4

PREPARE THE NEST

Rethinking Money, Debt, Assets, and Liabilities

RETHINKING MONEY

I was raised to believe that money was a bad thing. Well, not money itself, but the pursuit of money. Every now and then, I still find myself downplaying the importance of money. And yet I know that money is a necessary thing, an enjoyable thing, and, when used right, even a very loving, generous, and charitable thing.

![]()

Money is good for the good it can do.

GARY KELLER

At the most basic level, money is a necessity. It provides food, clothing, and shelter. It gives us wheels and heat and medicine. It gives us the freedom to get on an airplane to explore this beautiful world or to reconnect with loved ones living long-distance. Money can be used for good, loving purposes. It can be used to help out a friend. It can be donated to charity. It can help a homeless family start over. And it can literally buy time, in the form of time off of work, especially if you are self-employed or in retirement.

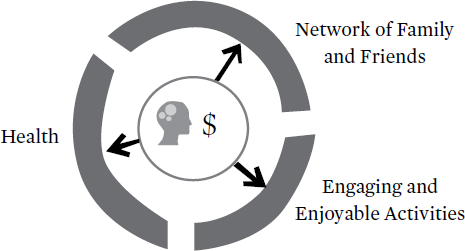

According to the book Retire Happy by Richard Stim, there are four essential ingredients to a happy retirement: money, health, a network of family and friends, and having engaging and enjoyable activities. However, superseding all of these factors, His Holiness the Dalai Lama asserts in his book The Art of Happiness, co-authored with Howard Cutler, that one’s state of mind, perspective, or outlook is—hands down—the most important determinant of happiness. Our outlook on our circumstance is indeed critical. After all, the very quality of our financial situations, our states of health, our networks of family and friends, and our activities are all quite literally defined by our perceptions and our appreciation of them.

However, since we live in the real world, and since our outlook doesn’t pay the bills (at least not by itself!), I believe that there are two key ingredients to a happy retirement that can help or hinder the success of all the others. These are our money and our mindset. I’ve portrayed these ingredients in relation to each other in Figure 4.1.

FIGURE 4.1. FOUR ESSENTIAL INGREDIENTS TO HAPPY RETIREMENT

In the center of the diagram, our state of mind is represented by the picture of the head, and our state of financial health is represented by the dollar sign. Around the outside are Stim’s remaining ingredients: our network of family and friends, the activities we find engaging and enjoyable, and our state of health.

Money and mindset affect everything. Money allows us to go out and enjoy time with friends (without being a burden on them!); our mindset helps us enjoy those friendships. Money allows us to travel, to visit long-distance loved ones, and to vacation, while our mindset makes it possible to take the initiative and appreciate these experiences. Money allows us to participate in whatever recreational activities we enjoy—or try new ones—and mindset allows us to be up for the adventure. Money is essential for maintaining our health as we get older—be it for copays or vitamins, acupuncture or exercise, long-term care insurance or walkers. And equally important, we need a positive state of mind in order to be simultaneously grateful for whatever our current state of health happens to be, as well as to be willing to do whatever is necessary to maintain or improve that particular state of health.

RETHINKING ASSETS AND LIABILITIES

Robert Kiyosaki teaches that an asset is something that brings money into your life on an ongoing basis, like a rental property. I completely agree with him. I also believe that assets go beyond this strict definition into other areas. For example, what about your friend who encourages you to follow your dreams and achieve your goals? Is this person an asset? What about your state of mind? Could positivity and motivation be considered assets?

I believe they are. These things, among other intangibles, are what fuel us. They are vital to our lives, to our success in achieving our dreams and goals, and ultimately to our happiness in this thing called life. As I see it, there are three overarching categories of assets: those of the heart, those of the mind, and those of the pocket. I developed Figure 4.2 to show how these asset classes fit together.

These three classes do not stand on their own. They are interdependent, with each affecting the others in a number of ways. The sweet spot is that spot right in the middle where all three asset classes are in effect. The heart feels alive, the mind is positive and proactive, and the pocket is enjoying positive cash flow through rental property or another type of passive income.

