CHAPTER 8

Depreciation

8.1 INTRODUCTION

Depreciation is defined as decrease in the value of a physical property or asset with the passage of time. A physical asset has value because it provides monetary benefits to its owner. These benefits are in the form of future cash flows resulting from (i) the use of the asset to produce salable goods or services, or (ii) the ultimate sale of the asset at the end of its useful life. Depreciation, thus, represents decrease in the value due to lessening in the ability to produce these future cash flows, as a result of several causes such as wear and tear and obsolescence.

Although, depreciation does occur, it is really difficult to determine its magnitude well in advance. Depreciation, indeed, is not an actual cash flow but it is a tax-allowed deduction included in tax calculation in almost all industrialized countries. Depreciation lowers income tax as per the relation Tax = (Income-Deductions)(Tax rate).

8.2 DEPRECIATION TERMINOLOGY

The definition of the terms that are used in depreciation calculation are given below.

Book Depreciation and Tax Depreciation: Book depreciation is used by corporation or business for internal financial accounting. It indicates the reduced investment in an asset based upon the usage pattern and expected useful life of the asset.

Tax Depreciation: is used in tax calculation as per government regulations. A company subtracts annual tax of depreciation from its annual income to calculate the amount of taxes due each year. However, the tax depreciation amount must be calculated using a government approved method.

First Cost: It represents the installed cost of the asset. In includes purchase price, delivery and installation fees, and other depreciable direct costs incurred to prepare the asset for use. The term unadjusted basis, B or simply basis, is used when the asset is new, whereas the term adjusted basis is used after some depreciation has been charged.

Book Value: It represents the remaining, undepreciated capital investment on the books or record of the company after the total amount of depreciation charges to date have been subtracted from the basis. The book value, BVt is usually determined at the end of each year.

Recovery Period: It represents the depreciable life n of the asset in years.

Market Value: It is defined as the estimated amount that can be realized if the asset were sold on the open market. The book value and market value of different assets may be substantially different. For example, the market value of real estate tends to increase, but the book value will decrease as depreciation charges are taken. On the other hands a computer may have a market value much lower than its book value due to changing technology.

Salvage Value: It is defined as the estimated value of the asset at the end of its useful life. The salvage value S of the asset may be positive, zero, or negative depending upon the type of asset and situation in which it is being sold.

Depreciation Rate or Recovery Rate: It represents the fraction of the first cost removed by depreciation each year. This rate, d, may be same each year or different for each year of the recovery period.

8.3 METHODS OF DEPRECIATION

Although, there are several methods for depreciation calculation, the following methods are commonly used and therefore, only these methods are discussed in detail.

- Straight line (SL) method

- Declining balance (DB) method

- Sum-of-the-year-digits (SYD) method

- Sinking fund method

- Service output method

8.3.1 The Straight Line (SL) Method

This method assumes that the decrease in the value of the asset is directly proportional to its age. This method derives its name from the fact that the book value of the asset decreases linearly with time. This method is widely used for computing depreciation cost owing to the fact that it is simple and gives uniform annual depreciation charge. If

| n = | Depreciable life of the asset or recovery period in years |

| B = | First cost or original cost or unadjusted basis in rupees |

| S = | Estimated salvage value at the end of the life of the asset in rupees |

| dk = | Annual cost of depreciation in the kth year (1 ≤ k ≤ n) in rupees |

| Dk = | Cumulative depreciation cost through kth year in rupees |

| BVk = | Book value of the asset at the end of k years in rupees |

Then:

The term (B - S) is referred to as the depreciable value of an asset. The following example illustrates the depreciation calculation by SL method.

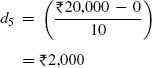

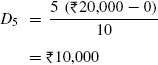

Example 8.1 A small equipment has first cost of ![]() 20,000 and a 10-year estimated life. The estimated salvage value of the equipment is zero at the end of 10 years. Calculate (a) depreciation cost during the fifth year, (b) cumulative depreciation cost through the fifth year, and (c) book value at the end of fifth year.

