Forecasting

Forecasts are the kernel of your business. They are the basis on which you raise money, negotiate premises and order raw materials. These are only a few of the decisions that need to be made in advance with only your forecasts as guidance on how much is needed. Making a wildly inaccurate forecast can, for example, lead to raising insufficient funds. When the business fails to meet expectations and begins to run short of money, it may prove impossible to raise further funds. Lenders are very wary of handing out more when forecasting has proved to be mistaken. The result could be liquidation, or bankruptcy if you are a partner or sole trader, and the end of your dreams.

However, making no forecasts at all is even sillier. You would have no guidance on when to take certain basic business decisions.

Given the importance of attaining a reasonable estimate of future sales, costs and cash balances, it follows that making the forecasts is a process that should not be hurried or treated casually. This process is usually carried out using a spreadsheet or utility forecasting program, though the quality of the forecast depends on the figures that you have inputted.

You must constantly strive to seek information on which forecasts can be based; you must constantly curb your over-optimism, which can lead to estimated sales figures that are too high and estimated cost figures that are too low. Question your first forecasts for the realism of their assumptions before accepting any figure as a part of the final forecasts.

Nevertheless, it is realistic to accept that some of the figures will be nothing more than a best guess given the current state of information available to you. However, your figures should have some grounding in fact, so when you present your case to your bank manager or other source of finance you can support the figure when challenged.

What is in this chapter?

There are three forecasts you need to make:

The chapter assumes that you are using a computerised spreadsheet or other program to prepare your forecast.

Cash flow forecast

The first point to note is that cash and profit are not the same thing at all, so the two forecasts may be quite different.

A cash flow forecast is a record of when you think you will receive cash in your business and have to pay it out. In your business plan, you should include monthly cash flow forecasting for at least one, preferably two years ahead. Depending on the size of your business, you may need to include yearly cash flow forecasts for a further three years.

Included in this chapter is a blank cash flow form (p. 288), which shows the typical headings and layout of a forecast. Obviously, the headings will vary with the nature of the business.

Detailed calculations for cash flow forecast

Do the cash flow forecast for your chosen accounting year. If, for example, you choose to end your accounting year at the end of April, your cash flow forecast will run from 1 May to 30 April.

It is important to make realistic assumptions about when you will receive the cash, or when you will have to pay it out. The purpose of the forecast is to throw up when your need for cash is at its greatest, so you can demonstrate what your funding requirements are.

1. Opening bank balance

This shows how much is actually in your business bank account at the start of each period. If you owe your bank money (have an overdraft), show this as a negative figure. If your forecast is made before you start trading, the opening bank balance is likely to be nil.

Your opening bank balance for one period will be the closing bank balance for the previous period.

2. Cash from sales

In here would go any cash you expect to receive when you sell your product, not in payment of an invoice you send out. If your business is a shop, most of your sales will be cash ones, so this would be the biggest element of your cash receipts. If you are registered for VAT, enter the figure you expect to receive, including VAT.

3. Cash from debtors

If you sell your product and do not receive payment at once, but instead send out invoices, you would enter here when you expect to receive the cash. Someone who owes you money (for example, has not yet paid your invoice) is a debtor. You should aim to get your invoices paid as quickly as possible, but most of your customers will expect to delay payment by at least one month (see Chapter 24, ‘Staying afloat’, for how to get your debtors to pay).

If you are registered for VAT, enter the figure you expect to receive, including VAT.

4. VAT (net receipts)

If you are not registered for VAT, ignore this section. Chapter 29, ‘VAT’, includes details of whether you should or should not be registered (p. 400). If you are registered for VAT, you will only expect to receive cash from the VAT system if for some reason your purchases, on which you can claim back VAT, are greater than your sales on which you have charged VAT.

This might happen as a rare occurrence if you have spent a lot of money while starting up, before your sales have got going. Another possible reason could occur if your sales are seasonal but your purchases are not. It could also happen if your sales are zero-rated, in which case you do not have to charge VAT on your sales, but you can claim it back on purchases (p. 404).

Monthly cash flow forecast

(for the period 1 January 2020 to 31 December 2020)

You may make your returns for VAT on a quarterly basis, so allow for this in your cash flow.

