Focus on: Basic Concepts—Module 9

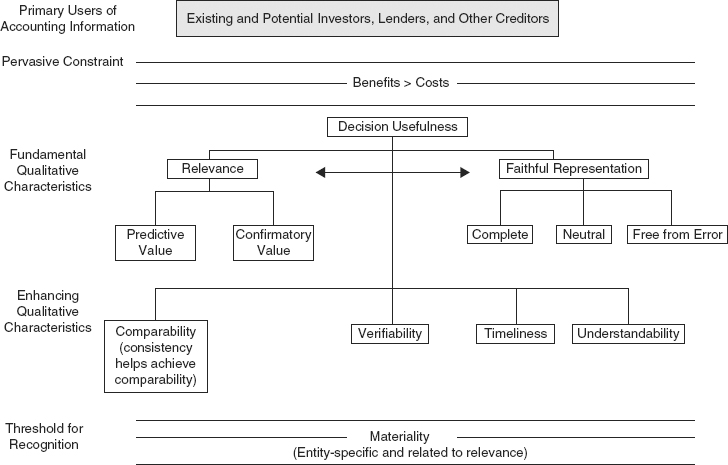

OBJECTIVES OF FINANCIAL REPORTING

The objectives of financial reporting are to provide:

- Information that is useful to potential and existing investors, lenders, and other creditors

- Information about the reporting entity’s economic resources and claims against those resources

- Changes in economic resources and claims

- Financial performance reflected by accrual accounting

- Financial performance reflected by past cash flow

- Changes in economic resources and claims not resulting from financial performance

Financial statements are designed to meet the objectives of financial reporting:

| Balance Sheet | Direct Information | Financial Position |

| Statement of Earnings and Comprehensive Income | Direct Information | Entity Performance |

| Statement of Cash Flows | Direct Information | Entity Cash Flows |

| Financial Statements Taken as a Whole | Indirect Information | Management and Performance |

Qualitative Characteristics of Accounting Information

IFRS® and U.S. Conceptual Framework as Converged

| Fundamental Characteristics/Decision Usefulness | Enhancing Characteristics |

| Relevance | Comparability |

Predictive value |

Verifiability |

Feedback value |

Timeliness |

Materiality |

Understandability |

| Faithful Representation | Constraints |

Completeness |

Benefit versus costs |

Neutrality |

|

Free from error |

Elements of Financial Statements

IFRS Elements

BASIC RULES AND CONCEPTS

Revenue Recognition

| Accrual method | Collection reasonably assured |

| Degree of uncollectibility estimable | |

| Installment sale | Collection not reasonably assured |

| Cost recovery | Collection not reasonably assured |

| No basis for determining whether or not collectible |

Installment Sales Method

| Installment receivable balance | Cash collections |

| × Gross profit percentage | × Gross profit percentage |

| = Deferred gross profit (balance sheet) | = Realized gross profit (income statement) |

Cost Recovery Method

All collections applied to cost before any profit or interest income is recognized

