Peter T. Chingos CPA

Mercer Human Resources Consulting

Walton T. Conn Jr., CPA

KPMG Peat Marwick LLP

John R. Deming CPA

KPMG Peat Marwick LLP

The nature and types of stock-based compensation plans and awards have constantly changed over the years. However, the two most significant problems in determining the appropriate accounting for such awards have remained the same:

Measurement of compensation cost (i.e., the determination of total compensation cost to be allocated to expense for financial reporting purposes)

Allocation of compensation cost (i.e., the determination of the period(s) over which total compensation cost should be allocated to expense and the method of allocation)

To be sure, employees are compensated by being awarded stock options when they contribute services. However, their employers do not incur any cost in compensating them that way, any more than they do in issuing previously unissued shares of their stock when they receive money from new stockholders. The preexisting stockholders are the ones who incur a cost when employees are awarded stock options, first a cost of contingent dilution of their ownership interest and later a cost of actual dilution of their ownership interest. A reporting entity should report the costs it incurs, not costs other entities incur. Ironically, after centering its consideration of reporting in connection with the awarding of employee stock options on the concept of compensation cost, the Financial Accounting Standards Board (FASB) implicitly agreed that the employers incur no cost when compensating the employees when awarding the options, though they do incur a cost in using up the services provided by the employees for which they are awarded options: ". . . issuances of equity instruments result in the receipt of . . . services, which give rise to expenses as they are used in an entity's operations."[33] Compensation cost is therefore a misnomer, and attempting to determine the amount and timing of such a nonexistent cost diverts attention away from determining the amount and timing of the cost of using up the services received from the employees. The American Institute of Certified Public Accountants (AICPA) Accounting Standards Division made that point to the FASB when the FASB was considering the issue. The FASB explicitly ignored that advice when it issued its Invitation to Comment: It stated that AcSEC's analysis is ". . . beyond the scope of this project."[34]

The authoritative accounting literature addresses the accounting for stock-based compensation in two pronouncements which are as follows:

APB Opinion No. 25, "Accounting for Stock Issued to Employees" (AICPA, 1972). Also see Interpretation of APB Opinion No. 25, "Accounting for Stock Issued to Employees" (AICPA, 1973).

Statement of Financial Accounting Standard No. 123, "Accounting for Stock-Based Compensation" (FASB, 1995).

The APB Opinion No. 25 is applicable "to all stock option, purchase, award, and bonus rights granted by an employer corporation to an individual employee . . . . "The Opinion contains substantial guidance in the application of its provisions to such plans.

Subsequent to the issuance of APB Opinion No. 25, the trend toward the adoption by enterprises of more complex plans and awards continued. Of particular significance was the increase in the number of combination plans—plans that provide for the granting of two or more types of awards to individual employees. In many combination plans, the employee, or the enterprise, must make an election from alternative awards as to the award to be exercised, thereby canceling the other awards granted under the plan.

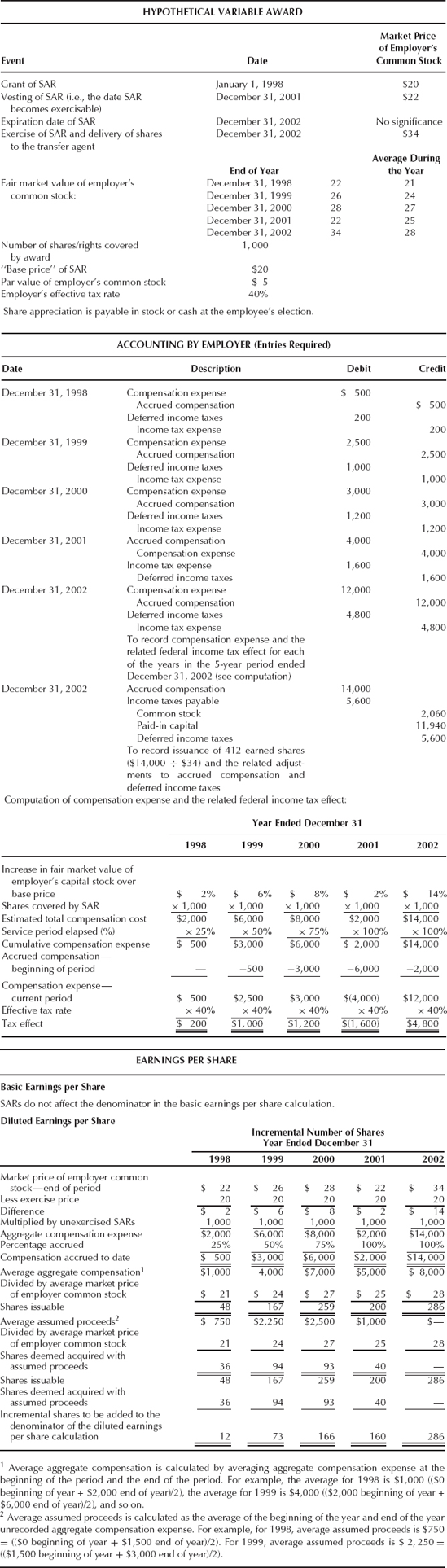

Following the issuance of APB Opinion No. 25, there was also a significant increase in the number of plans that provided for the granting of variable awards to employees. A variable award is one that at the date the grant is awarded, either (1) the number of shares of stock (or the amount of cash) an employee is entitled to receive, (2) the amount an employee is required to pay to exercise his rights with respect to the award, or (3) both the number of shares an employee is entitled to receive and the amount an employee is required to pay, are unknown. One of the most popular variable awards is the stock appreciation right (SAR). The SARs are rights granted that entitle an employee to receive, at a specified future date(s), the excess of the market value of a specified number of shares of the granting employer's capital stock over a stated price. The form of payment for amounts earned under an award of SARs may be specified by the award (i.e., stock, cash, or a combination thereof), or the award may permit the employee or employer to elect the form of payment.

Notwithstanding the guidance provided in APB Opinion No. 25, considerable disagreement continued to exist as to the appropriate method of accounting for variable awards. As a result, significant differences arose in the methods used by employers to account for variable awards, which led to numerous requests of the FASB for clarification. In December 1978, the FASB provided this clarification through the issuance of FASB Interpretation No. 28, "Accounting for Stock Appreciation Rights and Other Variable Stock Option or Award Plans," an interpretation of APB Opinion No. 25. In paragraph No. 2 of the Interpretation, the FASB specifies that:

APB Opinion No. 25 applies to plans for which the employer's stock is issued as compensation or the amount of cash paid as compensation is determined by reference to the market price of the stock or to changes in its market price. Plans involving SARs and other variable plan awards are included in those plans dealt with by [APB] Opinion No. 25.

The Interpretation provides specific guidance in the application of APB Opinion No. 25 to variable awards, particularly in those more troublesome areas where the greatest divergence in accounting existed prior to its issuance.

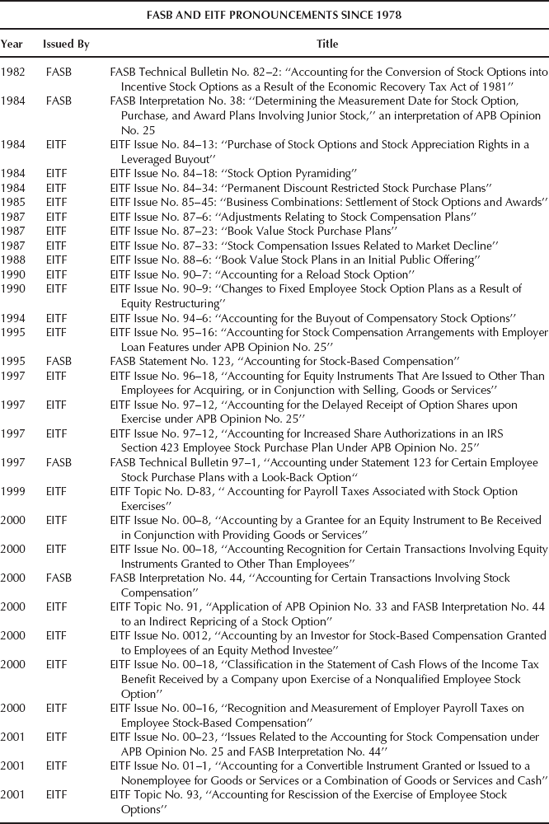

However, APB Opinion No. 25, as interpreted, failed to incorporate criteria that can be consistently applied to all types of plans. As a result, as new types of plans have evolved and changes in the tax laws have occurred, new interpretations and guidance have been required, resulting in a steady stream of pronouncements by the FASB and the Emerging Issues Task Force (EITF) since 1978, as shown in Exhibit 39.1.

