IV.2

Parametric Linear VaR Models

IV.2.1 INTRODUCTION

The parametric linear model calculates VaR and ETL using analytic formulae that are based on an assumed parametric distribution for the risk factor returns, when the portfolio value is a linear function of its underlying risk factors. Specifically, it applies to portfolios of cash, futures and/or forward positions on commodities, bonds, loans, swaps, equities and foreign exchange. The most basic assumption, discussed in the previous chapter, is that the returns on the portfolio are independent and identically distributed with a normal distribution. Now we extend this assumption so that we can decompose the portfolio VaR into VaR arising from different groups of risk factors, assuming that the risk factor returns have a multivariate normal distribution with a constant covariance matrix. We derive analytic formulae for the VaR and ETL of a linear portfolio under this assumption and also when risk factor returns are assumed to have a Student t distribution, or a mixture of normal or Student t distributions.

In bond portfolios, and indeed in any interest rate sensitive portfolio that is mapped to a cash flow, the risk factors are the interest rates of different maturities that are used to both determine and discount the cash flow. When discounting cash flows between banks we use a term structure of LIBOR rates as risk factors. Additional risk factors may be introduced when a counterparty has a credit rating below AA. For instance, the yield on a BBB-rated 10-year bond depends on the appropriate spread over LIBOR, so we need to add the 10-year BBB-rated credit spread to our risk factors. More generally, term structures of credit spreads of different ratings may also appear in the market risk factors: when portfolios contain transactions with several counterparties having different credit ratings, one credit spread term structure is required for each different rating.

There is a non-linear relationship between the value of a bond or swaps portfolio and interest rates. However, this non-linearity is already captured by the sensitivities to the risk factors, which are in present value of basis point (PV01) terms. Hence, we can apply the parametric linear VaR model by representing the portfolio as a cash flow, because the discount factor that appears in the PV01 is a non-linear function of the interest rate.

We may also base parametric linear VaR and ETL estimates on an equity factor model, provided it is linear, which is very often the case. Foreign exchange exposures are based on a simple linear proportionality, and commodity portfolios can be mapped as cash flows on term structures of constant maturity forwards or interest rates. Thus, the only portfolios to which the parametric linear VaR method does not apply are portfolios containing options, or portfolios containing instruments with option-like pay-offs. That is, whenever the portfolio's P&L function is a non-linear function of the risk factors, the model will not apply.

In the parametric linear VaR model, all co-dependencies between the risk factors are assumed to be represented by correlations. We represent these correlations, together with the variance of each risk factor over some future risk horizon h, in an h-day covariance matrix. It is this covariance matrix – and in mixture linear VaR models there may be more than one covariance matrix – that really drives the model. To estimate the covariance matrix we employ a moving average model.1 These models assume the risk factors are i.i.d. From this it follows that the h-day covariance matrix is just h times the 1-day covariance matrix, a result that is commonly referred to as the square-root-of-time rule.2

In the standard parametric linear VaR model we cannot forecast the covariance matrix using a GARCH model.3 When a return is modelled with a GARCH process it is not i.i.d.; instead it exhibits volatility clustering. As a result the square-root-of-time rule does not apply. However, this is not the reason why we cannot use a GARCH process in the parametric linear VaR model. The problem is that when a return follows a GARCH process we do not know the exact price distribution h days from now. We know this distribution when the returns are i.i.d., because it is the same as the distribution we have estimated over a historical sample. But the h-day log return in a GARCH model is the sum of h consecutive daily log returns and, due to the volatility clustering it is the sum of non-i.i.d. variables. Thus far, we only know the moments of the h-day log return distribution, albeit for a general GARCH process.4

The outline of this chapter is as follows. In Section IV.2.2 we introduce the basic concepts for parametric linear VaR. Starting with VaR estimation at the portfolio level (i.e. we consider the returns or P&L on a portfolio, without any risk factor mapping), we examine the properties of the i.i.d. normal linear VaR model and then extend this assumption to the case where returns are still normally distributed, but possibly autocorrelated. This assumption only affects the way that we scale VaR estimates over different risk horizons; the formula for 1-day VaR remains the same. An extension of the normal linear VaR formula for h-day VaR is derived for the case where daily returns are autocorrelated, and this is illustrated with a numerical example.

Then we consider the more general case, in which we assume the portfolio has been mapped to its risk factors using an appropriate mapping methodology.5 We provide the mathematical definitions, in the general context of the normal linear VaR model, of the different components of the total VaR of a portfolio. The total VaR may be decomposed into systematic (or total risk factor) VaR and specific (or residual) VaR, where the systematic VaR is the VaR that is captured by the risk factor mapping. The systematic VaR may be further decomposed into stand - alone VaR or marginal VaR components, depending on our purpose:

- Stand-alone VaR estimates are useful for estimating the risk of a particular activity in isolation, without considering any netting or diversification effects that this activity may have with other activities in the firm. Diversification effects are accounted for when aggregating stand-alone VaRs to a total risk factor VaR. The ordinary sum of the stand-alone VaRs is usually greater than the total risk factor VaR, and in the normal linear VaR model it can never be less that the total risk factor VaR.

- Marginal VaR estimates are useful for the allocation of real capital (as opposed to economic capital) because the sum of all the marginal VaR estimates is equal to the total risk factor VaR (and real capital must always add up).

The next five sections provide a large number of numerical and empirical examples, and two detailed case studies, on the application of the normal linear model to the estimation of total portfolio VaR. We focus on the decomposition of the systematic VaR into components corresponding to different types of risk factor. Each section provides a detailed analysis of a different type of asset class.

- Section IV.2.3 examines the VaR of interest rate sensitive portfolios. These portfolios are represented as a sequence of cash flows that are mapped to standard maturities along a term structure of interest rates. Their risk factors are the LIBOR curve and usually one or more term structures of credit spreads. The risk factor sensitivities are the PV01s of the mapped cash flows. Here we use numerical examples to show how to disaggregate the total VaR into LIBOR VaR and credit spread VaR components.

- Section IV.2.4 presents the first case study of this chapter, on the estimation of VaR for a portfolio of UK bonds. We demonstrate how to use principal component analysis to reduce the dimension of the risk factors from 60 to only 3, and describe some risk management applications of this technique.

- Section IV.2.5 examines the normal linear VaR for stock portfolios, from a small portfolio with just a few positions on selected stocks, to a large international portfolio that has been mapped to broad market risk factors. We focus on the decomposition of VaR into systematic and specific factors, and the moving average methods that are used to estimate the covariance matrix.

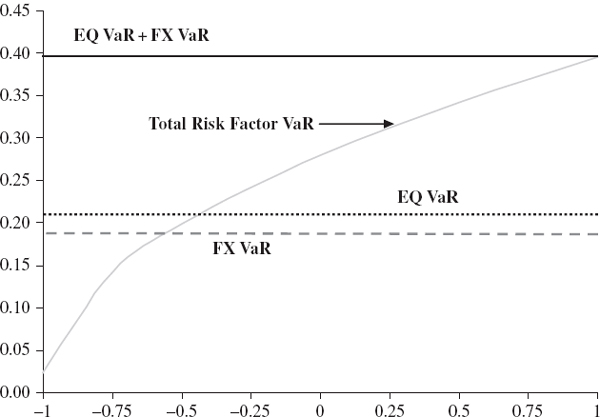

- Section IV.2.6 shows how to estimate the total VaR for an international stock portfolio, how to decompose this into specific and systematic VaR, and how to disaggregate total VaR into equity VaR, foreign exchange (forex) VaR and interest rate VaR components. We use numerical and empirical examples to calculate stand-alone and marginal VaR components for different types of risk factor, and to illustrate the sub-additivity property of normal linear VaR when component VaRs are aggregated.

- Section IV.2.7 presents a case study on the normal linear VaR of a commodity futures trading desk, using constant maturity futures as risk factors.

There are three other parametric linear VaR models that have analytic solutions for VaR. These are the Student t, the normal mixture and the Student t mixture models. They are introduced and illustrated in Sections IV.2.8 and IV.2.9. Of course, other parametric forms are possible for return distributions but these do not lead to a simple analytic solution and instead we must use Monte Carlo resolution methods. The formulae that we derive in Section IV.2.8 are based on the assumption that returns are i.i.d. We describe a simple technique to extend these formulae so that they assume autocorrelated returns. However, to include volatility clustering we would normally use Monte Carlo simulation for the resolution.6

Section IV.2.10 explains how exponentially weighted moving averages (EWMAs) are applied in the parametric linear VaR model, with a particular emphasis on the advantages and limitations of the RiskMetrics™ VaR methodology that was introduced by JP Morgan in the 1990s. Section IV.2.11 derives analytic formulae for the expected tail loss associated with different parametric linear VaR models. The formal derivation of each formula is then illustrated with numerical examples. Section IV.2.12 presents a case study on estimating the VaR and ETL for an exposure to the iTraxx Europe 5-year credit spread index. The distribution of daily changes in the iTraxx index has a significant negative skew and a very large excess kurtosis and, of the alternatives considered here, we demonstrate that its highly non-normal characteristics are best captured by a mixture linear VaR model. Section IV.2.13 concludes by summarizing the main results in this long chapter. As usual there are numerous interactive Excel spreadsheets on the CD-ROM to illustrate virtually all of the examples and all three case studies.