5. Other receipts

Put here any miscellaneous receipts of income that you expect to occur.

6. Sale of assets

This section is for you to record the proceeds you expect to get from selling any assets, for example a car or office equipment or intellectual property, such as a brand.

7. Capital

Put the amount of money you are going to invest in the business and make sure you put it in the month you expect to invest it. If anyone else is expected to invest in shares of the business, or in a partnership, or to lend you money (not including an overdraft with the bank), slot it in here.

8. Payment to suppliers

Put in here when you expect you will have to pay suppliers for their services or materials. The longer you delay paying suppliers’ invoices, the better it can be for your cash flow. This beneficial effect has to be balanced by any ill will created by late payment. A realistic assumption for your cash flow forecast will be that you will not have to pay your suppliers’ invoices until one month after you receive them. Whether you are registered for VAT or not, enter the amount including any VAT you will be paying to your suppliers.

9. Cash purchases

If you have to pay cash on the spot for purchases from suppliers, estimate the amount (including any VAT) and time in this section.

10. Wages/drawings

Put here the net amount after deducting tax and National Insurance contributions under the PAYE system for wages.

11. PAYE/NIC

Total the amount of tax under the PAYE system and the amount of National Insurance contributions you will deduct from your employees each month, as well as the amount of the employer’s contribution. You have to send this money in to the tax collector so that it is received by the 22nd of the following month. (But if your average PAYE and NIC payments are likely to be £1,500 a month or less, you can make quarterly payments, which will help your cash flow – contact HMRC’s payment enquiry helpline.)

If your business is a limited company and you pay yourself a salary as a director, your personal tax and National Insurance contributions will be collected in this way and entered at this point.

If you are a sole trader or partner, your personal tax on what you pay yourself will not be collected in this way. Instead, you will pay tax, and Class 4 National Insurance contributions if you pay them, in two instalments, in January and July, with any remaining balance the following January (p. 371). Enter the amount in the section ‘Tax payments’. However, your Class 2 National Insurance contributions will be collected each month, and you should reflect the amount here under ‘PAYE/NIC’. For more about your personal tax and National Insurance contributions as a sole trader or partner, see Chapter 28, ‘Tax’.

12. VAT (net payments)

If you are not registered for VAT, do not enter anything here. If you are registered for VAT, you should estimate the amount of tax you will be paying over to the VAT collector each quarter or other period (see Chapter 29, ‘VAT’).

13. Tax payments

If you run a limited company, enter the amount of tax you estimate you will pay on your company’s profits and when you will pay it. Corporation tax – that is, tax on your company’s profits – is payable nine months and one day after the end of your accounting year: ask your accountant* for more information.

If you are a sole trader or partner, your tax and any Class 4 National Insurance contributions payable will be paid in three instalments – on 31 January and 31 July, with the balance or a repayment on the following 31 January. For how to work out the amount of tax you will be paying, see Chapter 28, ‘Tax’.

14. Rent

Enter the rent you will pay in each month or quarter.

15. Uniform business rate

Enter the amount of the business rate and when you will have to pay it (p. 205). Do not forget you can opt to pay your rates monthly over a ten-month period. This can improve your cash flow.

16. Heating/lighting

These bills will be paid each quarter in arrears or monthly by direct debit. Remember to cater for heavy winter usage.

17. Telephone, web hosting and IT support

The telephone bill will be paid quarterly or monthly in arrears. Paying web hosting fees and IT support bills will be as you have agreed with these suppliers.

18. Professional fees

Payment of these bills will be fairly erratic; you must make your best guess, but try to obtain an estimate.

19. General expenses

Enter an estimate for those continuing and recurring, but small, expenses. These could include postage, fares, or whatever is required in your business. What exactly goes in here will have to be decided by you.

20. Capital expenditure

If you are going to buy any pieces of equipment, such as a car, computer, machinery, or web site development, enter the amount, including VAT, and when you estimate you will have to pay for it. If you are paying cash, put in the full amount. If you are going to buy on hire purchase or using a loan, you will enter the amount of the deposit and the monthly payments separately and in the correct months. Leasing payments will be monthly. Fees for web site development will be paid as agreed with your developer.