The nature and the frequency of these additional pronouncements underscore the difficulties in applying the primary pronouncements to the myriad of stock-based compensation awards that have arisen since their issuance.

To address this problem, the FASB undertook a major project in 1984 to reconsider the accounting for stock-based compensation, whether issued to employees or issued to vendors, suppliers, or other nonemployees. In October 1995, the FASB issued FASB Statement No. 123, "Accounting for Stock-Based Compensation." FASB Statement No. 123 allows companies to retain the current approach set forth in APB Opinion No. 25, as amended, interpreted, and clarified; however, companies are encouraged to adopt a new accounting method based on the estimated fair value of employee stock options. Companies that do not follow the fair value method are required to provide expanded disclosures in the footnotes. Thus, the FASB settled on a compromise solution to a complex issue that had become extremely politicized. The vast majority of entities have not elected the fair value method of accounting for stock options. Therefore, the financial statements of most companies include two presentations of a company's results of operations rather than the normal presentation of a single net income.

FASB Statement No. 123 was preceded by an exposure draft issued by the FASB that would have required a new accounting method that results in reporting expense in connection with virtually all stock options issued to employees. However, those who receive stock options believe a requirement to change to the new method could threaten their stock options: The Wall Street Journal reported that "FASB's chairman . . . Dennis Beresford . . . says he scoffed at the doomsday arguments during a heated discussion aboard one corporate jet. The executives he was debating invited him to exit the craft—at 20,000 feet."[35] And Beresford himself reported that ". . . the CEO of one of United States' most successful companies . . . said that if the FASB was allowed to finalize the draft as proposed 'it would end capitalism' "[36]

To prevent this "disaster," the U.S. Congress prepared a bill entitled the Accounting Standards Reform Act, which, if enacted, would have required the Securities and Exchange Commission (SEC) to pass on all new standards approved by the FASB. The bill stated, in part: ". . . any new accounting standard or principle, and any modification . . . shall become effective only following an affirmative vote of a majority of a quorum of the member of the [Securities and Exchange] Commission." The bill was proposed simply to pressure the SEC to prevent the FASB from making this particular exposure draft final.

When the FASB was considering accounting for stock-based compensation leading to the issuance of FASB Statement No. 123, it did not address practice issues related to Opinion No. 25, because the Board had planned to supersede Opinion No. 25. Because FASB Statement No. 123 did not supersede Opinion No. 25, the FASB issued its Interpretation No. 44 to address issues on the application of Opinion No. 25 in a number of circumstances. Interpretation No. 44 was developed within the framework of Opinion No. 25 and does not refer to the concepts in FASB Statement No. 123.

Interpretation No. 44 became effective July 1, 2000. Except as noted next, it was to be applied prospectively to new awards, exchanges of awards in business combinations, modifications to outstanding awards, and changes in grantee status that occurred on or after that date.

The guidance about modifications to fixed stock option awards that directly or indirectly reduce the exercise price of an award apply to modifications made after December 15, 1998. The guidance about the definition of an employee applies to new awards granted after December 15, 1998. The guidance about modifications to fixed stock option awards to add a reload feature applies to modifications made after January 12, 2000. To the extent that events covered by the Interpretation discussed in this paragraph occur after the applicable date but before July 1, 2000, the effects of applying the Interpretation are to be recognized only prospectively. Accordingly, no adjustments are to be made on initial application of the Interpretation to financial statements for periods before July 1, 2000. Additional compensation cost measured on initial application of the Interpretation attributable to periods before July 1, 2000, is not recognized.

The initial application of the guidance for awards to an entity's nonemployee board of directors, if previously accounted for as awards to nonemployees and now required by the Interpretation to be accounted for under Opinion No. 25, is to be reported as a cumulative effect of a change in accounting principle.

Since companies continue to use the intrinsic value approach prescribed by APB Opinion No. 25, the authors have separated the chapter into two distinct parts. The first part will cover the application of APB Opinion No. 25 and its related interpretations and EITF issues. The remainder of the chapter will address the application of FASB Statement No. 123.

FASB Interpretation No. 44 addresses questions that have been raised as to whether Opinion No. 25 applies to accounting by the grantor of stock compensation to independent contractors or other service providers not employees of the grantor. It states that Opinion No. 25 applies to grantor employers for only stock compensation to those who meet the definition of employee under Opinion No. 25 as amplified by Interpretation No. 44.

For purposes of applying Opinion No. 25, a person is an employee if the grantor consistently represents the person to be an employee under common law, as illustrated in case law and under U.S. Internal Revenue Service Revenue Ruling 87–14. For such a person to be a common law employee, the grantor must represent the person as an employee for payroll tax purposes. However, simply representing a person as an employee for payroll tax purposes is insufficient to indicate that the person is an employee for purposes of Opinion No. 25.

An exception to the guidance in the preceding paragraph involves a grantor of stock compensation to a person who provides services to the grantor under a lease or co-employment agreement between the grantor and another entity under which the grantor is not the employer of record for payroll tax purposes. Such a person is deemed to be an employee of the grantor under Opinion No. 25 if all of the following criteria are met:

The person is a common law employee of the grantor, and the other entity is contractually required to pay payroll taxes on the compensation paid to the person for services provided to the grantor.

The grantor and the other entity agree in writing to all of the following:

The grantor has the exclusive right to grant stock compensation to the person for the person's services to the grantor.

The grantor has a right to hire, fire, and control the activities of the person. (The other entity may have the same right.)

The grantor has the exclusive right to determine the economic value of the services performed by the person (including wages and the number of units and value of stock compensation granted).

The person can participate in the grantor's employee benefit plans, if any, on the same basis as comparable employees of the grantor.

The grantor agrees to and does remit funds to the other entity sufficient to cover the complete compensation of the person, including all payroll taxes, on or before a contractually agreed date or dates.

A nonemployee member of a grantor's board of directors ordinarily does not meet that definition of an employee. However, application of Opinion No. 25 is required to stock compensation granted to such a person for services provided as a director if the person (a) was elected by the grantor's shareholders or (b) was appointed to a board position to be filled by shareholder election when the existing term expires. Employee status is not involved for awards granted to people for advisory or consulting services in a nonelected capacity or to nonemployee directors for services outside their role as directors, such as legal or investment banking advice or for loan guarantees.

Except as indicated in the preceding paragraph, Opinion No. 25 does not apply to the accounting by a grantor for stock compensation granted to nonemployees. For example, it does not apply to the accounting by a corporate investor of an unconsolidated investee for stock options or awards granted by the investor to employees of the investee accounted for under the equity method.

Whether a person is an employee under Opinion No. 25 is evaluated for consolidated financial statements at the consolidated group level. Stock compensation based on the stock of any consolidated group member is accounted for under Opinion No. 25 if the person meets the definition of an employee for any entity in the consolidated group. For example, Opinion No. 25 applies to the accounting in the consolidated financial statements for awards based on parent stock granted to employees of a consolidated subsidiary, to awards in stock of a consolidated subsidiary granted to employees of the parent, and to awards based on a consolidated subsidiary's stock granted to the employees of another consolidated subsidiary.

Opinion No. 25 does not apply to accounting by an employer for stock compensation granted to its employees (a) by another entity, such as an investee, based on that entity's stock or (b) by the employer based on the stock of another entity. Though that would seem to apply to awards based on the stock of a subsidiary for purposes of reporting in the separate financial statements of the subsidiary, Opinion No. 25 does apply in such circumstances if the subsidiary is part of the consolidated group including the parent company for purposes of preparing its consolidated financial statements.

