More people should tell their dollars where to go instead of asking where they went.

A nickel ain't worth a dime anymore.

In 1975, Joe retired early at the age of 55 so that he could go fishing. He started receiving a pension check for $ 352.75 per month. Seven years later he started receiving Social Security. Today at the age of 85, Joe, who is in relatively good health, is still receiving his pension check of $ 352.75 each month and continues to go fishing almost every day. What I want to know is this: Is Joe going fishing these days because he wants to or because he has to?

According to a MetLife Employee Benefits Trend study, 61 percent of employees rank "outliving their savings" as their greatest retirement fear. Twenty-seven percent of those surveyed felt they were "significantly" behind in their savings, and 1 in 10 hadn't even started! Only half of the boomers surveyed had factored longevity into their retirement plans. Across all of the age groups in the study, employees were concerned about having enough money to live securely in retirement. Key concerns included:

Outliving retirement money (56 percent).

Having to work full-time or part-time to live comfortably in retirement years (51 percent).

Providing for your spouse/partner's long-term care needs (49 percent).

Providing for your own long-term care needs (47 percent).

Having enough money to take care of elderly parents or in-laws (44 percent).

Why not plan on living to 100 and develop a plan that guarantees that the only check that bounces is the one written to the undertaker?

The next step in your Income for Life planning process is to look at your sources of income, your life, and your money management, and then match what you have (or will have) against what you will need going forward. And, unless you want to be like Joe in the example above, who retired to what seemed to be a nice little pension in 1975, you need to be realistic about what the costs of living (surviving) might be 30 years down the road.

How have the expenses of daily living changed in a generation? The U.S. Bureau of Labor Statistics recently published a study of expenses in retirement that compared the expenses of a retiree in 1949 to a retiree in 2003. The following table shows some contrasts I have organized from the study:

1949 | Retirement Expenses | 2003 |

|---|---|---|

33% | Food, tobacco, and alcohol | 15% |

15% | Household operation | 16% |

14% | Clothing and accessories | 5% |

11% | Transportation | 17% |

10% | Housing | 18% |

6% | Recreation | 8% |

5% | Medical care | 13% |

The most notable changes in retirement living expenses in the past 50 years are the expenses for food, tobacco, and alcohol and medical care. What is going on here? In 1949, more was spent on eating, smoking, and drinking than on medical care, and in 1999, half as much was spent on these three and almost 200 percent more on medical care. Is there something we are not being told about the benefits of eating, smoking, and drinking? Or are today's retirees being taken for a ride by drug companies and health insurers—or are they simply living longer? Perhaps it's a combination of the two.

Former Congressman Gil Gutknecht of Minnesota claims it is the latter. His findings inspired him to sponsor the Pharmaceutical Market Access Act of 2003. While at a metropolitan pharmacy at the Munich, Germany, airport, he discovered that the prices for popular drugs are up to 600 percent more in the United States! Two examples are: Glucophage, which cost $29 85 in the United States and $5 in Germany, and tamoxifen, which cost $360 in the United States and $60 in Germany. No wonder so many U.S. seniors go to Mexico or Canada to purchase their drugs. Who can blame them?

This is the true joy of life: the being used up for a purpose, recognized by yourself as a mighty one: being a force of nature instead of a feverish, selfish, little clot of ailments and grievances, complaining that the world will not devote itself to making you happy.

— George Bernard Shaw

Going forward, it will be more beneficial to choose a posture of proactive health rather than get caught up in the health care system. We can make the preparations we feel are necessary (such as long-term-care insurance), but the greatest impact to our health will be rendered by the New Retirementality decisions we make, such as:

Work out your heart on a regular basis by walking, jogging, or some other aerobic exercise. One study showed that walking three times a week for two miles adds five years to your life expectancy; decreases depression, diabetes, and cancer rates; and helps you sleep better.

Engage in regular, light weightlifting. Lifting holistically produces not just physical strength and resilience but attitudinal and internal strength as well.

Maintain physical intimacy. The head actuarial at a leading insurance company told me of a conversation he had with a 75-year-old woman who was rated for a 20-year life insurance policy by his company. Having never seen this happen before, he called the woman to ask for the secret to her great health. Her reply, "Frequent and frantic sex."

Schedule charitable and altruistic activity into every week. Those who feel a sense of purpose live longer and better.

Don't join the "moan and groan" sorority or fraternity. Pessimism leads to an expedited health decline.

