There is in the act of preparing the moment we start caring.

We have come to the place where our money meets our life and heart, where we organize our financial expenses and income sources and attempt to bring them into alignment with our hierarchy of needs. By going through this brief financial planning exercise, we can synchronously settle the emotional and financial ledgers.

In this chapter, I have provided simple worksheets for organizing your finances in a way that puts first things first, clarifies what you can and can't pay for at this time, and offers peace of mind for the needs you can meet.

Many people have told me of going through life with a haunting, eerie feeling about their financial lives. They are afraid of those aching questions that never quite make it to the surface of a conversation: Am I walking a financial tightrope with my debt and spending? If my income took a hit, would my lifestyle fall like a house of cards? Is it okay to spend some money to have fun once in a while?

Am I really living within my means? Am I going to be financially stressed and miserable in my later years?

Like a lost hiker in the mountains who discovers a GPS instrument, just discovering where you are brings a degree of comfort—especially compared to the grinding fear in your belly that you are miles from safety. The exercises in this chapter will act like a financial global positioning instrument. You will gain clarity on where you stand with regard to funding your personal survival, safety, freedom, loved ones, and self-actualization. No more wandering and wondering.

Even if this exercise reveals that you still have a ways to go, there is newfound hope in finding clear direction to your destination. It helps you locate yourself.

How much money do you need each month to survive? Many of us have a general idea of how much it takes each month to make ends meet; however, making ends meet can include many items outside the purview of survival, such as dining out, club memberships, extra vehicles, and expensive toys.

I was surprised to discover, while conducting Income for Life dialogues, that the majority of people (over 80 percent) had never bothered to calculate their "survival" expenses. Top financial planners across the country have affirmed that because of disorganization, lack of initiative, or just plain denial, most people wouldn't think of calculating survival costs unless they were suddenly put in a position where survival was an issue (e.g., loss of a job with no good prospects on the horizon).

Some people act like they aren't sure they would want to know. Like someone with a nagging pain resisting a doctor's appointment, it may just be too depressing to find out. But after calculating survival costs, most people feel illuminated and comforted for knowing. Those who calculate and do not like where they are begin to see the relationship between their chosen survival lifestyle and the stress they are experiencing in their lives. Many of these people become more resolute to take steps to bring peace of mind to their financial life.

Getting by isn't cheap these days. Of course, it all depends on where and how you live. We all remember the days where we got by on next to nothing. The funny thing is, when I converse with people about those days, many say that, although they had less, they felt more content. Even though many were "just surviving" at some point in their life, they felt they had enough.

I called my son at college the other day to see what his survival budget was. He's 21 years old and living in a beautiful cabin on a lake in the boundary waters, a scene many middle-aged men dream of and will pay dearly for in their retirement years. My son informed me that it took a total of $450 a month to maintain this lifestyle. I asked for the details of his monthly survival ledger. They were:

Rent: $250

Groceries: $40 (Yes, you read that right—that is per month. "How can that be?" I asked. He informed me, "I buy potatoes, onions, flour, and staples, and catch and hunt the rest. We make up big pots of deer stew and ice-fish with a sense of purpose.")

Gas: $50

Utilities: $50

Bait, beer, and babes (his description): $60

Oh, for the ingenuity, resourcefulness, and contentment of youth. I remember stringing together such an existence myself—surviving off tips from waiting tables over lunch. It was refreshing for me to hear his budget. It highlighted how inflated with luxury is our modern definition of survival. We could get by with much less if we really had to, and even with a breakeven survival cost many thousands beyond my son's, it brings my soul comfort to know that my family and I could survive with much less and still have one another. We will continue to enjoy the existence we have as long as we can, but there is solace in knowing we could be content in a place where we may never have to go.

Like me at his age, my son dreams of someday having a new(er) truck, a house to call his own, a spouse, and children after that. His survival costs will escalate, as will the need to earn more. Hopefully, he will heed my lessons on debt management, living below his means, and paying his bills on time. Hopefully, he will never talk himself or be talked into a survival budget that strips away the joy of living, the joy of working, and the joy of building for the future.

There is comfort to be found in financial clarity. Take time to fill out the Survival Money Worksheet in Figure 18.1.

Discover your financial location in monthly and yearly terms. If you are married, discuss your survival situation (if you believe you both can survive the conversation, that is) and talk about how your current survival budget could be adjusted, should you ever face the prospect of having to do so.

