CHAPTER 4

![]()

COMPLETING THE ACCOUNTING CYCLE

OVERVIEW

During the accounting period, transactions are recorded daily in the journal. At convenient times, information is posted from the journal to the ledger. At the end of the accounting period, the accountant summarizes the effects of the many recorded transactions, adjusts the accounts, and prepares financial statements. To help organize the information, the accountant uses an organized piece of scratch paper called a worksheet. The worksheet is a simple tool and is an optional step in the accounting cycle. Its preparation and uses are discussed in this chapter. After financial statements are drafted, the nominal (or temporary) accounts must be prepared for the accumulation of data pertaining to transactions in the following accounting period. Closing entries are journalized and posted to do just that; they are a required step in the accounting cycle and are discussed in this chapter. At the beginning of the subsequent (new) accounting period, reversing entries may be prepared in order to facilitate the recording of cash receipts and disbursements that relate to adjusting entries of the prior period. Reversing entries are an optional step in the accounting cycle and are discussed in the appendix to this chapter.

SUMMARY OF LEARNING OBJECTIVES

- Prepare a worksheet. The steps in preparing a worksheet are as follows: (a) Prepare a trial balance on the worksheet (b) Enter the adjustments in the adjustment columns. (c) Enter adjusted balances in the adjusted trial balance columns. (d) Extend adjusted trial balance amounts to appropriate financial statement columns. (e) Total the statement columns, compute net income (or net loss), and complete the worksheet.

- Explain the process of closing the books. Closing the books occurs at the end of an accounting period. The process is to journalize and post closing entries and then rule (underline) and balance all accounts. In closing the books, companies make separate entries to close revenues to Income Summary, expenses to Income Summary, Income Summary to owner's capital, and owner's drawings to owner's capital. Only temporary accounts are closed.

- Describe the content and purpose of a post-closing trial balance. A post-closing trial balance contains the balances in permanent accounts that are carried forward to the next accounting period. The purpose of this trial balance is to prove the equality of these balances.

- State the required steps in the accounting cycle. The required steps in the accounting cycle are: (1) analyze business transactions, (2) journalize the transactions, (3) post to ledger accounts, (4) prepare a trial balance, (5) journalize and post adjusting entries, (6) prepare an adjusted trial balance, (7) prepare financial statements, (8) journalize and post closing entries, and (9) prepare a post-closing trial balance.

- Explain the approaches to preparing correcting entries. One way to determine the correcting entry is to compare the incorrect entry with the correct entry. After comparison, the company makes a correcting entry to correct the accounts. An alternative approach is to reverse the incorrect entry and then prepare the correct entry.

- Identify the sections of a classified balance sheet. A classified balance sheet categorizes assets as current assets; long-term investments; property, plant, and equipment; or intangibles. A classified balance sheet categorizes liabilities as either current or long-term. There is also an owner's (owners') equity section, which varies with the form of business organization.

- *Prepare reversing entries. Reversing entries are the opposite of the adjusting entries made in the preceding period. A company can choose to use or not use reversing entries. When reversing entries are used, they are made at the beginning of a new accounting period to simplify the recording of later transactions related to specific adjusting entries. In most cases, only accrual type adjusting entries are reversed.

*This material appears in Appendix 4A in the text.

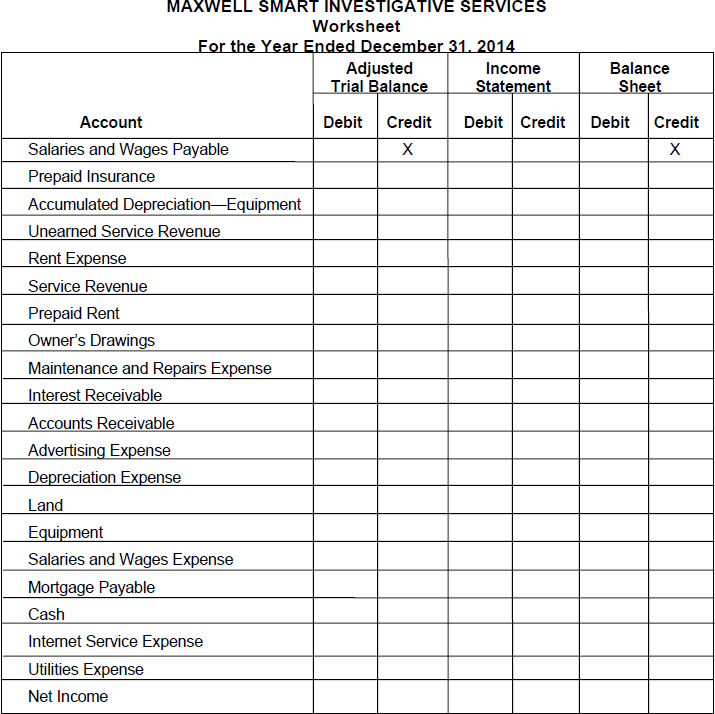

EXERCISE 4-1

Purpose: (L.O. 1) This exercise will allow you to quickly check your knowledge of how items are extended on a worksheet.

A partial worksheet for the Maxwell Smart Investigative Services Company appears below. (The accounts are not listed in their usual order, the worksheet is only partially illustrated, and the Trial Balance and Adjustments columns have been omitted.)

Instructions

For each account, place an “X” in the appropriate Adjusted Trial Balance column pair to indicate whether the account balance will appear in the Debit or Credit column (assume a normal balance in each account) on the worksheet. Also for each account, place an “X” in the appropriate Income Statement or Balance Sheet column to indicate the column to which the balance should be extended. The first one is done for you.

