3

WHY YOU NEED A “CHICKEN”

The Rewards and Risks of Rental Property

So, what’s with all the talk of chickens and eggs? Well, it’s simple. Just as chickens provide eggs day after day, income-producing rental properties provide cash flow month after month. If you aim to retire one day, and if you won’t have a pension to provide stable monthly income, you are going to need some monthly eggs. Sure, one big fat nest egg would also be nice, if you have that luxury. But as we’ve already discussed, you can never be totally sure how long that nest egg will last you. This means living in constant anxiety of the possibility that it could run out, as well as possibly having to live with the consequences of it actually running out. Best-case scenario, it doesn’t run out during your lifetime, but you may have little left over to pass on to your surviving spouse or your kids.

![]()

Rental property is the “pension” for those who don’t have a pension.

K. KAI ANDERSON

On the other hand, if you have little (or big) eggs streaming into your bank account every month, then you know exactly how long they will last. Those eggs will last until you sell your chicken. They can literally last forever.

Once you pay off your mortgages, the monthly income is available to use any way you like. If you pay off your mortgage sooner, the income could be your college savings plan, as it is ours. It could also mean early retirement, which is also part of our plan!

As with any type of investment, there are benefits as well as risks to owning rental property. After spending a moment to stress the importance of diversification, this chapter delves into the benefits and risks related to investing in real estate. In addition, since the risks are of a different breed than the risks in the stock market, I will also share some tips for how to reduce their chances of occurring and how to bounce back if they do.

BENEFITS OF RENTAL PROPERTY

There are many benefits to investing in real estate for the long term. While you must wait for some of these benefits, you get to enjoy many of them right away. The benefits you often enjoy right away include lowering the amount of income tax you currently pay (depending on your income) and creating a small amount of cash flow (after paying your mortgage principal, interest, and other expenses) to save, live off of, or reinvest. These aspects will be covered in detail in the following section of this chapter. The other benefits are less tangible. They include pride in ownership and the confidence that comes with that. They also include the peace of mind in knowing that you have created—with your own work—a safety net for your retirement and your older years in general.

In terms of the benefits you enjoy later on, the main one is serious cash flow resulting from having paid off your mortgage. Add to that the possible scenario of escalating real estate values and upward-trending rental rates over time. For a nominal entry fee on your part, you can eventually own—free and clear—an asset that is worth a serious chunk of change that provides steady income month after month. These now-and-later benefits are listed in Table 3.1.

TABLE 3.1. NOW-AND-LATER BENEFITS OF OWNING RENTAL PROPERTY

NOW |

LATER (ONCE MORTGAGE IS PAID OFF) |

Modest cash flow |

Serious cash flow |

Lower current income taxes |

Increased net worth |

Ownership of an asset that can be refinanced, to extract money, if needed |

Ownership of a non-liquid asset to sell or refinance if/when needed |

Pride in ownership |

Diversification beyond virtual bank accounts and virtual assets |

Peace of mind from having created a retirement safety net |

Diversification beyond stock market–based retirement accounts |

Benefit #1: Rentals Are a Way to Not Put “All Your Eggs in One Basket”

Diversification is the number one reason for owning at least one rental as a part of your long-term plan. The myth of mutual funds is that you are diversified. It may be true that you are somewhat diversified across different dividend- and non-dividend-paying stocks, bonds, and REITs. However, keep in mind that if all your savings are in virtual assets that rely on buying at one price and selling at a higher one to be profitable, then you are not truly diversified. To be truly diversified, you need to think beyond Wall Street. You need to think Main Street, or First Street, or even Pickle Street. In other words, think real estate.

Rental property is important to diversification for many reasons. For starters, the up–down cycles in real estate values don’t always line up with those of the financial markets. In fact, using data from the 1800s to the present, many economists agree that—while difficult to measure—real estate cycles often last about eighteen years.1,2,3,4 If this is accurate, then the next great dip in real estate values can be expected in roughly the year 2025. Meanwhile, opinions and theories on stock-market cycles are more variable with theorized cycles ranging from just a couple of years to roughly seven years to many years.5,6,7 Stock-market “day traders” can often see four or more cycles in a day.8

Owning rental real estate can protect you, and even help you thrive, regardless of what happens in the economy. More importantly, real estate is tangible. People will always need homes, meaning that the rental market demand will endure even if housing values go down. The long-term investors with tenants were relatively spared in the real estate crash that began in 2007. In fact, many landlords claim that the rental market had never been stronger. The sad truth was that during these hard times those who lost their homes to foreclosure were suddenly in need of rental housing.

Those who suffered the most when the real estate bubble popped fall into three main groups. The first group includes new-home buyers who were deemed “subprime” by mortgage companies but were given so-called “creative” mortgages anyway. They were deemed subprime because they would not have been able to afford their homes using a conventional thirty-year mortgage. As graphically demonstrated in the movie The Big Short, these individuals were intentionally and deceptively lured into mortgages with low and seemingly affordable initial payments, which escalated to unaffordable levels after a period of time. See chapter 8 for more information on these dangerous types of mortgages.

The second group of people who suffered in the housing crisis were existing homeowners who had tapped their home equity by refinancing or opening up lines of credit to purchase items or experiences. The burn came when some kind of hardship, like job loss or divorce, made it difficult to make the higher payments required by their new mortgage. Then, once home values plummeted below the amount financed, it became impossible for homeowners to sell those properties.

The third group who suffered in the crashing real estate market were the “flippers” and the “fix-and-flippers.” These are the individuals who had purchased a house either in hopes of riding the tide of appreciation or with plans to renovate and sell (i.e., fix and flip). They purchased at one price and hoped during those intoxicating days of double-digit appreciation that they would be able to sell a short time later at a higher price. Unfortunately, this plan was similar to those who buy a stock or mutual fund at one price and hope to sell for a higher price not too far down the road. When the music of the real estate market stopped, and especially if the home was midway through renovation and not rentable in its current state, these individuals were left holding the hot potato and got burned.

All three sets of people who suffered the most in the housing crisis were banking on appreciation. When you invest in real estate in the form of rental property held for the long term, you don’t bank on appreciation. Appreciation is a nice fringe benefit; however, the golden eggs are the cash flow, which brings us to Benefit #2.

Benefit #2: Rentals Provide Golden “Eggs” as Cash Flow

As we discussed in chapter 2, the number one threat to the nest-egg way of planning for retirement is the threat of running out of money. And the number one advantage of rentals is the antithesis of this threat: Rentals provide a steady, indefinite stream of income for you, month after month. Well maintained and well managed, they never run out.

In preparing for retirement, we are almost always asked to estimate the total amount of money that we think we’ll need once we stop working. The answer to this often-overwhelming question is usually calculated from a formula that is based on many different assumptions and questions. If you are using an online calculator, you may end up guessing the answers to these questions. For example, how are we to know what the actual rate of return will end up being on our investments? And should that number account for the impact of mutual-fund and financial-adviser fees, taxes, and conflicted financial advice as discussed in chapter 2? How are we to know what the rate of inflation will be after we stop working? And can we possibly know exactly how long we will live or how much we’ll need to spend on our health, housing, and leisure needs in retirement? With all this ambiguity, the expectation that we could get within a realistic ballpark estimate of our ideal retirement age, or the amount of money we’ll need to safely retire, is almost preposterous.

The thing is, these calculations are based on taking our projected life expectancy and working backward according to how much we expect to spend in the latter third of our lives, and how much we expect to have saved up at different points. The end result, our optimal retirement age, can be quite depressing.