20,000 and a 10-year estimated life. The estimated salvage value of the equipment is zero at the end of 10 years. Calculate (a) depreciation cost during the fifth year, (b) cumulative depreciation cost through the fifth year, and (c) book value at the end of fifth year.

Solution Given B = ![]() 20,000

20,000

n =10 years

S=0

(a) d5 = ? (b) D5 = ? (c) BV5 = ?

(a) Using Eq. (8.1), we get

(b) Using Eq. (8.2), we get

(c) Using Eq. (8.3), we get

Example 8.2 A company purchased a small machine for ![]() 1,00,000. It paid sales taxes and shipping costs of

1,00,000. It paid sales taxes and shipping costs of ![]() 10,000. The installation cost of the machine is

10,000. The installation cost of the machine is ![]() 5,000 and its estimated useful life is five years. The estimated salvage value of the machine at the end of its useful life is

5,000 and its estimated useful life is five years. The estimated salvage value of the machine at the end of its useful life is ![]() 10,000. Calculate (a) depreciation cost during the third year, (b) cumulative depreciation cost through the third year and (c) book value at the end of third year.

10,000. Calculate (a) depreciation cost during the third year, (b) cumulative depreciation cost through the third year and (c) book value at the end of third year.

Solution Given B = ![]() 1,00,000 +

1,00,000 + ![]() 10,000 +

10,000 + ![]() 5,000 =

5,000 = ![]() 1,15,000

1,15,000

n = 5 years

S = ![]() 10,000

10,000![]()

8.3.2 The Declining Balance (DB) Method

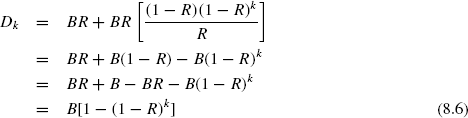

This method is also known by other names such as Matheson formula, constant percentage method. In this method, it is assumed that the annual cost of depreciation is a fixed percentage of the book value at the beginning of the year. The ratio of the depreciation in any one year to the book value at the beginning of the year is constant throughout the life of the asset and is designated by R(0 ≤ R ≤ 1). R is taken equal to 2/n when a 200% declining balance is used. This gives rate of recovery twice the straight line rate of 1/n and the declining balance method is known as double declining balance (DDB) method. Similarly, R = 1.5/n if 150% declining balance method is specified. The following relationships are used for calculating depreciation costs by DB method:

For first year

Since BV1 = B

Similarly, for second year

For third year

In general, depreciation cost in kth year i.e. dk is

The relationship for cumulative depreciation cost through kth year is obtained as:

Dk = d1 + d2 + d3 + ……… dk

= BR + BR(1 – R) + BR(1 – R)2 + ……… + BR(1 – R)k-1

= BR + BR[(1 – R) + (1 – R)2 + ……… + (1 – R)k-1]

(1 – R) + (1 – R)2 + ……… + (1 – R)k-1 forms a geometric series and its sum is

obtained as

Thus,

Similarly, book value at the end of useful life of the asset is given as:

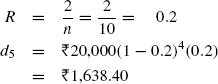

Example 8.3 Solve Example 8.1 by double declining balance (DDB) method.

Solution Given, B = ![]() 20,000

20,000

n = 10 years

S = 0

(a) d5 = ? (b) D5 = ? (c) BV5 = ?

(a) Using Eq. (8.5), we get

For DDB,

(b) Using Eq. (8.6), we get

(c) Using Eq. (8.7), we get

8.3.3 Sum-of-the-Years'-Digits (SYD) Method

The annual depreciation cost for a given year by SYD method is obtained by taking the product of SYD depreciation factor for that year and the difference between unadjusted basis (B) and the salvage value of the asset at the end of its useful life. In order to compute SYD depreciation factor for any year, use the following steps:

- List the digits corresponding to the number for each year of life in reverseo rder

- Compute the sum of these digits

- Divide each number of the reverse-ordered list by the sum to obtain SYD depreciation factor for each year of life of the asset.