Engage in work or activities that utilize your talents and challenge your brain. "Continuing to work keeps the mind sharp and the body healthy, which aids in maintaining a positive attitude," says Dr. Russell Clark, a 103-year-old real estate developer.

Drink a little coffee to start your engine and a little red wine to wind it down. You've seen the studies. Cheers!

If you have spent any amount of time in a nursing home, you know you don't want to go there—or at least you want to do your best to delay a stopover. I like to visit occasionally because I draw personal motivation and insights from talking to residents, and because I steel my own resolve toward healthy living.

By the way, the estimated cost of an annual nursing home stay in 2034 is expected to be $ 190,000, according to the Journal of Financial Planning (July 2003). And you don't get a lot of room for your money. If you have to end up in a nursing home, it's better to reside in Jackson, Mississippi, than in New York—the New York last-stop costs three times more than in Jackson.

Stay focused on healthy living and follow some of the great examples of active and vibrant 80-and 90-year-olds. Your health habits will have a major impact on both your quality of life and the quantity of income available for that life. Think of health habits as an investment—in yourself.

As baby boomers move closer to their 59 ½ birthday party, they are becoming increasingly aware of financial issues tied to enjoyable retirement years. But there may be a "disconnect" with money focus and money habits, as patterns with self-directed retirement and investment accounts seem to indicate. First, let's take a look at the change in financial focus, and then we'll explore the self-sabotaging patterns.

Attitudes toward retirement saving have changed dramatically, according to a study by AXA Financial. The study contrasted the focus and attitudes from 1993 with those of 2003 and discovered the following:

1993 | 2003 | |

|---|---|---|

Use IRAs | 17% | 40% |

Concerned about adequate resources in retirement | 26% | 43% |

Live within means/lower debt | 81% | 90% |

Although the focus of the baby boomer crowd seems to be changing, prudent money behavior is not keeping in step with the new focus. Two examples are 401(k) cash-outs and individual returns over the last decade compared to fund and index returns. According to a study conducted by Hewitt (a global outsourcing and consulting firm) of 200,000 workers who changed jobs, far too many people are cashing out of their retirement funds while in transition.

Forty-five percent of transitioning workers cashed out their 401(k) accounts when they changed jobs. Whatever the reasoning was for cashing out would likely not hold up as a sound financial rationale. Making a purchase with tax-advantaged funds and paying a 10 percent penalty on top of the new taxes is not a good move. If the reasoning was that the amount in the account was inconsequential, then this can hardly be perceived as good news either. This study is especially troubling because 39 percent of the people who cashed out were 60 years old and older!

Why would we need less tax-deferred savings as the result of losing or changing jobs? If we needed the money to simply survive, that would be understandable, but to take the money now and rob ourselves of future earnings proves that many of us may simply need to be protected from ourselves. Lack of restraint in the present can cause long-term financial problems.

A case in point is the story of why the State of Nebraska jettisoned its 401(k) plan (see Steven Neff King, "Riding Herd," Investment Advisor, August 2003). While the average pension in Nebraska returned an average 11 percent over 30 years, the average return for individuals was 6 to 7 percent. The Street.com reported, "Nebraska's decision offers proof that the average investor lacks the knowledge, and perhaps just as important, the interest necessary to invest for retirement on his own."

It seems that the problems in Nebraska were not confined to that area of the country but are universally hinged to human nature. A recent Dalbar study exposes the shocking results of the do-it-yourself and self-directed retirement approach. Here are the annual averaged returns for equities, pensions, and individual investors from 1984 through 2004:

Equities—12.9 percent

Pensions—13.1 percent

Individual investors—3.5 percent

Yes, you read it right: 3.5 percent! Over a 17-year period, how much retirement lifestyle impact is there between 3 percent and 13 percent? It's the difference between building a penthouse and an outhouse.

The self-directed, do-it-yourself approaches were motivated with good intentions, but time has shown that most of us have neither the expertise (or the time to gain the expertise) nor the needed attention span to successfully manage such a proposition. Another revelatory fact of the Dalbar study was that "market timers" in stock mutual funds (those trying to predict highs and lows) lost an average of 3.3 percent! My advice? Hire a competent, caring, and honest professional. Pay him or her the fee (whether it's a percentage or flat) and get on with your life. If you don't know how to find a financial professional who fits that description, read Chapter 21, "Finding the Right Wealth-Building Partner."

When we look at the difference between returns on equity (12.9percent) and doing it yourself (3.5 percent), most of us could have hired a negligent manager who charged 5 percent and did nothing but throw funds into stock indexes—and we would have done better. We would have suffered much less damage than what we did to ourselves with ill-timed moves and very bad Warren Buffett imitations.

