CHAPTER 2

![]()

THE RECORDING PROCESS

OVERVIEW

Due to the great number of transactions that occur daily in most businesses, accountants do not find it practical to present the cumulative effects of these transactions on the basic accounting equation in tabular form as we did in Exercise 2 in Chapter 1. Instead, they have developed a system by which the effects of transactions and events may conveniently be recorded, sorted, summarized, and stored until financial statements are desired. That system is the focus of this chapter.

SUMMARY OF LEARNING OBJECTIVES

- Explain what an account is and how it helps in the recording process. An account is a record of increases and decreases in specific asset, liability, and owner's equity items.

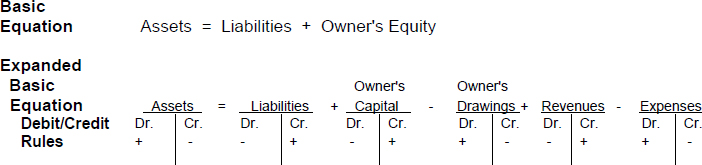

- Define debits and credits and explain their use in recording business transactions. The terms debit and credit are synonymous with left and right. Assets, drawings, and expenses are increased by debits and decreased by credits. Liabilities, owner's capital, and revenues are increased by credits and decreased by debits.

- Identify the basic steps in the recording process. The basic steps in the recording process are: (a) analyze each transaction in terms of its effect on the accounts, (b) enter the transaction information in a journal, and (c) transfer the journal information to the appropriate accounts in the ledger.

- Explain what a journal is and how it helps in the recording process. The initial accounting record of a transaction is entered in a journal before the data is entered in the accounts. A journal (a) discloses in one place the complete effect of a transaction, (b) provides a chronological record of transactions, and (c) prevents or locates errors because the debit and credit amounts for each entry can be easily compared.

- Explain what a ledger is and how it helps in the recording process. The ledger is the entire group of accounts maintained by a company. The ledger provides the balance in each of the accounts as well as keeps track of changes in these balances.

- Explain what posting is and how it helps in the recording process. Posting is the transfer of journal entries to the ledger accounts. This phase of the recording process accumulates the effects of journalized transactions in the individual accounts.

- Prepare a trial balance and explain its purposes. A trial balance is a list of accounts and their balances at a given time. Its primary purpose is to prove the mathematical equality of debits and credits after posting. A trial balance also uncovers errors in journalizing and posting and is useful in preparing financial statements.

TIPS ON CHAPTER TOPICS

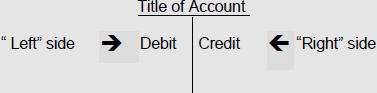

| TIP: | An account is an individual accounting record of increases and decreases in a specific asset, liability, owner's equity, revenue, or expense item. An account consists of three parts: (1) the title of the account, (2) a left or debit side, and (3) a right or credit side. In classrooms and in textbooks, we refer to this as a T-account. We need a separate account for each item reported in the income statement and balance sheet. When we refer to a specific account (such as Cash or Accounts Payable or Service Revenue), we capitalize its name.

The basic form of any T-account is as follows:

Periodically, the accounts are totaled to arrive at balances. For each account, the amounts entered on the debit side are totaled, and the amounts entered on the credit side are separately totaled. The difference between these two totals is the account's balance; the balance appears on the side that has the greater total. |

| TIP: | To journalize or journalizing refers to the process of recording a transaction or event in a journal. To post or posting refers to the transferring of information from journal entries to the appropriate ledger accounts. The posting phase of the recording process accumulates the effects of journalized transactions in the individual accounts. |

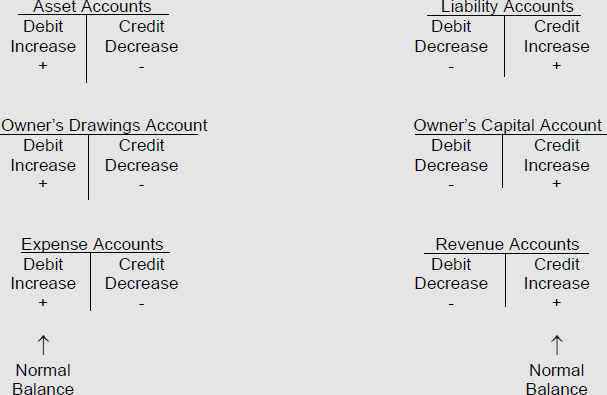

ILLUSTRATION 2-1

EXPANDED BASIC ACCOUNTING EQUATION AND DEBIT AND CREDIT RULES (L.O. 2)

| TIP: | A “+” indicates an increase and a “−” indicates a decrease. Therefore, a transaction which causes an increase in an asset is recorded by a debit to the related asset account; a transaction which causes a decrease in the same asset is recorded by a credit to the same account. |

| TIP: | Drill on the “debit and credit rules” until you can quickly and correctly repeat them. If you memorize the rules for an asset account, you can figure out the rules for all other types of accounts by knowing which rules are the opposite of the rules for assets and which are the same as the rules for assets. |

| TIP: | “Debit” is a term that simply refers to the left side of any account. Thus, the debit side of an account is always the left side. “Credit” is a word that simply refers to the right side of an account. Thus, the credit side of an account is always the right side of the account. The phrase “to debit an account” means to enter an amount on the debit side of an account. Abbreviations are Dr. and Cr. |

| TIP: | Total assets at December 31, 2014 = Total liabilities at December 31, 2014 + Owner's capital balance at January 1, 2014 − Owner's drawings during the year of 2014 + total Revenues earned during 2014 − total Expenses incurred during 2014. (Carefully notice the dates involved in the expanded equation.)