For example, for an asset having useful life of six years, SYD depreciation factors are as follows:

Year |

Digits in Reverse Order |

SYD Depreciation Factor |

|---|---|---|

1 |

6 |

6/21 |

2 |

5 |

5/21 |

3 |

4 |

4/21 |

4 |

3 |

3/21 |

5 |

2 |

2/21 |

6 |

1 |

1/21 |

| Sum of digits | 21 |

The annual cost of depreciation for any year k is given as

The book value at the end of year k is given as:

The cumulative depreciation through the kth year is given as:

Example 8.4 Solve Example 8.2 by SYD method.

Solution Given, B = ![]() 1,15,000

1,15,000

n = 5 years

S = ![]() 10,000

10,000

(a) d3 = ? (b) D3 = ? (c) BV3 = ?

(a) Using Eq. (8.9), we get

(b) Using Eq. (8.10), we get

(c) Using Eq. (8.11), we get

8.3.4 The Sinking Fund Method

In this method, it is assumed that the funds required to replace the asset accumulates in a sinking fund. The total fund accumulated in the sinking fund plus interest on it up to any given time is assumed to be equal to the total depreciation cost up to that time. With this method a uniform yearly deposit can easily be calculated, if the estimated life, salvage value and interest on the sinking fund are known. The depreciation cost for any year is subsequently obtained by adding annual deposits and accumulated interest for that year. For an interest rate of i%, the following relationships are used to calculate

depreciation costs and book value of the asset:

Example 8.5 Solve Example 8.1 by 8% sinking fund method.

Solution Given, B = ![]() 20,000

20,000

n = 10 years

S = 0

i = 8%

(a) d5 = ? (b) D5 = ? (c) BV5 = ?

d = (![]() 20,000 – 0)(A/F, 8%, 10)

20,000 – 0)(A/F, 8%, 10)

= (![]() 20,000)(0.0690)

20,000)(0.0690)

= ![]() 1,380

1,380

(a) d5 = (![]() 13,800)(F/P, 8%, 4)

13,800)(F/P, 8%, 4)

= (![]() 1,380)(1.3605)

1,380)(1.3605)

= ![]() 1,877.49

1,877.49

(b) D5 = (![]() 20,000 – 0)(A/F, 8%, 10)(F/A, 8%, 5)

20,000 – 0)(A/F, 8%, 10)(F/A, 8%, 5)

= (![]() 20,000)(0.0690)(5.8666)

20,000)(0.0690)(5.8666)

= ![]() 8,095.91

8,095.91

(c) BV5 = ![]() 20,000 – [(

20,000 – [(![]() 20,000 – 0)(A/F, i%, n)(F/A, i%, k)]

20,000 – 0)(A/F, i%, n)(F/A, i%, k)]

=![]() 20,000 –

20,000 – ![]() 8,095.91

8,095.91

= ![]() 11,904.09

11,904.09

8.3.5 The Service Output Method

This method assumes that the depreciation cost of an asset is based on the service that it will render during the useful life. Depreciation for any period is computed on the basis of service that has been rendered during that period. If,

B = First cost or original cost or unadjusted basis in rupees.

S = Estimated salvage value at the end of the life of the asset in rupees.

Y = Maximum capacity of service of the asset during its useful life.

y = Quantity of service rendered in a period.

Then, the depreciation is computed per unit of service rendered as given below:

Depreciation per unit of service = (B – S)/Y

Depreciation for y units of service in a period = ![]()

Example 8.6 A small equipment has first cost of ![]() 20,000 and a 10-year estimated life. The estimated salvage value of the equipment is zero at the end of 10 years. It is expected that the equipment will be used a total of 10,000 hrs over a period of 10 years. In the fifth year of operation, the estimated usage is 600 hours and the cumulative usage by the end of fifth year is 6,000 hours. If the depreciation is based on hours of use, determine (a) depreciation cost during the fifth year, (b) cumulative depreciation cost through the fifth year and (c) book value at the end of fifth year.

