Transition Strategies

Resource Mobilization Through Merchandisable Feedstock Intermediates

P. Lamers, E. Searcy and J.R. Hess, Idaho National Laboratory, Idaho Falls, ID, United States

Abstract

A variety of feedstock types will be needed to grow the bioeconomy. Respective logistics and market structures will be needed to cope with the spatial, temporal, and compositional variability of these feedstocks. At present, pilot-scale cellulosic biorefineries rely on vertically integrated supply systems designed to support traditional agricultural and forestry industries. The vision of the future feedstock supply system is a network of distributed biomass processing centers (depots) and centralized terminals. This introduces methods to increase feedstock volume while decreasing price and quality supply uncertainties. Depots are located close to the resource, while shipping and blending terminals are located in strategic logistical hubs with access to high bulk transportation systems. The system emulates the current grain commodity supply system, which manages crop diversity at the point of harvest and at the storage elevator, allowing subsequent supply system infrastructure to be similar for all resources. The initiation of depot (pilot) operations is seen as a strategic stepping stone to transition to this logistic system. A fundamental part of initiating (pilot-) depot operations is to establish the value proposition to the biomass grower, as biomass becomes available to the market place only through mobilization. A feedstock supply industry independently mobilizing biomass by producing value-add merchandisable intermediates creates a market push that will derisk and accelerate the deployment of bioenergy technologies. Companion markets can help mobilize biomass without biorefineries. That is, depots produce value-added intermediates that are fully fungible in both a companion and the biorefining market. To achieve this, a separation between feedstock supply and conversion industry may be necessary.

Keywords

Biorefinery logistics; depot; market transition; resource mobilization; feedstock quality

8.1 Objective and Link to Previous Chapters

Building on the analyses done in earlier chapters, this chapter details and discusses transition strategies to bridge the current cellulosic biorefinery feedstock supply system, based on low energy and low bulk density, instable formats (eg, bales), to an advanced feedstock supply system, entailing merchandisable intermediates of high energy and bulk density that are stable and flowable (eg, pellets).

In chapter “Biomass Supply and Trade Opportunities of Preprocessed Biomass for Power Generation,” Batidzirai et al. show that feedstock supply systems benefit from preprocessing, such as densification, which increases bulk and energy density but also improves flowability, physical homogeneity, and storability. This reduces transport costs and greenhouse gas (GHG) emissions per energy unit, allowing an increased sourcing radius. International sourcing is already established industry practice in today’s biopower and “first-generation” biofuel industries. The biofuel industry, relying on oil, starch, and sugar crops, has seamlessly integrated with the existing grain, vegetable oil, and sugar logistics supply chains. The cellulosic biofuel industry however still relies on regional, conventional logistic patterns and market structures (eg, direct, annual contracts with growers). The biopower industry finds itself in between these extremes. While wood pellets fulfill requirements for density, stability, flowability, etc., international sourcing is not yet organized in a commodity market. In fact, as shown by Olsson et al. in chapter “Commoditization of Biomass Markets,” an early commodity exchange platform for wood pellets in Rotterdam failed. At this stage, wood pellet supply contracts are directly agreed between buyer (energy utility) and seller (producer).

To reach a competitive minimum fuel selling price (MFSP), cellulosic biorefineries will require economies of scale. The scale-up of current, first-of-a-kind plants will depend on the ability of the logistics system to supply large quantities of homogeneous feedstock intermediates to allow for a continuous operation. The transition towards such a system will need to bridge logistical as well as market structures. In chapter “Commodity-Scale Biomass Trade and Integration With Other Supply Chains,” Searcy et al. provide several suggestions on how existing supply chains could be utilized by the feedstock industry. Olsson et al. address market structures in chapter “Commoditization of Biomass Markets.” This chapter builds upon these analyses and lays out specific logistical and market stepping stones to bridge the current to a future bioeconomy feedstock supply system.

8.2 Challenges Within Large-Scale Biorefinery Feedstock Supply Chains

Concerns about the sustainability of food and fodder crop-based biofuels (see chapter: “Sustainability Considerations for the Future Bioeconomy” for details) have spurred the promotion of advanced biofuels, part of the future bioeconomy, which focus on nonfood or feed biomass resources such as residual biomass from agricultural, forestry, and other industry operations (eg, municipal solid waste); energy crops; or woody biomass. Harvest operations in agriculture and forestry, however, are aimed to maximize the yield of the target crop (eg, grain), not the residual fraction. This implies that residual biomass is highly variable both spatially and temporally (Kenney et al., 2013); which has implications for the operation of large-scale biorefineries that have a relatively constant demand. Some of the critical uncertainty factors in cellulosic biofuel supply chains, influencing the effectiveness of their configuration and coordination in the system, include uncertainty with respect to feedstock supply quantity, quality, and price (influenced by weather, etc.), biorefinery demand fluctuations linked to biofuel and oil price changes, as well as regulatory and policy changes (see also Sharma et al., 2013). An overview of potential challenges is presented in Table 8.1.

