Chapter 11

The Revolution in Big Data and SME Lending in the Emerging World

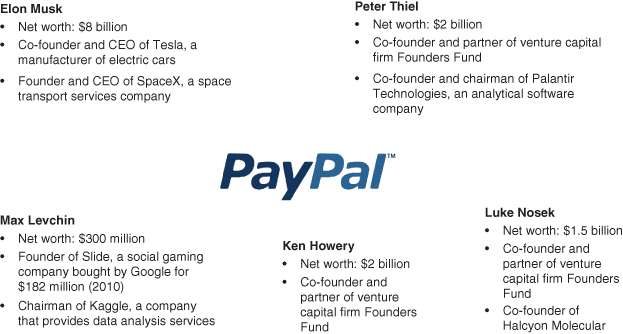

After they created PayPal, owners Peter Thiel and Elon Musk realized that they had created a vast technological infrastructure that had a host of potential applications in addition to the tasks required to create a secure payment system. So they decided to spin out some of this technology and make new applications. Thiel and others have gone on to create many new companies engaged in payment systems, data collection, big data analytics, complex systems for trading various assets, quasi-bank lending systems, cybersecurity, credit card activity, and crowdfunding for projects (figure 11.1).

Figure 11.1 Billionaires Are Creating Their Own Financial Ecosystem

Source: Schulte Research websites

The fortunes made from earlier companies like PayPal, Square, and others have created a new center of economic gravity. They have created a new hope that a small guy can get rich with a good idea involving ways to gather and allocate money. They have created a new environment for funders with a lot of money who have seen fortunes made from crowdfunding and peer-to-peer funding because banks are in no shape to lend. Ideas are meeting people at a time when great talent either is leaving banks in disillusionment or is being pushed overboard to cut costs. (I believe we will see much greater consolidation in banks in 2015 and 2016, so let's assume many more entrepreneurs will be flooding the streets with good ideas.) Money is meeting optimism and talent in institutions that obey the law at a time when interest rates are zero and people are competing against banks that have been torpedoed by angry regulators, prosecutors, and shareholders. Simply put, a smart man or woman sitting in an investment bank in a career track that is going nowhere has great incentive to go out and make it on his or her own in ways that were undreamt of before. Of course, not all will make it big. But some will. There will be blowups and flakey scammers. But I strongly believe this trend toward what we can call “big data citizen funding” is irreversible.

We have a perfect storm of energy, momentum, and money swirling around creative centers in London, San Francisco, and other cities, while banks are bogged down by compliance, shrinking margins, prosecutions, massive fines, poor morale, and high costs. The buzz in the world of technology has created a need for speed and bandwidth. It seems that the only thing holding back greater innovation in the phone or the computer is technology. So, firms who know there is profit in speed have brought about astounding advances in speed and bandwidth as witnessed by Table 11.1. Think about how much we can do on the phone that was impossible only three years ago. From 2014 to 2018, companies like Cisco estimate that the traffic flow through the cell phone system will increase by 6×—not 60 percent! This means it will be six times more than what it was in 2013. As an example, it will be conceivable to run an entire home entertainment system on a phone by 2017.

Table 11.1 Astounding Speed of Technological Advance

| Parameter | 2000 | 2014 | 2018 Forecast | 2000–2018 Improvement (× times) | 2014–2018 Improvement (× times) |

| Global Fixed Internet IP Traffic Petabytes/month | 75 | 42,000 | 86,500 | 1,100 | 2 |

| Global Mobile Data Traffic Petabytes/month | <1 | 2,500 | 15,000 | 16,000 | 6 |

| Processor—No. of Transistors (months) | 21 | 5,000 | 80,000 | 4,000 | 16 |

Source: Cisco

The highway is being built at speeds undreamed of just a few years ago, offering a vast scope of possibility for new types of companies and new types of data management to emerge that can allow local commercial banks to widely distribute financial products and collect money safely and securely. It will allow marketing companies to create entirely new campaigns through social networks. It allows retail to create personalized products and bypass the physical store. It allows manufacturing to lower costs, create rapid ubiquity anytime and anywhere in the world, and have perfect fidelity in the ever-cheaper products it sells globally. Education companies can create digital education tools that can reach hundreds of millions of people with no schools. Financial services can foster innovations that connect anyone in society to any financial transaction anytime and anywhere. And these firms can do this with superior returns.