IV.2.2 FOUNDATIONS OF NORMAL LINEAR VALUE AT RISK

This section introduces the normal linear VaR formula, first when VaR is measured at the portfolio level and then when the systematic VaR is measured by mapping the portfolio to its risk factors. We also discuss the rules for scaling normal linear VaR under both i.i.d. and autocorrelated returns. Then we derive the risk factor VaR, and its disaggregation into stand-alone VaR components and into marginal VaR components. We focus on consequences of the normal linear model's assumptions for aggregating VaR. Finally, we derive the incremental VaR, i.e. the impact on VaR of a small trade, in a linear portfolio with i.i.d. normally distributed returns.

IV.2.2.1 Understanding the Normal Linear VaR Formula

The formal definition of VaR was given in Section IV.1.4, and we summarize it here for convenience. Let

be the discounted h-day return on a portfolio. Here Bht denotes the price of a discount bond maturing in h trading days and Pt denotes the value of the portfolio at time t. Then the 100α% h-day VaR estimated at time t is

where xht, α is the lower α quantile of the distribution of Xht, i.e. P(Xht < xht, α) = α.

Derivation of the Formula

The normal linear VaR formula was derived in Section IV.1.5.1. It is convenient to summarize that derivation here, but readers should return to Section IV.1.5 if the following is too concise. In the normal linear VaR model we assume the discounted h-day returns on the portfolio follow independent normal distributions, i.e. Xht is i.i.d. and

The parameters μht and σht are the forecasts made at time t of the portfolio's expected return over the next h days, discounted to today, and its standard deviation. Amongst other things, these will depend on both the risk horizon and the point in time at which they are forecast.

Applying the standard normal transformation to (IV.2.2) gives7

where Z is a standard normal variable. Thus

where Φ−1(α) is the standard normal α quantile value, such as

By the symmetry of the normal distribution function,

![]()

Hence, substituting the above and (IV.2.1) into (IV.2.3) gives the 100α% h-day parametric linear VaR at time t, expressed as a percentage of the portfolio value, as

To estimate normal linear VaR we require forecasts of the h-day discounted mean and standard deviation of the portfolio return, and to obtain these forecasts we can make up scenarios for their values, scenarios that would normally be based on the portfolio's risk factor mapping, so that we can find separate scenario estimates for the different risk factor component VaRs. Alternatively, we can base the forecasts for the mean and standard deviation of the portfolio return on historical data for the assets or risk factors. This is useful, to compare with the results based on the historical simulation model using identical data.

When using historical data, for a long-only portfolio we would create a constant weighted historical return series based on the current allocations.8 Then we base our (ex-ante) forecasts of the mean and standard deviation on the (ex-post) sample estimates of mean and variance.

For a long-short portfolio we use changes (P&L) on the risk factors and keep the holdings constant rather than the portfolio weights constant. For a cash-flow map, we keep the PV01 vector constant, and use absolute changes in interest rates and credit spreads. In both cases we produce a P&L series for the portfolio. Then the mean and standard deviation of the P&L distribution, and hence also the VaR, are estimated directly in value terms.

Drift Adjustment

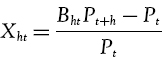

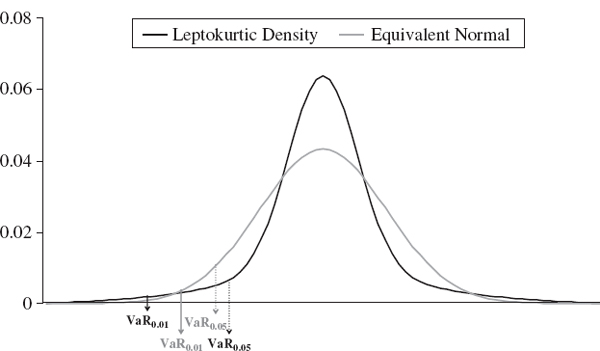

From the discussion in Section IV.1.5.2 we know that a non-zero discounted expected return μht can be important. Fund managers, for instance, may sell their services on the basis of expecting returns in excess of the discount rate. Figure IV.2.1 illustrates how a positive mean discounted return will have the effect of reducing the VaR. We have drawn here a normally distributed h-day discounted returns density at time t, with positive mean μht and where the area under the curve to the left of the point μht − Φ−1(1 − α)σht is equal to α, by the definition of VaR.

Figure IV.2.1 Illustration of normal linear VaR

In Section IV.1.5.2 we showed that it is only for long risk horizons and when a portfolio is expected to return substantially more than the discount rate that the drift adjustment to VaR, i.e. the second term in (IV.2.5), will have a significant effect on VaR. Hence, we often assume the portfolio is expected to return the risk free rate so that μht, the present value of the expected return, is zero. We shall assume this in the following, unless explicitly stated otherwise.

Without the drift adjustment, the normal linear VaR formula is simply

![]()

Henceforth in this chapter we shall also drop the implicit dependence of the VaR estimate on the time at which the estimate is made, and write simply

for the 100α% h-day VaR estimate made at the current point in time, when the portfolio's expected return is the discount rate.

Scaling VaR to Different Risk Horizons

When normal linear VaR estimates are based on daily returns to the portfolio, we obtain a 1-day VaR estimate using the daily mean μ1 and standard deviation σ1 in the VaR formula. How can we scale this 1-day VaR estimate up to a 10-day VaR estimate, or more generally to an h-day VaR estimate?

The normal linear VaR estimate assumes that the daily returns are i.i.d. We have to approximate the returns by the log returns, as explained in Section IV.1.5.4, then

- the h-day mean is h × daily mean, μh = hμ1;

- the h-day variance is h × daily variance,

.

.

In this case, it now follows directly from (IV.2.5) that

![]()

So, under the assumption of i.i.d. returns, it is only when the portfolio is expected to return the discount rate, i.e. μ1 = 0, that

Note that the scaling argument above applies to any base frequency for the VaR. For instance, we could replace ‘day’ with ‘month’ above. Then the square-root-of-time scaling rule will apply to scaling the 1-month VaR to longer horizons, but only if we assume the monthly return on the portfolio is the risk free (discount) rate. For example, if this assumption holds and the 1-month VaR is 10% of the portfolio value, then the 6-month VaR will be ![]() of the portfolio value. When returns are normal and i.i.d. and the expected return on the portfolio is the risk free rate, we could also apply the square-root law for scaling from longer to shorter horizons. For example, annual VaR = 25%⇒ monthly VaR = 25% × 12−½ = 7.22%.

of the portfolio value. When returns are normal and i.i.d. and the expected return on the portfolio is the risk free rate, we could also apply the square-root law for scaling from longer to shorter horizons. For example, annual VaR = 25%⇒ monthly VaR = 25% × 12−½ = 7.22%.

However, the square-root scaling rule should be applied with caution. Following our discussion in Section IV.1.5.4, we know that even when the returns are i.i.d. the square-root scaling rule is not very accurate, except for scaling over a few days, because we have to make a log approximation to returns and this approximation is only accurate when the return is very small.9 Moreover, it does not usually make sense to scale 1-day VaR to risk horizons longer than a few days, because the risk horizon refers to the period over which we expect to be able to liquidate (or completely hedge) the exposure. Typically portfolios are rebalanced very frequently and the assumption that the portfolio weights or risk factor sensitivities remain unchanged over more than a few days is questionable. Hence, to extrapolate a 1-day VaR to, for instance, an annual VaR using a square-root scaling rule is meaningless.

How Large is VaR?

The assumption that portfolio returns are i.i.d. and normal is usually not justified in practice, so the normal linear VaR model gives only a very crude estimate for VaR. However, this is still very useful as a benchmark. It provides a sort of ‘plain vanilla’ VaR estimate for a linear portfolio, against which to measure more sophisticated models.

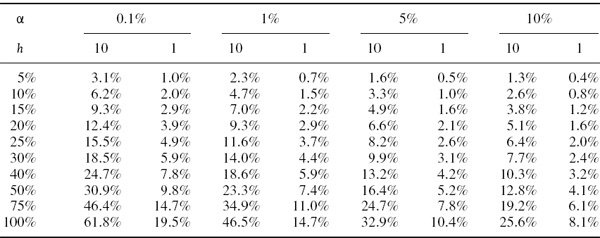

Table IV.2.1 illustrates the normal linear VaR given by (IV.2.6) for different levels of volatility and some standard choices of significance level and risk horizon. All VaR estimates are expressed as a percentage of the portfolio value. Each row corresponds to a different volatility, and these volatilities range from 5% to 100%. We only include risk horizons of 1 day and 10 days in the table, since the VaR for other risk horizons can easily be derived from these. In fact, we only really need to display the 1-day VaR figures, because the corresponding 10-day VaR is just ![]() times the 1-day VaR under the i.i.d. normal assumption.

times the 1-day VaR under the i.i.d. normal assumption.

Table IV.2.1 Normal linear VaR for different volatilities, significance levels and risk horizons

In our empirical examples we shall very often calculate the 1% 10-day VaR, as this is the risk estimate that is used for market risk regulatory capital calculations. Hence, from the results in Table IV.2.1:

- in major currency portfolios that have recently had volatility in the region of 10%, we would expect the 1% 10-day VaR estimate to be about 5% of the portfolio value;

- equity portfolios, with volatilities running at 40–60% at the time of writing, could have 1% 10-day VaR of about 25% of the portfolio value;

- credit spreads have been extremely volatile recently and so interest rate VaR is unusually high at the moment, unless all counterparties have AA credit rating;

- energy portfolios, and many other commodity portfolios, tend to have the highest VaR. With oil prices being highly volatile at the time of writing, the 1% 10-day VaR for energy portfolios could be up to 40% of the portfolio value!