![]()

Obstacles are those frightful things you see when you take your eyes off the goal.

HENRY FORD

Industrialist and originator of the five-day

workweek (1863–1947)

Instead of working backward, try working forward. As Kim Kiyosaki, author of Rich Woman and It’s Rising Time, recommends, try thinking about your “number” in a new way. Instead of calculating backward from death to retirement age to present day, calculate forward to see how long your money will last if you had to stop working right now.

Suppose you have $30,000 saved up in your 401(k) and $3,000 worth of expenses per month. To figure out how many months you could last on these savings, simply divide $30,000 by $3,000/month and your result is ten months. Ouch! This example shows, in plain numbers, the problem with the nest egg. If you are going to stop earning a paycheck, then you are going to need your money to last longer than ten months . . . a lot longer.

Even if you’ve saved up $300,000, if you spend at the rate of $3,000 per month, your money will last you only a hundred months, or a mere 8.33 years! If you have a million dollars, $3,000 per month in spending will last you 27.78 years. In this last scenario, if you retire at age 62, then your funds will expire just before you turn 90. Then what? Note that these calculations are rough and do not factor in any growth (or loss) if the funds are held in the stock market, nor do they adjust for inflation or the time value of money.

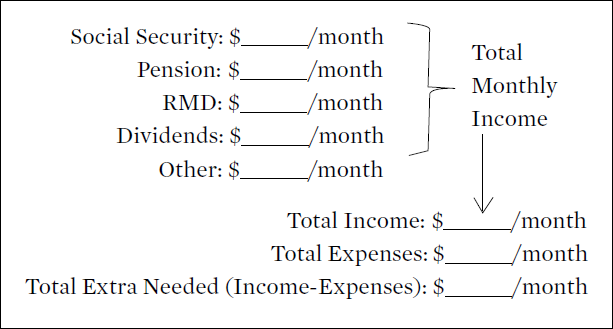

Now let’s calculate in a forward direction how much you’ll really need. Add up all your sources of monthly income that you expect to receive after you stop working: Social Security, pension, RMD, dividends from any dividend-producing asset, and anything else that might be a part of your unique picture. To assist with the Social Security and RMD lines, simply refer back to the online resources that I provided in chapter 1.

Keep in mind that it is best not to use the “Other” line to divide up your savings into a monthly amount, because the point of this exercise is to calculate the amount of reliable monthly income you can expect to receive, even if you were to live forever. The only way to get monthly income from savings would be to know how long you’ll live in order to know how to divide the number. Plus, keeping your savings out of this calculation will give you a conservative sense of the monthly income you’ll need, allowing you to reserve your savings for emergencies and larger purchases. See Figure 3.1.

Add up the income streams to get the total income that you expect to receive each month and enter this on the “Total Income” line. On the “Total Expenses” line, simply use your current monthly income or your current monthly expenses as a rough guide for what you will need in retirement. Even though you may be inclined to subtract your home mortgage payment from this amount (if you expect to have it paid off by the time you plan to retire), you may want to be conservative and keep it in. The reason: There’s always something. Even if your mortgage is paid off, you may have some other expense in its place, like another mortgage, long-term care expenses, and so forth.

FIGURE 3.1. CALCULATING TOTAL EXTRA NEEDED (PER MONTH)

Finally, subtract your “Total Expenses” from your “Total Income” to come up with your “Total Extra Needed.” This is the amount of additional monthly income you will need in order to achieve financial comfort in retirement. You’ll learn about this in chapter 5; however, this is what I call the “Level II Goal.” Also in chapter 5, I share the notion of the “Level III Goal” of complete financial self-sufficiency once the mortgages are paid off. To set yourself up for the Level III Goal, you’ll want to enter “0” on the Total Income line. This makes all of your other expected sources of income a bonus. If any of these sources dry up or vanish, for any reason, then you will still have the monthly income from your rental properties.

Once you determine the amount of cash flow you need, you can play around with the modifiable Cash Flow Analysis (CFA) Tool at www.GetaChicken.com. Table 3.2 shows a static example of the CFA Tool. The specific number of properties for the Level II or III Goal depends on how much monthly income you expect to need in retirement and how much income you expect your properties to produce. The Level II Goal has the added variable of how much income from other sources you expect to receive.

As an oversimplified example, imagine that your calculation informs you that to be comfortable (the Level II Goal), your “Total Extra Needed” is $2400 per month, and that the properties you are able to buy will generate $803 each month after all expenses, but not including mortgage principal and interest (the “NOI” line on Table 3.2). In this example, assuming the mortgages are paid off by the time you retire, you will need three properties (or one multi-unit property) that generate $2400 per month in cash flow, to complement your other sources of income and provide the degree of financial comfort you seek. Keep in mind that property types and income-generating potentials vary by geographical region, so be sure to do your research using numbers that are relevant to your own market.

Just as cash flow wins the game of Monopoly, cash flow will also help you win the game of retirement. Money coming into your bank account every month is the key to reducing both worry and hardship, especially when it comes to leaving the workforce and giving up your salary for good. In fact, if you own rental property, you are not giving up your salary; you are merely trading the salary you receive from your employer to a salary that you receive from your property’s tenants.

TABLE 3.2. CASH FLOW ANALYSIS TOOL ($100,000, 20% DOWN, 30-YEAR)

No other investment has had as consistent and powerful an effect on the average person’s net worth as real estate ownership.

GARY KELLER

Founder of Keller Williams Realty and

author of The Millionaire Real Estate Investor

Benefit #3: Rentals Help You Build Your Net Worth

Net worth is defined as the sum of your assets minus the sum of your debts, though, as we discuss in chapter 4, not all debts are the same. Credit card debt and other “bad debt” must be deducted from your net worth. But “good debt,” for example a mortgage on a cash-flowing investment property, is more complicated. The way I see it, when it comes to good debt, net worth is like energy.

Do you remember learning about the two forms of energy back in your school days in science class? Not to give you an unpleasant flashback, but do you remember potential and kinetic energy? As a refresher, potential energy is stored energy (before being released) and kinetic energy is energy of motion (after being released). Potential energy results from work being performed against an object, like when you compress a spring. When the spring is released, the potential energy turns into the powerful kinetic energy of motion.

How does this connect to real estate and why is it so important? Well, imagine that you buy a cash-flowing rental property using the good debt of a mortgage. Like compressing a spring, you must do physical work to acquire and maintain that potential energy. During this time, the mortgage prevents the cash flow from being all that great. The length of time you hold that spring depends on the length of your mortgage. More rentals equate to a higher total value (and more work!) and greater levels of stored, potential energy. As you continue holding the spring, and as you gradually pay down the mortgage, this potential net-worth energy waits quietly for release. The moment the mortgage on a property is completely paid off is the moment that the passive net-worth energy is released and kinetic net-worth energy—the liberated cash flow—is experienced.

Benefit #4: Rentals Create Equity

Equity is defined as the difference between the amount a property is worth and the amount of debt you have on it. In shorthand, it is the property’s “value” minus your mortgage balance, or “principal.” It is an odd concept because it is based in part on hard numbers (the actual amount you owe at any given point in time) and in part on soft numbers (the amount you think it is worth at the same point in time).

When you first buy a property, you may have very little equity in it. However, as time progresses, your equity will gradually grow through the combined forces of paying down your principal and appreciation (assuming your property value does appreciate). As this happens, your actual net worth grows while your potential net-worth energy becomes closer to being released, as discussed in the previous section.