The need for speed is now wedded to an entrepreneurial class with lots of equity funding to create solutions to unmet needs at far lower prices with far lower costs. This is, in essence, the dilemma of the bank. These companies are reducing complexity by consolidating many functions into one go-to conduit. They are increasing productivity by eliminating mail and turning the bank branch into a museum piece—similar to the phone booth of old. These companies are increasing the speed and manipulation of data with instant reporting, something most banks have not yet figured out. They are creating clever programs to alert users of financial services about bogus fees being charged by the bank. They are reducing transaction costs and creating greater profitability per transaction, something the high-cost banks cannot fight. These new technology companies are saving time, reducing paper trails, and eliminating both real and bogus fees, which the banks have considered the privilege of an elite few. In essence, financial technology has now found a back door to the fortress that was “the bank” and is exploiting it in every area. Meanwhile, the banks are unaware of the intrusion and are acting as if all is well when the status quo is changing by the day.

Let's break this all down and look at the various divisions to see how these banks will be affected by the above phenomenon. Global universal banks like Deutsche Bank, Citi, J.P. Morgan, Barclays, BNP, Société Générale, Credit Suisse, and Morgan Stanley have eight divisions:

- Investment advisory/wealth management

- Derivatives

- Credit cards

- Commercial lending

- Stock and bond trading

- Alternative investments

- Investment banking

- Payments and clearing

These will remain mainstays of these banks. No one is saying differently. The point here is that every one of these businesses is under threat from financial technology firms around the world. This chapter is about the banks' vulnerabilities and the way in which new technologies have already eaten into bank profitability. As far as I can see, these trends are likely to take on new momentum and accelerate. The opinion of Andy Haldane, the executive director of financial stability at the Bank of England, put a fine point on what I am about to describe: “Banking may be on the cusp of an industrial revolution the upshot of which could be the most radical reconfiguration of banking in centuries.”1

In the area of wealth management, there are many new technologies coming down the pike that are ingenious. Companies like Wealthfront are entering the fray and offering ways of replicating indices. This software can be automated and offers solutions for tax savings and portfolio management. Furthermore, companies like AlphaClone have ingenious software that can get all available public information on up-to-date portfolios for funds that are known as either good stock pickers or good dividend players or smart fixed income players. In this way, anyone can “clone” portfolios of some of the best investors globally in no time. These and many other tools are now available that put powerful tools into the hands of amateur investors. (For lecture purposes, see From High Finance to iFinance: Do Not Fear the Digital Revolution.)

Brad Hintz is a famous bank analyst who writes on this topic. He recently left the highly respected broker/dealer Sanford Bernstein Research and offered some parting thoughts: “Banks, under pressure, have pulled back on commodities and FI trading, leaving a gap in the market to be filled by new actors, such as hedge funds and other lightly regulated entities. Regulation has boosted revenues at clearing houses, which are mainly owned by exchanges.”2 This is the understatement of the century. Many lightly regulated entities are moving into all of these areas at a very fast pace.

What Happens When Sales and Research Can't Be Paid for Access or IPO Research?

Another nail in the coffin on the world of equity trading comes from regulators. A combination of new regulations and new technologies may render these divisions redundant. Regulators are deciding in unison that fund managers who use the equity services may no longer pay for “corporate access.” This includes the setting up of meetings during grueling trips to several countries. What if an analyst and the sales team can no longer be paid by investment banking? What if an analyst and the sales team can no longer be paid for their relationships with corporations? If funds are banned from paying for these activities, then the raison d'être for the research/sales/trading platform for equities ceases to exist. Most long-only funds and hedge funds now trade through electronic platforms, anyway.

After the Regulators, New Technology Is Leading to End Times for High-Touch Banking

Regulators and technology are taking away the equity trading platforms of investment banks. They are taking away the commodity trading platforms. And slowly but surely, they are taking away the fixed income platforms, as fixed income trading also becomes mechanized. Take away the advisory function, because corporate access and much of the front-facing business of trading stocks, bonds, and commodities evaporates. This is problematic for labor, in that many business schools, for instance, still prepare people for roles such as research and sales, and these roles are disappearing in favor of entrepreneurial roles connected to information technology. Some of these business schools, as they say, did not “get the memo.” A few examples among a multitude of that which can more cheaply and more efficiently replicate the functions of advisor, salesman, and analyst are Estimize, eToro, EquaMetrics, and SecondMarket. Table 11.2 shows how these companies threaten the sales/trading/research function.

