CHAPTER 36

Calculation 30: Principal and Interest per Period

What It Means

In an amortized mortgage with level payments, a portion of each payment represents interest, and the balance is applied to the reduction of principal. How do you figure the interest/principal breakdown for a given payment?

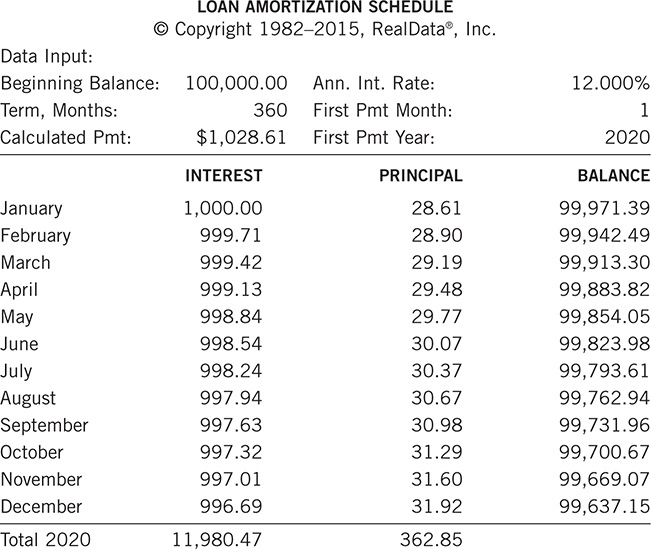

In the chapter “Principal Balance/Balloon Payment,” you saw a page from an amortization schedule that helps make this clear. In the particular loan shown there, the annual interest rate is 12%. You can calculate the monthly payment amount by using any of the techniques in the “Mortgage Payment/Mortgage Constant” chapter or by simply letting the amortization schedule software do it for you. At 12% interest and over a term of 360 months, the monthly payment required to amortize the loan is $1,028.61. The following schedule shows the progression of interest and principal over one year.

What are the mechanics of this progression? We’ve chosen an interest rate of 12% annually to make the schedule easy to follow. You make payments monthly; that means you are paying 1% per month on the outstanding balance. You must allocate your payment first to cover the interest, and then apply whatever is left over to reduce the principal. You borrowed $100,000, so you have use of that amount for one month at 1% per month, which costs $1,000 in interest. Because your payment is $1,028.61, there is $28.61 left to reduce the principal.

After the January payment, you have an outstanding balance of $99,971.39. You have the use of that amount of the lender’s money for the second month, so that’s the sum on which you must pay interest. One percent of 99,971.39 is 999.71. Again, your payment takes care of the interest first, which leaves 28.90 to apply to the principal. This process continues each month until all the principal is paid.

How to Calculate

Interest portion of a payment = Outstanding Principal Balance × Periodic Rate

Principal portion of a payment = Payment amount less Interest portion

Example

You have a mortgage with an annual interest rate of 6%. After you make your June payment of $2,700, a balance of exactly $400,000 remains on the loan. What is the interest and principal breakdown of your July payment?

If your annual interest rate is 6% (0.06), then your monthly rate is 1/12 of that, or 0.005. Apply the formula for the interest portion:

Interest portion of a payment = Outstanding Principal Balance × Periodic Rate

Interest portion of a payment = 400,000 × 0.005 = 2,000

Now that you know the interest portion is $2,000, it is easy to calculate the principal:

Principal portion of a payment = Payment amount less Interest portion

Principal portion of a payment = 2,700 less 2,000 = 700

Test Your Understanding

Why are amortizing mortgage payments more heavily weighted toward interest early in the life of the loan but gradually shift toward principal repayment as the loan progresses (as the loan becomes “seasoned,” to use the parlance of commercial lenders)?

Answer

The interest component of your payment is highest at the very beginning of the loan because your utilization of the lender’s funds is highest at that point. During the first month, you’re using the full face amount of the loan, so you must pay the highest fee (i.e., interest). With each installment, you are also repaying some of the principal, so the amount of the lender’s money you are using goes down each month, and so does your interest charge. The payment is a fixed amount; as the interest component declines (because you are paying for the use of less and less of the lender’s money), the principal component increases.