8

OWN A CHICKEN

How to Get Your First (or Next) Rental Property

This chapter is all about getting your chicken: that is, your own egg-laying rental property. As you’ll see in this chapter, whether you are seeking your first rental, your second, or your fifth, there are many different ways to acquire it. You can:

1. Find the golden chickens in your life

2. Do a traditional purchase

3. Think outside the box (or chicken yard!)

4. Put your nest egg to work

5. Put your chicken to work

If this sounds mysterious, don’t worry. I’ll explain each of these five general ways in this chapter. Keep reading! Buying or acquiring your first (or next) rental may not be as hard as you think.

![]()

Our only limitations are those we set up in our own minds.

NAPOLEON HILL

FIND THE GOLDEN CHICKENS IN YOUR LIFE

There are many ways to acquire rental property without actually spending money of your own. You just need to find the golden chickens that are already in your life. As you will see, these moves are not rocket science, nor are they the privilege of the elite class. These are quite basic moves. They are the building blocks behind many investors’ success, both in getting started and in continuing to build financial safety, comfort, and even self-sustainability for the long term.

Move (and Keep Your Old House as a Rental)

If you own your own home, the easiest way to acquire your first investment property is simply to move and convert your existing house to a rental. In fact, as you will see from reading the stories of real-life people I call “not-chickens” in Online Appendix B, this is without question the most common way most of the people whom I interviewed for this book acquired their first rental. (It’s also how we got started ourselves.) Converting your existing home into a rental is an excellent, fairly simple, and relatively affordable way to acquire a rental property without actually purchasing one from scratch.

Many people assume they need to sell their house when they buy their next one. This isn’t necessarily true, especially if you are able to take advantage of a low-down-payment mortgage (see the “Think Outside the Chicken Yard” section of this chapter) or another low- or no-down-payment strategic move as described in this chapter. Many people also fear that tenants will destroy their beloved home. The cure to this fear is a matter of shifting one’s mindset from viewing it as a home to thinking of the property as a long-term investment. The house is still the same house—it’s just that its function has shifted.

Converting your existing home into a rental makes sense in many life stages. Perhaps you are midlife and eager to move up from that starter home that you purchased when you were younger. Maybe you’ve finished raising your children and are ready to downsize. Or perhaps you’ve been relocated or you’ve accepted a job in another state. Whatever the case may be, and whether you are planning to move near or far, consider hanging on to your home and renting it out rather than letting go of it.

The main deciding factor should be whether the expected rent will cover your anticipated expenses. Since you know your home intimately, you probably already have a pretty good idea of the expenses. The next step is to do your research to get a feel for what your home may be worth in terms of the market rent. If you have reason to believe—after checking with a realtor or doing your own research on Craigslist, Zillow, or another rental platform—that the rent will be greater than your mortgage payment and other expenses, then the decision is easy. Keep it. In fact, it is a brilliant way to get around the fear hump in terms of going out and purchasing an investment property from scratch. Simply converting an existing home into a rental can significantly ease that transition and speed up your achievement of the Level I Goal.

If you wish to move and keep your existing home as a rental, it is essential that you contact your mortgage holder. Explain why you would like to move. If you have a Federal Housing Administration (FHA) loan, you are probably fine as long as you’ve occupied the house for at least a year. Other types of loans can vary. However, it is important that you talk to your bank in advance, because with some loans, if the lender discovers that you’ve moved, they have the right to call the loan due in full. It’s always safest to call and get permission, in advance, before you move and rent out your home.

I should mention here that there is a powerful piece of the U.S. tax code called the “Primary Residence Exclusion” (PRE), which allows you to sell your home without paying capital gains taxes, as long as you meet certain criteria.1 To qualify, you need to have lived in your home for at least two of the past five years. In addition, the profit from the sale of your home must be less than $250,000 if you are single, or less than $500,000 if you are married and file jointly.

Many people assume that they need to buy a more expensive new home for themselves in order to take advantage of the PRE. Others just assume it’s something they should do. The truth is that, if you decide to do a PRE, you can do whatever you like with the proceeds. If you are considering a move, I encourage you to consider all your options.

The first option is probably the most common use of the PRE: Sell your first home, tax-free, and use the proceeds from the sale to afford the down payment on a next home, usually (though not necessarily) of a higher price tag. Depending on your stage of life and if, for example, you are aiming to move to an area with better schools, this might be a very real priority. However, keep in mind that if you do this, you may be trading one liability for a greater liability (with a potentially more expensive mortgage, tax bill, utility bill, etc.). That said, since there is no limit to the number of times you can benefit from the PRE, you can always sell your new home down the road (after at least two years), tax-free, and then downsize and/or buy an investment property with the proceeds.

This brings us to the second option. If the numbers work out, you can keep your existing home and turn it into a rental property. If you choose this option, you will have converted a liability (since your house costs you money each month) into an asset (by generating monthly income). Plus, depending on your income, this could lower your income taxes each year or increase your refund, due to your being able to write off the depreciation and other deductions. (See the “Taxable Income” section of the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide available at www.GetaChicken.com.) If you convert your home to a rental, again, there is flexibility. You can still sell your property using the PRE if you do so within three years of operating the home as a rental (as long as you lived in it for at least two years prior to that). If you are past the three-year mark of renting it out (assuming, again, that you lived in it for the two years prior to that), then you have the option of trading into another investment property using the 1031 Exchange, another tax-free method for selling property, which is discussed later in this chapter at length. You can also keep the property as a rental, indefinitely, and continue to pay off the mortgage so that it may provide extra income and additional options further down the road.

As a third option, you can sell your home and purchase another investment property, tax-free, using proceeds from the PRE. Simply use the profit from the sale of your home to buy a single-family home, multi-family house, or apartment building. If you go with a multi-unit option, you can live in one of the units, if you want to, although you don’t have to, of course.

Table 8.1 shows the comparison between the three options just discussed. If you like the idea of the second or third option, don’t forget to run your numbers! (Again, check out my free Cash Flow Analysis [CFA] Tool at www.GetaChicken.com.) Remember, it’s only an asset if the rental income is equal to or greater than all of the monthly expenses, combined.

TABLE 8.1. COMPARISON OF THE TYPICAL “PRIMARY RESIDENCE EXCLUSION” (PRE) MOVE VERSUS TWO OTHER OPTIONS (ASSUMING RENTAL INCOME SURPASSES RENTAL EXPENSES)

When Two Hearts Become One

It is often the case that when two formerly single, divorced, and/or widowed individuals fall in love, they each have their own home. Rather than seeing this as a problem, see it as an opportunity! Instead of selling one house and moving into the other, consider keeping one as a rental. Even better, start fresh in a new home together and keep both properties as rentals. Just because two hearts become one doesn’t mean that two houses must also become one. Instead, let them become three!

Save the Family Home

Have you, or you and your siblings, recently inherited the family home? If so, I recognize that this inheritance comes with the loss of someone who may have been very dear to you. It may be hard to let go of the home that is filled with memories. In fact, I believe you should seriously consider keeping it, especially if it is completely paid off. Even if it’s not, if the potential rent is equal to or greater than the monthly expenses and/or if it will be paid off within the next couple of years, then you should seriously consider keeping it as an asset. You may want to hire a property management company if you are worried about the work involved in managing it or unfairly burdening one sibling. A property manager will take on the job of finding a tenant, collecting rent, attending to repair needs, and depositing money directly into your and your siblings’ bank accounts each month.