Table 11.2 Excellent Tools for Research in Equities and Fixed Income

| Company Name | Largest Investor | What They Do | Who Can They Threaten? | Comment |

| Estimize | Contour Venture Longworth Venture |

Algorithm to reduce bias, get better data sets. | Equity research division of banks | Raised US$1.5 million Claims more accurate than Wall Street 69.5% of time |

| eToro | Spark Capital | Dynamic algorithm trading platform. Allows users to replicate the financial trading activity of others. |

Legacy/existing stock, commodity, and FX markets | Threatens exchanges |

| EquaMetrics | N/A | Powerful algorithm for trading (Rizm). | Replace intelligence of: Fund managers Asset managers Investment advisors |

Raised US$5 million |

| SecondMarket | Social+Capital Partnership | Connects private/public investors with unique investments. Allows companies and funds to raise capital. |

Existing stock markets | Raised US$35 million so far and is also backed by Li-Ka Shing and Temasek |

| Trefis | Semyon Dukach, Stephen Marcus |

Can replicate all valuation methods. Allows users to break down company earnings and derive stock prices. |

Equity research division of banks Valuation experts |

Could be standard tool for all PMS |

As we saw in the previous chapter, many large corporations are also taking their mergers and acquisitions (M&As), legal, and advisory businesses in-house. I showed multiple examples of how firms like Facebook and Microsoft are creating their own mini-investment banks inside their companies and abandoning the use of investment banks for M&A as well as advisory roles. This also presents problems for the investment banking side of the business. Is this development due to mistrust? Is it due to the poor reputation banks have for inappropriate conduct in multiple areas? Or does it have to do with the rapid nature of the change in nascent industries? If so, does this mean that people on the ground who are owners of businesses and are intimately familiar with obtuse technologies in Silicon Valley tend to have better judgment than bankers in New York or even in San Francisco? It is probably a combination of all of these.

I have pointed out that there are significant problems with the advisory, broker/dealer, and investment side of the business. I predict that some of these divisions, especially equity sales/trading/research, will be downsized, sold, or closed soon. (Standard Chartered Bank closed its entire equity sales and research group in Asia in January 2015.) This trend will likely start in New York and spread to London, Hong Kong, and Singapore. Other hubs like Frankfurt, Geneva, Zurich, Tokyo, and Shanghai will likely follow. Indeed, China may entirely leapfrog the multiyear and painful decline of the high-touch broker and create purely electronic trading platforms without large and expensive sales or research teams. My experience of working inside a Chinese bank is that senior management looks at research and asks, “What's the point?”

There is not only a revolution in new financial technology upstarts who are creating grassroots solutions to research, funding, and banking. Many people in the heavyweight firms that dominate commodities, foreign exchange, banking, and fixed income are leaving to create exchange platforms that are more efficient, have better technology, and are much cheaper than existing players. This means that commissions for trading in commodities, foreign exchange, equities, bonds, and derivatives are falling fast. This puts a further squeeze on banks and causes further cuts in spending. Banks are forced to go further down the experience chain to hire cheaper people who are going up against ever larger and more sophisticated hedge funds, for instance. Over time, many hedge funds despair about the quality of people in many broker-dealers and stop dealing with them. They no longer feel like they are losing out to access to information when they switch off activity with a certain Wall Street bank and elect to move onto a cheap exchange to transact trades. Cost-cutting begets lower quality, which begets customer resentment, which begets less business. It is a downward spiral from which it is difficult to recover.

Crowdfunding Is Threatening Traditional Lending

Now, let's take a look at the more traditional banking side of the business and the new technologies that are coming along and putting a dent into the traditional banking activity. Crowdfunding originally was a response to the effects of the global financial crisis. Banks were saddled with losses, fines, prosecutions, reduced capital, and general fear of the market, and loans dried up. So, ingenious people came along who tried to create new forms of credit. Crowdfunding is just one of these responses.

Crowdfunding has morphed into several variations on a theme. One of these is a system whereby consumers pre-purchase the initiator's services or products; this variant is widely used by artists, musicians, and film producers. (Watch what Alibaba does with Lionsgate Films on this. The companies have agreed on prefunded films, which Alibaba will stream inside China. This is a new form of film funding that is truly exciting and could alter the economics of filmmaking.)