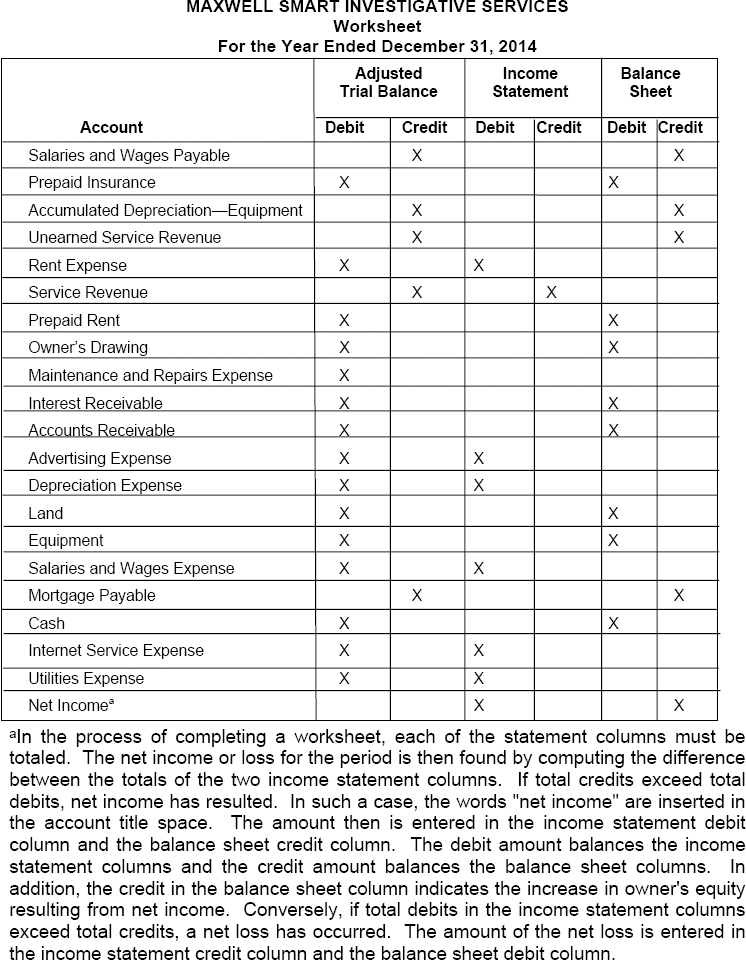

SOLUTION TO EXERCISE 4-1

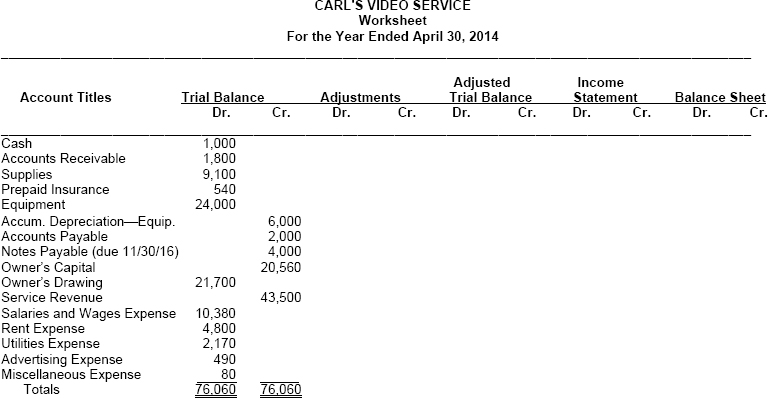

EXERCISE 4-2

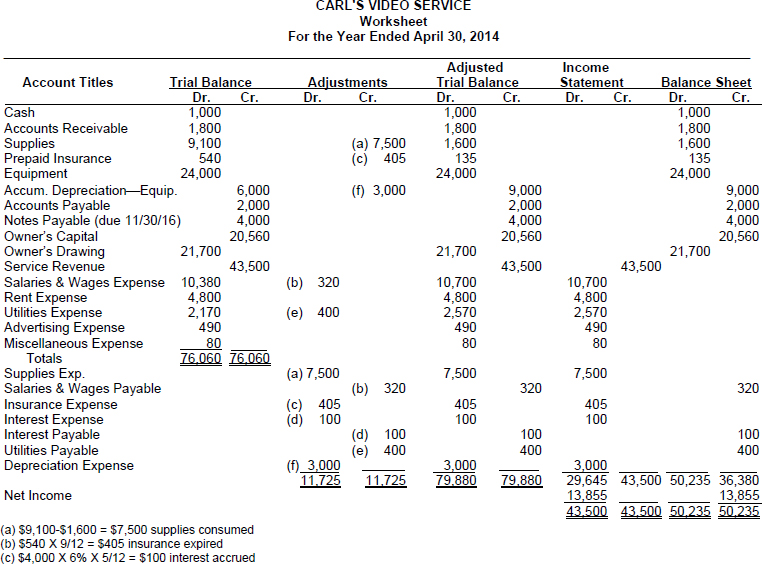

Purpose: (L.O. 1) This exercise illustrates the function of a worksheet.

Carl's Video Service has a fiscal year ending on April 30. The following information is available:

(a) Supplies on hand at April 30, 2014, amount to $1,600.

(b) Wages incurred but not paid at April 30, 2014, amount to $320.

(c) The $540 balance in the Prepaid Insurance account represents a payment for 12 months that began on August 1, 2013.

(d) The note payable bears interest of 6% per year and was issued on December 1, 2013.

(e) The estimated amount of utilities consumed but unpaid as of year end amounts to $400.

(f) Depreciation on equipment for the year amounts to $3,000.

Instructions

Complete the worksheet for Carl's Video Service for the year ended April 30, 2014. The trial balance has already been put on the worksheet for you.

| TIP: | Remember to cross-reference (key) your adjustments by use of the appropriate letters. |

| TIP: | Before beginning a worksheet, think about the steps involved in its completion:

Step 1: Prepare a trial balance on the worksheet. Step 2: Enter the adjustments in the adjustments columns. Step 3: Enter adjusted balances in the adjusted trial balance columns. Step 4: Extend adjusted trial balance amounts to appropriate financial statement columns. Step 5: Total the statement columns, compute the net income (or net loss), and complete the worksheet. |

| TIP: | The debit and credit columns for every column pair must be equal before you can proceed to the next column pair. (This pertains to the first three column pairs.) |

| TIP: | Every amount appearing in the adjusted trial balance column pair must be extended to one of the four statement columns. Debit amounts go to a debit column further to the right and credit amounts go to a credit column further to the right of the adjusted trial balance column pair. |

| TIP: | When a dollar amount is added to balance the income statement column pair of columns, the same amount must be added in an opposite debit or credit column in the balance sheet column pair. This amount in a balance sheet column indicates the impact of net income (or net loss) on owner's equity. |