IV.2.2.2 Analytic Formula for Normal VaR when Returns are Autocorrelated

It is important to simplify models when they are applied to thousands of portfolios every day. A very common simplification is that returns are not only normally distributed but also generated by an i.i.d. process. But in most financial returns series this assumption is simply not justified. Many funds, and hedge funds in particular, smooth their reported results, and this introduces a positive autocorrelation in the reported returns. Even when returns are not autocorrelated, squared returns usually are, when they are measured at the daily or weekly frequency. This is because of the volatility clustering effects that we see in most markets.

There are no simple formulae for scaling VaR when returns have volatility clustering. Instead, we could apply a GARCH model to simulate daily returns over the risk horizon, as explained in Sections IV.3.3.4 and IV.4.3. In this section we derive a formula for scaling VaR under the assumption that the daily log returns rt are not i.i.d. but instead they follow a first order autoregressive process where ![]() is the autocorrelation, i.e. the correlation between adjacent log returns.10

is the autocorrelation, i.e. the correlation between adjacent log returns.10

Write the h-period log return as the sum of h consecutive one-period log returns:

Assuming the log returns are identically distributed, although no longer independent, we can set μ = E(rt+i) and σ2 = V(rt+i) for all i. Autocorrelation does not affect the scaling of the expected h-period log return, since ![]() . So the h-day expected log return is the same as it is when the returns are i.i.d.

. So the h-day expected log return is the same as it is when the returns are i.i.d.

But autocorrelation does affect the scaling standard deviation. Under the first order autoregressive model the variance of the h-period log return is

Now we use the identity

Setting x = ![]() and n = h − 1 in (IV.2.8) gives

and n = h − 1 in (IV.2.8) gives

This proves that when returns are autocorrelated with first order autocorrelation coefficient ![]() then the scaling factor for standard deviation is not

then the scaling factor for standard deviation is not ![]() but

but ![]() , where

, where

Hence, we should scale normal linear VaR as

Even a small autocorrelation has a considerable effect on the scaling of volatility and VaR. The following example shows that this effect is much more significant than the effect of a mean adjustment term when the portfolio is not expected to return the risk free rate. Thus for the application of parametric linear VaR to hedge funds, or any other fund that smoothes its returns, the autocorrelation adjustment is typically more important than an adjustment to the VaR that accounts for a positive expected excess return.

EXAMPLE IV.2.1: ADJUSTING NORMAL LINEAR VAR FOR AUTOCORRELATION

Suppose a portfolio's daily log returns are normally distributed with a standard deviation of 1% and a mean of 0.01% above the discount rate. Calculate (a) the portfolio volatility and (b) the 1% 10-day normal linear VaR of the portfolio under the assumption of i.i.d. daily log returns and under the assumption that daily log returns are autocorrelated with first order autocorrelation ![]() = 0.2.

= 0.2.

SOLUTION Under the i.i.d. assumption and assuming 250 trading days per year, the annual excess return is 0.01% × 250 = 2.5% and the volatility is

![]()

The 1% 10-day VaR is

![]()

That is, the 1% 10-day VaR is 7.26% of the portfolio's value.

But under the assumption that daily log returns have an autocorrelation of 0.2, the volatility and the VaR will be greater. The adjustment factor, i.e. the second term on the right-hand side of (IV.2.10) is calculated in the spreadsheet. It is 124.375 for h = 250, and 4.375 for h = 10. Hence, the volatility is

![]()

and the 1% 10-day VaR is

![]()

That is, the 1% 10-day VaR is now 8.72% of the portfolio's value.

Following this example, some general remarks are appropriate.

- Even this relatively small autocorrelation of 0.2 increases the 1% 10-day VaR by about one-fifth, whereas the daily mean excess return of 0.01% (equivalent to an annual expected return of 2.5% above the discount rate) only decreases the 1% 10-day VaR by 0.1%.

- The higher the autocorrelation and the longer the risk horizon, the greater the effect that a positive autocorrelation has on increasing the VaR. For higher autocorrelation and longer risk horizons, the VaR could easily double when autocorrelation is taken into account. And of course, negative autocorrelation decreases the VaR in a similar fashion.

IV.2.2.3 Systematic Normal Linear VaR

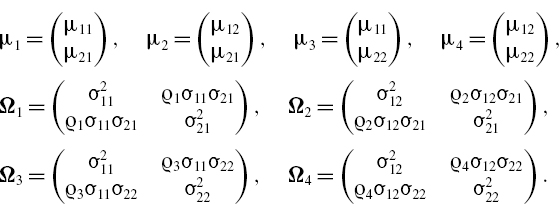

For reasons that have been discussed in the previous chapter, it is almost always the case that the risk manager will map each portfolio to a few well-chosen risk factors.11 The systematic return or P&L on a portfolio is the part of the return that is explained by variations in the risk factors. In a linear portfolio it may be represented as a weighted sum,

where Xi denotes the return or P&L on the ith risk factor and the coefficients θi denote the portfolio's sensitivity to the ith risk factor.12 If we use the risk factor returns on the right-hand side of (IV.2.12) rather than their P&L, and the sensitivities are measured in percentage terms, then Y is the systematic return; otherwise Y is the systematic P&L on the portfolio.13

To calculate the systematic normal linear VaR we need to know the expectation E(Yh) and variance V(Yh) of the portfolio's h-day systematic return or P&L. We can use the factor model (IV.2.12) to express these in terms of the expectations, variances and covariances of the risk factors. To see this, write the vector of expected excess returns on the risk factors as

![]()

write the vector of current sensitivities to the m risk factors as θ =(θ1,…, θm)′ and denote the m × m covariance matrix of the h-day risk factor returns by Ωh. Then the mean and variance of the portfolio's h-day systematic returns or P&L may be written in matrix form as14

The normal linear VaR model assumes that risk factors have a multivariate normal distribution; hence, the above mean and variance are all that is required to specify the entire distribution. Substituting (IV.2.13) into (IV.2.5) gives the following formula for the 100α% h-day systematic VaR:

In many cases we assume that the expected systematic return is equal to the discount rate, in which case the discounted mean P&L will be zero and (IV.2.14) takes a particularly simple form:

The above shows how the systematic normal linear VaR can be obtained straight from the risk factor mapping. We only need to know the current:

- estimate of the risk factor sensitivities θ;

- forecast of the h-day risk factor returns covariance matrix Ωh.

Note that both these inputs can introduce significant errors into the VaR estimate, as will be discussed in detail in Chapter IV.6.

A common assumption is that each of the risk factors follows an i.i.d. normal process. In the absence of autocorrelation or conditional heteroscedasticity in the processes, the square-root-of-time rule applies. In this case,

In other words, each element in the 1-day covariance matrix is multiplied by h. Thus, just as for the total VaR in (IV.2.7), the h-day systematic VaR (IV.2.15) can be scaled up from the 1-day systematic VaR using a square-root scaling rule:

![]()

Two simple numerical examples of normal linear systematic VaR have already been given in Section IV.1.6. A large number of much more detailed examples and case studies on normal linear systematic VaR for cash flows, stock portfolios, currency portfolios and portfolios of commodities will be given in this chapter and later in the book.

IV.2.2.4 Stand-Alone Normal Linear VaR

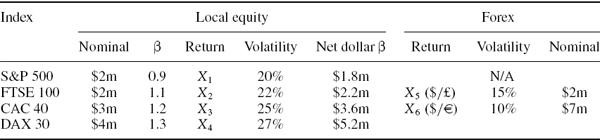

In Section IV.1.7 we explained, in general non-technical terms, how systematic VaR may be disaggregated into components consisting of either stand-alone VaR or marginal VaR, due to different types of risk factor. The stand-alone VaR is the systematic VaR due to a specific type of risk factor. So, depending on the type of risk factor, stand-alone VaR may be called equity VaR, forex VaR, interest rate VaR, credit spread VaR or commodity VaR.

Due to the diversification effect between risk factor types, and using the summation rule for the variance operator, in the normal linear model the sum of the stand-alone VaRs is greater than or equal to the total systematic VaR, with equality only in the trivial case where all the risk factors are perfectly correlated. However, in the next subsection we show how to transform each stand-alone VaR into a corresponding marginal VaR, where the sum of the marginal VaRs is equal to the total risk factor VaR.

In this subsection we specify the general methodology for calculating stand-alone VaRs in the normal linear VaR model. Although the derivation of theoretical results is set in the context of the normal linear VaR model, it is important to note that similar aggregation and decomposition rules apply to the other parametric linear VaR models that we shall introduce later in this chapter.

For the disaggregation of systematic VaR into different components we need to partition the risk factor covariance matrix Ωh into sub-matrices corresponding to equity index, interest rate, credit spread, forex and commodity risk factors. In the following we illustrate the decomposition when there are just three risk factor types, and we shall assume these are the equity, interest rate and forex factors. Although we do not cover this explicitly here, other classes of risk factor may of course be included.

Let the risk factor sensitivity vector θ, estimated at the time that the VaR is measured, be partitioned as

where θE, θR and θX are column vectors of equity, interest rate and forex risk factor sensitivities. For simplicity we assume the interest rate exposure is to only one risk free yield curve, but numerical examples of interest rate VaR when there are several yield curve risk factors and the exposures are to lower credit grade entities are given in Section IV.2.3.

