Biorefineries

Industry Status and Economics

H. Stichnothe1, D. Meier2 and I. de Bari3, 1Thünen Institute of Agricultural Technology, Braunschweig, Germany, 2Thünen Institute of Wood Research, Hamburg, Germany, 3Division of Bioenergy, Biorefinery and Green Chemistry, ENEA Centro Ricerche Trisaia, Policoro, Italy

Abstract

This chapter focuses on techno-economic assessments of biobased products from fermentation and fast pyrolysis. We briefly describe underlying methodologies and summarizea number of literature studies dealing with conversion pathways using fermentation and fast pyrolysis. However, data are limited on the techno-economic evaluation of innovative biorefinery processes. We identify methodological challenges for techno-economic assessment of biofuels and biobased chemicals and describe limits of comparing results from different studies. We depict the lessons learned from lignocellulosic ethanol and show examples of biobased chemicals and bio-oil that are already produced at large scale. In the longterm, biobased chemicals and biofuels must compete on cost and performance with petrochemicals and petroleum fuels, however at present biofuels and biobased chemicals derived from lignocellulosic biomass are hardly cost-competitive.

Keywords

2G bioethanol; cost estimation; commercial plants; bio-oil; fermentation; fast pyrolysis

3.1 Introduction

Frequently, feedstock composition determines the choice of the conversion strategy, and a range of technologies are available for bioenergy production. The use of versatile, robust technologies is one of the key factors in biorefineries. The synergetic combination of process technologies can lead to the development of advanced biorefineries where nonfood biomass, preferably from residues and waste, is converted by a combination of mechanical, thermochemical, chemical, and biochemical processes, into a range of materials, chemicals, and energy. Hence, the maximum value is achieved from each feedstock.

In fact, the possibility of diversifying both the feedstock and the final products would help biorefineries cope with continuously changing market dynamics and connected commercialization constraints, because the same infrastructure could be leveraged to produce a broad range of products in response to changing market conditions.

Currently, biofuel production is driven by politically motivated incentive schemes as well as the desire for a more sustainable fuel alternative. Although there is already a market for a number of biobased plastics and other biobased chemicals, the demand is considerably lower in comparison to traditional fossil fuel-based plastics. However, the market for biobased chemicals is anticipated to increase significantly in the near future, for example, the global biobased biodegradable plastics market is forecast to grow by 18% between 2014 and 2020 according to a report of Future Market Insight.1 Integrated biorefineries producing biobased products using bioenergy produced on-site and exporting just the bioenergy surplus is a promising way forward.

At present the majority of biorefineries do not provide the synergetic combination. Most large-scale fermentation plants still run on starch or sugar as feedstock, but there is a preference to use lignocellulosic-derived sugars in the future, because of rising sugar prices and public concerns. Large-scale fast pyrolysis plants produce mainly bio-oil for stationary burners and in the midterm bio-oils could be upgraded to transportation fuels and platform chemicals. Although promising, integrated biorefineries still have to prove that they can become cost-competitive.

3.2 Economics

Cost estimation is a specialized subject and a profession in its own right (Towler, 2007). The development of a new biorefinery, its design and construction, requires huge investments; cost estimations are often paramount for deciding the economic viability of biorefineries, and must be performed on a case-by-case basis. However, it is possible to make (rough) cost estimations based on data from demo plants, process modeling, and/or literature at various stages of the biorefinery development.

3.2.1 Economic Considerations

Total cost can be divided into capital expenditures (CAPEX) and operating expenditure (OPEX). CAPEX can be subdivided into plant costs, off-site costs, and engineering costs. Plant costs represent the capital necessary for the installed process equipment with all auxiliaries that are needed for complete process operation (ie, piping, instrumentation, insulation, foundations, and site preparation). Off-site costs are not directly related to the process operation, they rather include costs of the addition to the site infrastructure, for example, power generation units, boilers, pipelines, offices, etc. According to the American Association of Cost Engineers, fixed capital investment can be divided into outside battery limits (OBL) or off-site and inside battery limits (IBL). IBL comprises one or more geographic boundaries, to specify the area where production takes place, enclosing all associated equipment and production facilities. OBL includes facilities such as storage, utilities, administration buildings, or auxiliary facilities. Engineering costs include costs for detailed design of equipment, construction supervision, project management, etc.

OPEX consists of fixed and variable costs. Variable costs comprise cost of feedstock and supplies, waste management, product packaging, finished and semifinished products in stock, etc. Fixed costs comprise salaries, taxes, license fees, interest payments, marketing costs, etc.

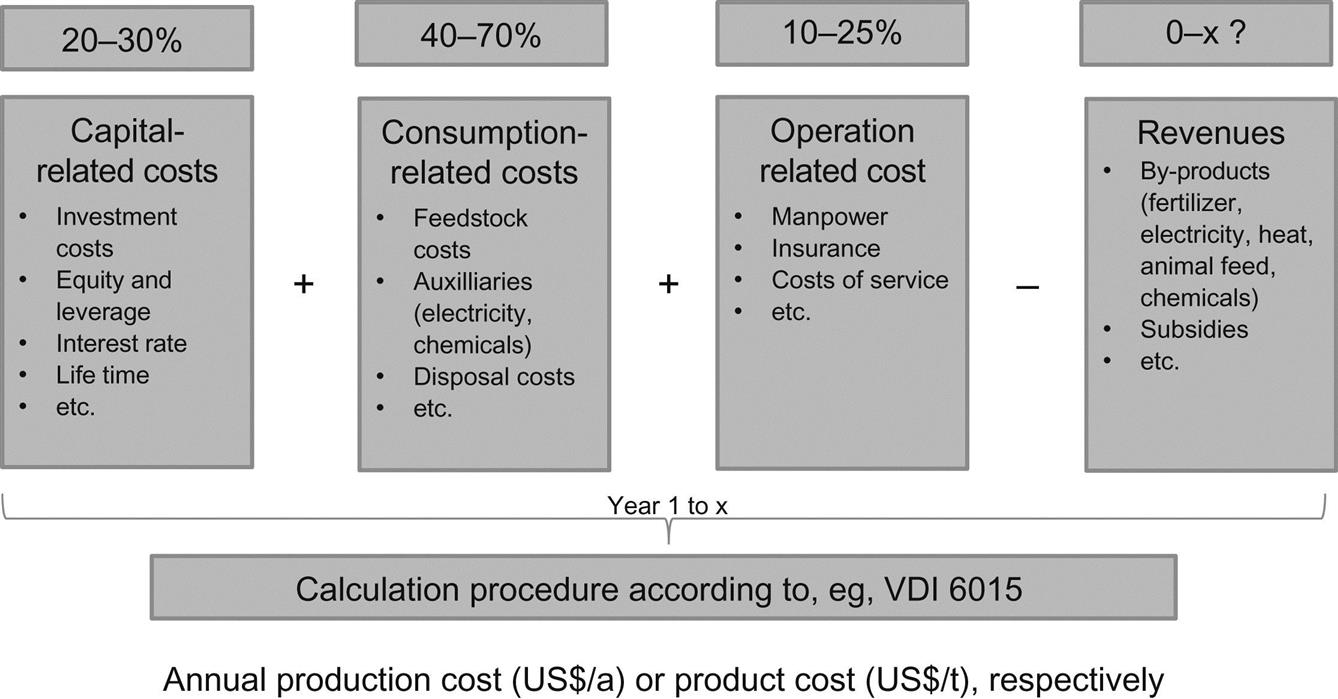

A generic approach on how to conduct the economic assessment, the most relevant cost parameters, and ballpark figures for first-generation (1G) feedstock is depicted in Fig. 3.1.

