8. A Handful of Content: Games, Mobile Applications, and Mobile Marketing

Electronic gaming has continued its rapid rise, now claiming more revenue than either movies or music. However, gaming faces challenges. Classic video gaming, focused on a specific sector of the population, must widen its base while also battling the prime concerns of consumers: which device, what type of access, and how about that content? In the meantime, social and mobile gaming are charging up from behind, riding the wave of smartphones and tablets, changing the gaming and the marketing landscape. This ever-increasing interest in gaming is causing many products and services to include gaming in their marketing efforts.

Where devices go, marketing is soon to follow. The ability to track consumers as they actually reach a buying decision is an intriguing part of this new platform.

The Game’s Afoot

Ten years ago, we predicted that video games would outstrip movie (box office) revenue within the next ten years. We were wrong—it actually happened within four years of the release of our earlier edition of this book. Gaming is huge. The global video-game market was worth around $56 billion last year, more than twice the size of the recorded-music industry and nearly a quarter more than the magazine business.1 The U.S. industry is projected to reach $25 billion by 2017.2

1 “All the World’s a Game,” The Economist, December 10, 2011.

2 “New Reports Forecast Global Video Game Industry Will Reach $82 Billion By 2017,” Forbes, July 8, 2012.

However, like every other entertainment platform, the digital disruption is taking the air out of current business models, deflating some sectors while others rise. Digital downloads and online gaming have weakened overall revenue for video games. Device and access, the same underlying earth-movers that are affecting other entertainment platforms, are having the same impact here: disrupting current business models while forming a base for new ones. Consumers are finding new devices to take their games where they want and new ways to access their favorites, heavily favoring mobile versus computer or console-based games.

This shift is taking its toll, roiling hardware and software sales. But with mobile and online gaming charging up, forecasts for the overall growth of the platform are still rosy.

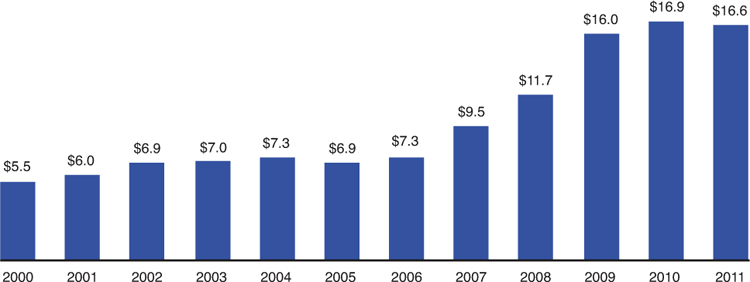

Consider the two charts in Exhibits 8-1 and 8-2.

Exhibit 8-1 U.S. electronic game sales growth, 2000 to 2012

Source: The Entertainment Software Association, 2012

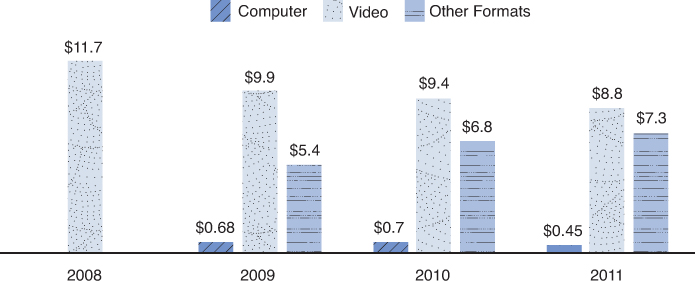

Exhibit 8-2 Electronic game sales by segment, 2008 to 2011

Source: The Entertainment Software Association, 2012

See the leap in 2009? That’s the beginning of the digital onslaught. Exhibit 8-2 gives a closer look at the impact.

Those “other formats” include subscriptions, digital full games, digital add-on content, mobile apps, social network gaming, and other physical delivery—all of the new access models and platforms that have come on line in the four years, from smartphones to tablets to the cloud. Sales of video games, the classic hard disc/console-driven variety, have been steadily declining, while online delivery, social, and mobile games—the ones you play on your iPhone or Android—have been rising. Today, it’s hard to find a device with a screen that doesn’t offer an interactive entertainment experience.