SOLUTION TO EXERCISE 4-2

EXERCISE 4-3

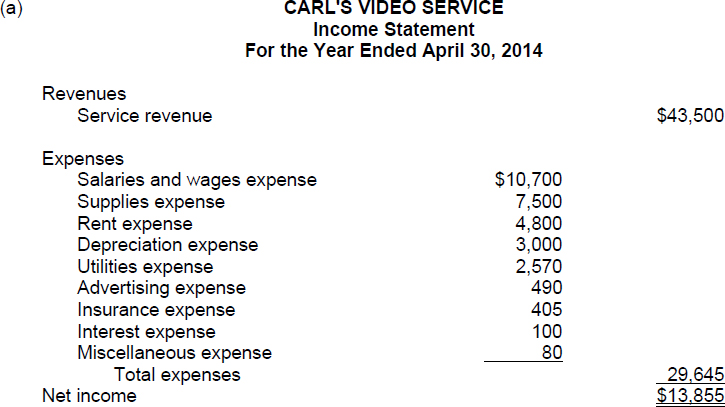

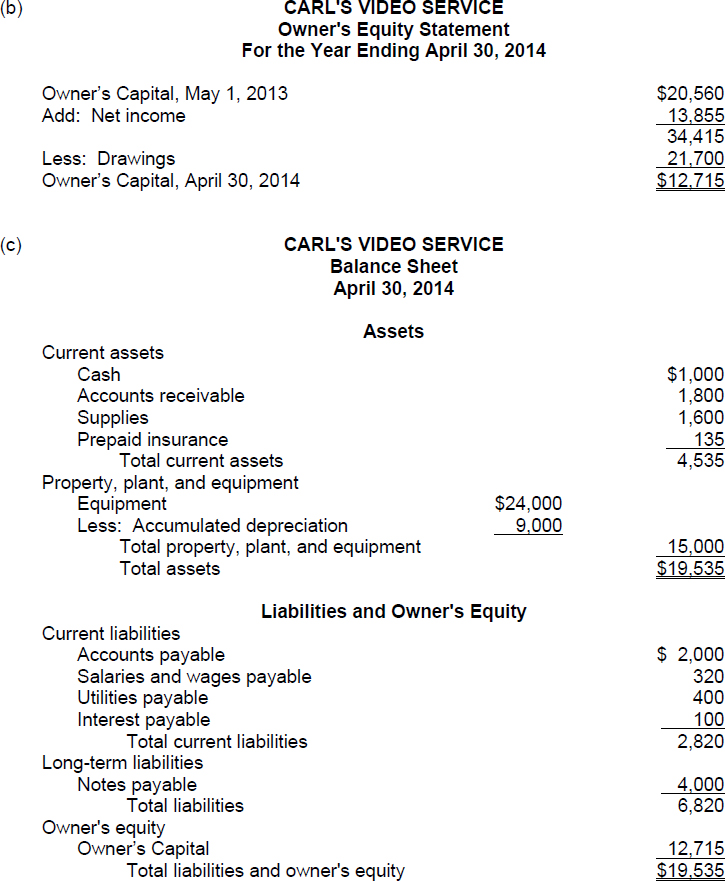

Purpose: (L.O. 1, 6) This exercise will illustrate the preparation of financial statements from information contained in the worksheet.

A worksheet is a tool used by most accountants to aid in the organization of data for the preparation of financial statements.

Instructions

Refer to the Solution to Exercise 4-2. Use the completed worksheet for Carl's Video Service to:

(a) Prepare an income statement for the year ending April 30, 2014.

(b) Prepare an owner's equity statement for the year ending April 30, 2014.

(c) Prepare a classified balance sheet at April 30, 2014.

SOLUTION TO EXERCISE 4-3

EXERCISE 4-4

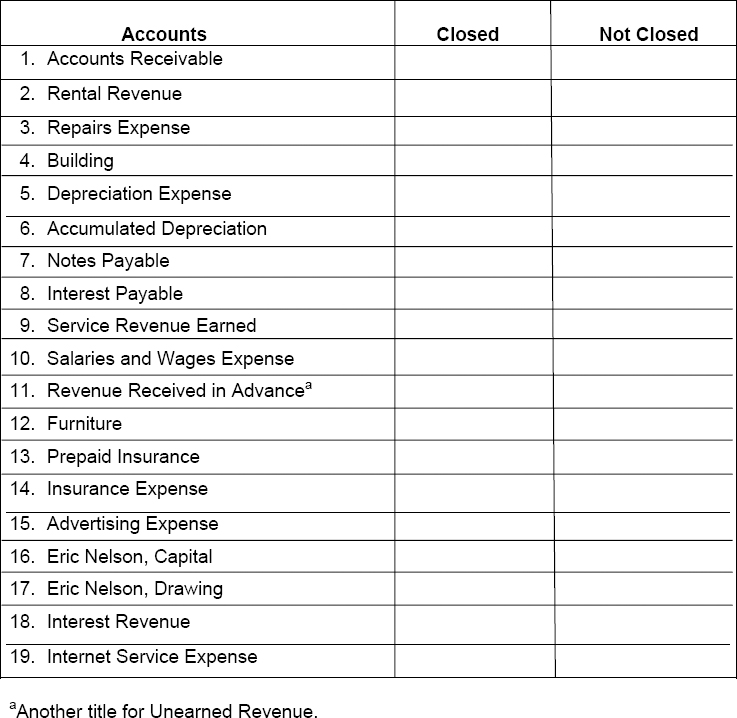

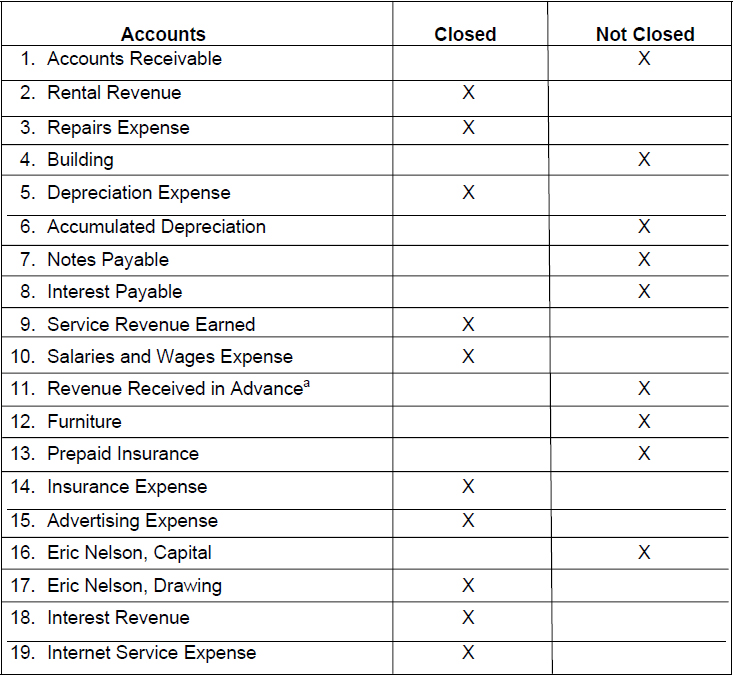

Purpose: (L.O. 2) This exercise will give you practice in identifying those accounts which are closed at the end of the accounting period and those accounts which are not closed.