Investment costs are an important contributor to the economic feasibility of lignocellulosic biorefineries (Anex et al., 2010; Brown, 2015). Investment costs are more important for second-generation (2G) biorefineries than for 1G biorefineries because feedstock costs are lower and processing lignocellulosic biomass is more challenging (Hytönen, 2009; Zinoviev et al., 2010; Brown, 2015); hence capital investment costs are higher.

Innovative new conversion technologies usually follow a development pathway from the lab, to piloting, then demonstration, and finally the construction of a commercial plant. The number of years for a biobased product to reach commercialization depends heavily on economics and hence on drop-in versus nondrop-in (existing demand and infrastructure), type of conversion technology, and supply chain integration. Various methods are applied for estimating investment costs when plants or processes are scaled-up.

3.2.1.1 Factorial Method

Preliminary cost estimates can be based on the purchased equipment cost with all additional cost components based on it and estimated through different “factors,” that is, certain percentages of the purchased equipment cost. The factorial cost estimation method was developed by Lang (1947, 1948) and frequently used in chemical engineering in early design stages. Although biorefineries may differ from chemical plants, a similar approach is appropriate (Stanil, 2011). The accuracy of the result of the factorial method depends on what stage the design has reached at the time the estimate is made, and on the reliability of the data available on equipment costs. Quantified predictions can only be done for a limited amount of time ahead, since uncertain market conditions and rapid technology development result in sharp price inflation.

The equation for the cost estimation is:

(3.1)

where Cc = fixed capital costs, fL = Lang factor, can be obtained from chemical engineers design books (eg, Peters et al., 2002; Towler, 2007), and Ce = total costs of major equipment.

The “Lang factor” depends on the type of process, that is, solids processing (fL = 3.1), liquid processing (fL = 4.2) and liquids–solids processing (fL = 3.6).2

If more detailed information is available, compounds such as piping, electrical power, control instruments, etc., can be considered individually. The individual costs are summed to generate the total capital investment costs.

3.2.1.2 Step Accounting Method

Step accounting methods attempt to correlate the capital investment cost of a process with the values of its fundamental process parameters. These values might be the number of significant process steps, plant capacity, temperature, pressure, materials of construction, number of significant process steps, etc. The term significant process step (or functional unit) defines all equipment and auxiliaries necessary to complete an operation in the production stream, as defined by the American Association of Cost Engineers. This method is useful when the plant has a limited number of products, for example, power or fuel production, but difficult to apply for multioutput systems such as new and innovative biorefineries.

3.2.1.3 Exponential Method

The cost of a future plant can be estimated based on historical cost data of similar plants. The same applies for estimating the costs of specific process equipment, for example, heat exchanger, distillation units, etc.

(3.2)

(3.2)

(3.2)where ACC1 = annual capital cost of unit or scale (Q1), for example, large scale; ACC2 = annual capital cost of unit or scale (Q2), for example, demo scale; m = scale exponent; and corrF = correction factor, if the design is highly comparable corrF = 1.

Calculating the capital costs for a biorefinery or specific equipment is not straightforward because comparable facilities are not built yet and thus appropriate factors, for example, Lang factors, for future biorefineries are hardly available. If future biorefineries are comparable to established chemical plants, then the cost estimation methods described above can be also used to estimate the product price depending on the scale-up. They can also be used to define optimization targets for the process design and the scale-up process. An example of how the exponential method can be used is shown below.

Example:

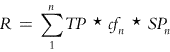

For the scale-up the residence time and the conversion rates (cf1–n) are the most relevant parameters. As first approximation product costs (PC) can be estimated based on throughput (TP), conversion factor (cf), annual capital costs (ACC), operation costs (OC), and revenue (R) according to the following equation:

(3.3)

The selling price (SP) can be expressed as function of the residence time if the throughput and the conversion rate are assumed to be constant.

(3.4)

The acceptable residence time (rt) for a plant at technical scale can be calculated using the SP as a constraint. The revenue from byproducts depends linearly on the throughput. Hence the revenue can be expressed as function of the throughput when the SP for each byproduct (n) is used:

(3.5)

(3.5)

(3.5)ACC does not increase linearly with scale; therefore the acceptable residence is higher at large scale than at technical scale for a given minimum selling price (MSP). The exponential method can be used to estimate the ACC of large-scale plants (LS) based on ACC of technical scale plants (TS). The exponential method is frequently used in chemical engineering and is expressed as:

(3.6)

(3.6)

(3.6)where the exponent (m) usually varies between 0.6 and 0.7.

Using Eqs. (3.5) and (3.6) in Eq. (3.4) allows calculating of the acceptable residence time for a given scale-up (TS→LS). The equations above also allow defining optimization targets, for example, conversion factors for the main and the byproduct(s) under consideration of the MSP of the product(s) for a given process design. However, those calculations are based on point estimates and incur a substantial uncertainty due to price fluctuations. One method to reduce the uncertainty is to model the statistical distribution of prices in combination with sensitivity analysis methods such as Monte Carlo simulation.

The methods described above are applicable if comparable plants exist. In the last decade many plants have been built for the production of biofuels and bioenergy, therefore reliable cost data exist for those technologies. Table 3.1 provides an overview of typical investment and operation costs of matured technologies at different scales.

Table 3.1

Overview of investment and operation costs of bioenergy-related technologiesa

| Technology | Plant production capacityb | Investment costs (range) | Operation costs (range) | Preferred feedstock | ||

| Minimum capacity | Typical capacity | Maximum Capacity | ||||

| Pyrolysis (fast) | 15,000 t/year | 45,000 t/year | 300,000 t/year | 600–3000 € per kWinst | 11% of investment | Wood and dry biomass |

| Anaerobic digestion | 0.3 MWe | 0.5 MWe | 4 MWe | 1800–4000 € per kWinst (0.5–2 MW) | 11% of investment | Nearly all kinds of organic biomass |

| First-generation bioethanol | 10,000 t/year | 250,000 t/year | 1,000,000 t/year | 700–1000 € per t/year | 11% of investment | Starch (wheat, potatoes, etc.) |

| Esterification (biodiesel) | 10,000 t/year | 100,000 t/year | 500,000 t/year | 400–600 € per t/year | 11% of investment | Oils and fats |

| Direct liquefaction | 5000 t/year | 50,000 t/year | 200,000 t/year | 900 € pert/year | 11% of investment | All kinds of organic waste streams |

aThis information is kindly provided by NOVIS GmbH.

b1 t=1000 kg=1 Megagram (Mg).

In general, the first-of-its-kind commercial plant shows disadvantages with regard to the total capital investment but also operational costs in comparison to succeeding installations. Several installations are frequently needed to enhance efficiencies due to technical learning. High-value material utilization of all product streams is essential to achieve profitability of complex biorefineries.

The production of bioethanol is the most matured biotechnological process. Historical data allow estimating the cost reduction potential due to technological progress, which has been made for ethanol production from woody material and agricultural residues. The techno-economic development of ethanol from cellulosic feedstock is depicted below.

In the early technology development stage ethanol production costs can be used as a proxy for other products derived from cellulosic sugars, for example, butanol, furan derivatives, etc. However, that is just a rough estimation because equipment costs and energy costs differ, although similar equipment is needed for purification and upgrading.

