CHAPTER 17

USE CASES IN RETAIL

Over the past several years the retail sector has been bombarded with challenges. Brick-and-mortar stores have closed in record numbers and continue to do so. Indeed virtually every member of the entire industry is at high risk. They are vexed by several threats ranging from increased competition from online super-shopper sites such as Amazon to a plethora of more brand-specific problems, such as a lack of differentiators, pricing pressures, muddled marketing messaging, poor business processes, online pricing/brand comparison sites, customer reviews on their own websites, vulnerability to customer social messaging, and an overall disconnection with the buying public. Their former strategies in merchandising, merchandise selection, pricing models, customer service, and marketing are no longer working as effectively as they have in the past.

Consider these findings from an April 2014 report on apparel retailers by Stealing Share, a company that conducts brand research and provides corporate rebranding, marketing strategy, competitive analysis, brand positioning, brand training, and brand design for clients:

Despite what the retailers say, they are not. The major learning while Stealing Share strategists were looking at the retail market was how much it was full of blaring noise. Everything—from style to messaging to operations—ran together to form a ceaseless blob that consumers are increasingly tuning out.

The differences between retailers are as thin as blades of grass. It may be the most undifferentiated market we have ever seen. That is why the doomsday scenario is in play for many retail outlets.

Think about this. Only 10 years ago, The Gap was the 18th largest retailer in the nation. Last year, it was 33rd. The Sears Holding Company (which owns both Sears and Kmart) saw sales drop 9.2% in 2013. J.C. Penney’s dropped a whopping 24.7%.

We could go on and on. But the future is coming and changes must be made. Take heed. If you don’t, you will lose.

OLD TACTICS IN A BIG DATA RE-RUN

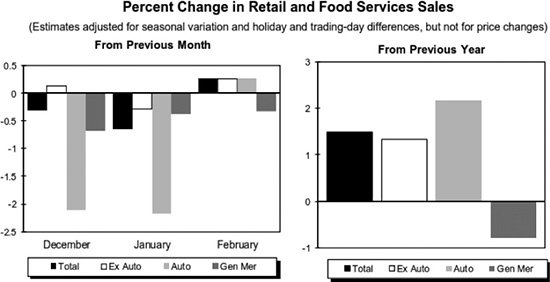

The state of the retail market can be clearly conceptualized by looking at Figure 17.1, which is a snapshot of month-to-month and year-to-year estimates for the industry from the U.S. Census Bureau’s “Advance Monthly Sales for Retail and Food Services” report that was released on March 13, 2014. As you can see, this sector undeniably isn’t doing well as of this writing.

Figure 17.1 Month-to-month and year-to-year estimates for the industry from the U.S. Census Bureau’s “Advance Monthly Sales for Retail and Food Services” report, released on March 13, 2014.

Source: U.S. Census Bureau News Release at http://www.census.gov/retail/marts/www/marts_current.pdf.

Retailers are aware of this, of course. But typically they are at a loss as to what to do about it. Therefore, they experiment with big data—usually focusing on transactional data but occasionally on a smattering of social media data—while they continue to beef up old tactics, such as loss leaders and product discounts offered to all buyers and often across all stores, in the hopes that something will work. In other words, instead of using data to figure out new tactics, most retailers are trying to fit more information into existing tactics.

Unfortunately, repeating old tactics will not change anything. At most they’ll succeed in temporarily enticing a few shoppers in the moment, but it is unlikely they can hold onto them for any meaningful amount of time in the absence of brand loyalty and brand differentiators. So it is that shoppers come and go between store brands with little positive effect on the retailers’ bottom lines.

Consider this analysis of the current retail clothing market from the aforementioned Stealing Share report:

In this paradigm, and because of their polar positions, luxury retailers and discount stores already come with a built-in audience. Those shoppers seeking exclusivity for the privileged and top designer fashion will frequent the high-end markets, while those seeking a value will hit the discount shop.

This then leaves the largest portion of the market in and around the middle. Here we find department and specialty stores lurking about, but without any real defining factors that separate them from the other contenders.

In this realm, the department store aims to steal market share from both the luxury and discount category. The lunacy in that is the only way these stores can gain market share is by way of discounting merchandise and building store locations nearby. That’s all.

Obviously a growth plan based on both a revenue loss (discounting merchandise) and an increase in expenses (building more brick-and-mortar stores) doesn’t have good odds at succeeding. The sector is badly in need of new business models and newer, more successful tactics—two things that big data excels at.

Retail Didn’t Blow It; the Customers Changed

Part, but not all, of the problems that this sector faces comes from a radical change in consumer shopping behavior borne from the last recession. The recession of 2007–2009 created a lasting change in U.S. consumer mindsets wherein materialism and brand consciousness nearly disappeared. Retailers struggled to survive the recession, stripped of any former brand advantages and customer loyalties, and the subsequent downward pressures on pricing and already too thin margins.