Even though equity is not actual money in your bank, more equity is always better because of the flexibility it affords. You can refinance to purchase more property. You can sell to make another large purchase, such as a vacation home. And, of course, once you own a property without a mortgage (“free and clear”), you can keep this new-kinetic net-worth energy as an uninhibited source of income.

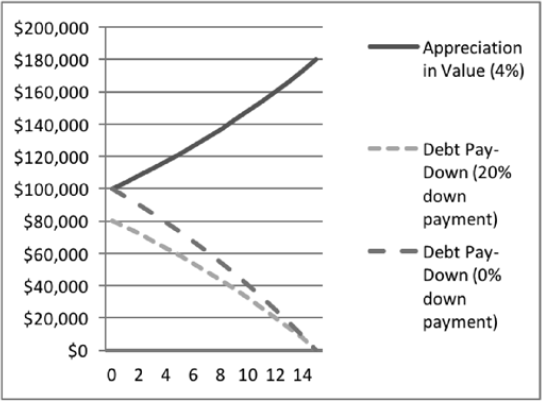

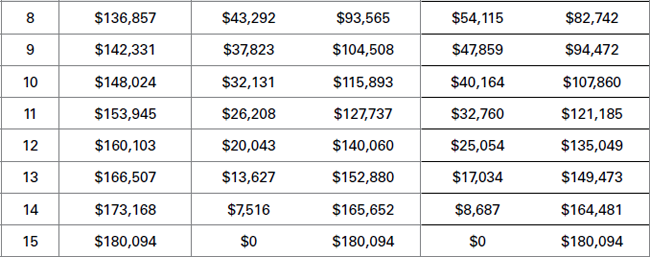

Figure 3.2 and the corresponding Table 3.3 show an example of how this works over time. As you look at Figure 3.2, focus on the spread between the solid line and each of the two dashed lines. The line that curves upward shows hypothetical appreciation of 4 percent per year. Remember that appreciation is to be considered a fringe benefit, not a guarantee. It’s the icing on the cake, but it is not the cake.

The two lines that arc downward are based on the hypothetical situation of paying off a $100,000 fixed-rate mortgage over fifteen years at 4 percent interest.‡ The lighter dashed line assumes a down payment of 20 percent. The darker dashed line assumes either that no down payment was made or that the property was purchased at roughly 20 percent below market value.

As you move along to the right, you can see that as you pay off your mortgage and assuming the property value increases at an average of 4 percent per year, the spread between the upper line and the two lower lines becomes quite wide. This spread represents your equity in the property. In the end, the property that you proudly and boldly took ownership of for twenty thousand dollars, or less, will have grown into a solidly income-producing asset worth $180,000 after fifteen years. (Note that in the situation of flat or even negative appreciation, you still come out as a winner due to the equity gained through debt pay-down.)

Before closing this section, I want to stress the dangers of interest-only mortgages, which are in part to blame for the housing and mortgage crisis of 2008. Interest-only mortgages come with substantial risk in the event that you need to refinance or sell due to changing priorities or circumstances in your life. For example, in Figure 3.1, with an interest-only mortgage your safety and/or gain would be completely reliant on the upper arc of appreciation. The lower two arcs would be nonexistent since you would not be paying down any of the principal. This might be fine in a world of guaranteed appreciation. However, remember that appreciation is not guaranteed. If the market becomes such that it is impossible to sell or refinance when you need to, and if all your equity depends on the upper arc of appreciation, then you would be in trouble.

As you’ll see in chapter 5, the Ultimate Goal is to pay your mortgage off completely and get to the end of one of the two lower arcs shown in Figure 3.2. The upper appreciation arc is largely out of your control but can be enhanced by maintaining and upgrading your property over the years.

FIGURE 3.2. NET RESULT OF ACTUAL DEBT PAY-DOWN ($100,000 MORTGAGE AMORTIZED OVER 15 YEARS AT 4% INTEREST) AND HYPOTHETICAL APPRECIATION ACROSS TWO DOWN PAYMENT SCENARIOS (0% AND 20%)

TABLE 3.3. ACTUAL DEBT PAY-DOWN ($100,000 MORTGAGE AMORTIZED OVER 15 YEARS AT 4% INTEREST) AND HYPOTHETICAL APPRECIATION ACROSS TWO DOWN PAYMENT SCENARIOS (0% AND 20%)

Benefit #5: Rentals Can Lower Your Taxes

When you work for a living, you pay taxes. However, in many situations, when you own rental properties, Uncle Sam pays you. Depending on your income, buy-and-hold real estate investing is one way you can actually reduce the amount you pay in income tax from your work, even while being taxed on the rental income you receive.

There are two ways owning a rental can help you at tax time. The first is through tax deductions. You can deduct your property taxes and mortgage interest, just as you can on a personal residence. Plus, you can write off all operating and maintenance expenses related to your property in the same way that a business owner can write off expenses related to running his or her business. Deductible expenses include property and landlord umbrella insurance, maintenance, repairs, marketing, and even meals over which you discuss the state of affairs with the rental. Remember to keep your receipts, track your expenses, and work with a good accountant to be sure you capture all your allowable deductions. Be sure to discuss these concepts with your CPA, too, so that you don’t miss out on any deductions. Also talk with your CPA because these benefits do not affect everyone equally; they vary by personal circumstance and income.

The second way investors benefit at tax time is through “depreciation.” Depreciation might sound like a bad thing: After all, it can mean the opposite of appreciation. However, in IRS language, it means tax break . . . whether or not your property goes down in value. Depreciation is a powerful, and—believe it or not—mandatory, tax incentive for owners of investment real estate to deduct the hypothetical wear and tear of the property (the structure, appliances, many of the materials such as tile, etc.). Land is not depreciable. I’ve provided a practical example of how depreciation works in the section on “Taxable Income” in the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide available at www.GetaChicken.com.

There are other tax advantages to owning rental property. For example, if you sell a property at a loss, you can take this as a deduction against your other earned income. This is different from selling stocks at a loss because these stock-related losses can only be applied to similar stock-related income. If all your stocks go down, and you don’t have income to report, you are limited in the extent to which you can take deductions.

Real estate also offers tax advantages over your typical savings account. If you happen to receive interest on your savings (though this hasn’t been possible in many years), you pay taxes on this growth at the same tax rate as your ordinary earned-income tax bracket. With real estate, as long as you’ve owned the property for at least a year, if you decide to sell your property you may pay a lower capital-gains rate than you do on your ordinary income taxes, though you have to pay back the amounts deducted in depreciation over the years. Another advantage is that you can use the advanced tax strategy called the “1031 Exchange” to trade up into a new investment property without having to pay taxes on the capital gains from the sale. See the section “Put Your Chickens to Work” in chapter 8 for more information on this and other advanced moves related to buying, selling, and trading property.

If you want to read all the tax rules yourself, right from the IRS, you can find them in the government document www.irs.gov/pub/irs-pdf/p527.pdf.9 However, for a much easier and more enjoyable read, check out Amanda Han and Matthew MacFarland’s book, The Book on Tax Strategies for the Savvy Real Estate Investor.

Benefit #6: Rentals Protect You from Inflation

Many of us were raised with the advice to save our money. I was, too. As a young teen, back when most banks were small, local banks, my parents took me on an adventure to our town bank, to open up my very first savings account. I had discovered the profession of babysitting and I was beginning to make some real money. It was the early ’80s, and there was actually an interest rate attached to my account. I remember literally watching my savings grow, dollar by dollar, even without adding extra money to the account!