I’ll go into these three asset classes next. Note that it may appear that this section veers a bit off the point of my message of diversifying retirement planning with rental property. However, as you read this section, you will see how nurturing the assets of the heart and mind will boost the assets of the pocket and your eventual success in protecting your late-life financial security and retirement dreams.

FIGURE 4.2. ASSET CLASSES FOR THE 21ST CENTURY

![]()

A stranger is just a friend I haven’t met yet.

WILL ROGERS

Assets of the Heart

Assets of the heart include all the positive relationships in your life. These include your relationships with your spouse or partner, your kids, other family members, and your neighbors, friends, co-workers, and business associates. Even your relationships with total strangers count here. Assets of the heart include laughter, pleasure, romance, leisure, play, and good times in general. Assets of the heart also include conversations, activities, and interests that ignite your passion.

Investing in assets of the heart means prioritizing time for the people in our lives who matter most. This includes being present with our loved ones, listening to them, holding them, snuggling and cuddling and having fun with them. It means reaching out to friends to keep those friendships alive and healthy. It also includes being helpful and pleasant to others, whether it is volunteering for a cause, helping someone out in need of a favor, or simply sharing a smile or friendly exchange with people you encounter throughout the day. For many people, investing in assets of the heart means being a part of a religious or spiritual community. It may also mean being a part of some other kind of group, like a rock band, hiking group, book club, soccer team, or whatever it is that you enjoy.

Liabilities of the Heart

The opposite of an asset is a liability. It is something that brings you down, zaps you of energy, or sucks money from your life. In the case of the heart, liabilities include relationships that have become unhealthy, unhappy, or toxic. However, before you are too quick to blame your significant other, remember that our relationships can be strained by our own negativity, criticism, and/or the inability to let go of stress, anxiety, or the need to work. It is important to learn to keep those traits in check and to let yourself, or even force yourself, to be lighthearted and fun at times.

Other liabilities of the heart could include friendships that don’t lift you up or bring out your best. Liabilities could also include the absence of friendships or activities outside of your work and family. Rather than coasting on autopilot through life, take a close look at who and what is in your life and, as with your primary relationship, pump some new energy into those friendships and activities that make you a better, happier, and more interesting person.

Assets of the Mind

Assets of the mind include things such as positivity, grace, courage, willingness to learn from mistakes, eagerness to continue learning, being daring, and taking action. It takes work to foster these qualities in one’s own mind, especially when faced with work demands, personal stress, and negative input from the world at large. However, again, like the assets of the heart, you have the right, and the responsibility to yourself (and to your loved ones), to do so.

There are so many ways to continually foster the assets of your mind! As with the assets of the heart, one way is to surround yourself with positive people, such as those who are striving toward their own personal goals or working for the good of humanity in some way. Other ways include meditation or prayer, journaling, reading, exercise, dance, playing music, or whatever it is that works for you to help you clear your mind. Reading spiritual, motivational, or psychological self-help books is also an excellent way to foster and nurture the assets of the mind. There are so many excellent books. As a place to start, I highly recommend Napoleon Hill’s groundbreaking classic on the power of the mind, Think and Grow Rich, which I reference later in chapter 6.

![]()

Emancipate yourselves from mental slavery, none but

ourselves can free our minds!

BOB MARLEY

Liabilities of the Mind

Liabilities of the mind include paralyzing fear, procrastination, inaction, laziness, avoidance, delusion, and ignorance. We are all victims of the liabilities of the mind at times, but succumbing to them for extended periods of time can have a very negative effect on you, your loved ones, and your future financial prospects.

As a side note, if you think you might be one who overindulges in drinking, drugging, eating, gambling, gaming, watching back-to-back Netflix shows, or some other behavior that lessens your ability to reach your full potential, then these could have very harmful effects on your state of mind (and body) over time. Left untamed, these patterns can become addictions, and addictions can spread like a cancer to affect other assets of your mind, heart (your relationships and passions), and pocket (your financial security and retirement dreams).