Converting from Cash Basis to Accrual Basis

Revenues

| Cash (amount received) | xx | |

| Increase in accounts receivable (given) | xx | |

Decrease in accounts receivable (given) |

xx | |

Revenues (plug) |

xx |

Cost of Sales

| Cost of sales (plug) | xx | |

| Increase in inventory (given) | xx | |

| Decrease in accounts payable (given) | xx | |

Decrease in inventory (given) |

xx | |

Increase in accounts payable (given) |

xx | |

Cash (payments for merchandise) |

xx |

Expenses

| Expense (plug) | xx | |

| Increase in prepaid expenses (given) | xx | |

| Decrease in accrued expenses (given) | xx | |

Decrease in prepaid expenses (given) |

xx | |

Increase in accrued expenses (given) |

xx | |

Cash (amount paid for expense) |

xx |

Balance Sheet

| Current Assets | Current Liabilities |

Cash |

Short-term debt |

Trading securities |

Accounts payable |

Current securities available for sale |

Accrued expenses |

Accounts receivable |

Current income taxes payable |

Inventories |

Current deferred tax liability |

Prepaid expenses |

Current portion of long-term debt |

Current deferred tax asset |

Unearned revenues |

| Long-Term Investments | Long-Term Debt |

Noncurrent securities available for sale |

Long-term notes payable |

Securities held to maturity |

Bonds payable |

Investments at cost or equity |

Noncurrent deferred tax liability |

| Property, Plant, and Equipment | Stockholders’ Equity |

| Intangibles | Preferred stock |

| Other Assets | Common stock |

Deposits |

Additional paid-in capital |

Deferred charges |

Retained earnings |

Noncurrent deferred tax asset |

Accumulated other comprehensive income |

Current Assets and Liabilities

| Assets | Liabilities |

Economic resources |

Economic obligation |

Future benefit |

Future sacrifice |

Control of company |

Beyond control of company |

Past event or transaction |

Past event or transaction |

| Current Assets | Current Liabilities |

Converted into cash or used up |

Paid or settled |

OR Requires use of current assets |

|

Longer of: |

Longer of: |

One year |

One year |

One accounting cycle |

One accounting cycle |

IFRS and Current Liabilities

- Short-term obligations expected to be refinanced must be classified as current liabilities unless there is an agreement in place prior to the balance sheet date.

- A “provision” is a liability that is uncertain in timing or amount.

- If outcome is probable and measurable, it is not considered a contingency.

- “Probable” means greater than 50%.

- A “contingency” is not recognized because it is not probable that an outflow will be required or the amount cannot be measured reliably.

- Contingencies are disclosed unless probability is remote.

Special Disclosures

Significant Accounting Policy Disclosures

Inventory method

Depreciation method

Criteria for classifying investments

Method of accounting for long-term construction contracts

Risks and Uncertainties Disclosures

Nature of operations

Use of estimates in the preparation of financial statements

Certain significant estimates

Current vulnerability due to concentrations

Subsequent Events

An event occurring after the balance sheet date but before the financial statements are issued or available to be issued. Measured through the issuance date.

Two types of events are possible:

IFRS: Subsequent events measured through the date the financial statements are authorized to be issued.

Related-Party Transactions

Exceptions:

Reporting the Results of Operations

Preparing an Income Statement

| Multiple Steps | Single Step |

| Revenues | Revenues |

| – Cost of sales | + Other income |

| = Gross profit | + Gains |

| – Operating expenses | = Total revenues |

Selling expenses |

– Costs and expenses |

General and administrative (G&A) expenses |

Cost of sales |

| = Operating income | Selling expenses |

| + Other income | G&A expenses |

| + Gains | Other expenses |

| – Other expenses | Losses |

| – Losses | Income tax expense |

| = Income before taxes | = Income from continuing operations |

| – Income tax expense | |

| = Income from continuing operations |

Computing Net Income

| Income from continuing operations (either approach) | |

| ± | Discontinued operations |

| ± | Extraordinary items |

| = | Net income |

(Cumulative changes section was eliminated by precodification SFAS 154.)

IFRS Income Statement

- Revenue (referred to as income)

- Finance costs (interest expense)

- Share of profits and losses of associates and joint ventures accounted for using equity method

- Tax expense

- Discontinued operations

- Profit or loss

- Noncontrolling interest in profit and loss

- Net profit (loss) attributable to equity holders in the parent

- No extraordinary items under IFRS

Errors Affecting Income

Error (ending balance)

| Current Statement | Prior Statement | |

| Asset overstated | Overstated | No effect |

| Asset understated | Understated | No effect |

| Liability overstated | Understated | No effect |

| Liability understated | Overstated | No effect |

Error (Beginning balance – Ending balance is correct)

| Asset overstated | Understated | Overstated |

| Asset understated | Overstated | Understated |

| Liability overstated | Overstated | Understated |

| Liability understated | Understated | Overstated |

Error (Beginning balance – Ending balance is not correct)

| Current Statement | Prior Statement | |

| Asset overstated | No effect | Overstated |

| Asset understated | No effect | Understated |

| Liability overstated | No effect | Understated |

| Liability understated | No effect | Overstated |

Extraordinary Items

Classification as extraordinary—two requirements (both must apply)

One or neither applies—component of income from continuing operations

Extraordinary

A hailstorm damages all of a farmer’s crops in a location where hailstorms have never occurred

Acts of nature (usually)

Not Extraordinary

Gains or losses on sales of investments or property, plant, and equipment

Gains or losses due to changes in foreign currency exchange rates

Write-offs of inventory or receivables

Effects of major strikes or changes in value of investments

Change in Accounting Principle: Allowed Only if Required by New Accounting Principles or Change to Preferable Method

Use retrospective application of new principle:

Journal entry:

Special Changes

Changes in accounting principle are handled using the prospective method under limited circumstances. No calculation is made of prior-period effects, and the new principle is simply applied starting at the beginning of the current year when the following changes in principle occur:

- Changes in the method of depreciation, amortization, or depletion

- Changes whose effect on prior periods is impractical to determine (e.g., changes to last in, first out [LIFO] when records don’t allow computation of earlier LIFO cost bases)

(Note: The method of handling changes in accounting principle described here under ASC 250-10 replaces earlier approaches, which applied the cumulative method to most changes in accounting principle. Precodification SFAS 154 abolished the use of the cumulative method.)

