IV.5

Value at Risk for Option Portfolios

IV.5.1 INTRODUCTION

The previous chapters in this book have focused on two aspects of VaR modelling: the risk characteristics of portfolios with different types of risk factors, and the modelling of the risk factors. Until now we have only applied the models that we have developed to simple portfolios where the portfolio mapping is a linear function of their risk factors. Now we extend the analysis to discuss how to estimate VaR and expected tail loss for option portfolios.

The most important risk factors for an option are the change in price of the underlying asset, the square of this price change and the change in the implied volatility. The squared price change is necessary because an option price is non-linearly related to the underlying price. This introduces an extra degree of complexity into the construction of a VaR model for an option portfolio.

When VaR estimates for option portfolios are scaled over different risk horizons we are making an implicit assumption that the portfolio is being dynamically rebalanced at the end of each day, to keep its risk factor sensitivities constant. For this reason, we call such a VaR estimate a dynamic VaR estimate. Then, even though the portfolio returns cannot be normal and i.i.d., it is common practice to scale the daily VaR to longer risk horizons using a square-root scaling rule. Indeed, it is admissible under banking regulations, although the Basel Committee indicates that this practice may ultimately be disallowed.1 Dynamic VaR estimates are suitable for actively traded portfolios, in particular for assessing the risk of a portfolio that is always delta–gamma–vega neutral and for assessing the VaR when the portfolio is held at its risk limits, if these limits are defined in terms of risk factor sensitivities. However the use of a square-root scaling rule can be a significant source of model risk.

The alternative is to measure the VaR directly from the h-day P&L, without scaling up a 1-day VaR estimate to a longer risk horizon. In this case we are assuming the portfolio is not traded during the risk horizon, and so we call such a VaR estimate a static VaR estimate. Static VaR is suitable for estimating the risk of a single structured product that is not intended to be dynamically rebalanced. In practice, assuming no rebalancing over the risk horizon is not realistic for option portfolios. Option traders write options because they think they know how to hedge their risks, and they believe they can make a profit after accounting for their hedging costs, often rebalancing their hedged portfolio several times per day.

If the risk factor returns are normal and i.i.d. it makes no difference to a linear portfolio whether we scale the daily VaR to longer risk horizons using the square-root scaling rule, or measure the VaR directly from the h-day return or P&L distribution. That is, the static and dynamic VaR estimates are the same. But this is not the case for option portfolios. Static VaR estimates have gamma, vega and theta effects that are much more pronounced than they are in dynamic VaR, with the gamma effect being the greatest.

Our focus in this chapter will be on modelling the non-linear characteristics of portfolios, rather than on the precision of the VaR methodology. Nevertheless, from the many empirical examples given in this chapter we are able to draw some strong general conclusions about the appropriate type of VaR model to apply to option portfolios.

Whilst analytic approximations to options VaR based on delta–gamma mapping may seem attractive, the option portfolio P&L resulting from this approximation is highly skewed and bimodal so it is very difficult capture with a parametric model. Moreover, accurate VaR estimation requires a precise fit in the tails of this distribution, and even small discrepancies between the parametric form and the empirical distribution can lead to large errors in the analytic approximation to VaR.

We shall show that standard historical simulation is suitable for dynamic VaR estimation, but there are problems with trying to use a non-parametric model for static VaR estimation. Typically, the precision of a standard historical VaR estimate relies on using daily risk factor returns in a very large number of simulations. From these we could estimate a 1-day VaR non-parametrically and scale up this estimate to longer risk horizons, under the assumption that the option portfolio has stable, i.i.d. returns. But this approach assumes that the portfolio is rebalanced daily to return the risk factor sensitivities to their values at the time the VaR is estimated, so it gives an estimate of dynamic VaR, not static VaR. For a static portfolio that is not traded over the risk horizon we need to estimate the h-day VaR as a quantile of the h-day P&L distribution. Standard historical simulation based on overlapping data will distort the tail behaviour of the P&L distribution in such as way that VaR estimates at extreme quantiles can be seriously underestimated. In fact, the only way that we can estimate the static h-day VaR in the context of historical simulation is by introducing a parametric model for the conditional distributions of the portfolio returns, such as a GARCH model.2

A strong conclusion that is drawn from this chapter is that the only viable method for estimating the static VaR for option portfolios is parametric simulation, using either Monte Carlo or the filtered historical simulation method of Barone-Adesi et al. (1998, 1999). Either way, option portfolio VaR estimates must be based on a suitable risk factor returns model, not only a non-normal multivariate distribution for risk factor returns but also a model that captures the dynamic properties of risk factor returns. Our empirical examples demonstrate how important it is to include volatility clustering effects in price risk factors. Mean reversion in volatility risk factors is also of some importance, except over very short risk horizons.

Even if efficient Monte Carlo simulation algorithms are based on an appropriate model for risk factor returns, there is another important source of error in VaR for an option portfolio. This is the risk factor mapping. For a portfolio of options it is standard to base the risk factor mapping on a Taylor expansion, where the risk factor sensitivities are given by the portfolio Greeks. But a Taylor expansion is only a local approximation, meaning that it is only accurate for small changes in risk factors. However, because VaR is a loss that we are fairly confident will not occur, to assess VaR we need to consider large movements in risk factors. Thus the Greeks approximations only give a crude approximation to the VaR. In particular, these approximations are of limited use when stress testing a portfolio because, in stress testing, risk factors are set to very extreme values.

On the other hand, to estimate VaR for a large complex option portfolio without using a risk factor mapping may take a considerable amount of time. The Greeks approximations have the major advantage that they facilitate real-time VaR calculations, and these are necessary when traders are operating under VaR limits. Typically, limits might be set at the 95% confidence level, over a daily risk horizon. Real time VaR calculations could then be based on delta–gamma–vega approximation in a Monte Carlo or historical dynamic VaR model.

The outline of this chapter is as follows. Section IV.5.2 discusses the characteristics that differentiate option portfolios from linear portfolios, for the purposes of VaR measurement. We briefly summarize the risk factor mappings for option portfolios and then provide a critical review of the practice of scaling VaR for option portfolios from a daily risk horizon to longer risk horizons.

Section IV.5.3 describes some simple analytic approximations to VaR estimates for option portfolios. We focus on a large complex portfolio where exact evaluation is impractical, so that a risk factor mapping must be applied. First we derive a simple delta – normal VaR approximation that treats an option portfolio as if it were linear. Then a quasi-analytical method for calculating the VaR, based on a delta–gamma mapping, is explained. The method relies on fitting quantiles, or better still the whole P&L distribution, to the moments of a multi-factor delta–gamma representation.

In Section IV.5.4 we explain how historical simulation could be applied to options and option portfolios. The section begins with empirical examples of VaR when options are revalued exactly, using the pricing model, starting with a standard European option but also including an example based on an analytic approximation to the price of an option with a path-dependent pay-off. Then we move on to option portfolios, first with exact repricing of the options at the risk horizon and then when the portfolio P&L is mapped to risk factors. Of particular interest is the study of historical VaR for a delta–gamma-hedged option portfolio. Such a portfolio has minimal price risk only if it is continually rebalanced to maintain delta–gamma neutrality. This section concludes with a case study on measuring the historical dynamic VaR of a hedged energy options trading book.

Section IV.5.5 describes the application of Monte Carlo VaR to options and option portfolios. The basic steps of Monte Carlo VaR for options are understood in the context of a simple application: measuring the VaR and ETL of a standard European index option.3 The core of the model is the simulation of two negatively correlated risk factors, i.e. the underlying equity index price and its implied volatility. We use this example to demonstrate the difference between static and dynamic VaR. That is, we measure the h-day VaR directly from an h-day P&L distribution, which is the correct way to estimate the VaR of a static portfolio such as a simple European option, and then we measure it from the simulated daily P&L distribution and then scaling by the square root of h. The second method makes some strong assumptions about portfolio rebalancing over the risk horizon, which are not appropriate for a fixed position in a single option, and hence it ignores the crucial gamma, vega and theta effects that are very important to capture in a VaR estimate for an option.

Thereafter Section IV.5.5 considers Monte Carlo VaR based on risk factor mapping of an option portfolio. We explain how delta–gamma–vega mapping is used to revalue the option at the risk horizon and then examine the Monte Carlo VaR model for portfolios of options on several underlyings, applying a multivariate Taylor expansion for the mapping to risk factors. We conclude with a case study on the development of an appropriate risk factor returns model for a large portfolio of energy options. Section IV.5.6 summarizes and concludes.

The material in this chapter assumes knowledge of the analytic, historical and Monte Carlo VaR models described in previous chapters of this volume. Readers should also be familiar with the option theory in Chapter III.3 and the option portfolio mapping methodologies described in detail in Sections III.5.5 and III.5.6.

IV.5.2 RISK CHARACTERISTICS OF OPTION PORTFOLIOS

The value of an option is a non-linear function of its risk factors. Even if we ignore volatility and other less important risk factors, the price of an option is always a non-linear function of the underlying asset price S. This section begins by reviewing the essential details about mapping option portfolios, then we discuss the implications of non-linear risk factor mapping for VaR assessment.