Instructions

The following accounts were taken from the financial statements of a local business. Indicate whether each of the following accounts would or would not be closed at the end of the accounting period by placing an “X” in the appropriate column.

| TIP: | Remember the general rule: All nominal accounts (revenues, expenses, and owner's drawing) are closed and all real accounts (assets, liabilities, and owner's capital) are not closed. Therefore, to determine if an account will be closed or not closed, analyze the classification of the account. |

| TIP: | Ten of the following are nominal or temporary accounts; nine are real or permanent accounts. |

SOLUTION TO EXERCISE 4-4

EXERCISE 4-5

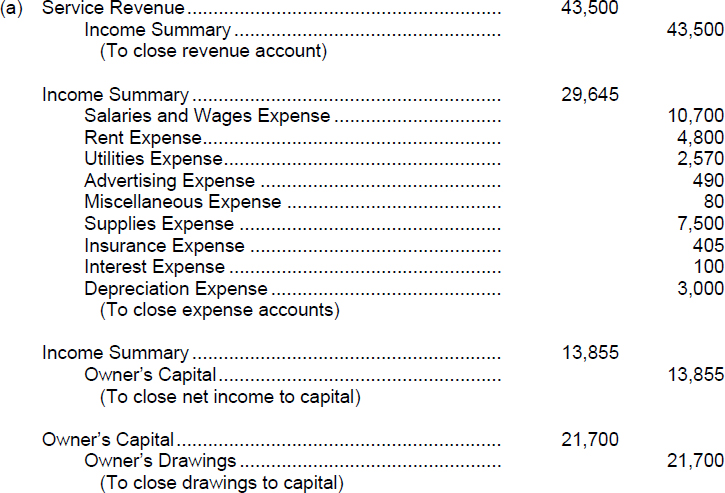

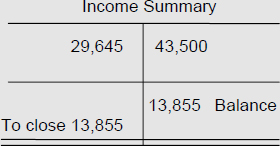

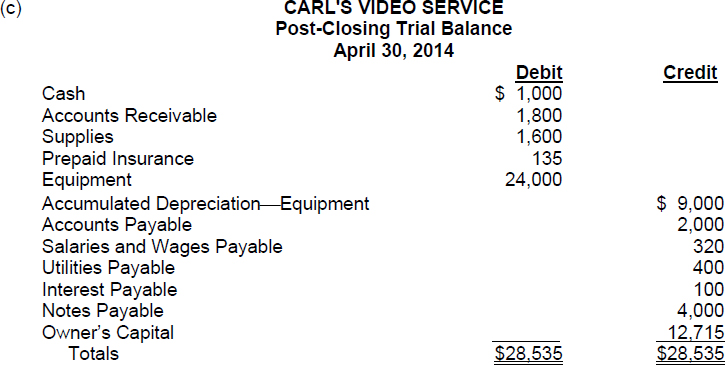

Purpose: (L.O. 2, 3) This exercise illustrates the preparation of closing entries and a post-closing trial balance, and discusses the importance of both.

The recording and posting of closing entries is a required step in the accounting cycle.

Instructions

Refer to the Solution to Exercise 4-2.

(a) Prepare the closing entries for Carl's Video Service at April 30, 2014.

(b) Discuss the two reasons why closing entries are prepared.

(c) Prepare a post-closing trial balance for Carl's Video Service.

(d) Explain why a post-closing trial balance is prepared and indicate what type of accounts will appear on the post-closing trial.

SOLUTION TO EXERCISE 4-5

(b) The major reason closing entries are needed is that they prepare the temporary (nominal) accounts for the recording of transactions of the next accounting period. Closing entries produce a zero balance in each of the temporary accounts so that they can be used to accumulate data pertaining to the next accounting period. Because of closing entries, the revenues of 2014 are not commingled with the revenues of the prior period (2013). A second reason closing entries are needed is that the owner's capital account will reflect a true balance only after closing entries have been completed. Closing entries formally recognize in the ledger the transfer of net income (or loss) and owner's drawings to owner's capital as shown in the owner's equity statement.

(d) The purpose of a post-closing trial balance is to prove the equality of the permanent (real) accounts after the closing entries have been recorded and posted. The accounts appearing on a post-closing trial are the ones having balances that are carried forward into the next accounting period which can be described as the real accounts or the permanent accounts or the balance sheet accounts.

EXERCISE 4-6

Purpose: (L.O. 4) This exercise will review the proper sequence of the required steps in the accounting cycle.

The required steps in the accounting cycle are listed in random order below.

| _______ a. | Prepare an adjusted trial balance. |

| _______ b. | Analyze business transactions. |

| _______ c. | Prepare a post-closing trial balance. |

| _______ d. | Prepare a trial balance. |

| _______ e. | Prepare financial statements. |

| _______ f. | Post to ledger accounts. |

| _______ g. | Journalize and post adjusting entries. |

| _______ h. | Journalize and post closing entries. |

| _______ i. | Journalize the transactions. |

Instructions

Indicate the proper sequence of the steps by numbering them “1,” “2,” and so forth in the spaces provided.

| TIP: | As you work through this exercise, concentrate on the logical step progression and the flow of information in the data gathering process. |

SOLUTION TO EXERCISE 4-6

- 6

- 1

- 9

- 4

- 7

- 3

- 5

- 8

- 2

EXERCISE 4-7

Purpose: (L.O. 1, 4) This exercise reviews the procedures involved in the accounting cycle when the two optional steps, a worksheet and reversing entries, are employed.

Ten steps in the accounting cycle for a company which uses a worksheet and reversing entries are listed in random order below.

| _______ a. | Journalize and post closing entries. |

| _______ b. | Prepare financial statements from the worksheet. |

| _______ c. | Prepare a post-closing trial balance. |

| _______ d. | Balance the ledger accounts and prepare a trial balance on the worksheet. |

| _______ e. | Journalize and post adjustments made on the worksheet. |

| _______ f. | Record transactions in the journal. |

| _______ g. | Journalize and post reversing entries. |

| _______ h. | Post from journal to the ledger. |

| _______ i. | Complete the worksheet (adjusting entries, adjusted trial balance and extend amounts to financial statement columns). |

| _______ j. | Analyze business transactions. |

Instructions

Arrange the ten procedures carried out in the accounting cycle in the order in which they should be performed by numbering them “1,” “2,” and so forth in the spaces provided.

| TIP: | As you work through this exercise, concentrate on the logical progression and the flow of information in the data gathering process. |

SOLUTION TO EXERCISE 4-7

- 8

- 6

- 9

- 4

- 7

- 2

- 10

- 3

- 5

- 1

ILLUSTRATION 4-1

BALANCE SHEET CLASSIFICATIONS (L.O. 6)

Current assets—includes cash and items which are expected to be converted to cash or sold or consumed within the next year (or operating cycle, whichever is longer).

Long-term investments—includes assets such as investments in stocks and bonds of other companies which can be realized in cash, but conversion into cash is not expected within the next year (or operating cycle, whichever is longer).

Property, plant, and equipment—includes long-lived tangible assets (land, building, equipment, and machinery) that are currently being used in operations (used to produce goods and services for customers). Assets in this category are often referred to as plant assets or fixed assets. They are not held for resale.

Intangible assets—includes assets that lack physical substance, such as patent, copyright, trademark, or trade names that give the holder exclusive right of use for a specified period of time. Their value to a company is generally derived from the rights or privileges granted by governmental authority.

Current liabilities—includes obligations that are due within a year and are expected to require the use of existing current assets (or the creation of other current liabilities) to liquidate them such as accounts payable, short-term notes payable, interest payable, and unearned service revenue.

Long-term liabilities—includes obligations that do not meet the criteria to be classified as current liabilities such as bonds payable, mortgages payable, long-term notes payable, lease liabilities, and obligations under employee pension plans.