20,000 and a 10-year estimated life. The estimated salvage value of the equipment is zero at the end of 10 years. It is expected that the equipment will be used a total of 10,000 hrs over a period of 10 years. In the fifth year of operation, the estimated usage is 600 hours and the cumulative usage by the end of fifth year is 6,000 hours. If the depreciation is based on hours of use, determine (a) depreciation cost during the fifth year, (b) cumulative depreciation cost through the fifth year and (c) book value at the end of fifth year.

Solution Depreciation per hour ![]() =

= ![]() 2.0 per hour

2.0 per hour

d5 = 600 hours (![]() 2.0 per hour) =

2.0 per hour) = ![]() 1,200

1,200

D5 = 6,000 hours (![]() 2.0 per hour) =

2.0 per hour) = ![]() 12,000

12,000

BV5 = ![]() 20,000 –

20,000 – ![]() 12,000 =

12,000 = ![]() 8,000

8,000

PROBLEMS

- Define depreciation. What are reasons for computing depreciation?

- Distinguish between

- Book depreciation and tax depreciation.

- Book value and market value.

- Commonwealth Infra Ltd has just purchased a semi automatic concrete mixer for

22,00,000. Its expected life is 15 years and the salvage value at the end of its useful life is 3,50,000. Using the double declining balance (DDB) method, compute (a) depreciation cost during the sixth year, (b) cumulative depreciation cost through the sixth year, and (c) book value at the end of sixth year.

22,00,000. Its expected life is 15 years and the salvage value at the end of its useful life is 3,50,000. Using the double declining balance (DDB) method, compute (a) depreciation cost during the sixth year, (b) cumulative depreciation cost through the sixth year, and (c) book value at the end of sixth year. - Kailash Automobiles has purchased a biometric system for its employees in 12,00,000. The expected life of the system is 15 years. The salvage value of the system at the end of its useful life is 20,000. Find the following using the 8% sinking fund method of depreciation:

- Depreciation at the end of fifth and eighth year.

- Book value at the end of third and sixth year.

- By each of the methods indicated below, calculate the book value of a book binding machine at the end of 5 years if the machine originally cost 1,50,000 and had an estimated salvage value of 10,000. The useful life of the machine is 8 years.

- Straight line method of depreciation.

- 6% sinking fund method.

- Ranbaxy has purchased a bottle filling machine for 5,00,000. The plant engineer estimates that the machine has a useful life of five years and a salvage value of 10,000 at the end of its useful life. Using the straight line method, compute (a) depreciation cost during the third year, (b) cumulative depreciation cost through the third year and (c) book value at the end of third year.

- Alpha Chemicals has procured a blending unit for 5,00,000. Its salvage value at the end of its useful life is almost negligible and can be taken as zero. Its output during the useful life is equivalent to 1,20,00,000. During the fifth year of its operation it gave an output equivalent to 10,00,000 and the cumulative output worth 50,00,000. Determine the depreciation for the fifth year of the operation of the unit and book value at the end of fifth year using the service output method.

- A machine costing 5,00,000 is estimated to be usable for 1,000 units and then have no salvage value.

- What would be the depreciation charge for a year in which 400 units were produced?

- What would be the total depreciation charged after 800 units were produced?

- An asset costs 2,00,000 and has a useful life of 10 years and a salvage value of 20,000. Determine the depreciation charge for the third year and the book value at the end of third year using (a) double declining balance (DDB) method, and (b) sum-of-year-digits (SYD) method.

- Nova Auto Ltd. has purchased a car painting plant for 20,00,000. Its expected life is 10 years and the salvage value at the end of its useful life is 1,00,000. Using the sum-of-the-year-digits (SYD) method, compute (a) depreciation cost during the third year, (b) cumulative depreciation cost through the fifth year and (c) book value at the end of sixth year.