5

THE PRIMARY AND ULTIMATE GOALS

Setting the Goal That Is Right for You

THE ULTIMATE GOAL

The Ultimate Goal is to pay off your mortgage(s) so that the income from your property or properties can become your monthly living income. Property that is not tethered to a mortgage—that you own free and clear—is all yours. The bank can’t take it back, because the bank no longer co-owns it with you. Monthly cash flow is maximized, because you will no longer have to pay the principal and interest, the largest of your property expenses (although, of course, you will need to continue paying taxes and insurance and budgeting for capital expenses). As you will see in Figure 5.1 later in this chapter, once you are liberated from your mortgage payment, the income from your property will shoot up and become an integral part of your retirement plan.

You should always bear in mind the Ultimate Goal. It should be a factor when you are considering a property and evaluating different mortgages. The type of mortgage you attain for your property will be a key factor in your ability to achieve the Ultimate Goal. This is a key theme throughout Part Three of the book, in particular chapter 9, “Hatching Your Plan,” and chapter 10, “Do the Chicken Dance!”

DETERMINE YOUR LEVEL I, II, OR III PRIMARY GOAL

It’s time to decide your destiny. What do you want your future to look like? In this chapter, I offer three different Primary Goals for diversifying your retirement plan using the tool of real estate. You get to choose your own adventure.

If you simply desire to provide a level of safety for your retirement by diversifying beyond your Social Security and/or mutual fund–based retirement accounts, then you should set and attain the modest and realistic Level I Goal of owning just one rental property.

If you are feeling a bit more ambitious and would like to strive for a higher level of safety, comfort, and peace of mind in your retirement, as afforded by greater cash flow each month, then you should decide to set and attain the Level II Goal.

Finally, if you are seeking complete financial self-sufficiency once all your mortgages are paid off, then the Level III Goal is for you. This is for persons who have the ambition, time, and resources to create enough cash flow to cover all of their living expenses in retirement. With the Level III Goal, Social Security, pensions, and retirement accounts are all considered bonus. If these sources disappear for any reason, the cash flow afforded by your Level III Goal will sustain you and provide the lifestyle of your making for all your living days. These three Goals are outlined in Table 5.1 and described in detail in the pages that follow.

TABLE 5.1. THE LEVEL I, II, AND III GOALS

Level I Goal |

One rental property as a retirement backup plan, providing a level of safety through authentic diversification |

Level II Goal |

Enough rental income to supplement other sources of income in retirement (or once mortgages are paid off), providing a degree of comfort through additional monthly income |

Level III Goal |

Enough rental income to cover living expenses and property expenses in retirement (or once the mortgages are paid off), providing complete financial self-sufficiency |

The Level I Goal: Diversification and Safety Net

The minimal and most modest goal that I hope you will consider setting for yourself upon reading this book is the acquisition of one rental property for the long term. One property, well chosen and well managed, will provide a level of diversification and safety for your later years—beyond the stock market and Social Security—that simply would not otherwise be there. Consider your one rental as an insurance policy against a sudden decline in the stock market—or, worse, a sustained recession, depression, technical failure, identity theft, or even cyberterrorist attack on the stock market, striking just when you need your money most.

As I’ll get into in Part Three, there are many ways to acquire your first rental. For example, if you own your own home, one of the easiest and most common ways that people get started is to find a new home for yourself and turn your existing home into a rental. If you don’t already own your home, you may want to purchase a two-to four-unit house and move into one of the units. Check out the many stories in Online Appendix B for real-life examples of these commonly employed first moves (look for Venesa, Kevin and Andrea, John, and Deb’s stories).

Whether you turn your home into a rental or purchase one from scratch, the rent that you receive every month from your tenants will gradually pay off your mortgage, until you ultimately own it free and clear. You may have only modest cash flow in the beginning, but, whether it takes just a few years or thirty, once you’ve paid off the mortgage you will have a continuous, sustainable, and healthy amount of income streaming into your bank account every month. As you get older, this income will trend upward. In retirement, this income stream will supplement your Social Security income, and your pension if you are lucky enough to have one, and whatever retirement savings you’ve accumulated over the course of your life.