So why are those traditional games slipping? First, consider the expense related to hard-core video gaming, the classic 37-year-old-guy variety: the game itself, the HDTV, the sound system or the premium headphones. It’s an expensive hobby. With mobile/social gaming, there are expenses—the smartphone, the tablet—but they aren’t necessarily specific to gaming per se; you’re using that device for many other purposes. And the games themselves are far less expensive.

And then there’s the content. The video game industry, long scrutinized for the violent “first-shooter” games that dominate the landscape, has been slow to move into other areas. They have a dedicated base that has kept the business growing for many years. But that base is saturated. The industry needs to move beyond those average 37-year-old males, or it will continue to contract.

Younger players—the ones who might normally be picking up the baton—are entering the gaming universe through different devices. They won’t suddenly switch their mode of play just because they get a job, at least not in the numbers they did in earlier days.

This isn’t lost on the game developers. Even such giants as Disney, which once believed that video games could have perfect synergy with feature releases, are shuttering some of their gaming divisions as they shift their focus to the mobile/social world, where gaming is ramping up at steeper angles than video ever did.

It isn’t that we’ve stopped playing. Far from it. We’ve just moved on.

So who is playing these days?

Players by the Numbers

The Entertainment Software Association (ESA) offers plenty of interesting data in its recently published report, Essential Facts about the Computer and Video Game Industry.3 Among the figures cited are these nuggets:

3 “2012 Sales, Usage and Demographic Data: Essential Facts about the Computer and Video Game Industry,” the Electronic Software Association.

![]() The average U.S. household owns at least one dedicated game console, PC, or smartphone.

The average U.S. household owns at least one dedicated game console, PC, or smartphone.

![]() Forty-nine percent of U.S. households own a dedicated game console, and those that do own an average of two.

Forty-nine percent of U.S. households own a dedicated game console, and those that do own an average of two.

![]() The average game player is 30; 32% are under 18; 31% are 18 to 35; and 37% are 36+.

The average game player is 30; 32% are under 18; 31% are 18 to 35; and 37% are 36+.

Now let’s talk gender—and this is where it gets interesting.

![]() Forty-seven percent of all players are women, and women over 18 years of age are one of the industry’s fastest growing demographics.

Forty-seven percent of all players are women, and women over 18 years of age are one of the industry’s fastest growing demographics.

![]() Today, adult women represent a greater portion of the game-playing population (30%) than boys age 17 or younger (18%).

Today, adult women represent a greater portion of the game-playing population (30%) than boys age 17 or younger (18%).

According to Flurry,4 a consulting firm specializing in “the New App Economy,” though the classic hardcore gamer was male (60% versus 40%), women are driving the rising revenue in social and mobile gaming, 53% to 47%. This same source tells us that this female gamer earns over 50% more than the average American and is more than twice as likely to have earned a college bachelor’s degree.

4 Farago, Peter, “Mobile Social Gamers: The New Mass-Market Powerhouse,” February 22, 2001, http://blog.flurry.com/.

A few more facts to add to the mix, again from the ESA:

![]() Sixty-two percent of gamers play games with others, either in person or online. Seventy-eight percent of these gamers play with others at least one hour per week.

Sixty-two percent of gamers play games with others, either in person or online. Seventy-eight percent of these gamers play with others at least one hour per week.

![]() Thirty-three percent of gamers play social games.

Thirty-three percent of gamers play social games.

Gaming Platforms: Video

Up until just recently, when we said “video games,” we immediately thought of either the hard-disc variety that fit into a console, or the computer-based games that allowed for a massive multiplayer online (MMO) experience. These types of games typically fit into the following revenue models5:

5 Chulis, Kimberly, “Big Data Analytics for Video, Mobile, and Social Game Monetization,” July 17, 2012, www.ibm.com/developerworks/.