IV.5.2.1 Gamma Effects

In Section III.5.5 we developed the simplest possible mapping of a single option to its price risk factor, the delta – gamma approximation. This may be written:

where R = ΔS/S is the return on the underlying asset and δ$ and γ$ denote the value delta and value gamma of the option.4 More precisely,

where N is the number of units of the underlying that the option contracts to trade and pv is the point value of the option.

The P&L of a portfolio of options on the same underlying may also be represented by (IV.5.1), but now δ$ and γ$ denote the net value delta and value gamma of the portfolio. For all options on the same underlying we can simply add up the value deltas to find the net value delta, and similarly the net value gamma is just the sum of the individual gammas.

When an option portfolio has several underlying price risk factors there are two alternative approaches to price risk factor mapping. Either we use a simple approximation like (IV.5.1) based on price beta mapping or we use a multivariate delta – gamma approximation. It is also possible to combine both approaches. Below we extract the relevant formulae from Section III.5.5 to summarize the possibilities.

The price beta mapping approach is described in Section III.5.5.5. It depends on representing each underlying price risk factor return Ri in terms of a single index risk factor return R. From the model derivation we know that formula (IV.5.1) still applies, but now

where ![]() and

and ![]() are the net value delta and gamma for each price risk factor and

are the net value delta and gamma for each price risk factor and

Thus we perform a regression of each underlying return on an index return and use the regression betas in (IV.5.4) to estimate the value delta and gamma.

In Section III.5.5.6 we developed an alternative mapping for portfolios with several underlying price risk factors. This is the multivariate delta – gamma approximation, which takes the form

Here R = (R1,…, Rn)′ is the vector of the underlying assets' discounted returns,

and

where P is the price of the portfolio. The multivariate mapping is more complex but more accurate than the price beta mapping approach. It is also possible to combine the two approaches using more than one index risk factor in the beta mapping, thus reducing dimensions of the multivariate delta–gamma approximation.

From our discussion in Section III.5.5.4 we know that a position with positive gamma (e.g. a long position on a standard call or put) has a convex pay-off, so that losses are less and profits are more than they would be under a corresponding linear position; and a position with negative gamma (e.g. a short position on a standard call or put) has a concave pay-off, so that losses are greater and profits are less than they would be under a corresponding linear position. An option portfolio with positive delta and gamma (e.g. a long call) gains more from an upward price move and loses less from a downward price move than a linear portfolio with the same delta. But an option portfolio with positive delta and negative gamma (e.g. a short put) will gain less from an upward price move and lose more from a downward price move than a linear portfolio with the same delta.5 Thus positive gamma reduces the risk and negative gamma increases the risk of an option portfolio, relative to the delta-equivalent exposure. This is termed the gamma effect on the risk of an option portfolio.

IV.5.2.2 Delta and Vega Effects

The general expression for the delta – gamma– vega approximation to the P&L of a portfolio of options, possibly on different underlyings, is

where Δσ is a vector of changes in implied volatilities, and the value delta and gamma are defined in (IV.5.7), but how is the value vega vector ν$ calculated? Each option in the portfolio has its own implied volatility as a risk factor. So in large portfolios it is necessary to reduce the number of volatility risk factors. Typically this will be achieved by either vega bucketing or volatility beta mapping.

Under volatility beta mapping, Section III.5.6.4 explains how to calculate the portfolio's position vega, νP, with respect to a reference volatility such as the 3-month at-the-money (ATM) volatility or a volatility index. We use the formula

where Ni denotes the number of units of the underlying that the ith option contracts to buy or sell, νi denotes the vega of the ith option and ![]() is the volatility beta of the ith option. This volatility beta may be estimated by regressing the ith option implied volatilities on the reference volatility. Then, the portfolio's value vega with respect to this reference volatility is the sum of the position vegas multiplied by the point values of the options.

is the volatility beta of the ith option. This volatility beta may be estimated by regressing the ith option implied volatilities on the reference volatility. Then, the portfolio's value vega with respect to this reference volatility is the sum of the position vegas multiplied by the point values of the options.

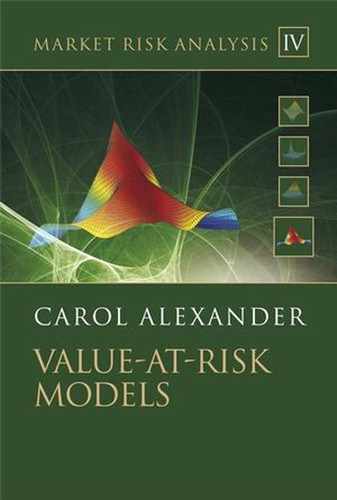

If the underlying price and volatility are negatively and symmetrically related, then the vega effect reinforces the delta effect for a put and offsets the delta effect for a call. To see this, first suppose the price falls dramatically, and so the volatility jumps up. Now consider these positions:

- long call – the call price decreases due to the underlying price fall, but increases due to volatility increasing, thus compensating the loss on the long position;

- short put – the put price increases due to the underlying price fall, so you make a loss on the short position, and the put price increases due to volatility increasing and this compounds the loss.

Now suppose the price increases, so the volatility decreases, and consider these positions:

- short call – the call price increases due to the underlying price increase, but the loss on the short position is offset by a compensatory decrease in the call price due to volatility decreasing;

- long put – the put price decreases due to the underlying price increase, and the loss on the long position is compounded by a decrease in the put price due to volatility decreasing.

The situation is summarized in Table IV.5.1, which shows that the delta–vega effects are most prominent in put options.

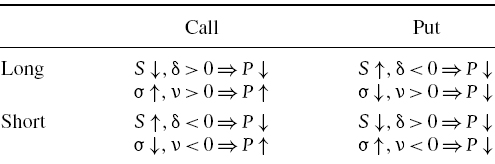

However, in stock and equity index option portfolios, there is an asymmetric negative price– volatility relationship. That is, volatility tends to increase considerably when there is a large fall in the underlying price, but following a large rise in the underlying price of the same magnitude volatility tends to decrease only a little, if at all. Thus the vega effect on a long put or short call is negligible. Therefore the most important vega effect to account for in VaR estimation is on a short put, since here it augments the delta effect. By contrast, the vega effect on a long call offsets the delta effect. The situation is summarized in Table IV.5.2, where we see that short put positions have the most pronounced delta–vega effects.

Table IV.5.1 Delta and vega effects (symmetric negative price–volatility relationship)

Table IV.5.2 Delta and vega effects (asymmetric negative price–volatility relationship)

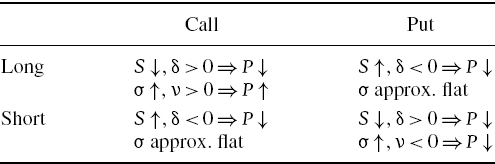

Finally, suppose the underlying price and volatility are asymmetrically and positively related, as they often are for commodity options. That is, volatility increases considerably following a price rise, but does not decrease very much following a price fall of the same magnitude. Then the vega effect reinforces the delta effect on a long put, offsets the delta effect on a short call and is negligible for a long call or a short put. The situation is summarized in Table IV.5.3, where it is now the long put positions that have the most pronounced delta–vega effects.

Table IV.5.3 Delta and vega effects (asymmetric positive price–volatility relationship)

IV.5.2.3 Theta and Rho Effects

Here we summarize the Taylor expansions that approximate the P&L of an option portfolio when interest rate and time risk factors are included in the mapping.6 Later in this chapter we shall use these approximations to estimate the VaR of option portfolios.

The general expression for the delta – gamma– vega– theta– rho approximation to the P&L of a portfolio of options, possibly on different underlyings, is

where the value delta and gamma are defined in (IV.5.7).7 The value theta θ$ is the sum of each position theta multiplied by the point value of the option. Since option prices generally decrease as they approach expiry, the maturity or theta effect is to increase the risk of long positions, and decrease the risk of short positions.

The value rho vector π$ is calculated as the sum of each position rho multiplied by the point value of the option. Note that there is a curve of interest rate risk factors r unless all the options in the portfolio have the same maturity. But unless the underlying of the option is an interest rate or bond, changes in interest rates only affect the discounting of future expected pay-offs. Hence, the rho effect on portfolio risk that stems from changes in interest rates is typically very small.

IV.5.2.4 Static and Dynamic VaR Estimates

Static VaR is calculated over an h-day risk horizon on the assumption that the current portfolio is held over the next h days. Of course, when no trading takes place the risk factor sensitivities are not constant during the risk horizon. In dynamic VaR we assume the risk factor sensitivities are constant over the risk horizon. Then the portfolio must be rebalanced each time a risk factor changes.

For portfolios containing very long-dated options, and a risk horizon of only a few days, a constant risk factor sensitivities assumption is feasible even without rebalancing. Otherwise the use of constant risk factor sensitivities over the risk horizon assumes that the portfolio is rebalanced at the end of each day to return risk factor sensitivities to their values at the beginning of the day. For instance, the portfolio may be rebalanced daily to be delta–gamma neutral, or to keep the position Greeks at their limit values. When a trader operates under limits on his net value delta, gamma, vega and possibly other Greeks, it is very informative to estimate the VaR assuming the trader is at his limits.