Not so these days. As of the writing of this book, the United States has had near zero-percent interest rates on savings accounts for many years. Even certificates of deposit (CDs) are essentially useless in terms of growing your money over time.

This is where inflation comes in. Inflation is a term that quantifies the extent to which prices escalate from one year to the next, in the general economy, in a given country. It can be highly variable between countries and over time. For example, while prices of consumer goods in the United States inched up only 1.6 percent between 2001 and 2002, they skyrocketed 13.5 percent between 1979 and 1980.10

On average, prices tend to increase each year by about 2 to 3 percent over the year before.11 What this means for savings accounts these days is dire. If you put your money in a savings account that earns no interest, then this translates to a real-world interest rate of roughly negative 2 to 3 percent per year.

In contrast, consider rental property. Rental property that you purchase with a fixed-rate mortgage is a great way to protect yourself against inflation. This is because your payments are locked in place at the time you purchase or refinance your property. Your monthly payment stays constant as time goes on and as inflation is at play in the economy. Relative to the increasing costs of all your other expenses, your fixed-rate mortgage payment will, in essence, be going down.

Benefit #7: Rentals Boost Your Return on Investment (ROI)

Return on investment is a measure to help you decide how to get the biggest bang for your buck when you have money to invest. It can be helpful when you are trying to decide between a couple of different properties (as shown in the property evaluation section of the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide available at www.GetaChicken.com). It can also be useful if you are trying to decide between buying a rental property and putting money somewhere else—like in a stock, mutual fund, certificate of deposit (CD), or savings account. In this section, you will see how rental property compares with these other ways that you can invest your money, and even the old-fashioned method of hiding it under a mattress. Table 3.4 shows profoundly different rates of return based on the different ways you can hold your money.12 Table 3.4 also shows the impact of hypothetical 3 percent inflation on each savings method. While these are just annual rates of return, you can imagine the impact of these rates over many years.

Annual Cash-on-Cash Return is one measure of ROI. It is defined as the amount of money the asset generates in a year divided by the total amount paid out of pocket for the asset. For real estate, the “amount made” is your total annual cash flow (income-expenses). The “amount paid” is the total amount that you paid to acquire the property, including the down payment, closing costs, and expenses for repairs and upgrades.

Cash-on-Cash Return = Amount made/Amount paid

Recall from your middle school math lessons that the smaller your denominator (the amount paid), the larger your result. What this means is that the less you invest out of your own pocket, the higher your cash-on-cash return. Recall also that you can’t divide by zero; otherwise, the result shoots to infinity. What this means is that if you were to pay absolutely nothing for the property (including closing costs and repairs), then your cash-on-cash return would technically shoot the moon. This type of no-down-payment scenario is rare, but technically does occur when you convert a primary residence into a rental.

![]()

A money market may be the ultimate risk because it will likely lag inflation.

JOHN BOGLE

Founder of Vanguard and author of

The Clash of Cultures: Investment vs. Speculation

Financial risk is defined as the probability of losing money. This means that even though it may feel like the safest thing to do with your money would be to stuff it under the mattress or lock it away in a savings account, this is actually the further thing from the truth when it comes to growing your money. In comparison with other investment strategies, saving your money in a non-interest-bearing account is actually the “riskiest” strategy. And yet, as a side note, don’t confuse this method of saving with holding a stash of cash as an emergency fund for your rental properties and life in general. This is essential, and is covered in depth under Risk #4, later in this chapter.

Similar to a savings account, a money market account is, in theory, supposed to be a very low-risk investment, with the principal staying at its cash value. However, there are times when this is not the case. In 1994 and again in 2008, a phenomenon called “Breaking the Buck” occurred, in which a money-market fund’s investment income became so low that it did not cover its own operating expenses or investment losses, and the value of the account actually became worth less than the amount of money originally invested. It is called “Breaking the Buck” when the net value of one dollar in a money-market fund falls below one dollar.

TABLE 3.4. AVERAGE RATES OF RETURN BY INVESTMENT WITH AND WITHOUT ADJUSTMENT FOR 3% INFLATION*

INVESTMENT TYPE |

APPROXIMATE RATE OF RETURN |

INFLATION-ADJUSTED RATE OF RETURN |

Cash under the mattress |

0% |

–3%* |

Cash in the bank |

0% |

–3%* |

Money Market Funds |

0% |

–3%* |

Certificate of Deposit |

1% |

–2% |

Bond |

4% |

1% |

Low Risk Stocks |

5% |

2% |

Medium Risk Stocks |

9% |

6% |

High Risk Stocks |

15% |

12% |

Real Estate (25% down) |

17% |

14% |

Real Estate (20% down) |

19% |

16% |

Real Estate (0% down) |

Infinite |

Infinite |

*For the purpose of this table, the inflation rate is assumed to be 3 percent.13 Real estate purchase assumptions include purchase price of a $100,000, thirty-year term, self-managed property. See the Cash Flow Analysis (CFA) Tool in Table 3.2 and at www.GetaChicken.com. Rates do not reflect the impact of fund or broker fees (see Threat #3 in chapter 2, “Very Real Threats to a Very Fragile Egg”). Table data source: http://www.smareserves.com/why-3-inflation/.

RISKS OF INVESTING IN REAL ESTATE

As you can tell by now, I strongly believe that owning one or more cash-flowing rental properties is an important—if not essential—part of a truly diversified plan. Chapter 2 went into the many threats and risks of relying solely on retirement accounts and savings accounts. Now that we’re at this point, you’re probably wondering, “But what about all the risks involved with rental property? Surely real estate is risky, too!”

I’ll go into the risks and general downsides in this section. But before I do, I want to mention that risk in real estate is different from throwing your money into a mutual fund, closing your eyes, and hoping things turn out peachy. This is because you have a certain amount of control to prevent risks from manifesting in the first place. And if they do arise, you have a certain amount of control to recover, provided you have emergency funds and/or undesignated income from your salary that you can fall back on if necessary. That element of control might be daunting, but it can also be incredibly empowering. Read on and you’ll see exactly what I’m talking about.

Risk #1: The Tenant from Hell

Just as we can lessen our risk of developing some chronic diseases by eating well and exercising, we can lessen our risk of having a terrible tenant destroying our precious investment by doing a thorough tenant screening. And if we do wind up with the tenant from hell—like the one who fails to pay the rent on time, fails to clean, collects pets like others collect stamps, whose cats are apparently unable to find a clean litter box to do their business, and whose poor dogs were never taken out on walks so they did all their business in the basement (yes, we had that tenant!)—there are measures we can take to recover.

When this happened to us, we lost two months of rent during the time it took to clean and repair the property and re-rent it, though we had a security deposit for one of those months to lessen the sting. We had to hire someone to pull out all the carpet and refinish the hardwood floors underneath. And we—with the help of a clearly very dear friend along with my very loving mother who happened to be visiting at the time—pinched our noses and removed seemingly infinite amounts of dog and cat poop from the basement and back yard. Unbelievably gross, yes. But we were able to recover. And in the end, we possessed not only an upgraded property, but also an improved landlording IQ! We had become smarter about doing tenant screenings, and we had become stronger and more assertive as well. We learned to “just say ‘No’” to requests for “just one more cat”—or any cat, for that matter. In the end, we continued to own this incredible cash-flowing asset with a fifteen-year mortgage that will be paid off in time to cover our daughter’s college tuition before supplying us with a chunk of our future monthly retirement income. But from that point forward, we learned to never cut corners on the tenant screening process again.