Whether it is the cost of booze or smokes, Starbucks or Coke, lottery-playing or day-trading, these patterns of behavior, which are the domain of the mind, ultimately also hurt our bottom line, which is our forever line. I say “forever line” because one day leads to the next, and the next, and so on. If we maintain unhealthy patterns, then we will one day wake up to find ourselves in exactly the same place—or even further behind. If this is your situation, I encourage you to find a private therapist or check out a 12-Step program that is relevant to your situation to take back the reins of your life.1

Assets of the Pocket

I’ve put assets of the pocket last, not because this category is the least important: To the contrary, it is essential to the subject of this book! I’ve included this last in order to avoid trivializing how very important the assets of the heart and mind are to a successful, happy, and even financially abundant life both before and during retirement.

The category I’ve called “Assets of the Pocket” refers to your “financial house” (or free-range chicken yard!) and the extent to which it is in order (or has at least one egg-laying chicken!), especially in preparing for retirement. Assets of the pocket actually have little to do with your job, because you won’t have that when you retire. Assets of the pocket have nothing to do with the resale value of your car or jewelry, because it is unlikely that you could sell these things for anywhere close to what you originally paid for them. And they have little to do with the size of your bank account or retirement accounts, because no matter how much you have, there is no way to really know how long your funds will last you in the end.

Assets of the pocket have everything to do with owning one (or more) sustainable asset that brings passive income into your life on a regular basis, thereby setting you up for a worry-free retirement. It’s all about getting that chicken! Not just any chicken—one that will lay eggs for you month after month in perpetuity. One that you can eventually pass to your loved ones when you die.

So how do you go about getting this chicken? Well, this is the subject of the rest of this book. However, the most basic answer is that you use a mortgage. In fact, mortgages were invented to help the vast majority of us buy homes that we wouldn’t otherwise be able to afford. Robert Kiyosaki, author of the game-changing book Rich Dad Poor Dad, explains that if a mortgage is used to purchase a cash-flowing rental property, then this mortgage is “good debt.” Good debt is debt that improves your financial situation in both the near term and the long run, while bad debt worsens it in both. As he famously says, “Good debt puts money in your pocket.”

Liabilities of the Pocket

Like assets of the heart and mind, assets of the pocket also have their villain: the liabilities of the pocket. Again, according to Robert Kiyosaki, if something takes money from you every month, then it is a liability. This will be doubly true once you retire, since you will no longer be able to rely on income from your job to sustain the cost of that liability.

Liabilities of the pocket basically equate to bad debt that you take on when you purchase things that don’t create income. Bad debt is money that you must pay back every month while getting nothing in return (except for whatever it is that you purchased). Bad debt usually takes the form of credit card debt but also can include car loans, personal home mortgages, and lines of credit. While you may feel that some liabilities are necessary, like your home and car, be careful not to fool yourself into buying a more expensive home or car by calling these things assets. They are still liabilities; and the greater the purchase price, the greater your monthly liability tends to be.

![]()

Your home is not an asset.

ROBERT KIYOSAKI

Anything that must be sold to recapture its value does not count as an asset for retirement-planning purposes. After all, who in the world is going to buy that flat-screen TV off you for the same price you paid, when they can just go to a store and get a new one off the shelf, on sale, instead? And what if you can’t find someone to buy your house for at least the amount you paid for it? We’re all way too familiar with that scenario from the housing meltdown beginning in 2008.

Most people factor their home into their retirement picture. After all, you’ve certainly heard it said that our home may be the largest investment, or asset, we ever purchase. But is this really the case? To cut to the chase, the answer is, well . . . it depends. Before the mortgage is paid off, it is just a liability. After you pay off the mortgage, it depends on your operating expenses (utilities, taxes, insurance, etc.) and whether your home can make you any money. According to Kiyosaki’s definition, technically speaking, if you rent out the garage or a room in the house, and if the rent covers your operating expenses, then your home becomes an asset.

Whether or not you decide to rent out space in your home, it is widely accepted that a key component to any retirement strategy is to live mortgage-free in your own home. There are other benefits to owning your own home. For one thing, it’s your home, your abode. Also, at tax time, you get to deduct your mortgage interest, your homeowner’s insurance, and any points you may have paid at closing.2 Finally, as you’ll see in chapter 8, if you buy a property with an investor’s mindset (as detailed in the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide at www.GetaChicken.com), then, at any age or stage in your life, you can move out and turn your home into a cash-flowing rental property.