Another is widespread equity funding of companies by individuals. This is true capitalism, as it is a diversified group of people using nothing but cash to fund a good idea. There is no bank debt. There is no banker. It is a crowd of people who are willing to fund a good idea. (This is at the heart of Kickstarter and is true diversification.) Let's remember that stock markets are now just a big exchange-traded fund (ETF) where money that goes into equities is spread equally over all stocks in the Dow 30 or the S&P 500. There is no differentiation, so ETFs are a kind of socialism. Stocks receive a larger capitalization by a distribution of wealth by a remote and arbitrary decision-making machine. Big-cap stocks get larger, and small-cap stocks get smaller.

Table 11.3 shows a few of the leading contenders that have had a big influence in the world of crowdfunding.

Table 11.3 A New Breed Finding New Credit Methods and Reducing Nonperforming Loans

| Company Name | Largest Investor | What They Do | Who Can They Threaten? | Comment |

| Bilbus | Seedcamp | Financing, e-invoicing, and cash flow forecasting. Strengthening working capital. | White collar: accounting professionals, commercial bankers | Will annihilate the back office |

| FeeFighters | Hyde Park Angels (acquired by Group in April 2013) | Helps compare payment providers to find the cheapest merchant account provider, or credit card processor. | Square and other existing payment disruptors Beating banks but now these disruptor firms are cannibalizing each other |

Deflationary |

| Funding Circle | Union Square Ventures | Peer-to-peer platform connecting investors with established businesses who want to borrow in the U.K. | Bank margins and the physical need for a banker | Deflationary |

| iwoca | Talis Capital | Flexible funding structure for ecommerce sellers relying on credit score transaction data and business's selling accounts. | Bankers and physical banks | Deflationary |

| Kabbage | Thomvest Ventures David Bonderman |

Online provider for working capital to small business. Lends money by gathering data sources from eBay, Amazon, UPS, PayPal to determine loan amount. | Bankers and physical banks. | Smart; celebrity funding list |

| Fund2.Me | N/A | Allows entrepreneurs to list their ideas, and connect with investors for funding purposes. | Bankers and physical banks | May attract small business from China to seek funding in HK through online investor |

From 2011 to 2013, the amount of funds raised by crowdfunding had grown from US$1.5 billion to US$5.2 billion, and the number of crowdfunding platforms had more than tripled. North America and Europe currently dominate, but Asia is, I believe, catching on quickly. These crowdfunded projects tend to be short in duration. They are launched quickly and usually completed in about 10 weeks. Some commercial bankers may want to say that this is only a drop in the bucket, or that this is an untested fad that is bound to blow up. This view may be naïve. A multibillion-dollar ecosystem is building up around these companies and dozens more that comprise a new form of funding, which also includes marketing, advertising, and buzz for new products. This is nothing short of the creation of a better, smarter, faster financial ecosystem that includes marketing, advertising, technology, entrepreneurship, and far lower costs compared to many banks that are lost in the universal banking model of the 1990s.

This new ecosystem being created involves funding, entertainment, marketing, advertising and social networking. It integrates crowdfunding with Facebook and other crowd venues (such as Kickstarter and the ones named above) to create a way to fund new ideas for products that are tied into the advertising for the product, ideal demographics for the product, and a self-feeding buzz that can catapult a well-funded product using nothing but word of mouth and the ever-present Like button.

A fascinating documentary on this is a PBS Frontline show called “Generation Like.” These established companies and upstarts, which are helping to create demand for new products, are morphing into a new ecosystem that involves value-added advertising, marketing, and social buzz. Unlike the banks, none of these companies are facing multiple criminal charges. They are using social media like Facebook to create sales for new ideas that would never be funded by bank credit. Furthermore, some brands are created literally overnight and receive funding overnight because millions of people on Facebook click Like. In turn, these new companies create a generation of devoted customers who can bypass traditional financial services because they are technologically savvy and can use alternative means to spend, invest, and save their money. It is a new ecosystem, which the banks think is a passing phase, if not an irritating and flaky nuisance. They are flat-out wrong.