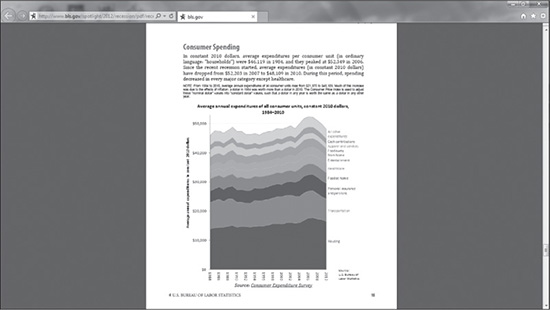

Figure 17.2 shows a U.S. Bureau of Labor Statistics, Consumer Expenditure Survey chart, from a 2012 report titled “The Recession of 2007–2009.” It shows average annual expenditures of all consumer units, aka households, in constant 2010 dollars, for the years 1984 to 2010. Note that in 1984, average total expenditures per household were $46,119 and in 2010, a year after the close of the recession, the average was a meager $48,109 nearly two decades later.

Figure 17.2 Average annual expenditures of all consumer units, aka households, in constant 2010 dollars, for the years 1984 to 2010.

Source: U.S. Bureau of Labor Statistics, Consumer Expenditure Survey at http://www.bls.gov/spotlight/2012/recession/pdf/recession_bls_spotlight.pdf.

Some retailers did not survive that recession. Those that did make it through, albeit battle scarred, pinned their hopes on a return of the traditional U.S. mindset of valuing materialism, favoring brands, and embracing debt. That so far hasn’t happened. Retailers now fear that brand loyalty has been permanently put aside as most consumers favor steep discounts and an avoidance of debt when possible.

Brand Mutiny and Demon Customers

In fact, American consumers were showing signs of brand mutiny and a preference for steep discounts prior to the recession. This emerging shift did not go unnoticed by savvy brands. Some in retail thought it not only possible to fight back against these growing consumer behaviors but they also boldly and publicly stated that was their intention. The results were not pretty nor particularly helpful to the brands.

On July 6, 2004, CBS News reported that Larry Selden, a consultant that worked for Best Buy, called customers who were not loyal to the store and did things found unprofitable to the retailer “demon customers.” Selden co-wrote a book titled Angel Customers and Demon Customers wherein he wrote “while retailers probably can’t hire a bouncer to stand at the door and identify the value destroyer, they’re not powerless.”

And with that, the retail industry proactively began to seek ways to ditch customers who do deplorable things like buy stuff, get the rebate, and then return the item for a credit or a cash refund. But retailers didn’t stop there. They began to turn their sights on discouraging and outright exorcising “demon customers” who only bought doorbuster sales items, without buying anything at regular price while doing so.

In other words, they ceased to see the sale of “loss leaders” as an expected loss and a necessary cost of doing business and instead came to see such losses as an attack on their profits by thieving “demon” customers. That mind shift in retailer thinking persists today and it’s still not particularly helpful to retailers. The more profitable approach is not in culling customers from your customer base but in developing every customer in your base to increasingly higher levels of profitability. We’ll get to that in a moment, but for now let’s continue with our exploration of the notion of culling customers.

Retailers sought other ways to cull their customer lists too; keeping profitable customers while ditching as many unprofitable ones as they could identify. Typically they achieved this, at least in part, through the use of customer relationship management (CRM) software, which gave them insights to customer behavior primarily through transactional data. With CRM they could easily see who was buying what and at what price point and how regularly. From that information it became possible to offer incentives for good customers, other incentives for irregular customers, and none at all for the demonic bargain hunters.

Then along came the recession and good customers began to delay purchases and even stray from their favorite stores to find better prices. Customers who bought irregularly continued to do so or not at all. And thus the by-then broadly defined “demon customer” ranks (bargain hunters) grew to an unprecedented size. It became obvious that retailers could no longer be so picky about who they wanted to sell to. The race to the bottom of pricing was then on in earnest. However, pricing wars usually don’t work as a long-term survival tactic because already slim margins get slimmer while business costs typically rise or stay the same. Of course, store closings and staff reductions quickly followed to reduce business costs. That in turn also decreased the customer experience thereby producing a further loss in sales and erosion of brand loyalty. The industry’s business was now circling around the drain. Still, they held on as best they could and hoped for a better day.

Customer Experience Began to Matter Again

When things appeared to be improving a bit economically speaking, retailers turned to another tactic. This time it was to improve the customer experience in an effort to reestablish a brand differentiator and to rejuvenate brand loyalty. Customer experience management is a blended approach of using software by the same name, called CEM or CX for short, and affecting changes in both the real and virtual worlds. The intent was to view the entire operation from the customer’s perspective and revamp anything necessary to make the shopping experience more pleasurable and memorable.

These efforts typically took everything into account from where shopping carts were placed in the parking lot, the lineup of vehicles on a dealer’s lot, or other “outside the door” elements of the operation, through the door to the actual shopping experiences there, be it on a virtual or real store floor, and all the way through cash-out, the at home experience, and customer service afterwards. Although this effort continues today, it still hasn’t produced the effects retailers hoped for—more cash in their coffers.