For ease of aggregation it is best if all three vectors θE, θR and θX are expressed in percentage terms, or all three are expressed in nominal terms. Table IV.2.2 explains how these vectors are measured, and here we assume the numbers of equity, interest rate and forex risk factors are nE, nR and nX respectively. We also use the notation:

- P to denote the value of the portfolio in domestic currency at the time the VaR is measured;

- βi to denote the portfolio's percentage beta with respect to the ith equity risk factor;

- PV01i to denote the portfolio's PV01 with respect to the ith interest rate risk factor;

- Xi to denote the portfolio's nominal exposure to the ith foreign currency in domestic terms.

Table IV.2.2 Risk factor sensitivities

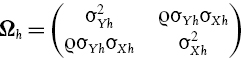

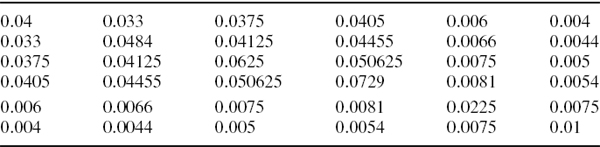

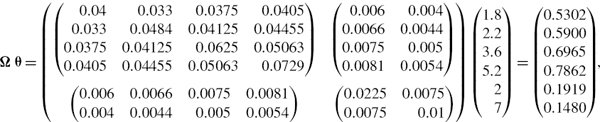

Now we partition the h-day covariance matrix Ωh into sub-matrices of equity risk factor return covariances ΩEh, interest rate risk factor return covariances ΩRh and forex risk factor return covariances ΩXh and their cross-covariance matrices ΩERh, ΩEXh and ΩRXh. Thus we write the risk factor covariance matrix in the form

This partitioned matrix has off-diagonal blocks equal to the cross-covariances between different types of risk factors. For instance, if there are five equity risk factors and four foreign exchange risk factors, the 5 × 4 matrix ΩEXh contains the 20 pairwise h-day covariances between equity and foreign exchange factors, with i,jth element equal to the covariance between the ith equity risk factor and the jth forex risk factor.

Ignoring any mean adjustment, the systematic normal linear VaR is given by (IV.2.15) with θ partitioned as in (IV.2.17) and with Ωh given by (IV.2.18). With this notation it is easy to isolate the different risk factor VaRs.

- Equity VaR, i.e. the risk due to equity risk factors alone: Set θR = θX = 0 and (IV.2.15) yields

- Interest rate VaR, i.e. the risk due to interest rate risk factors alone: Set θE = θX = 0 and (IV.2.15) yields

- Forex VaR, i.e. the risk due to forex risk factors alone: Set θE = θR = 0 and (IV.2.15) yields

Even if the cross-covariance matrices are all zero the total VaR would not be equal to the sum of these three ‘stand-alone’ VaRs. The only aggregation rules we have are that the sum of the stand-alone components equals the total systematic VaR if and only if the risk factors are all perfectly correlated, and that the sum of the squared stand-alone VaRs is equal to the square of the total VaR if the cross correlations between risk factors are all zero.15

IV.2.2.5 Marginal and Incremental Normal Linear VaR

In Section IV.1.7.3 we showed that the total systematic VaR is equal to the sum of the marginal component VaRs, to a first order approximation. In the normal linear model the gradient vector (IV.1.29) is obtained by differentiating (IV.2.15) with respect to each component in θ.

Using our partition of the covariance matrix as in (IV.2.18) above, and the risk factor sensitivities vector θ partitioned as in (IV.2.17), the equity marginal VaR is given by the approximation (IV.1.30) with θR = θX = 0, and so forth for the other component VaRs. That is, we set the other risk factor sensitivities in θ to zero, compute the gradient vector and then approximate the marginal VaR as

In Section IV.1.7.3 we also showed how to use the gradient vector to assess the VaR impact of a trade, i.e. to compute the incremental VaR. In the specific case of the normal linear VaR model the incremental VaR is, to a first order approximation, given by

where θ is the original risk factor sensitivity vector and Δθ is the change in the risk factor sensitivity vector as a result of the trade. Note that this approximation can lead to significant errors if used on large trades. The approximation rests on a Taylor linearization of the parametric linear VaR, but the parametric linear VaR is actually a quadratic function of the sensitivity vector.

To apply the general formulae (IV.2.22) and (IV.2.23) we must derive the gradient vector g(θ) under the normal linear VaR model assumptions. The 100α% h-day normal linear systematic VaR is given by (IV.2.25). Differentiating this, using the chain rule, gives the gradient vector of first partial derivatives, which in this case is

The gradient vector, which Garman (1996) calls the DelVaR vector, has elements equal to the derivative of VaR with respect to each of the components in θ. Now using (IV.2.22) gives the marginal VaR. A numerical illustration of the formula is given in Example IV.2.5 below.

Specific examples of the decomposition of normal linear VaR into stand-alone and marginal VaR components, and of the calculation of incremental VaR, will be given below. For instance, see Examples IV.2.4–IV.2.6 for cash flows and Examples IV.2.14–IV.2.16 for international equity portfolios.

IV.2.3 NORMAL LINEAR VALUE AT RISK FOR CASH-FLOW MAPS

This section analyses the normal linear VaR of a portfolio of bonds, loans or swaps, each of which can be represented as a cash flow. The risk factors are one or more yield curves, i.e. sets of fixed maturity interest rates of a given credit rating. Later in this section we shall decompose each interest rate into a LIBOR rate plus a credit spread. In that case the risk factors are the LIBOR curves and possibly also one or more term structures of credit spreads with different credit ratings.

The excess return on the portfolio over the discount rate will be significantly different from zero only when the portfolio has many exposures to low credit quality counterparties and when the risk horizon is very long. Since the PV01 vector is expressed in present value terms, and since there is no constant term in the risk factor mapping of a cash flow, the discounted expected return on the portfolio is zero, so it is only the volatility of the portfolio P&L that determines the VaR.

In this section all cash flows are assumed to have been mapped to standard maturity interest rates in a present value and volatility invariant fashion. Since we have covered cash-flow mapping in considerable detail in Section III.5.3, and furnished several numerical examples there, we shall assume the reader is familiar with cash-flow mapping in the following. We characterize a portfolio by its mapped cash flow at standard vertices, or by its PV01 sensitivity vector directly.

IV.2.3.1 Normal Linear Interest Rate VaR

We begin by considering only the interest rate risk factors, without decomposing these into LIBOR and credit spread components. In Section IV.1.6.3 we derived a formula for normal linear interest rate VaR, repeated here for convenience:

where θ = (PV011,…, PV01n)′ is the vector of PV01 sensitivities to the various interest rates that are chosen for the risk factors.

A simple example of normal linear VaR for a cash-flow portfolio was given in Section IV.1.6.3, and the first remark that we make here is that in that example the covariance matrix was expressed in basis points. The reason for this is that the PV01 vector contains the risk factor sensitivities to absolute, basis point changes in interest rates, and not to relative changes.

In highly developed markets, returns on fixed income portfolios are usually measured in terms of changes, rather than relative terms. This is natural because the change in the interest rate is the percentage return on the corresponding discount bond. Volatilities of changes in interest rates are often of the order of 100 basis points. But in some countries, such as Brazil or Turkey (at the time of writing), interest rates are extremely high and variable and their volatilities are so high that they are commonly quoted in percentage terms. In this case care should be taken to ensure that the PV01 sensitivities are also adjusted to relate to percentage changes in interest rates or, when PV01 sensitivities relate to changes, the covariance matrix of interest rates must be converted to basis point terms. The following example illustrates how to do this, assuming the returns are normal and i.i.d.

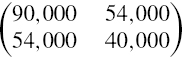

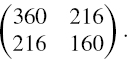

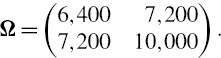

EXAMPLE IV.2.2: CONVERTING A COVARIANCE MATRIX TO BASIS POINTS

Suppose two interest rates have a correlation of 0.9, that one interest rate is at 10% with a volatility of 30% and the other is at 8% with a volatility of 25%. What is the daily covariance matrix in basis point terms?

SOLUTION For the 10% rate with 30% volatility, the volatility is 0.1 × 0.3 = 300 basis points; for the 8% rate with 25% volatility, the volatility is 0.08 × 0.25 = 200 basis points. For the correlation of 0.9, the covariance is 0.9 × 300 × 200 = 54,000 in basis points squared. Hence the annual covariance matrix is

and, assuming 250 trading days per year, the daily covariance matrix is, in basis point terms

IV.2.3.2 Calculating PV01

Consider a cash flow CT at some fixed maturity T, measured in years, which we assume for simplicity is an integer.16 The present value of the cash flow based on a discretely compounded discount rate RT, expressed in annual terms, is

Then, by definition,

A useful and very accurate approximation to (IV.2.27) is derived in Section III.1.8.2. It is repeated here for convenience:

Again, this is valid when T is an integer number of years. Otherwise a small adjustment should be made to the discount factor, as explained in Section III.1.8.2.

Because of the unwanted technical details when working with discretely compounded rates, practitioners usually convert discretely compounded rates into their continuously compounded equivalents for calculations. Using the continuously compounded rate rT that gives the same present value as the discretely compounded rate, we have, for any maturity T, not necessarily an integral number of years,

Thus the PV01 approximation for any T may be written

See Section III.1.8.2 for further details and numerical examples.