3.2.2 Economic Lessons Learned From Bioethanol and Bio-Oil Derived From Lignocellulosic Biomass

The National Renewable Energy Laboratory (NREL), Golden, CO, USA, has developed case models that document progress and cost targets for energy carrier production from cellulosic feedstock (Anex et al., 2010; Kazi et al., 2010; Swanson et al., 2010; Wright et al., 2010; Davis et al., 2013). The economics analysis includes at a conceptual level of process a design to develop flow diagrams using commercial simulation tools, for example, ASPEN PLUS. The capital investment costs are estimated based on the plant design using the factorial method; working costs are estimated based on similar chemical plants (Wright et al., 2010). The simulation software is also used to calculate the mass and energy flows in order to estimate the operation costs. Detailed information of the technology model is available (Aden, 2008, 2009).

The NREL cost model for ethanol and/or hydrocarbons from cellulosic feedstock is based on a plant capacity of 2000 t (biomass demand) per day (t/day). For bioethanol the model includes the following process steps:

![]() Pretreatment (dilute acid and enzymatic digestion);

Pretreatment (dilute acid and enzymatic digestion);

![]() Biological conversion of sugars to ethanol;

Biological conversion of sugars to ethanol;

![]() Product recovery and upgrading (assuming lignin for combustion);

Product recovery and upgrading (assuming lignin for combustion);

Kumar and Murthy (2011) have modeled the conversion of grass straw to ethanol; grass straw is a byproduct of grass seed production and has a cellulose content of 31%. They used dilute acid, dilute alkali, hot water, and steam explosion as pretreatment in their model to estimate the production costs of all pretreatment methods followed by fermentation. Lignin residue was sufficient to cover the energy demand of pretreatment, conversion, and upgrading. The authors estimated ethanol production costs as US$ 1.06, 1.12, 1.02, and 1.09 per kg ethanol for dilute acid, dilute alkali, hot water, and steam explosion pretreatment, respectively, at a plant capacity of approximately 750 t/day (Kumar and Murthy, 2011). The main factors were feedstock costs and enzyme costs. Kazi et al. (2010) investigated the conversion of corn stover to ethanol and came to the same conclusion that enzyme costs and feedstock costs are the most important factors.

There are several optimization options that are suitable to reduce the production costs, for example, improved conversion efficiency of underutilized biomass fractions (mainly hemicellulose) with production of additional value-added products. Besides feedstock and enzyme costs, the pentose conversion rate is another important option for reducing ethanol production costs. Xylose is the most important pentose obtained via acid hydrolysis and can be thermochemically converted into furfural. Furfural, a common industrial chemical, is a potential platform chemical for biopolymers (Choudhary et al., 2012).

Interest in drop-in biofuels, especially for aviation, continues to grow. Tao has conducted a techno-economic assessment for the production of n-butanol, iso-butanol, and ethanol from corn stover. In contrast to cellulosic ethanol fermentation technology, n-butanol and especially iso-butanol fermentation technology, has not yet been fully demonstrated even in bench studies (Tao et al., 2014). However, the authors concluded that if fermentation of xylose and glucose to butanol would reach 85% yield, the minimum SP would then be comparable to that of ethanol.

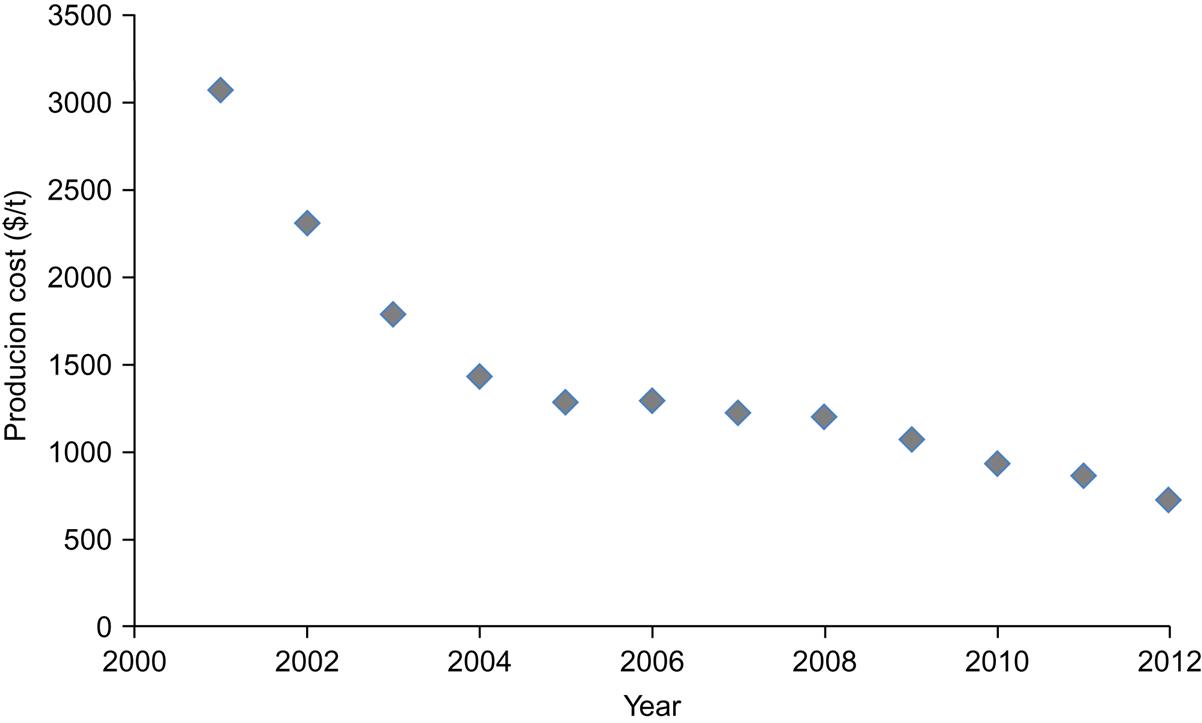

Results from various NREL techno-economic studies about lignocellulosic bioethanol production in the period from 2001 to 2012, shown in Fig. 3.2, reveal that cost reduction up to a factor of four to five could be achieved due to technical learning over such a long time period. That may also be achievable for the production of higher value-added products in the next decade.

For the production of cellulosic ethanol, cost reduction was mainly achieved through technological improvements in the areas of pretreatment and conditioning, enzymatic hydrolysis (and associated improvements in enzyme performance reflecting commercial enzyme package improvements), and fermentation, while the feedstock cost contributions to ethanol SP remained relatively constant.

For 1G biofuels, feedstock significantly influences production costs, whereas for 2G biofuels, the share decreases and becomes less than 40% (Hamelinck et al., 2005). The production cost of ethanol from cellulosic biomass is sensitive to economy of scale (Argo et al., 2013; Muth et al., 2014). However, the optimal size of biorefineries depends also upon the nature of the feedstock. Preprocessed feedstock in depot systems enables larger biorefinery sizes—at least conceptually but might compromise greenhouse gas emission (GHG)-reduction targets (Muth et al., 2014).