The point is to have as much money as possible available for you to do with what you want. We can be our own worst enemy when it comes to reaching this point. Know your ability, availability, and attention span, and do what is best for you in the long run and get help where you need it.

If you had ever told me that I would be working in retirement, I would have told you that you were crazy. After being a pilot for many years, I figured I would spend my days golfing and taking it easy. Now, I'm 72 and I'm driving a limo three days a week ... and loving it!

— Fred, Ft. Lauderdale, Florida

As a result of shrinkage in 401(k) and 403(b) accounts, many people are planning to work longer than they had originally anticipated. If you have the New Retirementality, this can be a good thing, because it means you are going to be doing work you feel good about, at a pace you can easily keep. Also, if you have the New Retirementality, you know that the elements of challenge, networking, and usefulness tied to your work are going to ameliorate your aging prospects.

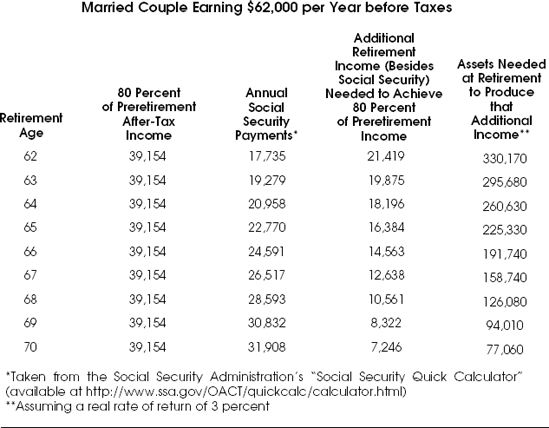

A recent study by the Congressional Budget Office, titled "Baby Boomers' Prospects in Retirement" (November 2003), illustrated how much impact one to five extra years of work can have on the economics of retirement. Consider a couple, Bobby and Brenda Boomer, both in their 60s, with a household income of $62,000 per year. After taxes, this couple typically takes home approximately $49,000. If we assume an 80 percent retirement income replacement rate (a rate promoted by many financial professionals), then this couple will need $39,000 per year to live on.

If both were to retire at 62, they would receive almost $18,000 in Social Security benefits, which leaves a balance of $21,000 needed per year for the next 21 years, assuming the age expectancy for people retiring at their age and a 3 percent real (inflation-adjusted) rate of return on their assets. To produce the additional $21,000 would require an accumulation of just over $330,000 by this couple at the time of retirement.

However, if Bobby and Brenda waited three years to retire, they would receive almost $23,000 in Social Security benefits and would need to finance the balance of $16,000, which would require $225,000 at the time of retirement. By working three years longer, not only would they have more tucked away, but they also would actually need less. This sounds like a much more comfortable position to be in—a position with some breathing room.

At this point, if Bobby and Brenda decided to work part-time after their retirement for reasons of purpose, passion, activity, and sanity, they would have even more financial latitude. They may be in a position to finance all the activities and expenses listed in their hierarchy of "financial" needs.

According to the chart in Figure 19.1 (borrowed from the Congressional Budget Office study), if Bobby and Brenda were really enjoying their work and wanted to continue until they were 70, they would be even better off, with a bigger nest egg to fund their future. Working until 70 would reduce the needed nest egg to $77,000 from the $330,000 needed at age 62. Their Social Security benefits alone at age 70 would be $32,000.

Each additional year of work provides the following financial benefits:

Increases your Social Security benefit.

Reduces the amount of wealth needed at retirement.

Increases your time to earn returns on your savings.

According to the Congressional Budget Office study, if Bobby and Brenda Boomer had arrived at age 62 with only $26,476 but continued to work to age 70 and saved 10 percent of their income per year during the additional working years, they could still retire at 80 percent of their working income.