Big Data and the Demon Customer Revival

Then along came big data and the insights it could bring. At first retailers were enthralled with the ability to get to know their customers better and therefore make personalized offers they hoped would entice more sales per customer. But it wasn’t long before many of the retailers moved from a “we’re here to serve” motive to a “yeah, but what have you done for me lately, customer” attitude. In other words, many retailers reverted back to a version of the demon customer mindset. The effort was no longer pointed at attracting, rewarding, and maintaining good customers through loyalty programs and personalized offers, but to punish and drive away customers the retailers deemed not just unprofitable, but not profitable enough.

One example of this can be seen in a February 6, 2014 CBS New York report:

A warning if you shop online and have a habit of returning items, you may be in for a surprise—more retailers are starting to take notice and some are even punishing repeat offenders…

“The days of using your living room as a fitting room are yes, going to be coming to a close,” retail expert Carol Spieckerman said. “For retailers, returns are an absolute nightmare.”

In addition to charging restocking fees, stores may also start revoking free shipping, CBS 2’s Kristine Johnson reported.

Promotions and coupons may also be a thing of the past for customers who frequently return merchandise.

And this, despite the fact that retailers are largely still unable to differentiate themselves to any appreciable degree and are still locked in an unsustainable pricing war. As the authors of the Stealing Share report put it, “the retail industry is amuck… What does the future hold? How can any retail environment survive when most retailers are simply copying one another? At the end of the day, is price, discounting, and over-saturating the market the only game worth playing? Are the department store websites eating their own young?”

Yes, the industry is a complete mess but to their credit, they are seeking ways to right the ship again. Big data is the best tool they have in doing so. But that’s not to say that they’ve figured out quite how to use it yet. Even so, they’ll have to keep trying and keep experimenting because really they have no choice if they are to survive and prosper.

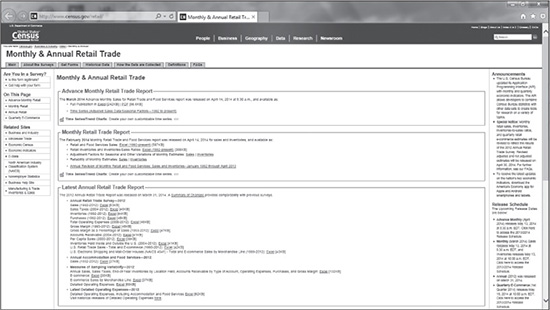

You can always find data on where the retail sector stands as of the most recent reporting/survey dates at the U.S. Department of Commerce, U.S. Census Bureau, most notably on its website in the Monthly and Annual Retail Trade data sets and reports. Figure 17.3 shows a screenshot of the Bureau’s data set lists in this category as of this writing. The Bureau regularly updates these data sets and provides new reports, so it is a good idea to check back often.

Figure 17.3 The U.S. Department of Commerce, U.S. Census Bureau’s data set lists in this category as of this writing.

Source: U.S. Department of Commerce, U.S. Census Bureau at http://www.census.gov/retail/.

WHY RETAIL HAS STRUGGLED WITH BIG DATA

Big data tools, unlike any other, can show retailers what is happening now rather than merely dissecting what happened in the past, uncloak emerging threats and opportunities, and spur changes in innovation, processes, and future business model needs. Right about now, every retailer reading this is totally disgusted, having heard all this before but not seeing any of it actually work profitably—or at least not seeing it work to the extent proponents loudly and broadly claim. That disgust and aggravation is not unwarranted, however the fault lies not in the big data tools, but in how they are currently approached and used.

The problem retailers have run into so far using big data is two-fold. First, the data hygiene problem can lead to crippling big data failures. For one thing, “information certainty” gets fuzzier outside of structured data, that is, the retailer’s own transactional data. In other words, the retailer knows that their own transactional data is both correct and uniformly structured in “conventional” databases, whereas much of the data they now import, such as from social media, is not. Well, the retailer presumes its transactional data is correct. In some cases that data is clean; in others, not so much. It all depends on how well the retailer breaches data siloes, integrates software, synchronizes file changes, and purges outdated information—as is the case in any other organization’s data operations.

Dirty data and/or incomplete data lies at the heart of nearly 40% of all failed big data projects. Yes, it is hard to understand how such massive amounts of data, especially when combined with other data set inputs, could be incomplete, but that is often the case. Just because you have lots of information about some things doesn’t mean the information you’re still missing won’t hurt your output. The key is to look for data and form algorithms that complete the puzzle you’re trying to solve in such a way that you end up with an accurate and full picture. Otherwise, all you have is a picture of something unrecognizable or suggestive of something different than it should portray because it has too many missing pieces.