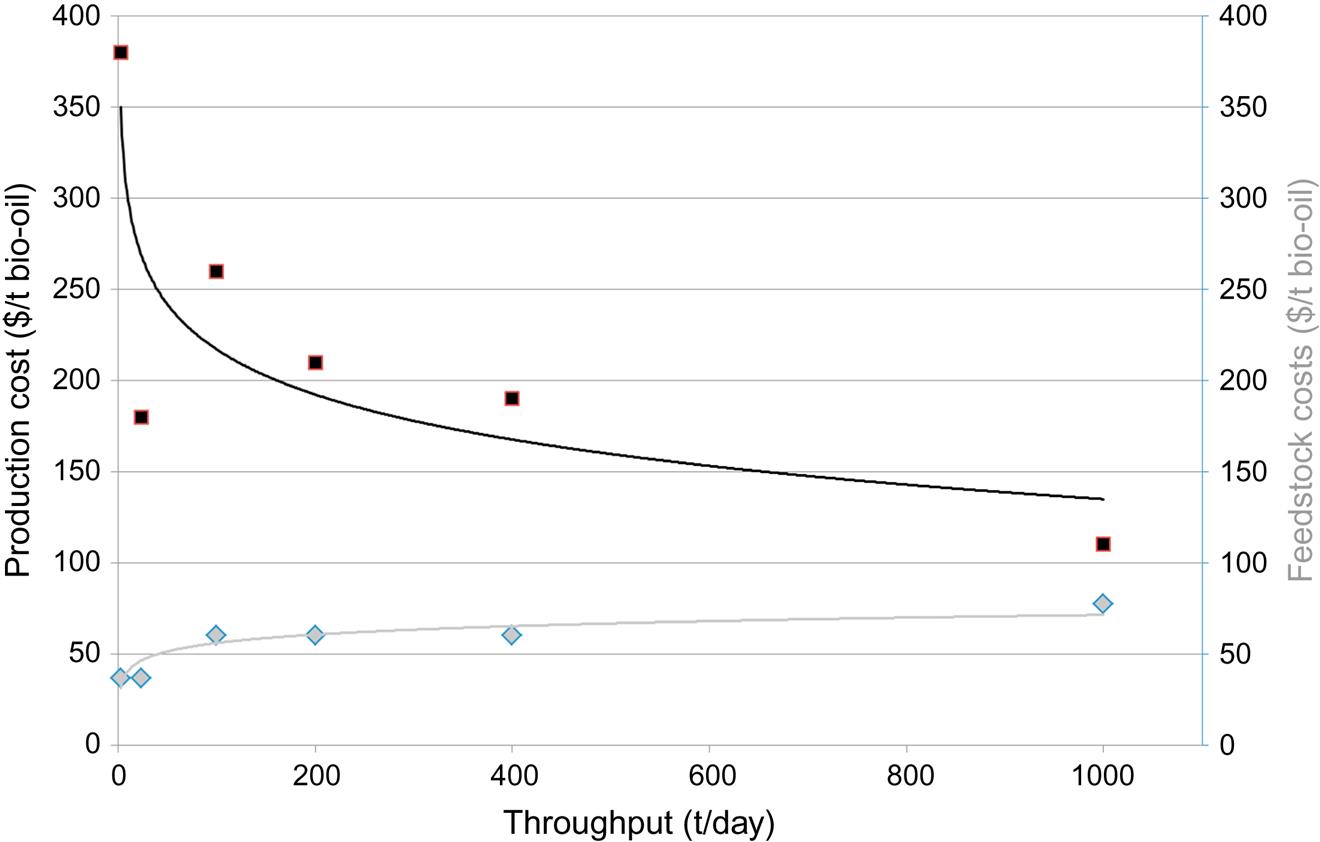

For processes dealing with high volumes of raw material and high capital costs, marginal changes in feedstock cost (including transport) can make the difference. Therefore, in assessing the economic viability of a lignocellulose biorefinery, trade-off between plant size and feedstock delivery costs must be taken into account. Ringer et al. (2006) provided scale-dependeny cost information on the production of bio-oil from wood chips.

Fig. 3.3 shows that the specific production costs decrease with scale, although the feedstock costs increases mainly due to transport costs. There is obviously a limit, where cost reduction due to technological progress is compensated by increasing cellulosic feedstock (and transport) cost (Argo et al., 2013). Transport costs can vary substantially. Estimation of feedstock cost is not straightforward due to the lack of formal markets for a large part of possible feedstock and due to site-specific availability and procurement constraints. This aspect is discussed in detail in chapters “Biomass Supply and Trade Opportunities of Preprocessed Biomass for Power Generation” and “Commodity Scale Biomass Trade and Integration With Other Supply Chains.”

Currently, the production of hydrocarbons from cellulosic feedstock is not cost-competitive to hydrocarbons from crude oil. Davis et al.(2013) summarize their findings as: “Tailoring the hydrolysate stream to the microorganism tolerance will be essential for improving overall yields and lowering production costs. Reduction of hydrolysate conditioning costs could also be realized through a better understanding of the tolerance of hydrocarbon-producing microbes to lignin and other cellulosic sugar substrate impurities and other potential inhibitors. There are several optimization possibilities that are suitable to reduce the production costs, for example, improving conversion efficiency of underutilised fractions of the biomass (mainly hemicellulose) or conversion of lignin to higher value-added products.” However, the latter would require the replacement of lignin by other energy carriers and that might lead to a trade-off between maximizing the GHG savings and reducing the production costs. Currently, lignin is mostly used as fuel on-site to cover the heat and/or power demand of the biorefinery.

For the techno-economic evaluation of innovative industrial processes, often limited data are available. The economic assessment of biorefineries depends on a number of factors such as feedstock costs (Argo et al., 2013; Muth et al., 2014), specific preprocessing and process equipment (Muth et al., 2014), plant capacity, etc. Moreover, some of those factors are site-specific, for example, feedstock logistics, process waste utilization, integration in existing installations, etc. Economic estimations have been conducted for green biorefineries in Ireland (O’Keeffe et al., 2011, 2012) and elsewhere (Höltinger et al., 2014), sugar cane biorefineries in Brazil (Cavalett et al., 2012), for thermochemical production of biofuels (Bridgwater, 2009; Reyes Valle et al., 2015), the production of advanced biofuels (Turley et al., 2013), lignocellulosic biorefineries (Kazi et al., 2010; Benali et al., 2014; Cheali et al., 2015), integrating bioethanol production into Kraft pulp and paper mills (Hytönen, 2009) but also for biorefinery-relevant separation techniques (Sievers et al., 2014) and pretreatment techniques (García et al., 2011). The results of the studies are hardly comparable because assumptions such as interest rate, equipment lifetime, and modeling approaches are different.

Investment cost estimations are mostly point estimates and do not take the uncertainties inherent in the methodology into account. The accuracy of the result depends on the quality of the input data and the calculation approach. Brown (2015) has recently reviewed techno-economic studies of thermochemical cellulosic biorefinery and conducted a sensitivity analysis based on economic data available in the public domain. He concluded that the choice of estimation methodology differs across the techno-economic assessments and has a substantial impact on the final result. The difference of capital investment costs of a biorefinery with a capacity of 2000 t/day can be as high as US$ 300,000 million depending on the chosen estimation method and assumptions (Brown, 2015). Therefore, it is important to assess the uncertainty by sensitivity analysis if estimation methods are used for supporting decision making.

Daugaard et al. (2015) discuss how increasing biorefinery capital and feedstock learning rates could significantly reduce optimal size and production costs of biorefineries. The authors suggest that there is an economic incentive to invest in strategies that increase the learning rate for producing advanced biofuels.

3.3 Demonstration and Full-Scale Plants

The large-scale production of biobased products via fermentation of lignocellulosic-derived sugars is still in its infancy; except for bioethanol. Thermochemical conversion of lignocellulosic biomass at a largescale is more targeted to produce biofuels than biobased chemicals. Fast pyrolysis is probably the most interesting thermochemical conversion technology because the yield of bio-oil is high and it can be used both for energy and/or chemicals production.

3.3.1 Fast Pyrolysis: Current Status

Currently, the main objective of fast pyrolysis is to produce bio-oil that can be directly used in stationary boilers or in the near future after hydrogenation as transportation fuel. In the mid-term bio-oil could also be used as drop-in (after partial upgrading) in naphtha-crackers of conventional refineries or even as source for chemicals. The technological development in the area of fast pyrolysis of mainly woody biomass is driven by the demand for 2G biofuels.

