never be collected (hence, will never be converted to cash). Selection “c” is false because cash is not involved in the entry to set up the allowance; no fund is set aside for this purpose. (Solution = d.)

- (L.O. 3) The balance of the Allowance for Doubtful Accounts account at January 1, 2014 was $5,900. During 2014, accounts receivable amounting to $8,000 were written off. Estimated uncollectible accounts expense for 2014 amounts to $7,100. The balance of the Allowance for Doubtful Accounts account to be reported on the balance sheet at December 31, 2014 is:

- $13,000.

- $ 7,100.

- $ 6,800.

- $ 5,000.

Approach and Explanation: Draw a T-account for the account in question. Visualize the journal entries to write off accounts and to estimate bad debt expense. Enter the resulting postings as they would be reflected in the allowance account.

It is evident that the company is using the percentage-of-sales basis of applying the allowance method because its entry to the allowance account is based on the amount of bad debts expense rather than an appropriate ending balance for the allowance account. (Solution = d.)

- (L.O. 3) The following data are available for 2014:

Sales, cash $200,000 Sales, credit 500,000 Accounts Receivable, January 1 80,000 Accounts Receivable, December 31 72,000 Allowance for Doubtful Accounts, January 1 4,000 Accounts written off during 2014 4,600 The journal entry to record bad debt expense for the period and to adjust the allowance account is to be based on an estimate of 1% of credit sales. The entry to record the uncollectible accounts expense for 2014 would include a debit to the Bad Debt Expense account for:

- $7,200.

- $5,600.

- $4,400.

- $5,000.

Approach and Explanation: Think about the emphasis of the entry when the percentage-of-sales basis is used. This basis emphasizes the income statement. Therefore, 1% times credit sales equals expense. $500,000 × 1% = $5,000. The balance of the allowance account before adjustment does not affect this computation or entry. (Solution = d.)

- (L.O. 3) The following data are available for 2014:

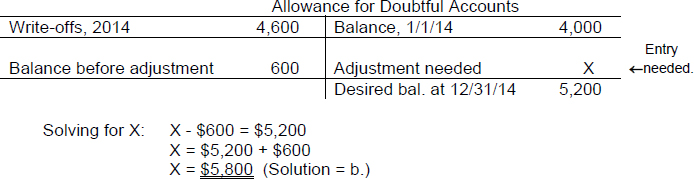

Sales, cash $200,000 Sales, credit 500,000 Accounts Receivable, January 1 80,000 Accounts Receivable, December 31 72,000 Allowance for Doubtful Accounts, January 1 4,000 Accounts written off during 2014 4,600 The journal entry to record bad debt expense for the period and to adjust the allowance account is to be based on an aging analysis of accounts receivable. The aging analysis of accounts receivable at December 31, 2014, reveals that $5,200 of existing accounts receivable are estimated to be uncollectible. The entry to record the uncollectible accounts expense for 2014 will involve a debit to the Bad Debt Expense account for:

- $9,800.

- $5,800.

- $5,200.

- $4,600.

Approach and Explanation: An aging analysis is performed to determine the best figure to represent the cash (net) realizable value for accounts receivable in the balance sheet. Thus, $5,200 is the desirable balance for the allowance account at the reporting date. Determine the existing balance in the allowance account and the adjusting entry needed to arrive at the predetermined balance.

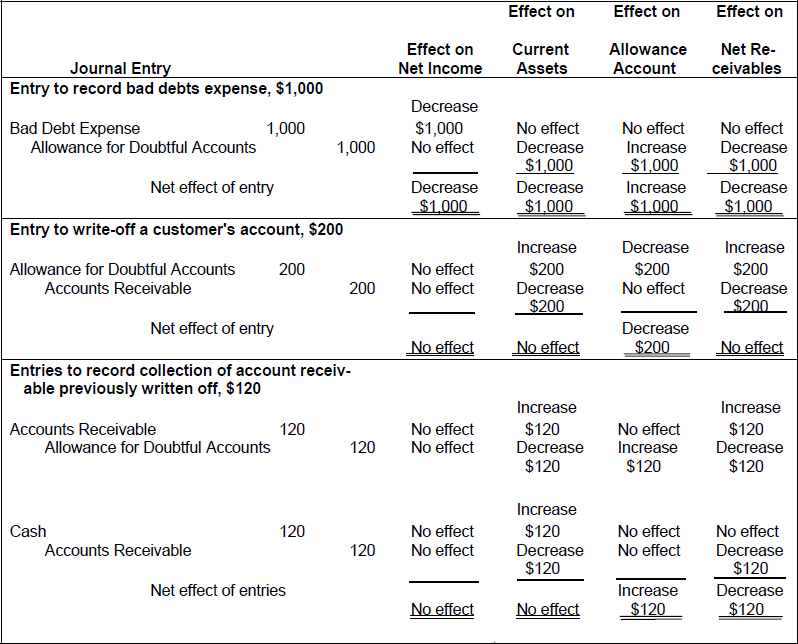

- (L.O. 3) Gatorland recorded bad debt expense of $30,000 and wrote off accounts receivable of $25,000 during 2014. The net effect of these two transactions on net income was a decrease of:

- $55,000.

- $30,000.

- $25,000.

- $5,000.

Approach and Explanation: Reconstruct both entries referred to in the question. Then analyze each debit and each credit separately as to its effect on net income.