Owner's capital at January 1, 2014 − Owner's drawings for 2014 + Revenues for 2014 − Expenses for 2014 = Owner's capital balance at December 31, 2014. (Thus, owner's drawings, revenues, and expenses are subdivisions of the Owner's Capital account because they explain reasons why total owner's equity changes. Although all changes in owner's equity could be recorded in the Owner's Capital account, it is preferable to use separate accounts for each type of revenue, each type of expense, and owner's drawings so that detailed data on these items can be accumulated and reported.) Assets at December 31, 2014 = Liabilities at December 31, 2014 + Owner's Capital at December 31, 2014. |

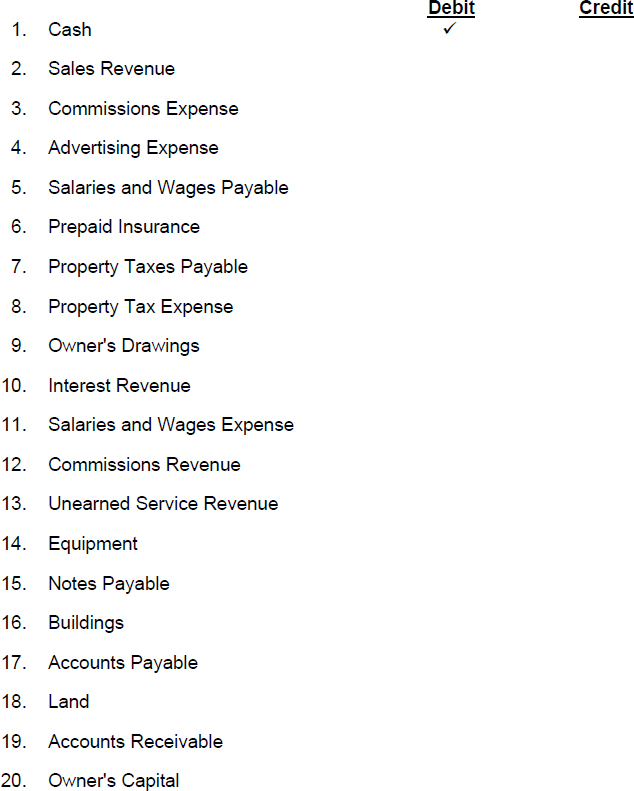

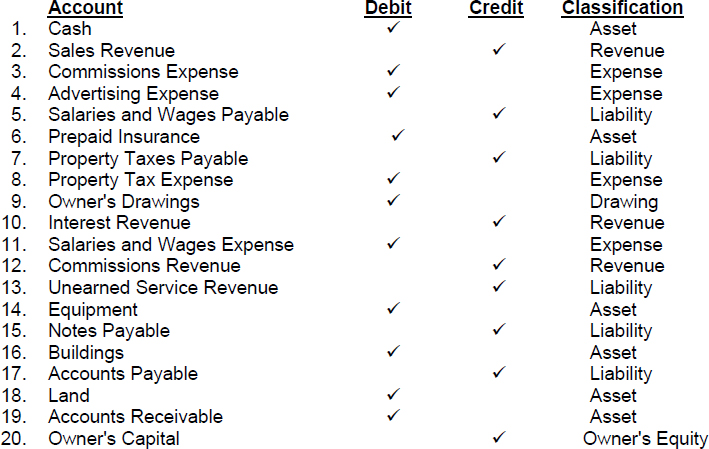

EXERCISE 2-1

Purpose: (L.O. 2) This exercise will test your understanding of the debit and credit rules.

A list of accounts appears below:

Instructions

For each account, put a check mark (![]() ) in the appropriate column to indicate if it is increased by an entry in the debit (left) side of the account or by an entry in the credit (right) side of the account. The first one is done for you.

) in the appropriate column to indicate if it is increased by an entry in the debit (left) side of the account or by an entry in the credit (right) side of the account. The first one is done for you.

| TIP: | In essence, you are being asked to identify the normal balance of each of the accounts listed. The normal balance of an account is the side where increases are recorded. |

SOLUTION TO EXERCISE 2-1

Approach: Determine the classification of the account (asset, liability, owner's capital, drawing, revenue or expense). Think about the debit and credit rules for that classification.

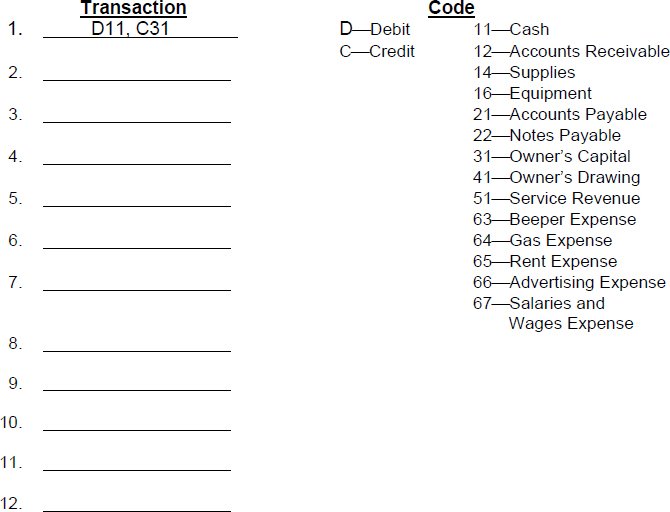

EXERCISE 2-2

Purpose: (L.O. 2, 4) This exercise will give you practice in applying the debit and credit rules.