Save Your House from Foreclosure

If you are at risk of losing your home to foreclosure, time is of the essence. For whatever reason, if you can no longer afford your payments, then you may have a couple of options. The first option is to create extra income by renting out a room or part of the house and informing your lender about this plan to become current on your payments.

Another option is to rent out your entire home. The simple fact that you can’t afford your payment doesn’t mean there isn’t someone else out there who can. If you are at risk of losing your home and if you can rent it out for at least your monthly mortgage payment, I urge you to not passively let the bank take your home. Instead, consider quickly renting another (more affordable) place for yourself, cleaning up your home, and renting it to someone else. Note that if it feels too tight, financially, it may work out better to rent out the rooms in your home separately as a house-share to generate substantially more income (see chapter 7). Again, notify your lender of your plan to become current and check with your local property registration office to be sure you are in compliance with local laws and filing requirements.

Saving your home and renting it out will benefit many people. Your new tenant will benefit from the housing that you are able to provide. You will benefit by not destroying your credit, by keeping your home for the long term, and by converting your home into an asset. Your neighbors, and their property values, will also benefit by your avoiding foreclosure. Eventually, you will find yourself actually making money off the house that you once came so close to losing.

Save Your House from a Custody Battle or Loss in Divorce

If your marriage or significant relationship is on the rocks, you may want to try to do something to save it. Whether it’s getting healthy, getting counseling, enrolling in an Imago workshop, or checking out “hot yoga,” you just never know. It just might be possible to resuscitate your relationship. But . . . if “over” means over, then, if you own a home with your ex, you will need to decide what to do with that home. Assuming you are still capable of making decisions together, then you might want to consider keeping it as a rental and hiring a property manager. The property manager can issue two separate checks (or direct deposits) and two separate sets of monthly reports. Depending on your relationship with your ex, this may or may not sound like a realistic idea. If your ex wants nothing to do with you or the house, then by all means take the house (as long as the cash flow works out positively)! You can turn it into a rental or house-share yourself if there is positive cash flow and make lemonade from this lemon-like situation.

Use a Home Equity Line of Credit (HELOC)

Whether you’re buying your first investment property, or a next one, a common and powerful strategy is to use the equity in a property that you already own as funds for the down payment on the next. You’ll see from reading the stories of other “Not-Chickens” (Online Appendix B) that many of the people I interviewed have used this strategy to advance to the Level I, II, or III Goal and enjoy a consistent stream of income in their retirement years.

There are generally three ways to leverage your existing property to purchase rental property, without having to come up with money out of your own pocket, for the down payment:

1. Refinance your existing property (personal residence or rental property) at a higher amount and use the additional funds for a down payment and closing costs.

2. Obtain a tax-deductible home equity line of credit (HELOC) on your primary residence.

3. Open a tax-deductible home equity loan on your primary residence.

Your choice will depend on a number of factors. If you have a low interest rate on your first mortgage, or if you are several years into your loan, refinancing may not be the best route. In this case, a second mortgage in the form of a HELOC or home equity loan may be best. The downside to a HELOC, however, is that the rate is variable and as interest rates go up, so does your payment. If it’s possible to refinance at a lower term length—for example, jumping from a thirty-year term to a fifteen- or twenty-year term—while also pulling money out at a low interest rate, then this would be an ideal scenario for refinancing.

Your options will depend on what interest rates are doing at any given time, a factor that is out of our control. Get a range of numbers from your mortgage broker or banker (such as the interest rates and associated payments at different term lengths and total values) and spend some time doing the math. Remember, too, that doing a refinance will cost you some money, including the cost of a new appraisal. Ask your mortgage broker or banker if any of the closing costs and fees can be wrapped into your new mortgage and what that associated payment would be. In the end, it may very well be worth it; however, these costs should be factored into the equation.

It is essential that you do some additional math before initiating this move. Your cash-flow calculations must always include the total amount financed from all sources. In this strategy, the total amount financed should include your new property’s primary mortgage payment plus the extra amount that you will be paying each month on your existing property. Add both together and complete the Cash Flow Analysis (CFA) Tool on my website at www.GetaChicken.com to determine your monthly cash flow and return on investment before moving ahead with this move.

The housing crash that began in 2007 taught us all an invaluable lesson about converting property equity into cash to pay for fun stuff that doesn’t pay you back. However, recall from chapter 4 that debt used to purchase an income-producing asset is actually good, productive debt. When you take action, in this way, to purchase a good, cash-flowing rental property, then you are joining a select—but not altogether uncommon—club of individuals who have created lasting wealth by leveraging resources they already own . . . in other words, by using the golden chickens already in their lives.

TRADITIONAL PURCHASE

Using a Real Estate Agent or Broker

The most common way to purchase rental property is with the assistance of a licensed real estate agent or broker. Working with a good real estate agent can be very advantageous. For one thing, real estate agents are professionally trained in all aspects of the home-buying process, so you can rely on them to be your advocate through the entire process, from the offer to the inspection to the closing table. They also have access to those little black lock boxes that are on every house listed on the retail market. Your agent has access to literally all homes that are listed on the market, even bank-owned foreclosures. This means that you and your agent can go and view a ton of properties and get a feel for the market, even in just one afternoon.

Here are some tips for using a real estate agent or broker to buy a rental property:

1. You are not required to sign an exclusivity agreement with a buyer’s agent to work together. However, as a matter of integrity, if you want to submit an offer on a given property, it is important that you go through the agent who originally showed it to you.

2. Know what you are looking for, share your criteria with your agent, and be stringent about adhering to your criteria. (Use the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide at www.GetaChicken.com to design your criteria for your ideal rental property.)

3. View as many properties as possible in your key geographic areas. Get to know your key areas inside out and get to know the types of properties, and their property values, that are typical in those areas. If you start feeling pressure from your agent to hurry up and “just buy something,” or if he or she hints that you are wasting their time with low offers or multiple viewings, then you should simply quit and find another agent.

4. Make offers on many properties. Ultimately, one will be accepted.

5. Keep your offers low. Aim for 20 percent lower than market value. Only make offers or accept counteroffers that fall within your cash-flow parameters.

6. Say no to creep! What this means is that if your upper bound is $200,000, don’t go a dollar over $200,000. You need to stay in control. Otherwise, in negotiations you will find yourself agreeing to a higher and higher price tag. If this property doesn’t work out within your financial parameters, don’t worry. Another one will.

7. Never get attached to investment property. If it doesn’t make sense financially or isn’t practical for some other reason, just move on.

Mortgages

The mortgage is what separates real estate investing from other means of investing. The power of real estate is that you are able to borrow money from a bank, or another lender, to purchase an income-producing asset, that would otherwise be completely unattainable, but that you eventually own in full. Not only can you use a mortgage, almost everyone does. In fact, nobody expects you to buy a property with “all cash,” though that certainly is an option if you happen to have the means and want to hit the ground running in terms of strong cash flow.