Once you have added up your survival expenses, place the total in the total box at the bottom of the worksheet.

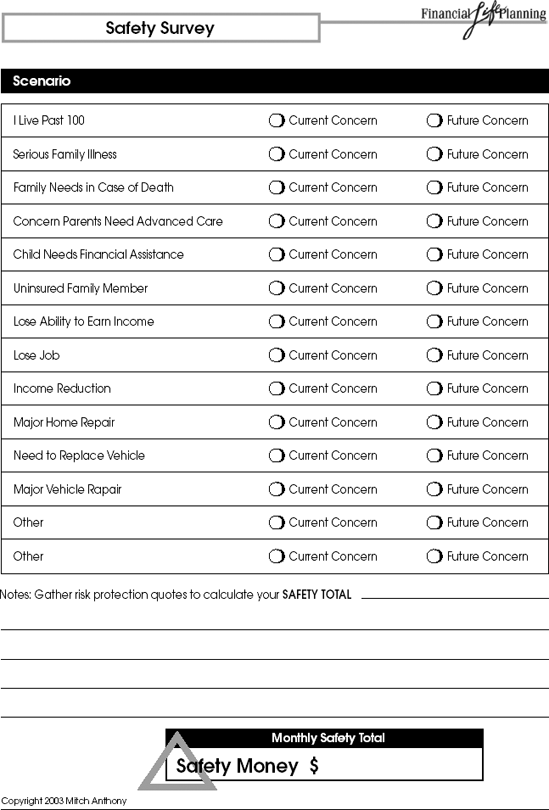

Once you ensure that you can meet your survival needs and those of your loved ones, it is time to think about protecting that survival: "Me build hut, me build fence around hut to keep out thief and tiger." Inflation is a thief over time. If you are 50 and live to 100 and inflation continues at the same rate it has for the last 50 years, it will have taken 86 percent of your spending power in the next 50 years. As Figure 18.2 illustrates, predators such as disability or long-term care for a loved one—exposures in our risk protection—are waiting to pounce on us at vulnerable moments in life.

I get paid to give speeches and have been for the past 20 years. What if tomorrow I lost my ability to speak publicly? How would I replace that income for my family? That is a safety issue.

Fred's mother is showing signs of decline at 75 years of age. Her home and life savings would be consumed if she were placed in an assisted living facility. This is a safety issue for Fred's entire family.

Bob has longevity in his genes. His father is 92 and going strong. His mother is 90. His grandparents all lived into their late 90s. Bob's finances, invested as they currently are with his current rate of withdrawal, will disappear when he is 83. This is a safety issue for Bob and his children.

Jerry has worked hard and saved a lot of money in his professional career. He's two years from eligibility for his pension. His daughter, a recent graduate from college, can't find employment and has no health coverage. If a catastrophic illness or accident should happen, Jerry could be wiped out, erasing the 35 most fruitful earning years of his life. This is a safety issue for Jerry and his wife heading into the next phase of their life.

Many of the safety issues can be addressed through insurance products such as long-term care, health insurance, health insurance supplements, disability coverage, life insurance, and homeowners coverage. Many people also choose to use insured investments that guarantee their principal and a rate of return that outpaces historical inflation rates to address their long-term income needs such as the possibility of living to 100.

Insurance companies are in the business of helping people manage their risks. Exactly how much risk you can tolerate is up to you. Each individual has a distinct and individual tolerance for risk in his or her life. For the sake of awareness, it's important for every one of us to have a conversation about the exposures and vulnerabilities in our life and in the lives of our family members. At the end of that conversation, we can each decide where we desire protection and, ultimately, how much protection we can afford.

Another factor that impacts your need for safety is whether you feel your best earning years are ahead of you or behind you. If you feel they are behind you or you currently are at your peak, safety will assume a more prominent position in your mind.

The fact that people continue to build homes on fault lines proves that everyone is unique in his or her response to risk. Some people are comfortable with the risk of living to 100 and trusting that income will be there, and others are not. Some people are comfortable dealing with aging and long-term-care issues when they arise, while others would rather prepare ahead and remove future exposure. As with all risks in life, we must first acknowledge that the risk is there, then decide how to respond to that risk.