Table 8.1

Summary of the challenges associated with biomass supply chain operations

| Challenges | Description of issues |

| Technical and technological | Geospatial and temporal variability of biomass |

| Compositional variability of biomass | |

| Biomass quality impacts conversion yields | |

| Current supply chains are designed around high-value agriculture and forestry products, not around optimizing residue extraction | |

| Financial | High capital costs (CAPEX) |

| Drive to reduce CAPEX (smaller plants) vs. economies of scale (larger plants) | |

| Technical complexity limiting access to finance | |

| Risks associated with new technologies (insurability, performance, rate of return) | |

| Extended market volatilities (energy and food markets) | |

| Social | Potential health and safety risks |

| Pressure on transport sector | |

| Public acceptance (“Not-In-My-Backyard”) | |

| Environmental | Consistent, international sustainability frameworks and respective governance |

| Safeguarding of best management practices (BMP) | |

| Safeguarding GHG benefits across the whole supply chain | |

| Safeguarding water and soil conservation | |

| Policy and regulatory | Impact of fossil fuel tax on biomass transport |

| Underestimation of feedstock challenges | |

| Heavy focus on solving technological issues, limited attention to market barriers (eg, fossil fuel subsidies) | |

| Institutional and organizational | Varied ownership arrangements and priorities among supply chain parties |

| Lack of feedstock supply cooperatives | |

| Limited number of success stories | |

| Growers and traders are reluctant to expand their portfolio to include lesser value products (eg, cellulosic biomass) without dedicated, multiple markets to sell to |

8.3 Feedstock Supply System Types: Conventional and Advanced

Feedstock variability with respect to quantities and resulting changes in supply costs (ie, prices) are largely associated with irregular harvest volumes, linked to inclement weather (eg, droughts) and other conditions affecting harvest timing. Variations in quality, particularly for agricultural residues, are linked to natural, compositional and introduced variability. Empirical data for corn stover, for example, suggests that the harvest year has the strongest effect on compositional variation (eg, physiological ash or carbohydrate content), followed by location and plant variety (Templeton et al., 2009). Harvest practices add an additional layer of complexity. For instance, single-pass harvest where combine and baling operation are done at once and the residue does not touch the ground, ash contamination (ie, introduction of soil) is significantly reduced in comparison to conventional, multipass harvest, where a separate combine and baling operation takes place (Hess et al., 2009).

To supply a national or global bioeconomy, logistics and market structures will need to address and cope with the spatial, temporal, and compositional variability of biomass. Only a reduction of this variability, that is, a constant, large quantity supply within quality specifications, can guarantee stable and high conversion yields necessary for a viable business operation such as a cellulosic biorefinery relying on these supply streams.

At present however, pilot-scale cellulosic biofuel production facilities rely on vertically integrated feedstock supply systems designed to support traditional agricultural and forestry industries, hereafter referred to as conventional systems, where feedstock (predominantly agricultural residues such as wheat straw and corn stover) is procured through contracts with local growers, harvested, locally stored, and delivered in low-density format to the nearby conversion facility (Fig. 8.1). These conventional systems were designed to support traditional agricultural and forestry industries. The conventional system has been demonstrated to work in a local supply context within concentrated supply regions (eg, the US Corn Belt).