In general, what the three asset classes (heart, mind, and pocket) boil down to is this: In the different areas of your life, are you being filled up, or depleted? Fed, or starved? Every now and then, I like to take an inventory of these different areas of my life and make adjustments where necessary. I believe this is vital for both day-to-day and long-term happiness and fulfillment.

![]()

Never say “Poor me.” Saying “ Poor me”

only makes you more poor.

K. KAI ANDERSON

How to Turn a Liability into an Asset

What to Do with an Existing Negative Cash-Flowing Rental Property?

Rental properties fall into the liability trap when they are not “cash-flowing”—that is, when they cost you more money each month than they bring in. The number one way to avoid a bad-debt rental property is to buy the right property at the right price. (See the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide and the free Cash Flow Analysis [CFA] Tool on my website at www.GetaChicken.com.)

If you currently own an investment property that has zero to negative cash flow, you need to find a way to turn your rental liability into a rental asset. There are a few ways to do this. One method is to enroll in the governmental Section 8 program. Landlords with Section 8 property often report that they can achieve market rent with the added security of being paid every month by the government.

Another way to improve your cash flow is to refinance your mortgage to achieve a lower monthly payment. Refinancing involves replacing your current mortgage with one that has better terms in order to achieve one of three goals: lower your payment, slice off time until payoff, or take out additional funds. If your goal is to improve the cash flow on a property, then you’ll want to lower your monthly payment, of course. This may be possible if you can get a lower interest rate or if you shift from a lower-term mortgage to a higher-term one: for example, going from a fifteen-year to a thirty-year mortgage.

We’ve found that, hands down, the absolute best way to boost the cash flow on a property is to turn it into a house-share and rent by the room to responsible individuals. The details of this are shared in chapter 7, “Borrow a Chicken.” For example, for a little extra work on our part, converting one of our single-family properties into a house-share boosted the total rental income from $1,350 to $2,400 per month. Plus there is the unmatched feel-good benefit of providing affordable housing to several individuals, rather than attempting to raise the rent on one tenant.

Other ways to increase cash flow are to have the tenants pay their own utilities if they are not already doing so, charge extra for on-site parking, and install coin-operated laundry or vending machines or another amenity. Using one of these methods (or raising the rent) should be done cautiously, however, as they could cause excessive financial burden on your tenants or cause them to seek housing elsewhere.

If you are losing too much money on a rental that you already own, and if you’ve already exhausted all of these methods, then it may be best to sell that property and start over. Other factors in your decision should be the length of time until the mortgage is paid off, the anticipated repair needs of the property, and whether you can afford to float the negative portion of the cash flow from your regular income source until things shift or until the mortgage is paid off.

Remember that a decision to bail should be about cash flow, not property value. When your rental is cash-flow positive, and if you are in it for the long term, it won’t matter so much what the property value is. You can weather any storm or turbulent real estate market, as long as you have rent-paying tenants.

Your Home

In getting on top of finances, one goal should be to take a good look at all of your liabilities and then convert them into assets wherever possible. Even though your home is not an asset, you may be able to make it work for you, at least a little. For example, if you have extra space in your home, you can rent it to someone for a little extra money each month, or list it on www.Airbnb.com. With your landlord’s approval, you can do this even if you don’t own the home yourself.

Chapter 7, “Borrow a Chicken,” goes into this in depth. However, I will briefly mention here that we rented space in our home for a period of time, and it was a win-win-win. Two very responsible college gals rented our finished basement (and shared our kitchen and living space); we benefited from $800 in monthly income; and our young daughter fell in love with them! They loved her back and, as any parent knows, life is often easier when there are other fun, loving, trustworthy adults in the home. Needless to say, if you have children—and even if you don’t—trustworthiness is essential!

