CHAPTER 39

Calculation 33: Adjusted Basis

What It Means

When you sell an income-property investment, the taxable profit that you realize is called the gain on sale (see Part II, Calculation 35), or simply gain. In order to calculate the gain, you need to know the selling price of the property as well as its adjusted basis. Under the current tax code, the adjusted basis is the original cost of an asset such as real estate, plus capital improvements and costs of sale, less accumulated depreciation.

In order to determine the gain on sale, you first calculate the adjusted basis and then find the difference between that amount and the selling price.

How to Calculate

The formula for adjusted basis reads as follows:

Original Basis (Purchase Price)

plus Capital Additions

plus Costs of Sale

less Cumulative Depreciation, Real Estate

less Cumulative Depreciation, Capital Additions

= Adjusted Basis

Example

You purchase a property for $200,000. The next year, you make $50,000 in capital additions. By the time you sell the property, you have taken $19,000 in depreciation on the original property and $5,100 on the additions. You sell the property, paying $22,000 as costs of sale. What is your adjusted basis?

The following is a form you can use for adjusted basis calculations:

Now fill in the amounts, and you’ll find that your adjusted basis for this property is $247,900:

Test Your Understanding

You purchase a property for $250,000. At the end of the first year, you make a $35,000 capital addition. At the end of the second year, you make a $30,000 addition. After five years, you sell the property for $475,000. At the time of sale, you have accumulated $25,000 depreciation on the original property, $3,500 on the first addition, and $3,000 on the second addition. You expect to pay selling costs of 6%.

1. What is your adjusted basis at the time of sale?

2. What is your gain on sale?

Answer

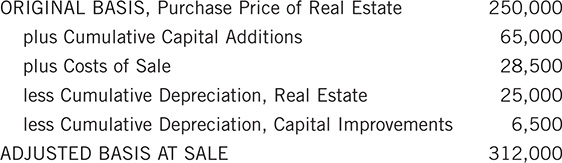

1. You need to start with a few preliminary calculations. You have two capital additions; add those together for a total of 65,000. Similarly, you must combine their cumulative depreciation, which totals 6,500. Finally, you need to calculate the costs of sale—6% of 475,000, or 28,500. Now you’re ready to fill in the form:

Your property’s adjusted basis is $312,000.

2. To find the gain on sale, you calculate the difference between the selling price and the adjusted basis:

Your gain on sale is $163,000.