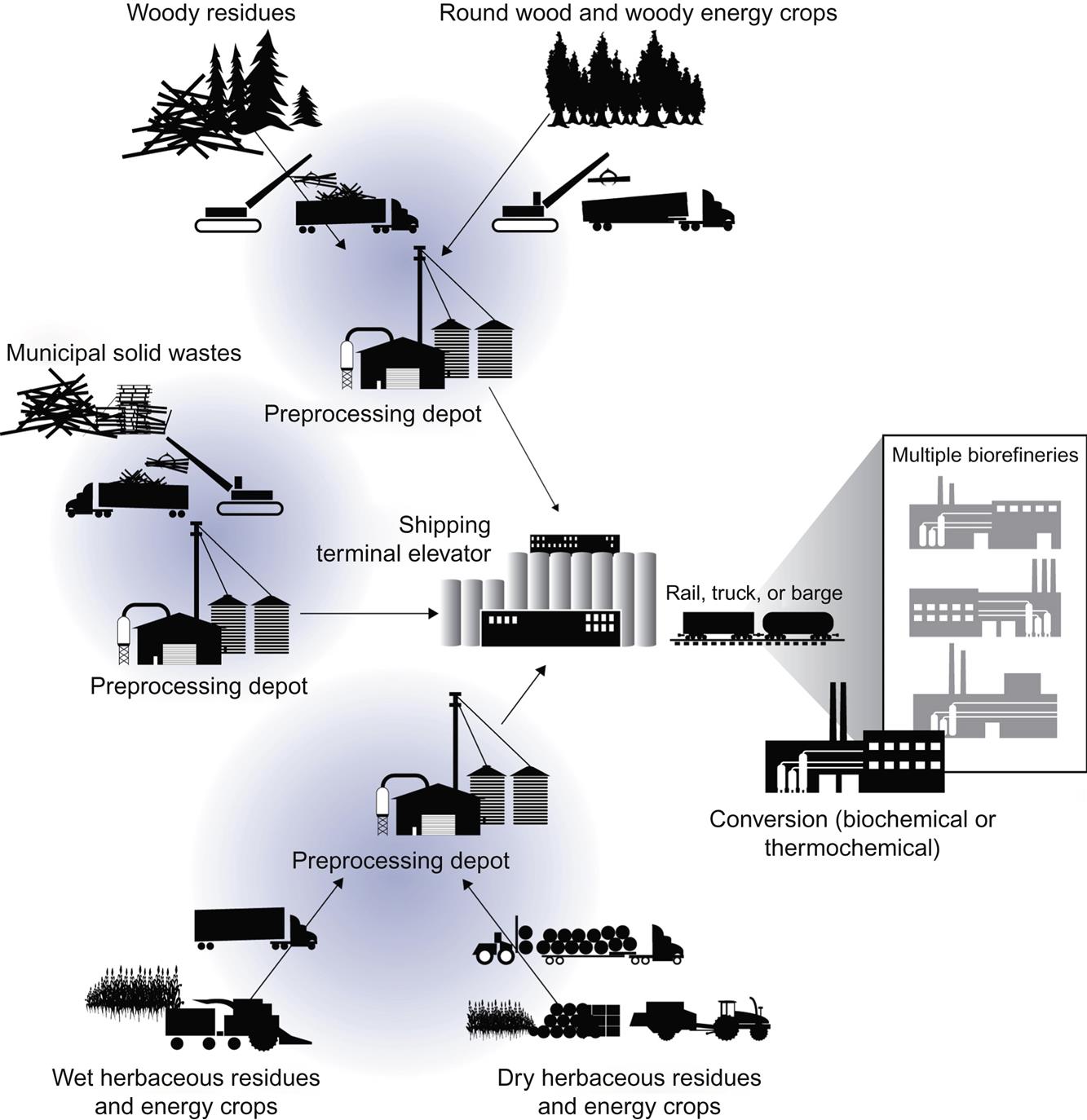

Different analyses (Hess et al., 2009; Argo et al., 2013; Jacobson et al., 2014a; Muth et al., 2014) suggest that the conventional system may not be able to achieve high-volume, low-cost feedstock supply outside of high biomass yield regions and could even encounter issues in highly productive areas in some years due to inclement weather (eg, drought, flood, heavy moisture during harvest, etc.). High-volume, low-cost feedstock supply, however, is a prerequisite for the advanced biofuel industry to scale-up and become (more) competitive with fossil-fuel-derived alternatives. Furthermore, feedstock supply uncertainties tend to increase the risk, which (to some extent) has limited the cellulosic biorefinery concept from being broadly implemented. Advanced feedstock design systems (Hess et al., 2009) introduce methods to reduce feedstock volume, price, and quality supply uncertainties. Advanced systems are based on a network of distributed biomass preprocessing centers (depots) and centralized terminals/elevators (Fig. 8.2). In this system, depots are located close to the biomass resource while shipping and blending terminals are located in strategic logistical hubs with easy access to high bulk transportation systems (eg, rail or barge shipping).

A fundamental difference between the two logistics systems is that the conventional system relies on existing technologies and agri-business systems to supply biomass feedstocks to pioneer biorefineries and requires biorefineries to adapt to the diversity of the feedstock (eg, square or round bales, silage, etc.). The advanced system on the other hand emulates the current grain commodity supply system, which manages crop diversity at the point of harvest and at the storage elevator, allowing subsequent supply system infrastructure to be similar for all resources (Hess et al., 2009; Searcy and Hess, 2010) (Fig. 8.3). Through preprocessing (at the depot) and blending (at the terminal), the variability within the system is reduced significantly in terms of quality and quantity, thus also stabilizing cost/price projections.

8.4 Depot Configurations and Evolvement

Common pelleting (ie, densification and stabilization) has enabled the forest industry to trade woody biomass in large volumes internationally. This is a transition from the previously dominating trade of wood chips, having moisture contents of up to 50%, which could only be traded locally or cross-border for low-value markets such as energy, or needed to be of high quality to access distant, higher-value markets such as pulp and paper.

Due to the low-density format of agricultural residues, traditional thinking suggests cellulosic biorefineries are best suited to be located in high-biomass-yielding areas, and should be designed to handle single feedstock of similar format such as wheat straw bales or corn stover (Hess et al., 2009). Regional preprocessing however, through a network of depots, would allow biorefineries to be built almost anywhere, including lower yield areas (Argo et al., 2013). This would not only allow biorefinery siting based on other, often very relevant criteria, including tax incentives, infrastructure, trained labor, etc., but may also prevent potential resource competition among biorefineries.

Individual depots could not only increase energy and bulk density, but also include quality management to achieve compositional homogeneity and specific cost targets by blending multiple feedstock. A network of depots could supply biorefineries with sufficient feedstock (volume), possibly from different biomass in a variety of forms (eg, square and/or round bales, chipped, bundled, raw, etc.). Depots would have a continuum of functionality, from a “standard depot” that would, at a minimum, include particle size reduction, moisture mitigation, and densification, to “quality depots” which may include additional preprocessing steps such as leaching, chemical treatment, or washing (see Lamers et al., 2015a for a detailed techno-economic analysis of different depot configurations).

8.4.1 Early-Stage Depots

The first depots to emerge would likely focus on improving feedstock stability (for storage), increase bulk density (for transport), improve flowability (for stable in-feed rates), and reduce dry matter loss (DML). Influencing feedstock quality is a result of these activities rather than a primary target of the operation. Passive quality management is optionally possible via feedstock blending.

Indirect quality impacts include, for example, drying, which is done to prevent DML. Consistent moisture levels however also benefit conversion efficiency and improve in-feed. Pelleting is done to increase bulk density and transportability, a key aspect in derisking the feedstock supply system. At the same time, using pelleted feedstock also reduces contamination as it sterilizes (through compression and drying). Small-diameter components, including impurities such as soil are drained in the liquor stream of the conversion pretreatment steps (eg, deacetylation).