The assumption we make about rebalancing affects the way we compute an h-day VaR, for h > 1. We shall now explain exactly how our rebalancing assumption affects the option's VaR estimate, in the theoretical context of the delta–gamma approximation (IV.5.1) of the portfolio's P&L where the underlying log returns are assumed to be normal and i.i.d. The delta–gamma mapping gives an approximate change in the portfolio value as a quadratic function of the underlying return, with coefficients determined by the value delta and value gamma of the portfolio. Our assumption that the log returns on the underlying are normal and i.i.d. implies that they scale in distribution with the square root of time. We now consider two cases.

Static VaR

Denote by R the daily log return on the underlying price risk factor. Assuming this is i.i.d. and normal, the h-day log return on the underlying price has the same distribution as the random variable h½R.8 Hence, the h-day P&L on the option portfolio, as represented by the delta–gamma mapping, may be written

where δ$ and γ$ are the value delta and value gamma at the time that the VaR is measured.

Note that the presence of the gamma term in (IV.5.14) implies that the P&L will not scale with the square root of h, hence

We conclude that under the no rebalancing assumption it is not correct to compute the 1-day portfolio VaR of an option portfolio and simply scale this to an h-day horizon, using a square-root law or any other power scaling law. The correct procedure is to use the h-day risk factor returns to derive the portfolio's P&L distribution, and then derive the VaR.

The no rebalancing assumption has the advantage that the proper theta effect and gamma effect are captured by the VaR estimate if the position is not traded during the risk horizon. When revaluing the portfolio h days ahead, the time to expiry of each option is decreased by h days. Option prices generally decrease as they approach expiry, so the theta effect is to increase the VaR for long positions, and decrease the VaR for short positions. By contrast, the gamma effect decreases the VaR for long positions, and increases the VaR for short positions on standard options, as explained in Section IV.5.2.1.

It is easy to estimate static VaR using Monte Carlo simulations. This is because Monte Carlo VaR models are flexible enough to generate h-day log returns Rh directly. One simply obtains the structured Monte Carlo simulations using the assumed statistical model for h-day risk factor returns. The 100α% h-day delta–gamma VaR, based on the Monte Carlo approach then uses the approximation

However, there are two problems here. First, the Taylor approximation is only valid for small changes in the underlying returns, and the potential size of these returns increases with h. So is it inadvisable to apply Taylor expansion to estimate static VaR over long risk horizons. A second problem is that to adopt the assumption of no rebalancing with standard historical VaR calculations,9 we can only use overlapping data on the h-day risk factor returns, since non-overlapping data of frequency equal to the risk horizon are not usually available in sufficient quantity to estimate VaR accurately. But the use of overlapping data on risk factor returns will truncate the tails of the P&L distributions, as discussed in Section IV.3.2.7. This will be illustrated empirically in Section IV.5.4.

Dynamic VaR

Dynamic VaR assumes that the portfolio is rebalanced during the risk horizon to maintain constant risk factor sensitivities. If simulations are at the daily frequency, it must be assumed that the portfolio is rebalanced once a day over a period of h days, each time returning δ$ and γ$ to the value delta and value gamma at the time that the VaR is estimated. This type of VaR estimate is used to estimate the VaR of a dynamically hedged portfolio, or to estimate the VaR at a trader's sensitivity-based limits.

Assume that the daily log returns on the risk factors are i.i.d. Then, under the constant risk factor sensitivity assumption, the trader faces the same risk at the beginning of each day during the risk horizon. In this case, the h-day P&L for the option portfolio is just the sum of h independent and identical 1-day P&Ls. However, although i.i.d., the portfolio P&L distribution will not be normal even if the risk factor returns are, because the portfolio mapping is a quadratic and not a linear transformation of a normal variable. Hence, it may not be very accurate to scale the 1-day VaR to longer risk horizons using a square-root scaling rule. If the P&L distribution is stable then a different power law scaling rule may be applied (see Section IV.3.2) and then VaRh,α = h1/ξVaR1, α for some constant ξ, not necessarily equal to 2.

Although the P&L of an option portfolio is definitely not normally distributed, it is sometimes assumed nevertheless that ξ = 2, and hence that

But this assumes the gamma, vega and theta effects on h-day P&L also scale with ![]() , which is not the case. The theta effect is captured by the term θΔt in the Greeks approximation, so when a 1-day horizon is scaled up to 10 days using (IV.5.17) the effect is

, which is not the case. The theta effect is captured by the term θΔt in the Greeks approximation, so when a 1-day horizon is scaled up to 10 days using (IV.5.17) the effect is ![]() θ/365, whereas based on a 10-day P&L it should be 10 θ/365. And even if the delta effect scales with

θ/365, whereas based on a 10-day P&L it should be 10 θ/365. And even if the delta effect scales with ![]() , the gamma effect should scale with h. The vega effect is more complex: if there is asymmetry in the price–volatility relationship this is only likely to be apparent at the daily frequency, so scaling up 1-day VaR by the square root of time could be augmenting or diminishing the VaR, depending on the market, the type of option and the sign of our position.

, the gamma effect should scale with h. The vega effect is more complex: if there is asymmetry in the price–volatility relationship this is only likely to be apparent at the daily frequency, so scaling up 1-day VaR by the square root of time could be augmenting or diminishing the VaR, depending on the market, the type of option and the sign of our position.

The daily rebalancing assumption is approximate for two main reasons. First, the square-root scaling rule may not be appropriate, if it is used. Whilst the P&L of an option might conceivably have a stable distribution, it highly unlikely to be normal. Secondly, the daily P&L distribution is estimated by decreasing the maturity of each option by only 1 day and discounting the portfolio price by only 1 day, so scaling up a VaR that is estimated this way diminishes the theta effect, i.e. that option prices tend to decrease as they approach expiry. Daily rebalancing also diminishes the gamma effect, which can be considerable for short dated options;10 and it distorts the vega effect, which can be considerable for long dated options.

Over one day the underlying price and volatility tend to move much less than they would over a 10-day or longer risk horizon. Hence, when VaR is estimated over one day, and then scaled up, the gamma, vega and theta effects will be too small. As a result, we expect the VaR estimate for positive gamma positions (e.g. a long call or put option) to be greater when based on daily rebalancing than it is when we estimate VaR from a directly computed h-day P&L distribution. And the opposite is the case for positions with negative gamma.

We shall be comparing the static and dynamic VaR estimates in several empirical examples and case studies in this chapter, to highlight the effect that the assumption we make about rebalancing will have on the VaR estimate. And we shall specifically focus on this issue in Examples IV.5.3 and IV.5.7, in the context of the historical VaR model. As explained above the static VaR is more sensitive to the portfolio gamma, vega and theta than dynamic VaR. Although they are the same at the daily horizon, the two assumptions can lead to totally different VaR estimates when the risk horizon is more than a few days, and so it is important to choose the assumption that is closest to the trading practice of the particular portfolio.

IV.5.3 ANALYTIC VALUE-AT-RISK APPROXIMATIONS

This section begins with a description of the mapping of option portfolios to the underlying prices, interest rates, time – and indeed any risk factor except volatility. Mapping to volatility risk factors is quite a challenge, and is covered in the next section. We then describe how these mappings allow an analytic approximation to the VaR of an option portfolio. However, for more complex risk factor mappings, and in particular those that include volatility as a risk factor, we must estimate VaR using simulation.

IV.5.3.1 Delta Approximation and Delta–Normal VaR

For a portfolio of options on a single underlying the first order Taylor approximation to the portfolio's discounted P&L is

where δ$ is the value delta of the portfolio and R is the discounted return on the underlying.

Since (IV.5.18) is a simple linear transformation the VaR based on (IV.5.18) is very easy to calculate. For instance, suppose the discounted h-day returns on the underlying asset are normally distributed with mean and standard deviation μh and σh. Thus

where Rh denotes the discounted h-day return on the underlying. By (IV.5.18) the approximate distribution of the h-day P&L on the portfolio is

Option pricing theory is based on the assumption that the expected return on the underlying asset is the risk free discount rate. To be consistent with this assumption we set μh = 0. Now, from (IV.5.20) it follows that we can apply the normal linear VaR formula given in Section IV.2.2.1 to approximate the 100α% h-day VaR of the option portfolio as

where Φ−1(1 − α) is the 1 − α quantile of the standard normal distribution. In other words, the portfolio has a VaR that is approximately δ$ times the VaR of the underlying asset.

More generally, we can apply a delta mapping to portfolios of options on several underlyings. The mapping is

where P is the portfolio price, ![]() is the vector of net position deltas and ΔS = (ΔS1,…, ΔSn)' is the vector of changes in the underlying prices. Equivalently,

is the vector of net position deltas and ΔS = (ΔS1,…, ΔSn)' is the vector of changes in the underlying prices. Equivalently,

where ![]() is the vector of value deltas and r = (R1,…, Rn)′ is the vector of returns on the underlying prices.

is the vector of value deltas and r = (R1,…, Rn)′ is the vector of returns on the underlying prices.