The Jewel in the Crown for Financial Technology: SME Lending

Another area that I think is the jewel in the crown of all these new industries is the small- and medium-sized enterprise (SME) market. It is a cliché to say that most businesses are small businesses, but it's true. Of 27 million businesses in the United States, 21 million have less than five people. This means that almost 80 percent of the firms in the United States are small businesses. Now, add to this the statistic that banks reject 80 percent of small business applications. And let's add in the fact that loans to small businesses during the global financial crisis have fallen by 30 percent. We have a starved market where potentially millions of customers have no access to credit to start businesses.3

Companies that have come forth to fill this enormous gap include Kickstarter, Kiva, Indiegogo, and Lending Club. Table 11.4 shows their businesses, profiles, deal structures, and other data. Many people now call these people “citizen lenders.” Lending Club is a variation on this theme, as it collects a pool of capital and is more like a private equity firm in that it offers an internal rate of return to those who fund the entity. Kickstarter, Indiegogo, and Kiva do not have any sort of interest rate charged on funds. It is pure equity in return for a prearranged product, reward, or service.

Table 11.4 Crowdfunding Is True Diversification and Citizen Funding

| Kickstarter | GoFundMe | Indiegogo | Fundable | |

| Year Founded | 2009 | 2010 | 2008 | 2012 |

| Total Fund Pledged (US$) | 1 billion+ | 390 million | 200 million | 180 million |

| Industry Focus | Creative projects | Personal use or charity | Personal use, charity, or start-up business | Small business or start-up |

| Type of Crowdfunding | Reward-based | Donation-based | Reward-based | Reward-based Equity-based |

| Fee Charge | 5% of raised fund if funding goal achieved | 5% of raised fund | 4–9% of raised fund depends on the scheme you choose | A flat monthly fee of US$179 |

| Successful Funding Cases | Pebble, a customizable watch for iPhone and Android, raised $10 million in funding. | A victim of the Boston Marathon bombing raised over $800,000 to pay for medical costs. | Ubuntu Edge, a smartphone and desktop computer in one device, raised $12mn in funding. | Plum raised $760,000 to develop software to control household lights from smartphones. |

Should banks be worried? Many of the bankers in the United States and United Kingdom with whom I have discussed this issue have a somewhat cavalier attitude. I wonder if this cavalier attitude is merited. Francisco Gonzales is chairman of BBVA in Spain. His take on all of this is simple. He inferred that banks that are not prepared for such new competitors face certain death. I have gone further in my own research to international portfolio managers and have said that investors should only buy banks that have IT specialists under 40 years of age on their boards of directors. Without a cadre of “young lions,” banks lack the aggression, curiosity, and innovation to move ahead. I fear, however, that such initiatives may be watered down or eliminated due to hypervigilant compliance that is suspicious of any new activity. The “police state” atmosphere may prevent many global banks from being able to respond to this siren call from the likes of BBVA.

Banks that do not have a history of criminal activity—and are therefore not all hung up with district attorneys and attorneys general—do have leeway to act. They have the good faith of the regulator and are, therefore, offered more rope. Banks like Commonwealth Bank of Australia (CBA) do not have an adversarial role with their own regulators. Therefore, they can hire people like Rob Jesudason as a CEO of Asia and implement revolutionary technology systems without a stupefying maze of do's and don't's. The old saying for banks goes as follows: “The lower the behavior, the higher the regulation.” So far, Australian banks have not been ensnared into the web of illegality that currently dominates the scene in the West.

The companies in Table 11.4 have made terrific inroads into the world of crowdfunding. The amounts are low—only a few billion. But these companies are a few years old. Furthermore, there are many more behind these four companies. Another that is growing quickly is Funding Circle, which now has a lending portfolio of almost US$500 million. It was only founded 16 quarters ago, and its current nonperforming loan rate is 2.2 percent, on a par with the U.K. banks that have been offering loans for decades. Why is this happening? Dan Hyde in This Is Money said that in a survey, almost 80 percent of borrowers preferred to go through peer-to-peer (p2p) funding over banks if they are seeking a loan.* This information is important and banks should pay attention to this powerful global trend that is, I believe, only just starting and that is irreversible.

There is another important reason why this is happening. An important theme of this book is the way in which banks have earned the enmity of the common man, while other companies have come along over the past decade and earned respect. The effect of branding is extremely important. Financial technology companies have not only preserved their brand value but have also dramatically improved their branding, while the branding of the banks has fallen sharply. For example, one survey from Accenture asked: “What company would you pick if it were a bank?” Fifty percent of people polled would prefer companies like Square. PayPal and Apple were also preferred. One out of four people would prefer a branchless digital bank. More than 70 percent of people polled saw a bank as nothing but a transactional institution and had no personal ties to it. For now, anyway, the regulatory, legal, branding, and reputational winds are very definitely blowing toward financial technology and away from traditional banking. Many banks have tossed their reputations overboard in the past few years. At the Annual General Meeting of shareholders of Deutsche Bank, one disgruntled shareholder took the microphone and asked the assembled board of directors, “Is there any scandal in which Deutsche Bank is not involved?” That says it all.