Second in the retailers’ two-fold problem is the lack of creativity in the formation of big data questions. Like many organizations in every industry, retailers typically ask the same old questions of big data that they asked of smaller data. Namely those are in the vein of “who are my best/worst customers” and “which products are moving best/making me the most money?” While it’s perfectly understandable to ask these questions repeatedly, they give too narrow a view if that is all you ask. Further, asking the same questions of big data that you’ve always asked in the course of your business keeps your mind in the same framework as before, thereby blocking new thoughts and ideas. The goal before retailers today is to change the organization into a highly distinctive, fully differentiated, profit-generating machine. How are you going to do that by doing the same things over and over again ad nauseam?

This trap of asking the same old questions of big data is harder to escape than you might think. Because the ultimate concern of any business is on costs and profits, the questions asked of big data tend to exclusively focus on those concerns too. Certainly the answers to these questions are pressing and important. However, they are also too pointed. You can poke a hole for a glimpse of what you need with these pointed questions, but you can’t slice the blinders from your view with them. Just as many now-disappeared railroad companies of the last century failed to adapt because they narrowed their view to “we’re in the railroad business” rather than the broader, and proper, question of “we’re in the transportation business,” retailers today need to call on big data to answer both the “small” familiar questions of profits and loss items but also the broader “meta” questions that can mean the difference ultimately between success and mere survival.

WAYS BIG DATA CAN HELP RETAIL

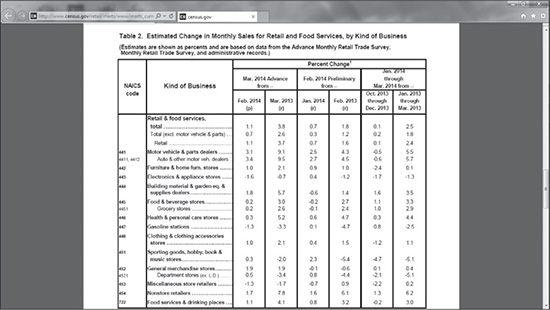

In a nutshell, these typical problems with using big data, or in plotting the path forward in general, is why retailers are having a tough time in finding their way. Instead, retailers find themselves continuing to resort to cliché advertising messaging, personalized marketing that is anything but, and broadly offered, deep discounts they can ill afford. If status quo continues to be projected into big data projects in retailing, than status quo will be the result of the efforts, i.e. small gains if there are any gains at all. Figure 17.4 is a table from the U.S. Census Bureau News’ press release on its “Advance Monthly Sales For Retail and Food Services February 2014” report showing “Estimated Change in Monthly Sales for Retail and Food Services by Kind of Business” for the period. As you can see, in status quo, as depicted in this chart, is not where retailers would like to see their business stay.

Figure 17.4 U.S. Census Bureau News’ press release showing estimated change in monthly sales for retail and food services.

Source: U.S. Census Bureau News’ press release. See current version at http://www.census.gov/retail/marts/www/marts_current.pdf (Table 2).

In order to break that pattern, retailers need to do something different. That means looking at the business differently and deliberately seeking out new ways to find profit. To that end, additional big data projects should include, but not be limited to, the tactics discussed in the following sections.

Product Selection and Pricing

The goal here is to ultimately aid in differentiation through product selection, product bundling and grouping, and value-added services and incentives. This is also a way to note product fluctuations and product category movements and trends early and overall. This can help in determining which items to discount and what merchandise your buyers should be buying in the future.

For example, retailers have historically stocked apparel in their stores according to national apparel size averages. But this tactic may be costing them revenue when customers can’t find their size on racks and shelves to buy. If the problem of size availability continues, customers may actually become discouraged and stop shopping at that store entirely. Meanwhile, the retailer has left-over product at the end of the season that it must now mark-down which further cuts into its revenue. If, however, a retailer stocks sizes according to customer needs and preferences in each store location, the opposite reaction occurs: more product is sold and customers regularly return as they know they’ll likely find their size in most items at that store. This is the beginning of a brand differentiator and budding new brand loyalty.

Such sizing data already exists and brands can either act on that data alone or add it to their algorithms to further enhance their product buying and inventory decisions. It would be a mistake to determine size selections based on the store’s transactional data alone as that data would not account for items not purchased (lost sales) due to size unavailability and therefore is unlikely to deliver the correct answer in the analysis.

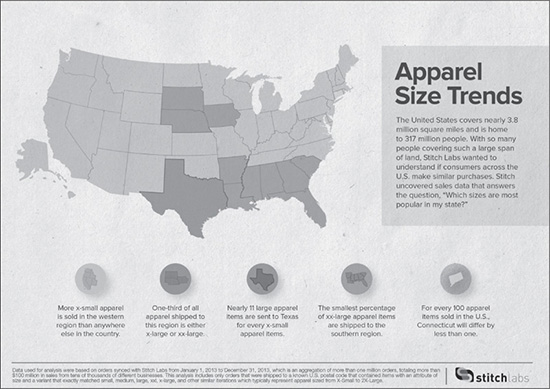

So where is that existing apparel size data? One place you can find it is at Stitch Labs, a producer of inventory management control systems. The company says it analyzed more than $100 Million in apparel sales from tens of thousands of retailers to determine sizing trends across the United States.