A friend of mine who spent 30 years in the insurance industry put it this way: "No one buys insurance wanting to use it. It's a lot like a plunger—nobody ever buys one hoping they get to use it, but should they ever need one and don't have it, they'll find themselves knee deep in it and wishing they had one then." Risk protection is not something you get excited about having, but according to Maslow it is a basic emotional need in our lives. There is some peace of mind in knowing that, if life or Mother Nature brings adversity, we will be safe.

Go through your Safety Survey worksheet in Figure 18.2 and note where your vulnerabilities exist. Are there cracks in your financial foundation? What coverages do you have in your work benefits? You may need to sit down with an insurance provider to calculate long-term-care, disability, or other coverages. Take the time to calculate the monthly cost of building a fence of emotional safety around your survival.

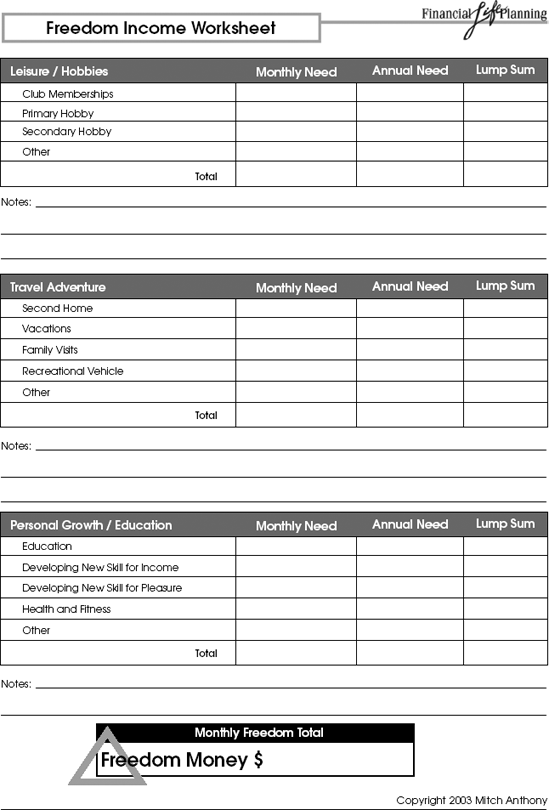

What are the things you do that make life worth living? What are the activities and places that bring joy to your life? What is the reward you look to after long hours, weeks, and months at your job? (See Figure 18.3.)

These hobbies, pursuits, and adventures are the engagements that motivate us and energize us to keep our hand to the plow. Without such weekly, monthly, or yearly rewards, life becomes drudgery and Jack becomes a dull boy.

A friend recently told me about a neighbor, a dairy farmer, who at the age of 48 was diagnosed with cancer of the colon. This man had not taken a single day off, including holidays, in 35 years. My friend commented that his neighbor was, as expected, quite miserable, but in all the years he had known him he had always been quite miserable.

How happy could any of us be without taking a cathartic break in more than 10,000 days? The human species was not made this way. "And, on the seventh day, God rested from all his labors."

I know many people in the cattle business, and they tell me that cows don't take days off—and neither can the people who care for them. Some have been fortunate enough to find people who could fill in for short periods, so they could experience the occasional rest and relaxation. What great dividends short periods in diversion of leisure can pay.

My wife Deb and I share a similar philosophy in life—work hard and play hard. My wife's play happens to include horses (I play golf and basketball), and so her freedom bill is a lot higher than mine—but it does motivate me to keep working hard! We both work out of our home and try to work efficiently to leave time for play. The opportunity for fun is a constant motivation in our working life. We treasure our leisure pursuits enough that we will pay the price of labor to ensure that the opportunity for fun is always there.

Our fun bill can run rather high. A friend once warned me to never get a hobby that eats. I didn't understand his point until I married a horse lover. Horses set off a financial domino effect that simply starts with the purchase of the horse: food and board, training, vet bills, farrier bills (new shoes every seven weeks), horse accessories, truck and trailer to pull said horsey, and did I mention horse insurance? Can you tell I like to whine about the horse bills? I often threaten my wife that I am going to start a new national support group called "Equini-non" for men who love women who love horses. Did I also mention that my wife has now thoroughly indoctrinated our daughter in this deception as well? (Multiply the above freedom expense by a factor of two.)