When there is this kind of a shift in public perception, can you guess who a Congressman or Senator wants to court for campaign money? Access to Congress and steady behavior creates influence. According to the Silicon Valley Business Journal, in the latest election cycle, Silicon Valley's biggest political contributors gave more than US$50 million in campaign donations, making this group one of the largest contributors in the country. Interestingly, the split was roughly 55 percent Democrat and 45 percent Republican. Of the 13,000 individual citizens who gave the most, almost one-third of this group came from Silicon Valley. As campaign contributions shift away from banking toward financial technology, regulations will change. One example of this was the Jobs Act. Aimed at promoting private equity rather than bank debt as a means in setting up entrepreneurial activity, the Jobs Act passed in the House by a vote of 390 to 23. This bill legalized equity-based crowdfunding and was less than 50 pages. Now, contrast this against the Dodd-Frank bill, which is a regulatory ball and chain on the banks as a result of their bad behavior and is 14,000 pages. Guess who will win out?

This trend is important because in Nomi Prins' book, All the Presidents' Bankers, she has gone through the presidential papers of several 20th century administrations and, starting with President Rooosevelt, she notes that Wall Street was the first stop for campaign contributions. In his 1980 campaign, President Carter turned to Wall Street for a significant portion of his funding. (Up-and-coming Boy Wonder, Robert Rubin, helped Carter raise money.) Of course, Ronald Reagan received a lot of his funding from Wall Street and eventually picked Donald Regan as his Secretary of the Treasury. Regan was CEO of Merrill Lynch.

This is no more. Raising money from bankers in a high-profile way does not work in this day and age. Hence, we see more campaign contributions coming from a new generation of California-based financial technology entrepreneurs who are socially liberal but have a hybrid form of libertarian economic thinking. They advocate a liberal agenda in social affairs but want the government to stay out of everything else. This is, in a strange way, the polar opposite of traditional conservative Republican thinking.

Big Data, Crowdfunding, and the SME: The Magic Formula

In the past two years or so, a new chapter is being written. If there is a new capacity to sift through vast amounts of information—billions of bits of information on consumer habits in seconds—if there is a new source of gathering capital through crowdfunding, why not combine these to create new ways of lending that banks cannot do because they lack the flexibility, regulatory goodwill, innovation, and ingenuity? In other words, if a company like Intuit or Indinero comes along and offers software to help companies manage their receivables or payables, won't this information, which is shared with crowdfunders or smaller, more flexible banks (and highly accurate), allow these institutions to gain confidence to lend to various companies since they will have a better picture of the liquidity conditions of a company? What if these companies went further and offered software to help these companies manage tax, payroll, and overall working capital considerations?

If these companies can gather pools of capital and also manage the real-time software that is a constant examination of cash management, then they can become a genuine partner of this company and feel comfortable investing with them. They can have true and accurate information on taxes, payroll, and working capital. Furthermore, these lending pools can bypass ratings agencies that have tarnished their reputations by spurious rating activity, which helped the issuer more than the buyer of debt. This is precisely what is underway in a big way globally. The epicenter of this is in the United States, but it is spreading quickly to other parts of the world. I believe this phenomenon hit Asia only in the latter half of 2014. The one bank in Asia that is rapidly implementing this idea is CBA. CBA does not sell this software; it gives the software to companies for free. In this way, both the company and the bank act as partners and can have transparent information each day at 9 A.M. about the liquidity conditions of the company.