![]() Pay-to-play: Requires players to pay a monthly subscription fee

Pay-to-play: Requires players to pay a monthly subscription fee

![]() Free-to-play: Involves an upfront software cost but no additional payments

Free-to-play: Involves an upfront software cost but no additional payments

![]() Freemium: Allows players to access game content and play for free but offers options to pay for additional content and access

Freemium: Allows players to access game content and play for free but offers options to pay for additional content and access

Some games have been around long enough to combine more than one model. World of Warcraft is the most profitable game in history, generating nearly $700 million in sales of the original game and expansions, with another $1.4 billion in subscription revenue.6

6 Blizzard Entertainment Statistics, www.statisticbrain.com.

In addition, these games have created allied industries. The Entertainment Software Association estimates that 2011 content sales generated an additional $5.59 billion in hardware sales. Our old friend licensing and merchandising makes its appearance here as well, with $2.62 billion in accessories, including clothing. However, with the drop in content sales now hitting its fourth consecutive year, video games reflect the appearance of a maturing industry.

The marketing of video games has many similarities to the movie business. Games are advertised in all mediums, including TV and prior to trailers in movie theaters. Titles are released simultaneously across all platforms: Xbox, PS3, and PC. In addition, many games are released regularly once a year, or once every two years, like film sequels.

One of the most important trends now underway, from the perspective of our overall discussion, is the shift in gaming console usage. Today’s gaming consoles are all Internet-enabled and allow for over-the-top access to a wide variety of content, far more than just online games. Most of them come already preloaded with Netflix, Vudu, Hulu, and various social networking favorites. It is not out of the realm of possibility that set-top boxes could become a thing of the past, with what was formerly known as a gaming console being the media conduit in the typical home—which will also allow gamers to connect to the cloud, the quickly growing home of gaming software.

Gaming Platforms: Social

Social gaming refers to gaming that requires interaction with others, rather than gaming in solitude. Although this is certainly an attribute of video games, the term is most often used to describe games that are connected to social networking as the primary focus—in other words, you can’t play the game alone.

Social games got their big start—revenue is predicted to reach $8.6 billion in 20147—with Facebook, where Zynga, the game developer responsible for such hits as FarmVille and ChefVille, profited from allowing gamers to start for free but achieve higher status by buying up. Gamers can use actual money or Facebook credits to purchase in-game virtual goods to help them perform better, get premium access, and move to higher levels faster.

7 “Social Game Revenue Should Outgrow Facebook by 2014,” www.allfacebook.com, via a study by SuperData Research, October 10, 2011.

But social game developers are moving away from Facebook, primarily due to two factors:

![]() The potential growth of non-Facebook social gaming due to increased device ownership and use

The potential growth of non-Facebook social gaming due to increased device ownership and use

![]() The restrictions that Facebook has placed on game developers, including higher revenue cuts for the site and an increasing inability for developers to post adverts on users’ walls

The restrictions that Facebook has placed on game developers, including higher revenue cuts for the site and an increasing inability for developers to post adverts on users’ walls

Of that forecasted $8.6 billion, over $5 billion should be coming from non-Facebook social gaming by 2014, according to the same source. Like everything else, this growth will be facilitated in part by the ongoing move to mobile platforms.

Going Mobile

Even as the gaming console works to become the center of our home-media universe, the consumer is walking away: out of the family room, into the street, wherever they wish to go. The shift to mobile applications has all the makings of a tsunami, riding the currents of new devices, better access, and more content. And surfing along with it are the entertainment marketers, weaving content and advertising together in one seamless curl.

Gaming Platforms: Mobile

The one constant in entertainment is this: if it’s good (and sometimes even when it’s not), people want more. Entertainment platforms—movies, television, cable, even books and magazines—have turned into huge industries to feed the public’s desire for pleasure. As always, it is technology that moves the business forward, and in the digital disruption, the prime mover is the mobile device: smartphones and tablets. And when it comes to mobile content, games reign supreme.

What’s ‘Appening

What drives the mobile world are applications. The word itself generically applies to all types of software for all types of devices, but for the purposes of this discussion—and in the minds of more and more consumers—applications, or apps, are specific programs written to perform specific tasks for use on a mobile device.