This means that rather than footing the entire cost of the property, we only need to come up with money for the down payment. The down payment is the portion of the purchase price that you typically must pay from your own funds to demonstrate to your lender that you will not walk away from your obligations to pay your mortgage. The bank likes you to have a little skin in the game. Whether it’s for our personal residence or our Level I, II, or III Goal, it is the mortgage that makes our dreams possible. It is the paying off the mortgage(s) that makes our dreams come true (The Ultimate Goal).

When it comes to purchasing a property that you plan to use for rental purposes, if you go with a conventional bank you have very few options in terms of the amount you will be required to provide as a down payment. Usually you will be required to provide 25 percent of the purchase price. That said, there are a number of options for a noor low-down-payment mortgage on an investment property, which I cover, later in this chapter, under the section “Think Outside the Box (or Chicken Yard!).”

Remember that the short-term goal of your investment property is to generate cash flow. The lower your down payment is, the higher your mortgage and the lower your cash flow will be. This means that if you use a lower-down-payment program, be sure the cash flow works out. As long as your interest rate is fixed and you are in an area with strong rental demand, you should have no issues meeting your monthly mortgage obligation and paying down your mortgage with the Ultimate Goal of paying it off.

Understanding Your Monthly Payment

Each monthly payment is typically composed of four elements: principal, interest, taxes, and insurance. These four elements are often referred to by the acronym PITI.

![]() Principal: The P in PITI is your principal. This is the portion of your payment that goes toward the total amount remaining on your loan (also referred to as the principal) with each payment. The principal component of your PITI directly lowers the amount that you owe on your total balance each following month. Over time, as the overall amount owed becomes smaller, your equity increases (assuming your property does not go down in value).

Principal: The P in PITI is your principal. This is the portion of your payment that goes toward the total amount remaining on your loan (also referred to as the principal) with each payment. The principal component of your PITI directly lowers the amount that you owe on your total balance each following month. Over time, as the overall amount owed becomes smaller, your equity increases (assuming your property does not go down in value).

![]() Interest: The first I in PITI refers to the “interest,” or the amount you pay to your lender, with every payment, for the privilege of having a mortgage with them. It’s basically your (non-optional) way of saying “thank you.” After all, it’s your lender who has made it possible for you to purchase this property in the first place. It’s an expensive thank-you, but ultimately this thank-you will be paid by your tenants, on your behalf, with their monthly rent, as I’ve explained in chapter 3, “Why You Need a ‘Chicken.’”

Interest: The first I in PITI refers to the “interest,” or the amount you pay to your lender, with every payment, for the privilege of having a mortgage with them. It’s basically your (non-optional) way of saying “thank you.” After all, it’s your lender who has made it possible for you to purchase this property in the first place. It’s an expensive thank-you, but ultimately this thank-you will be paid by your tenants, on your behalf, with their monthly rent, as I’ve explained in chapter 3, “Why You Need a ‘Chicken.’”

You can shop around for the best interest rate to a certain degree, or pay “points” at the time of closing for a lower rate. A point simply refers to an amount of money equal to 1 percent of the total loan amount. Two points correspond to 2 percent of the mortgage amount, and so on. Each point typically reduces the interest rate by one-eighth to one-quarter of a percentage point.

![]() Taxes: The T in PITI refers to the real estate property taxes that are owed to your jurisdiction. They are usually held in escrow by the bank and folded into your mortgage payment. Bear in mind that as your property value increases over time, it is not uncommon for your property taxes to creep up as well. If you believe your assessed value (for taxes) is higher than the actual or appraised value, then you usually have the right to appeal.

Taxes: The T in PITI refers to the real estate property taxes that are owed to your jurisdiction. They are usually held in escrow by the bank and folded into your mortgage payment. Bear in mind that as your property value increases over time, it is not uncommon for your property taxes to creep up as well. If you believe your assessed value (for taxes) is higher than the actual or appraised value, then you usually have the right to appeal.

![]() Insurance: The last I in PITI refers to insurance, specifically property or homeowner’s insurance. All conventional lenders require borrowers to insure their property, in the event the asset experiences some kind of trauma that affects its value. You can shop around for different insurance quotes to find one that works best for you.

Insurance: The last I in PITI refers to insurance, specifically property or homeowner’s insurance. All conventional lenders require borrowers to insure their property, in the event the asset experiences some kind of trauma that affects its value. You can shop around for different insurance quotes to find one that works best for you.

Be sure to enter all these factors into your Cash Flow Analysis (CFA) Tool at www.GetaChicken.com. You can plug in the various terms of the loan (term length, interest rate, and total loan amount) and it will calculate your actual monthly payment (principal and interest portions only).

Selecting Your Mortgage Term

Whether you are purchasing a new property or refinancing one that you already own, you generally have four options regarding the length of your mortgage: ten, fifteen, twenty, and thirty years. These terms equate to the number of years until your asset will be completely paid off. Shorter terms get you to your goal faster, but have higher payments, which lessen your monthly cash flow and increase your overall risk.

Make sure to compare the payments associated with different mortgage options carefully before selecting a product. If you are concerned about safety, you will want to select a more conservative term like a thirty-year mortgage. This keeps your monthly payment lower than the alternatives and increases your cash flow. You always have the option of paying it down faster, if you like, for example at the payment amounts associated with the ten-, fifteen-, or twenty-year mortgages. However, when cash flow is tighter or if times get tough, you can always simply resort to your actual thirty-year payment amount.

If you have sufficient potential cash flow, you may want to select a lower-term mortgage so that you can be ambitious in paying down your principal and building equity. This will help you achieve your Ultimate Goal of having one income-producing property owned free and clear. If you are a Level II or III Goal investor, you can eventually use the equity to purchase additional property.

Note, however that it is often the case that a ten-year mortgage has the same interest rate as a fifteen-year mortgage. This means that there would be no clear advantage to locking yourself into a ten-year rate with a higher payment. Rather, it would be better to secure the same rate on a fifteen-year product and then, if your cash flow allows, pay the principal down using the payment amount associated with the ten-year mortgage. The fifteen-year mortgage will be safer and provide more flexibility than the ten-year mortgage, at no cost in the interest rate.

Creative Mortgages—A Cautionary Word

I love creativity! From the arts to ideas to inventions to personalities, creativity is what makes each of us interesting. It’s what makes our whole world interesting. However, when it comes to mortgages, you are better sticking to the plain vanilla “fixed-rate mortgage” of whatever length best meets your needs.

There are several different types of so-called “creative” mortgages that had a heyday during the housing bubble of 2005–2007. In large part, they (and the unscrupulous mortgage brokers issuing them) are responsible for the bursting of that housing bubble.

The three most common creative mortgages are balloon, interest-only, and adjustable-rate. At best, unlike fixed-rate mortgages, these products offer no protection against the forces of inflation over time. At worst, they can be downright lethal.

Balloon mortgages are mortgages in which, after a set period of time making payments, the entire balance of the mortgage becomes due in full, also known as “ballooning.” Some people get balloon mortgages intending to sell or refinance before the remainder of the loan is due. However, if the market changes and the value of the property drops, you may not be able to go through with this plan and could be at risk of losing the house. No matter what your intentions are, it is risky to get a balloon mortgage.