The examples in the remainder of this section assume that a cash flow has been previously mapped to the interest rate risk factors, and that the values of the mapped cash flows are not discounted to present value terms. This is because the PV01 vector θ of risk factor sensitivities themselves will convert the change in portfolio value at some time in the future into present value terms.

We now consolidate the application of the normal linear VaR model to cash-flow portfolios by considering a simple numerical example. We make the assumption that the interest rate risk factors are the same as those used for discounting, so there is no drift adjustment term in the VaR formula. We also assume that interest rate changes are generated by i.i.d. multivariate normal processes, so that we can scale the normal linear VaR using the square-root-of-time rule. In particular, the h-day covariance matrix is just h times the 1-day covariance matrix.

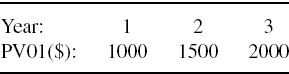

EXAMPLE IV.2.3: NORMAL LINEAR VAR FROM A MAPPED CASH FLOW

Consider a cash flow of $1 million in 1 year and of $1.5 million in 2 years' time. Calculate the volatility of the discounted P&L of the cash flows, given that:

- the 1-year interest rate is 4% and the 2-year interest rate is 5%;

- the volatility of the 1-year rate is 100 basis points, and the volatility of the 2-year rate is 75 basis points; and

- their correlation is 0.9.

Hence calculate the 5% 1-day and the 1% 10-day normal linear VaR.

SOLUTION In the spreadsheet we use (IV.2.27) to calculate the PV01 vector as

![]()

Then we calculate the covariance matrix in basis point terms from the volatilities and correlation, as described above, yielding

Now the volatility of discounted P&L is

To convert this into a 100α% h-day VaR figure we use the relevant standard normal critical value from (IV.2.4) and the square-root-of-time rule. Assuming 250 risk days per year, the 5% 1-day VaR corresponding to the volatility of $28,052 is

![]()

Similarly, assuming the number of 10-trading-day periods per year is 25, the 1% 10-day VaR is

![]()

IV.2.3.3 Approximating Marginal and Incremental VaR

The gradient vector (IV.2.24) allows us to express, to a first order approximation, the incremental effect on VaR resulting from each of the cash flows in a trade. Denote the change in the PV01 cash-flow sensitivity vector as a result of a small trade by Δθ. Each incremental VaR corresponding to a cash flow at one specific maturity is an element of another vector Δθ ⊗ g(θ), where ⊗ denotes the column vector obtained as the element by element product of two column vectors. The net incremental VaR of the new trade is given by the sum of the separate components of this vector, i.e. by (IV.2.23). Using this in (IV.2.23) will give a first order approximation to the change in VaR when any of the PV01 cash-flow sensitivities change.

The following example illustrates how we can approximate the effect of a new trade on the VaR by considering only the cash flow resulting from the proposed trade, thus avoiding the need to revalue the VaR for the entire portfolio each time a new trade is considered.

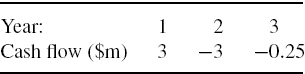

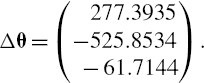

EXAMPLE IV.2.4: INCREMENTAL VAR FOR A CASH FLOW

Consider a cash-flow map with the following sensitivity vector:

Suppose the interest rates at maturities 1, 2 and 3 years have volatilities of 75 basis points, 60 basis points and 50 basis points and correlations of 0.95 (1yr, 2yr), 0.9 (1yr, 3yr), and 0.975 (2yr, 3yr). Find the 1% 10-day normal linear VaR. Now assume that interest rates are 4%, 4.5% and 5% at the 1-year, 2-year and 3-year vertices and suppose that a trader considers entering into a swap with the following cash flow:

What is the incremental VaR of the trade?

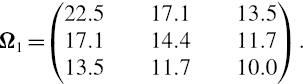

SOLUTION The 1-day risk factor covariance matrix, in basis point terms, is

For instance, the top left element 22.5 for the 1-day variance of the 1-year rate is obtained as 752/250 = 22.5. We are given

![]()

and so

The square root of this, i.e. $16,443, is the 1-day standard deviation of the discounted P&L. The 10-day standard deviation is obtained, using the square-root-of-time rule, as

![]()

Hence the 1% 10-day normal linear VaR is

![]()

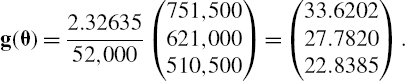

For a 10-day risk horizon,

From above we have ![]() . Hence the DelVaR vector is

. Hence the DelVaR vector is

Calculating the PV01 sensitivity vector of the swap's cash flows, using (IV.2.27) gives

Hence, the components of the incremental VaR are

This shows that the positive cash flow at 1 year increases the VaR by approximately $9326 but both of the negative cash flows on the swap will decrease the VaR, by approximately $14,609 and $1409 respectively. The total incremental VaR for the swap is the sum of these, i.e. approximately −$6693. Hence, adding the swap would reduce the VaR of the portfolio.

Incremental VaR is based on a linear approximation to the VaR, which is a non-linear function of the risk factor sensitivities, so it should only be applied to assess the effect of trades that are small relative to the overall size of the portfolio. Also, in order to properly compare the incremental VaR of several different trades, the cash flows from these trades need to be normalized. Obviously, if trade A has double the magnitude of the cash flows of trade B, the incremental VaR of trade A will be twice that of trade B. That is, we should normalize the trades, so that the incremental VaRs per unit of cash flow are compared. There are several ways of doing this. For instance, we could divide each PV01 by the sum of the absolute values of all PV01s in the sensitivity vector of the trade, or we could divide each PV01 by the square root of the sum of the squared PV01s. More details are given in Garman (1996).

IV.2.3.4 Disaggregating Normal Linear Interest Rate VaR

In this subsection we continue with simple numerical examples of normal linear interest rate VaR to examine the case of an exposure to two yield curves. Such an exposure arises in many circumstances: it can result from an international portfolio containing interest rate sensitive securities; or from any type of foreign investment in forwards and futures;17 even in international commodity portfolios, where we may prefer to use constant maturity futures as risk factors, the forex risk is usually managed by hedging with forex forwards and these are mapped to the spot forex rate. A forex forward mapping thus gives rise to an exposure to the foreign LIBOR curve.

In equity and commodity portfolios the interest rate risk factors are usually much less important than the equity or commodity risk factors and, for international portfolios, the forex risk factors. Usually the equity, commodity, interest rate and forex risk exposures are managed by separate desks. Hence, in the examples in this section we keep things simple by considering only the interest rate part of the risk.

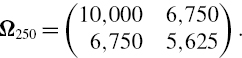

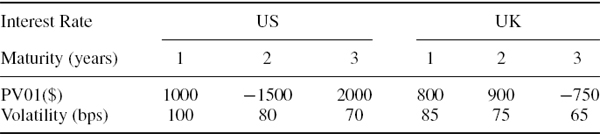

EXAMPLE IV.2.5: NORMAL LINEAR VAR FOR AN EXPOSURE TO TWO YIELD CURVES

In Table IV.2.3 we display the PV01 vectors, both in US dollars, for a portfolio with exposures to the UK and US government yield curves. For simplicity we assume the portfolio has been mapped to only the 1-year, 2-year and 3-year interest rates in each county, and the basis point volatilities for these interest rates are given below each PV01. The correlation matrix of daily interest rates is given in Table IV.2.4. Calculate the 1% 10-day normal linear interest rate VaR, the stand-alone VaR due to the US and UK yield curve risk factors, and the marginal VaRs of these risk factors.

Table IV.2.3 PV01 of cash flows and volatilities of UK and US interest rates

Table IV.2.4 Correlations between UK and US interest rates

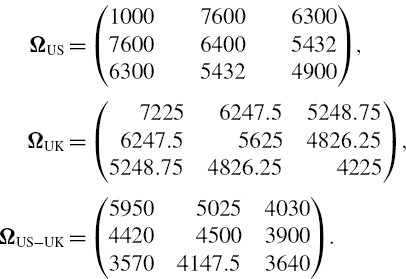

SOLUTION Using the information given in Tables IV.2.3 and IV.2.4, the annual covariance matrix is written in partitioned form as

where

We also write the PV01 vector as

![]()

where

![]()

Under the usual normal i.i.d. assumption, the 1% 10-day total risk factor VaR is then

![]()

For the stand-alone US interest rate VaR we simply use ΩUS and θUS in place of Ω and θ (and similarly, we use ΩUK and θUK for the UK interest rate VaR). The results, which are calculated in the spreadsheet for this example, are:

So the sum of the stand-alone VaRs is $95,604, which is considerably more than the total interest rate VaR.

However, the marginal VaRs do add up to the total interest rate VaR. To calculate these we first compute the DelVaR vector g (θ) using (IV.2.24). Working at the annual level,18 we have

![]()

Now we can recover the 1% annual total interest rate VaR as θ′g (θ) and the two 1% annual marginal VaRs as

Similarly,

The sum of the marginal VaRs is $87,688, which is identical to the total interest rate VaR.

IV.2.3.5 Normal Linear Credit Spread VaR

An exposure to curves with different credit ratings arises from a portfolio with investments in company bonds, corporate loans or swaps, asset backed securities, collateralized debt obligations and non-bank loans such as mortgages. All exposures can be mapped as cash flows at standard vertices, and for each vertex we represent the risk factors as the LIBOR rate of that maturity and the various spreads over LIBOR for each credit rating.