Not that my fun doesn't cost something as well: a golf membership at a good golf club, the early spring golf outing with the boys, and Titleist Pro V1 balls that I have no business buying given their short life expectancy in my golf bag.

Then there is the family trip each year to an exotic spot like Mexico or the Caribbean. We decided some time ago after watching how fast the kids were growing up that we needed to make a conscious effort at creating some magical travel memories together.

It all adds up, but in our life it adds up to fun—and balance. We have a sense of balance in our personal and family life that keeps us all looking forward and staying out of ruts along the way. It was well worth the exercise for us to sit down and figure out how much these freedoms are costing us and how we will continue to pay for them.

For some, freedom money is about more than leisure. It is about the freedom to pursue personal growth and expanding their capabilities. These pursuits also come with a price tag, whether it be pursuing a degree, taking language lessons, or embarking on a self-improvement course. These freedom initiatives can also bring great joy into our lives, as we sense ourselves expanding and growing. The cost of these pursuits needs to be calculated into our freedom income ledger as well. Tally up your freedom costs on the Freedom Income Worksheet, and calculate the monthly income needed in the total box at the bottom.

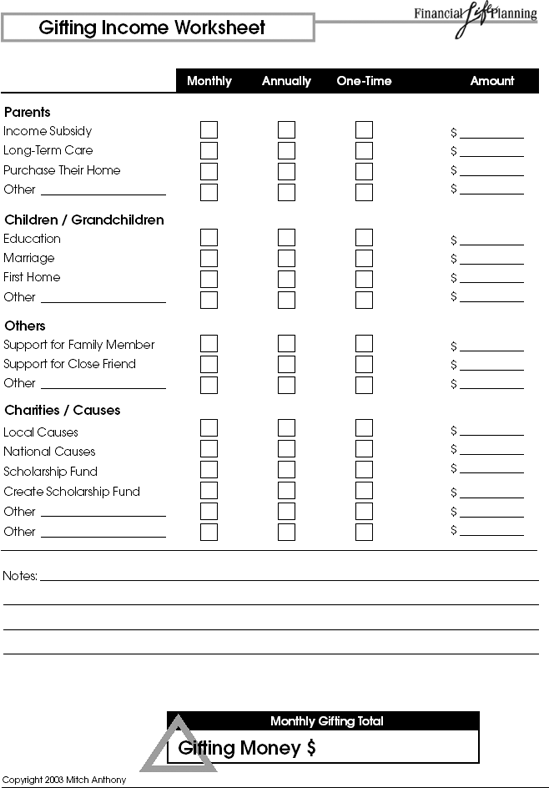

Once we pass survival, safety, and freedom in our financial hierarchy of needs, we come to the place of giving to others. (See Figure 18.4.)

This is not to say that we can't do any giving along the way while we pay our bills related to survival safety and freedom. Many people form the "charitable habit" and systematically give 10 percent of their income in tithes to their church, 5 percent to charities, or periodically support causes that come around asking for help.

I believe that the ultimate intention of wealth is to eventually give back all that was gathered—and to do this in ways that will improve lives and meet real needs in our world. Naked we came, and naked we will leave. I'm reminded of the old joke of the wealthy man who left an equal third of his wealth to his banker, doctor, and lawyer with the agreement that they would place it in his casket before his burial. The banker and doctor grudgingly dropped in their share and watched with horror as the lawyer dropped in a check for his share. He knew the old boy would have no use for it now. And neither will we one day. Take the case of the McDonald's restaurant fortune left by Ray and Joan Kroc. At the end, all those billions of burgers sold ended up being billions of dollars in the hands of the Salvation Army and other charitable organizations funding their noble efforts at helping the less fortunate. This is a picture of wealth as it should be.

Many people who have found wealth in modern times have taken instruction from the lessons of spoiled and shiftless trust-fund babies produced by inheritances and have decided to place no such curse on their own children. Because of the expenses of longer life expectancies for our parents and protracted tenures in retirement for us, it is inevitable that the expenses of our predecessors will take precedence over the expenses of our progeny. After all, our children have more earning years ahead of them. You might also consider the example you set for your children by stepping up and helping your parents, if need be. This is an example they may someday need to repeat.

In America, when I talk to audiences about gifting to their parents, creating parental pensions, and the general attitude of

dismissal and neglect that suffuses our culture's approach to aging, I'm met with either knowing nods or shamed avoidance.