Owner's equity—includes the owner's contributions and profits retained for use in the business. For a proprietorship, there is one capital account. For a partnership, there is a capital account for each partner. For a corporation, owner's equity is called stockholders' equity and includes two subclassifications—Capital Stock and Retained Earnings.

EXERCISE 4-8

Purpose: (L.O. 6) This exercise will allow you to practice identifying the classification of accounts on a classified balance sheet.

A list of the balance sheet classifications appears below along with a list of account titles for the Steve Martin Corporation.

Classifications

| CA | Current Assets |

| INV | Long-Term Investments |

| PPE | Property, Plant and Equipment |

| ITG | Intangible Assets |

| CL | Current Liabilities |

| LTL | Long-Term Liabilities |

| OE | Owner's Equity |

| NRBS | Not Reported on the Balance Sheet |

Accounts

_____ 1. Accounts Receivable

_____ 2. Salaries and Wages Payable

_____ 3. Notes Payable (due in 4 years

_____ 4. Office Equipment

_____ 5. Notes Payable (due in 6 months)

_____ 6. Patents

_____ 7. Notes Payable (due in 4 months)

_____ 8. Bonds Payable (due in 20 years

_____ 9. Notes Receivable (due in 3 years

_____ 10. Mortgages Payable (due in 5 years)

_____ 11. Salaries and Wages Expense

_____ 12. Prepaid Insurance

_____ 13. Delivery Trucks

_____ 14. Copyrights

_____ 15. Cash

_____ 16. Utilities Expense

_____ 17. Depreciation Expense

_____ 18. Unearned Rent Revenue

_____ 19. Interest Receivable

_____ 20. Rent Revenue

_____ 21. Owner's Capital

_____ 22. Buildings

_____ 23. Prepaid Advertising

_____ 24. Prepaid Property Taxes

_____ 25. Investment in Orlando Aviation Authority Bonds

_____ 26. Property Taxes Payable

_____ 27. Short-term Investment

_____ 28. Land

_____ 29. Parking Lots and Driveways

_____ 30. Franchises

_____ 31. Unearned Subscription Revenue

_____ 32. Utilities Payable

Instructions

Indicate which balance sheet classification is the most appropriate for reporting each account listed above by selecting the abbreviation of the corresponding section. If the account is not a real (permanent) account, use the abbreviation NRBS for Not Reported on the Balance Sheet.

Approach: Mentally review the brief descriptions of each classification. (See Illustration 4-1.) Use these descriptions to aid your analysis.

SOLUTION TO EXERCISE 4-8

| Item # | Solution |

| 1. | CA |

| 2. | CL |

| 3. | LTL |

| 4. | PPE |

| 5. | CL |

| 6. | ITG |

| 7. | CL |

| 8. | LTL |

| 9. | INV |

| 10. | LTL |

| 11. | NRBS |

| 12. | CA |

| 13. | PPE |

| 14. | ITG |

| 15. | CA |

| 16. | NRBS |

| 17. | NRBS |

| 18. | CL |

| 19. | CA |

| 20. | NRBS |

| 21. | OE |

| 22. | PPE |

| 23. | CA |

| 24. | CA |

| 25. | INV |

| 26. | CL |

| 27. | CA |

| 28. | PPE |

| 29. | PPE |

| 30. | ITG |

| 31. | CL |

| 32. | CL |

Selected Explanations:

- Salaries and Wages Expense (Item #11), Utilities Expense (Item #16), Depreciation Expense (Item #17), and Rent Revenue (Item #20) are all income statement accounts. Hence, they are nominal or temporary accounts and do not belong on the balance sheet.

- Prepaid items such as Prepaid Insurance (Item #12), Prepaid Advertising (Item #23), and Prepaid Property Taxes (Item #24) are generally expected to be consumed within the next year or operating cycle, whichever is longer; hence, they are current assets.

- Unearned Rent Revenue (Item #18), unless otherwise indicated, should be treated as if it will be earned within the year following the balance sheet date; hence, it is a current liability. If evidence existed to show the unearned amount was not expected to be earned in the next year, it would be classified as a long-term (noncurrent) liability. The same reasoning applies to Unearned Subscription Revenue (Item #31).

- Interest payments are typically due monthly, quarterly, semiannually, or at least annually. Hence, we expect to collect the amount in Interest Receivable (Item #19) within the next year (unless evidence exists to the contrary).

- Investments such as Investment in Orlando Aviation Authority Bonds (Item #25) should be assumed to be held for a long-term purpose (unless there is evidence to the contrary); hence, they are classified as long-term investments. If an investment is held for sale and is expected to be sold within the next year as is (Item #27), it should be classified as a current asset.

EXERCISE 4-9

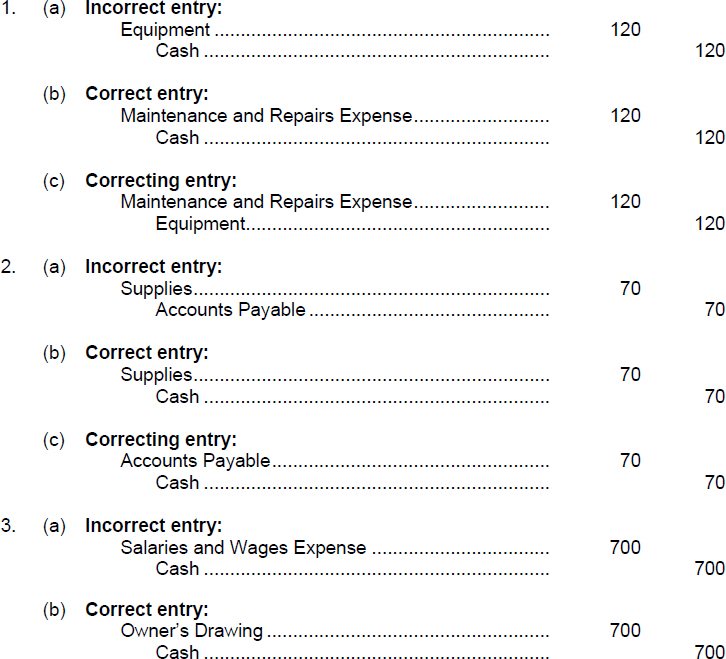

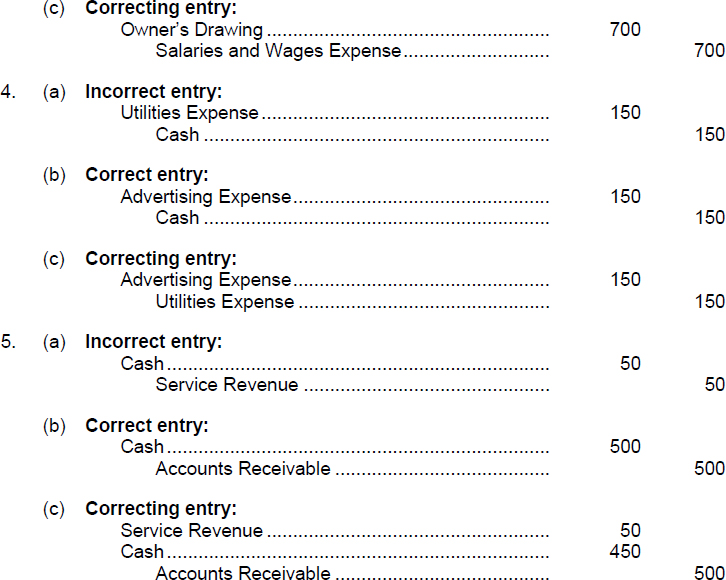

Purpose: (L.O. 5) This exercise will illustrate how to correct errors made in the recording process.