This is just a linear mapping based on risk factor returns that we might assume to have a multivariate normal distribution. So, following the usual reasoning (see Section IV.1.6.3, for instance) we have

where Ωh is the h-day covariance matrix of the discounted returns on the underlying asset. We might also assume they have a multivariate Student t distribution, as explained in Section IV.2.8, in which case (IV.5.24) would be modified to

EXAMPLE IV.5.1: DELTA–NORMAL VAR

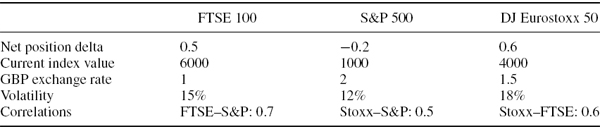

A portfolio of options on the FTSE 100, S&P 500 and DJ Eurostoxx 50 indices has the characteristics shown in Table IV.5.4. The options are for £10 per point on the FTSE 100, $100 per point on the S&P 500 and €10 per point on the DJ Eurostoxx. Calculate the value deltas in sterling terms and hence compute the delta–normal approximation to the 1% 10-day VaR for a UK investor, under the assumption that exchange rates are constant.

Table IV.5.4 Characteristics of equity indices and their options

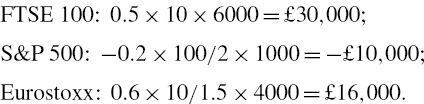

SOLUTION The net value deltas in sterling terms are as follows:

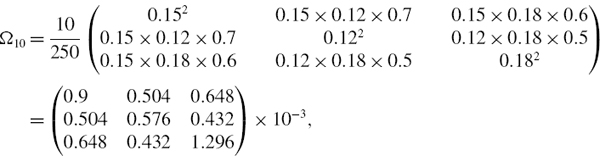

The 10-day covariance matrix of the daily risk factor returns is

and so the 10-day variance of the portfolio P&L is

Using (IV.5.24) this gives a 1% 10-day VaR of ![]() .

.

Because the portfolio is assumed to be linear in the above example, we get the same answer from static and dynamic VaR estimation. That is, we get the same answer whether we assume that the portfolio is:

- rebalanced daily to maintain the current values of the net position deltas, in which case we can multiply the 1-day VaR by

to get the 10-day VaR; or

to get the 10-day VaR; or - not traded during the 10-day period, in which case we base the VaR on the 10-day covariance matrix.

This is true for a linear portfolio with i.i.d. normal returns, but when we include gamma effects we obtain different results depending on the assumption about rebalancing.

Several extensions to the normal linear VaR have been described in Chapter IV.2 of this volume. We can measure the VaR and the ETL of any portfolio with a linear risk factor mapping using a Student t distribution or a normal mixture distribution, for instance. All these generalizations can be carried over to option portfolios when their risk factor mapping is the basic delta map given by (IV.5.22). However, a linear risk factor mapping such as (IV.5.22) is extremely inaccurate as an approximation for the P&L for an option portfolio. The values of most option portfolios will be a highly non-linear function of the underlying asset prices. As a result, the delta–normal VaR model should not be used, even for simple option portfolios.

IV.5.3.2 P&L Distributions for Option Portfolios

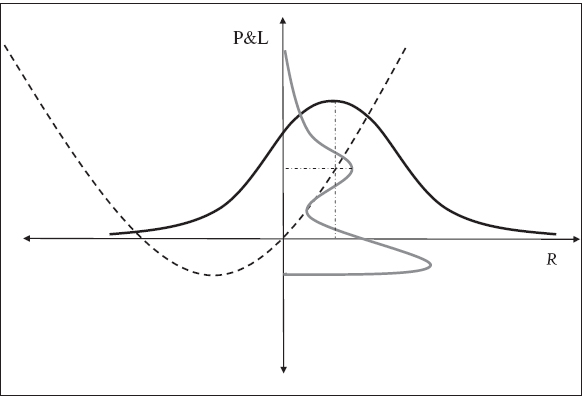

Figure IV.5.1 illustrates how the delta–gamma approximation translates the distribution of risk factor changes into a distribution of price changes for the option portfolio. We assume there is a single risk factor with return R. The distribution of R is assumed to be normal and its density is shown by the black curve. The vertical axis represents the option portfolio P&L given by the delta–gamma approximation (IV.5.1). The delta–gamma approximation is a quadratic function of R that is indicated by the dashed curve, and the option portfolio P&L density that is derived by applying this approximation to each value of R is shown by the grey curve drawn relative to the vertical axis.

Figure IV.5.1 The P&L distribution resulting from delta–gamma approximation

On the figure we have indicated the mean return, assumed positive, using a dot-dashed vertical line. We also indicate, using a horizontal dot-dashed line, that the delta–gamma approximation translates the mean return into a local maximum of the P&L density. Another local maximum is obtained when the return is negative, and this time the maximum occurs at a negative value for P&L.

The figure shows that even when we use a simple delta–gamma approximation to the portfolio P&L, its distribution is highly non-normal. This is because the delta–gamma approximation gives the P&L as a weighted sum of the return and the squared return, and if the returns are normally distributed the squared returns have a chi-squared distribution. Also, the expectation of the squared return is not zero. Hence, the expected P&L is not zero even when the expected return on the underlying is zero.11 The P&L distribution induced by the delta–gamma approximation is therefore positively skewed, bimodal and may also be highly leptokurtic.

IV.5.3.3 Delta–Gamma VaR

We now derive an analytic approximation to the VaR of a portfolio of options on several underlyings. To do this we need to fit a distribution with density function such as that shown by the grey, skewed, bimodal curve in Figure IV.5.1.

Consider the h-day P&L given by the delta–gamma representation (IV.5.6), where the returns on the underlying assets have a multivariate normal distribution with covariance matrix Ωh. Of course the option portfolio P&L will not have a normal distribution, since it includes sums of squared normal variables. But we can use (IV.5.6) to estimate the mean, variance, skewness and kurtosis of the P&L distribution, assuming the approximation (IV.5.6) is reasonably accurate.

The expectation of the right-hand side of (IV.5.6) is given by12

where tr is the trace of a matrix, i.e. the sum of its diagonal elements. After some calculations, we derive the following expressions for the higher moments of the distribution of the discounted P&L:

Hence, the skewness and kurtosis of the delta–gamma representation are

Although the above expressions look complicated, they allow one to calculate the mean, variance, skewness and kurtosis of the delta–gamma P&L distribution (IV.5.6) for an option portfolio with many underlyings. If we know the price risk factor sensitivities δ$ and Γ$ that characterize the portfolio, and the covariance matrix Ωh of h-day returns on the underlying prices, then we can derive the moments of the P&L distribution.

Now suppose we have calculated the first four moments as explained above. How do we estimate the VaR? One possibility is to apply a Cornish – Fisher expansion to approximate a quantile from these moments using the methodology explained in Section IV.3.4.3. However, we know from our empirical studies in Section IV.3.4 that for highly leptokurtic distributions this is will not provide results that are as accurate as those derived by fitting a Johnson SU distribution to the moments. The method is illustrated in the next example. It uses Tuenter's algorithm for fitting the Johnson SU distribution, as explained in Section IV.3.4.4.13

EXAMPLE IV.5.2: DELTA–GAMMA VAR WITH JOHNSON DISTRIBUTION

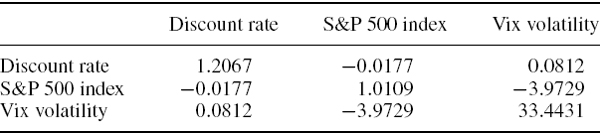

Consider a portfolio of options on bonds and on equities with a P&L that has the delta–gamma approximation

The units of measurement are millions of US dollars. Thus the net value delta is $1 million with respect to the bond index and $5 million with respect to the equity index. The value gamma matrix is also measured in millions of dollars. Suppose that the returns on the bond and equity indices are normally distributed with volatilities of 30% and 20% and a correlation of −0.25. Fit a Johnson distribution to the distribution of the portfolio P&L. Hence, estimate the 1% 10-day VaR of the portfolio and compare your result with the delta–normal VaR based on (IV.5.25).

SOLUTION We have

The 10-day covariance matrix of the risk factor returns is

In the spreadsheet for this example we calculate the moments of the 10-day P&L distribution based on (IV.5.26)– (IV.5.31) and the results are: mean $0.150 million, standard deviation $0.256 million, skewness 1.1913, and excess kurtosis 47.153. Since the excess kurtosis is positive, we can fit a Johnson SU distribution to these parameters using Tuenter's algorithm.14 The result is a delta–gamma 1% 10-day VaR of $261,024. The corresponding delta–normal VaR is $451,096. Clearly, ignoring the gamma effect leads to considerable error when computing VaR. The portfolio has a positive gamma, so we know from our discussion in Section IV.5.2.3 that the VaR will be considerably reduced when we take the gamma effect into account.

Because it is not bimodal the Johnson distribution that was applied in the above example is not the best way to fit the first four moments of the option portfolio P&L distribution. We have used it because it is practical, and because Section IV.3.4 demonstrated that if the P&L distribution is very leptokurtic, as it is in the example, it is better than using a four moment Cornish–Fisher expansion.15 However, the P&L distribution is bimodal and highly skewed as well. The VaR at extreme quantiles is heavily influenced by the tail behaviour of the P&L distribution, and it is difficult to capture this well with any analytic approximation.

IV.5.4 HISTORICAL VALUE AT RISK FOR OPTION PORTFOLIOS

This section presents several empirical examples on the computation of historical VaR for option portfolios. We begin by studying the simplest possible portfolio: a position on a standard European option on the S&P 500 index. The position requires revaluing for every historical scenario of underlying price and volatility risk factor changes. This is easy when we just apply the Black–Scholes–Merton formula to revalue the portfolio at the risk horizon, but the portfolio revaluation can take considerable time for portfolios of exotic, path-dependent options.