To address feedstock stability, bulk density, and flowability issues, depot process flow would likely include particle size reduction, moisture mitigation, and densification. An example of an early-stage depot is a common pelleting process involving a two-stage size reduction (grinding), drying, and pelleting. Additional modifications could be made to make the process more efficient. An example of such modifications could include a high-moisture pelleting process; which varies in process sequence, dryer type, and size compared to the common pelleting process.

8.4.2 Later-Stage Depots

As more depots enter the marketplace, they would evolve from focusing on addressing format and creating a uniform product, to actively addressing feedstock quality aspects specific to the end-use market it targets, for example, cellulosic biorefineries, animal feed, or the heat and power sector. They could produce enhanced feedstock (with lower contamination levels) or even process intermediates and thus reduce the pretreatment requirements at the client facility (Jacobson et al., 2014b; Lamers et al., 2015b). To match end-use markets, various kinds of pretreatment steps are possible within these “quality” depots. Thermal pretreatment technologies (eg, torrefaction) create feedstock with structural homogeneity and superior handling, milling, and cofiring properties. Chemical pretreatment changes the composition and structure of the biomass. This reduces the energy required to grind or densify the feedstock, improves flowability and storage stability, and removes contaminants detrimental to downstream biorefinery processes.

An example of addressing quality at the depot is the ammonia fiber expansion (AFEX) process. AFEX is a promising pretreatment that involves an ammonia-based process resulting in physical and chemical alterations to lignocellulosic biomass that improves their susceptibility to enzymatic attack (Bals et al., 2011). As part of a depot concept, AFEX pretreatment of corn stover and switchgrass has been shown to generate a higher return on investment compared to other depot configurations, for example, wood-based pyrolysis facilities (Bals and Dale, 2012). Furthermore, AFEX pellets can be sold to animal feed operations.

8.5 Depot Deployment

8.5.1 Overcoming the Mobilization Gridlock via Merchandisable Intermediates for Multiple Markets

Feedstock supply systems are currently in a gridlock, where growers will likely not invest in a depot due to slow market growth of biorefineries and the current, limited demand from a single, regional client (biorefinery). On the other hand, biorefineries continue to be limited in expanding their operations in size and number due to high feedstock supply variability in quantity, quality, and price. Thus, a market for feedstock intermediates generated by decentralized depots will not emerge by itself. Rather, a transition strategy is required to break the current development gridlock.

The advanced system is seen as a mature logistical and market structure in which multiple depot types and transloading terminals operate in a high volume (ie, liquid) and competitive feedstock market to serve multiple industries in the bioeconomy. A stepwise introduction of the depot concept is seen as an organic transition towards this vision; yet depots alone do not represent the advanced supply system.

A fundamental part of initiating (pilot-) depot operations is to establish the value proposition to the biomass grower, as the biomass becomes available to the market place only through mobilization. Mobilization is creating the economic drivers required to catalyze the infrastructure investment and biomass resource development investment necessary to transition biomass from available resource, that is, what is on the field, to a merchandisable resource, that is, what is available for sale (Box 8.1).

The current paradigm for developing feedstock supply systems is that it requires a market pull (ie, new biorefineries) to mobilize the resources. A feedstock supply industry that would independently mobilize biomass by producing value-added merchandisable intermediates however creates a market push that will derisk and accelerate deployment of bioenergy technologies. Accomplishing this would still require a market pull, but initially the pull comes from existing markets; thus, the need for multiple markets (Fig. 8.3).

An obvious question emerges: how do you mobilize biomass into the marketplace without biorefineries to purchase the feedstock? The answer: with companion markets. That is, depots that produce value-added product intermediates that are fully fungible into both the companion market and the biofuels refining market. The stronger, established companion market mobilizes the biomass resource, and that mobilization pushes the second-generation biofuels market into existence. Examples of such markets are biopower or animal feed operations (Fig. 8.3).

Biopower, including cofiring coal with biomass, provides an opportunity to demonstrate value-added advanced preprocessing, developing technologies and systems that could be leveraged by a growing biofuels industry. An example of a technology under development that would minimize, if not eliminate, the need for retrofitting existing coal plants is thermal treatment, such as torrefaction. Torrefaction, and advanced preprocessing technology that could be integrated into a depot slowly dries the biomass to remove essentially all water, such that the feedstock is very friable. The hope is that torrefied feedstock could be handled, fed, and burned very much like coal (Nunes et al., 2014). Another example is AFEX pretreatment (Bals and Dale, 2012), which is value-added processing of biomass for biochemical conversion, but is also a value-added intermediate product for livestock feed. Yet another example is applying thermal treatment strategies to produce oil product with acceptable “shelf-life” as a value-added intermediate for oil-refining routes, but also produces value-added products for heat, power, and specialty markets (liquid smoke, cosmetics, etc.). Technologies are being developed to support the production of a stable bio-oil intermediate at depot-scale.

8.5.2 Separating the Vertical Supply Chain

Continuing along the vertically integrated path that pioneer cellulosic biorefineries have taken will constrain the bioenergy industry to very high-biomass-yielding areas, limiting the industry’s ability to increase in scale to larger plants, and scale as an industry at any size plants. Advanced feedstock supply systems, and depots in particular, enable a bifurcated profitable feedstock supply industry, independently viable from the biofuels industry.