Other banks that are rapidly implementing these types of systems are BCA in Indonesia, UOB in Singapore, and CBA in Australia. Santander in Spain has an extensive financial technology platform, which puts it ahead of HSBC and Standard Chartered. BBVA gets it and is running ahead of regional giants. U.S. Bank also has a good reputation for grabbing onto this technology. By and large, however, the larger global universal banks have been sleepy. It boggles the imagination why these banks do not adapt this technology more quickly. The answer is clear for all to see. The larger universal global banks have so tarnished their reputations that instituting any global initiative is virtually impossible because these initiatives must be passed through dozens of regulators who are not that inclined to be cooperative because of history of mistrust. They simply do not believe the banks who say, “We are sorry and we will never break the law again.” The infractions of too many banks are as long as your arm and have infected hitherto-sacred institutions such as the London Interbank Offered Rate (LIBOR) daily fixing, which is what the world's system used to be based on. Global FX markets have been tarnished by illegal behavior. Banks have received heavy fines for manipulating the Japan interbank market. The bad behavior has infected many equity and bond exchanges. This behavior has infected foreign exchange markets in every major financial center. It has infected credit default swap markets. It has affected commodity markets. Local regulators are not in the mood for illegal activity or irresponsible lending practices that can cause an economy to implode overnight. In this way, slow-and-steady activity by clean and law-abiding equity-funded crowdfunders, SME software entrepreneurs, peer-to-peer lenders, or trusted regional banks may win out. It is unlikely the global universal larger banks will have their regulatory probation lifted any time soon or will have become small enough to flexibly and adroitly go on the offensive. Absence of trust and excessive size hinders them severely.

These smaller, entrepreneurial organizations now have the goodwill of regulators, the capacity, the technology and wherewithal to break into the SME market. And they can do it because monolithic banks are in legal and regulatory quicksand. Think about it. The largest unmet need in the world is the SME. This is a company with between US$500,000 and $8 million in revenues and anywhere from 3 to 30 employees. There are millions of these companies, especially in the emerging world. And they are utterly blocked from bank credit for an assortment of reasons.

One of the reasons why growth is not higher in the emerging world is that there is a plutocracy of wealthy, landed gentry who have access to credit (it is only ever a small number of families—between 8 and 20—who control economics in the emerging world) and tens of thousands of small companies that are deprived of credit. These companies are forced to get credit from often unregulated financial entities or outright loan sharks. They pay extortionate rates of interest, in the neighborhood of 30 percent to 40 percent. What if they bought software (or were given software) by a crowdfunder who could monitor and verify the weekly or monthly operations of this entity by watching its liquidity conditions, payroll, tax payments, and working capital requirements? A crowdfunder (or a smart bank) could quickly command market share and clean up for one simple reason: These entities, which could have comfort by analyzing (on a daily or weekly basis) the cash balances of a company, could lend to these companies and charge interest rates of 15 percent or 18 percent with a high degree of certainty. The company doing the borrowing at 18 percent would see these rates as a tremendous relief compared to extortionate levels of borrowing rates of 40 percent, which the company was paying in the past from very unpleasant loan sharks and the like. Everyone wins. Word will spread and others will join the bandwagon. Some of these small companies will become big companies and a virtuous circle will ensue. Ecosystems will form and banks either will be forced to change or will create the seeds of their own demise by refusing to grasp technological change.

Examples: Bringing Together the Data To Create New Opportunities and Reliable Credit Ratings

If these companies can grow to critical mass and avoid bad lending problems, there is a good chance they can disrupt the funding structure of millions of SMEs globally. They can offer 30–180 day credit products with a good degree of confidence because they understand the business of their client better than most. They can gather capital and act as a private equity funder using traditional bank products and a far cheaper rate than banks. They can enter the equipment leasing business. They can enter real estate funding under similar funding structures. They can easily steal away trade finance, since banks have a heavy burden from Basel II with regard to funding trade finance.

It is not inconceivable to see these companies entering into wealth products for the families of these companies. It would be easy to envision these financial technology companies offering tailored financing. It would also be easy to see how these firms could use financial supply chain optimization, because they would eventually grow large enough to potentially have data on both buyer and seller.

So far, a company like Funding Circle can offer credit far faster than a bank and can offer a slightly better rate. And in this cycle, the nonperforming loan rate of Funding Circle is currently lower than the average for U.S. banks. As and when they grow larger, these financial technology crowdfunders can gain economies of scale and really eat into traditional bank businesses. The finance function can be automated. Cash flow can be made more transparent for all to see. And the early feedback is that these new types of software allow a company to understand their firm better than ever before, never mind the lending entity. These companies are not out to create false fees or bogus charges and engage in criminality. Companies like Intuit want to make money from creating good software.

Companies like Kabbage can go further and enter into the world of the individual. It can turn the analysis of data into a microevent and offer money to people based on elaborate analysis of their e-commerce activity. Kabbage can offer cash in one day. Companies like UPS have entered into agreements to allow Kabbage to examine shipping histories. Kabbage is growing at more than 250 percent per annum, and if it achieves some kind of critical mass, there is no telling what it can do with smart analysis of big data. The savings to the customer could be enormous.