There are currently over 500,000 apps available. By the time you read this, that number might have doubled. Unlike software packages such as Microsoft Office—broad-based programs that integrate into the operating system of a computer, which require hundreds of thousands of programming hours to create and maintain—applications can be (relatively) quickly developed by entrepreneurs hoping to hit it big.

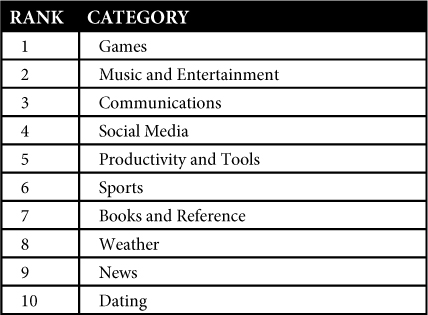

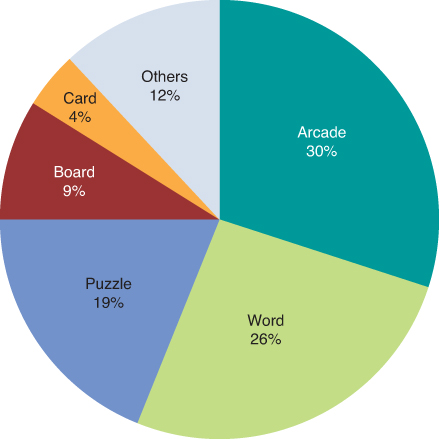

That’s a good thing because the consumer is clamoring for them and especially for entertainment, as shown in Exhibit 8-3.

Exhibit 8-3 Top Ten Mobile Application Categories8

8 “Mobile Game Applications: Special Report,” January 2013, Millennial Media, www.millenialmedia.com.

The types of games that people are interested in cover a broad swath. In Exhibit 8-4, we can determine the ranking of the particular categories based on impressions: the number of times the app is located and loaded.

9 Ibid.

Monetizing Mobile

There are three basic forms of monetization in the mobile app world. The first, of course, is the revenue generated from the purchase of the application. Part of the appeal of apps is their pricing. Consumers seem to easily equate value to apps in the $.99 to $4.99 range, where they operate as inexpensive impulse buys.

The second stream comes from advertising. Gaming companies offer in-game banner ads, video offers, and full-page advertisements. In fact, ad-supported revenue in mobile gaming applications grew 119% year-over-year in 2012. More on the mechanics of this in just a moment.

The third and possibly the most rapidly growing form of revenue comes from in-game purchases. Though the original focus of gaming apps tended to be on the number of downloads a game might generate, at anywhere from $.99 and up, in-game purchases are...ahem...changing the game in gaming. Eighty percent of the 10 top-grossing iPhone apps in America—and 85% of the top 20—are now free. And why not? The real money is coming from what the gamer buys once he’s in the game. Hooked on a driving game but unable to rise through the ranks? Purchase a more powerful race car. The buys aren’t necessarily inexpensive, either: Top-grossing games like Rage of Bahamut offer in-app purchases ranging from $0.99 to $99.99.

Ka-ching, ka-ching.

Gaming is a big business that will continue to get bigger. Industry analyst R.W. Baird estimates that this sector will continue to grow at a rate of 15% to 20% for the next several years.10 There will be more devices, more ways to access games, but most important, it will continue to reach into new demographics. Gaming is becoming more small-d democratic and far more accessible, on all levels. But most of all, gaming taps into one great desire harbored by nearly every living being in one form or another: the desire to play.

10 “Game Industry Forecast Shows Solid Growth,” October 12, 2011, www.industrygamers.com.

Why We Game

Play is a critical element in human society. As children, we play to learn. The quote, “Play is the work of children,” has been attributed to many people, but regardless of who said it first, it’s true. Play teaches children how to be social and how to compete, creates a reward structure, and, oh yeah, it’s fun. Play is something we spend a tremendous amount of time on when we are young, and with any luck, we find ways to bring it into our lives as we age.

Gaming is growing because it hits those long-ago-learned hot buttons. Some games allow for social interaction. Some allow for reward, and some give players the chance to become well-respected leaders or guides. Most tickle the need for competition. In short, games offer users a valuable personal experience, one tailored to the perceptions of the individual. One of the great fallacies of social interaction is the concept that people are only incentivized by money—many businesses have made this mistake, losing employees to competitors who offered a different type of reward: a sense of accomplishment based on the opinions of their peers; an ability to give value back to society. Gaming operates within these same principles.