With a change in status of a grantee to or from that of an employee of the grantor while an outstanding stock option or award is retained by the grantee with no modification of any of its terms, compensation cost under Opinion No. 25 is measured as if the award were newly granted at the date of the change in status. Only the portion of the newly measured cost attributable to the remaining vesting (service) period is recognized as compensation cost prospectively from the date of the change in status. Further, no adjustment is made to compensation cost recognized by the grantor before the change in status unless the award is forfeited unvested because the grantee does not fulfill an obligation. A modification made to a vested award's terms as a result of a change in status has no effect. If the grantee terminates employment before vesting, the cumulative estimate of compensation cost recorded in previous periods is reduced to zero by decreasing compensation cost in the period of forfeiture.

If there is a change in status of a grantee to or from that of an employee of the grantor while an outstanding stock option or award is retained by the grantee with a modification to the award at the time the status is changed, the modified award is treated under Opinion No. 25 as a new award appropriate to the new status of the grantee. Compensation cost thus measured is recognized in full over the remaining vesting (service) period, if any. Compensation cost previously recognized for the forfeited award, if any, is adjusted to zero in the period of forfeiture. A modification is deemed made if its terms would have required it to be forfeited on the change in status and the terms are then modified to continue the award. The modification in effect reinstates or extends the life of the award as a new award to the grantee immediately after the change in status. Similarly, a modification and an effective reinstatement of an award is made if the terms of the award (or underlying plan) provide for the award to continue at the discretion of the grantor and the grantee retains the award after the change in status.

As an exception, a change in grantee status from an employee to a nonemployee as a direct result of a spin-off does not change the grantor's accounting under Opinion No. 25. This applies to only awards granted and outstanding, including adjustments to those awards, at the date of the spin-off. This exception does not apply to other kinds of transactions, such as sale by a parent company of a large enough percentage of the shares of a subsidiary requiring the parent company to deconsolidate the subsidiary.

The APB Opinion No. 25 provides that a plan must have the following four characteristics in order to be considered as noncompensatory:

Substantially all full-time employees meeting limited employment qualifications may participate (employees owning a specified percentage of the outstanding stock and executives may be excluded).

Stock is offered to eligible employees equally on the basis of a uniform percentage of salary or wages (the plan may limit the number of shares of stock that an employee may purchase through the plan).

The time permitted for exercise of an option or purchase right is limited to a reasonable period.

The discount from the market price of the stock is no greater than would be reasonable in an offer of stock to stockholders or others.

Because Opinion No. 25 refers to a plan that qualifies under Section 423 of the U.S. Internal Revenue Code as a noncompensatory plan, which permits discounts of up to 15 percent, such a plan has the characteristic required under item 4. Further, for a stock option with an exercise price fixed at the date of grant, a discount of the exercise price of no more than 15 percent from the stock price on that date is reasonable for application of item 4.

Section 423 of the U.S. Internal Revenue Code permits a qualified employee stock purchase plan to contain a look-back option. A look-back option, for example, is a provision in an employee stock purchase plan that establishes the purchase price as the lesser of the stock's market price at the grant date or its market price at the exercise (purchase) date. Because Opinion No. 25 states that a plan that qualifies under Section 423 is noncompensatory, a plan with a look-back option qualifies as noncompensatory under Opinion No. 25.

A compensatory plan is any plan that does not have all four characteristics of a noncompensatory plan. It should be recognized, however, that awards granted under compensatory plans do not necessarily result in recognition of compensation expense by the employer. An employer recognizes compensation expense with respect to awards granted pursuant to a compensatory plan only if the application of the measurement principle results in the determination of compensation cost.

Paragraph 10 of APB Opinion No. 25 sets forth the following "measurement principle" for the measurement of compensation cost related to stock option, purchase, and award plans:

Measurement Principle—Compensation for services that a corporation receives as consideration for stock issued through employee stock option, purchase, and award plans should be measured by the quoted market price of the stock at the measurement date less the amount, if any, that the employee is required to pay . . . . If a quoted market price is unavailable, the best estimate of the market value of the stock should be used to measure compensation . . . . The measurement date for determining compensation cost in stock option, purchase, and award plans is the first date on which are known both (1) the number of shares that an individual employee is entitled to receive, and (2) the option or purchase price, if any.

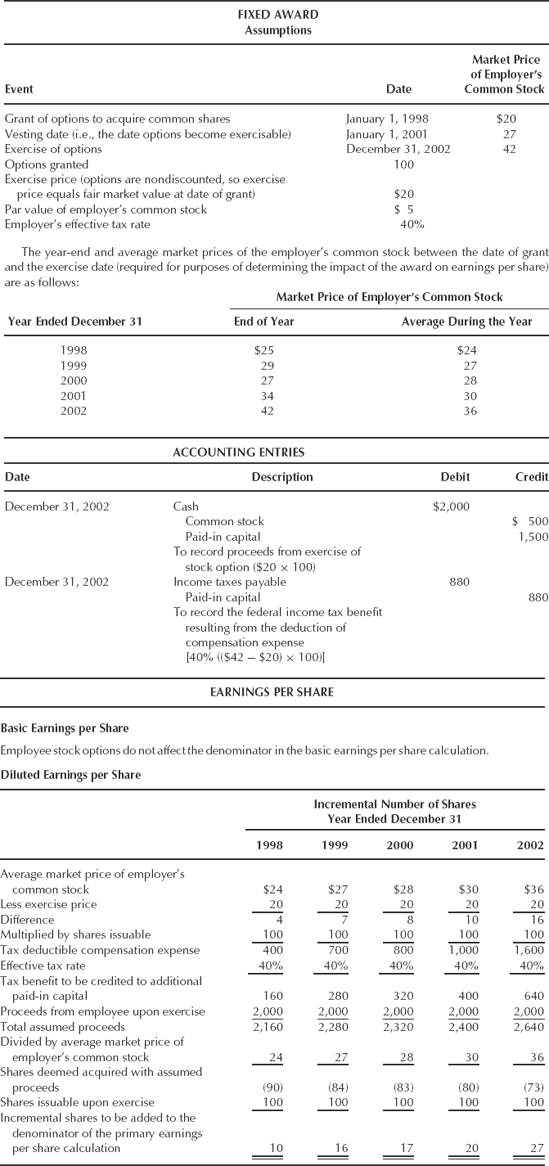

When both of the factors specified in paragraph 10 of APB Opinion No. 25 are known at the grant or award date (i.e., a fixed award), total compensation cost for an award is measured at the grant date. However, when either or both of these factors are not known at the grant or award date (i.e., a variable award), an employer should estimate total compensation cost each period from the date of grant or award to the measurement date based on the quoted market price of the employer's capital stock at the end of each period. This latter point is clarified in FASB Interpretation No. 28, which defines the compensation related to variable plan awards as:

The amount by which the quoted market value of the shares of the employer's stock covered by the grant exceeds the option price or value specified, by reference to a market price or otherwise, subject to any appreciation limitations under the plan. Changes, either increases or decreases, in the quoted market value of those shares between the date of grant and the measurement date [as defined in APB Opinion No. 25] result in a change in the measure of compensation for the right or award.

A proper understanding of the measurement principle of APB Opinion No. 25 (including the clarification set forth in FASB Interpretation No. 28) is essential to determining the appropriate accounting, including the amount of compensation expense to be recognized. Paragraphs 11(a) through 11(h) of APB Opinion No. 25, as well as subsequent FASB and EITF pronouncements, contain guidance on the application of the measurement principle, as discussed in the following paragraphs.

Paragraph 11(a) states:

Measuring compensation by the cost to an employer corporation of reacquired (treasury) stock that is distributed through a stock option, purchase, or award plan is not acceptable practice. The only exception is that compensation cost under a plan with all the provisions described in paragraph 11(c) may be measured by the cost of stock that the corporation (1) reacquires during the fiscal period for which the stock is to be awarded and (2) awards shortly thereafter to employees for services during that period.

Thus compensation cost of an award of stock for current services may be measured by the cost of reacquired treasury stock only if the above conditions and those specified in paragraph 11(c) (see below) of the Opinion are met. Otherwise, compensation cost should be measured as of the measurement date otherwise determined in accordance with the criterion set forth in paragraph 10 of the Opinion.

Paragraph 11(b) states:

The measurement date is not changed from the grant or award date to a later date solely by provisions that termination of employment reduces the number of shares of stock that may be issued to an employee.