The bottom line is that companies like Intuit create new financial systems that integrate invoices, payments, and accounting records with all sorts of devices like phones, computers, and tablets. They can create customized features for various industry environments. They offer flexible, fair, and cheap software packages. There is no downloading. There are no contracts. A customer can cancel at any time. Why is this, as yet, still confined to the United States? Why is it not spreading into emerging markets? You watch. This revolution is slowly spreading across the Pacific Ocean. Companies like Moody's Analytics are stealthily using their U.S. technology bases to sell these types of bespoke software to companies, but this trend is very young.

Payment Systems

The last area where there is a more recognizable story is in payment systems. The traditional retail sector (books, magazines, household items, luxury items, cosmetics, etc.) is in a tailspin because virtually anything anyone wants to buy anywhere in the world is available online for a lower price. Needless to say, this is all deflationary due to the hyperefficiency with which companies like Amazon interact with these payment systems. The world of payments moves away from physical/retail activity with high rents to a private cyberworld of private purchases of ever cheaper items. All of this can be done more efficiently, more quickly, and with instant global pricing comparisons and payments, which will always search for the ever better discount. Table 11.5 shows what existing payment systems are able to do.

Table 11.5 Payment Systems Are Bleeding into Social Networks

| Company Name | Largest Investor | What They Do | Who Can It Threaten? | Comment |

| Alipay | N/A | Can provide 500 million customers with all bank services without a physical bank. Allows individuals and businesses to execute online payments. | Providers of individual payment systems (cards-only, online transfers) PayPal |

No legacy technology Breaking the rules Keep an eye on Yuebao (collectively received RMB 6.6 billion in deposits from Alipay users) |

| Adyen | N/A | Improving the efficiency of online and credit card payments as well as offering face-to-face payments. | Providers of individual payment systems (cards-only, online transfers) | NA |

| BitCoin | N/A | Digital currency that allows P2P transactions. An alternative foreign exchange. | Central banks, real foreign exchange Macroeconomists |

Gimmicky? |

| Dwolla | Union Square Ventures, Village Ventures, | Foreign exchange movement at low or no cost. | Providers of payment systems, payment terminals | 5 years old |

| Square | Starbucks, Citi Ventures |

Allows users to swipe credit card through the use of smartphones. All in one payment, inventory management, ordering, item sharing. |

Providers of payment systems, solutions, and terminals | Marquee list of participants Have raised more than US$300 million Antifraud system that shows where the transaction was made |

| Tenpay | N/A | Bolting credit card API to the phone and bypassing cards. | Providers of payment systems (cards-only, online transfers) | No legacy history; breaking all the rules |

Second-generation payments have already begun and are moving the system in different directions. This is similar to the way in which funding is tying itself to social networks. These payment systems are also tying themselves to social networks. Not only are these companies, such as Klarna, Venmo, and Stripe, easier and cheaper to use than existing payments systems, they are now flexible enough to be attached to social network entities like Facebook, where people can combine their social activity with their financial activity with the click of a button. The differences among and between checking accounts, savings account credit cards, and charge cards blur, and companies can even offer a “bridge loan” in funding of purchases. See Table 11.6 for more details about how these companies operate. These companies have high margins and, despite being around for a few years, have strong profit-generating power. Many banks are nowhere to be found in this area.

Table 11.6 Fascinating New Experiments in Payments with New Credit Checking

| Venmo is a payment app that enables you to send money instantly for free with social networking functions. Payments can be made with friends. Money can be held in Venmo account, or “cashed out” to a checking account. It is fun, simple, and fast. The goal: accepted like Visa and used like Facebook. |

| Klarna was founded in 2005. It is a Swedish-based e-commerce company that provides payment services for online storefronts. They assume stores' claims for payments and handle customer payments, thus eliminating the risk for seller and buyer. Most payment systems, like PayPal, require users to have money in their account or a credit card on file before they can buy. But Klarna underwrites the financial risk for retailers until people pay for the goods, either right after checking out or when the product arrives in the mail. |

| Stripe was founded in 2009 and is an application programming interface that can be embedded on websites to accept payments (no merchant account). Stripe charges 2.9% + $0.3 per charge, the same rate set by PayPal with no fees for setup, monthly use, minimum charges, validation, or card storage. Stripe has US$130 million in funding, and is valued at $1.75 billion. Ex-PayPal investors. |