21. Bank interest and charges

If you have an overdraft or bank loan, estimate the amount and frequency of the interest charged. Get a quote from the bank manager.

22. Other payments

What goes in here depends on the nature of your business. It could include insurance, but if this is of reasonable size you should have a separate entry.

23. Closing bank balance

Work out the closing bank balance for the period by adding the opening bank balance to the total receipts and taking away the figure for total payments. The closing bank balance becomes the opening bank balance at the start of the next period.

Profit and loss forecast

A profit forecast should show what level of profit you expect your business to produce at the end of the period, according to the accounting records you keep. Your accounts will not be drawn up on a cash basis, so many of the figures in your profit forecast will be different from those in the cash flow forecast. Below there is an explanation of how and why the figures will differ.

Detailed calculations for profit and loss forecast

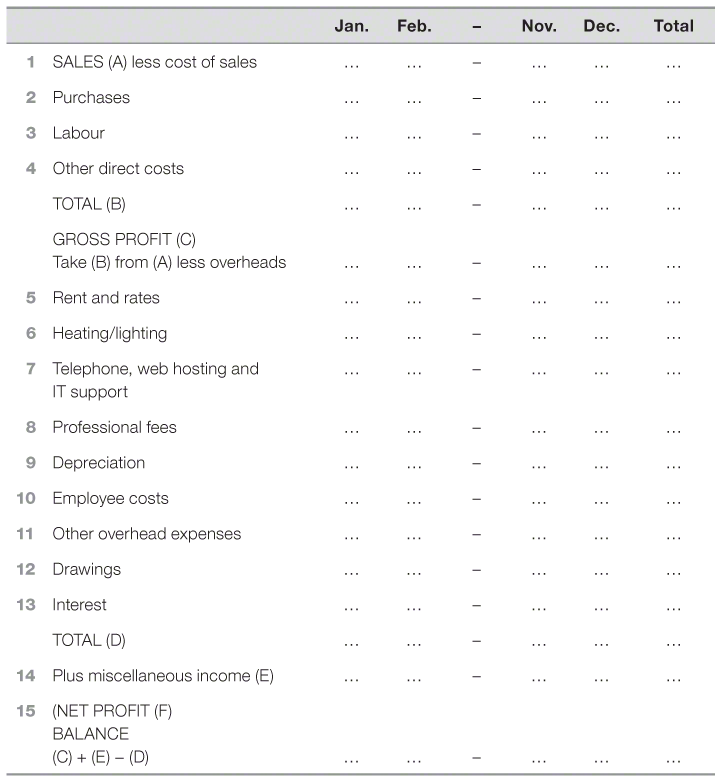

1. Sales

The figure you put in here is the sum of the invoices you expect to send out during the accounting period. It is not necessarily the sum of the cash you receive during the period (unless your business is a shop that makes only cash sales, for example). You could also describe the sales figure as the cash you receive during the period plus what you are owed at the end of the period less what you were owed at the end of the previous period.

If you are registered for VAT, you do not include the amount of VAT you charge on your sales, unlike in your cash flow forecast.

If your business is likely to be seasonal, or if you know of events coming up that might temporarily increase or decrease your sales figures, show this monthly effect. A reader of your business plan will not be impressed by a monthly figure that is level or shows a very steady rate of increase unless you can demonstrate that this is a realistic assumption.

When forecasting sales, you need to consider two factors: the number of units you can sell and the price you can get for these units.

2. Cost of sales: purchases

You are estimating for this section those costs that you would expect to vary with the level of your sales; if your sales go up, the level of direct costs goes up, and vice versa. In real life, things are not quite so cut and dried and often the distinction between direct costs and overheads is blurred. The important point is for you to have a clear idea about which you regard as overheads.

Purchases could be the raw materials you buy from your suppliers to manufacture your products. Or, if you are not a manufacturing business, they would be the items that you purchase to sell on to your customers, having added on your profit margin.