Knowing that, how are savvy marketers increasing their connections with consumers? By increasing the use of games at all levels of marketing.

Gamification

In their excellent overview, KISSmetrics, an online analytics company, defines gamification as the use of gaming in marketing to engage and influence consumer behavior.11 The concept isn’t new; detergent companies kept their sales steady during the Depression by offering sets of dishes that could only be completed by buying enough soap. Those companies were appealing to the inner desire for reward, a key component of gaming.

11 “How to Use Gamification for Better Business Results,” www.kissmetrics.com.

But the growing use of devices that deliver games affords marketers an easy connection to the consumers they wish to reach, and gamification offers them the vehicle. Google offers an intriguing interactive graphic that continually charts the rise in interest in gamification over the last several years, with key markers, at www.google.com/trends/explore#q=gamification.

KISSmetrics goes on to outline the key attributes of gamification12 as follows:

12 Ibid.

![]() Rewards: A reward is something you receive and feel positive about. The feeling positive part is the key ingredient. Consumers should be rewarded with virtual goods (such as points) for specific behavior (that is, a purchase, filling out a form, and so on), and those virtual items should offer access to exclusive privileges and rewards, such as levels or prizes.

Rewards: A reward is something you receive and feel positive about. The feeling positive part is the key ingredient. Consumers should be rewarded with virtual goods (such as points) for specific behavior (that is, a purchase, filling out a form, and so on), and those virtual items should offer access to exclusive privileges and rewards, such as levels or prizes.

![]() Loss Aversion: Most people strongly prefer avoiding losses to acquiring gains. One way to get going with this is to give people something right away that they can lose (unless they keep playing). When you join Zynga’s Farmville, you get a starter farm. If you don’t visit the farm and care for your crops, they wither and die.

Loss Aversion: Most people strongly prefer avoiding losses to acquiring gains. One way to get going with this is to give people something right away that they can lose (unless they keep playing). When you join Zynga’s Farmville, you get a starter farm. If you don’t visit the farm and care for your crops, they wither and die.

![]() Status, Competition, and Reputation: Most people inherently want a higher status not only to keep up, but to out-do the Joneses. This is why leaderboards are a good idea. Also, making achievements social encourages people to continually one-up and stay motivated to reach clear goals.

Status, Competition, and Reputation: Most people inherently want a higher status not only to keep up, but to out-do the Joneses. This is why leaderboards are a good idea. Also, making achievements social encourages people to continually one-up and stay motivated to reach clear goals.

![]() Feedback: Feedback tells users that their intended action was registered and shows the outcomes of that action. Seeing points accumulate as actions are taken establishes a clear and instant reward system. It’s also an immediate indication that the user is getting closer to her goal. Continually accomplishing small goals to reach a larger goal is often what makes games addictive.

Feedback: Feedback tells users that their intended action was registered and shows the outcomes of that action. Seeing points accumulate as actions are taken establishes a clear and instant reward system. It’s also an immediate indication that the user is getting closer to her goal. Continually accomplishing small goals to reach a larger goal is often what makes games addictive.

Examples of gamification are rampant. Airline loyalty programs allow customers to build status and gain rewards. Nike sells shoes by inserting a device that allows runners to track their stats and compete against others. Trip Advisor builds loyalty by assigning badges to travelers who submit reviews and continues to pump the connection through ongoing emails that remind the travelers that they need to post more to reach a higher status. Local businesses have used gamification principles in posting questions on Facebook and then rewarding locals who answer with some type of prize. It seems almost impossible to accomplish any task these days that isn’t pointing you toward a website or urging you to download an app.

Mobile Marketing

There are two constants in innovation as it relates to media. The first is any new media platform will eventually attract businesses based on sex. The second is any new media platform will soon become a handy marketing channel. After all, as we continue to discuss throughout this book, it’s the monetization of media that builds a business, and marketing is a key component of that effort.