To advance the cellulosic biofuels industry, a separation between feedstock supply and conversion is necessary. Thus, in contrast to the vertically integrated supply chain with a single industry, there are two industries in the advanced feedstock supply system: a feedstock industry and a conversion industry. The split is more beneficial for feedstock producers as they are able to sell into multiple markets. Unless there is a heavy competition among feedstock producers, the split may actually be disadvantageous for the conversion industry; which currently enjoys a monopsony situation (in which it is the sole demand party). Therefore, it may come to a hybrid system in which some upstream activities by the biorefineries secure a bulk of the feedstock and some volumes are bought via contracts (or the spot market) (Box 8.2).

8.6 Market Transition

8.6.1 Transition Periods

The depot concept is applied in the forest and agricultural sector, such as wood pellet production and the food/fodder industry (eg, farmer cooperatives). It is not yet widely used however with respect to agricultural residues, and is not part of current biorefinery feedstock supply chains. The appearance of depots across the biorefinery supply chain is expected to occur organically as biofuel producers add preprocessing equipment and storage to existing infrastructure to primarily buffer supply quantity and price risks.

Jacobson et al. (2014) provide a conceptual cost evaluation of this concept as part of an exploration of different feedstock supply management strategies via systems dynamic modeling. In a series of simulations, the authors show the resilience of the concept under several perturbation scenarios, such as weather-related regional supply shortages. The configuration does entail higher cost to the biorefinery but proved to handle volume and price risks better than without storage options. Thus, the investment in small-scale pelleting for short-term volume buffering provides long-term benefits to the biorefinery and becomes a critical element in derisking the supply system.

The organizational structure of a depot can be independent of the biorefinery (Table 8.2). While the biorefinery may own one or several depots, the depots could also be owned and operated by farmer cooperatives, in line with the historical growth of the US grain elevators. Depots may have various business models, that is, they could operate independent from the biorefinery, be owned and operated by the biorefinery, or even be owned by the biorefinery but operated by the producer, consistent, for example, with trends of US grain elevators. Depot location will most likely be driven by the ownership profile (biorefinery vs cooperation) as well as the existing logistical infrastructure (eg, rail lines, shipping terminals) and it is more likely that as quality becomes more uniform the further away the depot will be located from the biorefinery. This makes decentralized locations possible, also in low-yield areas.

Table 8.2

Market challenges and opportunities of the depot concept

| Challenges/opportunities | Explanation |

| Ownership | The ownership and organizational structures behind a depot directly influence the business strategy/behavior (including contractual issues between a depot and biorefineries, etc.). |

| Sizing and location | The initial depot concept entails distributed entities located in proximity to the biomass source; potentially followed by connections to terminals where feedstock is consolidated prior to further (bulk) distribution. Depot size will be defined by the sourcing radius and the respective biomass availability (year-round). Depot size influences economies of scale. The resulting question is whether optimal depot sizes exist and to what extent economies of scale can be utilized. |

| Single versus multifeedstock | Feedstock availability/seasonality will influence the depot size and technical layout. To be operating all year, feedstock flexibility will be key. Most likely depots will rely on field-storage options as the conventional system. |

| Single versus multiproduct | The flexibility of the depot to supply products to multiple markets will be crucial in defining its operational business risks and thus the attractiveness of an investment. A conventional pelleting operation could target industrial as well as residential heat markets (ie, produce to match different technical standards). The AFEX depot already produces pellets that can be applied in the biochemical conversion as well as the feed/fodder industry. |

| Preprocessing intensity | The level of preprocessing intensity at the depot depends on a number of factors including the typical markets it will sell to, size (economies of scale), biomass availability, access to capital, business strategy, etc. |

| Waste streams and treatment | Depending on the involved technical processes, depots may generate waste streams effluents that require treatment. The economic viability of a waste-water-treatment facility at a depot directly relates to depot size and profit. Thus, it appears that only larger, highly specialized depots would be able to compensate for such an investment. |

| Depots as well as biorefinery feedstock reception stations will create solid waste (eg, broken bales). Creating this organic material closer to the field creates options for reuse and reduction of transport costs to do so. Also, it may serve as a second income stream for the depot. |

The location decision for a depot is driven by the feedstock supply and existing logistical infrastructure (eg, rail lines, shipping terminals) and other factors (eg, socioeconomic). It becomes more independent from the biorefinery location as the improved feedstock material can be transported over long distances with minimal additional costs. This decentralizes biorefinery locations and also incorporates biomass from low-yield areas that would currently be too costly for a conventional supply system.