We shall also discuss how to apply historical VaR to the risk assessment of path-dependent options, but since our focus is on the methodology rather than computational details, the position considered will be a simple European look-back option. Although its pay-off is path-dependent, under the constant volatility assumption we still have an analytic formula for its price.16 If numerical methods have to be applied to price a large complex option portfolio this will be very time-consuming. VaR with exact revaluation can usually be estimated overnight, but for high frequency risk assessment purposes such portfolios are often better represented by a risk factor mapping. Hence, another empirical example in this section illustrates the historical VaR approach for a portfolio of options that have been mapped to their risk factors, where all the options are on a single underlying. We then extend this to portfolios of options on several underlyings and end the section with a case study on the historical VaR for a trading book of energy options.

Various enhancements of standard historical simulation (e.g. to account for volatility adjustment, or to apply parametric filtering based on a GARCH model) that improve its accuracy have been described in Section IV.3.3. However, to include these in the empirical examples of this section – which already require quite complex Excel workbooks – would obscure the main purpose of this section. We therefore examine the application of standard historical simulation only, showing that it can usefully be applied to estimate the dynamic VaR of an option portfolio, but it is not the best VaR model to use for static options positions, except when the risk horizon is short.17

IV.5.4.1 VaR and ETL with Exact Revaluation

How does one calculate the historical VaR and ETL of an option that can be priced analytically? In this section we consider a very simple portfolio, i.e. a short position on a 30-day European put on the S&P 500 index. These options are very actively traded on the CME. Each option is for $250 per index point, i.e. the pay-off function is

![]()

where ω is 1 for a call and −1 for a put and the strike K and S&P 500 index futures price S are measured in index points.18

Data

The risk factors of this portfolio are the S&P 500 futures price, the option's implied volatility, and the 30-day US LIBOR rate. For convenience, and specifically to avoid concatenating a very long series of 30-day index futures prices, we apply variations in the spot index price to the current index futures price. This only induces a very tiny error in our calculations because the basis risk between the S&P 500 spot index and its futures contract is negligible.19 Similarly, we shall apply variations in the S&P 500 volatility index, i.e. the Vix index, to the current implied volatility of the option. This assumes the option has a volatility beta of 1 with respect to the Vix index.20 Finally, for the interest rate we use the 1-month LIBOR rate.21

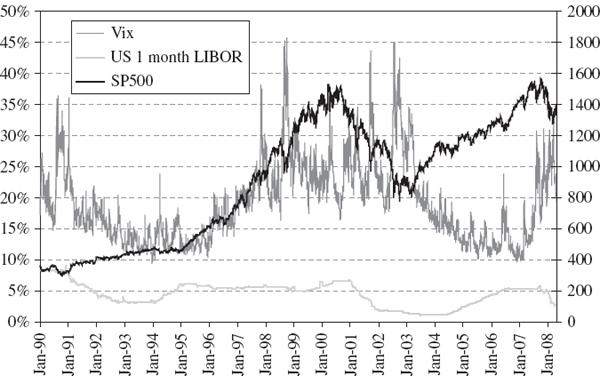

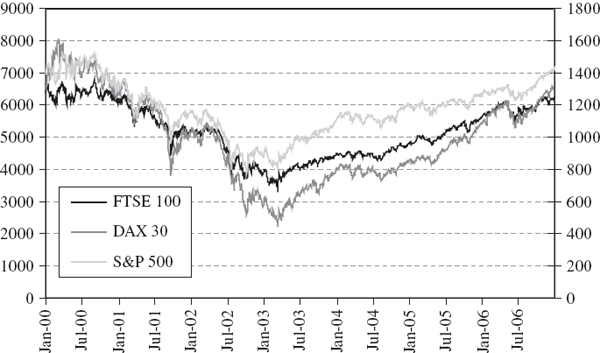

Daily data on these risk factors from 3 January 1990 until 25 April 2008 are displayed in Figure IV.5.2. The Vix and LIBOR are measured on the left hand scale and the index is measured on the right hand scale. The VaR will be measured on 25 April 2008, when the index futures price stood at almost 1400 and the Vix was at almost 20%. The main influence on the markets at this time, not just in the US but also in Europe and Asia, was the credit crunch that was precipitated by the sub-prime mortgage crisis in the US during 2007. To ease the credit squeeze, US interest rates had been cut considerably so that the 1-month LIBOR rate stood at only 2.86% at this time.

Figure IV.5.2 S&P 500 index price, Vix and 1-month US LIBOR, 1990–2008

Simulating Risk Factor Values

How should we simulate the risk factor values in the historical model? We know from our discussion in Section IV.3.2 that we need to use daily or even higher frequency returns on the risk factors so that we have enough data to measure VaR at the 99% or higher confidence level. This means that for h > 1 we have a choice between the following approaches, each having its own advantages and limitations.

(i) Estimate the VaR for a dynamically rebalanced position, and scale up the 1-day VaR estimate. This assumes that we rebalance the position each day to keep the Greeks constant.

(ii) Estimate the VaR for a static position using h-day simulations based on overlapping samples.

(iii) First estimate a parametric model for the conditional distributions of the returns in multi-step simulation, and then employ this model in the filtered historical simulation model of Barone-Adesi et al. (1998, 1999).22

The first two approaches have the advantage of simplicity but the disadvantage of inaccuracy. In case (i) the error stems from an assumption that the position has stable, i.i.d. returns and that we know the appropriate power law for scaling,23 and in case (ii) the error arises from the distortion of the tail behaviour of the portfolio return distribution.24 The third approach is more complex than the others, requiring the estimation of a GARCH model on the position's daily log returns and the application of the statistical bootstrap for simulation over the risk horizon.

We now ask how we should model the evolution of an option's risk factor returns in the framework of standard historical simulation. We shall answer this question in the context of a 1-day VaR estimate. Given T historical daily returns (or changes) on a risk factor, the first step in historical simulation is to derive the set,

![]()

of 1-day-ahead risk factor prices. For i = 1,…, n, each price ![]() it, is based on the current value

it, is based on the current value ![]() i of the risk factor when the VaR is measured and, under the assumption that the risk factor Xi follows a geometric process, we set

i of the risk factor when the VaR is measured and, under the assumption that the risk factor Xi follows a geometric process, we set

where rit = ln(Xit) − ln(Xi,t−1) is the daily log return on the risk factor, in the historical sample, at time t. But under the assumption that the risk factor Xi follows an arithmetic process, we use the daily changes xit = Xit − Xi,t − 1 and simulate the risk factor prices as

Should we use arithmetic or geometric stochastic processes to model the evolution of risk factors? Since we have a European option that is priced using the Black–Scholes–Merton formula, we should assume the underlying asset price follows a geometric Brownian motion. Thus the log return on the underlying price is a normally distributed random variable, and we should simulate prices using (IV.5.32). But what about the volatility and interest rate processes? It is not entirely clear whether these are governed by arithmetic or geometric processes in the real world. However, following our empirical results in Section II.5.3.6, I would advise that we assume the real-world processes for interest rates and volatility are also geometric. Hence, in all the case studies for this section we have used simulated interest rates and volatilities that are also based on (IV.5.32). This also has the advantage that simulated volatilities and interest rates cannot be negative.

Another reason to use log returns rather than absolute changes in risk factors is that over a long historical period there could be significant trends in the risk factors. In that case, an absolute change of 100 index points (or 100 basis points) ten years ago could have had quite a different significance compared to a similar change today.

It is also convenient to use log returns since the sum of h consecutive log returns is the h-day log return. Then, for a static VaR estimate, we use the h-day log return at time t, rhit to simulate the ith risk factor price h days ahead as

The result of the historical simulation of the underlying risk factors will be a set of 1-day ahead or h-day ahead values for the risk factors. The time ordering implicit in these values is not important, although it is important to couple the simulations of the values of different risk factors, to retain the implicit correlation between them. However, the time ordering of the returns that are used to generate these values can be important, to adjust for volatility clustering. In that case, the simulated risk factor values are generated from the volatility-adjusted returns.

Building the P&L Distribution and Estimating VaR

In the case of our simple S&P 500 option the risk factors are just the index futures price, the option's implied volatility, and the US LIBOR rate. In static VaR, the simulated values for the risk factors are used to revalue the option at the risk horizon. If the risk horizon is h days, the maturities of the simulated futures price, implied volatility and interest rate must be reduced by h days.

By way of illustration, consider a single standard European option position, and denote the price of the option at time t by25

![]()

Suppose the VaR is estimated at time t = 0. Then the forward looking discounted P&L from a long position on the option in h trading days, i.e. in hc calendar days, is

where f0 is the current value of the option, pv is the point value for the position and rhc is the hc-day continuously compounded discount rate. We know everything on the right-hand side of (IV.5.35) except for the option price fh in h trading days' (i.e. in hc calendar days') time.26 To simulate this, we apply the Black–Scholes–Merton pricing formula to a simulated pair (Sh, σh) of values for the underlying price Sh and for the option's implied volatility σh, in h trading days' time.

