CHAPTER 37

Calculation 31: Maximum Loan Amount

What It Means

You know that when you apply for a home mortgage, you typically need to pass muster according to certain underwriting ratios. Most lenders require that your housing costs and your total debt payments not exceed specific percentages of your income.

With commercial mortgages, your personal credit is not irrelevant (being a deadbeat is seldom an advantage when it comes to borrowing money), but you will find that the lender is particularly interested in the ability of the property to produce income.

Even if you are a great credit risk, the amount of financing you are likely to obtain against a piece of income property will be limited by the interaction of three factors:

1. Net operating income (NOI)

2. Lender’s minimum debt coverage ratio (DCR)

3. Loan terms (as expressed by the annual mortgage constant)

We discussed these factors in Chapters 3 through 5 of Part I; each also has a chapter of its own in Part II. If you’re not yet familiar with these terms, you should review that material first.

How to Calculate

Maximum Loan Amount = Net Operating Income / Minimum Debt

Coverage Ratio / Mortgage Constant (annual)

In this formula, the NOI represents the property’s ability to produce income before financing; the mortgage constant accounts for the effects of financing; and the DCR expresses the amount of breathing room that must be maintained between the NOI and the debt service.

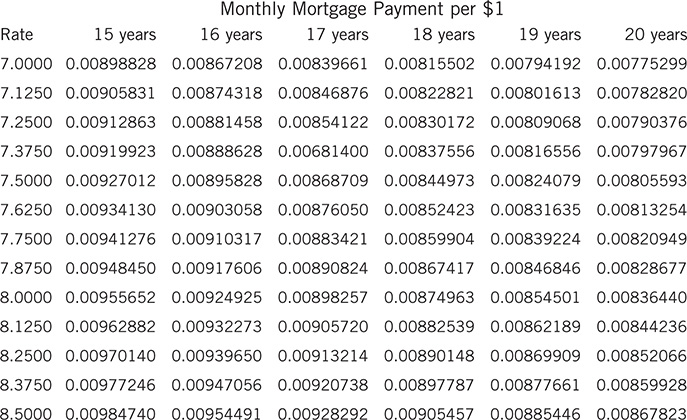

A table of monthly mortgage constants is available at http://www.realdata.com/book. For the purposes of the examples in this chapter, you can use the excerpt from that table that you see below. Because the table provides monthly constants and you need the annual factors, you must multiply the constant by 12. The revised formula now reads:

Maximum Loan Amount = Net Operating Income / Minimum Debt

Coverage Ratio / (Monthly Mortgage Constant × 12)

Example

You want to refinance a property that has an NOI of $120,000. Your lender offers a loan at 8% for 20 years and requires a DCR no less than 1.20. Under these terms, what is the maximum loan your property would support? Round the answer to the nearest $5,000.

Maximum Loan Amount = Net Operating Income / Minimum Debt

Coverage Ratio / (Monthly Mortgage Constant × 12)

Maximum Loan Amount = 120,000 / 1.2 / (0.00836440 × 12)

Maximum Loan Amount = 996,286 (round to 995,000)

Test Your Understanding

You’re seeking financing for a property with an NOI of $100,000. One lender requires a DCR of 1.3 at 7.875% for 20 years. A second lender requires a DCR of 1.2 at 7.625% for 15 years. Which lender is likely to give you the largest loan? Would the outcome change if both lenders offered loans for 20 years?

Answer

First lender at 20 years, 7.875%, 1.3 DCR:

Maximum Loan Amount = Net Operating Income / Minimum Debt

Coverage Ratio / (Monthly Mortgage Constant × 12)

Maximum Loan Amount = 100,000 / 1.3 / (0.00828677 × 12)

Maximum Loan Amount = 773,553 (round to 775,000)

Second lender at 15 years, 7.625%, 1.2 DCR:

Maximum Loan Amount = 100,000 / 1.2 / (0.00934130 × 12)

Maximum Loan Amount = 743,413 (round to 740,000)

Second lender at 20 years, 7.625%, 1.2 DCR:

Maximum Loan Amount = 100,000 / 1.2 / (0.00813254 × 12)

Maximum Loan Amount = 853,909 (round to 855,000)

In the question as stated originally, the first lender presented a more restrictive DCR and a higher interest rate. However, it also permitted a longer loan term, and that longer term reduced the debt service enough to justify a greater maximum loan. When the second lender matched the 20-year term, its lower rate and lower DCR requirement clearly gave it the advantage.