This paragraph makes it clear that a requirement that an employee remain employed by the granting enterprise for a specified period of time in order for his rights to become vested under a stock-based compensation award does not preclude a determination, as of the grant or award date, of the total compensation cost to be recognized as an expense by the granting employer.

Paragraph 11(c) states:

The measurement date of an award of stock for current service may be the end of the fiscal period, which is normally the effective date of the award, instead of the date that the award to an employee is determined if (1) the award is provided for by the terms of an established formal plan, (2) the plan designates the factors that determine the total dollar amount of awards to employees for the period (for example, a percent of income), although the total amount or the individual awards may not be known at the end of the period, and (3) the award pertains to current service of the employee for the period.

The effect of this paragraph is to allow the designation of the end of a fiscal period as the measurement date when all of the conditions specified in paragraph 11(c) are met, even though the actual awards to individual employees may not be determined until after the close of the fiscal period.

Paragraph 11(d) states:

Renewing a stock option or purchase right or extending its period establishes a new measurement date as if the right were newly granted.

This paragraph reflects a very important concept. Its application could result in measurement of compensation cost with respect to outstanding stock option or purchase rights upon their renewal or extension, even though no compensation cost was ascribable to the original award under the measurement principle of APB Opinion No. 25. For example, any excess of the quoted market price of an employer's capital stock over the exercise price of a stock option at the date of renewal or extension is compensation cost; this may require recognition of compensation cost in addition to any compensation cost associated with the original award.

Paragraph 11(d) addresses "renewals" and "extensions" of stock purchase rights. There are modifications other than renewals and extensions that could also have an impact on the accounting for previously granted awards.

The EITF Issue No. 87–33, "Stock Compensation Issues Related to Market Decline," addresses a series of issues related to modifications to stock option and award plans as a result of market decline. The EITF's consensus on these issues generally precludes reversals of previously recognized compensation expense when outstanding awards are modified because of market value declines and, in many instances, require measurement and recognition of compensation cost for both the original and the modified award.

FASB Interpretation No. 44 addresses several issues related to modifications to stock option and award plans that change the life of the award through an extension of the exercise period or a renewal, decreases the exercise or purchase price of the award, or increases the number of shares the grantee is entitled to receive, including the addition of a reload feature.

A modification that renews a fixed award or extends the award's period (life), including a modification contingent on a future separation from employment, results in a new measurement of compensation cost the same as a newly granted award. Any intrinsic value at the modification date in excess of the amount measured at the original measurement date is recognized as compensation cost over the remaining future service period if the award is unvested, or immediately if the award is vested, for any employee who could benefit from the modification.

A modification that increases the life of an option award on separation from employment, but not beyond the original maximum contractual life of the award, is an extension of the award at the date the separation occurs and the life of the award is extended. The intrinsic value of the award is measured at the date of the modification, and any intrinsic value in excess of the amount measured at the original measurement date is recognized as compensation cost if the separation occurs. If the award vests and is exercised before the separation, any incremental intrinsic value at the date of the modification is not recognized, because the life of the award has not been extended. Attribution of additional compensation cost may require estimates, and adjustment of the estimates may be necessary in later periods.

If the original terms of the award provide for vesting to be accelerated at the discretion of the grantor (or on some other discretionary basis), subsequent acceleration of vesting is a modification. In contrast, if vesting is accelerated based on the occurrence of a specific event or condition in accordance with the original terms of the award, for example, if the original terms of an award specify that vesting is accelerated on retirement, death, or disability, no modification has been made and no new measurement of compensation cost is required.

A fixed stock option award may be subject to a modification by having its exercise price reduced (commonly called repricing). The exercise price has been reduced if the fair value of the consideration required to be remitted by the grantee on exercise is less than or potentially less than the fair value of the consideration required of the grantee according to the original terms of the award. Such an award is accounted for as variable from the date of the modification to the date the award is exercised, forfeited, or expires unexercised.

An exercise price can be reduced indirectly. For example, the grantor can give the grantee a cash bonus arrangement that is paid only if and when the award is exercised. This is an example of a combined stock award and cash bonus arrangement, discussed below. Or the grantor can allow the grantee to exercise the award with a full-recourse note that does not bear the market interest rate. If the exercise price has been reduced indirectly, the guidance in the preceding paragraph applies.

A grantor can directly or indirectly modify an award by reducing the exercise price contingent on the occurrence of a specified future event or condition, for example, if a certain earnings target or stock price is achieved in the future. Such a modification causes the award to be variable for the remainder of its outstanding life regardless of whether the triggering event occurs or the contingency provisions expires without the contingency occurring. In contrast, the original terms of a stock option award may provide for a reduction to the award's exercise price if a specified future event or condition occurs. If so, variable accounting is applied from the date of grant. A measurement date would occur and variable accounting would stop when the contingency is resolved or the contingency provision expires.

A grantor can, in effect, cancel an option award, for example, by modifying its terms to reduce or eliminate the likelihood that the grantee will exercise the option, such as by increasing the exercise price or curtailing the remaining life of the award. Any such modification is a cancellation.

A grantor can indirectly reduce the exercise price of a fixed stock option award by canceling or effectively canceling it or settling it for cash or other consideration and granting a replacement award at a lower exercise price, either before or after the cancellation or effective cancellation. If a cancellation and an award are combined that way, the replacement award is given variable accounting until it is exercised, is forfeited, or expires unexercised.

An option award cancellation is combined with another option award with a lower exercise price and results in an indirect reduction to the exercise price of the combined award if the other award is granted to the grantee within one of the following periods:

The period before the date of the cancellation that is the shorter of six months or the period from the date of the grant of the canceled option

The period ending six months after the date of the cancellation

To identify the replacement award that becomes subject to variable accounting on the cancellation of an award, the grantor first looks back in the period before the cancellation described in (a) above. If the award was granted during that period with an exercise price below that of the canceled award, the award and the canceled award are combined. If canceled options remain that were not combined with a replacement award in the look-back period, the grantor then looks forward to the period described in (b) above. If an award is granted during that period at an exercise price below that of the canceled award, the award and the canceled award are combined. When looking backward and then forward, options granted at dates closest to the date of cancellation are first identified as the replacement award. If the replacement award is identified in the look-back period, variable accounting for the award begins at the cancellation date. Prior-period financial statements are not restated if the award was accounted for as a fixed award in those statements.

Nevertheless, an oral or written agreement or implied promise by the grantor to compensate the grantee for any increase in the market price of the stock after a cancellation but before grant of a replacement award requires variable accounting for the replacement award regardless of the amount of time between the cancellation and the replacement grant. Any agreement between the grantor and the grantee when an option award is granted to cancel at a future date another outstanding option award requires variable accounting for the newly granted award from the date of grant.

The preceding also applies to the cancellation of an option award that has been accounted for as variable because of a reduction to that award's exercise price through a prior modification. But any option award granted during the look-back and look-forward periods, regardless of the exercise price of the replacement award, is eligible to be the replacement award. Thus, any replacement or modified award that has been accounted for as a variable award retains that status.

A cancellation of a fixed stock option award and the grant of stock results in a new measurement of compensation cost for the stock grant. The exercise price has been effectively reduced to zero. Variable accounting does not therefore apply to the replacement award. Any excess of the number of shares underlying the canceled fixed stock option award over the number of shares of the replacement stock award is subject to the guidance in the immediately preceding paragraphs.

An equity restructuring is a nonreciprocal transaction between an entity and its shareholders, such as a stock dividend, spin-off, stock split, rights offering, or recapitalization through a special, large, nonrecurring dividend that causes the market value per share of the stock underlying the option award to decrease. Such a restructuring may adjust the exercise price, the number of shares, or both of outstanding stock options or awards. (Ordinary cash dividends or distributions are not equity restructurings for this purpose.) The grantor may reduce the exercise price, increase the numbers of shares under the award, or both, to offset the decrease in the per share price of the stock underlying the award. No accounting consequence results from such an equity restructuring if both of the following are met:

The aggregate intrinsic value of the award immediately after the change is not greater than the aggregate intrinsic award immediately before the change.

The ratio of the exercise price per share to the market value per share is not reduced.