Taking each vector of simulated values of the risk factors in turn, we obtain the VaR estimate as follows:27

- With no rebalancing (i.e. static VaR) we obtain many simulated h-day-ahead portfolio values, from which we build an empirical distribution of the h-day portfolio P&L, and discount this to today. The 100α% h-day VaR is minus the α quantile of this distribution.

- With rebalancing to constant sensitivities (i.e. dynamic VaR) we obtain many simulated 1-day-ahead portfolio values, from which we build an empirical distribution of the daily portfolio P&L, and discount this to today. The 100α% 1-day VaR is minus the α quantile of this distribution. Then, to extrapolate this figure to an 100α% h-day VaR, we apply the square-root-of-time or some other power law scaling rule.

The next example compares the application of standard historical simulation to static and dynamic VaR estimates for a single option. Note that both approaches have errors: errors in static historical VaR arise from the use of historical overlapping samples, and errors in dynamic historical VAR arise from the use of a square-root scaling law. But these errors are unlikely to affect our decision about whether to apply static or dynamic VaR measures in the first place. This decision only depends on our assumptions about the position. If we are estimating the VaR of a non-traded position we use should static VaR, and if we are estimating the VaR of a trader's limits, or of his current position (assuming it is rebalanced to maintain constant risk factor sensitivities over the risk horizon) we should use dynamic VaR.

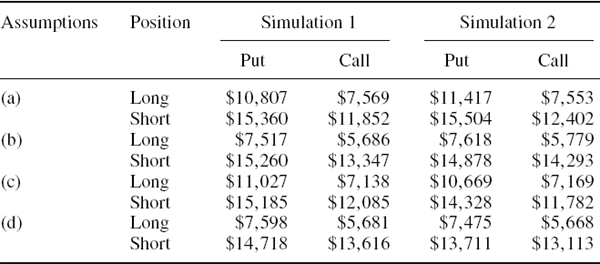

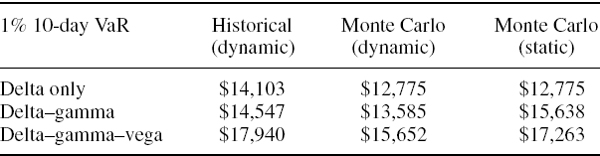

EXAMPLE IV.5.3: STATIC AND DYNAMIC HISTORICAL VAR FOR AN OPTION

Use standard historical simulation to estimate the 1% 10-day VaR for an unhedged position on a standard European call or put on the S&P 500 index. Estimate both

- static VaR, using 10-day overlapping returns on the risk factors, and

- dynamic VaR, scaling up the daily VaR to a 10-day horizon using the square-root-of-time rule.

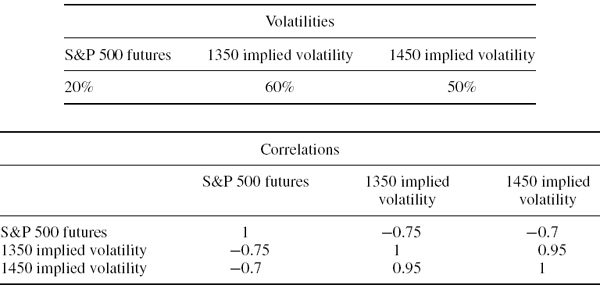

Consider long and short positions on a 30-day call and a 30-day put, both with strike 1400. The VaR is estimated on 25 April 2008 when the index is at 1400 and the index volatility is at 20%. For clarity, and since this will have very little effect on the result, assume the discount rate is 0%.28 Use the same historical scenarios on the S&P 500 index and the Vix volatility that were used in the previous example.

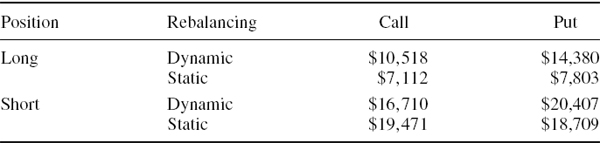

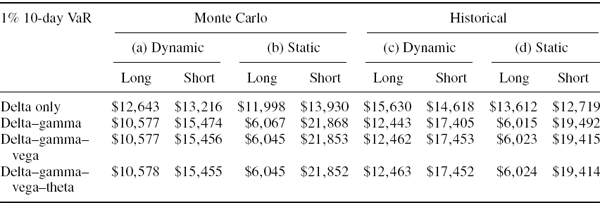

SOLUTION The spreadsheet for this example generates scenarios based on the daily log returns on the S&P 500 and Vix between 3 January 1990 and 25 April 2008, as we have described above. It prices the option using each of the simulated {price, volatility} scenarios. Then it calculates the P&L as the difference between the discounted scenario price and the current price of the option. This is the P&L for a long position, and the opposite difference is the P&L for the short position. Multiplying the lower 1% quantile of the distribution of these price changes by the index point value of $250 gives the 1% 10-day VaR of the unhedged position as in Table IV.5.5.

Long positions. Since the options have only 30 days to maturity the long positions have quite a large positive gamma; the gamma effect will decrease the static VaR considerably and the application of a square-root scaling rule to 1-day VaR would underestimate this gamma effect considerably. This is why the 10-day dynamic VaR estimates for the long positions, which are based on the square-root scaling rule, are considerably larger than the static VaR estimates. However, since the simulations based on overlapping data can truncate the tails of the P&L distribution, the static VaR estimates based on overlapping data may be too low at high confidence levels (see the discussion following this example).

Table IV.5.5 1% 10-day VaR under different rebalancing assumptions

Why is the dynamic VaR for the long put so much larger than the dynamic VaR for the long call? The reason is the vega effect. The option's positive vega has the effect of offsetting the VaR for a long call, but augmenting (or at least not offsetting) the VaR for a long put, as explained in Section IV.5.2.2. The dynamic VaR is assumed to be based on a square-root scaling rule, and this could understate or overstate the vega effect, depending on the option and the risk factor characteristics. In stock index options dynamic VaR estimates tend to overstate the vega effect. This is because the daily changes in volatility have a small, negative autocorrelation and at the daily level there is a pronounced asymmetry in the index price– volatility relationship which is not present in 10-day returns (see Section IV.4.4.4). For both of these reasons, the square-root scaling rule tends overstate the vega risk of stock index options.

Short positions. We already know from the previous example that short positions on naked options are much more risky than long positions. This is why their VaR estimates in Table IV.5.5 are much larger than the VaR estimates for the long positions. The short positions have a large negative gamma, which should increase the static VaR, but in the dynamic VaR estimates the portfolio is rebalanced to keep the gamma constant over the risk horizon, so the gamma effect is diminished.

If the gamma effect were the only effect to consider we might suppose that the dynamic VaR will be less than the static VaR, and this is certainly the case for the short call, but this is not the case for the short put. Again, the reason lies with the vega effect, which we know from our discussion in Section IV.5.2.2 will augment the VaR for the short put position. Since dynamic VaR estimates overstate the vega effect in stock index options, the dynamic VaR estimate for the short put position is larger than the static VaR estimate.

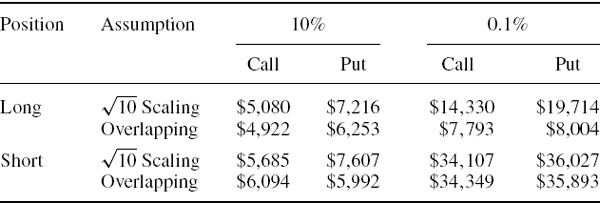

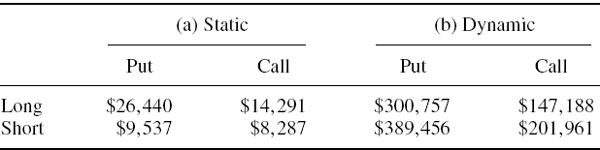

We know from our discussion in Section IV.3.2.7 that a potential problem with using overlapping data to estimate static VaR in the historical model is that the tail behaviour of the risk factor returns can be distorted so that VaR estimates at extreme quantiles may be too low. On the other hand, the use of a square-root scaling rule for dynamic VaR estimates also introduces errors, because at least one of the risk factors (i.e. volatility) is unlikely to scale with a square-root law.29 To illustrate these two sources of model risk, Table IV.5.6 shows the VaR estimates for the previous example, but now based on the 10% and 0.1% significance levels. Because we have a daily sample size of about 5000, there are only 500 non-overlapping 10-day P&Ls. This means that we can estimate the 10% quantile (by taking the 50th largest 10-day loss), and the 0.2% quantile is the largest loss. But we cannot measure the 0.1% quantile empirically, unless we use a statistical bootstrap, and the bootstrap merely increases the number of observations by repeating them. It introduces no new information to the data. So we only have an upper bound for the 0.1% quantile, i.e. the largest loss, which translates to a lower bound for the 0.1% VaR.

Using overlapping samples will generate about 5000 observations, but there is no new information in these data. Now it becomes possible to estimate the 0.1% quantile (as the 5th largest 10-day loss), but we would still underestimate the 0.1% quantile because the size of the 10-day losses is limited by the largest loss in the sample.