Mobile marketing has taken off in the past few years with, we would assume, much more to come. The following is a quick overview of the practice. Like everything else in the disruption, expect changes to occur momentarily, as devices multiply and standards are set.

The channels used by mobile marketing include

![]() SMS: Text messages to the device.

SMS: Text messages to the device.

![]() MMS: Multimedia messaging, which will include text, audio, and video to the device.

MMS: Multimedia messaging, which will include text, audio, and video to the device.

![]() Push Notifications: Specific to particular apps on a device, alerting the user to information, including marketing, distributed by the creator of the app.

Push Notifications: Specific to particular apps on a device, alerting the user to information, including marketing, distributed by the creator of the app.

![]() QR Codes: The digitized, square glyphs that appear in the corner of ads in other media or as ads themselves. A user scans the glyph with his or her device and is directed to the website or mobile app of the advertiser.

QR Codes: The digitized, square glyphs that appear in the corner of ads in other media or as ads themselves. A user scans the glyph with his or her device and is directed to the website or mobile app of the advertiser.

![]() Proximity System Messages: If a device has GSM capability, the user might also receive messages that allow a specific location—a shopping mall, for example—to track his movements through the mall, offering him information about promotions of the stores nearest to his present location.

Proximity System Messages: If a device has GSM capability, the user might also receive messages that allow a specific location—a shopping mall, for example—to track his movements through the mall, offering him information about promotions of the stores nearest to his present location.

As a consumer, you may be aware that there are certain “opt-out, opt-in” protocols for mobile marketing. As a marketing professional, you will want to consider how your particular target market might or might not have interest in being on the receiving end of your message. Older consumers tend to relish privacy more than younger consumers, who seem to enjoy being aware of/sold on the latest trend.

Mobile Advertising

Mobile advertising is a hot topic. Proponents claim that the data now available through the give and take of the digital universe allows marketing firms to directly target specific consumers at the minute of their decision, thereby delivering the message to exactly the right person at exactly the right time. Others say that more traditional forms of advertising—which, in this case may include banner ads on websites—based on publications that focus on specific target audiences will still afford a better response. The practice is simply too new to fully vet.

The cost and frequency of mobile advertising is determined through complex algorithms; the “buy” occurs in real-time auctions that happen constantly.

Mobile advertising is facilitated though mobile advertising agencies who generally target specific networks, based on the clients’ desired strategy. These networks differ by reach. The following description of the various networks is based on the work of dotMobi, a U.K. firm specializing in mobile marketing.13

13 http://mobithinking.com/mobile-ad-network-guide.

![]() Blind Networks: The largest in terms of publishers, advertisers, and impressions. Serves a high volume of advertising to an extensive base of mostly independent mobile sites/apps, supplemented by premium publishers’ unfilled inventory. Offer many options for targeting but might not allow advertisers to choose specific websites. Performance advertising is the norm, paid by cost per click (CPC). For marketers who want an active response to their ads: Clicking through a banner to the advertiser’s site, click to download/call, and so on. CPC varies with supply and demand, determined through a self-service auction system.

Blind Networks: The largest in terms of publishers, advertisers, and impressions. Serves a high volume of advertising to an extensive base of mostly independent mobile sites/apps, supplemented by premium publishers’ unfilled inventory. Offer many options for targeting but might not allow advertisers to choose specific websites. Performance advertising is the norm, paid by cost per click (CPC). For marketers who want an active response to their ads: Clicking through a banner to the advertiser’s site, click to download/call, and so on. CPC varies with supply and demand, determined through a self-service auction system.

![]() Premium Blind Networks: Medium-sized, with a higher proportion of premium publishers (big-traffic mobile sites of well-known brands; newspapers, broadcasters or operator portals). Some exclusive relationships. Attracts a higher proportion of brand advertising, paid for on a CPM basis. Advertising may still be blind or semi-blind (that is, targeted at a channel), but a premium price might buy a specific spot on a specific site. Costs vary considerably—as high as U.S. $20 CPM.