If those criteria are not met, the modified award is accounted for under Opinion No. 25 as variable from the date of the modification to the date the award is exercised, is forfeited, or expires unexercised. If they are met but the terms of the original award have also been modified to either accelerate the vesting or extend the life of the award, a new measurement of compensation cost is made at the date of the modification as if the award were newly granted. Cash or other consideration provided to restore the economic position of the grantee as a result of an equity restructuring transaction is recognized as compensation cost. The guidance concerning restructuring is applied without regard to whether the provisions of the stock option or award provide for adjustments to the terms in the event of an equity restructuring.

A modification that increases the number of shares to be issued under a fixed stock option award requires the award to be accounted for as variable from the date of the modification to the date the award is exercised, is forfeited, or expires unexercised.

A grantor that modifies a fixed stock option award to add a reload feature, which provides for the grant of a new option award on the exercise of an existing award if specified conditions are met, applies variable accounting for the modified award from the date of the modification to the date the award is exercised, is forfeited, or expires unexercised. The methods used to determine the exercise price, the number of shares, and the life of the reload grant are irrelevant. Variable accounting is required for each additional grant that includes a reload feature under a reload feature that provides for multiple subsequent grants through further reloads.

Total compensation cost is measured as the sum of the following if a fixed stock option or award is canceled or modified and a new measurement of compensation cost or variable accounting is required as a result of the modification:

The intrinsic value of the award (if any) at the original measurement date

The intrinsic value of the modified (or variable) award that exceeds the lesser of the intrinsic value of the original award (1) at the original measurement date or (2) immediately before the modification

When a stock option or award is modified and a new measurement of compensation cost or variable accounting is required, the remaining unrecognized original intrinsic value, if any, plus any additional compensation cost measured under (b) above is recognized over the remaining vesting (service) period, if any. If the modified award is fully vested at the date of the modification, any additional compensation cost to be recognized is recognized immediately. Recognized compensation cost for an award forfeited because an employee does not fulfill an obligation is reduced to zero by decreasing compensation cost in the period of the forfeiture.

Additional compensation cost measured as of the modification date for modifications to accelerate vesting or to extend the life of an award on a specified future separation from employment (but not beyond the award's original maximum contractual life) for all awards for which the modification results in an effective term extension or an effective renewal. Attribution of additional compensation cost may require estimates and adjustments of the estimates in later periods.

Compensation cost is adjusted for increases or decreases in the intrinsic value of a modified award that requires variable accounting in subsequent periods until the award is exercised, is forfeited, or expires unexercised. Compensation cost is not, however, adjusted below the intrinsic value (if any) of the modified stock option or award at the original measurement date unless the award is forfeited because the employee does not fulfill an obligation.

If cash is paid to an employee to settle an outstanding stock option, to settle an earlier grant of a stock award within six months after vesting, or to repurchase shares within six months after exercise of an option or issuance, total compensation cost is measured as the sum of the following:

The intrinsic value of the stock option or award (if any) at the original measurement date

The amount of cash paid to the employee (reduced by any amount of cash paid by the employee to acquire the shares) that exceeds the lesser of the intrinsic value (if any) of the award (1) at the original measurement date or (2) immediately before the cash settlement

The following guidance differs on whether the entity is a public entity or a private entity for this purpose. For this purpose, a public entity is any entity (a) whose securities trade in a public market either on a stock exchange (domestic or foreign) or in an over-the-counter market, including securities quoted only locally or regionally, (b) that makes a filing with a regulatory agency in preparation for the sale of any class of equity securities in a public market, or (c) that is controlled by an entity that meets criterion (a) or (b). A subsidiary of a public entity or a public entity with thinly traded stock follows the accounting for the public entity. But an entity with publicly traded debt but no publicly traded equity securities follows the accounting for a nonpublic entity.

For public reporting entities other than for shares expected to be repurchased at fair value for required tax withholding, variable accounting is required for a stock option or award with a share repurchase feature if the shares are expected to be repurchased within six months after option exercise or issuance of the shares. For a repurchase feature that is a right held by the employee to sell the shares back to the entity, variable accounting is required for the award if the right can be exercised within six months of issuance of the shares. After an option is exercised, the employee bears the risks and rewards of ownership with respect to those shares (except that if the consideration for exercise is a nonrecourse note, the substance is the same as a stock option and the employee bears no risks or rewards of ownership in the shares received). A subsequent repurchase of the shares by the entity (except within six months after option exercise or share issuance) thus represents a separate transaction to acquire treasury stock that is accounted for apart from the original stock option or award.

If the grantor repurchases shares within six months of issuance or option exercise and the repurchase was not expected by the grantor before the date of the repurchase, the grantor follows the preceding guidance for cash settlement of an earlier award.

If a share repurchase feature gives the employee the right to sell the shares back to the grantor after option exercise or share issuance for a premium that is not fixed or determinable over the then-current stock price, that feature creates an arrangement that requires variable accounting, even if the share cannot be sold back to the entity within six months after option exercise or issuance. If such a feature gives the employee the right to sell shares back to the entity for a fixed dollar amount over the stock price but not within six months of issuance of the shares, the fixed premium is recognized as additional compensation cost over the vesting (service) period.

For nonpublic reporting entities, variable accounting is not required for a stock option or award with one of these share repurchase features:

The stated share repurchase price is equal to the fair value of the shares at the date of repurchase, the employee cannot require the entity to repurchase the shares within six months of option exercise or share issuance, and the shares are not expected to be repurchased within six months after exercise or share issuance.

The stated share repurchase price is not the fair value of the shares at the date of repurchase, but the employee has made a substantial investment and must bear risks and rewards normally associated with share ownership for at least six months.

Shares are repurchased for tax-withholding purposes at the grantor's minimum statutory withholding rates, including payroll taxes, applicable to supplemental taxable income.

A substantial investment has been made for purposes of an award that contains a repurchase feature at other than fair value when the employee invests in a form other than services rendered to the entity an amount equal to 100 percent of the stated share repurchase price calculated at the date of grant. If the award is an option, a substantial investment therefore cannot be made before exercise of the option. Because the award is variable, compensation cost is recognized for any intrinsic value of the option from the date of grant to the date a substantial investment has been made.

For purposes of paragraph 11(g) of Opinion No. 25 for both public and nonpublic entities, to determine the variable amount not required, required tax withholding is defined as the employer's minimum statutory withholding rates for federal and state tax purposes, including payroll taxes applicable to such supplemental taxable income. Withheld amounts in excess of that rate do not represent the employer's required tax withholding for this purpose.

If an election to repurchase shares on exercise in excess of the number necessary to satisfy the employer's required tax withholding is at the discretion of the employee, variable accounting is required from the date the award is granted to the date the award is exercised, is forfeited, or expires unexercised. If the terms of an award are silent on tax withholding, or if the repurchase of shares for tax withholding in excess of the number necessary to satisfy the employer's required tax withholding is at the discretion of the employer, variable accounting is not required. However, in either circumstance, if the employer exhibits a pattern of consistently approving repurchases of excess shares, variable accounting is required from the date of grant for all awards under the plan.

If shares are repurchased on exercise of a fixed option award in excess of the number necessary to satisfy the employer's required tax withholding, a new measurement of compensation cost is required for the entire award.

Changes to the exercise price or the number of share of a fixed stock option award as a result of an exchange of fixed stock option awards in a business combination accounted for by the pooling of interests method have no accounting consequence if both of the following are met at the date of exchange:

The aggregate intrinsic value of the options immediately after the exchange is no greater than the aggregate intrinsic value of the options immediately before the exchange.

The ratio of the exercise price per option to the market value per share is not reduced.

If those criteria are not met, a new measurement of compensation cost is required.

Vested stock options or awards issued by an acquirer in a business combination accounted for by the purchase method in exchange for outstanding awards held by employees of the acquiree are considered to be part of the purchase price paid by the acquirer for the acquiree and accounted for under FASB Statement No. 141. The fair value of the new (acquirer) awards are included as part of the purchase price.