Table IV.5.6 Comparison of 10% and 0.1% 10-day VaR under different rebalancing assumptions

Looking at the results in Table IV.5.6, the 0.1% VaR estimates of long options exposures are far too low when based on overlapping data. This is evident from the estimates of only $7793 for the call and $8004 for the put. These 0.1% VaR estimates are not very much greater than the 10% VaR estimates! On the other hand, since we have a static position the VaR estimates based on the square-root scaling rule are too high for the long positions, and too low for the short positions, because they virtually ignore the gamma effects. They are also too high for the put relative to the call, because they overstate the vega effect, as discussed above.

In summary, there is a considerable amount of model risk in standard historical simulation when applying this methodology to measure static options VaR, even though there is no parametric model to estimate.

EXAMPLE IV.5.4: HISTORICAL VAR AND ETL OF A DELTA-HEDGED OPTION

On 25 April 2008 you sell a European put on the S&P 500 index futures with strike 1400 and maturity 30 days. The index futures price is at 1398, the market price of the option is 32, its delta is −0.4991 and its implied volatility is 19.42%. Use the historical data shown in Figure IV.5.2 to estimate the 1% 1-day VaR and ETL of the unhedged short put option position and of the delta hedged portfolio. Then compare the results with those for a long position on the put, and for both short and long positions on a call with the same strike and maturity, and the same market price as the put.30

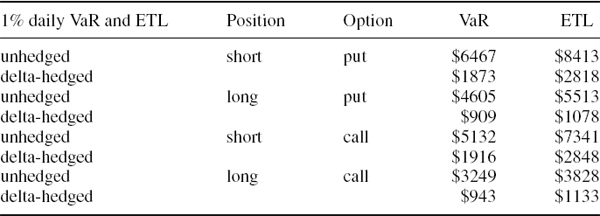

SOLUTION Note that these options are on the futures rather than the index, although we use the index to generate scenarios for the futures price as described earlier. So we price the options on the futures using each of the {futures price, volatility, interest rate} simulations.31 Then the unhedged P&L is calculated as the difference between the simulated option price, discounted by 1 day, and the current price of the option (i.e. 32). This is the P&L for a long position, and the opposite difference is the P&L for the short position. Multiplying the lower 1% quantile of the distribution of these price changes by the index point value of $250 gives the 1% 1-day VaR of the unhedged short put position as $6467. Clearly the VaR for naked short options position is huge, and that is why traders must hedge the options that they write.

Now consider a delta hedge that is held for a period of 1 day, offsetting the short put position by purchasing δ = −0.4980 (i.e. taking a short position) on the index futures.32 This time, the discounted price changes on the hedged portfolio are calculated for each of the historical scenarios. Multiplying the lower 1% quantile of the distribution of these price changes by the index point value gives the 1% 1-day VaR of the hedged short put position as $1873. This not small because we have not hedged the gamma or vega risk of the option.

For the ETL calculations we record the daily losses that exceed the 1% quantile of the daily P&L distribution.33 Then the estimate of the daily ETL is the average of these excess losses, i.e. $8413 for the naked short put position and $2818 for the delta-hedged portfolio. These figures represent the expected loss given that the VaR is exceeded, so they provide some idea of the potential for extreme losses on options positions.

Now we use the spreadsheet to estimate the 1% 1-day VaR and ETL for the long put, and for a short and a long position on a call with the same strike and maturity, i.e. 1400 and 30 days, a market price of 32 and an implied volatility of 20.67%.34 The results, which are displayed in Table IV.5.7, show that the long positions have much less risk than the short positions. This is because they have positive gamma. The gamma for 30-day near ATM options is relatively large, and that is why there is so much difference between the risk from going long and short these call and put options, even after delta-hedging.

Table IV.5.7 Comparison of VaR and ETL for long and short calls and puts

The historical P&L distribution has a very large excess kurtosis.35A long position also has a large positive skewness and a short position has a large negative skewness. The ETL increases with kurtosis in the P&L distribution but decreases with positive skewness. Hence the ETL is not very much greater than the VaR for a long position, but it is substantially greater than the VaR for a short position, particularly for the delta-hedged short positions. The long positions have an ETL that is approximately 20% greater than the VaR, whereas the delta-hedged short positions have an ETL that is about 50% greater than the VaR.

This example illustrates the huge risks taken by option traders and the clear need for accurate and active hedging. The 1% 1-day VaR of the unhedged short put is $6467, relative to a position value of 32 × $250 = $7750, and at $8413 the 1% 1-day ETL exceeds the position value. However, the delta-hedged short put has much lower VaR and ETL, and this is relative to an initial position value of (32 + 0.4980 × 1398) × $250 = $182,062.

We have already mentioned, several times, that ignoring the discount rate as a risk factor would have a negligible effect on the VaR. The next example justifies this statement empirically.

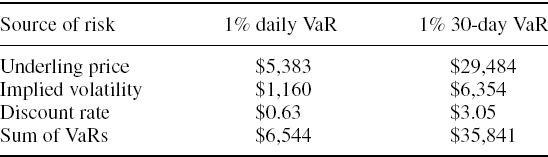

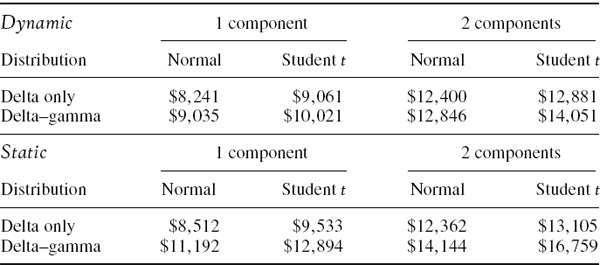

EXAMPLE IV.5.5: INTEREST RATE, PRICE AND VOLATILITY RISKS OF OPTIONS

Decompose the total historical VaR of the unhedged short put position in Example IV.5.4 into the VaR due to uncertainty in the underlying price, uncertainty in volatility and uncertainty in the discount rate. Then scale these figures up, using a square-root law, to estimate the dynamic VaR over the life of the option.

SOLUTION From Example IV.5.4 the total 1% 1-day VaR of the unhedged short put is $6467. To disaggregate this into stand-alone components we must create three separate historical simulations of the P&L where, instead of changing all three risk factors as in the previous example, we change only one of them. Thus the price risk is measured by a quantile of the P&L distribution generated by changing the underlying price but keeping volatility and discount rate constant at their current levels. Similarly, the volatility risk is measured by a quantile of the P&L distribution generated by changing the volatility but keeping price and discount rate constant at their current levels. And the interest rate risk is measured by a quantile of the P&L distribution generated by changing the discount rate but keeping price and volatility constant at their current levels. The results for the 1% 1-day VaR decomposition of the unhedged short put are shown in the first column of Table IV.5.8, and in the second column we have scaled these figures up to a 30-day risk horizon, using a square-root rule.36

These results show that by far the most important risk factor for an option is the underlying price. The volatility risk is substantial but still, the stand-alone price risk is almost four times the stand-alone volatility risk. The only inconsequential risk is that due to uncertainty in the discount rate.

Table IV.5.8 Disaggregation of option VaR into price, volatility and interest rate VaRs

IV.5.4.2 Dynamically Hedged Option Portfolios

Typically option traders will hold portfolios that are delta–gamma–vega neutral. Of course, as the underlying risk factors change, the hedges will have to be rebalanced. Rebalancing too frequently will erode any profits from writing options because of the transactions costs. It is therefore common to rebalance positions on a daily basis, to set the delta, gamma and vega back to zero. But the trader still runs substantial risks; and these risks would not be detected in daily VaR calculations based on delta–gamma–vega portfolio mapping, since the delta, gamma and vega will always be zero when the VaR is measured.37

To assess such risks we consider a simple European option that is gamma and vega hedged with other options on the same underlying and then delta hedged with the underlying, as explained in Section III.3.4.6. We compute the 1-day VaR of the hedged portfolio based on exact revaluation and then, assuming the portfolio is rebalanced to be delta–gamma–vega neutral at the end of each day, the 10-day dynamic VaR is estimated as ![]() times the 1-day VaR.

times the 1-day VaR.

EXAMPLE IV.5.6: VAR AND ETL FOR A DELTA–GAMMA–VEGA HEDGED PORTFOLIO

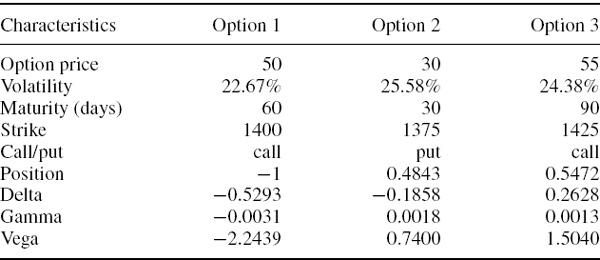

A trader writes a standard 60-day European call on the S&P 500 index futures with strike 1400 when the current index futures is at 1398. The call has a price of 50 and an implied volatility of 22.67%. To gamma–vega hedge he buys two other S&P 500 futures options: a 30-day put with strike 1375 and a 90-day call with strike 1425. The 30-day put has price 30 and implied volatility 25.58% and the 90-day call has price 55 and implied volatility 24.38%. Using the same historical {price, volatility, interest rate} simulations that were used in Example IV.5.4, estimate the 1% 10-day VaR and ETL of the delta–gamma–vega neutral portfolio assuming it is rebalanced at the end of each day to return the delta, gamma and vega to zero. Assume the discount rate is 2.75% at all maturities up to 90 days.