Interest-only mortgages are mortgages in which the principal is never paid down (unless you proactively make extra payments). Also, similar to a balloon mortgage, interest-only mortgages become due in full at some specified point in the future. In other words, you could be stuck with the original balance of your mortgage forever, like a mouse running on a treadmill, until it is suddenly due in full. As I shared in chapter 3, in the “Equity” section, an interest-only mortgage comes with the risk of forcing your property to achieve equity only through appreciation, rather than by paying down the principal. In the event your property doesn’t appreciate in value, and assuming you don’t make extra payments toward the principal over time, the interest-only aspect of the mortgage makes it impossible to gain equity, reduces your options for selling or refinancing, and elevates your risk.

Finally, an adjustable-rate mortgage, also called an ARM, is a mortgage that boasts a low “introductory” interest rate and monthly payment. However, after a given period of time—usually two to five years—the rate and payment can jump up, sometimes dramatically. From there, the rate can continue to increase gradually. There is a “lifetime cap,” or maximum amount to which it can increase, but this cap can be significantly higher than the introductory amount. Sadly, some lenders allow borrowers to qualify for these mortgages based on a seemingly affordable initial payment, rather than the lifetime cap, resulting in an unaffordable mortgage a few years down the road.

To wrap up, I cannot emphasize enough that you want a fixed-rate mortgage for your personal and investment properties. Don’t gamble on these other dangerous types of mortgages that I just described. If you currently have one of these mortgages, it would very likely be in your best interest to refinance as soon as possible into a fixed-rate mortgage. If necessary, you can mix and match a bit—for example, by refinancing two properties and using equity in one to pay the other down to a level that allows it to be refinanced. (See chapter 10 for more refinancing ideas.) Get as creative as you like, but do get out of your creative mortgage.

Whether you think you can or you can’t, you’re right.

HENRY FORD

THINK OUTSIDE THE BOX (CHICKEN YARD!)

Become the Queen Bee of Your Own Hive

If you don’t mind living next to your tenants, you can massively jump-start your Level I, II, or III Goal by buying a multi-family investment property. The property could be as small as a duplex or as large as an apartment building.

What makes this move particularly doable is that you can buy your multi-family personal residence using a low-down-payment program (3 percent) from the Federal Housing Administration (FHA). If you purchase a property that is in the Fannie Mae HomePath program or the Freddie Mac HomeSteps program, investors are allowed to purchase with only 10 percent down. See www.homepath.com and www.homesteps.com for more information and a list of available properties across the United States.

If you are a veteran, a Veteran’s Administration (VA) loan can provide 100 percent financing (in other words, no down payment) if you purchase a duplex, triplex, or four-unit apartment building, as long as you plan to live in one of the units yourself for at least a period of time.2 This can be an excellent way to get started in real estate investing, while paying virtually nothing out of your own pocket as en entry fee and having your rental income pay for your own living expenses. Note also that while VA loans cannot be used to purchase single- and multi-family properties that you do not plan to reside in, they can be used to refinance a rental property that you formerly occupied as your personal residence. VA loans are available even to those who have been affected by bankruptcy or foreclosure.

The immediate appeal of this strategy of buying a multi-family home and living in one of the units is that the rent from the other unit(s) either partially or totally covers your mortgage, thereby reducing your own personal living expenses dramatically! The mid-range appeal is that, after some time, you can either stay or move out. Either way, you’ve got your chicken. The longer-term appeal is that once your mortgage is fully paid off, you will have a fully cash-flowing multi-unit property and you will have achieved the Ultimate Goal.

This strategy of buying a multi-family house and living in one of the units is an extremely common way that people get started in owning rental property. This method can work well for so many types, whether you are younger or older, newly married or freshly divorced, nonparents, parents, or empty-nesters. In Online Appendix B, I share the stories of many individuals and couples who got started in this way. John started as a young single guy looking to save a little money. Deb was newly divorced with two young children looking to start over in a more strategic way. Also check out Alfredo and Rose’s story in which, as newlyweds, they literally leapfrogged over the Level I and II Goals and settled right in with the Level III Goal in one almost breathtaking move. Finally, this is an awesome plan for those who are a little older in years to downsize their living space while acquiring an income-producing asset at the same time. See Enid and Marisha’s stories at www.GetaChicken.com, both of whom are forward-thinking later-life Queen Bees who have created a way to live humbly in their own “all expenses paid” self-built communities.

Similar to the house-share concept, a main benefit of a multi-unit property is that if one tenant leaves, the vacant unit only accounts for a portion of the total income rather than the entire income, as it would in a single-family house. Plus, the CapEx costs will be less than they would be across multiple homes since the components are all under one roof. See chapter 3, Risk #4, the Risk of Costly Repairs, for a review of CapEx. This move comes with two potential headaches. Tax time could be difficult, since personal and investment expenses will need to be separated. Also, you might regret living right next door to your tenants! On the other hand, like Marisha, you may actually enjoy the convenience and potential sense of community that it provides.

People who have used this strategy have literally catapulted their investment goals. After a period of time, usually after a year or two or whenever their lender gives approval, some people move and find a tenant to take their unit. Those with aggressive goals, like John, Deb, Enid, Marisha, and Jake and Mary, have repeated the process with additional multi-family homes. See Online Appendix B for their amazing stories and additional warnings and suggestions.

Buy Your Home with an Investor’s Eye

Another strategy for cleverly acquiring a rental property is to purchase—with an investor’s eye—a single-family home for yourself. The idea here is to use the three critical rental-property criteria (see the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide available at www.GetaChicken.com) to select a property. Then, after a certain length of time, you find a quality tenant, move out, and turn the property into a rental. Before you implement this strategy, it is important to talk with your lender about the length of time that you’ll be required to live in the property before being allowed to convert it into a rental.

The reason this is a powerful strategy is because it costs less to buy a property that you plan to live in (single family, duplex, or multi-unit) than it does to buy one that you plan to rent out from the beginning without residing in it at all. You can get a better interest rate, and you are allowed to use a smaller down payment. Traditionally, the down payment is 20 percent, as compared to the 25 percent that is required for an investment property. However, there are plenty of programs that allow you to purchase a property for your own residence with much lower down payments than the traditional 20 percent.

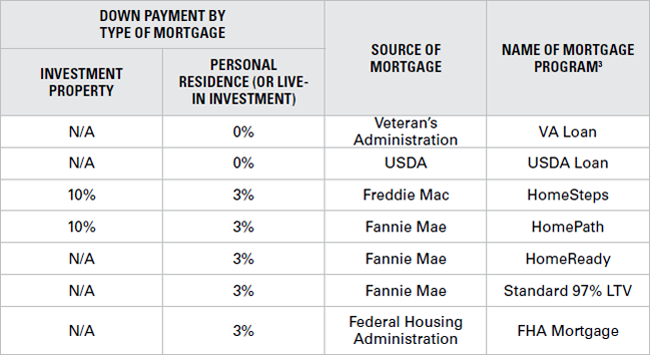

For starters, many cities and jurisdictions have special programs for first-time home buyers. You can find these online by searching “First-time home buyer program” with your city or town name. Many areas also have special low-down-payment programs for teachers, police officers, or veterans. In addition, some areas offer “live-near-your-work” home-buying programs and some universities, hospitals, and companies offer similar programs as well. In addition, Table 8.2 shows a number of different loan options that are available to home-buyers as of the writing of this book.