Your Other Stuff

More than ever, you have opportunities to make money off your liabilities—that is, your existing stuff and your space. For example, you can rent out your car through sites like www.Turo.com (formerly known as RelayRides), www.carclub.easycar.com/home/carowners, and www.getaround.com. A growing company called FlightCar (www.flightcar.com) allows you to make money on your car when you drop it off at the airport, rather than paying for airport parking. The car-sharing revolution has gone international with Germany’s www.mitfahrgelegenheit.de, France’s www.drivy.com, and Australia’s www.drivemycar.com.au, among many other companies across many other countries.

You can make money off of your other stuff too. You can rent out space in your home through www.Airbnb.com. You can rent out your parking pad or parking garage through sites like www.JustPark.com. You can rent out extra land to gardeners and farmers through www.SwapItShop.com or, in Canada, www.SwapSity.ca. If you are a dog lover, you can take in someone’s dog while they are on vacation through sites like www.DogVacay.com and www.Rover.com. You also can rent out your skis and bikes and other recreational equipment through www.SpinLister.com. In fact, through sites like www.us.Zilok.com (www.uk.Zilok.com in the UK, etc.), you can pretty much rent out anything you own!

RETHINKING SPENDING

This book is about using rental property to boost the income in our lives, especially as we prepare for retirement. And, just as the cash flow of a property involves money coming in and money going out, the same is true for our personal lives. This means that it is important to get a grip on our outgoing money just as much as the incoming. That said, I recognize that there are tons of books on saving and budgeting, so I will try to offer a brief, fresh perspective on the subject in the remaining pages of this chapter.

![]()

Goals are theoretical, habits are actual.

DANIELLE LAPORTE

I believe most of us have patterns or daily habits that keep each of us at a given, unique, and relatively stable state of being. We stay at that state until we change some element of our behavior (either positive or negative, large or small) on a consistent and even daily basis. Starting a new daily pattern is like adjusting the temperature on our own personal thermostat. Once we begin our new pattern, things start to shift . . . until we land at our next thermostat setting, or “temperature,” or state of being.

This is what I call the Thermostat Change and Results Theory, or just Thermostat Theory for short. As a disclaimer, my theory is scientifically untested, as far as I know; however, you can try it out in your own life and share with me, anecdotally, how it goes for you. To all research psychologists and physiologists, have at it!

Thermostat Theory is a way of shifting your life by shifting your metaphorical temperature setting. It can be applied to anything in our lives: finances, friendships, clutter, health . . . you name it. In fact, while this book is about retirement planning using real estate, Thermostat Theory is probably easiest to understand in the context of weight control.

Consider the example of Mary, portrayed in Figure 4.3. Mary is fifty pounds overweight. If she makes one small positive change, on a daily basis, she will start to make progress in the right direction, perhaps without even seeing it herself. Her weight will shift until it lands on that invisible new setting and will remain stable as long as she maintains that change. For example, in Figure 4.3, you can see the impact of her replacing her daily sugared soda at lunch for ice water with lemon. By doing this, she has essentially changed the setting on her invisible thermostat.

FIGURE 4.3. THERMOSTAT THEORY (AS APPLIED TO HEALTHY HABITS)

If Mary maintains this first change and then makes yet another small change, such as adding five to ten minutes of exercise to her morning routine, things will shift ever so slightly again until she lands on her next setting. And so on, until she reaches a healthy weight. At that point, if she maintains the daily habits that brought her to her healthy new setting, she will be able to enjoy her new state of well-being indefinitely.

Thermostat Theory works in the opposite direction as well. In fact, I am convinced that this is how people go from healthy to unhealthy without even realizing what happened. Little by little, the incremental changes we make and maintain on a daily basis pile up. Of course, the impact of this phenomenon may be especially pronounced at key periods in our life, such as when our body’s metabolism is naturally changing as we get older. In the same example of Mary, if she had added a second Coke to her day, rather than eliminating the first, her body weight would have gradually shifted in the other direction. Behind the scenes and beneath her skin, her body would be undergoing a subtle shift until, after a certain length of time, it would reach a slightly higher setting. The key here is that a random Coke or donut is not what makes the difference. It’s when the behavior is repeated the next day, and then the next, and becomes a daily pattern.