A list of transactions appears below:

- Dan Harrier invests $1,000 cash in his new business, Ultimate Detailing.

- Purchases equipment for $600 cash.

- Purchases $300 of supplies on account.

- Rents a vehicle for the month and pays $250.

- Pays $100 for an ad in a local newspaper.

- Purchases gas for $20 on credit.

- Sells services for $200 cash.

- Sells services for $300 on account.

- Pays $90 wages for an assistant's work.

- Withdraws $80 for personal use.

- Pays for use of beeper service, $30.

- Borrows $2,000 from the Cash-N-Carry Bank in anticipation of expanding the business.

Indicate how you would record each transaction. What account would you debit and what account would you credit? Use the appropriate code designation. The first transaction is coded for you.

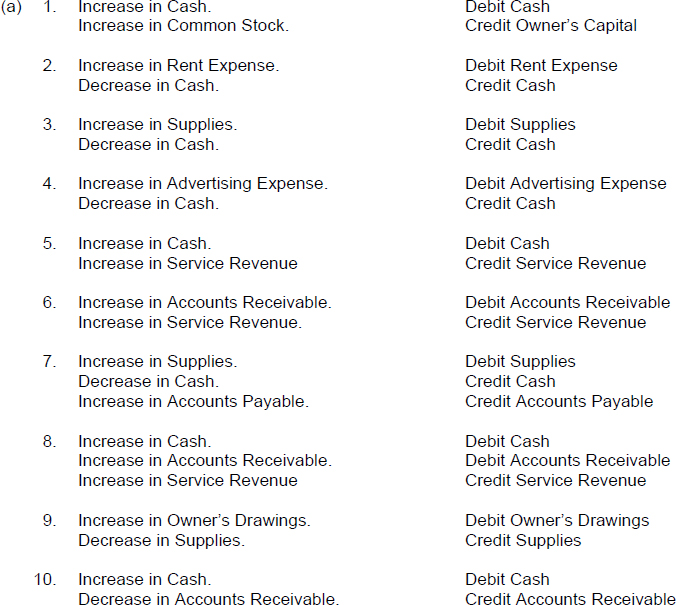

SOLUTION TO EXERCISE 2-2

Approach: Analyze each transaction to determine what items are increased or decreased. Translate that information into debit and credit language by applying the debit and credit rules (see Illustration 2-1). Visualize the resulting journal entry.

Transaction

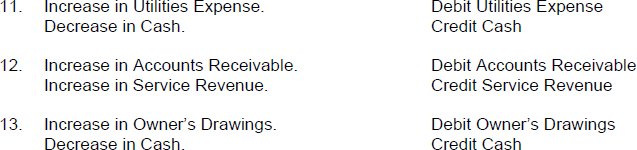

- D11, C31

- D16, C11

- D14, C21

- D65, C11

- D66, C11

- D64, C21

- D11, C51

- D12, C51

- D67, C11

- D41, C11

- D63, C11

- D11, C22

| TIP: | The account Supplies on Hand is often titled Supplies. |

| TIP: | The fourth transaction could be recorded by a debit to Prepaid Rent and a credit to Cash at the date the rent is paid (at the beginning of the rental month). Then, at the end of the rental month, the expired amount would be transferred to the expense account (this approach will be explained in Chapter 3). |