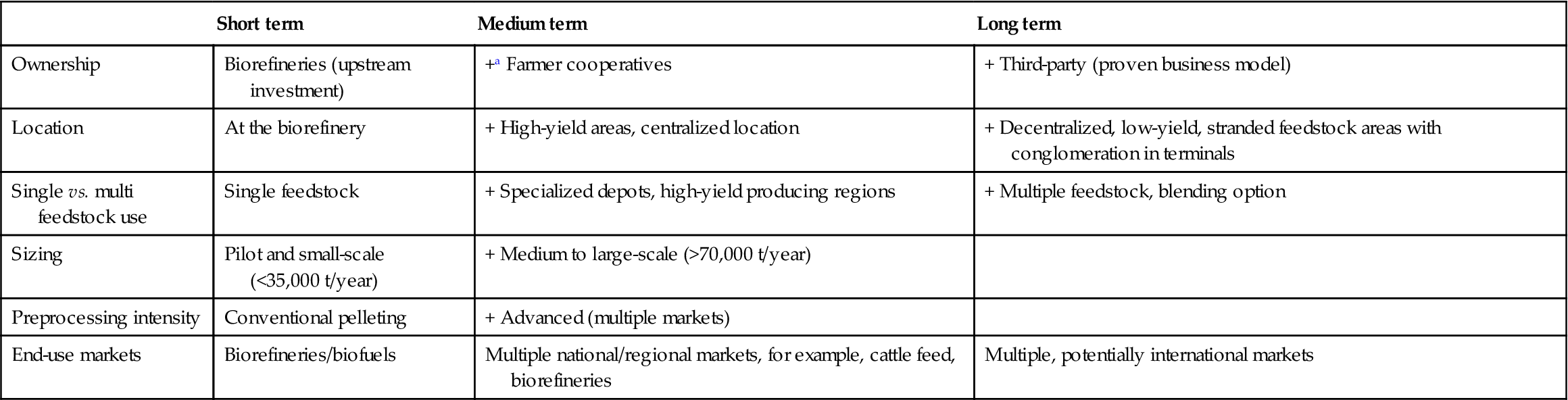

Table 8.3 provides a suggestion for potential transition periods of the industry along several key depot characteristics. The main influencing factors include ownership structures, as well as location and sizing decisions, which relate to specialized (single feedstock) or flexible (multifeedstock) depots. The type, number, and size of the end-product market will significantly drive the deployment speed of the depot concept.

Table 8.3

Depot transition periods by elements of characteristics

| Short term | Medium term | Long term | |

| Ownership | Biorefineries (upstream investment) | +a Farmer cooperatives | + Third-party (proven business model) |

| Location | At the biorefinery | + High-yield areas, centralized location | + Decentralized, low-yield, stranded feedstock areas with conglomeration in terminals |

| Single vs. multi feedstock use | Single feedstock | + Specialized depots, high-yield producing regions | + Multiple feedstock, blending option |

| Sizing | Pilot and small-scale (<35,000 t/year) | + Medium to large-scale (>70,000 t/year) | |

| Preprocessing intensity | Conventional pelleting | + Advanced (multiple markets) | |

| End-use markets | Biorefineries/biofuels | Multiple national/regional markets, for example, cattle feed, biorefineries | Multiple, potentially international markets |

a‘+’ indicates additions to the previous, earlier transition periods.