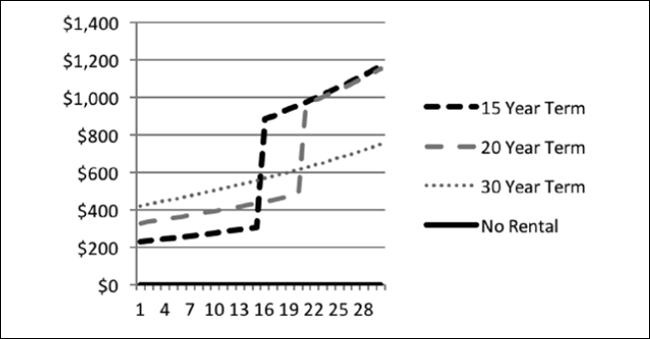

Figure 5.1 provides an example of the degree of diversification and safety that you could attain for yourself on a monthly basis with just one rental property. This graph shows rents over time with a hypothetical 2 percent increase each year to keep up with the rate of inflation, plus a jump in cash flow at the time the mortgage is completely paid off. Note that the 2 percent rent escalation is for example purposes only. It is not possible in all locations at all times, nor is it always in your best interest to implement it.

FIGURE 5.1. MONTHLY CASH FLOW (AFTER EXPENSES) OVER 30 YEARS (ASSUMING 20% DOWN, NO PROPERTY MANAGER, AND HYPOTHETICAL 2% RENT APPRECIATION PER YEAR)

This graph shows mortgages at terms of fifteen, twenty, and thirty years for comparison. If you are able to sacrifice a little in monthly cash flow in the early years with a fifteen-year mortgage, then you will be able to jump to higher levels of income much sooner. To bring the message home, the graph also shows the impact of not investing at all, as represented by the flat line at the bottom of the chart.

You can see that the small move of acquiring one rental property can add a stream of income to your life, both now and when the property is paid off, that would be otherwise nonexistent. Figure 5.1 is for demonstration purposes only. The actual numbers will vary based on your property and geographic area.

The Level II Goal: Financial Comfort

The Level II Goal brings even more benefits than the Level I Goal just described. Going beyond the realm of modest diversification, the Level II Goal entails creating enough income to supplement whatever it is that you expect to receive in retirement to meet your anticipated monthly expenses at that time. The “Total Extra Needed” formula presented in chapter 3 can help you determine how much cash flow you’ll need to create in order to achieve the Level II Goal of financial comfort in retirement.

By acquiring enough rentals, or rental units (in the case of a multi-family home), to supplement your expected income in retirement, you will also create additional flexibility, as described in chapter 8. These rentals will have a lasting effect on your life by providing a modest income before you retire, heightened income once your mortgages are paid off, and ongoing income for your family or favorite charity long after you are gone. In addition, having multiple properties will allow you to sell or refinance one down the road, if you need to, while still enjoying the cash flow of the others.

Keep in mind that owning more than one property should be used in conjunction with your broader retirement plan. In addition, it is important to remember that the Level II Goal should be achieved incrementally. There is work involved in acquiring property, preparing it to be rented, and finding a great tenant. Each rental also demands emergency funds. Proceed slowly so that you will be successful in the end.

The Level III Goal: Complete Financial Self-Sufficiency

With the Level III Goal, the cash flow from your rental properties completely pays for your lifestyle once the mortgages are entirely paid off. You are completely self-sufficient, whether or not you have additional income from any other source. If the stock market tanks, you will be fine. If your promised pension vanishes, you will be fine. If your Social Security checks are slashed, you will also be fine.

In fact, if you achieve the Level III Goal, you will be better than fine. In addition to sustainable monthly income, you will have options afforded by greater potential (and eventually kinetic) net worth energy. For example, if you desire early retirement, you may retire as soon as your mortgages are paid off. You also have options in terms of selling and “trading up,” as I’ll discuss later in the book.

The specifics of this goal are to acquire enough properties that, once your mortgages are paid off, your total rental income exceeds your total monthly expenses for those properties plus all of your own personal expenses. Depending on the type of properties you purchase and your geographic region, and your expenses, the Level III Goal may be attainable with a handful of single-family properties or one multi-unit building. We attained the Level III Goal of complete financial self-sufficiency with five properties, a couple of which are rented room by room as house-shares. Once our mortgages are paid off, we will be positioned to retire comfortably, with complete financial self-sufficiency.