Unvested stock options or awards granted by an acquirer in a business combination accounted for by the purchase method in exchange for stock options or awards held by employees of the acquiree are considered to be part of the purchase price for the acquiree, and the fair value of the new (acquirer) awards are included in the purchase price. However, to the extent that service is required after the consummation date of the acquisition in order to vest in the replacement awards, a portion of the intrinsic value (if any) of the unvested awards is allocated to unearned compensation and recognized as compensation cost over the remaining future vesting (service) period. The amount allocated is based on the portion of the intrinsic value at the consummation date related to the future vesting (service) period. The amount is calculated as the intrinsic value of the replacement awards at the consummation date multiplied by the fraction that is the remaining future vesting (service) period divided by the total vesting (service) period, which is the vesting period before the consummation date plus the remaining future period required to vest in the replacement award. Any intrinsic value of the replacement awards allocated to unearned compensation cost is deducted from the fair value of the awards for purposes of the allocation of the purchase price to the other assets acquired.

Awards granted under a plan subject to shareholder approval generally are not deemed granted until approval is obtained, and, therefore, no measurement date can occur before then. However, if management and the members of the board of directors control sufficient votes to approve the plan, a grant date and therefore a measurement date may be deemed to have occurred before shareholder approval, because approval then is merely a formality.

Deferred tax assets recognized for temporary differences related to stock options or awards under Opinion No. 25 should not be adjusted for subsequent declines in the stock price. Such assets are determined by the compensation expense recognized for financial reporting rather than by reference to the expected future tax deduction, which would be estimated using the current intrinsic value of the award. A valuation allowance to reduce the carrying amount of the assets is established only if the grantor expects future taxable income to be insufficient to recover the assets in the periods in which the deduction would otherwise be recognized for tax purposes.

A cash bonus and a stock option award are accounted for as a combined award if payment by the grantor or refund by the employee of the cash bonus is contingent on exercise of the option award. A cash bonus that is not fixed and that is contingent on exercise of an option award is accounted for as a variable award. A fixed cash bonus that is contingent on exercise of a fixed option award is accounted for as a combined fixed award with the cash bonus reducing the stated exercise price of the option award. A cash bonus, regardless of whether it is fixed or variable, that is contingent on vesting of a stock option or award is accounted for as compensation cost separate from the stock option or award.

Paragraph 11(e) states:

Transferring stock or assets to a trustee, agent, or other third party for distribution of stock to employees under the terms of an option, purchase, or award plan does not change the measurement date from a later date to the date of transfer unless the terms of the transfer provide that the stock (1) will not revert to the corporation, (2) will not be granted or awarded later to the same employee on terms different from or for services other than those specified in the original grant or award, and (3) will not be granted or awarded later to another employee.

This paragraph reinforces the principle that the measurement date is the first date on which are known both (1) the number of shares that an individual employee is entitled to receive and (2) the option or purchase price, if any. The authors are not aware of any awards that have been structured in a manner that has resulted in an acceleration of the otherwise determined measurement date as a result of the application of paragraph 11(e).

Paragraph 11(f) states:

The measurement date for a grant or award of convertible stock (or stock that is otherwise exchangeable for other securities of the corporation) is the date in which the ratio of conversion (or exchange) is known unless other terms are variable at that date (paragraph 10b). The higher of the quoted market price at the measurement date of (1) the convertible stock granted or awarded or (2) the securities into which the original grant or award is convertible should be used to measure compensation.

Awards to employees of convertible stock or rights to purchase convertible stock are not common. Nevertheless, this paragraph provides guidance in measuring the compensation cost of such awards. Further guidance can be found in FASB Interpretation No. 38, "Determining the Measurement Date for Stock Option, Purchase, and Award Plans Involving Junior Stock," an interpretation of APB Opinion No. 25.

Paragraph 11(g) states:

Cash paid to an employee to settle an earlier award of stock or to settle a grant of option to the employee should measure compensation cost. If the cash payment differs from the earlier measure of the award of stock or grant of option, compensation cost should be adjusted (par. 15). The amount that a corporation pays to an employee through a compensation plan is "cash paid to an employee to settle an earlier award of stock or to settle a grant of option" if stock is reacquired shortly after issuance. Cash proceeds that a corporation receives from sale of awarded stock or stock issued on exercise of an option and remits to the taxing authorities to cover required withholding of income taxes on an award is not "cash paid to an employee to settle an earlier award of stock or to settle a grant of option" in measuring compensation cost.

The intent of this paragraph seems quite clear. If an earlier award of stock or stock options is ultimately settled by cash payment to the employee, the amount actually paid is the final measure of compensation cost to be recognized by the employer, regardless of the amount of compensation cost previously determined. However, in practice, application of this paragraph has often proved difficult and, as a result, a number of EITF Issues have dealt with cash settlements of awards, as discussed in the following paragraph.

This pronouncement sets forth the EITF's consensus that the "target company" in a leveraged buyout should recognize compensation expense in the amount of cash paid by the target company to acquire outstanding stock options and SARs.

Similar to the consensus in EITF Issue No. 84–13, this consensus indicates that when a target company settles outstanding stock options or awards "voluntarily, at the direction of the acquiring company, or as part of the plan of acquisition, APB Opinion No. 25 requires that the settlement be accounted for as compensation expense in the separate financial statements of the target company."

This consensus addresses stock option plans that contain a cash bonus feature that provides for a reimbursement to employees of the taxes payable as a result of the exercise of a nonqualified stock option (a "tax-offset bonus"). The consensus indicates that awards under such plans are variable awards. Thus, the existence of a tax-offset bonus related to a stock option award requires that the entire award (the stock option plus the cash bonus feature) be accounted for as a variable award, as the option and the tax-offset bonus are viewed as a single variable award. This consensus is consistent with footnote 1 to FASB Interpretation No. 28, "Accounting for Stock Appreciation Rights and Other Variable Stock Option or Award Plans" which states, in part, "Plans under which an employee may receive cash in lieu of stock or additional cash upon the exercise of a stock option are variable plans for purposes of the Interpretation as the amount is contingent upon the occurrence of future events." The significant point here is that two different awards, one being a fixed award and the other a variable award, should be accounted for as a single, variable award.

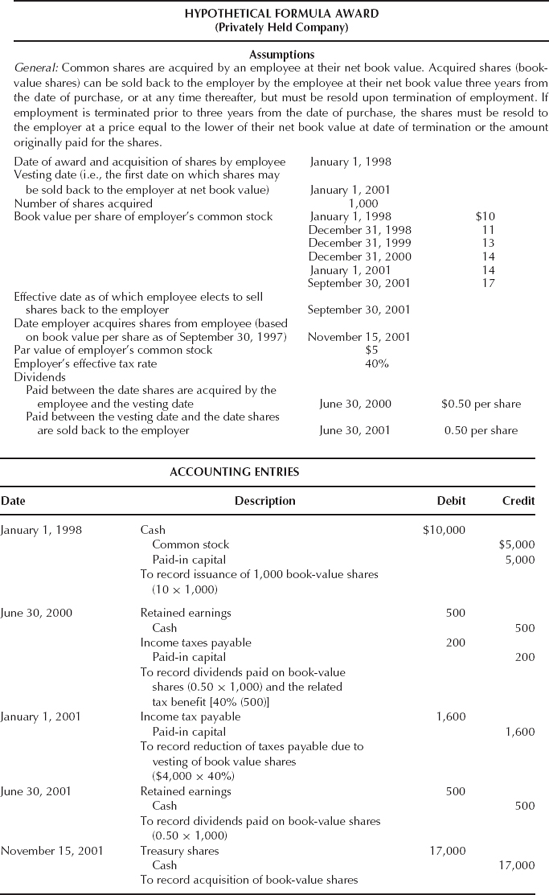

This consensus provides much-needed guidance in accounting for formula-based plans, under which employees purchase shares, or are granted options to acquire shares, of the employer's common stock at a formula price. The formula price is usually based on book value, a multiple of book value, or earnings. Additionally, the employee must sell the acquired shares back to the employer upon retirement or other termination of employment, at a selling price determined in the same manner as the original purchase price.

Privately held companies only:

No compensation expense should be recognized for changes in the formula price during the employment period "if the employee makes a substantive investment that will be at risk for a reasonable period of time." This consensus applies to plans where the employee is allowed to resell all or a portion of the acquired shares to the company at fixed or determinable dates, as well as plans where the shares are resold to the company only upon retirement or other termination of employment.