3.3.1.1 Ensyn Corp (ENSYN, 2014)

Ensyn Corp (Canada) is executing its renewable fuels business in alliance with UOP, a Honeywell company. This alliance takes place through Envergent Technologies, LLC (Envergent), a joint venture between Ensyn and UOP.

A pyrolysis oil demonstration project at Manitoba Hydro involved the production and use of pyrolysis oil as a replacement for heavy fuel at the Tolko Kraft Paper Mill in The Pas, Manitoba. The equipment and services are provided by Ensyn Technologies Ltd. The cofiring demonstration plant successfully fired over 60,000 L of bio-oil in 2010 with stable combustion. Extensive emissions monitoring indicated improvements in boiler performance. A second demonstration is planned for a grain-drying operation where bio-oil will replace propane (Manitoba, 2014).

Recently, Memorial Hospital in North Conway, New Hampshire, shifted from petroleum to Ensyn’s Renewable Fuel Oil (RFO) for their heating system. RFO is certified according to ASTM D7544-10 (Standard Specification for Pyrolysis Liquid Biofuel), which ensures the highest levels of quality, reliability, and performance when used as a fuel in industrial burners.

Ensyn is supplying Memorial Hospital with 300,000 gallons/year of Ensyn’s RFO cellulosic biofuel under a 5-year, renewable contract. This contract allows the hospital to fully replace its petroleum fuels with Ensyn’s renewable fuel, and reduce its GHG emissions from heating by approximately 85%. Memorial Hospital’s boiler has been operating successfully on 100% RFO since September 2014.

Lastly, in early October 2014, Ensyn announced a 7-year renewable contract to supply Valley Regional Hospital in Claremont, New Hampshire, with 250,000 gallons/year of RFO. Under this contract, the hospital intends to replace its entire heating fuel requirements with Ensyn’s RFO. Deliveries are expected to begin in April, 2015.

Ensyn also provided Petrobas with bio-oil from spruce for test trials at demo-scale. Bio-oil was directly coprocessed in a fluid catalytic cracking (FCC) unit without any type of hydrodeoxygenation and with a regular gasoil FCC feed up to 20%wt. The bio-oil and the conventional gasoil were cracked into valuable products such as LPG and gasoline (Pinho et al., 2015).

3.3.1.2 KIT (Bioliq)3

The bioliq process, developed at the Karlsruhe Institute of Technology (KIT), aims to produce synthetic fuels and chemicals from biomass (Dahmen et al., 2012). This process requires a feed that can easily be fed to the gasifier at elevated pressures being atomized by oxygen as the gasification agent. Fast pyrolysis was chosen as the most promising process to produce this feed, by mixing pyrolysis condensates and char to a so-called bioliqSyncrude, exhibiting a sufficiently high heating value, and being suitable for transport, storage, and processing. This slurry-gasification concept has been extended to a complete process chain via an on-site pilot plant erected KIT.

The three subsequently constructed parts of the plant, funded by the German Ministry of Food, Agriculture, and Consumer Protection, consist of the fast pyrolysis and biosyncrude production, the 5 MWth high-pressure entrained-flow gasifier operated at up to 8 MPa (both in cooperation with Lurgi GmbH, Frankfurt), as well as the hot gas cleaning (MUT Advanced Heating GmbH, Jena), dimethylether, and final gasoline synthesis (Chemieanlagenbau Chemnitz GmbH).

The technical concept of the pilot plant is based on the Lurgi-Ruhrgas mixer reactor, previously devoted to coal degassing or heavy crude coking. The actual flow scheme is depicted in Fig. 3.4. In November 2014, the whole process chain was demonstrated successfully at KIT and the first synthetic fuel was produced.

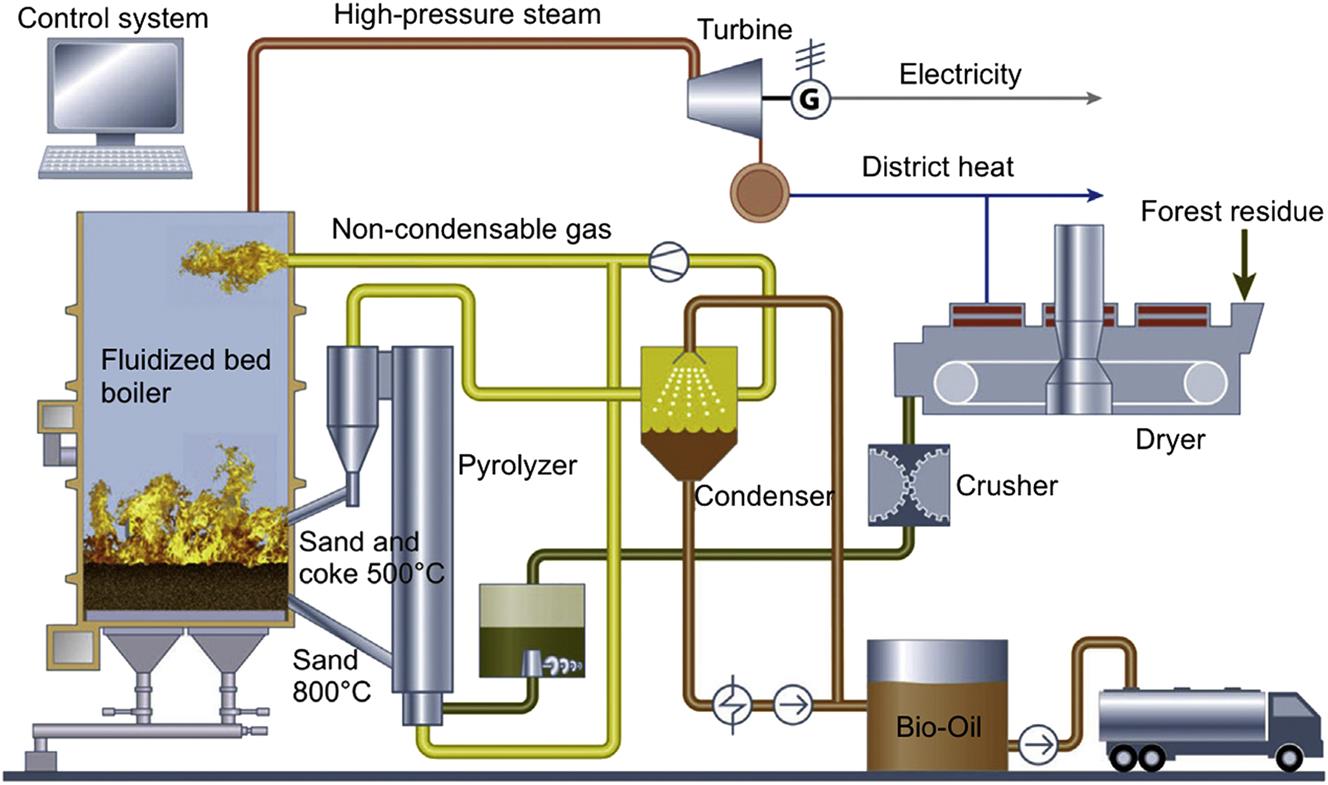

3.3.1.3 Fortum

The new technology has been developed into a commercial-scale concept in cooperation between Fortum, Metso, UPM, and VTT as part of TEKES Biorefine research program. Fortum commissioned a first-of-its-kind fast pyrolysis plant in 2013, which has been operating since 2014. It was the first-of-its-kind at commercial scale and is shown in Fig. 3.5. The bio-oil plant is integrated with existing combined heat and power production and an urban district heating network in Joensuu, Finland. Wood chips from forest residues are dried and then fine-milled before they are fed into the pyrolysis reactor together with hot sand. The bio-oil production capacity is 50,000 t/year. The bio-oil and the char are conveyed to the CHP unit, where the bio-oil replaces heavy fuel oil. The steam is used the district heating network and surplus electricity is fed into the national grid. This helps to reduce CO2 emissions by 59,000 t/year and SO2 emissions by 320 t/year.