TABLE 8.2. NO- AND LOW-DOWN-PAYMENT LOAN OPTIONS

The point of this section is to encourage you to be forward-thinking when you buy your primary residence. Rather than simply thinking of your immediate needs, or even thinking of it as your forever-home, if you buy a primary residence with an investor’s eye, then you give yourself options that will last your whole life. Think of what other people, specifically your future potential tenants, will be looking for in a home and what rents they might be willing to pay. When permitted by your lender, and when it makes sense in your life, you will have the opportunity to move out and keep the property as a long-term investment.

Check out the “Determine Your Criteria” section in the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide available at www.GetaChicken.com to help identify the best financials and other qualities for this purchase. Table 8.2 shows a number or no- and low-down-payment options available for the purchase of a property intended as a primary residence (or, in the case of multi-unit properties, for combined investment and personal residence purposes). Compare these down payment options to the 25 percent that is typically needed for property that is purchased for investment purposes from the get-go and it is clear why this such a powerful strategy.

It is worth noting here that—unlike the loans issued in the housing crisis of the 2000s—Fannie Mae and Freddie Mac are now run by the government. These programs are primarily designed to help individuals, whose income supports a mortgage, but who have difficulty saving for a down payment. In the case of a duplex or multi-unit property, the income from the rented units is allowed to count toward your qualifying income. If you are using one of these no- or low-down-payment options to purchase a new primary residence, be sure that the interest rate is fixed and that your job is stable, to ensure that you can continue making the payments for as long as you keep it as a residence.

Purchase with Seller Financing

With seller financing, the seller plays the role of the bank. Also called owner financing or a “purchase-money mortgage,” this move entails making payments directly to the person who is selling you their property, at a given interest rate, over a certain period of time, just as you would make payments to a bank. The main benefit to the buyer is that the terms are more negotiable than what you typically find with bank financing. Seller financing can be used for either a portion of the total purchase price of a property or the whole amount. In fact, everything is negotiable with seller financing. This is because the agreement is only between you and the seller. As long as both parties agree, the sky is the limit in terms of how creative you can get. Be careful, however, not to get into a creative mortgage, like one of the three types I described earlier in this chapter, where your payment jumps up after a period in time or where your entire loan is due after a specified time period. Be sure to run everything by an accountant before you proceed, and have a lawyer draft or review your seller-financing document.

Seller financing can come in handy if you have trouble qualifying for a standard mortgage or if you’ve maxed out the number of mortgages that you are allowed. Note that while most banks have a five-mortgage limit per borrower, some small banks (shared within the Online Appendix C, Recommended Reading and Other Resources) are less restrictive. There are also fewer closing costs at settlement since many of the loan origination fees are eliminated for the buyer, accounting for nearly 2 to 5 percent of the total loan price.

Seller financing has benefits for the seller, too, of course. These are good to understand as you pitch the idea to potential sellers and in the event you want to provide seller financing to someone else one day. First, if an owner is eager to sell, this expands the available options for the owner and allows him or her to avoid having to list the property. It also provides payments with interest and has the tax advantage of spreading out the seller’s capital gains over multiple years, rather than taking them all in one lump sum the year of the property sale. Another tax benefit to spreading out the gains is that it may prevent the owner from getting bumped into a higher tax bracket. Finally, if the seller is older in age, seller financing can be a way to provide for one’s loved ones by ensuring a continuous stream of income after death without them having to deal with property management.

While seller financing might sound like a gimmick reserved for late-night “no money down” infomercials, it is more common than you may realize. It is estimated that about 10 percent of homes sold in the United States involve some sort of seller financing.4 And yet, keep in mind that in spite of the benefits, if you are able to strike a seller-financing deal, it is important not to sacrifice your criteria in terms of the quality of the home and your cash-flow requirements. You do not want to end up with the headache of “one person’s trash” if they were unable to sell the property to anyone else. As an example, we once landed a seller-financing deal with the owner of a large rental property portfolio. This good-humored, older gentleman agreed to sell us his two-unit property, with financing of 80 percent of the purchase price. We put the property under contract with a $1,000 earnest-money deposit, fully refundable if we were not completely satisfied with the results of the property inspection. (See the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide at www.GetaChicken.com for other essential escape clauses to include in your contract.) Indeed, the inspection revealed an excessive amount of deferred maintenance and old systems, basically a looming CapEx nightmare (see chapter 3), so we backed out and our deposit was returned.

Purchase Your Landlord’s Rental

Are you currently renting either a single-family home or an apartment in a multi-family home that you wouldn’t mind owning? Or do you have older kids or a college student who is renting a place that you would consider owning or even jointly purchasing with your daughter or son? If so, then a very smooth move for acquiring real estate is to approach the landlord about purchasing the property.

This is not such an unusual strategy. After all, in many areas, your landlord is actually required by law to give you the “first right of refusal” if he or she plans to sell their single family home. With yourself, or your grown children, as the “owner occupants,” you will be able to get better terms than purchasing as an investment. For example, the down payment will usually be smaller and the interest rate will usually be a bit lower. Refer back to the “Buy Your Home with an Investor’s Eye” section of this chapter.

Whether you approach the landlord or whether the landlord approaches you (or your daughter or son), you might want to ask the landlord about the possibility of seller financing. Since you are a known entity to the landlord and have ideally been making the rent payments faithfully and on time, the landlord/owner may be willing to provide a loan in place of a traditional lender’s mortgage. This “seller financing” option, just discussed, means that you could potentially buy the property with a smaller down payment than you would need with a regular bank. Depending on the willingness and helpfulness of the landlord and if the property is owned free and clear of a mortgage (and your negotiation skills!), you may not need to come up with a down payment at all.

Remember, everything is negotiable. If your landlord trusts you and has no urgent need for the entire proceeds from the sale, he or she may be interested in providing some financing. Remind the landlord that if you default on your loan, the property would simply revert back to him or her. Make sure to have everything drawn up in writing and be sure that the property fits in with your ideal purchase criteria. (Again see the R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide at www.GetaChicken.com.)

After you are the proud owner of your landlord’s property, you may want to use the house-share strategy of renting out extra rooms in your home, as discussed in chapter 7. Eventually, when it comes time for you (or your kids, if you are the parent) to move out of this home, you can keep it and rent it out or you can trade up into another property, tax-free, using the PRE discussed earlier. Whether or not you buy or rent your next home after you ultimately move out, you will likely be further ahead than if you had not purchased the property. Even if you become a tenant again, you will benefit from the tax advantages of owning investment real estate and you will benefit in the long term by having a cash-flowing asset with a mortgage that your tenants are gradually paying off on your behalf.

![]()

If there is something to gain and nothing to lose

by asking, by all means ask!

W. CLEMENT STONE

Entrepreneur and “New Thought” author (1902–2002)

Lease/Sublet with Option to Buy

The “lease/sublet with option to buy” is similar to the lease/sublet discussed in chapter 7, except you have the added benefit of being allowed to purchase the property within a certain window of time, if you wish. The lease/sublet with option to buy is a way of acquiring a property for a long-term investment rather than using it only as a time-limited source of monthly income.