Another way of looking at this is that the Level III Goal entails completely replacing your current salary with income from your rental properties once the mortgages are paid off. On the “Total Extra Needed” formula of chapter 3, you will want to leave all the income lines blank. The goal here is to create enough rental income that you will be completely self-sufficient, whether or not these other potential sources of income are present. These other items can be the icing on the cake. Sure, they would be nice, but you won’t have to rely upon them for your survival or to maintain your current standard of living once you stop working.

Bear in mind that, as with the Level II Goal, the Level III Goal takes dedication, work, time, and adequate emergency funds. If you have the opportunity to purchase a multi-family building, rather than several single-family homes, or if you decide to trade up your Level II Goal properties into one apartment building, that will probably get you to your goal faster with less expense, time, and energy, since everything will be under one roof. Even your CapEx will be lower as a proportion of your total income, as discussed in chapter 3, under “Risk #4, the Risk of Costly Repairs.” If an apartment building is your goal, be sure to take time to educate yourself further before taking the plunge!

Beyond the Level III Goal

If the Level III Goal is all about complete financial self-sufficiency after your mortgages are paid off, then going beyond the Level III Goal entails amassing enough property that you achieve this outcome even before your mortgages are paid off.

If you are looking to get out of the “rat race” in the near future by going beyond the Level III Goal and replacing your job with real estate, keep in mind that this takes time and dedication.

Real estate is a long, slow road, and it is work. If your mind is set on going beyond the Level III Goal, then it is important not to give up on your job (and income!). Think of your job as a means to an end, an opportunity to build some initial investment capital for your real estate investing. Your job will also help you qualify for mortgages, which is an important function in and of itself. Finally, your job will support your daily living expenses, until the day your real estate investments can take over, and the surplus income can help stock your emergency fund to prepare for unexpected real estate–related expenses that come up from time to time.

However, going beyond the Level III Goal is only realistically achievable for those who are truly obsessed with so-called financial freedom. It is reserved for those who have a burning desire, dedication, and drive to become very wealthy in either time or money. These characteristics, plus a willingness to take risks, are essential ingredients of investors who have created significant cash flow and amassed significant wealth through real estate. The methods in this book can certainly put you on the path to catapult you beyond the Level III Goal, if this is your desire.

I should note, however, that going beyond the Level III Goal is beyond my aim in writing this book. My mission is simple: It is to help working adults across all walks of life reclaim their retirement dreams and protect their late-life financial security through retirement diversification using the powerful tool of even just one income-producing rental property.

Don’t be pushed by your problems.

Be led by your dreams.

RALPH WALDO EMERSON

Essayist and Transcendentalist (1803–1882)

Decisions, Decisions

If you are not sure where to start, it is probably best to simply start with the Level I Goal. You can always decide later whether to proceed to Level II or III. If you have already achieved the Level I Goal of owning one rental property, you have conquered your initial fears and gained some experience as a landlord and property owner. If this is your case, and since you are reading this book, you are clearly ready for the Level II or Level III Goal. In fact, I believe that real estate investing might be a little like getting a tattoo. While I am tattooless myself, I’ve heard that once you have your first tattoo, you are on the lookout for your second, and then your third. . . .

Still others may want to leapfrog right over the Level I Goal by buying a multi-family home or apartment building. This is what Alfredo and Rose (see Online Appendix B) did when they bought an apartment building and moved into one unit. This is not necessarily the easiest or most gradual approach; however, it could get you to the Level II or III Goal in one move if that is your desire.

Setting and achieving a Level I, II, or III Goal could be a pivot point in your life, one away from struggle and stress and toward financial safety, comfort, or even complete self-sufficiency in your later years. And with that, now that you’ve selected your Goal, it is important to set yourself up to actually achieve it, which is my aim in presenting the next chapter: “Why Did the Chicken Cross the Road?”

![]()

Set your mind on a definite goal and observe how

quickly the world stands aside to let you pass.

NAPOLEON HILL