Privately held and publicly held companies:

If options are granted to employees to purchase shares at the formula price and the employees can resell the options, or the shares acquired upon exercise of the options, to the company upon retirement or other termination of employment, or at fixed or determinable dates, the consensus of the EITF is the same for both privately held and publicly held companies. The consensus indicates that compensation expense should be recognized for increases in the formula price from the grant date to the exercise date (i.e., the award should be accounted for as a variable award). The consensus further indicates that the expense previously recognized should not be reversed upon exercise of the option, and that "additional expense would be recognized if the shares are sold back to the company shortly after exercise, as required by paragraph 11(g) of APB Opinion No. 25."

The SEC observer at the EITF provided the following clarification of the SEC staff's views of book value plans for publicly held companies:

The SEC Observer indicated that the SEC staff views a book value plan for a publicly held company as a performance plan and noted that it should be accounted for like an SAR.

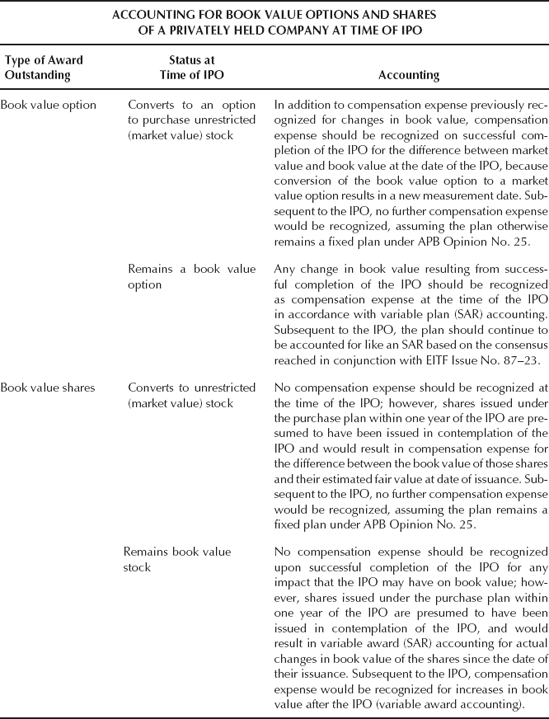

As previously noted, a difference exists between accounting for book value purchase (and other formula-based) awards by privately held and publicly held companies. This difference, of course, raised questions as to the accounting to be applied to these types of awards when a privately held company becomes publicly held. This issue was subsequently addressed in EITF Issue No. 88–6, "Book Value Stock Plans in an Initial Public Offering."

This consensus addresses a number of issues related to the October 1987 stock market decline, including "How to account for the repurchase of an outstanding option and the issuance of a 'new' option." The Task Force consensus on this issue was that "paragraph 11(g) of APB Opinion No. 25 does not apply if an existing option is repurchased in contemplation of the issuance of a new option that contains terms identical to the remaining terms of the original option except that the exercise price is reduced . . . ." The consensus also indicates that "the cash paid to repurchase the original option represents additional compensation that should be charged to expense in the current period."

The effect of this consensus is to preclude an employer from decreasing compensation cost associated with a stock option award, by "settling" the award through a cash payment that is less than the amount of compensation cost previously determined, and then granting a "new" option to the same employee that contains terms identical to the remaining terms of the original option except that the exercise price is reduced. In the event such an arrangement were entered into, application of the consensus would (1) require the employer to charge the amount of the cash payment to expense in the current period, (2) prohibit the reversal of previously recognized expense associated with the original option, and (3) require continued amortization of any compensation measured at the original measurement date that had not been amortized and, additionally, could result in the measurement of additional compensation expense associated with the "new" award.

The consensus also requires similar accounting when an option is "repriced," as opposed to the situation described above where an option is canceled and reissued.

As previously noted, EITF Issue No. 87–23 addresses certain issues related to the accounting for stock purchase awards to employees, where the purchase price is a formula price based on book value or earnings, and where the shares must ultimately be sold back to the company by the employee at a price determined in the same manner as the original purchase price. The consensus set forth in EITF Issue No. 87–23 makes certain distinctions between privately and publicly held companies with respect to the accounting for these types of awards.

In EITF Issue No. 88–6, the Task Force reached a consensus that a book value stock purchase plan of a publicly held company should be viewed as a performance plan and should be accounted for like an SAR (this is consistent with the SEC observer's comment noted under the discussion of EITF Issue No. 87–23 above). Thus, for a publicly held company, compensation expense should be recognized for increases in book value (or other formula price based on earnings) on awards outstanding under such a plan. For a privately held company, however, under the consensus reached in EITF Issue No. 87–23, no compensation expense would be recognized for such increases in the book value or other formula price, regardless of when the awards were granted.

The Task Force also reached consensuses in EITF Issue No. 88–6 related to the recognition and measurement of compensation expense by a privately held company for such awards in the event of a subsequent IPO (i.e., when a privately held company becomes a publicly held company). These consensuses are set forth in Exhibit 39.2.

EITF Issue No. 88–6 also contains certain guidance regarding pro forma disclosures for these types of plans in the event of an IPO, as well as an exhibit that contains "Examples of the Application of APB Opinion No. 25 and the EITF Consensus from Issue Nos. 87–23 and 88–6 in an IPO."

EITF Issue No. 87–33 addressed the settling of options and the issuance of new options. In this issue, the Task Force was asked to address the buyout, or settling, of options without an issuance of new options. In the consensus, the Task Force imposes a rebuttable presumption that options granted within six months of the buyout of the outstanding options would be considered replacement options. In such a case, the issuer would have to consider the implications of EITF Issue No. 87–33.

The Task Force reached a consensus that the total amount of compensation cost to be recognized is the sum of: (1) the compensation cost amortized to the buyout date; (2) the options' intrinsic value, if any, at the buyout date in excess of the compensation cost recognized as expense to the buyout date; and (3) the amount, if any, paid for the options in excess of their intrinsic value at the buyout date. In addition, any remaining unamortized compensation cost related to the original options would not be included in income for any period. Exhibit 94–6A of the EITF Issue No. 94–6 provides examples.

Paragraph 11(h) states:

Some plans are a combination of two or more types of plans. An employer corporation may need to measure compensation for the separate parts. Compensation cost for a combination plan permitting an employee to elect one part should be measured according to the terms that an employee is most likely to elect based on the facts available each period.

If more than one type of award is granted to an employee under a plan, the measurement principle must be applied to each award for purposes of measuring compensation cost to an employer. Furthermore, if a combination plan permits an employee to elect one award from a number of alternative awards, compensation cost should be measured in terms of the award the employee is considered most likely to elect in view of the facts available each period. In many combination plans involving alternative awards, an employer retains the right to approve or reject an employee's election under certain circumstances, giving the employer significant control over the determination of the award under which compensation cost will be measured.

FASB Interpretation No. 28 provides additional guidance with respect to combination plans. In that Interpretation, the FASB specifies that in combination plans involving both an SAR or other variable award and a fixed award (e.g., a stock option), compensation cost should normally be measured and allocated to expense under the presumption that the variable award will be elected by the employee. However, this presumption may be overcome if experience or other factors, such as ceilings on the appreciation available to the employee under the variable feature, provide evidence that the employee will elect to exercise the fixed award.

Stock option pyramiding is a stock option exercise approach that developed subsequent to the issuance of APB Opinion No. 25. This approach involves the payment by the employee of the option exercise price by transferring to the employer previously owned shares with a current fair value equal to the exercise price. In EITF Issue No. 84–18, "Stock Option Pyramiding," the Task Force reached a consensus that "some holding period" for the exchanged shares is necessary to "avoid the conclusion that the award of the option is, in substance, a variable plan (or a SAR), thereby requiring compensation charges." A majority of the Task Force members indicated that a six-month period would satisfy the holding period requirement.

In a subsequent consensus set forth in EITF Issue No. 87–6, "Adjustments Relating to Stock Compensation Plans," the Task Force addressed a "phantom" stock-for-stock exercise arrangement, under which an employee holds "mature" shares meeting the holding period requirement discussed in EITF Issue No. 84–18. In this consensus, the Task Force indicated that if the exercise is accomplished by the enterprise issuing a certificate for the "net" shares (i.e., the shares issuable upon exercise of the option less the number of shares required to be relinquished to pay the exercise price), as opposed to the enterprise accepting the mature shares in payment of the exercise price and then issuing a new certificate for the total number of shares covered by the exercised option, the plan remains a fixed plan.