The following errors were discovered in the books of the Cool Way AC Repair Shop.

- A cash payment of $120 for repairs on a typewriter was recorded by a debit to Equipment and a credit to Cash.

- A cash payment of $70 for office supplies was recorded by a debit to Supplies and a credit to Accounts Payable.

- An owner's drawing was recorded by a debit to Salaries and Wages Expense and a credit to Cash for $700.

- A cash payment of $150 for an ad appearing in Sunday's edition of the local newspaper was recorded by a debit to Utilities Expense and a credit to Cash for $150.

- A $500 cash receipt from a customer on account was recorded by a debit to Cash for $50 and a credit to Service Revenue for $50.

- The first interest payment made this accounting period (on a note payable) was for $1,000, which included $300 of interest accrued at the end of the last accounting period. The payment was recorded by a debit to Interest Expense for $1,000 and a credit to Cash for $1,000. (No reversing entries were made at the beginning of this accounting period.)

- A $300 cash sale of services was recorded by a debit to Accounts Receivable for $300 and a credit to Service Revenue for $300.

- A cash payment of $2,000 for some new tools was recorded by a debit to Equipment for $200 and a credit to Cash for $200.

Prepare an analysis of each error showing

(a) the incorrect entry,

(b) the correct entry, and

(c) the correcting entry.

SOLUTION TO EXERCISE 4-9

| TIP: | This one is tricky because both the amount and an account were in error in the original entry. |

Approach: Compare the correct entry with the incorrect entry to determine the accounts which need to be increased or decreased in the correcting entry to arrive at their correct balances.

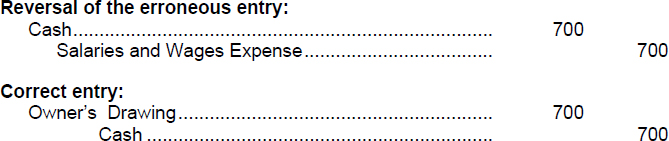

Alternate Approach: If you are not usually successful in identifying the appropriate correcting entry by using the approach above, a simpler approach may be to reverse the incorrect entry and prepare the correct entry. These two entries together constitute the correction. For example, refer to error number 3. The correction could be made by the following:

Notice that these two entries are the equivalent to the single correcting entry given earlier in the solution as:

![]()

You can readily tell this because in the two entry (second) approach, the debit to Cash for $700 offsets the credit to Cash for $700 which leaves only the remainder of the entries having an impact on account balances. That remainder is a debit to Owner's Drawing and a credit to Salaries and Wages Expense for $700.

EXERCISE 4-10

Purpose: (L.O. 1 thru 7) This exercise will quiz you about terminology used in this chapter.

A list of accounting terms with which you should be familiar appears below:

| Classified balance sheet | Long-term liabilities |

| Closing entries | Operating cycle |

| Correcting entries | Permanent (real) accounts |

| Current assets | Post-closing trial balance |

| Current liabilities | Property, plant, and equipment |

| Income Summary | Reversing entry |

| Intangible assets | Stockholders' equity |

| Liquidity | Temporary (nominal) accounts |

| Long-term investments | Worksheet |

Instructions

For each item below, enter in the blank the term that is described.

- _____________________A multiple-column form that may be used in making adjusting entries and in preparing financial statements.

- _____________________Entries made at the end of an accounting period to transfer the balance of temporary accounts to a permanent owner's equity account, owner's capital.

- _____________________A list of permanent accounts and their balances after a company has journalized and posted closing entries.

- _____________________Revenue, expense, and drawing accounts whose balances a company transfers to owner's capital at the end of an accounting period.

- _____________________Balance sheet accounts whose balances companies carry forward to the next accounting period.

- _____________________A temporary account used in closing revenue and expense accounts.

- _____________________An entry, made at the beginning of a new accounting period, that is the exact opposite of the related adjusting entry made in the previous period.

- _____________________The average time that it takes to purchase inventory, sell it on account, and then collect cash from customers.

- _____________________Cash and other resources that a company expects to convert to cash or use up within one year.

- _____________________Generally, investments in stocks and bonds of other companies that companies normally hold for many years. Also includes long-term assets such as land and buildings, not currently being used in operations.

- ______________________Assets with relatively long useful lives, currently being used in operations.

- ______________________Noncurrent assets that do not have physical substance.

- ______________________Obligations that a company expects to pay from existing current assets within the coming year.

- ______________________Obligations that a company expects to pay after one year.

- ______________________Owners' equity of a corporation; the ownership claim of shareholders on total assets.

- ______________________The ability of a company to pay obligations expected to become due within the next year.

- ______________________Entries to correct errors made in recording transactions.

- ______________________A balance sheet that contains a number of standard classifications or sections.

SOLUTION TO EXERCISE 4-10

- Worksheet

- Closing entries

- Post-closing trial balance

- Temporary accounts (or nominal accounts)

- Permanent accounts (or real accounts)

- Income Summary

- Reversing entry

- Operating cycle

- Current assets

- Long-term investments

- Property, plant and equipment

- Intangible assets

- Current liabilities

- Long-term liabilities

- Stockholders' equity

- Liquidity

- Correcting entries

- Classified balance sheet

ILLUSTRATION 4-2

USE OF REVERSING ENTRIES VERSUS

NO REVERSING ENTRIES USED* (L.O. 7)

*This material is covered in Appendix 4A in the text.

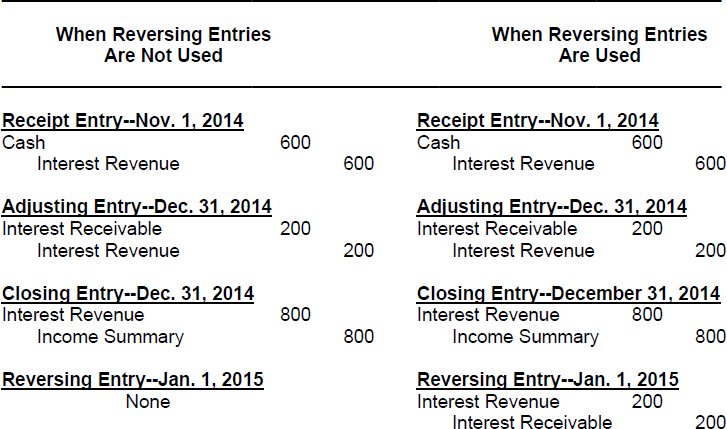

Reversing entries are most often used to reverse two types of adjusting entries: accrued revenues and accrued expenses.