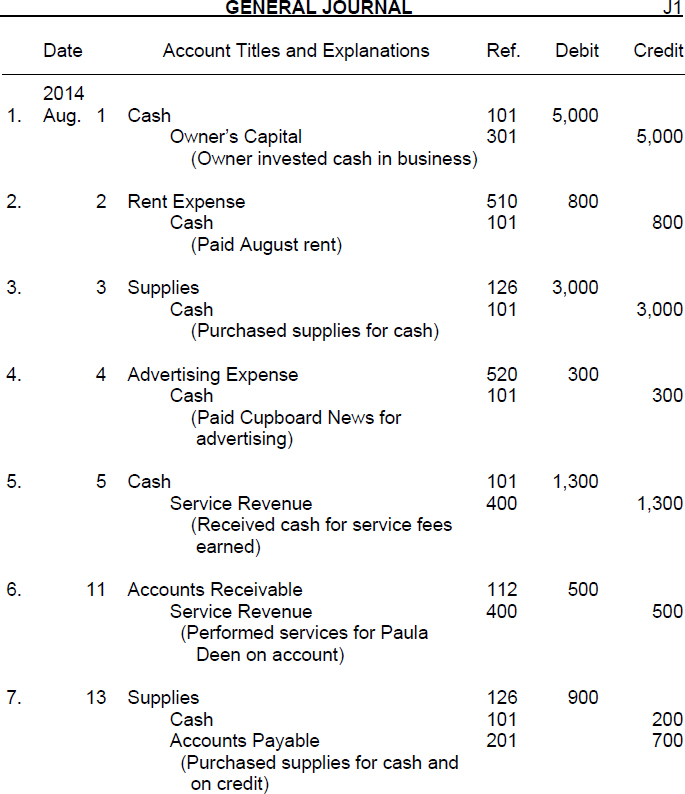

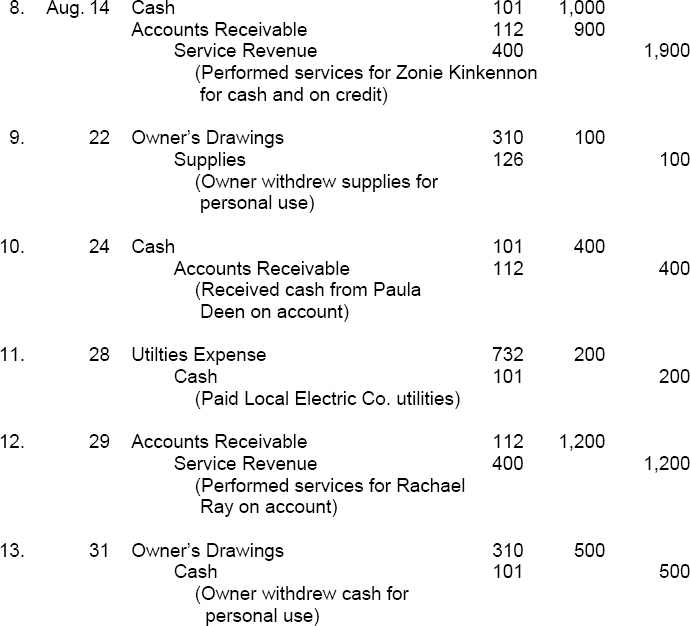

EXERCISE 2-3

Purpose: (L.O. 4) This exercise will illustrate how to record transactions in the general journal.

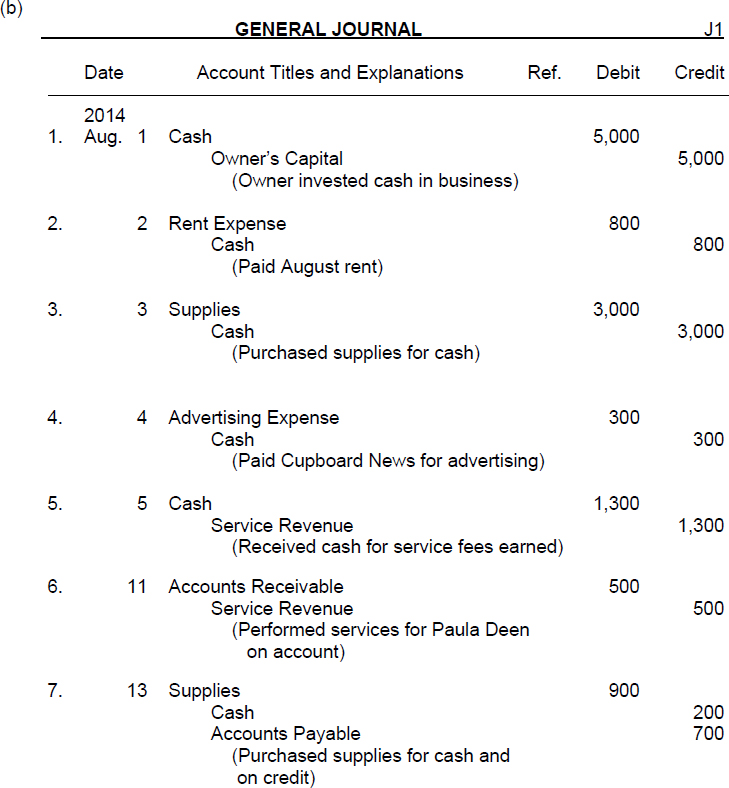

Transactions for the Mariah Carey Motorcycle Repair Shop (from Exercise 1-2) for August 2014 are repeated below.

| 1. | August 1 | Nick begins the business by depositing $5,000 of his personal funds in the business bank account. |

| 2. | August 2 | Nick rents space for the shop behind a strip mall and pays August rent of $800. |

| 3. | August 3 | Nick purchases supplies for cash, $3,000. |

| 4. | August 4 | Nick pays Cupboard News, a local newspaper, $300 for an ad appearing in the Sunday edition. |

| 5. | August 5 | Nick repairs a cycle for a customer. The customer pays cash of $1,300 for services rendered. |

| 6. | August 11 | Nick repairs a cycle for a customer, Paula Deen, on credit, $500. |

| 7. | August 13 | Nick purchases supplies for $900 by paying cash of $200 and charging the rest on account. |

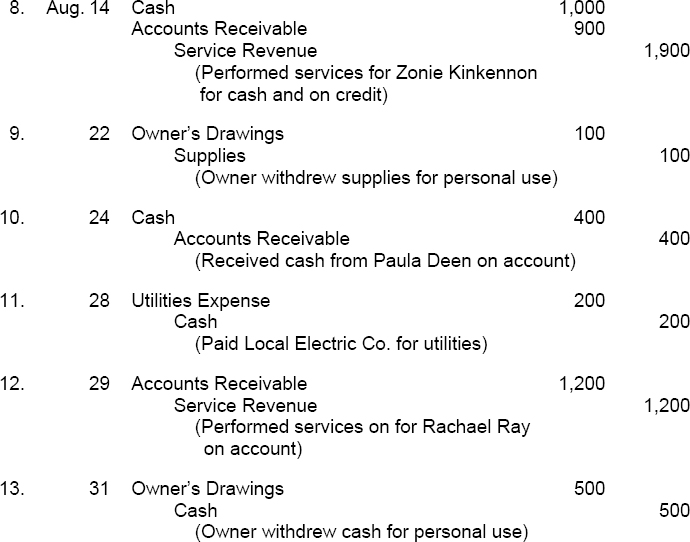

| 8. | August 14 | Nick repairs a Harley for Zonie Kinkennon, a champion rider, for $1,900. Nick collects $1,000 in cash and puts the rest on account. |

| 9. | August 22 | Nick takes home supplies from the shop that had cost $100 when purchased on August 3. |

| 10. | August 24 | Nick collects cash of $400 from Paula Deen. |

| 11. | August 28 | Nick pays $200 to Local Electric Co. for utilities incurred during the month of August. |

| 12. | August 29 | Nick repairs a cycle for Rachael Ray for $1,200 on account. |

| 13. | August 31 | Nick transfers $500 from the business bank account to his personal bank account. |

(a) Explain the impact of each transaction on the elements of the basic accounting equation and translate that into debit and credit forms.