FIGURE 4.4. THERMOSTAT THEORY (AS APPLIED TO SPENDING)

Our spending habits and level of financial stability operate in the same way. In Figure 4.4, let’s consider a similar example, but one applied to spending. In this case, Mary has difficulty paying her credit card bill each month. If she changes her thermostat setting by making one small change, such as curbing her $5/day Starbucks coffee habit, and if she consistently sticks with it, day after day after day, her new lifestyle will slice $150 off her monthly statement (or provide her an extra $150 to put toward her next bill). If she sticks with this for a whole year, she’s looking at about $1,825 in found money!

If Mary then changes her thermostat setting again by making a second small change, and does this on a daily basis, she will bring her spending setting down another degree. For example, if Mary begins packing a lunch to bring to work instead of spending $10 on lunch, then she will save roughly $200 per month or $2,400 over the course of the year. She will be on her way to liberating her finances and achieving higher and more lasting goals for herself.

Just as diet and exercise work hand in hand for the ultimate effect on your health, your financial situation is affected by income and spending. It is important to first know where your money is going. You may want to start by opening up your credit-card and bank statements and looking at each line item.

Are there services or items for which you are being automatically billed that you no longer use? When you try this exercise, you will probably find, as we did, that we were being automatically billed for things we’d long since forgotten about. It is important to check your statements regularly for these sneaky automatic deductions. Once you find a suspicious or useless automatic charge, without even stopping to use the bathroom, go pick up the phone, call the company, and cancel your subscription or service.

The next step is to take a close look at your spending habits. When I did this, I discovered that my statement was riddled with charges from my workplace cafeteria. While I had absolutely no grounds to contest the charges with Sodexho, and arguing about the prices would do little to no good either, I could do as Michael Jackson sang and take a good look at the person in the mirror. I could simply change my daily habits. Armed with information on how much money I was literally flushing down the toilet every day at work made it much easier to take the time to pack my lunch each morning.

I invite you to try thinking of small, maybe even ridiculously small, changes in the positive direction that you might be able to make in your own life. Try picking one change and then make it a habit. Do this three days in a row, and you own it. You are on your way to a new pattern, new lifestyle, and, little by little, a new future. What spending habit are you willing to change first?

Your answer: ____________________________

In a seminal book called The Millionaire Next Door: The Surprising Secrets of America’s Wealthy, authors Thomas J. Stanley and William D. Danko enlightened readers on their counterintuitive finding that, much of the time, people who appear wealthy often have a very low net worth, and those who appear only “average” are often truly very wealthy.3 This is because truly wealthy people care about retaining their wealth for the long term. On the other hand, people who care more about appearances and immediate gratification often load themselves down with consumer debt and as a result get trapped into a lifestyle that is unsustainable . . . especially when the work stops.

![]()

Too many people spend money they haven’t earned,

to buy things they don’t want,

to impress people they don’t like.

WILL ROGERS

American cowboy, actor, and humorist (1879–1935)

When people develop a habit of financing their “wants,” one “want” leads to the next, which leads to the next, and so forth. If you are stuck in this pattern, you may have discovered that “having” is not nearly as satisfying as the next “want” is alluring. To make matters worse, you may be suffocating under a mountain of bad debt, surrounded by liabilities that no longer excite you. Consumer debt can be particularly devastating when there is some kind of uncontrollable shift to the income side of the equation. A job loss or divorce could flatten the whole house of cards in a flash. And if it gets bad enough, retirement could become a pipe dream.

Stanley and Danko revealed a surprising fact: Authentic wealth has little to do with income. In fact, those who are authentically wealthy look as “regular” as your next-door neighbor. This authentically wealthy neighbor may drive an old car, buy groceries at discount grocery stores like Aldi, and may even choose to shop for clothes at the local thrift store. The authentically wealthy neighbor will gladly accept a hand-me-down to avoid buying something new, much less putting it on credit. They have daily spending habits that are controlled and based on needs rather than wants the majority of the time. Ultimately, these daily habits serve to keep them on a healthy and sustainable financial plateau.