As an example of the flow of information through the accounts when using reversing entries versus the flow when no reversing entries are used, consider the following information and the resulting entries and account balances. Notice that you arrive at the same account balances, regardless of your path, by the time financial statements are to be prepared.

Data:

A three-year note receivable for $12,000 was accepted on May 1, 2014. It carries a 10% interest rate. The interest is to be collected every 6 months so the first interest receipt was on November 1, 2014 and the second interest receipt is scheduled for May 1, 2015. The annual accounting period ends on December 31, 2014. Two months of accrued interest exists at year end.

Entries:

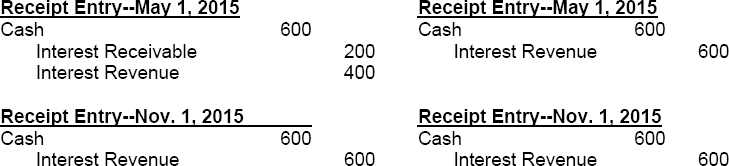

The posting of the entries through Nov. 1, 2015 is reflected as follows:

| TIP: | The differences are highlighted in bold print. Notice that by the end of the day on December 31, 2014, the account balances are the same regardless of which alternative is chosen. Also, by the end of the day on May 1, 2015, the account balances are once again the same under both approaches. (Abbreviations are: Rec. = Receipt; Rev. = Reversing; Adj. = Adjusting.) |

| TIP: | Notice how reversing entries allowed the bookkeeper to record the receipt of $600 on May 1, expediently like the November 1, 2014 receipt (debit to Cash for $600 and a credit to Interest Revenue for $600) without looking in the records to determine if the receipt is partially for revenue earned in a prior period or not. (Think of the time savings if you collect varying amounts of accrued interest from hundreds of different sources.) |

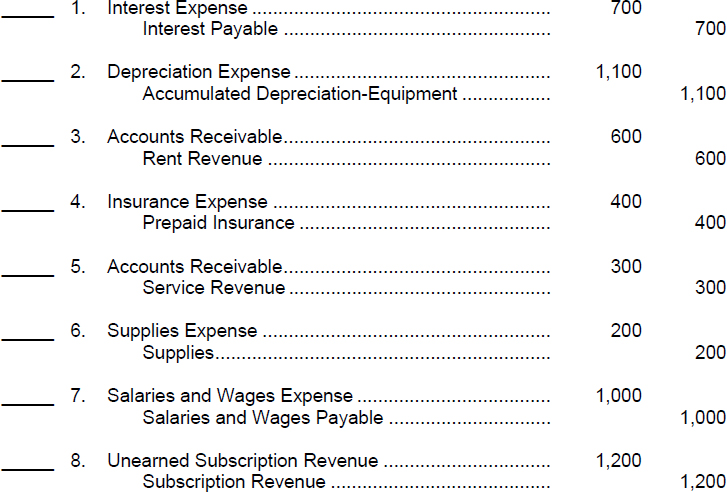

*EXERCISE 4-11

Purpose: (L.O. 7) This exercise will provide practice in determining which adjusting entries may be reversed.

The following represent adjusting entries prepared for the Office Furniture Design Company.

Instructions

For each adjusting entry above (prepared at December 31, 2014), indicate if it would be appropriate to reverse the entry at the beginning of 2015. Indicate your answer by writing yes or no in the space provided.

SOLUTION TO EXERCISE 4-11

- Yes

- No

- Yes

- No

- Yes

- No

- Yes

- No

- An expense accrual type adjustment can always be reversed. The reversing entry will eliminate the payable balance established by the adjustment and create a credit balance (an abnormal balance) in the expense account at the beginning of the new period. Thus, when the related cash is paid for the interest, the payment can be recorded by a credit to Cash and a debit to Interest Expense for the entire amount paid. (The abnormal balance in the expense account which was created by the reversing entry is eliminated with the posting of the cash payment entry.) This entry to record the cash payment is simpler than the alternate route of using no reversal and recording a portion of the payment (representing the accrued amount) by a debit to a payable account and the remainder (incurred in the new period) by a debit to the expense account.

- An adjusting entry to record depreciation should never be reversed. It would not make sense to reverse this adjustment because to do so would reduce the depreciation to date (accumulated depreciation).

- A revenue accrual type adjustment can always be reversed. The reversing entry will eliminate the receivable balance established by the adjustment and create a debit balance (an abnormal balance) in the revenue account at the beginning of the new period. Thus, when the related cash is collected from the tenant, the receipt can be recorded by a debit to Cash and a credit to Rent Revenue for the entire amount received. (The abnormal balance in the revenue account is eliminated with the posting of the cash collection entry.) This entry to record the cash receipt is simpler than the alternate route of using no reversal and recording a portion of the collection (representing the accrued amount) by a credit to the receivable account and the remainder (earned in the new period) by a credit to the revenue account.

- An adjusting entry to transfer the expired portion of the insurance premium from an asset account (prepaid) to an expense account should never be reversed. A reversing entry would put the expired portion back into an asset account.

- An adjusting entry to record accrued revenue can always be reversed. Refer to the logic explained for item 3. above.

- An adjusting entry to transfer the cost of consumed supplies from an asset account to an expense account should never be reversed. Refer to the logic explained for item 4. above.

- An adjusting entry to record accrued expense can always be reversed. Refer to the logic explained for item 1. above.

- An adjusting entry to transfer the earned portion of the revenue collected in advance from the unearned account to an earned account should never be reversed. A reversing entry would put the earned portion back into an unearned (liability) account, which would not make sense because that portion of the cash received has been earned and no liability remains for that portion.

ANALYSIS OF MULTIPLE-CHOICE QUESTIONS

- (L.O. 2) Which of the following accounts is a nominal (temporary) account?

- Cash.

- Prepaid Rent.

- Accumulated Depreciation.

- Advertising Expense.

Approach and Explanation: Write down the definition of a nominal (or temporary) account. A nominal account is an account which is closed at the end of an accounting period. Think of what types of accounts get closed—revenues, expenses, owner's drawing. Think of what types of accounts never get closed—asset, liability, and owner's equity. Identify the classification of each of the accounts mentioned:

Cash Asset Prepaid Rent Asset Accumulated Depreciation Contra Asset Advertising Expense Expense When judging if an account is temporary or permanent (real), a contra account is classified in the same manner (temporary or permanent) as the account to which it relates. Hence, a contra asset account is a real account. (Solution = d.)