(b) Journalize the transactions listed above. Include a brief explanation with each journal entry.

SOLUTION TO EXERCISE 2-3

Approach: Write down the effects of each transaction on the basic accounting equation. Think about the individual asset, liability, or owner's equity accounts involved. Apply the debit and credit rules to translate the effects into a journal entry.

| TIP: | Refer to the Solution to Exercise 1-2 for an analysis of the effects of the transaction on the individual components of the basic accounting equation. Refer to Illustration 2-1 for the summary of the debit and the credit rules. |

EXERCISE 2-4

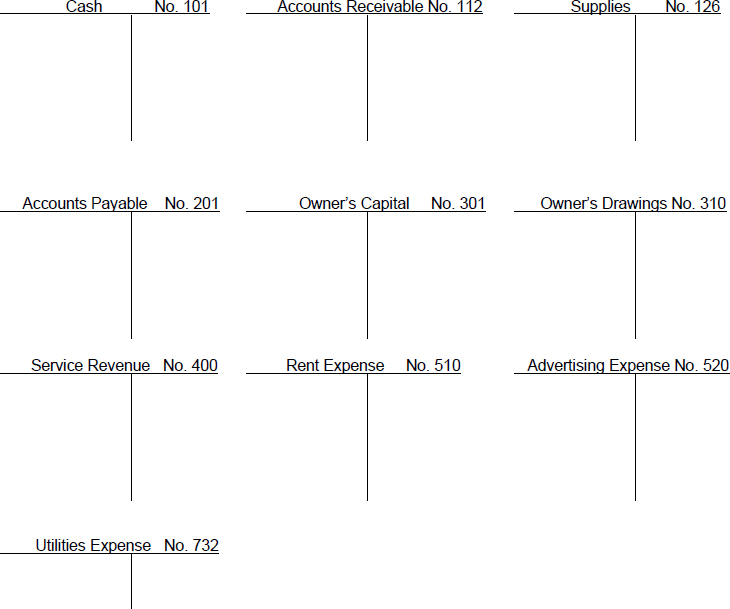

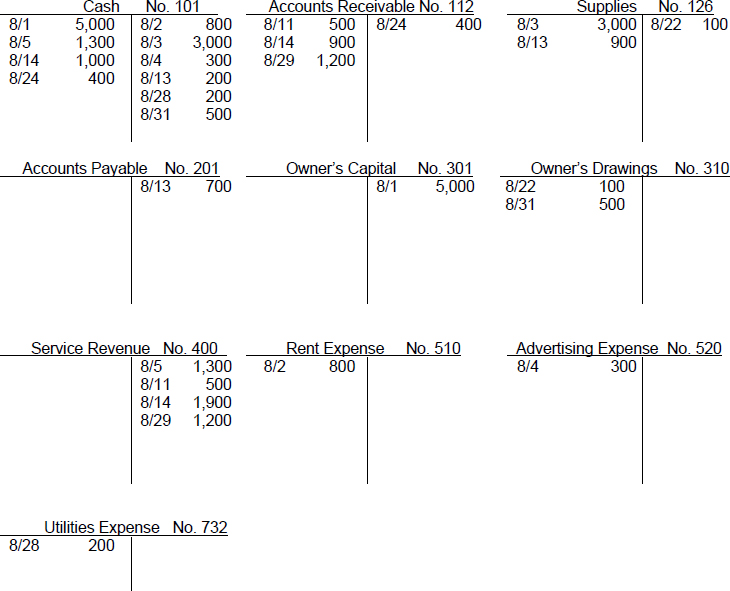

Purpose: (L.O. 6) This exercise will illustrate how to post transactions from the general journal to the general ledger.

Journal entries to record transactions for the Mariah Carey Motorcycle Repair Shop for August 2014 appear in the Solution to Exercise 2-3.

Instructions

Post the entries referred to above from the general journal to the following T-accounts. In the reference column of the journal, write the account number to which a debit or credit amount is posted.

SOLUTION TO EXERCISE 2-4

Explanation: Posting refers to the process of transferring journal entries to the ledger accounts. This phase of the recording process accumulates the effects of journalized transactions in the individual accounts. Posting involves the following steps:

- In the ledger, enter, in the appropriate columns of the account(s) debited, the date, journal page, and debit amount shown in the journal.

- In the reference column of the journal, write the account number to which the debit amount was posted.

- In the ledger, enter, in the appropriate columns of the account(s) credited, the date, journal page, and credit amount shown in the journal.

- In the reference column of the journal, write the account number to which the credit amount was posted.

The use of the reference column in the journal serves two purposes. It allows for:

(a) Cross referencing between the journal and the ledger which facilitates tracing of transactions from the journal to the ledger at a later date.

(b) A method of noting that the posting has been completed.

When T-accounts are used, such as in this exercise, the journal page of the debit or credit amount being posted is typically omitted in the ledger.