We now explain how to decompose the linear VaR of an interest rate sensitive portfolio into LIBOR and spread components, using continuous compounding (because the mathematics is so much easier). In this case we may write an interest rate of a given credit rating as the sum of the continuously compounded LIBOR rate and the continuously compounded credit spread for that rating. That is, for maturity T and at time t,

where r(t, T) denotes the spot LIBOR rate with maturity T at time t, and rq(t, T) and sq(t, T) respectively denote the interest rate and credit spread, both with credit rating q.

The VaR is calculated in exactly the same way as above, and the only difference is that the variance of the interest rate rq(t, T) can, if we wish, be decomposed into three terms: the variances of the LIBOR rate and the credit spread, and their covariance. This variance decomposition is obtained by applying the variance operator to (IV.2.31):

We now explain how to decompose the total interest rate VaR into LIBOR VaR and credit spread VaR, for a portfolio of a given credit rating, in the context of the normal linear model. Dropping the time and maturity dependence for simplicity, we denote the set of interest rates of credit rating q with different maturities by the vector rq, the LIBOR rates of these maturities by r and the corresponding credit spreads by sq.

We account for the correlations between interest rates using the yield curve covariance matrix, and now we partition this matrix into LIBOR and spread covariance matrices, and their cross-covariance matrix, as

If we want to make the risk horizon of the matrix explicit, then the covariance matrix corresponding to h-day changes in interest rates is written as

Suppose there are n LIBOR rate and n credit spread risk factors at the same maturities. The four matrices in the partition on the right-hand side of (IV.2.34) are then n × n matrices and Ω has dimension 2n × 2n. Now, what is the 2n × 1 risk factor sensitivity vector? The PV01 sensitivity to the change in interest rate of a given maturity is the change in the present value of the cash flow for a one basis point fall in that interest rate. But since the interest rate is the sum of the LIBOR rate and the credit spread, this one basis point fall could be in either the LIBOR rate or the credit spread of that maturity. Thus, assuming the vertices of the risk factor mapping are the same for LIBOR and credit spreads, the PV01 is same for both LIBOR and the credit spread. In other words, with the decomposition (IV.2.34) of the covariance matrix, the corresponding PV01 is the vector with the PV01s at the n vertices in the LIBOR rate risk factor set, and then these are repeated for the vertices in the credit spread risk factor set. Thus ![]() where in this case

where in this case

But due to the limitations of historical data, it usually the case that the maturities at which credit spreads are recorded are a proper subset of the maturities in the LIBOR rate risk factor set.19 So in general, θR ≠ θS because they do not even have the same dimension.

Now the total VaR due to LIBOR and spread is given by the usual formula,

![]()

Setting θR = 0 gives the stand-alone credit spread VaR, and setting θS = 0 gives the stand-alone LIBOR VaR. The marginal contributions to VaR and the incremental VaR of a new trade are all calculated using the gradient vector in the usual way.

The extension of this decomposition to a portfolio containing exposures with several credit ratings is straightforward. For example, with two credit ratings in the portfolio we decompose the covariance matrix thus:

and the PV01 vector is written as the column vector

![]()

where θR is the PV01 of the combined exposure to the two different credit ratings, θS1 is the PV01 of the exposure to the first credit rating, and θS2 is the PV01 of the exposure to the second credit rating.

The following example illustrates the decomposition of interest rate VaR for a portfolio with exposures to a single credit rating.

EXAMPLE IV.2.6: SPREAD AND LIBOR COMPONENTS OF NORMAL LINEAR VAR

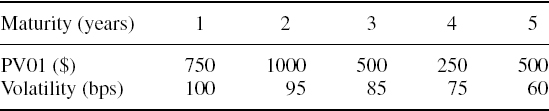

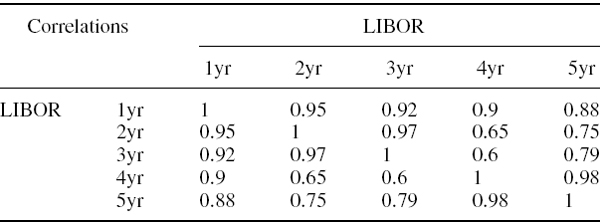

A portfolio of A-rated corporate bonds and swaps has its cash flows mapped to vertices at 1 year, 2 years, 3 years, 4 years and 5 years. The volatilities of the LIBOR rates (in basis points per annum) and PV01 vector of the portfolio are shown in Table IV.2.5. The correlations of the LIBOR rates are shown in Table IV.2.6.

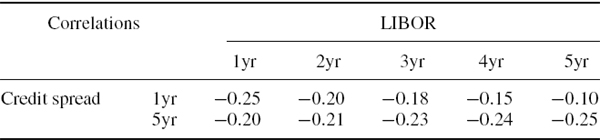

The 1-year and 5-year A-rated credit spreads are, like the LIBOR parameters, assumed to have been estimated from a historical sample. Suppose the 1-year spread has volatility 80 basis points per annum and the 5-year spread has volatility 70 basis points per annum, and their correlation is 0.9. Suppose the cross correlations between these credit spreads and the LIBOR rates of different maturities are as shown in Table IV.2.7. Estimate the 1% 10-day total interest rate VaR and decompose the total VaR into the VaR due to LIBOR rate uncertainty, and the VaR due to credit spread uncertainty. Then estimate the marginal VaR of the LIBOR and credit spread components.

Table IV.2.5 PV01 of cash flows and volatilities of LIBOR rates

Table IV.2.6 Correlations between LIBOR rates

Table IV.2.7 Cross correlations between credit spreads and LIBOR rates

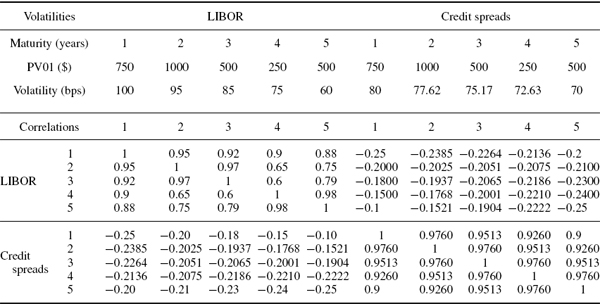

SOLUTION We shall employ a simple linear interpolation between variances and between squared correlations to fill in the elements of the matrices ΩS and ΩRS.20 The full matrix Ω is a10 × 10 matrix, and the volatilities and correlations in this matrix are shown in Table IV.2.8.

The PV01 vector is

![]()

with

![]()

This yields the 1% annual total risk factor VaR:

![]()

Table IV.2.8 Volatilities and correlations of LIBOR and credit spreads

Multiplying this by ![]() gives the 1% 10-day total risk factor VaR as $137,889.

gives the 1% 10-day total risk factor VaR as $137,889.

For the stand-alone LIBOR VaR we simply use ΩR and θR in place of Ω and θ (and similarly, we use ΩS and θS for the credit spread VaR). The results, which are calculated in the spreadsheet for this example, are:

So the sum of the stand-alone VaRs is $220,224, which is much larger than the total VaR, due to the negative correlation between interest rates and credit spreads.

As usual, the marginal VaRs sum to the total VaR. To calculate these we first compute the annual gradient vector using the usual formula. This gives

![]()

The 1% annual total VaR is ![]() and this has already been calculated as $689,443. The two 1% annual marginal VaRs are

and this has already been calculated as $689,443. The two 1% annual marginal VaRs are

and

The sum of the marginal VaRs is identical to the total VaR.

IV.2.4 CASE STUDY: PC VALUE AT RISK OF A UK FIXED INCOME PORTFOLIO

The above example employed a cash-flow mapping to just five vertices, and included just one credit rating. But in practice there could be 50 or 60 vertices, and several credit ratings. With n vertices and k credit ratings there will be kn risk factors, so the risk factor correlation matrix could have a very large dimension indeed. However, the risk factors are very highly correlated and for this reason lend themselves to dimension reduction through the use of principal component analysis (PCA).21 This section demonstrates how to apply PCA to reduce the dimension of the risk factor space when estimating the VaR of interest rate sensitive portfolios so that the new risk factors (i.e. the principal components) are uncorrelated variables that capture the most commonly experienced moves in interest rates.

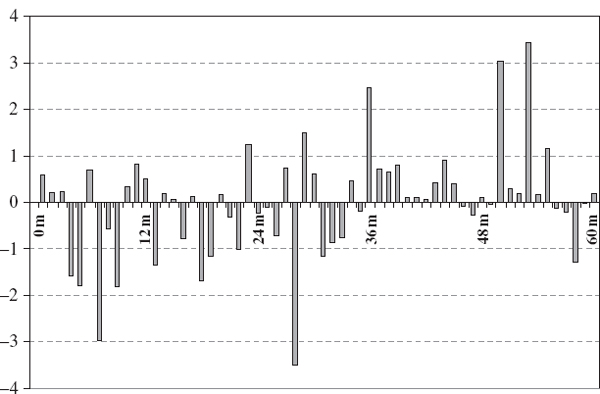

We consider a portfolio of UK bonds (and/or swaps) on 31 December 2007. We ignore the credit spread risk and suppose that its cash flows have been mapped to the spot market rates at intervals of one month using the volatility, present value and duration invariant cash-flow map described in Section III.5.3. Then the PV01 of the mapped cash flow is computed as explained in Section III.1.8 and the resulting PV01 vector is depicted in Figure IV.2.2.