A financial planner from Asia recently told me that when he sits down to talk with clients in their 40s and 50s, one of their first concerns is creating "pocket money" for their parents. This is the first concern, because Asians place a premium on experience and age over youth. Our culture worships beauty and youth—albeit ephemeral beauty and ignorant youth. In Korea, the birthdays most worthy of celebration are the 1st and the 70th. Here, we are supposedly over the hill at 50. Whose hill? Does this mean we expect to go into decline after 50? Many people are still ascending at age 80.

The Gifting Income Worksheet in Figure 18.4 takes into consideration parents, children, extended family and friends, and causes near and dear to your heart. Some issues you will need to sort through, prioritize, and calculate around are:

Subsidizing a parent's survival or freedom costs.

Contributing toward children's education.

Contributing toward children's "getting started" costs (i.e., wedding, first home, etc.).

Creating income streams for your favorite causes.

Creating a scholarship fund for youth facing hardships and/ or pursuing careers you are familiar with.

Giving one-time gifts to a project or cause.

My friend, Roy Diliberto, CFP, an exceptional financial planner in Philadelphia, loves to tell the story of a woman in her 70s who came to see him with over $2 million and a cost of living that was minimal. Roy asked her if she was charitably inclined. She replied that she was not. Rather than just letting it go, Roy challenged her to take a closer look at her neighborhood and community and look for areas where her gifts might make a difference right away. In their next meeting, she told Roy she had found three causes she wanted to start supporting immediately. She had a new energy and excitement in her voice as she described the work of the three causes she had located. Now, many years later, Roy reports that all this client can ever talk about are the causes she supports. She has added a few more to the original three, and has added a new layer of meaning to her own existence.

Roy believes that we make a big mistake when we relegate talk of charitable giving to estate-planning conversations. By doing so, the giver misses out on the joy of giving. The New Retirementality take on gifting is to be giving while you're living. Be a firsthand, rather than posthumous, witness to your charity.

Tally up the gifts and income streams you'd like to create. How much will it cost each month or each year? Place your gifting total at the bottom of your gifting worksheet.

Do something you love and you'll never have to work a day in your life.

—George Burns

The last income category to evaluate is the expenses associated with our dreams, or to borrow from Maslow, the cost of self-actualization. Self-actualization takes a different form for every individual. Here are some of the dreams I've heard from individuals:

Starting and running my own business.

Taking a year to travel the world.

Working for Habitat for Humanity.

Writing a book.

Going back to school to be trained as an artist, teacher, musician, etc.

Trying different forms of volunteer work.

Owning a boat and sailing around the world.

Restoring old cars.

Woodworking.

Giving time and talents to a ministry.

Building a dream home.

Taking children and grandchildren on a long European vacation.

The list is as endless as the number of people who dream. The worksheet in Figure 18.5 is about being, having, and doing. We dream to be someone. It is that wistful seed that lives unsprouted within us. There will most likely be costs associated with planting that seed.

We dream of having and doing things. Maybe we want to have and do just for a while or maybe permanently, depending on whether we decide we like the having and being enough. But there are obvious costs to having (like owning the boat or RV) and less obvious costs to doing (like owning the time needed to do what we will with it).

Owning one's own time is at the core of the need for self-actualization. How can we be and do what we dream of being and doing if our time is owned by another? Or consumed with simply paying bills? There are many in our culture whose dreams are drowning in inflated survival costs. They have some decisions to make.

There are many others who would be doing better economically if they pursued their heart's passion, but just don't realize it. (I've always been bothered by the assumption that if you follow your heart, you'll make less money.) If, on the other hand, you know what you really want to do will pay less, then a negotiation with your lifestyle will be necessary to get you to the position where you can begin collecting a "play check." Remember, a "playcheck" is when you have so much fun doing what you're doing that you can't believe someone is paying you to do it.

Tally up your totals for each need on Maslow's hierarchy and you are now ready for working out the income side of your life ledger—how to pay for the life you need and want. (See Figure 18.6.) At some point, we all will need to engage in the process of figuring out how to make our income provide the lifestyle we want and last a lifetime. It is time to tie our assets to our liabilities. Financially speaking, all the totals you have factored into your Income for Life plan are financial liabilities. Peace of mind and contentment enter the picture when we designate exactly what assets will pay for which liabilities.