The general journal for the Mariah Carey Motorcycle Repair Shop should appear as follows when the posting process is completed:

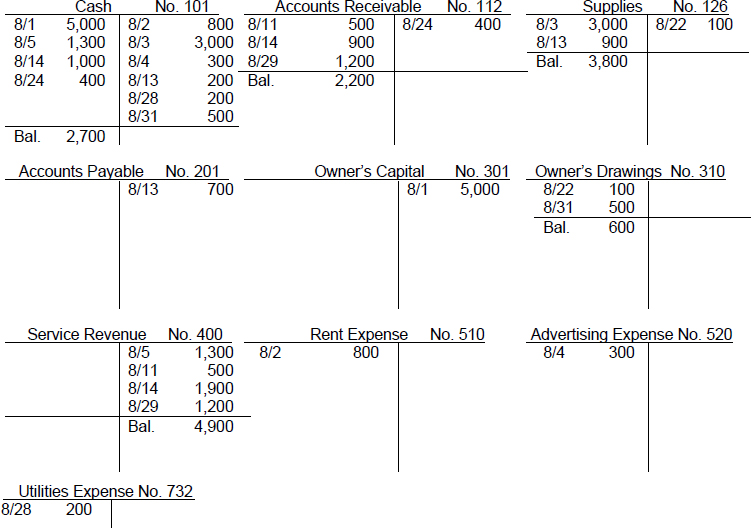

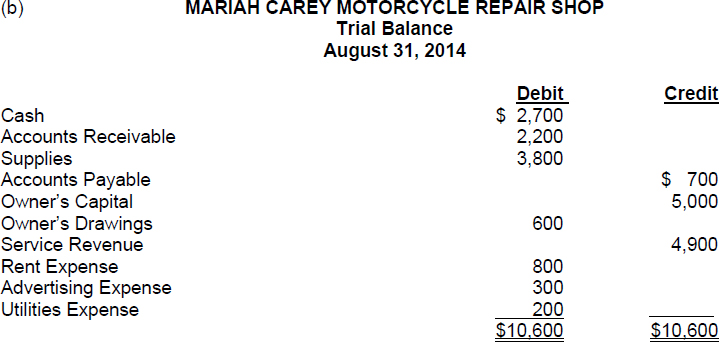

EXERCISE 2-5

Purpose: (L.O. 7) This exercise will (1) illustrate how to prepare a trial balance, and (2) will discuss the reasons for preparing a trial balance.

A trial balance is prepared after all transactions have been posted from the journal to the ledger.

Instructions

Refer to the Solution to Exercise 2-4

(a) Determine the balance of each account in the ledger.

(b) Prepare a trial balance.

(c) Describe a trial balance and list the reasons why it is to be prepared.

| TIP: | To balance a T-account, a balancing line is to be drawn in the T-account; the balance is entered beneath that line on the side of the account which has the largest total. (An account balance is determined by totaling the debits and totaling the credits and taking the difference between those two totals.) If an account has only one entry in it, no balancing line is needed because that one entry readily establishes the account's balance. |

SOLUTION TO EXERCISE 2-5

(c) A trial balance is a list of the accounts and their balances at a given point in time. A trial balance serves several purposes, including:

- It proves that the ledger is in balance (that is, that total debits equal total credits in the ledger accounts). If errors are made in journalizing and posting, they may be detected in the process of preparing a trial balance.

- It is a starting point for organizing the information to be reported on a company's financial statements.

| TIP: | Scan over Exercises 2-3, 2-4, and 2-5. Notice the logical progression of the steps in recording, classifying, and summarizing the transactions. In Exercise 2-3, each transaction had to be identified and analyzed in terms of its effects on various accounts. Then the transactions were recorded in the journal. In Exercise 2-4, the information in the journal is transferred (posted) to the ledger. Thus, all transactions that affect individual components of the basic accounting equation are summarized together. In Exercise 2-5, the accounts are balanced, and a trial balance is prepared which furthers the summarization process and checks for the maintenance of equality of debits and credits in the recording and posting phases. |

| TIP: | To sum a column of figures (such as the debt column of a trial balance) is sometimes referred to as to foot the column. When the summation is completed and the total is entered at the bottom of the column, the column is then said to be footed. |

EXERCISE 2-6

Purpose: (L.O. 7) This exercise will test your ability to identify the effects of errors that commonly occur in the process of recording and posting transactions. As you will see, some errors cause the accounts to be out of balance, thus quickly identifying the existence of an error. However, some errors do not cause an imbalance in the accounts and are more difficult to discover.

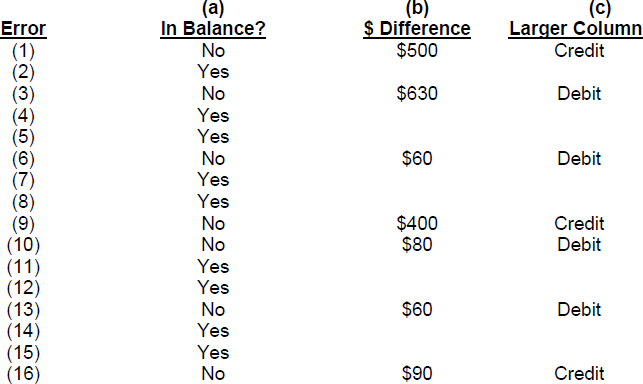

An inexperienced bookkeeper for Nip-N-Tuck Alteration Shop made the following errors in journalizing and posting the transactions that occurred during February 2014.

- The credit portion of a journal entry to record a $500 loan payment was posted to the ledger twice.

- A fictitious transaction was recorded in the journal for the amount of $300.

- A cash payment of $700 for rent was recorded in the journal by a debit of $700 to Rent Expense and a credit of $70 to Cash.