Monthly profit and loss forecast

(for the period 1 January 2020 to 31 December 2020)

The figure you put in your profit and loss account will be different from the cash flow figures for payments to suppliers and cash purchases. For the profit calculation, you need the sum of the invoices you receive in the period for materials.

Another way of working out the purchase figure for this forecast is to say it is what you pay for supplies in the period plus what you owe at the end of the period less what you owed at the start of the period.

If you are registered for VAT, you do not include the figure for VAT that you are charged by your supplier for your profit forecast. If you are not registered for VAT, you do include the figure for VAT.

Points to look out for when you are forecasting costs include:

- making sure that the level of costs corresponds to the amount of sales you expect to make;

- allowing for any changes in the prices of raw materials that you can reasonably expect to occur in the period.

3. Cost of sales: labour

Here include the cost of your employees who are directly involved with manufacturing your product. As with purchases, the distinction between staff who are directly involved with production and those who count as overheads can be blurred. On the whole, if you do not think that employees’ wages are directly related to the amount of work you have, it may be more satisfactory to include employee costs in overheads.

Remember to include all your employee costs; this implies gross salary, your NI contributions as an employer plus any other costs.

The figures may diverge slightly from those in the cash flow forecast, as PAYE and NI contributions are due the following month. Differences will show up only when you first take on an employee or their salary rises.

4. Cost of sales: other direct costs

Estimate here any other direct costs that you foresee.

5. Overheads: rent and rates

In the profit forecast, the total for rates should be spread evenly over the whole year. With rent, you should enter the cost for each period, which may not coincide with the timing of the payments.

6. Overheads: heating/lighting

You need an estimate for the cost of heating and lighting that you will use in each period. Usually you’re billed quarterly. This is the case even if you have chosen to pay monthly by direct debit, in which case the quarterly bill is set against the sum of your monthly payments.

7. Overheads: telephone

The treatment of the telephone is similar to that for heating and lighting. Costs of web hosting and IT support should be spread evenly over the year.

8. Overheads: professional fees

The figure to include here is what it costs you in legal and accounting fees. You should include the cost in the period in which the work is done for you, even if you do not receive the bill until the next period.

9. Overheads: depreciation

Depreciation is what you deduct from the value of an asset to reflect the fact that it is wearing out. This is an item that does not appear in the cash flow forecast. You work it out by taking the value of capital equipment at the start of each period and estimating a figure for its depreciation during the period. Typically, cars and office equipment are written off over three, four or five years. Web site development costs might be written off over two years.

Note that you do not put in the profit forecast what you pay for capital equipment, which does appear in the cash flow forecast.

10. Overheads: employee costs

This should be your estimate of employee costs that are not directly related to the volume of your sales (p. 232).

11. Overheads: other overhead expenses

Include overhead expenses not slotted in elsewhere.

12. Overheads: drawings

What you pay yourself.

14. Miscellaneous income

Put here an estimate of the other income you might receive, not as a result of the sales of your products. For example, if you have money invested, it might include interest.

15. Working out the net profit figure

You can work out a gross profit figure (C) by deducting the figure for direct costs (B) from the sales figure (A). In Chapter 24, ‘Staying afloat’, you will see how you can use the gross profit figure to work out the break-even point for your business (p. 324).

Once you have arrived at an estimate for gross profit, deduct the figure for overheads (D) and add on the amount of any miscellaneous income (E) to give your forecast net profit level (F).

Balance sheet forecast

A balance sheet for your business will show what you owe and what you are owed on one particular day. A forecast one will show your estimate of that picture at the end of the period.

There is more about accounting records needed to produce the right information for a balance sheet once you are in business in Chapter 27, ‘Keeping the record straight’. Your accountant should produce a balance sheet for you. If your business is likely to be fairly small-scale and you are only approaching your bank manager, and for a fairly modest sum, a forecast balance sheet may not be necessary.

In this section there are brief guidelines on how to work out what the balance sheet might be at the end of the period, once the forecast cash flow and profit and loss account are drawn up. And at the end of this chapter there is a blank balance sheet forecast for you to complete (p. 300).

Detailed calculation for balance sheet forecast

One important check on your balance sheet figures is to note that the figure for total assets should equal the figure for capital and liabilities together.