Premium Blind Networks: Medium-sized, with a higher proportion of premium publishers (big-traffic mobile sites of well-known brands; newspapers, broadcasters or operator portals). Some exclusive relationships. Attracts a higher proportion of brand advertising, paid for on a CPM basis. Advertising may still be blind or semi-blind (that is, targeted at a channel), but a premium price might buy a specific spot on a specific site. Costs vary considerably—as high as U.S. $20 CPM.

![]() Premium Networks: Limited number of prestige publishers—mobile operators and big-name destinations—serving as an extension of direct-sales teams. Example: Nokia and AOL’s mobile inventory is sold on their own sites. Predominant pricing model is CPM; majority of campaigns are brand advertising. Attracts big brand advertisers who are willing to pay premium prices for prime locations. CPM will vary wildly from U.S. $5 to $75.

Premium Networks: Limited number of prestige publishers—mobile operators and big-name destinations—serving as an extension of direct-sales teams. Example: Nokia and AOL’s mobile inventory is sold on their own sites. Predominant pricing model is CPM; majority of campaigns are brand advertising. Attracts big brand advertisers who are willing to pay premium prices for prime locations. CPM will vary wildly from U.S. $5 to $75.

![]() Local Mobile Ad Networks: Focus on publishers where users are looking for local information (that is, restaurants, stores, or weather). Publishers include directory services, mapping/navigation, and other sites/apps where users enter their locations. More targeted, will cost more, but (might) deliver better results than normal mobile ads.

Local Mobile Ad Networks: Focus on publishers where users are looking for local information (that is, restaurants, stores, or weather). Publishers include directory services, mapping/navigation, and other sites/apps where users enter their locations. More targeted, will cost more, but (might) deliver better results than normal mobile ads.

![]() Cost-Per-Action (CPA)/Affiliate Networks: Advertisers define the type of action they wish to achieve and specify the price they are willing to pay for each customer that fulfills this action, paying only when conversion is achieved. Defined actions could include subscriptions or registrations; downloads/installs/purchases; clicks to call; checks directions; uses coupon. Advertisers can specify the type of mobile sites/apps where ads will run (or cannot run) but not necessarily particular publishers. Campaigns can also target by geography, operator, handset, and demographic. Publishers select the advertiser campaigns they wish to run and decide where and when the ads will run. Publishers are only paid if users click through and perform the defined action.

Cost-Per-Action (CPA)/Affiliate Networks: Advertisers define the type of action they wish to achieve and specify the price they are willing to pay for each customer that fulfills this action, paying only when conversion is achieved. Defined actions could include subscriptions or registrations; downloads/installs/purchases; clicks to call; checks directions; uses coupon. Advertisers can specify the type of mobile sites/apps where ads will run (or cannot run) but not necessarily particular publishers. Campaigns can also target by geography, operator, handset, and demographic. Publishers select the advertiser campaigns they wish to run and decide where and when the ads will run. Publishers are only paid if users click through and perform the defined action.

Summary: Games, Mobile Applications, and Mobile Marketing

The ongoing convergence of devices, access, and content continues to drive entertainment forward, especially in the gaming platform. Revenue for the platform now exceeds that of movie box offices (but not extended movie revenue, a merchandising/licensing juggernaut all its own) and music. Gaming will continue to grow because it hits basic human triggers, including a desire for status, rewards, and interaction. Marketers can make use of gaming principles in all sectors, driving efforts across all device platforms. Hand-in-hand with the increase in mobile devices, mobile marketing and advertising offer an intriguing way to potentially reach consumers right at the moment of their buying decisions.

For Further Reading

Hasen, Jeff, Mobilized Marketing: How to Drive Sales, Engagement, and Loyalty Through Mobile Devices, John Wiley & Sons, Inc., 2012.

Krum, Cindy, Mobile Marketing: Finding Your Customers No Matter Where They Are, Pearson Education Inc., 2010.

McGonigal, Jane, Reality Is Broken: Why Games Make Us Better and How They Can Change the World, Penguin Press, 2011.

Zichermann, Gabe, and Christopher Cunningham, Gamification by Design: Implementing Game Mechanics in Web and Mobile Apps, O’Reilly Media, Inc., 2011.