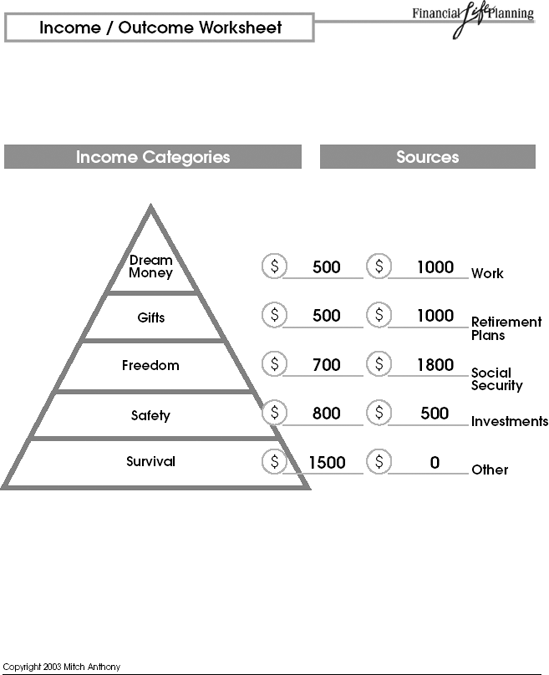

Following is a case study I have borrowed from a certified financial planner who uses the Maslow dialogue to help her clients calculate their income needs. Mark, age 58, wants to work full-time until he is at least 62, and then hopefully consult on a part-time basis after that. Bonnie, age 59, enjoys her part-time work as a real estate broker, has a nice network of customers established, and would like to continue as long as is possible.

Their survival expense is $2,700, which is easily met by Mark's take-home pay as a business manager ($4,600 a month). The additional $1,900 income can be used to pay Safety expenses, which come out to $1,800 monthly and include long-term-care insurance for Bonnie's mother and a policy they are paying for themselves.

Bonnie's part-time work as a real estate broker brings home an average of $1,500 monthly. Bonnie's income is applied to the Freedom expenses, which include a golf/tennis membership, time-share fees, and two annual vacations. The Freedom expense is $900 a month. They are using the $600 balance from Bonnie's income to eliminate debt, which will be cleared in two years' time.

Bonnie is eligible to begin taking distributions on her IRA in a few months, and their planner has calculated they can begin taking $600 a month out of a balance of $140,000 and still have a comfortable margin of safety. They plan to use this $600 per month for their gift needs ($500 monthly) and for miscellaneous expenses and entertainment. Their dream is to build a summer home on the Oregon coast (approximately $l,500/month), which they believe they will use earnings from approximately $175,000 in investments for about a year. At that time, they will begin using distribution from Mark's IRA (approximately $340,000) to make the monthly payment.

In seven years when Mark takes his retirement, they plan on selling their current home and transferring the equity to pay off most of the balance on their coastal home. They also plan on using the proceeds from their investments and Mark's IRA along with Mark's Social Security to make up the income needed as he transitions into a part-time consulting career.

Mark and Bonnie's accountant has suggested a number of income-providing investment tools, including real estate investment trusts, instant annuities, and corporate bonds, that they can utilize when they come to the point of needing to guarantee income from their accumulated assets. Their insurance agent has worked with them to make sure that their safety expenses regarding long-term care will be paid up before they make their big transition to the coastal home.

If you work with a financial professional, it would be important to consult with him or her on these important calculations to ensure that your retirement plans and investments are invested in such a way as to provide maximum income with the greatest degree of safety possible. (See the sample in Figure 19.2.)

You don't want to run out of money because of an unrealistic, assumed rate of return on investments or because of a lack of hedging and protection against the next bear market.

Everyone's Income for Life plan will be unique, because we all have needs particular to our situation and income sources that vary and fluctuate as we pass through various transitions.

Beware of singular-focus solutions promoted by people with self-interest at heart. Systematic withdrawals from mutual funds or equity accounts, bonds, and annuities can be good strategies when properly utilized, but rarely work as a total solution. Systematic withdrawals can turn into "dollar loss averaging" that causes you to run out of money, as we have seen it do more than once in recent years.

Bonds can put you in a bind when interest rates go against you. And the wrong annuity will not only lock you in to a rate of return but also can lock you up as far as access to your money goes. Remember, a guarantee of 5 percent looks awfully nice when the market is losing money, but it doesn't look so great when everyone else is getting 12 percent out of the market. It's great to get locked in, but it's not so great to be locked up.

A competent, caring, and trustworthy professional worth his or her weight in gold discovers the intricacies of your situation and researches the products most appropriate for your situation. Additionally, you want someone who keeps a regular pulse on the events and transitions in your life to make necessary adjustments along the way. Rarely is a financial plan implemented that does not require tweaking. Some life transitions may call for a complete overhaul. In these moments of stress, duress, and even grief, the last thing you want to be mucking through is who you can trust with your money decisions.

If you are going to handle all these matters on your own, it is paramount to develop not only an income plan for the present but also contingency plans in the case of extended illness, accident, loss of earning ability, and death.

The idea is not just to live long; it is to live well. To do that, you'll need to make sure your money lives as long as you do.