3.3.1.4 BTG BioLiquids BV

BTG BioLiquids BV (BTG-BTL) was established to commercialize the fast pyrolysis technology developed by BTG. The business model is to operate as a technology supplier, supplying the core components of the pyrolysis unit. A demonstration unit on a commercial scale was required to prove both the technology and the complete pyrolysis chain.

The core conversion process is a flash pyrolysis process based on BTG technology with a rotating cone. The feedstock will be crushed pellets imported from the USA and Canada via the port of Rotterdam. Excess heat will be converted into process steam to drive a steam turbine for electricity generation. Part of the low-pressure steam will be used to dry the biomass, while excess steam will be sent to AkzoNobel. The oil produced will be cofired in a novel modified gas burner at Royal Friesland Campina NV, a global dairy company. Pyrolysis off-take agreement concluded for a period of 12 years, equivalent to approximately 200 million liters (EMPYRO, 2014).

3.3.1.5 EMPYRO

Energy and Materials from Pyrolysis (EMPYRO) uses BTG fast pyrolysis technology. In May 2015 a fast pyrolysis plant started operating in Hengelo, Netherlands. In the plant, 5 t/hour of clean wood will be converted into about 3.2 t/hour of bio-oil. Excess heat generated from the combustion of the byproducts (gas and char) is used to provide heat for the biomass dryer, and to run a steam turbine to generate electricity. EMPYRO received an NTA8080 certificate, which is recognized by the EU Commission to demonstrate compliance with the European sustainability requirements for biofuels.

The produced bio-oil is sold to FrieslandCampina that uses the bio-oil as boiler fuel in their milk powder production site in Borcula as a substitute for natural gas in order to reduce GHG emissions.

The production capacity of the EMPYRO plant will gradually increase to its maximum of over 20 million liters of bio-oil annually.

3.3.2 Biochemical Conversion

Theoretically, the source of sugar is irrelevant for the fermentation process (whether derived from sugar cane, sugar beet, or lignocellulose), provided the sugar solution contains a suitable composition of sugars and does not contain inhibitors. However, specific microorganisms have specific requirements; they cannot use all sugars, are differently robust and produce distinguished products. Therefore, there are a number of possible combinations of feedstock, pretreatment options, and microorganisms, sometimes even to produce the same product.

3.3.2.1 Bioethanol Production

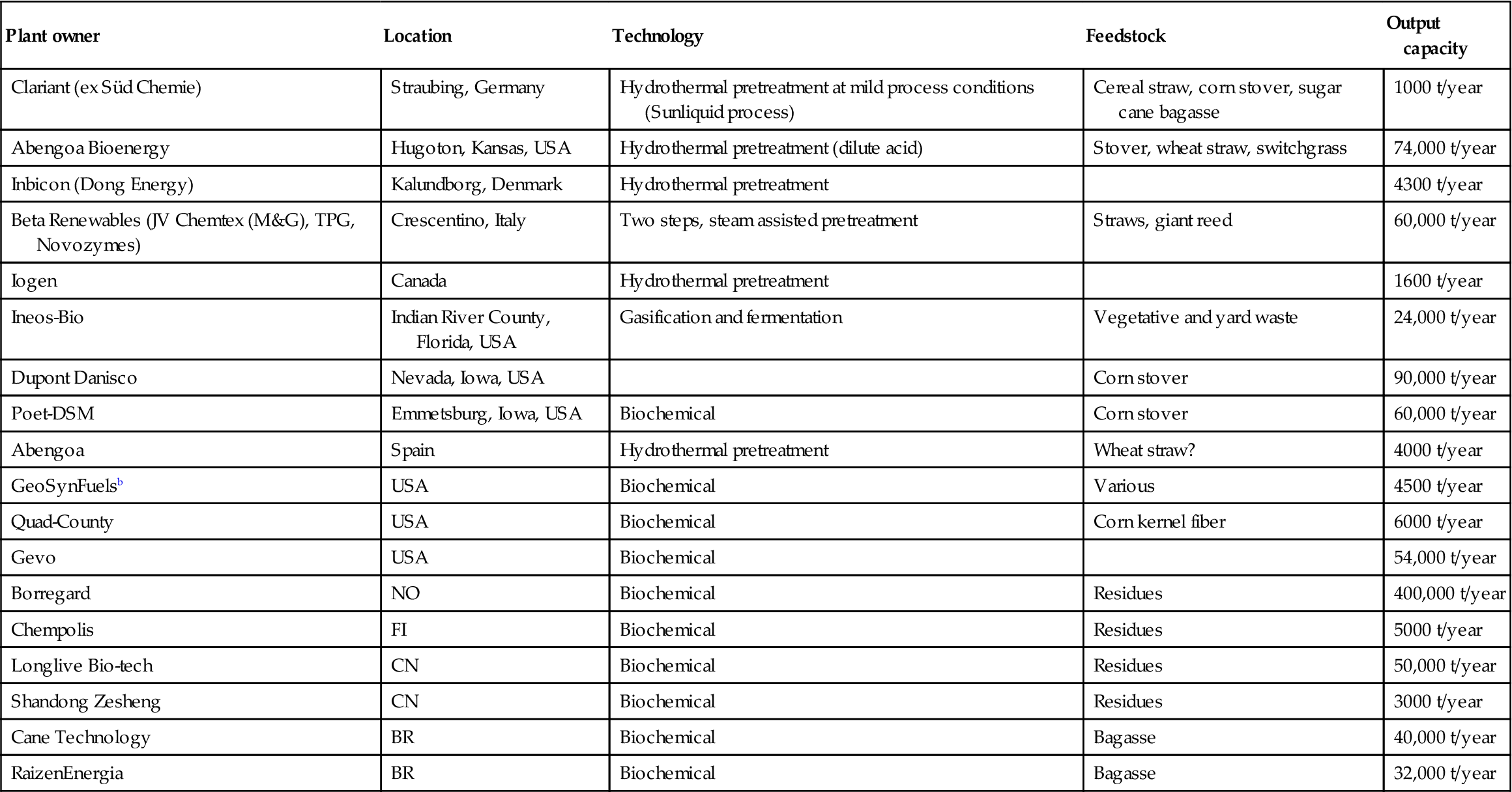

The use of lignocellulose-derived sugars is driven by the increasing demand for 2G bioethanol. Producing suitable sugar solutions from lignocellulosic feedstock, especially for the production of biochemicals, is still a challenge, although significant progress has been made in recent years. A number of demonstration plants for the production of 2G bioethanol have been built in order to investigate scale-up effects. The majority of these plants, mentioned in Table 3.2, use either hydrothermal or steam-assisted pretreatments.