“The data indicates that consumers in western states (California, Washington, Oregon, Idaho, Nevada, Utah and Hawaii) prefer smaller sized apparel, purchasing almost double the amount of X-Small apparel compared to the U.S. average,” the company announced in its report released to the press on June 24, 2014. “Consumers in South Dakota, Nebraska and Iowa, on the other hand, purchase the most X-Large and 2X-Large apparel. One in three pieces of apparel purchased in these states is an X-Large or 2X-Large.”

From this analysis, it is relatively easy to see how something as simple as changing the size selection of apparel in stores can significantly improve profits, customer satisfaction, and brand loyalty. Figure 17.5 is an infographic built from the Stitch Labs sizing data analysis for a fast overall view of customer size preferences per state.

The point is to use data in product selection and then work with data on optimum pricing to improve both your store profits and brand loyalty.

Figure 17.5 Infographic from Stitch Labs’ data analysis on customer preferred apparel sizes per state.

Source: Stitch Labs. Reprinted with permission.

Current Market Analysis

This includes analysis in near-real-time to note any shifts and trends in the overall market. Retailers need to watch for patterns found among indirect competitors such as those within the collaborative economy discussed in Chapter 8, those outside your retail category (luxury, discount, specialty, and so on), and those in geographic markets where you also have a store.

Use Big Data to Develop New Pricing Models

This could allow retail chains to avoid broadly available discounts that may hurt their bottom lines if these loss leaders become sole purchases. Look instead to adjusting pricing in personalized offerings that reward good customers and entice irregular and new customers. Avoid any actions designed to punish customers. Such is self-defeating because many of these so-called demon customers are actually suffering from a jobless recovery after the recession or otherwise temporarily encumbered. You don’t have to encourage their behavior, just avoid doing anything that will turn them off of your brand when they are in better financial circumstances. You also don’t want to inadvertently spark new regulations intended to stop price discrimination and unfair business practices. Remember that using big data successfully means using it to improve both the short- and long-term results.

Find Better Ways to Get More, Better, and Cleaner Customer Data

Approach data gathering in a way that respects privacy and actively solicits customer partnerships to aid in brand differentiation and customer loyalty. Your data will be cleaner (more accurate and up-to-date) if customers give it to you willingly than if you try to collect it on the sly. Consider offering customers something tangible for their data and self-service data updates, such as an extra service, a discount toward their next purchase (and every purchase after a self-service data update), points towards price discounts in the future, or access to first views and buying opportunities of new inventory or inventory “reserved” for these special data-sharing customers (inventory not offered on your website or in-store to other customers).

Whatever you do, do not think that offering a “personalized ad” is in anyway compensation for their data. The truth is everyone hates ads. Distributing and displaying them are to your benefit, not the customers’—at least that is the case in the customers’ minds. By all means you should be distributing highly-targeted, personalized ads—just don’t think you’re doing the customers a favor in doing so.

Study and Predict Customer Acceptance and Reaction

This should be done prior to investing in new technologies and changing stores. For example, analyze studies and tests for potential consumer reaction to service automation and self-service customer service before you fully invest in it. Also use big data to compute the mid- and long-term impacts of any changes you are considering.

Applebee’s and Chili’s Experiments

At the time of this writing, Applebee’s and its rival Chili’s are busy putting tablets on tabletops to enable customers to view menus, place their own orders, and cash themselves out, which will eventually reduce or eliminate the store’s need for waitresses, waiters, and cashiers. This is very appealing to restaurants as it means they can eventually wave goodbye or reduce the impact of minimum wage increases and other employee costs such as health insurance mandated through the Affordable Care Act.

A December 2, 2013 USA Today article reports that the tablets have 7-inch screens, which are larger than a cell phone’s but smaller than the tablets most consumers own. While the move clearly targets younger customers it may actually be a barrier to older customers who may have trouble viewing the screen or placing orders and making payments on it. This would be bad for restaurants as the U.S. population is aging, meaning that for years to come there will be far more older than younger customers in the market. Further, using tabletop technology reduces the personal interaction between restaurant staff and customers, thereby decreasing the chances of developing customer loyalty to the brand. So yes, it could reduce a restaurant’s employee expenses but it may also cost it in sales. The USA Today report said that Applebee’s plans to offset this somewhat by continuing to give patrons a traditional menu as well, at least for awhile. Even so, this move may very well backfire in the end.

For one thing, if the trend continues to automate every possible job, how far will that diminish the customer base? Think of it this way—if the recession harmed retailers to the extent that it did because of job losses and loss in consumer confidence, how can mass job reduction through automation affect retailers not only in the same time frame as a typical recession, but for all of the foreseeable future? Can retailers really afford to join the job elimination movement and cut off the hand that feeds it?