The lease/sublet with option to buy is similar to—yet also different from—other real estate arrangements that you may have heard of, such as “rent to own,” “rent with option to buy,” and “lease option.” Rent-to-own and renting with option to buy are most commonly used in reference to a tenant renting a home and having the option to buy it within a specific period of time, if they so choose. “Lease option” can also mean this; however, the term has been given new meaning by Wendy Patton, author of Investing in Real Estate with Lease Options and “Subject-To” Deals. Using her method, an investor can use a lease option to make money as a matchmaker between a buyer and seller in a rent-to-own arrangement.

However, our goal is to create sustainable income for the long term, and the lease/sublet with option to buy can be an excellent entry point for this goal. Before taking ownership, you have the opportunity to gain property management experience (if you don’t already have it), test out the property (and discover any potential chronic issues), and test out the rental market, all while boosting your own personal monthly income or saving up for the down payment. It is critical that your agreement with the owner specifies that, as in a lease/sublet, he or she is responsible for all maintenance and repair costs during the period of time before you own the property. Then, if and when you decide that you want to move forward with the purchase, and assuming you are able to line up financing to purchase the property, you go to settlement with the seller, and the property officially becomes an important part of your long-term retirement portfolio. However, if, for any reason, you don’t want to purchase the property, you do not have to exercise your option to purchase. At this point, depending on the structure of your agreement and your desires, you could either continue operating it as a lease/sublet or you could part ways with the seller.

You have a number of options for financing the purchase, should you decide to move forward. You can use conventional financing from a bank or mortgage broker. Or you can ask the owner of the property if he or she would be willing to provide financing. Your chances of a “Yes” are greatly enhanced if you are consistent and flawless in your rent payments (using automatic monthly withdrawal from your bank to ensure this!) and if you consistently maintain an attitude of respect and helpfulness with the owner. Some sellers may agree to provide financing, while others will be eager to sell their property, collect their money, and move on with their lives.

Share the Wealth (Partnering)

Partnering is a common financial strategy, especially among more seasoned investors. Equity partnerships mean that all partners are co-owners and are entitled to a share of the distribution of the profits (rather than working for a fee or a salary). Roles in an equity partnership can be shared and/or divided in any number of different ways. In one version, sometimes called an “elephant and mouse” partnership, one person (“the elephant”) finances the property, while the other (“the mouse”) invests his or her time in all aspects related to managing the property. They typically split the profits 50/50. This can work out equally well for those with more money but less time, as well as those with more time but less money.

There are many potential pitfalls to partnering, so it is best to sit down together and write down all the details of your agreement. Discuss all potential situations and worst-case scenarios that you can think of, and decide in advance how you would handle each. Meet with your own accountant and lawyer to further understand how things could unravel and how to best protect yourself and your personal assets if they do. Finally, an independent lawyer should draw up the understanding into a legal operating agreement, which should also be reviewed by your personal accountant and lawyer before you sign on the dotted line.

![]()

Surprise your doubts with action.

DANIELLE LAPORTE

PUT YOUR NEST EGG TO WORK

There are many ways you can purchase investment property using resources that you might not realize you have. When it comes to leveraging (and diversifying) your retirement accounts, you have a few options, though your choice will be guided by where your money currently resides. If you have a 401(k) or another type of employer-sponsored retirement plan, you can loan yourself money. If you have an IRA or self-employed 401(k), you can convert a portion of your account into a self-directed retirement account that allows you to invest in real estate. Finally, if you are over age 59½, you can use your retirement funds—wherever they reside—to buy a rental property. The following section goes into each of these options.

Loan Yourself Money from Your 401(k)

If you have a retirement plan through your employer, or former employer, then you are in possession of a valuable resource. The same is true if you have a self-employed “solo” 401(k). And yet, if you are like the vast majority of people, you will let that resource sit there on autopilot for decades, almost forgetting about it, while it builds slowly over time.

There is another option. And I’m not talking about early withdrawal. After all, pulling money out of these retirement accounts before age 59½ comes with a 10 percent penalty, a loss of money that is rightfully yours. Rather than withdrawing money early, I’m talking about a very different thing: loaning yourself money to purchase an investment property.

In this strategy, under current regulations, you can access up to $50,000 or half of your account value, whichever amount is smaller. You have the ability to use this loan any way you wish; however, I’m only recommending that you use it to purchase cash-flowing rental property. The interest rate is typically very low and—believe it or not—the interest payments go right back into your own account. You are literally a bank unto yourself in this move. You typically have up to five years to pay yourself back, which means that even though the interest rate is low, the payments are relatively high. Needless to say, the monthly loan repayment amount must be factored into the cash-flow analysis equation when you are deciding whether to undertake this strategy.

If you use this method to purchase a rental property, you will create two asset streams, from where there had formerly been just one. When you take a loan from your 401(k) or similar type of retirement account, you are literally giving yourself “seed money” for the down payment on an income-producing property. Then you are obligated to pay yourself back, on a monthly basis, over the course of five years or less. However, again, since you are both the lender and the borrower in this case, the small interest payment actually goes back into your retirement account.

If you opt for the relatively slow train of paying yourself back over the entire five years, then you use the cash flow from your rental to make the minimum payments. Then, if you were so inclined, you could systematically use this strategy to acquire a new rental every five years.

However, you don’t need to take the whole five years to pay back your 401(k) loan. There are a few other options. For example, if you buy below market value, or if you improve your property in a way that increases its value, then you may be able to refinance the entire amount (your primary mortgage plus your 401[k] loan) into a new mortgage and pay your account back that way. You typically need to wait until the property has “seasoned” for at least 365 days before refinancing. This is because if you get an appraisal within one year after purchasing it, the appraisal will usually include the price that you paid for the property as one of the comparable properties.

Another option, if you have equity in another property, is to refinance that other property at a higher amount and use those extra funds to pay off your 401(k) loan. Again, be sure that the refinanced amount fits into your cash-flow calculations for your property or your overall portfolio.

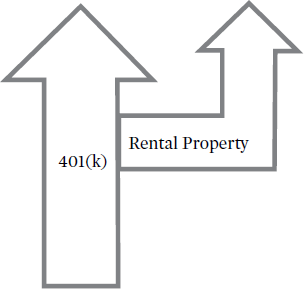

Once you’ve paid back your 401(k) loan, you’ll then have a 401(k) plus a rental property, rather than just a 401(k). See Figure 8.1. As you’ll read in Online Appendix B, Jen and Rachel have used this strategy a couple times, as have we. It is an excellent way to put your retirement funds to work in achieving the Level I, II, or III Goal. Loan to self, purchase, improve, rent out, refinance . . . and—for the Level II and III Goals—repeat!

FIGURE 8.1. USING ONE RETIREMENT ACCOUNT TO CREATE TWO ASSET STREAMS

There are two main considerations when thinking about a 401(k) loan. The first is whether your numbers will work well enough to keep you afloat for the five-year period in which you are paying yourself back. If there is any uncertainty in your numbers—particularly in terms of the rent you will be able to charge—then you may not want to embark on this kind of move. Don’t be overly optimistic when running your numbers. For example, always run your numbers with the rent at the lowest end of the realistic range. If they still work, then this could be an excellent way for you to acquire a property.