The problem arose because I was excited by the fact that the potential tenant seemed “really nice.” Thanks to my disillusioning experience with this individual, I came up with the phrase: “Good eggs and bad eggs look the same on the outside.” The lesson here is to never be swayed by someone’s positive appearance or friendliness. Being taken advantage of isn’t always limited to the work of ill-meaning scam artists (who, by the way, often present themselves very well, too!). It can also happen when you cross paths with well-meaning people who find themselves taking on more rent (or pets!) than they can afford. Always do credit and background checks. For added layers of protection, use a month-to-month lease with the right to terminate, for any reason, with thirty days’ notice.

Unfortunately, it is this kind of situation that spreads the fear of landlording. I’m pretty sure we grumbled about our situation as it was unfolding, and as we did, others latched on to it as the reason they would never want to be a landlord. However, what most people don’t understand is that property owners recover from these situations, go on to find great tenants, and continue paying down their mortgage until the house is paid off and becomes virtually pure revenue. A situation like this forces you to draw upon inner strength that you may not know you possess, and it can require you to dip into your emergency funds to cover the repair expenses or the mortgage while it is unrented; but the point is, you can recover.

The other takeaway is that you don’t have to learn the hard way. You can usually line up a quality tenant if you conduct a thorough screening, which I go into in depth in the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide available at www.GetaChicken.com. If you don’t want to take on this task yourself, you have options. For example, you can do what Kevin and Andrea do and simply enlist the services of a professional property manager. Check out their story, among others, in the Online Appendix B, True Stories of “Not-Chickens.”

To recover from a bad tenant situation, you have a couple of options. You can either evict, or do a “soft eviction.” I much prefer a soft eviction, because it allows the tenant to leave with pride intact and it is much quicker and less expensive than an eviction. In a soft eviction, you have a one-on-one, face-to-face meeting and, in a friendly but assertive way, share the reasons why the situation is not working out. I had to do this for one of our house-share tenants after the other three tenants came to me in a desperate plea. In my meeting with the fourth tenant, I came armed with a few rental listings that seemed equally desirable and even more affordable than her current lease with me. It was an emotional meeting, and I had to stress repeatedly that I liked her as an individual, but it was just not a good match. I refunded her entire security deposit to help her get started in another place. If your main goal is to get someone out of your property and return things to normal as quickly as possible, then sometimes a small amount of sacrifice is necessary to prevent a larger-scale and more lengthy legal fight.

If you absolutely must evict a tenant, you must have just cause and you must follow specific procedures, which vary by state. These typically include providing a specific type of written notice to the tenant and giving the tenant a chance to turn things around before proceeding with the eviction. Consult a real estate attorney to ensure that you follow the correct procedures. If you do end up having to go through a legal eviction, remember that, in the end, you will get your property back, you will recover financially, and you will be stronger and smarter because of the experience.

Risk #2: Plunging Property Values

Another common real estate fear is the risk of crashing property values, as occurred in the housing meltdown beginning in 2007. When this happened, “buy-and-hold” rental property owners were often completely unaffected by their properties’ plunging values. The values were only on paper. It was the rental income that mattered.

The difference for us in 2007 was that we were not trying to buy low and sell high. When the values of our properties plummeted, as they did for most homes virtually everywhere, we continued to rent them out just as we always had. In fact, as people started losing their life savings and their homes, we had more people interested in renting from us than ever before. What we and other property owners experienced was consistent with findings from a Harvard University study on rental housing trends in the United States. This study found an increasing proportion of renters and a decreasing proportion of homeowners across all income levels and household types in the five years following the recession that began in 2008.14

So, rather than selling their properties in the downturn, many individuals, including ourselves, decided to buy more property. It is terribly sad, but also undeniably true, that the housing meltdown provided an unending stream of discounted, bank-owned (“REO”) properties, as well as new renters for those properties.

Before you buy a rental or convert an existing home into a rental, you can take preventive measures that will help safeguard you against the risk of plunging property values. These measures are cures for Risk #3, the Risk of Vacancy, as well. First and foremost, you need to buy with cash flow in mind by ensuring that the property’s rental income is greater than the mortgage and other expenses combined. Second, you need to make sure that your property is in an area that people want to live in so that it is easy to rent. On a related note, the area should be one that is as bulletproof as possible to future downturns in the economy. In other words, invest in an area where people will be able to continue living if the economy tanks. For example, areas near universities are usually safe bets, whereas areas that are solely dependent on one factory or one major business are more risky. If that business lays off workers or if that factory shuts its doors, people will lose income and/or leave town, and your property could be in trouble.

Another way to prevent plunging property values from causing your demise is to stay away from fix-and-flip deals. The reason for this is that if property values take a hit while you are in the middle of a renovation, you could be stuck with a house and no way to sell it. See Risk #7 for more on the perils of fix-and-flip deals.

![]()

A funny thing happens in real estate. When it comes back, it comes back up like gangbusters.

BARBARA CORCORAN

Founder of the Corcoran Group, Inc., author of Shark Tales,

and Shark on ABC’s Shark Tank

Risk #3: The Risk of Vacancy

There’s no question that you need paying tenants in your property to cover the mortgage and other expenses and to make a little profit. As with all real estate risks, the emphasis is on preventing the issue and having the financial resources to recover gracefully if or when the issue does arise.

There are certain preventive measures you can take to ensure that you rarely have a vacancy. The first preventive measure has to do with the actual property you purchase. It is imperative that you have a property that people want to live in. This boils down to the general area, the precise location, and the quality and cleanliness of the property itself.

The second preventive measure has to do with property management, whether you do it yourself or hire someone else to do it for you. It is important to always anticipate vacancy. This even applies to new purchases. When you put a property under contract to purchase, ask the seller to grant you permission to show it to prospective tenants before settlement, in order to line up renters right away. We do this with all properties we purchase. Ideally, you will get a key (or the combination to the lockbox) so that you have access to the property yourself. If someone is currently living in the home, you’ll need to give them the courtesy of twenty-four hours notice before showing it to a potential tenant.

Go to any and all lengths to line up your tenant before settlement. Not only will this guarantee no vacancy from day one, it will also give you a feel for the rental market, the rent you can charge, and the amount of rental demand. If there is not enough demand to support the rent that you need to make the numbers work, you can still get out of the contract. If you do find a tenant for a property that you don’t own yet, be sure to add a clause to the rental agreement indicating that it is contingent on your taking ownership of the property.

If you already own the property, it is equally important that you or your property manager anticipate vacancies. Require that your tenants notify you two months before the lease ends if they plan to leave or renew. You can offer an incentive to your current tenant if he or she finds a replacement tenant. However, don’t rely on that tenant to do the work for you. In my experience, it is incredibly rare for a tenant to find a next tenant even if they are breaking the lease themselves. But if they do, be sure to go through the entire tenant-screening process yourself, as detailed in the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide available at www.GetaChicken.com.

You’ll want to start advertising the property as soon as you receive notice that your tenant is moving out. The sooner you start showing it to prospective tenants, the sooner you find a quality replacement. The R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide has more information on marketing your property. Again, if these tasks are not exactly your cup of tea, you can outsource them to a property manager. You can also hire a less-costly tenant finder, someone whose job it is to find and screen tenants, but who does not take on full property management services.

Finally, you can prevent vacancy by thoroughly screening your potential tenants, as I also go into in the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide. Doing thorough tenant screenings will lessen your chances of having to go through a later vacancy due to eviction. When you have a quality tenant, you’ll be more likely to keep him or her by proactively keeping your property nice and promptly responding to their requests and concerns. You can also keep a quality tenant by not raising their rent. In fact, we rarely raise the rent on our existing tenants. We usually only raise rents when there is turnover between tenants.