What Walmart Is Doing

Walmart isn’t so sure and is considering a move to increase consumers’ ability to buy from them through supporting an increase in the minimum wage. One might think, considering that Walmart is the largest private employer in the nation, that an increase in minimum wage would drive its payroll costs to untenable heights. But this is what Renee Dudley reports about the retail giant’s thoughts on the issue in her February 19, 2014 article in Bloomberg:

“Walmart is weighing the impact of additional payroll costs against possibly attracting more consumer dollars to its stores,” David Tovar, a company spokesman, said today in a telephone interview. “Increasing the minimum wage means that some of the 140 million people who shop at the chain weekly would ‘now have additional income,’” Tovar said.

In the mid-2000s, Walmart backed an increase in the federal minimum wage that eventually took effect in 2007. Asked whether Walmart would support another raise in the federal minimum wage, Tovar said, “That’s something we’re looking at. Whenever there’s debates, it’s not like we look once and make a decision. We look a few times from other angles.”

It is telling that Walmart, and not Applebee’s and Chili’s, is the poster child for big data use in retailing. It is also telling that Walmart is a super giant in retailing and not prone to mistakes in its market moves. Now think about that a moment. Which plan—eliminating jobs through automation or increasing minimum wage nationwide—is more likely to spur retail sales? A big data project run properly could easily determine that. There is no reason to guess or to cook up ideas and plans in an isolated bubble. Turn to big data and find out, and then make your move accordingly.

The J.C. Penney Failure

Consider J.C. Penney’s woeful tablet tale and its disastrous move away from its established but older customer base to cater to a younger, hipper crowd. Note that J.C. Penney isn’t a big data poster child either. If it had been, this scenario would never have come to be. Here is how Brad Tuttle reported in Time J.C. Penney’s horrific fall and the subsequent firing of CEO Ron Johnson, former retail superstar at Target and Apple stores:

As Johnson removed their beloved coupons and sales and increasingly focused on making J.C. Penney a hip “destination” shopping experience complete with boutique stores within the larger store, many of the chain’s oldest and most loyal customers understandably felt like they were no longer J.C. Penney’s target market. The return of “sales” hasn’t proved to bring about a return of these shoppers.

Johnson pictured coffee bars and rows of boutiques inside J.C. Penney stores. He wanted a bazaar-like feel to the shopping experience, and for J.C. Penney to be “America’s favorite place to shop.” He thought that people would show up in stores because they were fun places to hang out, and that they would buy things listed at full-but-fair price.

But early and often during the Johnson era, critics pointed out that J.C. Penney was not the Apple Store. The latter features cutting edge consumer tech that shoppers have grown accustomed to purchasing at full price. J.C. Penney, on the other hand, is stuck with a “reputation as the place your mom dragged you to buy clothes you hated in 1984,” as a Consumerist post put it. The idea that people would show up at J.C. Penney just to hang out, and that its old-fashioned shoppers would be comfortable with Johnson’s radical plans like the removal of checkout counters almost seems delusional [checkout counters were replaced with tablets].

In retrospect, Johnson and J.C. Penney seem like a horrible match. All along, Johnson insisted that he absolutely adored the venerable J.C. Penney brand. But if he loved it so much, why was he so hell bent on dramatically changing it, rather than tweaking and gently reshaping as needed?

Once again we see that gut instinct and past experience are not enough to steer a company in the right direction. Knowing the customer base intimately and leveraging their buying triggers is key and that requires a mastery of big data.

Sears and MetaScale—A Big Data Love Story

Sears was once the largest U.S. retailer by revenue count and enjoyed high ratings in consumer trust and brand loyalty. Since then, the very same problems that have plagued all of retail, such as shifting consumer shopping trends, the rise of online competitors and a major recession, have also tormented Sears. The giant retailer has tried several strategies to regain its footing in the market with mixed success. One of those strategies was an early foray into big data. It is still working hard with data to this day.

“We were already dealing with big data as we had already amassed a huge volume but it was expensive and inefficient to do much with it,” said Sunil Kakade, IT Director at Sears Holding Corporation, in a phone interview for this book. “Everyone accepted the limits of the technology at the time. But, the nature of our business was changing so we needed to find a tech platform that would enable us to compute more information, more often and cheaper.”

It was then that the company turned to Hadoop and took its first serious step into using big data to guide the company forward.

“We have thousands of jobs running at a time and we have learned a lot in this process,” said Kakade. “Big data is not going to solve all your problems though, so use the best of both worlds.”

Kakade offered a few more tips for retailers in that interview concerning using big data:

![]() Don’t lock yourself in with vendors. The whole nature of big data is open source, leverage that. Plus, the industry is immature and if you lock-in with one vendor or distribution you risk their going out of business and having to start over.

Don’t lock yourself in with vendors. The whole nature of big data is open source, leverage that. Plus, the industry is immature and if you lock-in with one vendor or distribution you risk their going out of business and having to start over.