SOLUTION First, gamma–vega neutral positions are computed in the spreadsheet. Then the position delta of the gamma–vega hedged portfolio is used to determine the delta hedge position on the S&P 500 index. The resulting option positions and their risk factor sensitivities are shown in Table IV.5.9.

For gamma–vega neutrality we have a position of 0.4843 on the 30-day put and 0.5472 on the 90-day call. The resulting position in all three options has a net delta of −0.5293 −0.1858 + 0.2628 = −0.4523. We assume we can buy exactly this amount of the underlying in the delta neutral hedge, so that there is no residual position risk.

Table IV.5.9 Characteristics of European options on S&P 500 futures

The spreadsheet revalues each option on every historical simulation, computes the discounted total P&L on the gamma–vega neutral portfolio, and also computes the discounted P&L on the delta–gamma–vega neutral portfolio that includes the position on the S&P 500 index futures. Since we are assuming daily rebalancing to constant risk factor sensitivities, the 10-day historical VaR for the delta–gamma–vega neutral portfolio is calculated as −![]() times the lower 1% quantile of this P&L distribution, and the ETL is

times the lower 1% quantile of this P&L distribution, and the ETL is ![]() times the average of the losses that exceed the 1% quantile of the distribution.

times the average of the losses that exceed the 1% quantile of the distribution.

The VaR is not zero: the 1% 10-day VaR is $871. And the 1% 10-day ETL is $968. We conclude that even when traders rebalance daily to delta–gamma–vega neutral positions they can run significant risks. This is because we have only hedged against small changes in the price and volatility risk factors. A delta–gamma–vega hedged portfolio would have a much smaller risk if it were rebalanced more frequently than once per day, but then the transactions costs could erode any benefit from hedging.

Readers may verify that the result in the above example is not unusual. Changing the options in the spreadsheet leads to similar results, i.e. the dynamic VaR for a delta–gamma–vega neutral portfolio is not insignificantly different from zero. As already mentioned, this is because the VaR estimate is based on exact revaluation: of course the dynamic VaR estimate would be zero if we based it on a delta–gamma–vega mapping, because the portfolio is rebalanced daily to set the delta, gamma and vega to zero.

IV.5.4.3 Greeks Approximation

The aim of this section is to illustrate the method for computing historical VaR when options have been mapped to risk factors. For an option portfolio on a single underlying, mapped to a single volatility risk factor, a delta-gamma–vega–theta representation allows us to approximate the price of the portfolio h trading days (and hc calendar days) ahead as

where f0 is the price of the portfolio today, Δt = hc/365, ΔS is the difference between an underlying price in h trading days' time, derived from a simulated daily log return on S, and the price today, σ is the difference between the simulated volatility in h trading days' time and the volatility today, and θP, δP, γP and νP are the position Greeks of the portfolio. Now the approximate discounted P&L on the portfolio may be written

where pv is the point value for options on this underlying.38

More detailed risk factor mappings could add other Greeks, such as rho (the sensitivity to changes in interest rates) or higher order sensitivities like vanna and volga. But the minor Greeks such as rho, vanna and volga usually have little effect on the portfolio VaR, as we demonstrate in this section, so delta–gamma–vega–theta mapping is often sufficient.

When using standard historical simulation for options we are always faced with the choice between, on the one hand, estimating static VaR and using overlapping data for ΔS and Δσ, and, on the other hand, estimating the dynamic VaR by basing (IV.5.37) on a risk horizon of 1 day and then scaling up the result to a risk horizon of h days. The following example illustrates the effect of this decision, and also examines the accuracy of VaR estimates based on Greeks approximations.

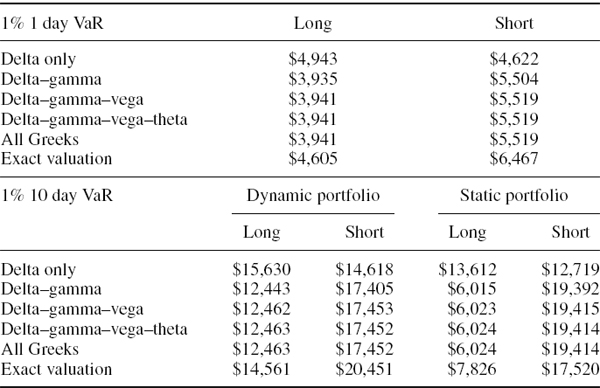

EXAMPLE IV.5.7: HISTORICAL VAR WITH GREEKS APPROXIMATION

Estimate the 1% 1-day and 10-day VaR of long and short positions on the put option in Example IV.5.4, and for the 10-day VaR. Assume first that the position is rebalanced daily to return the risk factor sensitivities to their values at the time the VaR is estimated, and then that the position is held static. Compare the results for a long and a short position on the put, based on delta-only, delta–gamma, delta–gamma–vega, delta–gamma–vega–theta and delta–gamma–vega–theta–vanna–volga–rho approximations.

SOLUTION In the spreadsheet for this example, the dollar Greeks are held constant and applied to the same historical {futures price, volatility, interest rate} simulations as in Example IV.5.4.39 The results are displayed in the top half of Table IV.5.10. Note that the results based on exact revaluation were already obtained in Table IV.5.5, Example IV.5.4.

The ‘delta only’ VaR is imprecise because it is a linear approximation to a highly non-linear relationship. The delta only approximation behaves like a linear portfolio, and as we know from previous chapters, the VaR can be greatly affected by non-constant volatility. The put has a positive gamma and so the delta–gamma VaR for the long position is less than the VaR based on the delta only approximation. But the opposite is the case for the short put position: there were many large negative price changes in the S&P 500 futures during the historical period, and the negative gamma increases the sensitivity of the option to such moves.

The delta–gamma–vega VaR figures include the portfolio's price changes due to changes in volatility. Changes in volatility have two effects on the portfolio's VaR. One effect is that the VaR increases due to the addition of another risk factor. If this were the only effect then VaR would increase, whatever the sign of the portfolio vega. But there is a second effect that is due to the correlation between the index price changes and the volatility changes, which is negative in this case. The net effect of adding the volatility risk factor to the delta–gamma representation is therefore indeterminate; it could increase or decrease the VaR.

Table IV.5.10 Historical VaR with Greeks approximation

It is clear from our results that once a delta–gamma–vega approximation is used, adding further Greeks has little effect on the VaR. But the most striking thing about these results is that the 1% VaR based on the Greeks approximation is considerably less than the VaR based on exact revaluation. Why is this difference so large? The main reason is that the historical VaR estimate is driven by some very large changes in the risk factors during the historical period. Specifically, there were some large price rises and volatility falls which have affected the long put, and some very large price falls and volatility rises which have affected the short put. A Greeks approximation is only accurate for small changes in the risk factors.

Now consider the 10-day VaR figures in the lower part of Table IV.5.10. When we assume daily rebalancing we approximate the 10-day VaR in the spreadsheet labelled ‘Dynamic VaR’ as the square root of 10 times the 1-day VaR. Under the no rebalancing assumption, we evaluate the 10-day VaR directly, in the spreadsheet labelled ‘Static VaR’, using overlapping data. The delta–gamma VaR is again less than the delta only VaR, for a long position, and greater than the delta only VaR for a short position. But now we can see that the gamma effect is much larger in the static VaR estimate than it is in the dynamic VaR estimate. This is because the dynamic VaR captures only a very small gamma effect, over a 1-day horizon only, and this is much smaller than the gamma effect over an h-day horizon.

This example shows that if we try to estimate VaR for a static options position or portfolio, by scaling up 1-day VaR estimates to a longer risk horizon, we will seriously underestimate the gamma effect on VaR. We would also underestimate the theta effect and distort the vega effect.40 Instead we should compute static VaR estimates, i.e. we should estimate VaR directly from the h-day P&L distribution, without scaling up a short-term VaR estimate to a longer-term risk horizon, and use exact revaluation if possible. However, the problem with using standard historical simulation here is that the tails of the h-day P&L distribution become truncated, so the VaR at extreme percentiles, and the ETL, are underestimated.

The exact revaluation of complex options without analytic expressions for the price requires a significant computational effort. Hence, it is often necessary to use a Greeks approximation to compute historical VaR. But the above example highlights a major problem with the application of Greeks approximation in the estimation of historical VaR for an option portfolio. Historical scenarios on daily changes in the risk factors are not always small changes; indeed, it is precisely the large changes in the risk factors that influence the VaR estimates, especially at extreme quantiles. Hence the application of standard historical simulation to obtain VaR estimates based on Greeks approximations is prone to imprecision.

The next example shows how delta–gamma–vega approximation is applied to estimate the VaR of a large portfolio containing options on several correlated underlyings. We consider an options trading book held by a UK bank on 31 December 2006, containing standard European options on UK, US and German stocks. The risk factors are the stock index futures and their respective volatility indices. To avoid having to concatenate constant maturity futures time series over a long historical period, we again infer the changes in the futures from the changes in the spot index. Hence, we assume the basis risk is zero, which introduces a small error in the calculation, but this is a very minor source of model risk in VaR models for portfolios of options on major indices.