The second consideration is that the amount that you loan yourself will be taken out of the stock market until you have paid yourself back in full. This means that if there is particularly strong growth in the stock market, you will miss out on that period of escalation. On the other hand, stepping out of the stock market is not always a drawback. For example, if the stock market is in a period of either flat growth, volatility, or outright decline, then this move could be an excellent way to pull out temporarily by essentially moving your money to “cash” (out of stocks) while making it productive at the same time. The challenge is—of course—predicting whether stocks will go up or down, a task that befuddles even the most expert financial analysts! That said, the goal here is not to attempt to time or predict the market: The goal is to leverage your existing resources to acquire a tangible asset for a truly diversified long-term retirement plan.

As a last note of caution, please recall—from chapter 4—the difference between assets and liabilities. Loaning yourself your precious retirement money, to purchase items or experiences that do not generate income, will only put you further behind and jeopardize your long-time financial safety. This strategy described here is reserved only for the acquisition of cash-flowing rental property.

Self-directed IRA (Roth and non-Roth)

If you have a sizable IRA (either Roth or non-Roth), you might want to consider rolling a portion of it into a self-directed Roth or non-Roth IRA. Rather than leaving all your eggs in one basket, you can diversify by buying a cash-flowing rental property with your IRA funds, just as we did.

The self-directed IRA is a well-kept secret, known only to the most savvy real estate investors but available to all. The self-directed IRA allows you to control your own retirement funds, rather than simply parking your money with a mutual-fund company. Once you’ve transferred a portion of your IRA funds into a new self-directed IRA account, you are allowed to invest this money however you like. In addition to purchasing real estate, some self-directed IRA companies allow you to invest in other things such as stocks, precious metals (silver, gold, platinum), oil, restaurants, your best friend’s start-up company, and the like. You can even play banker by lending money and collecting payments with interest.

In addition to the freedom to invest in creative ways under your own direction, there are other reasons that people like to invest with a self-directed IRA. The first is simply that this happens to be where they have the bulk of their savings. They may not have a lot saved up anywhere else, but they may have an IRA. These IRA funds can serve as an easy source of down-payment funds to broaden their retirement portfolio with the purchase of a rental property.

The second reason people like to invest with a self-directed IRA is that investments are protected from capital-gains taxes. This means that you can sell a property owned within your self-directed IRA without any tax consequences, and then reinvest your money in a next property or in another way. Even better, if your self-directed IRA is a Roth-type, then your investments are not subject to income tax when you withdraw them after age 59½. It is for this reason that a Roth IRA is typically far more advantageous than a non-Roth IRA.

If you are young and just starting out, it is a good idea to open up a Roth IRA or a self-directed Roth IRA and start socking money away every year. You can always convert a standard Roth IRA, managed by a mutual fund company, to a self-directed Roth IRA, later on, so don’t waste precious time by worrying about the details. Get that Roth IRA open, start making contributions, and let them grow with the market.

It is important to note that you are strictly prohibited from combining your self-directed IRA funds with your own personal funds. For example, all expenses related to a property owned by that account must be paid by that account, and all income received from that property must go directly back into that account.

In spite of the tax benefits of the self-directed Roth IRA, there are some potential downsides to consider. First, because investments in an IRA are already tax-deferred, depreciation expenses within an IRA do not offset your personal taxable income as they do with other investment property. Also, expenses must be handled by the self-directed IRA management company or a property manager, which come with a fee and can make administrative functions somewhat complicated.

Additionally, there are two types of taxes that may adversely affect some investments in a self-directed IRA: Unrelated Debt-Financed Income (UDFI) and Unrelated Business Income Tax (UBIT). UDFI is a tax that you pay for carrying a mortgage on a rental property rather than purchasing it solely with your retirement funds. The good news is that the tax is proportionate to the amount financed and can be lessened by deducting the property-related expenses. In years where there is no taxable income within the IRA, this tax does not apply.

The second type of tax, UBIT, affects those who use their self-directed IRA for active businesses, including fix-and-flip–type real estate ventures. It is essentially a tax assessed when an IRA invests in active income, instead of passive investment income such as rental real estate. This tax does not apply if, after renovating, you rent the home out for a period of time before selling.

With a property owned by your self-directed IRA, the rental income goes right back into the IRA account. It is not taxed annually, and if it is a Roth-type account, it will not be taxed upon withdrawal either (assuming withdrawal after age 59½). There is also no tax if you sell the property and reinvest the proceeds into another investment property.

I converted my Roth IRA into a self-directed Roth IRA in order to use the pool of money that I’d been growing over about fifteen years to invest in real estate. With this goal in mind, I purchased a property with “all cash” (i.e., no mortgage) for $75,000 in a neighborhood where purchase prices were typically between $120,000 and $140,000 at the time. The house was in desperate need of some renovation, bringing the total cost much higher than I’d originally planned. I hired a property management company, who rented it out for $1,300/month to start earning money back on the investment. I plan to eventually sell the property and redirect the funds from the sale into a multi-unit property, using a non-recourse loan and the UDFI tax that comes with it.

The R.O.R.E. Blueprint for Success: A Step-by-Step Companion Guide at www.GetaChicken.com has all the details on how to make this strategy work best for you. For more information on the self-directed IRA and whether it makes sense for your individual situation, consult with an accountant who has knowledge of and experience with self-directed IRA products.

Self-directed Solo Roth 401(k)

The Solo 401(k), also known as the Self-Employed 401(k) or the Individual 401(k), is a retirement plan for self-employed individuals. There are two types of Solo 401(k)s. The first type is the more common variety that is operated by a broker and involves investing in the stock market and mutual funds. The second type of Solo 401(k) is self-directed. Like the self-directed IRA, the self-directed Solo 401(k) allows you the freedom to invest in a variety of types of investments, including real estate.

The self-directed Solo 401(k) is actually more advantageous than the self-directed IRA for many reasons. For starters, the self-directed Solo 401(k) is not subject to UDFI or UBIT taxes, thus allowing more flexibility. Also, unlike the self-directed IRA, but similar to a typical 401(k), you are allowed to borrow up to $50,000 or 50 percent of your account value (whichever is smaller) from your account, without any taxes or penalties. In addition, the self-directed Solo 401(k) allows for higher annual contributions than the self-directed IRA.

Even better, in 2006 Congress created the Roth version of the self-directed Solo 401(k). This means that, like other Roth-type investment products, you can pay a small amount of tax up front, grow your account over time, and eventually withdraw your funds (after age 59½) tax-free. To repeat, you can legally buy and sell homes, rent homes, or conduct other investments, all without paying any tax on the earnings using the Roth version of the self-directed Solo 401(k).

With all these advantages in mind, you may be wondering, “Why would anyone choose a self-directed IRA over a self-directed 401(k)?” The answer is relatively simple. Where is your money? If you already have an IRA, then the self-directed Roth IRA is for you. If you are self-employed, then the self-directed Solo 401(k) is for you. If this is your case, you can simply roll over a portion of your existing 401(k) accounts (from previous employers) and/or your Solo 401(k) into your new self-directed Roth Solo 401(k) account and get started investing in real estate. As always, it is best to discuss your own particulars with an experienced accountant before you begin.

