CHAPTER 25

Calculation 19: Internal Rate of Return

What It Means

Internal rate of return (IRR) is probably the rate-of-return measurement most widely used by real estate professionals. It allows you to take into account both the timing and the magnitude of cash flows produced by your income-property investment.

It’s not a silver bullet; no approach to investment decision making is. And by no means should you use it to the exclusion of other measurements discussed in this book. Those others run a range from the simplistic to sophisticated, but virtually all of them can help fill in the whole picture. A property’s operating expense ratios, for example, may not give you enough information by themselves to guide you to a purchase decision, but they still may tell you something you absolutely need to know.

If you read Chapter 5 or if you have taken this series of short, calculation-based chapters in sequence, then you know that you can apply a particular discount rate—your required rate of return—to a series of future cash flows to determine what that income stream is worth today. If you rearrange that process, you can recharacterize the present value (PV) as your known present cost (i.e., the amount of cash you have to invest in order to make this purchase) and treat the discount rate (the rate of return) as your unknown.

In discounted cash flow, you estimated the future cash flows and the proper discount rate and then used that information to calculate the PV of your cash investment.

Now, if you forecast the future cash flows and the PV (i.e., the amount) of your actual cash investment, you can calculate the discount rate, which you call the internal rate of return.

How to Calculate

If you try to figure an IRR manually, you’ll spend a great deal of time. The process is an iterative, successive-approximations technique (math-speak for trial and error) that starts with a guess and narrows its way to a conclusion. Instead, use the Microsoft Excel template that you can download at http://www.realdata.com/book.

Example

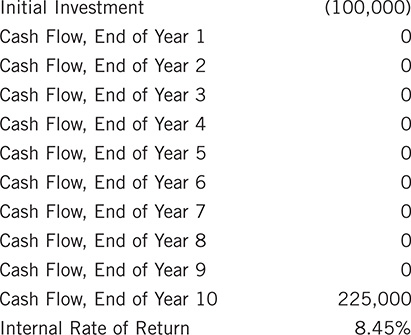

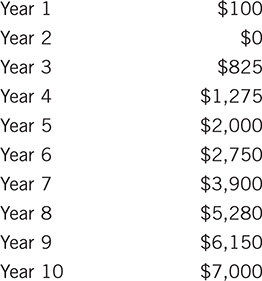

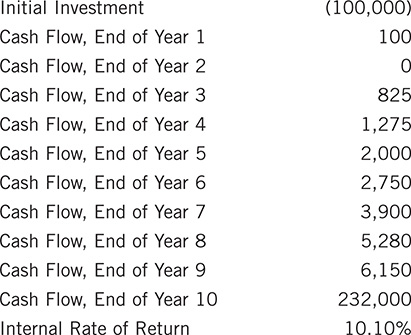

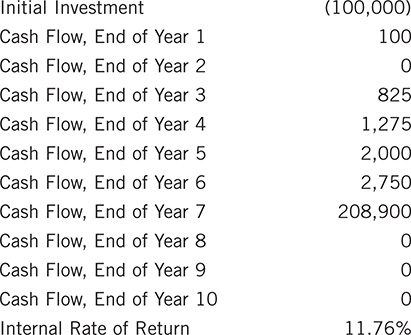

You’re considering the purchase of a property that requires a $100,000 cash investment. You forecast the following annual cash flows:

You expect to receive sale proceeds of $225,000 at the end of year 10. What is this investment’s IRR?

Enter the data into the Excel model as shown (remember that the cash flow for year 10 must include the sale proceeds):

Test Your Understanding

Using the Excel model and data from the preceding example, answer the following:

1. What happens to the IRR if you maintain the same cash flows and same proceeds, but can purchase the property with a cash investment that is $10,000 less?

2. What happens to the IRR if you invest the original $100,000, but sell at the end of year 7 and receive proceeds of $205,000?

3. If you received no cash flows from operating the property, but only the sale proceeds at the end of year 10, what would the IRR be on your $100,000 investment?

Answer

1.

3.