8.6.2 Supply Chain Opportunities

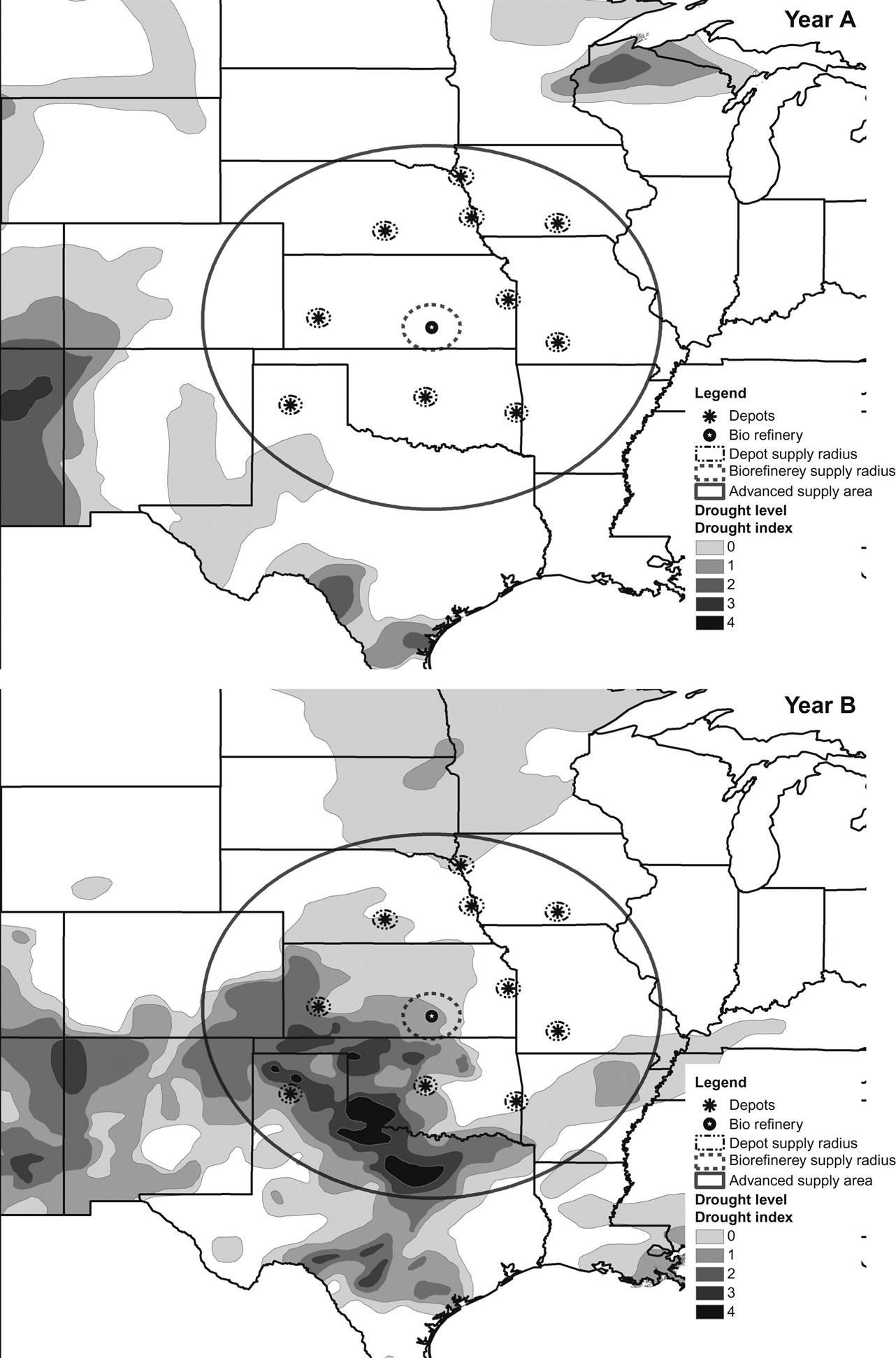

In a direct comparison, the conventional system actually has lower supply costs than an advanced system within limited (typically 80 km) radius around the biorefinery when it is situated in a high-biomass-yielding region, such as corn stover in Iowa. However, with an increasing sourcing radius and moving outside of high-yielding regions, supply costs in the conventional system increase exponentially while they remain almost stable in the advanced feedstock supply system (Muth et al., 2014). This allows the biorefinery to tap into resources that are not in its immediate vicinity and thus leverage supply risks in years with reduced harvests, for example, due to droughts. Fig. 8.4 shows drought effects across a sourcing area of a biorefinery located in the southern part of Kansas. It illustrates that without depots that have access to feedstock outside the heavily affected area, the biorefinery would run a heavy risk of not being able to source sufficient material (within reasonable cost limits) to allow a continuous operation.

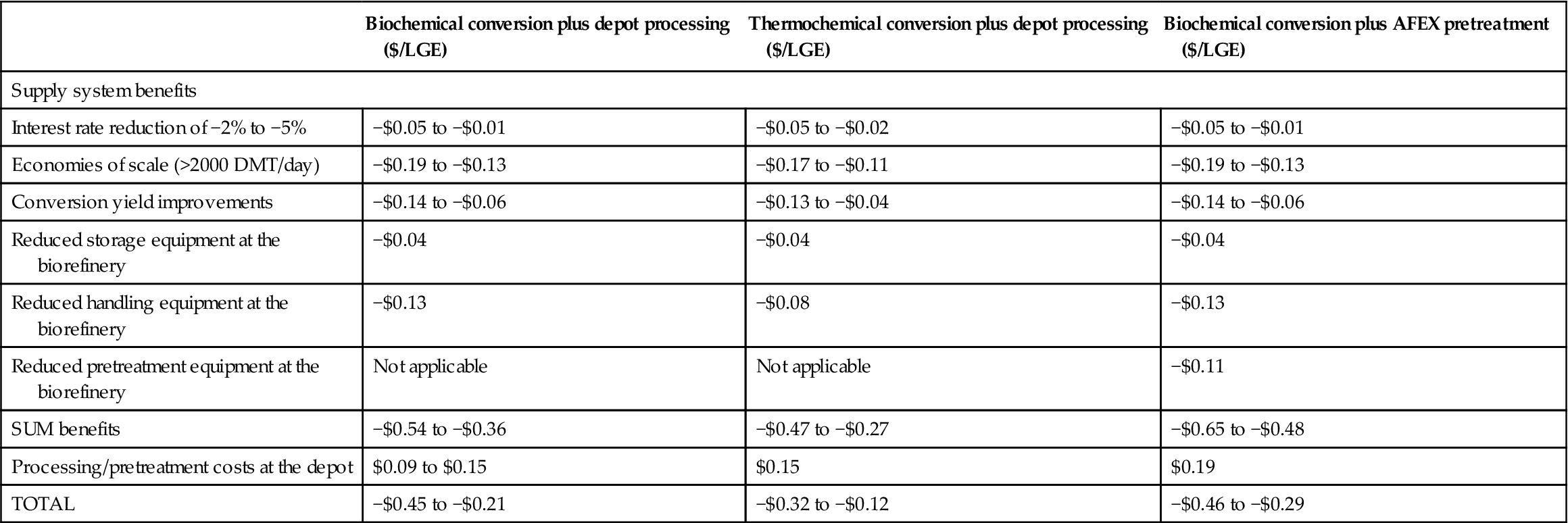

Advanced systems address many of the feedstock supply risks associated with conventional systems, and create wider system benefits; most of which translate into cost benefits and risk reduction across the entire biofuel supply chain. Cost benefits of an advanced feedstock supply system include, among others, supply risk reductions (leading to lower interest rates on loans), economies of scale, conversion efficiency improvements, and reduced equipment and operational costs at the biorefinery. Table 8.4 summarizes these benefits and compares them in US$ per liter of gasoline equivalent (LGE) produced. The reason for this measure is the US Department of Energy’s advanced biofuel production cost target of $0.79 per LGE by 2022. Note that this list of potential benefits is not exhaustive.