Figure IV.2.2 PV01 vector of a UK fixed income portfolio (£000)

Given the size of the PV01 sensitivities shown in Figure IV.2.2, with several exceeding ±£1000, there must be cash flows of ±£5 million or more at several maturities.22 Hence, the portfolio could contain long positions on bonds with face value of around £1 billion, and short positions on bonds with face value of around £1 billion or more. The present value of the portfolio may be much less than £1 billion of course, because it has a rough balance of positive and negative cash flows.

IV.2.4.1 Calculating the Volatility and VaR of the Portfolio

This section contains two examples, the first showing how to use the cash-flow map and the second showing how to compute the volatility and VaR of the portfolio.

EXAMPLE IV.2.7: APPLYING A CASH-FLOW MAP TO INTEREST RATE SCENARIOS

Consider the portfolio of UK bonds and swaps with PV01 vector θ shown in Figure IV.2.2. Find an approximation to the change in the portfolio's value given that UK interest rates change as follows:

(a) The UK yield curve moves upward with a parallel shift of 10 basis points at all maturities.

(b) There is a tilt in the UK yield curve where the 1-month rate increases by 35 basis points, the 2-month rate by 34 basis points, the 3-month rate by 33 basis points and so on up to the 59-month rate decreasing by 23 basis points and the 60-month rate decreasing by 24 basis points.

SOLUTION In the spreadsheet for this example we apply the relationship (IV.1.25), i.e.

with the basis point changes in interest rates specified in (a) and (b) above. Hence:

(a) Δr =(10, 10,…, 10)′ gives PV = £9518; and

(b) Δr =(35, 34,…, −23, −24)′ gives ΔPV = £396,478.

Since the portfolio has a balance of long and short exposures, its present value does not change much when the yield curve shifts parallel, as is evident in case (a) above. But the portfolio is much more exposed to a change in slope of the yield curve; Figure IV.2.2 shows that the portfolio is predominately short in bonds with maturities up to 3 years but its positions on bonds with maturities between 3 and 5 years are predominately long. Hence, the portfolio will increase in value if the yield curve shifts up at the short end and down at the long end. Indeed, under the scenario for interest rates in (b) above, the portfolio would make a profit of £396,478.

In the next three examples, all of which are contained in the case study workbook, we use an equally weighted covariance matrix Ω1 of the absolute daily changes in UK interest rates based on data from 2 January 2007 until 31 December 2007.23 The covariance matrix has dimension 60 × 60, so we do not show it here, although it can be seen in the Excel spreadsheet accompanying the following example.

EXAMPLE IV.2.8: VAR OF UK FIXED INCOME PORTFOLIO

Use the 1-day covariance matrix Ω1 given in the spreadsheet to find the volatility of the discounted P&L of the portfolio with PV01 vector θ shown in Figure IV.2.2. Assuming that each interest rate change is i.i.d. normally distributed, calculate the 1% 10-day VaR on 31 December 2007.

SOLUTION We first obtain the 1-day variance of the portfolio P&L as

![]()

But θ was given in units of £1000. Hence to convert this figure to the P&L volatility we must take the square root, multiply this by the square root of 250 (assuming there are 250 risk days per year) and then also multiply by £1000. The result is

![]()

Hence,

![]()

IV.2.4.2 Combining Cash-Flow Mapping with PCA

Principal component analysis is a powerful tool for representing any highly correlated system. In Chapter II.2 we explained how to apply PCA to a set of interest rates, and in Section II.2.3 we used the UK bonds that we are considering in this case study as an example. In this section we shall combine a principal component representation with the PV01 vector shown in Figure IV.2.2. In this way we obtain a set of sensitivities to a new set of interest rate risk factors: the first three principal components of the UK yield curve.

The general expression for a principal component representation of the changes in interest rates Δrt at time t is

where the factor weights matrix W* is the n × k matrix whose columns are the first k eigenvectors of the covariance matrix of absolute changes in returns; n is the number of risk factors, i.e. the dimension of the covariance matrix; and ![]() is the k × 1 column vector of the first k principal components at time t.

is the k × 1 column vector of the first k principal components at time t.

We use (IV.2.38) to derive the representation of our UK bond portfolio P&L in terms of sensitivities β to just k orthogonal risk factors (i.e. the principal components) instead of sensitivities to n highly correlated risk factors. Combining (IV.2.37) with (IV.2.38) gives

Hence, the new factor sensitivity vector is the k × 1 vector of constants obtained by taking (minus) the product of the transpose of the component factor weights matrix, W*′, which has dimension k × n, and the n × 1 PV01 vector θ. This way the number of risk factors has been reduced from n to k.

Now the interest rate VaR based on the principal component risk factors is

or, equivalently,

where D = diag (λ1,…, λk) is the diagonal matrix of the first k eigenvalues of the h-day risk factor covariance matrix Ωh. Note that if n = k (i.e. we only make the risk factors uncorrelated and do not reduce the number of risk factors) then W* = W, i.e. the matrix of all n eigenvectors, and WDW′ = Ωh. So unless we use PCA to reduce dimensions, the PC VaR estimate is identical to the ordinary interest rate VaR estimate.

The approximation (IV.2.39) of portfolio P&L is now based on new risk factors, i.e. the first k principal components. These are uncorrelated, whereas interest rate risk factors themselves are highly correlated. Moreover, the new sensitivity vector β is just a k × 1 vector, whereas the old PV01 sensitivity vector was an n × 1 vector, where n is much larger than k. In practice it is typical for n to be around 50 or 60 and for k to be only 3 or 4. So there is a huge reduction in dimension from basing VaR measurement on (IV.2.39) rather than using the ordinary risk factor VaR. Yet, the loss of accuracy from using PC VaR as an approximation to the interest rate VaR is negligible, particularly when it is set in the context of all the other sources of model risk in the normal linear VaR model.

The next example shows how to derive the quantities in (IV.2.40) and applies this formula to measure the PC VaR of our UK bond portfolio.

EXAMPLE IV.2.9: USING PRINCIPAL COMPONENTS AS RISK FACTORS

Suppose that the cash-flow representation of the bond portfolio whose PV01 vector is shown in Figure IV.2.2 was taken on 31 December 2007. Also suppose that we base our daily interest rate covariance matrix Ω1 on daily changes in the UK spot curve for maturities measured at monthly intervals up to 5 years, using the data period from 2 January to 31 December 2007.24 Find a principal component representation based on Ω1 with three principal components, and specify the diagonal matrix D that has their standard deviations along its diagonal. Then use this principal component representation to calculate the UK bond portfolio's sensitivities to the three principal component risk factors.

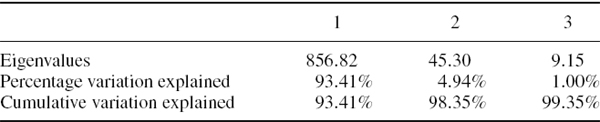

SOLUTION A PCA on the 60 × 60 covariance matrix is given in the Excel workbook for this case study. The first three eigenvalues are shown in Table IV.2.9, and we see that together the first three components explain over 99% of the total variation in UK interest rates over the past year. The first component alone accounts for 93.41% of the variation, so the rates were extremely highly correlated along the yield curve during 2007.

Table IV.2.9 Eigenvalues of covariance matrix of UK spot rates – short end

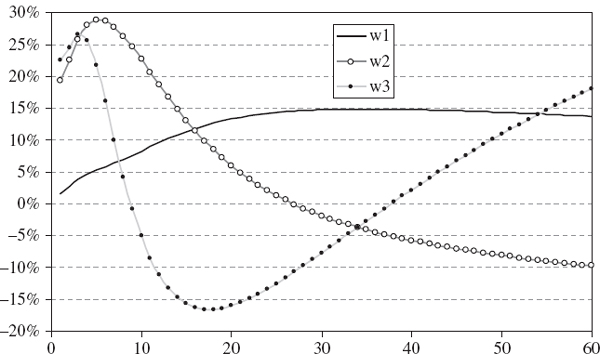

The first three eigenvectors belonging to these eigenvalues are plotted, as a function of the maturity of the interest rate, in Figure IV.2.3. These have the usual ‘trend–tilt–curvature’ interpretation that we are accustomed to when PCA is applied to a highly correlated yield curve, such as the Bank of England liability curves. However, as is usual for money market rates which are frequently affected by manipulation from the central bank, the very short term rates are less volatile than others, giving the eigenvectors a characteristic ‘dip’ at the short end. For instance, if the first principal component increases but the other components are unchanged, then the 1-month rate will hardly change, but the interest rates at maturities greater than 2 years will all change by a similar amount, i.e. by approximately 15% of the change in the first principal component.

Figure IV.2.3 Eigenvectors of covariance matrix of UK spot rates – short end

The diagonal matrix of standard deviations of the principal components has elements equal to the square root of the eigenvalues in Table IV.2.9, i.e.

Since by definition the first principal component has much the largest standard deviation, this would be the main determinant of the VaR if the sensitivity to each PC were the same. We estimate the PC sensitivity vector β using (IV.2.39), i.e. multiplying the matrix W* whose columns contain the first three eigenvectors by the 60 × 1 vector of PV01 sensitivities shown in Figure IV.2.2. In this way we obtain the new 3 × 1 sensitivity vector β for the principal component factors shown in Table IV.2.10. In fact, the sensitivity to the first PC is the smallest of the three.