![]() Dedicate multiple teams to big data because it is evolving and you have to stay on top of it. We also have software developers who are available if we need more help. You may want to do that too. It also helps to have teams dedicated according to functional expertise required by the systems, such as in supply chain, pricing, marketing, human resources, and so on.

Dedicate multiple teams to big data because it is evolving and you have to stay on top of it. We also have software developers who are available if we need more help. You may want to do that too. It also helps to have teams dedicated according to functional expertise required by the systems, such as in supply chain, pricing, marketing, human resources, and so on.

![]() Move forward and start making decisions now. You need a smart strategy first to take advantage of big data and optimize everything.

Move forward and start making decisions now. You need a smart strategy first to take advantage of big data and optimize everything.

Shortly after the company started using Hadoop for its own benefit, Sears launched MetaScale, a new big data subsidiary to serve not only Sears, but other companies too. Rachel King reported in her April 30, 2012 piece in the Wall Street Journal how this came to be:

Sears is certainly not the first retailer to try applying advanced business analytics to create more targeted marketing to its best customers. But it may be the first retailer to turn that activity into a service it will sell to companies in other industries.

On April 24, [2012], Sears launched MetaScale, a new big data subsidiary. For the last couple of years, [now former] Sears CIO Keith Sherwell has been using open source software called Hadoop that lets the retailer search through reams of information to better understand its business. For example, Sears discovered that many people who go into its stores to buy jewelry also buy tools.

Sherwell realized as he was providing services to other divisions of Sears internally that other businesses might also benefit from the expertise Sears had built with Hadoop. MetaScale is selling managed Hadoop services that will be customized and implemented in a matter of weeks. MetaScale will target customers with revenue in the range of $1 billion to $10 billion in industries such as healthcare and entertainment. MetaScale will avoid selling services to its competitors, said Sherwell. The day-to-day operations of MetaScale will be run by Sears CTO Phil Shelley.

These services can be used to better target offers to customers. For example, Hadoop software can search through raw transactional data from each cash register and online purchases at the item level to glean insights about a specific customer’s preferences.

While Sears’ original big data masterminds, former CEO Lou D’Ambrosio and former CIO Keith Sherwell, have exited the company, Sears’ big data efforts and MetaScale live on, albeit separately. The MetaScale website only mentions that it “grew out of a Fortune 100 enterprise” with no mention at all that the enterprise was Sears. Executives on the retailer end also make no mention of MetaScale when discussing their big data efforts. Presumably this is because MetaScale was spun off as a separate company and the two are trying to keep proper distance from one another even though MetaScale executives still speak fondly of their hard-won expertise with big data in the retail sector.

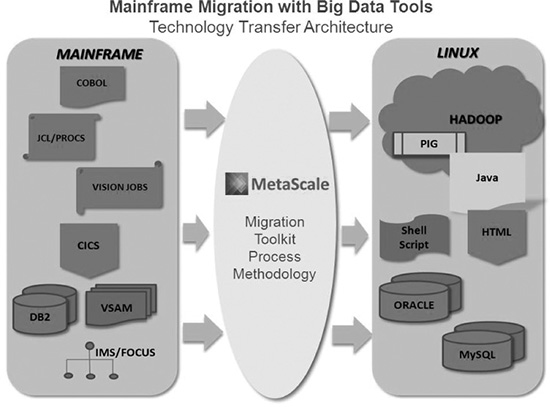

Figure 17.6 shows how MetaScale handles data migration from a mainframe using big data tools.

Figure 17.6 Mainframe migration with big data tools.

Source: MetaScale. Reprinted with permission.

Predict and Plan Responses to Trends in the Broader Marketplace

One mistake retail is notorious for repeatedly making is thinking it exists in its own bubble, unaffected by whatever else is going on in the world except maybe by changes in the economy. The rise of such disrupters as Amazon and eBay should have been a wake-up call to the industry and in some ways it was. But many retailers have yet to regain their footing since. Now there are more disruptors on the horizon and retailers will have to really scramble to catch up and surpass these challenges. Revisit Chapter 8 on the rise of the collaborative economy for an example of new challenges on that front.

Enter 3D Printers

There are other changes coming as well, such as 3D printers. Already manufacturers are using 3D printers, known in those circles as additive manufacturing, to produce goods faster, cheaper, and more precisely. Additive manufacturing means a device, a 3D printer, constructs the item by layering raw material to a precise, predetermined shape. By comparison, the traditional way is to use subtractive manufacturing, which means cutting or stamping a shape out of the raw material. In other words, the process subtracts the shape from a chuck of raw material. Subtractive manufacturing produces a lot of waste; additive manufacturing does not. As of this writing, additive manufacturing is well underway and producing everything from car parts to human dentures.