1. Fixed assets

These figures are fairly straightforward to work out. You know from your cash flow forecast when you plan to buy particular bits of equipment. Include all equipment that you have received before the end of the period, even if you have not paid for it. A fixed asset is something of a permanent nature, likely to remain in use in your business for some time.

The value you put in here is not just what you paid for the equipment; you also have to allow for the fact that it will have depreciated since the period started. You can obtain the figure for depreciation from your profit forecast. Deduct these figures from the appropriate cost of each piece of equipment, or written-down value at the start of the period, and enter the figures here.

Example

Richard Petworth is working out the depreciation for the office furniture he has bought for his business. There are a number of different ways of calculating this, but for office furniture he thinks he will write off the value in equal lumps over five years; this is called straight-line depreciation.

The furniture cost Richard £2,000. This means he writes off £400 from the value of it each accounting year. The written-down value at the end of the first accounting year is £1,600.

2. Current assets

The main current assets you are likely to have in your business are:

- cash;

- debtors (that is, what your customers owe you);

- stock (that is, products you have in store, either raw materials to make your product, half-finished products or unsold finished products).

Take the figure for cash straight from your cash flow forecast.

You can derive the figure for debtors from the cash flow and profit forecasts. You will have made some assumptions about number of units sold in each month and how quickly you will be paid your cash. From this you can calculate how much you would be owed for sales by your customers at the end of each period. Remember to include VAT if you are registered.

The figure for stock can also be derived from the other two forecasts. Count as stock all goods received from your suppliers to be used in your product but not yet used in products sold, even if you have not yet paid your suppliers’ bills. These should be shown at their ‘cost’ to you.

3. Capital

Put here the capital you used to start your business. The figure for profit and loss you take from your profit forecast. It is the cumulative figure at the end of the period. If you forecast a loss, put it in as a negative figure and it will be deducted from your capital.

4. Liabilities

Loans from the bank or another lender that are not due to be repaid within one year are medium- or long-term liabilities. Current liabilities are mainly:

- overdraft;

- tax payable, including VAT;

- creditors (that is, what you owe your suppliers at the end of the period).

The figure for overdraft can be taken from your cash flow forecast.

If you have made a profit in the period, you will need to estimate what tax will be payable. You may also have to include a figure for what you owe HMRC in VAT (if you are owed VAT, you should have an entry in the current assets section for this).

In the same way as you worked out debtors, so creditors can be estimated using the two other forecasts. It is the value of the amount of goods you have that you have not yet paid for.

Balance sheet forecast

(on 31 December 2020)

| Assets | ||||

| 1 | Fixed assets | |||

| Freehold property | £…… | |||

| Leasehold property | £…… | |||

| Office equipment | £…… | |||

| Vehicles | £…… | |||

| Plant/machinery | £…… | |||

| Other equipment | £…… | |||

| Total fixed assets (A) | £…… | |||

| 2 | Current assets | |||

| Cash in hand and at bank | £…… | |||

| Stock | £…… | |||

| Debtors | £…… | |||

| Total current assets (B) | £…… | |||

| Total assets (A) + (B) | £…… | |||

| Capital and liabilities | ||||

| 3 | Capital | |||

| Shareholders’/proprietor’s capital | £…… | |||

| Profit and loss | £…… | |||

| Total capital (C) | £…… | |||

| 4 | Medium-term liabilities | |||

| Loans | £…… | |||

| 5 | Current liabilities | |||

| Overdraft | £…… | |||

| Tax payable | £…… | |||

| Creditors | £…… | |||

| Total liabilities (D) | £…… | |||

| Total capital and liabilities (C) + (D) | £…… | |||

Summary

- Forecasts are very important if you make commitments on the basis that the figures are reasonably accurate.

- Make the forecasts conservative.

- A cash flow forecast is not the same as a profit and loss forecast.

- If you find it difficult to produce the forecasts, ask for help, for example from the Business Support Helpline* (or equivalent organisation), your book-keeper or an accountant.

- The treatment of VAT and depreciations needs special attention.

- Once you have the forecasts, use them to assess how viable your business will be and whether you will be able to make a living from it.