Risk #4: The Risk of Costly Repairs

The risk of having to make a costly repair from time to time is actually more of a guarantee than a risk. After all, it’s a known fact that stuff breaks down over time. These expenses should be anticipated, not feared. Every now and then, you will need to repair or replace a leaky roof, switch out an appliance, or deal with water in the basement. It’s a fact of life for any property owner. When something major needs to be repaired or replaced, this is called a capital expense, or “CapEx” for short. CapEx refers to larger repair expenses that come up less frequently but have a significant financial impact when they do.

There are several measures you can take to prevent costly repairs from destroying you or even occurring in the first place. The first occurs after you are under contract but before you purchase a property. (Read closely the “Evaluate Your Potential Property” in the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide.) You can lessen your risk by getting both a professional inspection coupled with estimates from contractors or service providers for repair costs.

You should also obtain the manufacture dates from your inspector and/or the seller’s paperwork for all appliances, heating and cooling systems, hot-water heater, and roof. If any system is beyond its life expectancy (see Table 3.5), and if you still think the property makes sense to buy, then it’s not too late to negotiate the contract with the seller. Ask to have the outdated system replaced before settlement, or request cash back from the seller at settlement to apply toward replacing the system yourself. Both of these options are preferable to simply lowering the purchase price, because that would still require you to pay for the replacement or repair out of your own pocket while only having a minuscule effect on lowering your mortgage.

The second—and essential—preventive step is to know how you will pay for repair expenses when they do arise. There are as many methods for this as there are ice cream flavors. And, as with ice cream, some methods are better than others, but they are all good. The worst flavor is none at all, an empty cone, and that is true for your backup plan as well. You need a flavor.

Some investors have an emergency fund, while others prefer to rely on a line of credit or surplus employment income. Investors also vary as to whether they set aside a certain percentage of the rental income, a percentage of the principal owed on the mortgage, a flat amount each month, or simply the minimum to maintain a given amount for each property owned. Some investors use a home warranty for repairs while others see this as a waste of money and prefer to use lower-budget handymen and secondhand appliances. Still others prefer to use larger companies that offer low-interest monthly payment plans, which they incorporate into their cash-flow analysis as a recurring line item until it is paid off, seeing this as an affordable way to replace something major like a new roof or heating system.

In spite of this real-life variation, it is widely regarded that the best strategy is to have an emergency fund set aside from the moment you purchase the property. The most conservative method—which is what banks like to see when you are applying for a loan—is six months of expenses that are “liquid” or easily accessible. Banks don’t usually care if these funds are in a retirement account or a savings account; but when it comes to your emergency fund, it is best to have this money separate from and in addition to your retirement savings. One method is to set aside an amount that is equal to your mortgage payment (principal, interest, taxes, and insurance, or “PITI”) plus 50 percent of your total projected rental income for six months for each property you own. So, as an example, if your monthly mortgage payment is $700, and if your rental income is $1200, then you’ll want to set aside at least $8400 ($4800 + $3600) as your emergency fund or “cash reserve” for this property.

Because you will be dipping into these funds for small and large expenses alike, you’ll need to replenish this account continually. When you run your numbers before deciding whether to purchase the property (see Cash Flow Analysis Form at www.GetaChicken.com), you should budget a certain amount of your rental income every month to go into this account.

While many people put in somewhere between 5 and 10 percent of the rental income, Brandon Turner of www.BiggerPocket.com, the go-to resource for articles and online discussion forums on all things real estate, uses a flat amount of roughly $200 per month on many of his single-family homes. He reached this number by listing out all the systems, their total replacement costs in his area, and the average life expectancy of each. He then calculated the average cost per month of replacing each item (see Table 3.5). This comes to roughly $2,400 each year, though this could be more for homes that are older, have older components, or have more deferred maintenance.15

TABLE 3.5. EXPECTED LIFE EXPECTANCY AND COST BREAKDOWN, PER SYSTEM FOR A TYPICAL SINGLE-FAMILY HOUSE

Source: www.biggerpockets.com/renewsblog/2015/10/13/real-estate-capex-estimate-capital-expenditures/.

The third preventive measure to lessen the occurrence of major repair issues is to stay on top of routine maintenance and to address small issues before they become big ones. For example, the seemingly small issue of a broken or clogged gutter can lead to water leaking through walls, destroying drywall, and inflicting mildew and mold. Yikes! Stay on top of the little stuff and the big stuff will stay away from you.

There is a risk with the small stuff, too, of course. The risk is that you won’t want to deal with these things and your procrastination could lead to larger repair issues or tenant frustration, followed by vacancy. There are a couple of different approaches to this risk. The first is to adjust your attitude. While I don’t particularly enjoy receiving calls about mice in the kitchen, I remind myself that an occasional house or tenant issue is the small price I pay now for a secure and even early retirement once the mortgages are paid off. I figure I can make this kind of time in order to ensure my family’s long-term financial security.

![]()

As one sows, one shall reap.

And I know that talk is cheap.

But the heat of the battle is as sweet as the victory.

BOB MARLEY

The “King” of Reggae

That said, the second option is to do what we do as much as possible with our local properties, and what Jen and Rachel do with all of their long-distance properties. (See Online Appendix B for their story.) We simply ask the tenants to help. Whenever possible, I ask the tenants to be available to meet the handyman or service contractor, and I schedule accordingly. This is far less intrusive on my own family time and usually just as effective, especially if the tenants are home anyway. Jen and Rachel, with long-distance properties, actually build into their rental leases a provision indicating that the tenant is responsible for meeting the maintenance and repair service providers at the property, as needed. (You can read about their experience managing rental property from a distance on my website at www.GetaChicken.com.)

The third option, of course, is to hire a property manager to take care of the details. If the monthly cash flow affords it, this can be an excellent way to own property for the long term and to not have to deal with the work involved in owning it. Many people choose this handsoff method, including couples Amanda and Matt, and Kevin and Andrea, whose stories I’ve included in Online Appendix B. Amanda’s story is definitely worth your time to read. She shares some lessons learned the hard way about unscrupulous property managers and how to identify them. My R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide available at www.GetaChicken.com will also help you avoid bad property managers and find a good one, remembering once again that: Good eggs and bad eggs look the same on the outside!

Risk #5: Funds Are Not “Liquid”

Many individuals in the finance industry would say that a downside of investing in real estate is that your money is not as “liquid” as it would otherwise be in a retirement or savings account. This means that you can’t access your money as easily, since you would have to sell or refinance your property to retrieve your equity in the form of cash.

I would argue that as long as you also have funds in a retirement account and an emergency fund, this is not actually a downside. With real estate, your funds are protected from identity theft, incompetent financial advisers, and the risk inherent in the stock market itself. And most importantly, with real estate your funds are protected from yourself.

When you have money invested in stocks and mutual funds, it can sometimes be way too convenient to cash them in. If the stock market takes a dip, the fear of a great loss may trigger the impulsive part of your brain to sell, even if at a loss. It’s just too easy to have instant access to your dough. But if you pull your money out on the downswing and then the market eventually rebounds, then you’ve locked in your losses by missing out on the rebound. The people who were most hurt in the Great Recession beginning in 2008 were those who sold their mutual funds and stocks during the downturn. And, sadly, among those who did so, those who were oldest in age were especially hard hit because they have had less time to start over in rebuilding their savings.