Thus, even though the "net" number of shares to be issued under either of the arrangements described above is not known at the date of grant, the use of qualifying mature shares to pay the option exercise price does not, under these two consensuses, change a plan that otherwise qualifies as a fixed plan to a variable plan. As a result, the enterprise is not required to recognize compensation expense for appreciation in shares under option subsequent to the date of grant solely because the award allows for payment of the exercise price of an option by surrendering mature shares owned by the employee or through a phantom stock-for-stock exercise involving mature shares owned by the employee.

Compensation consultants have developed a transaction that they believe enables employees to defer the taxable income derived from the exercise of stock options (and that also delays the employer's tax deduction) by deferring the employees' receipt of the shares of the stock. The transaction, typically referred to as a stock option gain deferral transaction, is accomplished by a stock-for-stock exercise. An employee receives new shares equal to the value of the shares tendered, and the remaining shares under option are credited to the employee's deferred compensation account. The employee then receives the shares from the deferred compensation account at retirement or some other future date.

In EITF Issue No. 97–5, "Accounting for the Delayed Receipt of Option Shares upon Exercise under APB Opinion No. 25," the Task Force addressed whether certain characteristics of stock option gain deferral arrangements would cause a new measurement date (or variable plan accounting) for financial reporting purposes under APB Opinion No. 25. An FASB staff announcement resolved the issue prior to the EITF's reaching a consensus. The announcement provides that variable plan accounting would be required if the employee does not meet the necessary six-month holding period set forth in EITF Issue 84–18, "Stock Option Pyramiding," which is discussed above. In addition, the announcement provides that an award that permits diversification into alternative types of investments makes the award subject to variable accounting. Accordingly, if an employee uses "mature" shares in the stock-for-stock exercise and if an award does not permit diversification, the delayed delivery of shares generally would not create a new measurement date or variable plan accounting.

EITF Issue No. 87–6, "Adjustments Relating to Stock Compensation Plans," addresses an issue that is similar to the stock option pyramiding issue discussed under (ix) above. The Task Force reached a consensus that "an option that allows the use of option shares to meet tax withholding requirements may be considered a fixed plan if it meets all the other requirements of APB Opinion No. 25. No compensation needs to be recorded for the shares used to meet the tax withholding requirements. The Task Force noted that this treatment would be limited to the number of shares with a fair value equal to the dollar amount of only the required tax withholding." Therefore, even though the net number of shares to be issued would not be known at the date of grant under these circumstances (since the shares to be withheld to cover the required tax withholding will not be known until the exercise date), plans with tax withholding features may be accounted for as fixed plans as long as they meet the other requirements for a fixed plan under APB Opinion No. 25.

APB Opinion No. 25 requires that compensation cost related to "stock option, purchase, and award plans should be recognized as an expense of one or more periods in which an employee performs services . . . . The grant or award may specify the period or periods during which the employee performs services or the periods may be inferred from the terms or from the past pattern of grants or awards."

FASB Interpretation No. 28 also indicates that compensation cost with respect to variable awards should be allocated to expense over the period(s) in which the employee performs the related services. However, the FASB went a step further in this interpretation by specifying that the service period is presumed to be the vesting period. The vesting period is normally the period from the date of the grant of the rights or awards to the date(s) they become exercisable. These criteria for determining the service period are considerably more definitive than the guidance provided in APB Opinion No. 25 and, in the authors' view, should be used for determining the service period for awards made pursuant to all stock-based compensation awards (i.e., both fixed and variable awards).

Compensation cost related to fixed awards should normally be allocated to expense over the service period on a straight-line basis. On rare occasions, however, circumstances may arise that would justify allocation on another basis. In any event, the method used should be systematic, reasonable, and consistently applied.

Allocating compensation cost related to variable awards to expense is more complex, because the measurement date and, thus, the final determination of compensation cost, occur subsequent to the date of grant. Total compensation cost with respect to a variable award must be estimated from the date of grant to the measurement date, based on the quoted market price of the employer's stock at the end of each interim period. Compensation cost so determined should be allocated to expense in the following manner:

If a variable award is granted for current and/or future services, estimated total compensation cost determined at the end of each period prior to the expiration of the service period should be allocated to expense over the service period. Changes in the estimated total compensation cost attributable to increases or decreases in the quoted market price of the employer's capital stock subsequent to the expiration of the service period (but prior to the measurement date) should be charged or credited to expense each period as the changes occur.

If a variable award is granted for past services, estimated total compensation cost determined at the date of grant is charged to expense of the period in which the award is granted. Changes in the estimated total compensation cost attributable to increases or decreases in the quoted market price of the employer's capital stock subsequent to the date of grant (but prior to the measurement date) should be charged or credited to expense each period as the changes occur.

APB Opinion No. 25 states in paragraph 15: "If a stock option is not exercised (or awarded stock is returned to the corporation) because an employee fails to fulfill an obligation, the estimate of compensation expense recorded in previous periods should be adjusted by decreasing compensation expense in the period of forfeiture." Application of this paragraph to a situation where an award is canceled or forfeited because employment is terminated prior to vesting of the award is straightforward; the previously accrued compensation should be eliminated by decreasing compensation expense in the period of cancellation or forfeiture.

However, prior to the issuance of FASB Interpretation No. 28, the application of this paragraph to combination plans was unclear. In a combination plan that permits an employee to elect either a fixed award (e.g., a stock option) or a variable award (e.g., an SAR), FASB Interpretation No. 28 specifies that compensation cost should be accrued based on the presumption that the employee will elect the variable award, unless there is evidence to the contrary. In cases involving combination plans where the employer has accrued compensation based on the presumption that the employee will elect to exercise the variable award and, due to a change in circumstances, it becomes more likely that settlement will be based on the fixed award (e.g., when appreciation in the quoted market price of the employer's capital stock exceeds the maximum appreciation an employee is entitled to receive upon exercise of an SAR), FASB Interpretation No. 28 specifies that the compensation accrued with respect to the variable award should not be adjusted by decreasing compensation expense, but should be recognized as consideration for the stock issued upon settlement of the fixed award. However, FASB Interpretation No. 28 further specifies that, if both the fixed award and the variable award are forfeited or canceled, accrued compensation should be eliminated by decreasing compensation expense during the period of forfeiture or cancellation.

EITF Issue No. 87–33, "Stock Compensation Issues Related to Market Decline," provides further clarification of APB Opinion No. 25, paragraph 15. In this pronouncement, "Task Force members agreed that the reversal of previously measured compensation would be appropriate only if the forfeiture or cancellation of an option or award results from the employee's termination or nonperformance."

Compensation expense associated with stock-based compensation awards is often deductible by the employer for income tax purposes in a different period from when such expense is recognized for financial reporting purposes. Such differences are temporary differences and should be accounted for as specified in FASB Statement No. 109, "Accounting for Income Taxes."

In many instances, however, there is a permanent difference between the amount of compensation expense recognized for financial reporting purposes and compensation expense deductible for income tax purposes. These differences generally arise because an employer is normally entitled to an income tax deduction for such awards equal to the amount of compensation reportable as income by the employee, and this amount is often different from the amount of compensation expense recognized by an employer for financial reporting purposes. In addressing this situation, APB Opinion No. 25 specifies that the reduction in income tax expense recorded by an employer with respect to a stock option, purchase, or award plan should not exceed the proportion of the tax reduction related to the compensation expense recognized by the employer for financial reporting purposes. Any additional tax reduction should not be accounted for as a reduction of income tax expense but, rather, should be credited directly to paid-in capital in the period that the additional tax benefit is realized through a reduction of current income taxes payable.

Occasionally, the amount of compensation expense for financial reporting purposes exceeds the amount of compensation deductible for income tax purposes. In these situations, an employer may, in the period of the tax reduction, deduct from paid-in capital and credit to income tax expense or previously recognized deferred taxes the amount of the additional tax reduction that would have resulted had the compensation expense recognized for financial reporting purposes been deductible for income tax purposes. However, this reduction is limited to the amount of tax reductions attributable to awards made under the same or similar plans that have been previously credited to paid-in capital.