Table 3.2

Selected second-generation ethanol operational in 2015 exceeding 1000 metric t/year of producta

| Plant owner | Location | Technology | Feedstock | Output capacity |

| Clariant (ex Süd Chemie) | Straubing, Germany | Hydrothermal pretreatment at mild process conditions (Sunliquid process) | Cereal straw, corn stover, sugar cane bagasse | 1000 t/year |

| Abengoa Bioenergy | Hugoton, Kansas, USA | Hydrothermal pretreatment (dilute acid) | Stover, wheat straw, switchgrass | 74,000 t/year |

| Inbicon (Dong Energy) | Kalundborg, Denmark | Hydrothermal pretreatment | 4300 t/year | |

| Beta Renewables (JV Chemtex (M&G), TPG, Novozymes) | Crescentino, Italy | Two steps, steam assisted pretreatment | Straws, giant reed | 60,000 t/year |

| Iogen | Canada | Hydrothermal pretreatment | 1600 t/year | |

| Ineos-Bio | Indian River County, Florida, USA | Gasification and fermentation | Vegetative and yard waste | 24,000 t/year |

| Dupont Danisco | Nevada, Iowa, USA | Corn stover | 90,000 t/year | |

| Poet-DSM | Emmetsburg, Iowa, USA | Biochemical | Corn stover | 60,000 t/year |

| Abengoa | Spain | Hydrothermal pretreatment | Wheat straw? | 4000 t/year |

| GeoSynFuelsb | USA | Biochemical | Various | 4500 t/year |

| Quad-County | USA | Biochemical | Corn kernel fiber | 6000 t/year |

| Gevo | USA | Biochemical | 54,000 t/year | |

| Borregard | NO | Biochemical | Residues | 400,000 t/year |

| Chempolis | FI | Biochemical | Residues | 5000 t/year |

| Longlive Bio-tech | CN | Biochemical | Residues | 50,000 t/year |

| Shandong Zesheng | CN | Biochemical | Residues | 3000 t/year |

| Cane Technology | BR | Biochemical | Bagasse | 40,000 t/year |

| RaizenEnergia | BR | Biochemical | Bagasse | 32,000 t/year |

aMost information taken from www.biofuelstp.eu/spm5/pres/monot.pdf and http://demoplants.bioenergy2020.eu/, accessed July 2015.

bDemoplant brought from Blue Sugars Corporation in 2014.

In addition to the initiatives listed in Table 3.2, there are several other industrial initiatives focused on the production of 2G ethanol. In 2012, Beta Renewables inaugurated the world’s first commercial biorefinery plant in northern Italy, producing 40,000 t/year bioethanol from straw and Arundo donax. In Brasil, a Beta Renewables plant producing 65,000 t/year bioethanol was built in cooperation with GranBio. The construction of a similar biorefinery by Beta Renewables in North Carolina, USA, is ongoing. Novozymes and Beta Renewables also announced their plans to construct a cellulosic ethanol facility in India. A joint venture between Anhui Guozhen Co and Beta Renewables plans to convert 970,000–1,300,000 t/year of agricultural residues into cellulosic ethanol, glycols, and byproducts such as lignin in Fuyang City (Anhui Province, PRC).

3.3.3 Biorefineries: Starch/Sugar-Based

Biobased chemicals and biofuels must compete on cost and performance with petrochemicals and petroleum fuels. At present, most chemical-producing biorefineries use starch or sugar as the major feedstock.

BASF, Novozymes, and Cargill jointly developed 3-hydroxypropionicacid a raw material for the production of biobased acrylic acid, in pilot scale.4 On the other hand, OPX Biotechnologies with its partner Dow Chemicals is aiming to commercialize bio acrylic acid by 2017. Their process is based on the direct conversion of dextrose (corn) or sucrose (cane) through genetically engineered E-Coli1/2 via OPXBIO EDGE Technology Platform. The global acrylic acid market is forecast to reach US$18.8 billion by 2020 from US$11 billion in 2013, corresponding to a global consumption of acrylic acid of 8.2 million t/year.5 OPXBio said it was already able to produce 38 cents/lb bioacrylic acid using sucrose feedstock at 8 cents/lb. The company plans to have a demonstration plant with a capacity of 600,000 lb/year in 2013.6 A commercial plant with a capacity of 100 million lb/year is expected by 2015.

Succinic acid has received increasing attention for the production of new polyesters with good mechanical properties combined with full biodegradability. The main actors are probably Succinity GmbH (a Corbion Purac and BASF joint venture) with a commercial production facility in Montmeló, Spain, and Reverdia (a joint venture between Roquette and DMS) with a commercial facility in CassanoSpinola, Italy. Both plants have a production capacity of about 10,000 t/year. In Canada, BioAmber, in collaboration with Mitsui & Co., is constructing a biobased succinic acid production plant at a bioindustrial park owned by Lanxess in Sarnia, Ontario. The plant will initially have a production capacity of 17,000 t/year. The capacity will be increased by a further 35,000 t/year and at the same site it is scheduled to produce 23,000 t/year of 1,4-butanediol.7 The estimated cost for the construction of the plant is US$110 million. For the production of succinic acid BioAmber wants to use a variety of feedstock, for example, corn, wheat, cassava, rice, sugarcane, sugar beet, and forest waste. The feedstock will initially be transported by trucks to a wet mill facility, where it will be processed into glucose (dextrose) sirup and other valuable coproducts. The glucose will then be transported to the Sarnia plant, where it will be fermented to raw biobased succinic acid and later purified to crystalline biobased succinic acid before being shipped. Costs of succinic acid production strongly depend on the plant size. Some investigations indicate a cost of US$ 2.20 (€ 1.96) per kg at the 5000 t/year. Liu (2000) estimated that the price can be lowered to US$ 0.55 (€ 0.50) per kg at a production capacity of 75,000 t/year. At present, succinic acid is mostly produced by the chemical process from n-butane through maleic anhydride. The incidence of the raw material cost can be estimated in US$ 1.027 per kg. On the other hand, glucose is sold at a price of about $0.39 per kg, and assuming the succinic acid yield of 91% (w/w) on glucose, the raw material cost in the bioprocess is then $0.428 per kg (Song and Lee, 2006). Thus fermentative production of succinic acid from renewable resources can compete with the chemical process.

NatureWorks produces polylactic acid (PLA) at a plant with a designed capacity of 140,000 t/year in 2003; its current capacity is 150,000 t/year. Total investment costs have been US$ 300 million in hardware and US$450 million in R&D, process development, and technical support.8 The current price of PLA is higher than the average cost of polyolefin (0.4–0.7 € per kg).9 On an industrial scale, producers are seeking a target manufacturing cost of lactic acid monomer to less than US$ 0.8 per kg because the SP of PLA should decrease roughly by half from its present price of US$ 2.2 per kg.10 This example shows that biobased materials are perceived as greener and therefore bought despite a higher price.

The European Commission Directorate-General Energy has released a report titled “From the Sugar Platform to Biofuels and Biochemical,” where product prices and market volumes are depicted; some of these are shown in Table 3.3.

Table 3.3

Estimated prices of biobased products and market volumes as recently assessed in a final report for the European Commission (E4tech et al., 2015)