Just as those who held on to their plummeting stock and mutual fund investments were able to survive the crash by waiting for the rebound, those who kept their overvalued properties after the housing crash also survived. In fact, many thrived. As an example, there are countless people who decided to buy a second property in the downturn, move, and convert their first home into a rental. Many of these “accidental landlords” were simply aiming to avoid selling their property at a loss or losing it to foreclosure. And, in the process, many used the opportunity to fulfill a long-awaited desire to own rental property. This was the case of Kevin and Andrea, as well as Beth and David (see Online Appendix B for their stories), two couples who converted their homes into rental properties because their values were too low to sell without taking a loss. Ironically, simply by seizing the opportunity to add even just one rental property to their investment mix, the housing crash helped these couples, and many others, lock in a more diverse and secure long-term financial plan.

![]()

Don’t wait to buy real estate, buy real estate and wait.

T. HARV EKER

NY Times No. 1 Best-selling author of Secrets of the Millionaire Mind™

Risk #6: The Expense of Mortgage Interest

Mortgage interest is the monthly (tax-deductible) fee that you incur as a part of your monthly mortgage payment for the privilege of having been given a loan to purchase a property. From your lender’s perspective, it is how they get paid for providing you a mortgage.

Table 3.6 shows how the cost of a mortgage over the life of a loan varies by interest rate and term. In this example of a $100,000 mortgage, the amount you would pay in mortgage interest can range from $15,873 to a whopping $189,664, a fee equaling almost two times the original mortgage amount!

TABLE 3.6. THE TOTAL INTEREST PAID (BY YOUR TENANTS) OVER THE LIFE OF A $100,000 MORTGAGE, BY VARYING TERM LENGTH AND INTEREST RATE COMBINATIONS

From this table, it is clear that lower interest rates for shorter terms are best. However, while the mortgage interest may be daunting, don’t let this scare you away from investing in real estate. Mortgage interest is more of a perceived risk than an actual one. Unlike when you purchase a home for your personal residence, it is not actually you who will be paying these interest-related fees—or your principal, taxes, insurance, or other expenses, for that matter. The reality is that, if you’ve done your cash-flow analysis right, before taking ownership of the property, then the rent from your tenants will cover everything until your mortgage is paid in full.

Yes, it’s true that the less you pay in mortgage interest, the greater your cash flow and the closer you are to owning your property free and clear. However, mortgage interest is not a reason to not invest in rental property. It is a means to an end. The bottom line is that your tenants pay the mortgage interest on your behalf, as a part of their rent, for the privilege of living in your home, so in that sense it doesn’t much matter if the mortgage interest is $15,873 or $189,664.

The impact of the mortgage interest depends on whether the property is your personal residence or whether it is a rental. When you buy a home or car or boat or anything else that comes with an interest rate (even small stuff on your credit card, if you don’t pay it back right away), you need to factor the total amount in interest over the life of the loan into the total cost of owning that item. This interest that you pay on your mortgage, loan, or credit card adds up over the years and is real money. On the other hand, when it comes to purchasing an income-producing asset like a rental property, if you’ve done your initial calculations right, then, for the reasons just described, these costs are more theoretical.

Risk #7: Investing in Higher-Risk Real Estate (In Other Words: What Not to Buy)

People often lump real estate investing into one group, not realizing that each of its many varieties are unique. The focus of this book is residential rental property. There are some other types of investments that are higher-risk for the beginning investor, as listed in Table 3.7 and described in this section. Some require advanced levels of training and experience. Some just don’t make sense from a cash-flow perspective.

TABLE 3.7. WHAT NOT TO BUY (AND WHY NOT)

WHAT NOT TO BUY |

WHY NOT? |

Condo No |

control over escalating condo fees and assessments |

Cheap home with very low rent |

Capital expenses will consume a higher proportion of the total income (thereby lowering the cash flow) than they would be on a home with high rental income |

High-end expensive home |

Rents not commensurate with property sales prices, thereby lowering the cash flow potential |

Major fixer-upper |

Challenging, expensive, and risky in the event of a downturn in real estate market |

Raw land |

Risky in the event that value does not increase. No monthly income (unless there is a business purpose for the land) |

REIT |

“Buy low, sell high” type of investment risk that moves with the overall market. No control over specific investments. No personal tax advantages |

Property in an undesirable or dangerous area |

Difficult to rent or sell, and/or unpleasant or unsafe to manage |

Property with potentially negative cash flow |

Can be draining on existing resources and risky in the event of a change in your salaried income |

Property purchased “sight-unseen” |

Issues that you wouldn’t know about without physically touring the property yourself |

Timeshare |

No control over annual expenses (taxes and maintenance), special assessment fees and no resale value |

Ugly house or neighborhood |

Difficult to rent to people who will help maintain the property and pay rent on time |

Vacation property |

Subject to vacancy if there is a sustained downturn in the economy |

Still others are rooted in the risk-based premise of buying at one price, crossing your fingers, and hoping to sell at a higher price down the road. This “capital gains” method of investing typically involves significantly more risk because, like investing in stocks and mutual funds, you may or may not be able to sell for a higher price when you need your money. It can be risky because the market could change dramatically after you get in but before you are able to get out, as happened to so many people in the housing bust beginning in 2007. This type of short-term investing is more akin to gambling. Long-term goals require a long-term plan, and the safest and most sustainable long-term plan is to patiently own and hold real estate for a long duration.

Properties That Are Purchased “Sight Unseen”

If there was one thing I learned from my father about investing in property, it was this: Never, ever buy a property without seeing it first. My dad learned this the hard way. When I was a kid, he decided it would be a good idea to purchase a charming little piece of land in the middle of woodsy New Hampshire. He lined up a mortgage for this parcel and made the purchase. After signing the stack of papers, he loaded up the whole family into the car for a very exciting trip up north to see our new property. Unfortunately, we were in for quite a surprise! That sweet little parcel of land, that we now owned, was directly across the street from the county dump! This was a brutal awakening for him and a lesson that my three siblings and I will never forget.

Always, always, always inspect your property. You don’t necessarily need to do this before putting it under contract, as long as you have a good “out” clause; however, you absolutely must see the property yourself before you go through with the purchase.

I’ve included an extensive segment on property evaluation and inspection in the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide to this book. Also, to help with your initial walkthrough, I’ve developed the quick-and-easy Anderson Inspection Method (AIM) Tool, which is downloadable for free on my website, www.GetaChicken.com.

Houses That Are Too Expensive or Too Cheap

For different reasons, you may have the most success if you stay in the middle price-range when buying a rental. For example, expensive homes often do not have rents that are commensurate with higher mortgages, thereby lowering your chances of attaining positive cash flow. As Gary Keller explains in his book The Millionaire Real Estate Investor, the best deals can often be those that are in the low end of the middle of any market.16 These so-called “bread and butter” homes constitute the largest market where the most people in the population are buying and renting homes.

Cheap houses are also dangerous when you consider the financial impact of making occasional major repairs. (Refer back to our discussion on capital expenses, or “CapEx,” under Risk #4 in this chapter.) The risk stems from the combination of the age of the property and its components, as well as the fact that many systems tend to cost roughly the same amount whether they are installed in an expensive house or a cheap house. As Brandon Turner, of www.BiggerPockets.com, explains:

Just because a house worth $400,000 is ten times more expensive than one that is $40,000, that doesn’t mean a roof, windows, paint, or anything else will also be ten times more expensive. What this means is that CapEx is a much greater percentage of the income when dealing with lower-priced properties. On a home that rents for $2,000 per month, the CapEx of $200 per month is 10 percent of the income, but on a home that rents for $600 per month, the CapEx of $200 per month will be a whopping 30 percent of the rent.17

Condos

Buying a condo might seem like a safe, worry-free investment strategy, but from a cash-flow perspective they can actually be rather risky. It’s a control issue: You have no control over the condo fees and the extent to which they can escalate each year. In addition, on occasion, a condominium building can also incur a very high expense for upgrades or extensive repairs that are not within budget. When this happens, and if there are insufficient funds in the reserve account, the condominium board will pass these so-called “special assessment fees” on to condo owners. These fees can be extremely expensive, ranging from $1,000 to $20,000, or more, per unit.