In the near future, 3D printers will be in wider use. Instead of shipping goods assembled in a manufacturing plant or from a retailer to a customer, in many cases design codes will be sent to on-site 3D printers instead and produced there. This situation will enable on-site production in regional or local distribution centers as well as on customer premises. For example, companies of the Kinko’s ilk can receive design codes and print items for customer pick-up or local delivery. This will of course diminish the need for long distance, overnight, and ground shipping services such as those provided by FedEx and UPS. Eventually, many items can be produced on the customer’s own 3D printer in their business and home. This will be especially true of items made from common and easily handled raw materials. If an image of the Star Trek replicator has popped into your mind, you’re not far off.

Home Body Scanners

Also in the near future will be the rise of home body scanners. Indeed these are in use today albeit in a limited fashion. Personal body scanners can be used in the privacy of the consumer’s own home to take precise body measurements. Such measurements can be used to virtually “try-on” and order clothing and other items made to fit perfectly. This will decrease or eliminate the need to return items after purchase to retailers because of fit or “look” issues. The body scan can be uploaded to a device screen where the consumer can then see how the item looks on them before purchase. If the consumer likes what they see, their measurements can then be sent to the retailer to purchase the item in a precise fit, rather than a generic size. The retailer can then upload the measurements to their own 3D printers to produce it, send the adjusted code to the customer’s 3D printer for production there, or send the measurements to a manufacturer to print and ship it.

The days of buying a piece of clothing in a size 6 or 12, or whatever general size grouping are quickly coming to an end. Instead, items will be ordered in “My Size” in whatever individual measurements are required. This will come to be because of the versatility of 3D printers in producing items individually rather than in bulk.

An example of such scanners in use today is Shapify, an online service that leverages handheld scanners and software to produce a physical but miniature 3D model of the person scanned. A November 19, 2013 article by Elisabeth Eitel titled “Does This $59 3D-Printed Figurine Make Me Look Fat?” in Machine Design explains how this system works:

The service uses models made with a commercial game controller sold for use with the popular Xbox 360 console to make a detailed scan of a person’s body and then additive manufacture a physical 3D model of it. More specifically, Artec’s Shapify service uses models made with a Xbox Kinect (or Kinect for Windows).

First, users scan themselves, friends, or family with the Kinect—one person at a time, please—and then upload the scans to the Shapify website. Next, software sends the models over a server to a 3D printer that generates the figurines. A week or so later, presto—the user gets her Mini Me (and Friends, where available) in the mail.

Figures 17.7 and 17.8 show examples of figurines that Shapify produces on a 3D printer using a person’s body scan made via an Xbox Kinect game console.

Figure 17.7 Figurine that Shapify produced on a 3D printer using a person’s body scan made via an Xbox Kinect game console.

Source: Shapify/Artec Group.

Figure 17.8 Another figurine from Shapify produced on a 3D printer.

Source: Shapify/Artec Group.

PREDICTING THE FUTURE OF RETAIL

Obviously these changes, separately and together, will abruptly alter how retailing is done. It behooves the industry to prepare for such now. Some retailers may want to strive to be the first to offer such since first to market has its advantages. Others may prefer to incorporate upcoming market changes into their model to enhance customer experience and continue to entice customers to shop at their brick-and-mortar stores.

Former J.C. Penney CEO Ron Johnson was not wrong in thinking of shopping as a social event and in trying to leverage that aspect to entice and retain more shoppers. There are reasons why customers do not exclusively shop online and shopping as a social experience is chief among them.

Johnson’s timing was a bit off and he followed his gut in creating what he thought a prime social experience for shoppers would be rather than building an experience more in tune with what the customer base defined the preferred social experience to be.

In the face of changes to come in retailing, such a plan may work marvelously well for other retailers. The point is that while Johnson’s instincts were right on the money, his actions based on that gut call were not. Had he used big data to understand his customer base better and plan his actions accordingly, the end of this story would have been vastly different and Johnson would have likely been hailed as a visionary.

If the brick-and-mortar retail sector is to save itself, it must hasten and improve its use and mastery of big data and other technologies. It must also reinvent itself in ways previously never imagined. Retailers cannot afford to operate on gut instinct or stick to business as usual.

SUMMARY

In this chapter you learned how the retail industry came to be in the position it is now. You learned that changes to the industry wrought by outside forces such as brand mutiny, online competitors, and the last recession have forever changed the marketscape for this sector. You also learned that retail companies have made some bad decisions along the way in their attempts to survive in the face of adversity and later to prosper in spite of it.

You also learned that the retail industry is still not in the clear as many challenges still remain and more change is coming. You now know what some of those are and how retailers might profitably address them.

Last but not least, you saw how retailers that have mastered big data, such as Walmart, compare to retailers that have not yet mastered it, such as Applebee’s and J.C. Penney. You saw from these comparisons how radically different the thinking and implementations are as a result—and the differences in outcomes, either already achieved or likely to come soon.

The take-away is that retail has to reinvent itself to stay in business—not just once but repeatedly. Big data offers the best and safest means with which to do that.