- (L.O. 2) Certain accounts are closed at the end of an accounting period in order to:

- reduce the number of items that get reported in the general purpose financial statements.

- prepare those accounts for recording of transactions of the subsequent accounting period.

- reduce the number of accounts that appear in the ledger.

- transfer the effect of transactions recorded in real accounts to the owner's capital account.

Approach and Explanation: Review the two reasons for preparing closing entries: (1) closing entries prepare the temporary accounts for the recording of transactions of the succeeding accounting period, and (2) closing entries transfer the net income (or net loss) amount and owner's drawings to owner's capital as shown in the owner's equity statement. Net income is determined by the balances in revenue and expense accounts (collectively called nominal or temporary accounts). (Solution = b.)

- (L.O. 2) A journal entry to close the Service Revenue account in the closing process will involve a debit to:

- Service Revenue and a credit to Income Summary.

- Income Summary and a credit to Service Revenue.

- Owner's Capital and a credit to Service Revenue.

- Service Revenue and a credit to Cash.

Approach and Explanation: Think of the normal balance of the account to be closed. Revenue accounts have a normal credit balance. A closing entry will involve the opposite action to that account; therefore, debit the Service Revenue account. All closing entries for income statement accounts involve the Income Summary account; therefore, credit Income Summary. (Solution = a.)

- (L.O. 2) If a business has profitable operations for the period, the balance of the Income Summary account will be closed by:

- a debit to Income Summary and a credit to Owner's Capital.

- a debit to Owner's Capital and a credit to Income Summary.

- debits to the expense accounts, credits to the revenue accounts, and a credit to the Income Summary account.

- debits to the revenue accounts, credits to the expense accounts, and a credit to the Income Summary account.

Approach and Explanation: Keep in mind that assets have normal debit balances and owner's equity has the opposite (credit) normal balance. Revenues increase owner's equity so revenue accounts have normal credit balances and expense accounts have normal debit balances. Revenue accounts are closed by debits to those revenue accounts and credits to Income Summary; expense accounts are closed by credits to those expense accounts and debits to Income Summary. When revenues exceed expenses, the entity is profitable and the Income Summary account therefore has a credit balance before closing. The Income Summary account is closed, in those conditions, by a debit to Income Summary (for its balance) and a credit to the Owner's Capital account. (Solution = a.)

- (L.O. 3) Which of the following groups of accounts have balances after the books have been closed at the end of an accounting period?

- All asset and revenue accounts.

- All expense and liability accounts.

- All asset, liability, owner's capital, revenue, and expense accounts.

- All asset, liability, and owner's capital accounts.

Approach and Explanation: Think of which accounts get closed. They are the temporary or nominal accounts (which include all revenue, expense and owner's drawing accounts). The real accounts are not closed (asset, liability, and owner's capital accounts). (Solution = d.)

- (L.O. 1) Before computing the net income figure for the period, the total of the income statement debit column of a worksheet is $42,000 and the total of the income statement credit column is $40,000. This indicates that:

- there was a net loss of $2,000 for the period.

- there was a net income of $2,000 for the period.

- the Income Summary account will be closed by a debit to that Income Summary account.

- an error has been made in preparing the worksheet.

Explanation: Debits on the income statement reduce net income; credits on the income statement increase income. An excess of debits over credits on the income statement results in a net loss. A net loss will cause a debit balance in the Income Summary account so that account will be closed by a credit. (Solution = a.)

- (L.O. 1) The preparation of a worksheet at the end of an accounting period will:

- eliminate the need for journalizing and posting adjusting entries.

- replace the preparation of individual financial statements.

- eliminate the need for preparing closing entries and a post-closing trial balance.

- serve as an aid to the accountant in organizing the data required for the preparation of financial statements.

Explanation: The worksheet is an optional step in the accounting cycle. It does not eliminate the need for adjusting entries, financial statements, or closing entries. These are prepared in the same manner whether or not a worksheet is prepared. (Solution = d.)

- (L.O. 1) In completing a worksheet, the account Depreciation Expense requires an amount in the adjusted trial balance column pair and also an amount in the:

- Income Statement debit column.

- Income Statement credit column.

- Balance Sheet debit column.

- Balance Sheet credit column.

Explanation: Depreciation expense is to appear on the income statement as a reduction in net income (debit). (Solution = a.)

- (L.O. 1) In completing a worksheet, the account Prepaid Insurance requires an amount in the adjusted trial balance column pair and also an amount in the:

- Income Statement debit column.

- Income Statement credit column.

- Balance Sheet debit column.

- Balance Sheet credit column.

Approach and Explanation: Think about the statement on which the Prepaid Insurance account will appear and where. Prepaid Insurance will appear on the balance sheet as an asset (debit). (Solution = c.)

- (L.O. 1) When revenues exceed expenses for a period, the worksheet will require the net income figure to be entered in the following columns to properly complete the worksheet.

- income statement debit column and balance sheet credit column.

- income statement credit column and balance sheet debit column.

- income statement debit column and balance sheet debit column.

- income statement credit column and balance sheet credit column.

Explanation: Revenue accounts have credit balances; expense accounts have debit balances. Due to worksheet technique, when revenues exceed expenses (credits in income statement column exceed debits in income statement column on worksheet), a debit is needed in the income statement column pair to balance that pair. That debit is the net income figure. Debits have to equal credits. The corresponding credit is to the balance sheet column pair. (Solution = a.)

- (L.O. 5) A piece of equipment was acquired for cash this period and was incorrectly recorded by a debit to Maintenance and Repairs Expense. The correcting entry should:

- increase assets and reduce expenses.

- increase expenses and reduce assets.

- increase liabilities and increase assets.

- reduce assets and reduce expenses.

Approach and Explanation: Write down the incorrect entry (debit to Maintenance and Repairs Expense and a credit to Cash) and the correct entry (debit to Equipment and a credit to Cash). Compare the two entries and identify the errors (Maintenance and Repairs Expense is overstated and Equipment is understated). Prepare the correcting entry (debit to Equipment and a credit to Maintenance and Repairs Expense). Notice that the effect of the correcting entry is to reduce expenses and to increase assets. (This solution ignores the depreciation that should also be recorded for the period.) (Solution = a.)

- (L.O. 7) Which of the following adjusting entries could be reversed at the beginning of the following accounting period?

- The entry to record depreciation for the period.

- The entry to record accrued revenue.

- The entry to transfer the expired portion of the supplies from an asset account to an expense account.

- The entry to transfer the earned portion of revenue received in advance from a liability account to a revenue account.

Approach and Explanation: Think about the adjusting entries that can be reversed. Accrual type adjusting entries can always be reversed (the procedure is optional). Prepayment type adjusting entries are usually not reversed. Selection “a” is incorrect because depreciation entries are never reversed. Selection “c” is incorrect because a reversing entry would put expired costs back into an asset account. Selection “d” is incorrect because a reversing entry would put earned revenue back into a liability account. (Solution = b.)