Between the rising condo fees and special assessment fees, the cash-flow situation on a condo can shift from positive to negative, overnight. In addition, many condo associations prohibit rental units or they charge extra fees to owners who rent out their units, a lesson that I learned when I rented out my condo (my very first rental property!).

In spite of these cash-flow downsides, you may be attracted to the seemingly lower maintenance involved in owning a condo. If so, keep in mind that, for the sake of your cash-flow stability over the long term, you may actually be better off buying a house in a middle-class neighborhood and hiring a property management company to take care of it for you.

Gambling on House Flipping (Don’t Flip the Bird!)

Fixing and flipping involves buying a run-down house, doing repairs and renovation, and then selling it at a price high enough to recoup your purchase price and renovation costs while making a little profit for your efforts.

Buying at one price and hoping to sell at a higher price is inherently risky. There are just too many ways to get burned . . . for example, by underestimating repair costs, over-improving a house, neglecting to consider holding costs (loan payments, utilities, taxes, etc.), failing to take into account short-term capital gains tax, and so forth. Plus there is the risk of unpredictable repair and renovation costs, contractors’ escalating quotes once a job is under way, disappearing or dishonest contractors, and new repair issues that arise once you look inside the walls, among other issues. It’s not that these things might happen; I know from experience that they will happen.

If you are just starting out and have no renovation experience, I strongly recommend staying away from fix-and-flip deals. One bad fix-and-flip experience could ruin you financially and turn you off to long-term real estate investing with properties that are closer to “move-in ready.”

After you become experienced with purchasing property, becoming a landlord, and attending to the more minor-league repairs and upgrades, you may (or may not) decide that this is something you eventually want to pursue. Fix-and-flips, done successfully, can help expedite your goals if you put the proceeds toward the balance of your existing mortgage(s) or apply them toward the purchase of a new rental or rental emergency fund. However, fix-and-flips and their many risks are way beyond the scope of this book.

It is unfortunate that so many people associate real estate investing with rehabbing rather than the safer variant of investing, which is holding property for the long term. I believe this is partly due to the rise of popular shows like Flip This House, among many others. These shows make fix-and-flip deals seem adventurous and highly profitable; however, the reality is that these kinds of deals can sink you. Again, buying for cash flow is the cure to this risk.

Gambling on Raw Land

Another area that can be confusing is that of raw land. If you purchase raw land in hopes of selling it for a higher price down the road, you are gambling, not investing. Raw land by itself is not technically an asset, as defined in chapter 4, because it does not typically provide cash flow. If you have a mortgage on this raw land, and no income, then it is actually a liability. (My Dad’s land by the dump was a double liability!) On the other hand, if you have a plan to create income from your land, perhaps by renting it to a valet car company (in the city), a farmer (in the country), or a fast-food restaurant or gas station (anywhere in between), then this land could become a powerful asset with high income potential and minimal property management. Take a look at Heather’s story in Online Appendix B. She purchased raw land and then strategically put the pieces together to lease it to a fast-food restaurant.

Purchasing raw land in hopes of making a profit when the price goes up is playing the dangerous game of speculation. However, if you are strategic, owning land as part of an income-generation strategy and leasing it to an individual or business can be an effective means of generating monthly income with potentially very little ongoing maintenance on your part. As you’ll see in chapter 4, the bottom line to remember is that an asset is only an asset if it puts money into your bank account every month. However, if something regularly takes money away from your bank account (like a mortgage on unutilized land), it is a liability.

Gambling on a Real Estate Investment Trust (REIT)

A real estate investment trust (REIT) is similar to a stock, except that you are investing in the real estate industry rather than a publicly traded company. An “Equity REIT” invests in commercial property (like shopping malls, office complexes, apartment buildings, hotels, etc.). A “Mortgage REIT” finances commercial loans. In both cases, when you are investing in a REIT, you are investing in a virtual asset.

REIT investing can be as easy as typing the right ticker symbol into an online stock trading site like E-trade. And yet, while this is obviously a ton simpler than finding the right property and managing tenants, there are downsides. For one thing, while REITs are thought to offer some diversification to the stock market, it’s not much. For example, if you compare the Vanguard REIT Index (ticker symbol VNQ) to the Dow, Nasdaq, or S&P on a site such as Yahoo Finance, you will see that all four generally move in tandem with each other. What this means is that if we experience another major stock market crash, it is likely that REITs will crash right along with the rest of the market, as they did in 2007. In contrast, and as I’ve mentioned earlier, many investors who owned rental property in the right areas, held for the long term, were able to do well because they continued to collect rent and pay their mortgages on time.

To the individual investor, REITs also lack many of the benefits that are inherent to brick-and-mortar real estate. You don’t get the tax benefits. You don’t get the cash flow, unless you have a dividend-paying REIT. And you don’t have the ability to use the leverage of a mortgage to your advantage to receive strong returns on investment. Most importantly, you are playing the role of a gambler when you buy something at one price with hopes that the price will go up over time. And yet, just like the stock market and house-flipping, this is just what many people are doing when they invest in REITs.

Gambling on a Timeshare

Is there any worse investment? Seriously, if you want to get ahead financially, I strongly recommend that you avoid timeshare pitches, even the ones that come with a free weekend at a tempting resort. Timeshare salespeople are paid big bucks to sound very convincing. The problem is that these things become worthless as soon as you sign on the dotted line. There is literally no resale value at all. Plus, in addition to the hefty initial sales price, there are ongoing annual taxes and maintenance fees—over which you have no control—which make timeshare ownership a costly endeavor. A timeshare is a liability to the nth degree. Trust me. I know this from experience. We got suckered into a timeshare long before we started purchasing rental property, and we’ve been stuck with it, and paying for it, ever since!

In Summary

Investing in real estate is not without risk. However, when you own residential rental property for the long term, it is a different kind of risk. Unlike the market and cyber-related risks of stock market–based retirement accounts—risks that are mostly out of your control—risks in real estate are more tangible, and as a result more preventable and controllable. Most longtime landlords and property owners have at least one horror story. We do, too. However, there are steps you can take to minimize your risk and help you manage things when the unexpected does strike. It all comes down to ensuring that you have funds to fall back on, buying the right property, and finding the right tenant. In the end, we recover from sour events, become empowered in the process, persist in owning the property, and continue paying down the mortgage until it is owned free and clear.

Many people fear the risks involved with owning rental property. You could choose to avoid all the potential suffering by never owning a rental property. But then you would never experience its benefits. Just like life, owning rental property entails some work and some lessons learned along the way. And yet if you don’t get into the game due to fear of whatever lessons you might have to learn along the way, then you will also miss out on the financial benefits and sense of empowerment that come with owning rental property.

‡ Note that Figure 3.2 and Table 3.3 do not include expenses such as mortgage interest, taxes, insurance, and other operating costs. Please see Risk #6 in this chapter for a discussion on mortgage interest and other expenses.