I learned a valuable lesson from my father when I was about twelve years old. The revolutionary Sony Walkman had hit the American shelves in 1980 and, two years later, was piping hot. This seemingly magical device was a handheld cassette player with radio, and . . . brace yourself . . . it came with earphones! It was a brand-new concept in the early ’80s, and as a young teen I desperately wanted one of my own. One day, my dad finally took me out to shop for one, even though I had to use my own money that I had been saving up over time. However, we didn’t just go out, buy a Walkman, and come home. My dad had another plan for me. As an impulsive pre-teen, I found it to be a thoroughly aggravating plan; but in looking back, I’m now grateful for it.

My dad and I shopped around, test-drove a bunch of devices, both Walkmans and spin-offs, and compared prices across several brands and stores. To make matters worse, he made me come home to think about my options and ponder whether this was really how I wanted to spend my money. His motto was: “Always go home empty-handed. If you want it bad enough, then you won’t mind going back out to buy it.”

In the end, I decided I really did want that Walkman spin-off “bad enough,” and we went back out a couple of days later to drop coin for the top (and cheapest) contender on the list. I share this story to pass on the valuable lesson I learned from my dad. The point isn’t to avoid spending money on nice things. It’s that when you do, make sure you do your research, shop prices (and these days check online reviews), and refrain from impulsive buys. Try to force yourself (and your kids for that matter) to go home empty-handed, as hard as it may be, because . . . if you want it bad enough, you truly won’t mind going back out to get it. In fact, I can tell you from experience that you’ll quite enjoy the trip!

When it comes to online shopping, you obviously can’t drive home empty-handed and then make a second trip back out. However, if you find something online that you really want, try closing the web page and doing something else for the rest of the day. Get outside. Call a friend. Make yourself wait at least a day or two. After a couple days, you might even discover that you’d forgotten all about the item and that it’s not all that important to you after all. Give yourself the chance to move on.

How many times have you come to the conclusion that someone you know is wealthy based on their fancy car, large home, or lavish vacations? It’s easy to fall for that trick. If we do, then we often fall for the second trick: Measuring our own self-worth or the quality of our lives, or even our happiness, against their stuff. We convince ourselves that we want what they have. But even if we succumb to a new SUV or a fresh set of appliances, do these things truly make us happy? Or do they just put us further behind?

The problem is that too much of this kind of spending could jeopardize your retirement prospects in two ways. The first is that you’ll have less money to put toward acquiring and maintaining an income-producing asset like a rental property, so you will literally build less potential net-worth energy for yourself. (Refer back to chapter 3, the “Benefits of Rental Property” section, for a refresher on potential and kinetic net-worth energy.)

The second way in which this kind of spending threatens your future finances and retirement prospects is that, if you finance the items, any bad debt you take on comes right out of your net-worth equation. It may not seem so terrible while you are working and able to make payments; however, once you stop working, the monthly payments will continue to take an uncomfortable slice out of your personal monthly cash flow.

My last point, which you probably already know, is that it is essential to pay off any credit card debt that you have. Otherwise, you will be paying interest on the amount borrowed, and then interest on that interest, and then interest on that interest’s interest, and so on, putting yourself further and further behind. If the cash-flow numbers work out, you can also refinance an existing rental property to strategically get back to ground zero and start fresh in curbing spending and paying off your credit card every month. Chapter 7 has some other great ideas for cleaning up bad debt.

This chapter was all about “preparing the nest” for good things to come. In other words, this has been about learning new ways of thinking about money, debt, assets, liabilities, and spending. By now, you may be eager to get started in creating a sustainable source of income that will be there for you after you retire. If so, turn the page. . . . You are ready for the first step of taking action: setting your goal! In the next chapter, I’ve outlined three goals for you to consider taking on as your own, goals that are specifically related to acquiring rental property to aid in a long-term retirement strategy. Then, in chapter 6, I will share five tricks to help you achieve your goal, or any goal, for that matter.

![]()

It may be hard for an egg to turn into a bird: It would be

a jolly sight harder for it to learn to fly while remaining

an egg. We are like eggs at present. And you cannot go

on indefinitely being just an ordinary, decent egg.

We must be hatched or go bad.

C.S. LEWIS