- A debit entry of $50 to the Accounts Receivable account was incorrectly recorded as a debit entry of $50 to the Cash account.

- A cash sale of $890 was incorrectly recorded in the journal as a cash sale of $980.

- The debit portion of a journal entry to record a $60 credit sale was posted to the ledger, but the credit portion of this entry was not posted.

- A $150 credit entry in the journal to the Accounts Payable account was posted as a credit to the Accounts Receivable account in the ledger.

- An entire entry in the journal to record the $75 payment to the City of Orlando for an annual business license fee was omitted in the posting process.

- A debit of $200 to the Equipment account was incorrectly posted as a $200 credit to the Equipment account.

- The debit portion of a journal entry to record a $80 sale on account was posted to the ledger twice.

- A $40 cash sale was completely omitted from the journal.

- A $45 cash sale was recorded in the journal twice.

- The balance in the Cash account was calculated incorrectly at $1,700. It should be $1,640.

- A payment on account of $190 was journalized and posted as a debit to Repairs and Maintenance Expense and a credit to cash for $190.

- A cash receipt of $80 from a customer on account was recorded twice in the journal.

- The debit portion of a journal entry to record a cash sale was correctly posted to the ledger for $120. The credit portion of the same journal entry was posted to the Sales account in the ledger for $210.

Instructions

For each error, indicate (a) whether or not the resulting trial balance will balance. If the trial balance will not balance, indicate (b) the amount of the difference, and (c) the trial balance column that will have the larger total. Consider each error separately. Use the following form, in which error (1) is given as an example.

SOLUTION TO EXERCISE 2-6

Approach: For each error:

(a) Determine if total debits equal total credits in the journal and in the ledger. An imbalance in debits and credits in the journal and posting errors may cause an imbalance of total debits and credits in the ledger.

(b) Determine the amount of difference and larger column if the trial balance is not in balance. Errors that will cause an imbalance in the trial balance include:

- Failure to record either the debit or credit portion (but not both portions) of a journal entry.

- Recording the debit and credit portions of a journal entry but for unequal amounts.

- Failure to post either the debit or credit portion of a journal entry.

- Posting either the debit or credit portion (but not both portions) of a journal entry more than once.

- Posting the debit and credit portions of a journal entry but for unequal amounts.

- Incorrect computation of a ledger account balance.

EXERCISE 2-7

Purpose: (L.O. 1 thru 7) This exercise will quiz you about terminology used in this chapter.

A list of accounting terms with which you should be familiar appears below:

| Account | Journalizing |

| Chart of accounts | Ledger |

| Compound entry | Normal balance |

| Credit | Posting |

| Debit | Simple entry |

| Double-entry system | T-account |

| General journal | Three-column form of account |

| General ledger | Trial balance |

| Journal |

Instructions

For each item below, enter in the blank the term that is described.

- _____________________A record of increases and decreases in specific asset, liability, and owner's equity items.

- _____________________The basic form of an account.

- _____________________A form with columns for debit, credit, and balance amounts in an account.

- _____________________A list of accounts and the account numbers which identify their relative location in the ledger.

- _____________________The right side of an account.

- _____________________The left side of an account.

- _____________________An account balance on the side where an increase in the account is recorded.

- _____________________An accounting record in which transactions are initially recorded in chronological order.

- ______________________An journal entry that involves three or more accounts (more than one debit and/or more than one credit).

- ______________________An journal entry that involves only two accounts (one debit and one credit).

- ______________________The most basic form of journal.

- ______________________The entering of transaction data in the journal.

- ______________________The entire group of accounts maintained by a company.

- ______________________The procedure of transferring journal entries to the ledger accounts.

- ______________________A list of accounts and their balance at a given time, usually at the end of the accounting period.

- ______________________The ledger that contains all of the asset, liability, and owner's equity accounts.

- ______________________A system that records, in appropriate accounts, the dual effect of each transaction.

SOLUTION TO EXERCISE 2-7

- Account

- T-account

- Three-column form of account

- Chart of accounts

- Credit

- Debit

- Normal balance

- Journal

- Compound entry

- Simple entry

- General journal

- Journalizing

- Ledger

- Posting

- Trial balance

- General ledger

- Double-entry system

ANALYSIS OF MULTIPLE-CHOICE TYPE QUESTIONS

- (L.O. 2) The left side of an account is called:

- debit.

- journal.

- credit.

- asset.

Explanation: The left side of any account is the debit side; the right side of any account is the credit side. (Solution = a.)

- (L.O. 2) Credits are used to record increases in:

- assets, revenues, liabilities, and owner's capital.

- expenses, liabilities, and owner's capital.

- revenues, owner's drawings, and assets.

- revenues, liabilities, and owner's capital.

Approach and Explanation: List the types of accounts which are increased by credits: liabilities, owner's capital, and revenues. Then look for the answer selection which matches your list. (Solution = d.)

- (L.O. 2) Which of the following accounts is increased by credits?

- Cash.

- Supplies.

- Prepaid Rent.

- Accounts Payable.

Approach and Explanation: List the types of accounts which are increased by credits: liabilities, owner's capital, and revenues. Identify each answer selection as an asset, liability, owner's capital, revenue or expense. Cash, supplies, and prepaid rent are all assets, and, thus, are increased by debits. Accounts payable is a liability and, thus, is increased by credits. (Solution = d.)

- (L.O. 4) The Ref. column of the journal is used to:

- cross reference entries in the ledger and to indicate that posting has been completed.