Table IV.2.10 Net sensitivities on PC risk factors

Figure IV.2.4 shows the first principal component, which is obtained from the first eigenvector. Since it is based on a covariance matrix that is expressed in basis point terms, the principal component is also measured in basis points. The coefficient of £428 on P1 means that a 100 basis point increase in the first principal component leads, approximately, to a £42,800 increase in the present value of the portfolio. From the first eigenvector in Figure IV.2.3 we see that a 100 basis point increase in the first component would be approximately equivalent to a yield curve movement that is up 15 basis points at maturities over 2 years, but up much less at shorter maturities. Our portfolio has some very large positive cash flows at maturities over 2 years so an upward shift of 15 basis points at the longer maturities, with less movement at the short end, will induce a much larger gain in the portfolio than a parallel shift of 15 basis points. The eigenvalues given in Table IV.2.1 tell us that the first principal component captured a very common type of movement in the yield curve. In fact, it accounts for 93.41% of the variation experienced in the UK government yield curve during 2007. By contrast, the exact parallel shift scenario that we used in Example IV.2.7 is not nearly as common.

Figure IV.2.4 First principal component of the UK spot rates – short end

EXAMPLE IV.2.10: COMPUTING THE PC VAR

Estimate the VaR of the portfolio based on the mapping to the first three principal components, i.e. based on (IV.2.40), and compare this with the full evaluation interest rate VaR from Example IV.2.8.

SOLUTION The spreadsheet for this example first gives the result of estimating the P&L volatility using the β vector shown in Table IV.2.3 and the diagonal covariance matrix of the principal components given by (IV.2.42). This gives

![]()

Then we compute the 1% 10-day VaR from this volatility, by multiplying it by the critical value Φ−1(0.99) = 2.32635 and by the scaling factor ![]() , giving the 1% 10-day PC VaR as £175,457, compared with £176,549 under full evaluation. The PC approximation leads to only a very small error in VaR (of about 0.6%). The error is a result of taking only three principal components, but this ignores only a small fraction of the variation in the risk factors.

, giving the 1% 10-day PC VaR as £175,457, compared with £176,549 under full evaluation. The PC approximation leads to only a very small error in VaR (of about 0.6%). The error is a result of taking only three principal components, but this ignores only a small fraction of the variation in the risk factors.

IV.2.4.3 Advantages of Using PC Factors for Interest Rate VaR

In addition to the advantage of dimension reduction, the principal component risk factors make it much easier to apply meaningful scenarios to interest rates. By changing just the first principal component, for instance, we obtain the change in our portfolio's value corresponding to the most likely shift in the yield curve, given the historical data used in the PCA. This is not usually a parallel shift in all yields, but it is approximately parallel at longer maturities, so for a portfolio with a high duration this scenario gives a portfolio sensitivity that is similar to that obtained via the standard duration approximation. But, since interest rates do not normally shift exactly parallel all the time, using a change in the first principal component is more representative of historical movements in yields than a parallel shift.

Moreover, the representation (IV.2.39) provides a more detailed analysis of our portfolio's responses than duration–convexity analysis. In addition to a roughly parallel shift, by changing the second principal component we can find the change in portfolio value corresponding to a specific tilt in the yield curve, i.e. the tilt that is most likely to occur, based on the historical yield curve movements. On changing the third principal component we obtain our portfolio's response to a specific (most likely) change in the yield curve convexity, and so on if more than three principal components are used in (IV.2.39).

Covariance matrix scenarios, which form the basis of many stress tests, are also very easy to implement using PCA. For instance, suppose the original cash-flow mapping of the portfolio is to 50 different maturities of interest rates. Then their covariance matrix is very large, i.e. 50 × 50. Performing stress tests on this matrix will not be a simple task. However, when using the principal component representation (IV.2.39) of the portfolio's P&L, stress tests need only be performed on a k × k covariance matrix, where typically k = 3. PC-based stress tests also take on a meaningful interpretation, i.e. stressing the most common changes in trend, tilt and curvature of interest rates.

Finally, by choosing only the first few components in the representation we have cut down the ‘noise’ in the data that we would prefer not to contaminate our risk measures. In highly correlated yield movements there is very little ‘noise’ and for this reason a three-component representation captures over 99% of the variations in our example. But in less highly correlated yields, much of the idiosyncratic variation in yields may not be useful for risk analysis, especially over the longer term. We saw a small reduction in the PC VaR estimate, compared with the usual VaR estimate, and this is to be expected if some of the variation is ignored. But with the yield curves in major currencies this reduction will be very small indeed. However, other systems such as implied volatilities or equities have much more noise and in this case the use of principal components could reduce VaR more significantly.

IV.2.5 NORMAL LINEAR VALUE AT RISK FOR STOCK PORTFOLIOS

Starting with the simplest case of just a few cash stock positions, we shall consider many linear equity portfolios in this section, including cash and futures positions with and without foreign exchange risk. The systematic parametric linear VaR estimates of an equity portfolio are based on forecasts of expected returns and standard deviations of returns, taken in the context of an equity factor model. Hence, this section draws on the material presented in Chapter II.1, where we covered the different types of factor models that are used for mapping equity portfolios.

IV.2.5.1 Cash Positions on a Few Stocks

In Section I.2.4 we showed how to compute the volatility of portfolio P&L, when the portfolio is characterized by its holdings in each of n stocks and we are given the covariance matrix of the stocks returns. Denote the n × 1 vector of portfolio weights on each stock by w, where each element of w is the holding in that stock divided by the total amount invested, i.e. the current price of the portfolio P. Denote the n × n stock returns annual covariance matrix by V.25 Then the portfolio return volatility is ![]() and the P&L volatility is Pσ.

and the P&L volatility is Pσ.

In Section IV.2.2 we showed how to convert a portfolio volatility into a 100α% h-day normal linear VaR estimate, for an arbitrary portfolio, under the assumption that the risk factor returns are multivariate normal and i.i.d. with zero expected excess returns. We ignore the effect on VaR of an expected return that is different from the discount rate, since this is very small unless h is very large. Then, with h measured in days and assuming there are 250 trading days per year, we have

More generally, and particularly when estimating the VaR for long term investments in equity funds, we may wish to include the possibility that the portfolio grows at a rate different from the discount rate over a long risk horizon. In this case we would include the drift adjustment to the VaR, as explained in Sections IV.1.5.1 and IV.2.2.

In the general case, to apply the normal linear VaR formula (IV.2.43) we need to forecast, over a risk horizon of h days, the standard deviation and mean of the portfolio returns. Let

- w denote the current vector of portfolio weights,

- E (xh) be the n × 1 vector of the stocks' expected excess h-day returns, and

- Vh be the h-day covariance matrix of stock returns.

Then the 100α% h-day normal linear VaR of the portfolio, under the assumption that the risk factor returns are multivariate normal and i.i.d. and expressed as a percentage of the portfolio value P is

The application of this formula is illustrated in the following example.

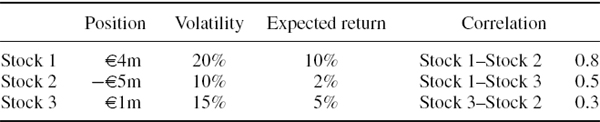

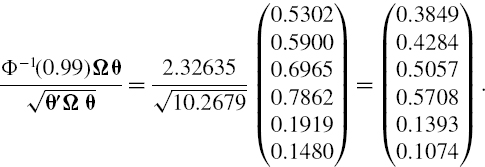

EXAMPLE IV.2.11: VAR FOR CASH EQUITY POSITIONS

Calculate the 1% 10-day parametric linear VaR for a portfolio that has the characteristics defined in Table IV.2.11, discounting using a risk free rate of 5%. How much is the VaR reduced by the mean adjustment? Repeat your calculations for a risk horizon of 1 year.

Table IV.2.11 Stock portfolio characteristics

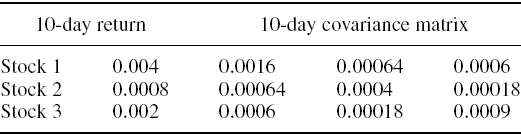

SOLUTION The calculations are performed in the accompanying spreadsheet, using the 10-day expected returns and the covariance matrix of 10-day returns displayed in Table IV.2.12. This gives an expected P&L of €14,000, a P&L standard deviation of €117,898 and a 1% 10-day VaR of €259,765. But without the mean adjustment, i.e. without the second term on the right-hand side of (IV.2.44), the 1% 10-day VaR is €273,738. Hence, the mean adjustment reduces the VaR by about 5%. Over a 1-year risk horizon the 1% VaR is €1,384,864 without the mean adjustment and €1,051,530 with the mean adjustment. Hence, over 1 year the drift adjustment is very important, as it leads to a 24% reduction in VaR.

Table IV.2.12 Characteristics of 10-day returns

Another way of looking at the results in the above example is to use Table IV.2.1, which tells us that the 1% 10-day VaR is very approximately about 10% of the portfolio value, depending of course on the portfolio volatility. So very approximately the VaR is about €100,000 per €1 million invested. In the above example the discount factor over 10 days corresponding to a 5% discount rate is 0.99805, and its effect is therefore about €(1 − 0.99805) million, i.e. approximately €195 per €1 million invested. This is negligible compared with the VaR. However, over a 1-year horizon the VaR is about 50% of the portfolio value, again depending on the portfolio volatility. And the discount factor over 1 year corresponding to a 5% discount rate is 0.95238. So its effect is about (1 − 0.95238) million euros, i.e. approximately €47,620 per €1 million invested, which is not insignificant compared with the VaR.