Focus on: Inventories—Module 10

INVENTORIES

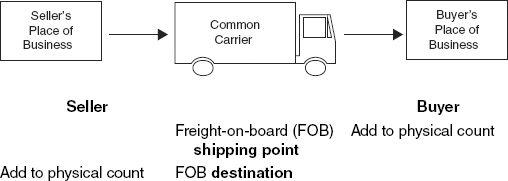

Goods in Transit

Abnormal costs expensed in current period instead of being included in inventory:

- Idle facility expense

- Wasted materials in production

- Double freight when items returned and redelivered

Cost of Goods Sold (COGS)

Beginning inventory

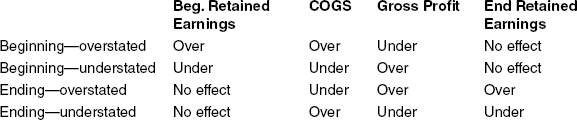

Inventory Errors

Periodic versus Perpetual

| Periodic | Perpetual | |

| Buy merchandise | Purchases | Inventory |

Accounts payable |

Accounts payable |

|

| Sell merchandise | Accounts receivable | Accounts receivable |

Sales |

Sales |

|

| COGS sold (COGS) | ||

Inventory |

||

| Record COGS | Ending inventory (count) | |

| COGS (plug) | ||

Purchases (net amount) |

||

Beginning inventory (balance) |

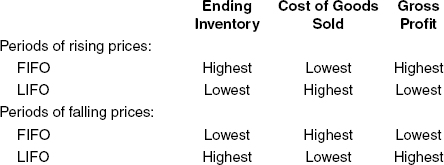

First in, first out (FIFO)—Same under either method

Last in, first out (LIFO)—Different amounts for periodic and perpetual

Average—Different amounts for periodic and perpetual

Inventory Valuation Methods

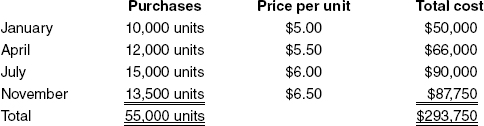

FIFO Application—Valuing Cost Of Sales and Ending Inventory

The earliest purchased goods are assumed to be sold first

Cost of sales and ending inventory values are identical under perpetual and periodic methods

Example: Beginning inventory = 0; Ending Inventory = 15,000

Calculate the value of ending inventory and cost of sales:

Ending inventory = 15,000 units (given) = November 13,500 units × $6.50 + July 1,500 units × $6.00 = $96,750 (ending inventory consists of the latest purchased units).

Cost of sales: Total available – Ending inventory = $293,750 − 96,750 = $197,000

LIFO Application—Valuing Cost of Sales and Ending Inventory Using the Periodic Method

The earliest purchased goods are assumed to be sold last

Cost of sales and ending inventory values are different under perpetual and periodic methods

Example of periodic method: Beginning inventory = 0; Ending Inventory = 15,000

Calculate the value of ending inventory and cost of sales:

Ending inventory = 15,000 units (given) = January 10,000 units × $5.00 + April 1,500 units × $5.50 = $58,250 (ending inventory consists of earliest purchased units)

Cost of sales: Total available – Ending inventory = $293,750 − 58,250 = $235,500

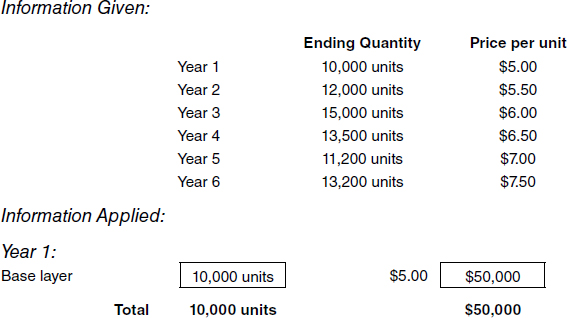

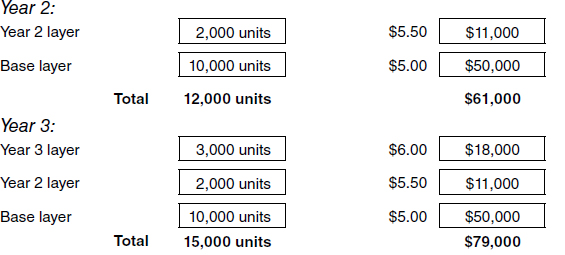

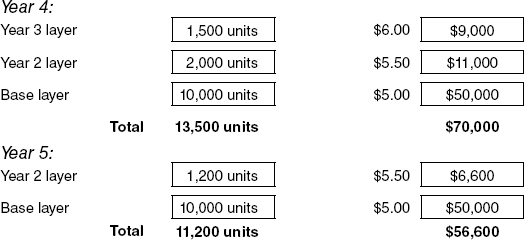

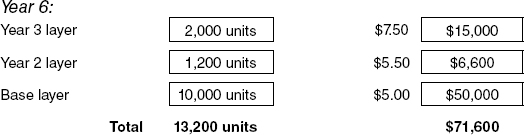

Applying LIFO Layers

For each layer:

Inventory quantity × Price per unit = Inventory value

Application of LIFO

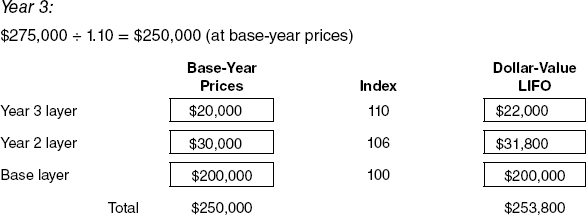

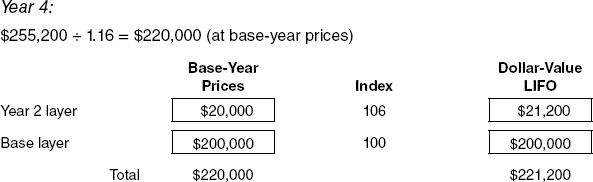

Dollar-Value LIFO

Less cumbersome than LIFO for inventory consisting of many items

Combines inventory into pools

Increases in some items within a pool offset decreases in others

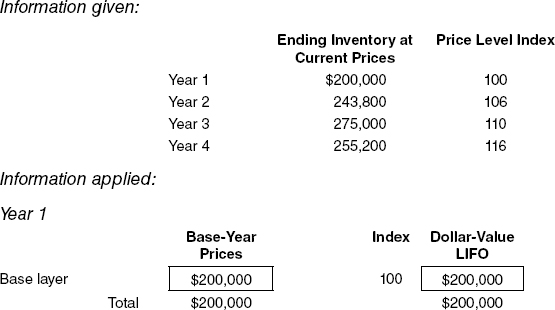

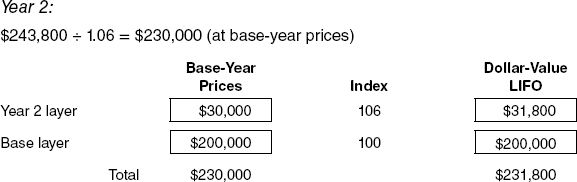

Applying Dollar-Value LIFO

For each layer:

Application of Dollar-Value LIFO

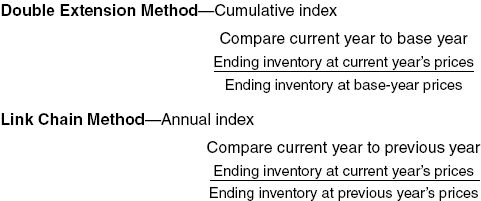

Dollar-Value LIFO—Calculating a Price Level Index

Simplified LIFO—Company uses a published index

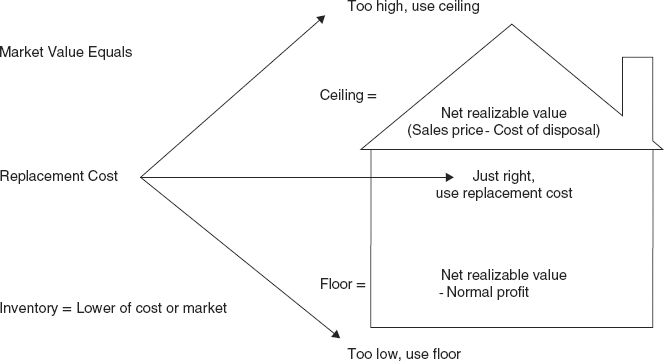

Lower of Cost or Market

Gross Profit Method for Estimating Inventory

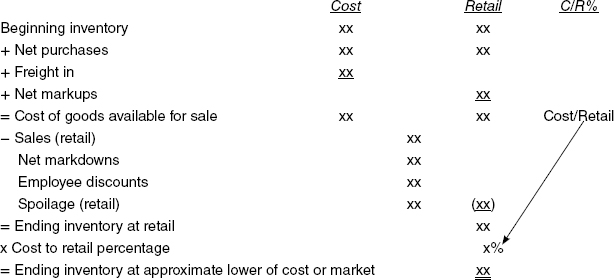

Conventional Retail (Lower of Cost or Market)

IFRS: Inventory

- LIFO not permissible

- Lower of cost or net realizable value (LCNRV) on item-by-item basis

- Biological assets carried at fair value less costs to sell at the point of harvest

LONG-TERM CONSTRUCTION CONTRACTS

Percentage of Completion

Use when:

- Estimates of costs are reasonably dependable

- Estimates of progress toward completion

Reporting profit

- Recognized proportionately during contract

- Added to construction in process

Balance sheet amount

- Current asset—Excess of costs and estimated profits over billings

- Current liability—Excess of billings over costs and estimated profits

Calculating profit

| Contract price | xxx | |

| Total estimated cost | ||

Cost incurred to date (1) |

xxx | |

Estimated cost to complete |

+ xxx | |

Total estimated cost (2) |

− xxx | |

| Total estimated profit (3) | = xxx |

Costs incurred to date (1) ÷ Total estimated cost (2) = % of completion (4)

% of completion (4) × Total estimated profit (3) = Estimated profit to date (5)

Estimated profit to date (5) – Profit previously recognized = Current period’s profit

Recognizing Losses

When loss expected:

Estimated loss |

xxx |

| + Profit recognized to date | xxx |

| = Amount of loss to recognize | xxx |

Completed Contract

Income statement amount

- Profit recognized in period of completion

- Loss recognized in earliest period estimable

Balance sheet amount

- Current assets—Excess of costs over billings

- Current liabilities—Excess of billings over costs

IFRS Construction Contracts

- Prohibit completed contract method