- (L.O. 3) Chelser Corporation performed an analysis and an aging of its accounts receivable at December 31, 2014 which disclosed the following:

Accounts receivable balance $100,000 Allowance for doubtful accounts balance 5,000 Accounts deemed uncollectible 7,400 The cash (net) realizable value of the accounts receivable at December 31 is:

- $87,600.

- $92,600.

- $95,000.

- $97,600.

Approach and Explanation: Read the last sentence of the question. “The cash (net) realizable value of the accounts receivable at December 31 is.” Underline cash (net) realizable value of accounts receivable. Write down the definition of cash (net) realizable value of accounts receivable—amount of accounts receivable ultimately expected to be converted into cash. Read the details of the question. If an aging shows $7,400 of the $100,000 accounts receivable are deemed uncollectible, then the remaining $92,600 are expected to be converted into cash. (Because the balance of the allowance account does not agree with the amount of uncollectibles per the aging, the allowance for doubtful accounts balance must be the unadjusted balance or the percentage of sales method is being used to determine the amount to record as bad debts expense.) (Solution = b.)

- (L.O. 5) The term “maker” as it applies to a promissory note refers to the:

- payee.

- lender.

- borrower.

- seller.

Approach and Explanation: Think about the terminology related to a promissory note:

Face value or face amount: Denomination of note. Principal.

Maker or borrower: Entity promising to pay face amount plus interest.

Payee: Entity to receive face value plus interest.

(Solution = c.)

- (L.O. 5) A note receivable with a face value of $20,000 was received from a customer. The note was dated April 1, 2014 and becomes due on April 1, 2015. Interest of 12% is payable at the maturity date. The income statement for the calendar year of 2014 should report interest income (or interest revenue) for this note of:

- $0.

- $600.

- $1,800.

- $2,400.

Approach and Explanation: Write down the formula for the computation of interest. Fill in the amounts known and solve for the unknown.

Interest would be accrued for the time between April 1, 2014 and December 31, 2014, which is nine months. (Solution = c.)

- (L.O. 6) The journal entry to adjust for the accrued interest on a note receivable involves:

- a debit to Interest Revenue and a credit to Notes Receivable.

- a debit to Interest Receivable and a credit to Notes Receivable.

- a debit to Interest Receivable and a credit to Interest Revenue.

- a debit to Interest Expense and a credit to Interest Payable.

Approach and Explanation: Recall that an accrued revenue is revenue that has been earned but not received. The adjusting entry to record an accrued revenue will increase revenue (record earned revenue) and increase a receivable (record the fact that the earned revenue has not been received.) Therefore, debit a receivable account and credit a revenue account. (Solution = c.)

- (L.O. 8) If a maker of a note fails to pay the amount due on the due date (defaults), the note is said to be:

- uncollectible.

- discounted.

- dishonored.

- due on demand.

Explanation: A note is said to be honored when it is paid in full at the maturity date. A dishonored note is a note that is not paid in full at maturity. (Solution = c.)

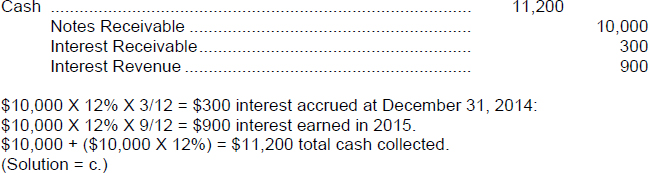

- (L.O. 8) A note receivable with a face value of $10,000 was received from a customer in connection with a sale of merchandise on October 1, 2014. The note has a stated interest rate of 12% and the principal and interest are both due on October 1, 2015. An appropriate adjusting entry was made on December 31, 2014, the end of the annual accounting period. No reversing entry was recorded on January 1, 2015. The journal entry to record the collection of the principal plus interest on October 1, 2015 will involve a credit to:

- Notes Receivable for $11,200.

- Interest Revenue for $1,200.

- Interest Revenue for $900.

- Cash for $11,200.

Approach and Explanation: Prepare the journal entry to record the collection of the principal plus interest on October 1, 2015. That entry is as follows:

TIP: If a reversing entry had been made on January 1, 2015, to reverse the prior period's accrual, the entry on October 1, 2015, would include a credit to Interest Revenue for $1,200 and no credit to Interest Receivable. - (L.O. 9) When the multiple-step format is used by Petite Clothiers Company for the income statement, bad debt expense (arising from sales to customers using the Petite Clothiers credit card) and service charge expense (arising from sales to customers using the VISA credit card) are to be:

- included with cost of goods sold.

- reported as selling expenses.

- reported as contra sales revenue items.

- reported as “other expenses” in the nonoperating section.

Explanation: Bad debt expense and service charge expense are to be classified as selling expenses; the “selling expenses” classification is a subsclassification of operating expenses. Thus, bad debt expense and service charge expense are not included with cost of goods sold expense or with nonoperating expenses and losses. (Solution = b.)

- (L.O. 9) Zollo Corporation's net accounts receivable were $500,000 at December 31, 2013 and $600,000 at December 31, 2014. The accounts receivable turnover was 5.0 for 2014 and net cash sales for 2014 were $200,000. Zollo's total net sales for 2014 were:

- $2,750,000.

- $2,950,000.

- $3,200,000.

- $5,000,000.

Approach and Explanation: Write down the formula for computing the accounts receivable turnover. Enter the data given and solve for the unknown (net credit sales). Add net cash sales ($200,000) to net credit sales ($2,750,000) to obtain total net sales ($2,950,000). The formula for the accounts receivable turnover ratio is: