The last problem we're going to see in this chapter is about prediction in time. The standard name for these problems is time series analysis, since the prediction is made on descriptors extracted in the past; therefore, the outcome at the current time will become a feature for the prediction of the next point in time. In this exercise, we're using the closing values for several stocks composing the Dow Jones index in 2011.

Several features compose the dataset, but in this problem (to make a short and complete exercise) we're just using the closing values of each week for each of the 30 measured stocks, ordered in time. The dataset spans six months: we're using the first half of the dataset (corresponding to the first quarter of the year under observation, with 12 weeks) to train our algorithm, and the second half (containing the second quarter of the year, with 13 weeks) to test the predictions.

Moreover, since we don't expect readers to have a background in economics, we've tried to make things as simple as possible. In a real-life situation, such a prediction will be too simple to get money out of the market, but in this short example we've tried to keep the focus on the time series analysis, dropping all the other inputs and sources.

Note

The full description of this problem can be found at: https://archive.ics.uci.edu/ml/datasets/Dow+Jones+Index.

According to the readme file distributed along with the dataset, there are no missing values; therefore, the loading operation is quite straightforward:

In:

import matplotlib.pyplot as plt

%matplotlib inline

import numpy as np

import pandas as pd

dataset = pd.read_csv('./dji/dow_jones_index.data')Let's now try to decode the rows we're interested in (stock and close): it seems that the closing values are all strings, starting with $ and followed by the floating point value relative to the closing price. We should then select the correct columns and cast the closing price to the right data type:

In:

print(dataset.head())

Out:

quarter stock date open high low close volume

0 1 AA 1/7/2011 $15.82 $16.72 $15.78 $16.42 239655616

1 1 AA 1/14/2011 $16.71 $16.71 $15.64 $15.97 242963398

2 1 AA 1/21/2011 $16.19 $16.38 $15.60 $15.79 138428495

3 1 AA 1/28/2011 $15.87 $16.63 $15.82 $16.13 151379173

4 1 AA 2/4/2011 $16.18 $17.39 $16.18 $17.14 154387761

percent_change_price percent_change_volume_over_last_wk

0 3.79267 NaN

1 -4.42849 1.380223

2 -2.47066 -43.024959

3 1.63831 9.355500

4 5.93325 1.987452

previous_weeks_volume next_weeks_open next_weeks_close

0 NaN $16.71 $15.97

1 239655616 $16.19 $15.79

2 242963398 $15.87 $16.13

3 138428495 $16.18 $17.14

4 151379173 $17.33 $17.37

percent_change_next_weeks_price days_to_next_dividend

0 -4.428490 26

1 -2.470660 19

2 1.638310 12

3 5.933250 5

4 0.230814 97

percent_return_next_dividend

0 0.182704

1 0.187852

2 0.189994

3 0.185989

4 0.175029

In:

observations = {}

for el in dataset[['stock', 'close']].iterrows():

stock = el[1].stock

close = float(el[1].close.replace("$", ""))

try:

observations[stock].append(close)

except KeyError:

observations[stock] = [close]Let's now create a feature vector for each stock. In the simplest instance, it's just a row containing the sorted closing prices for the 25 weeks:

In:

X = []

stock_names = sorted(observations.keys())

for stock in stock_names:

X.append(observations[stock])

X = np.array(X)Let's now build a baseline: we can try the regressor on the first 12 weeks, and then test it by recursively offsetting the data—that is, to predict the 13th week, we use the first 12 weeks; to predict the value at the 14th week, we use 12 weeks ending with the 13th one. And so on.

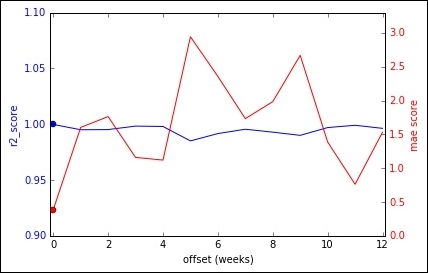

Note that, in this very simple approach, we build just a classifier for all the stocks, independently by their price, and we use both R2 and MAE to score our learner for each week of analysis (a score for the 13th week, one for the 14th, and so on). Finally, we compute mean and variance of these scores:

In:

from sklearn.linear_model import LinearRegression

from sklearn.metrics import r2_score, mean_absolute_error

X_train = X[:, :12]

y_train = X[:, 12]

regr_1 = LinearRegression()

regr_1.fit(X_train, y_train)

In:

plot_vals = []

for offset in range(0, X.shape[1]-X_train.shape[1]):

X_test = X[:, offset:12+offset]

y_test = X[:, 12+offset]

r2 = r2_score(y_test, regr_1.predict(X_test))

mae = mean_absolute_error(y_test, regr_1.predict(X_test))

print("offset=", offset, "r2_score=", r2)

print("offset=", offset, "MAE =", mae)

plot_vals.append( (offset, r2, mae) )

print()

print("r2_score: mean=", np.mean([x[1] for x in plot_vals]), "variance=", np.var([x[1] for x in plot_vals]))

print("mae_score: mean=", np.mean([x[2] for x in plot_vals]), "variance=", np.var([x[2] for x in plot_vals]))

Out:

offset= 0 r2_score= 0.999813479679

offset= 0 MAE = 0.384145971072

offset= 1 r2_score= 0.99504246854

offset= 1 MAE = 1.602203752

offset= 2 r2_score= 0.995188278161

offset= 2 MAE = 1.76248455475

offset= 3 r2_score= 0.998287091734

offset= 3 MAE = 1.15856848271

offset= 4 r2_score= 0.997938802118

offset= 4 MAE = 1.11955148717

offset= 5 r2_score= 0.985036566148

offset= 5 MAE = 2.94239117688

offset= 6 r2_score= 0.991598279578

offset= 6 MAE = 2.35632383083

offset= 7 r2_score= 0.995485519307

offset= 7 MAE = 1.73191962456

offset= 8 r2_score= 0.992872581249

offset= 8 MAE = 1.9828644662

offset= 9 r2_score= 0.990012202362

offset= 9 MAE = 2.66825249081

offset= 10 r2_score= 0.996984329367

offset= 10 MAE = 1.38682132207

offset= 11 r2_score= 0.999029861989

offset= 11 MAE = 0.761720947323

offset= 12 r2_score= 0.996280599178

offset= 12 MAE = 1.53124828142

r2_score: mean= 0.99489000457 variance= 1.5753065199e-05

mae_score: mean= 1.64526895291 variance= 0.487371842069On the 13 testing weeks, the R2 is 0.99 on average (with a variance of 0.0000157) and the MAE is 1.64 on average (with a variance of 0.48). That's the baseline; let's plot it:

In:

fig, ax1 = plt.subplots()

ax1.plot([x[0] for x in plot_vals], [x[1] for x in plot_vals], 'b-')

ax1.plot(plot_vals[0][0], plot_vals[0][1], 'bo')

ax1.set_xlabel('test week')

# Make the y-axis label and tick labels match the line color.

ax1.set_ylabel('r2_score', color='b')

for tl in ax1.get_yticklabels():

tl.set_color('b')

ax1.set_ylim([0.9, 1.1])

ax2 = ax1.twinx()

ax2.plot([x[0] for x in plot_vals], [x[2] for x in plot_vals], 'r-')

ax2.plot(plot_vals[0][0], plot_vals[0][2], 'ro')

ax2.set_ylabel('mae score', color='r')

for tl in ax2.get_yticklabels():

tl.set_color('r')

ax2.set_ylim([0, 3.3])

plt.xlim([-.1, 12.1])

plt.show()

Out:

Are we sure that the value of 12 weeks ago is still a good predictor for the current week? Let's now try to improve our scores by decreasing the training weeks. As an additional advantage, we will also have more training data. Let's try using 5 (a little more than a month):

In:

training_len = 5

X_train_short = X[:, :training_len]

y_train_short = X[:, training_len]

for offset in range(1, 12-training_len):

X_train_short = np.vstack( (X_train_short, X[:, offset:training_len+offset]) )

y_train_short = np.concatenate( (y_train_short, X[:, training_len+offset]) )

In:

regr_2 = LinearRegression()

regr_2.fit(X_train_short, y_train_short)

In:

plot_vals = []

for offset in range(0, X.shape[1]-X_train.shape[1]):

X_test = X[:, 12-training_len+offset:12+offset]

y_test = X[:, 12+offset]

r2 = r2_score(y_test, regr_2.predict(X_test))

mae = mean_absolute_error(y_test, regr_2.predict(X_test))

print("offset=", offset, "r2_score=", r2)

print("offset=", offset, "MAE =", mae)

plot_vals.append( (offset, r2, mae) )

print()

print("r2_score: mean=", np.mean([x[1] for x in plot_vals]), "variance=", np.var([x[1] for x in plot_vals]))

print("mae_score: mean=", np.mean([x[2] for x in plot_vals]), "variance=", np.var([x[2] for x in plot_vals]))

Out:

offset= 0 r2_score= 0.998579501272

offset= 0 MAE = 0.85687189133

offset= 1 r2_score= 0.999412004606

offset= 1 MAE = 0.552138850961

offset= 2 r2_score= 0.998668959234

offset= 2 MAE = 0.941052814674

offset= 3 r2_score= 0.998291291965

offset= 3 MAE = 1.03476245234

offset= 4 r2_score= 0.997006831124

offset= 4 MAE = 1.45857426198

offset= 5 r2_score= 0.996849578723

offset= 5 MAE = 1.04394939395

offset= 6 r2_score= 0.998134003499

offset= 6 MAE = 1.05938998285

offset= 7 r2_score= 0.998391605331

offset= 7 MAE = 0.865007491822

offset= 8 r2_score= 0.999317752361

offset= 8 MAE = 0.607975744054

offset= 9 r2_score= 0.996058731277

offset= 9 MAE = 1.62548930127

offset= 10 r2_score= 0.997319345983

offset= 10 MAE = 1.2305378204

offset= 11 r2_score= 0.999264102166

offset= 11 MAE = 0.649407612032

offset= 12 r2_score= 0.998227164258

offset= 12 MAE = 1.020568135

r2_score: mean= 0.998116990138 variance= 9.8330905525e-07

mae_score: mean= 0.995825057897 variance= 0.0908384278533With this approach, both R2 and MAE have improved, on average, and their variance is perceptibly lower:

In:

fig, ax1 = plt.subplots()

ax1.plot([x[0] for x in plot_vals], [x[1] for x in plot_vals], 'b-')

ax1.plot(plot_vals[0][0], plot_vals[0][1], 'bo')

ax1.set_xlabel('test week')

# Make the y-axis label and tick labels match the line color.

ax1.set_ylabel('r2_score', color='b')

for tl in ax1.get_yticklabels():

tl.set_color('b')

ax1.set_ylim([0.95, 1.05])

ax2 = ax1.twinx()

ax2.plot([x[0] for x in plot_vals], [x[2] for x in plot_vals], 'r-')

ax2.plot(plot_vals[0][0], plot_vals[0][2], 'ro')

ax2.set_ylabel('mae score', color='r')

for tl in ax2.get_yticklabels():

tl.set_color('r')

ax2.set_ylim([0, 2.2])

plt.xlim([-.1, 12.1])

plt.show()

Out:

Since the approach seems to be working better, let's now try to grid-search the best training length, spanning from 1 to 12:

In:

training_lens = range(1,13)

models = {}

for training_len in training_lens:

X_train_short = X[:, :training_len]

y_train_short = X[:, training_len]

for offset in range(1, 12-training_len):

X_train_short = np.vstack( (X_train_short, X[:, offset:training_len+offset]) )

y_train_short = np.concatenate( (y_train_short, X[:, training_len+offset]) )

regr_x = LinearRegression()

regr_x.fit(X_train_short, y_train_short)

models[training_len] = regr_x

plot_vals = []

for offset in range(0, X.shape[1]-X_train.shape[1]):

X_test = X[:, 12-training_len+offset:12+offset]

y_test = X[:, 12+offset]

r2 = r2_score(y_test, regr_x.predict(X_test))

mae = mean_absolute_error(y_test, regr_x.predict(X_test))

plot_vals.append( (offset, r2, mae) )

fig, ax1 = plt.subplots()

ax1.plot([x[0] for x in plot_vals], [x[1] for x in plot_vals], 'b-')

ax1.plot(plot_vals[0][0], plot_vals[0][1], 'bo')

ax1.set_xlabel('test week')

# Make the y-axis label and tick labels match the line color.

ax1.set_ylabel('r2_score', color='b')

for tl in ax1.get_yticklabels():

tl.set_color('b')

ax1.set_ylim([0.95, 1.05])

ax2 = ax1.twinx()

ax2.plot([x[0] for x in plot_vals], [x[2] for x in plot_vals], 'r-')

ax2.plot(plot_vals[0][0], plot_vals[0][2], 'ro')

ax2.set_ylabel('mae score', color='r')

for tl in ax2.get_yticklabels():

tl.set_color('r')

ax2.set_ylim([0, max([2.2, 1.1*np.max([x[2] for x in plot_vals])])])

plt.xlim([-.1, 12.1])

plt.title("results with training_len={}".format(training_len))

plt.show()

print("r2_score: mean=", np.mean([x[1] for x in plot_vals]), "variance=", np.var([x[1] for x in plot_vals]))

print("mae_score: mean=", np.mean([x[2] for x in plot_vals]), "variance=", np.var([x[2] for x in plot_vals]))

Out:

... [images are omitted] ...

results with training_len=1

r2_score: mean= 0.998224065712 variance= 1.00685934679e-06

mae_score: mean= 0.95962574798 variance= 0.0663013566722

results with training_len=2

r2_score: mean= 0.998198628321 variance= 9.17757825917e-07

mae_score: mean= 0.969741651259 variance= 0.0661101843822

results with training_len=3

r2_score: mean= 0.998223327997 variance= 8.57207677825e-07

mae_score: mean= 0.969261583196 variance= 0.0715715354908

results with training_len=4

r2_score: mean= 0.998223602314 variance= 7.91949263056e-07

mae_score: mean= 0.972853132744 variance= 0.0737436496017

results with training_len=5

r2_score: mean= 0.998116990138 variance= 9.8330905525e-07

mae_score: mean= 0.995825057897 variance= 0.0908384278533

results with training_len=6

r2_score: mean= 0.997953763986 variance= 1.14333232014e-06

mae_score: mean= 1.04107069762 variance= 0.100961792252

results with training_len=7

r2_score: mean= 0.997481850128 variance= 1.85277659214e-06

mae_score: mean= 1.19114613181 variance= 0.121982635728

results with training_len=8

r2_score: mean= 0.99715522262 variance= 3.27488548806e-06

mae_score: mean= 1.23998671525 variance= 0.173529737205

results with training_len=9

r2_score: mean= 0.995975415477 variance= 5.76973840581e-06

mae_score: mean= 1.48200981286 variance= 0.22134177338

results with training_len=10

r2_score: mean= 0.995828230003 variance= 4.92217626753e-06

mae_score: mean= 1.51007677609 variance= 0.209938740518

results with training_len=11

r2_score: mean= 0.994520917305 variance= 7.24129427869e-06

mae_score: mean= 1.78424593989 variance= 0.213259808552

results with training_len=12

r2_score: mean= 0.99489000457 variance= 1.5753065199e-05

mae_score: mean= 1.64526895291 variance= 0.487371842069The best trade-off is with training_len=3.

As you've seen, in this example we didn't normalize the data, using stocks with high and low prices together. This fact may confuse the learner, since the observations don't have the same center. With a bit of preprocessing, we may obtain better results, applying a per-stock normalization. Can you think what else could we do, and how could we test the algorithm?