Tap Your Retirement Account After Age 59½

If you are over age 59½, then you have earned the freedom to access your retirement accounts without penalty whenever you like and for any reason. So, instead of leaving all your eggs in that one basket, you may want to use this opportunity to move some of your funds into rental property. Any time you withdraw money from your retirement account after age 59½, it is called a normal distribution, because there is no penalty. If it is a Roth product, then you may withdraw your funds in as few or as many different normal distributions as you like without paying any tax. If you don’t have a Roth product, then you will need to pay income tax on your normal distributions.

As we discussed back in chapter 1, we are required to take regular withdrawals after age 70½ in what is called the RMD (required minimum distribution). This means that you have an eleven-year window (between ages 59½ and 70½) in which you are allowed to take out as much or as little money as you would like. Some people who have high account values on a non-Roth retirement account use the strategy of taking enough distributions during this eleven-year window so that both their balance and their tax bracket are lower once they are forced to begin withdrawing it regularly after age 70½. You will definitely want to consult a tax adviser to further understand how you will be affected by various IRS rules and how to best strategize your spending during these critical years.

The other factor to consider is that if your adjusted gross income from your RMD is over a certain amount, then you won’t receive the Social Security benefits that you may be expecting. In this scenario, up to 85 percent of your Social Security income could be lost to taxes. This is something many people with higher retirement account balances may not take into account when they are planning for retirement, something that is also definitely worthy of a conversation with your CPA at least a few years before turning 70½.

For both of these reasons, this eleven-year window of time, from age 59½ to age 70½, is an excellent time to withdraw some funds to purchase rental property, without a mortgage, if possible, so that it can provide solid monthly income for you right away. An experienced property manager will lessen the work entailed and allow you to relax and enjoy your well-earned retirement.

PUT YOUR CHICKEN TO WORK

Trade Up with a 1031 Exchange

Once you are the proud owner of one or more rental properties, you are allowed to sell your investment property and buy another one, tax-free. Perhaps you want to trade your property for one that has more income potential. Maybe you have your eye on a part of town that is becoming “hot” where you feel there may be greater appreciation potential. Perhaps you have had a difficult time finding quality tenants for your existing property. Or maybe you want to sell your single-family investment property and purchase a multi-unit building to generate greater cash flow and achieve the Level II or III Goal. Whatever the reason, trading up using 1031 Exchange is an excellent strategy to sell one investment property, and buy another investment property, without paying taxes on the sale of the first.

This advanced move is called the “1031 Exchange.” The 1031 Exchange gets its name from the piece of tax code to which it refers, and this code has a number of rules. I’ll go over the most important ones here, though you should consult with an experienced accountant and title agent before embarking on the 1031 Exchange:

1. You must have owned the original rental property for at least one year plus one day.

2. The purchase price for the new property must be equal to or greater than the sales price of the original property, and all the proceeds from the sale of the original property must be directed to the purchase of the second rental property. Any of the proceeds that you don’t direct into the new property is called “boot” and is taxable.

3. Both properties must be “like-kind” investments, which include virtually any kind of real estate held for investment purposes. It excludes personal residences, fix-and-flip properties, as well as other capital gains–type investments like stocks, bonds, oil, and precious metals.

4. Vacation properties qualify as replacement properties as long as there is an investment intent and as long as they meet both of the following two conditions for at least two years following the purchase: a) You rent it out at fair market rental rates to other people (not family members) for at least fourteen days each year; and b) You limit your personal use and enjoyment of the property to less than fourteen days each year or 10 percent of the number of days that it was actually rented out to other people.

5. If you are trading out of or into a multi-family home, in which you have been or will be residing, the 1031 Exchange only applies to the portion that can be considered investment.

6. You must enlist the services of a third party, called a “qualified intermediary,” to aid in the transaction. (Often your title company or closing agent can either serve as a qualified intermediary or recommend someone.)

7. Within forty-five days after the sale of your first property, you must identify to your qualified intermediary up to three potential properties that you would like to purchase. The property you end up purchasing must be on this short list.

8. Finally, you have exactly 180 days (or one half of a year) to purchase one of the properties that is on your list.

With the 1031 Exchange, you direct the proceeds from the sale of one or more investment properties into the purchase of a higher-priced investment property. For the balance, you can either obtain a mortgage or negotiate seller financing. As long as your equity (the difference between the amount you owe and the ultimate sales price) on the property that you are selling meets the down-payment requirements of your lender, you will not need to come up with additional down-payment funds.

For example, imagine that you own a couple of properties and, after a significant period of time, you sell them both under a 1031 Exchange. The amount remaining after paying off the existing mortgages is $600,000. Whether your aim is to buy an apartment building or a vacation property (to be rented for at least two years), if the purchase price is $1,000,000, then since the amount of funds is greater than 25 percent of the purchase price, you will not need to come up with additional money for the purchase. You can apply the $600,000 toward the purchase and use a mortgage for the remaining 40 percent of the balance. Needless to say, you would only act on this advanced strategy after having an experienced real estate accountant verify that the income will cover the mortgage and all expenses.

Reinvest and Build Net Worth

In chapter 3, I explained net worth in terms of potential and kinetic net-worth energy. You put work into creating your potential, and then you manifest that potential, in the form of kinetic net-worth energy, the moment you finish paying off your mortgage. If you go for the Level II or III Goal, you will not only boost your cash flow, but you will also boost your overall net worth once the mortgages are paid off. In other words, achieving the Level I Goal of owning one rental property is an excellent measure of safety, but owning more rentals can be even more powerful because the total mass is greater.

One way to build mass is to accumulate more value, through more property. If you are younger, you will have more time in which to do this. If you have set a Level II or III Goal of owning more than one property, you may want to do what many successful people do: They reinvest their equity in one property by refinancing it, pulling cash out, and using that money to purchase an additional rental property. I did this, as did a great number of people I interviewed. See the stories, online, of Deb, John, Jake and Mary, and Catherine, to name a few.

For easy math, as an example, say you invest $20,000 into a $100,000 rental property in a middle-class neighborhood. See the Cash Flow Analysis (CFA) Tool, Form #5 at www.GetaChicken.com. In this example, the return on investment is 23 percent. Over time, if the property appreciates to $120,000, you will have made back your initial investment of $20,000 in the form of equity. At this point, you can refinance 80 percent of the new property value, by obtaining a new $96,000 mortgage on the property and pulling out the remaining 20 percent ($24,000) to reinvest in another property.

In theory, when you have periods of appreciating values, and assuming positive cash-flow analyses, you could do this exponentially, with one property becoming two, two becoming four, four becoming eight, and so on. In fact, in the words of Robert Kiyosaki, “Professional investors invest their money in an asset, get their money back without selling the asset, and move their money on to buy more assets.”5 Using this formula can have a significant impact on your net worth down the road and can catapult your achievement of the Level II or III Goal.

This chapter provided an almost dizzying array of options, from acquiring your first rental to buying your next rental(s) and leveraging what you have to ensure that your long-term financial plan—your nest egg—is shatterproof. The next chapter, “Hatching Your Plan,” breaks these down and provides guidance based on your unique set of personal circumstances. Turn the page, and craft a plan that best meets your needs and circumstances and is best for you.