Table 8.4

Comparison of the additional preprocessing costs for an advanced feedstock supply system and its biorefinery investment and operation cost-benefits (Lamers et al., 2015b)

| Biochemical conversion plus depot processing ($/LGE) | Thermochemical conversion plus depot processing ($/LGE) | Biochemical conversion plus AFEX pretreatment ($/LGE) | |

| Supply system benefits | |||

| Interest rate reduction of −2% to −5% | −$0.05 to −$0.01 | −$0.05 to −$0.02 | −$0.05 to −$0.01 |

| Economies of scale (>2000 DMT/day) | −$0.19 to −$0.13 | −$0.17 to −$0.11 | −$0.19 to −$0.13 |

| Conversion yield improvements | −$0.14 to −$0.06 | −$0.13 to −$0.04 | −$0.14 to −$0.06 |

| Reduced storage equipment at the biorefinery | −$0.04 | −$0.04 | −$0.04 |

| Reduced handling equipment at the biorefinery | −$0.13 | −$0.08 | −$0.13 |

| Reduced pretreatment equipment at the biorefinery | Not applicable | Not applicable | −$0.11 |

| SUM benefits | −$0.54 to −$0.36 | −$0.47 to −$0.27 | −$0.65 to −$0.48 |

| Processing/pretreatment costs at the depot | $0.09 to $0.15 | $0.15 | $0.19 |

| TOTAL | −$0.45 to −$0.21 | −$0.32 to −$0.12 | −$0.46 to −$0.29 |

Note: Not all benefits associated with the depot concept have been quantified and included in this table.

As can be observed from Table 8.4, the cost of additional infrastructure in advanced systems (such as the depot) is more than offset by the savings that advanced feedstock supply systems enable across the entire biofuel supply system. Advanced systems, when matched with the appropriate mode of transportation, could help reduce temporal and spatial biomass variability and allow access to greater quantities of sustainable biomass within a cost target by decoupling the biorefinery from feedstock location. Additionally, densified feedstock has better flow characteristics, which improves transport to and within the biorefinery (via rail, ship, conveyor belts, etc.). This extends the sourcing radius for the biorefinery well beyond the typical 80-km radius of a conventional bale supply and mitigates risks associated with feedstock intermissions (eg, due to adverse weather, pests, and resulting competition for the remaining feedstock within close range). The biorefinery should thus be less vulnerable to feedstock volume, quality, and price volatility (affecting its profitability) and may not need to contract directly with feedstock producers. Reducing profitability risks could also help leverage the reluctance from the investment community to invest in larger facilities, enabling production economies of scale. The variability of feedstock supply to biorefineries in terms of both quality and quantity is recognized as an investment risk by financial institutions. Reducing the variability of feedstock supply will reduce associated project risks which will be reflected in the weighted average cost of capital for financing biorefineries. Also, advanced systems will reduce the handling infrastructure (for raw biomass in various formats) at the biorefinery, improve in-feed operations and thus reduce investment and operating costs. This should further reduce investment risks.

8.7 Conclusions

The cellulosic bioenergy industry is still in its infancy. However, a handful of US biorefineries had to implement feedstock supply strategies for commercial facilities. The vertically integrated feedstock supply systems developed by each of these biorefineries are similar to conventional supply system designs described in this section. Cost estimates for establishing the feedstock supply system on existing biomass resources (ie, existing crops, such as corn stover, rather than energy crops) have ranged from 30% to greater than 50% of the cost of the biorefinery.

Recently published analyses show that biorefineries, cellulosic or otherwise, that are attached to an existing and fully mobilized feedstock resource (corn stover being the reference feedstock) have a reduced risk profile that may translate into a 2–5% financing interest rate reduction (Hansen et al., 2015; Lamers et al., 2015b). Depending on the size of the biorefinery, this could resemble as much as a $0.05 per liter reduction in unit production cost over depreciable facility life. Additionally, evidence also suggests that facilities that do not have to develop their own supply systems can be fully operational 12–18 months sooner than those that must build supply systems. Combining the cost savings and faster start up time, there is great incentive for biorefineries to move beyond conventional supply systems.

The advanced feedstock supply system is envisioned to be a mature logistical and market structure in which multiple depot types and transloading terminals operate in a high volume (ie, liquid) and competitive feedstock market to serve multiple industries in the bioeconomy. A stepwise introduction of the depot concept is seen as an organic transition towards this vision; yet depots alone do not represent the advanced feedstock supply system. Initially, depots could entail solely processes to stabilize biomass for storage and transport. They could be owned by the biorefinery to buffer supply variations and reduce storage footprint and harmonize in-feed operations. Fully independent depots as well as advanced technical designs, for example, dilute acid pretreatment, may only emerge over time.

A critical component within the advanced system is the biomass processing depot. Depots, and more importantly advanced preprocessing technologies hosted at depots, can mitigate many risk factors faced by biorefineries associated with conventional supply systems, such as aerobic instability (ie, rotting and fire risk), high-quality variability, inefficient handling and transportation, supply chain upsets (due to weather, pests, etc.), just to name a few. In addition to helping current biorefineries reduce feedstock supply risk, depots essentially “mobilize” biomass resources into the market place by producing value-added merchandisable biomass intermediates that can be traded and aggregated.