Change in Estimate

- No retrospective application

- Change applied as of beginning of current period

- Applied in current and future periods

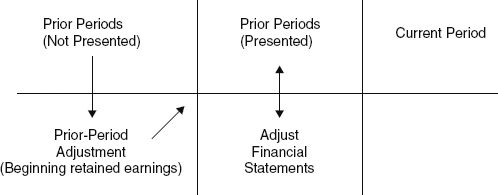

Error Corrections

Applies to:

- Change from unacceptable principle to acceptable principle

- Errors in prior period financial statements

When error occurred:

Discontinued Operations

When components of a business are disposed of, their results are reported in discontinued operations:

- Component—An asset group whose activities can be distinguished from the remainder of the entity both operationally and for financial reporting purposes.

- Disposal—Either the assets have already been disposed of or they are being held for sale and the entity is actively searching for a buyer and believes a sale is probable at a price that can be reasonably estimated.

All activities related to the component are reported in discontinued operations, including those occurring prior to the commitment to dispose and in prior periods being presented for comparative purposes.

Reporting Discontinued Operations

Lower section of the income statement:

- After income from continuing operations

- Before extraordinary items

Reported amount each year includes all activities related to the component from operations as well as gains and losses on disposal, net of income tax effects

- Expected gains and losses from operations in future periods are not reported until the future period in which they occur.

Impairment loss is included in the current period when the fair market value of the component is believed to be lower than carrying amount based on the anticipated sales price of the component in future period.

Reporting Comprehensive Income

Statement of comprehensive income required as one of the financial statements

- May be part of income statement

- May be separate statement

- Begin with net income

- Add or subtract items of other comprehensive income

Other comprehensive income includes:

- Current year’s unrealized gains or losses on securities available for sale

- Current year’s foreign currency translation adjustments

- Current year’s unrealized gains or losses resulting from changes in market values of certain derivatives being used as cash flow hedges

Reclassification Adjustments

- As unrealized gains (losses) recorded and reported in other comprehensive income for the current or prior periods are later realized, they are recognized and reported in net income. To avoid double counting, it is necessary to reverse unrealized amounts that have been recognized.

Accounting for Changing Prices

Accounting at Current Cost

Assets and liabilities reported at current amounts

Income statement items adjusted to current amounts

- Inventory reported at replacement cost

- Cost of sales = Number of units sold × Average current cost of units during period

- Differences in inventory and cost of sales treated as holding gains or losses

- Depreciation and amortization—Computed using same method and life based on current cost

Accounting for Changes in Price Level

Purchasing power gains and losses relate only to monetary items

- Monetary assets—Money or claim to receive money such as cash and net receivables

- Monetary liabilities—Obligations to pay specific amounts of money

Company may be monetary creditor or debtor

- Monetary creditor—monetary assets > monetary liabilities

- Monetary debtor—monetary liabilities > monetary assets

In periods of rising prices

- Monetary creditor will experience purchasing power loss

- Monetary debtor will experience purchasing power gain

Liquidation Basis of Accounting

SEC Reporting Requirements

Regulation S-X describes form and content to be filed

Regulation S-K describes information requirements

- Form S-1 (US)/F-1 (foreign)—Registration statement

- Form 8-K (US)/6-K (foreign)—Material event

- Form 10-K (US)/20F (foreign)—Annual report

- Form 10Q—Quarterly report

- Schedule 14A—Proxy statement

Regulation AB describes asset-backed securities reporting

Regulation Fair Disclosure (FD) mandates material information disclosures

- Compliance through an 8-K issuance

Fair Value Measurements

Six-step application process

Multiple disclosures for assets/liabilities measured at fair value on a recurring/nonrecurring basis

Fair Value Concepts

Fair value—The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (exit price) under current market conditions

Principal market (greatest volume of activity)

Most advantageous market (maximizes price received or minimizes amount paid)

Highest and best use—Maximize the value of the asset or group of assets

Valuation techniques

Fair value hierarchy (level 1, 2, and 3 inputs)

Fair value option—An election to value certain financial assets and financial liabilities at fair value