- indicate that entries have been properly posted to the financial statements.

- test the equality of debits and credits in the journal.

- indicate the initials of the employee who performed the posting process.

Explanation: The Ref. (Reference) column of the journal is left blank at the time a journal entry is made. At the time of posting, the ledger account number to which the amount is posted is placed in the Reference column to indicate what account received the posting. Thus, the Reference column in the journal is used to indicate whether posting has been completed and to what account an amount has been posted. (Solution = a.)

- (L.O. 4) The payment of rent for office space solely for the current period is recorded in the accounts by a debit to:

- Rent Expense and a credit to Cash.

- Rent Expense and a credit to Owner's Capital.

- Cash and a credit to Accounts Payable.

- Cash and a credit to Rent Expense.

Approach and Explanation: Do not read the answer selections until you analyze and journalize the transaction. Always start with the easiest part of the transaction. Cash was paid. Credit Cash to reduce its balance. Because the payment was for the rental of space for the current period, benefits do not extend beyond the current period; hence, an expense has been incurred. Debit Rent Expense to record the increase in expense. (Solution = a.)

- (L.O. 4) The journal entry to record the payment for three years' rent in advance involves a debit to:

- Rent Expense and a credit to Prepaid Rent.

- Owner's Capital and a credit to Cash.

- Prepaid Rent and a credit to Cash.

- Prepaid Rent and a credit to Owner's Capital.

Approach and Explanation: Analyze and journalize the transaction before you read the answer selections. Match your written response with the appropriate answer choice. Start with the easiest part of the transaction: a cash payment was made. Credit Cash to decrease the balance of that account. The payment is for benefits which are to extend beyond the current period; hence, an asset account should be increased (by a debit). The particular asset in this case is Prepaid Rent. (Solution = c.)

- (L.O. 4) The “book of original entry” is the:

- journal.

- ledger.

- trial balance.

- transactions book.

Approach: Complete the statement in the question stem before you look at the answer selections. Choose the selection which corresponds to your response. (Solution = a.)

- (L.O. 4) The receipt of cash from a customer for services to be provided in a future accounting period is recorded by a:

- debit to Cash and a credit to Unearned Service Revenue.

- debit to Cash and a credit to Service Revenue.

- debit to Unearned Service Revenue and a credit to Cash.

- debit to Service Revenue and a credit to Cash.

Approach and Explanation: Analyze the transaction and prepare the journal entry to record that transaction before you read the answer selections. The receipt of cash from a customer in advance of the earning of revenue causes the asset cash to increase and a liability (unearned service revenue) to increase. At a later time, the revenue will be earned; then the liability (unearned service revenue) will decrease and revenue will increase. (Solution = a.)

- (L.O. 5) Which statement is true regarding posting?

- Posting must be done at the end of each week.

- Posting must be done after the financial statements are prepared.

- Posting must be done immediately after the transaction is recorded in the journal.

- Posting may be done at any time but must be completed before financial statements are prepared.

Explanation: There is no set time to perform the posting process; however, financial statements cannot be prepared until all transactions are reflected in the accounts. Transactions are recorded in the accounts via the process of posting from the journal to the ledger. (Solution = d.)

- (L.O. 7) The debit column of a trial balance amounts to $78,000; the credit column also amounts to $78,000. Which error may still exist?

- A journal entry contains a correct debit amount and an incorrect credit amount.

- A debit entry to the Accounts Receivable account in the journal is incorrectly posted as a credit to the Accounts Receivable account in the ledger.

- The debit portion of a journal entry is posted to the ledger twice.

- A cash payment on account of $240 is incorrectly recorded as a cash payment of $420.

Approach and Explanation: Analyze each error (answer selection) and write down whether or not the error will cause the trial balance to be out of balance. Look for the selection which will not cause an imbalance in the trial balance (selection “d”). Both the debit and credit amounts recorded in the journal entry in selection “d” are in error. Selections “a”, “b”, and “c” all cause an imbalance in the trial balance. (Solution = d.)

- (L.O. 7) A transposition error in entering one ledger account balance on the trial balance will cause a difference figure in the trial balance totals that will be evenly divisible by:

- 2.

- 7.

- 9.

- 10.

Approach and Explanation: Set up an example for yourself to prove how this works. For instance, assume a $240 account balance is listed on the trial balance as $420. That error causes a difference of $180 which is divisible by 2, 9, and 10. Another example would be 9 entered for 90. The difference is 81 which is divisible by 9. Thus, the answer is narrowed down to the digit of 9. (Solution = c.)

- (L.O. 7) Which of the following errors will cause an imbalance in the trial balance?

- Omission of a transaction in the journal.

- Posting an entire journal entry twice to the ledger.

- Posting a credit of $720 to Accounts Payable as a credit of $720 to Accounts Receivable.

- Listing the balance of an account with a debit balance in the credit column of the trial balance.

Approach and Explanation: Analyze each error (answer selection) and write down whether or not the error will cause the trial balance to be out of balance. Look for the selection which will cause an imbalance (selection “d”). Selections “a”, “b”, and “c”, do not cause an imbalance in the trial balance. (Solution = d.)

- (L.O. 7) A trial balance that is in balance proves that:

- all entries have been entered in the journal correctly.

- total debits equal total credits in the ledger accounts.

- all entries have been posted from the journal to the ledger correctly.

- no significant errors exist in the ledger accounts.

Explanation: A number of errors can still exist even though a trial balance is in balance. A trial balance that balances only proves that there are equal amounts of debits and credits in the ledger accounts. (Solution = b.)