| Product | Price ($ per t) | Volume (1000 t/year) | % of total market |

| Bioethanol | 815 | 71,310 | 93 |

| BDO | >3000 | 3.0 | 0.1 |

| n-butanol | 1890 | 590 | 20 |

| Succinic acid | 2940 | 38 | 49 |

| Xylitol | 3900 | 160 | 100 |

| Farnesene | 5581 | 12 | 100 |

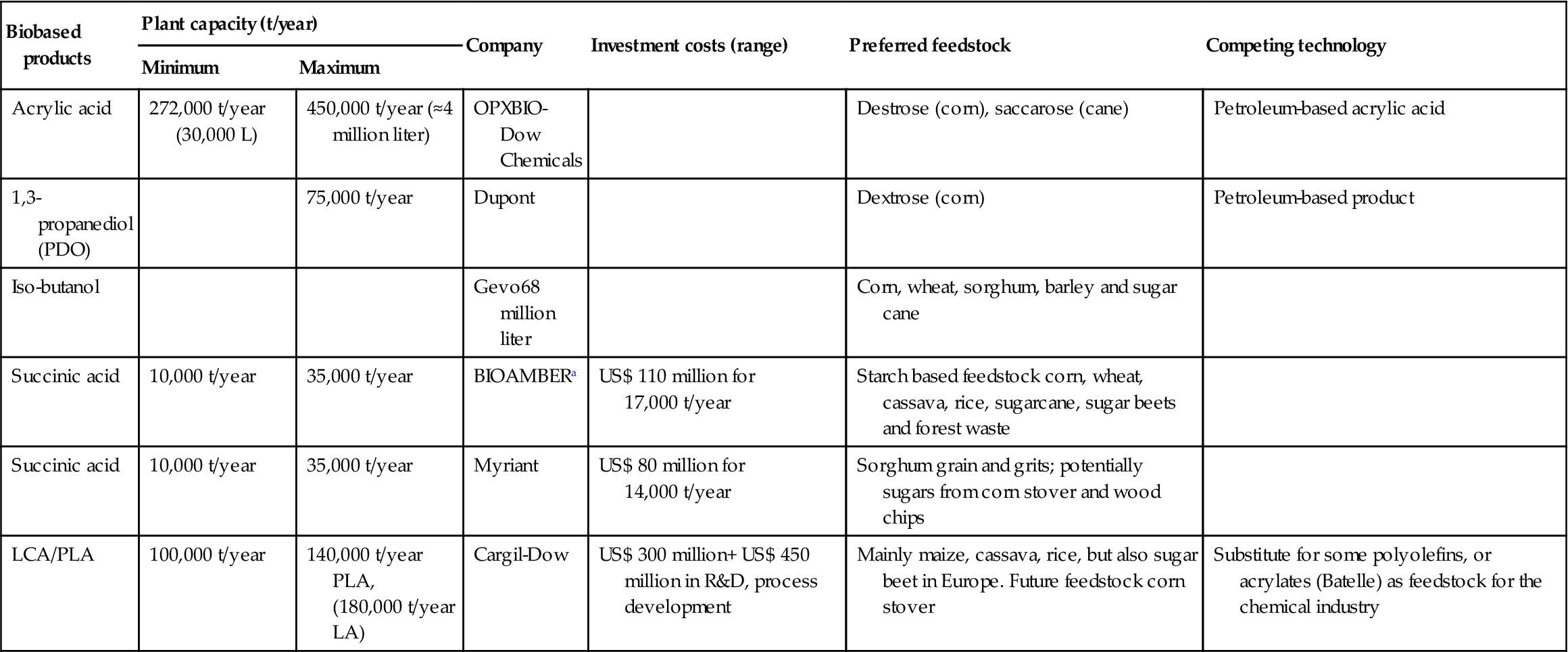

Selected chemicals produced at a large scale and briefly described above are shown in Table 3.4.

Table 3.4

Selected biobased chemicals produced at a large scale

| Biobased products | Plant capacity (t/year) | Company | Investment costs (range) | Preferred feedstock | Competing technology | |

| Minimum | Maximum | |||||

| Acrylic acid | 272,000 t/year (30,000 L) | 450,000 t/year (≈4 million liter) | OPXBIO-Dow Chemicals | Destrose (corn), saccarose (cane) | Petroleum-based acrylic acid | |

| 1,3-propanediol (PDO) | 75,000 t/year | Dupont | Dextrose (corn) | Petroleum-based product | ||

| Iso-butanol | Gevo68 million liter | Corn, wheat, sorghum, barley and sugar cane | ||||

| Succinic acid | 10,000 t/year | 35,000 t/year | BIOAMBERa | US$ 110 million for 17,000 t/year | Starch based feedstock corn, wheat, cassava, rice, sugarcane, sugar beets and forest waste | |

| Succinic acid | 10,000 t/year | 35,000 t/year | Myriant | US$ 80 million for 14,000 t/year | Sorghum grain and grits; potentially sugars from corn stover and wood chips | |

| LCA/PLA | 100,000 t/year | 140,000 t/year PLA, (180,000 t/year LA) | Cargil-Dow | US$ 300 million+ US$ 450 million in R&D, process development | Mainly maize, cassava, rice, but also sugar beet in Europe. Future feedstock corn stover | Substitute for some polyolefins, or acrylates (Batelle) as feedstock for the chemical industry |

aUnder construction.

3.4 Summary and Outlook

Results presented in this review are based on a diverse array of literature studies that include numerous, and sometimes differing, assumptions. The data quality of the literature sources used in this study is not homogeneous, and that causes an inherent uncertainty about the actual performance of the different pretreatment and conversion technologies when implemented at a large scale.

Fossil-based fuels and materials have a higher dependency on oil prices than their bio-counterparts. Most recently oil prices have been rather volatile, for example, in 2009 the average oil price was at US$ 60 per barrel, in 2011 at US$ 105 per barrel, and in January 2015 below US$ 50 per barrel. Hence, it is extremely difficult to forecast at which oil price biobased products become cost-competitive incomparison with their fossil counterparts. As a rule of thumb cost-competitiveness of biobased products increases with increasing oil price and decreasing feedstock costs. Currently, the production of bioenergy and biofuels is subsidized in many countries (Kraxner et al., 2013). However, the utilization of biomass in biorefineries seems to provide higher value creation in the long term and is more sustainable than the production of bioenergy and/or biofuels alone. There are various strategies but there are no distinct policy drivers for the utilization of biobased chemicals, in direct contrast to the biofuels industry where various national regulations are driving rapid growth (Hermann et al., 2011). However, rapid growth in lignocellulosic feedstock utilization will require changes in the supply chain infrastructure and may also need more efficient socioeconomic and policy frameworks (Richard, 2010), for example, an expanded policy that includes biobased products provides added flexibility without compromising GHG targets (Posen et al., 2014).

Currently, no biomass pretreatment technology able to convert lignocellulosic biomass into sugars for fermentation is cost-competitive with conventional sugar. There is no single preferred pretreatment method, with mild acid hydrolysis and steam explosion, dilute and concentrated acid, and mild alkaline processes all planned to be used in biofuel plants in the near future.

Fermentation of low-cost sugar is economically the most attractive option for the production of biofuels and other biorefinery products, particularly PLA and succinic acid (Posada et al., 2013; Gerssen-Gondelach et al., 2014). The integration of different pretreatment and conversion technologies in biorefineries can maximize the use of all biomass components and improve both the economic and the ecological efficiency of the whole value chain. However, eco-efficient biobased value chains call for different ways of thinking about agriculture, energy infrastructure, processing industry, and rural economic development. A key challenge for developing and growing a commercially secure bioeconomy is a reliable and consistent feedstock supply.

In the longterm, thermochemical and biochemical conversion of lignocellulosic biomass are promising technologies for the production of biofuels and biobased chemicals. Realizing the long-term opportunities of lignocellulosic biomass conversion depends both on technological learning and fossil fuel prices (Saygin et al., 2014). Some chemical companies may also be keen to decouple their base and intermediate materials from fossil-based sources.

At present, the bioeconomy is a political concept and efforts from all actors are required for its realization. The pace of large-scale implementation of biorefineries depends not just on the environmental and economic performance of pretreatment and conversion technologies, but also on governmental policy framework and societal preferences. It is unlikely that a single solution or policy will determine the extent to which biorefineries are incorporated into a global biobased economy. Rather, it is likely that a robust portfolio of solutions, appropriate for site-specific conditions (eg, feedstock availability, supply chain infrastructure, rural development strategies, etc.), will be needed to sustainably address the future material and energy demand (Wilcox, 2014).