CHAPTER 10

Economy Study With Inflation Considered

10.1 INTRODUCTION

Inflation is observed nearly every day in personal and professional life. The government units, business, and industrial corporations closely watch and analyse the impact of inflation rate. When inflation is considered, an engineering economy study yields different results compared to one in which it is not considered. In the last few years, inflation has been a major concern in India and in most industrialized nations. Inflation rate is sensitive to real as well as perceived factors of the economy. Factors such as the cost of energy, interest rates, availability and cost of skilled people, scarcity of materials, political instability, and money supply have significant short-term and long-term impacts on the inflation rate. Owing to the significance of inflation, it is necessary to incorporate the effects of inflation into an economic analysis. This chapter covers the basic techniques that integrate inflation into economic analysis.

10.2 EFFECTS OF INFLATION

We understand very well that ![]() 1,000 now does not have the same purchasing power as it had few years back. In other words,

1,000 now does not have the same purchasing power as it had few years back. In other words, ![]() 1,000 now cannot purchase the same amount of a commodity as

1,000 now cannot purchase the same amount of a commodity as ![]() 1,000 did few years back. This happens due to inflation. Inflation is defined as an increase in the amount of money necessary to obtain the same amount of a commodity or service before the inflated price was present. Inflation occurs because the value of currency has gone down and consequently, it takes more money to purchase the same amount of goods or services. In order to compare the monetary amounts that occur in different time-periods, the different-valued currency must first be converted to constant-value currency so that they represent the same purchasing power over time.

1,000 did few years back. This happens due to inflation. Inflation is defined as an increase in the amount of money necessary to obtain the same amount of a commodity or service before the inflated price was present. Inflation occurs because the value of currency has gone down and consequently, it takes more money to purchase the same amount of goods or services. In order to compare the monetary amounts that occur in different time-periods, the different-valued currency must first be converted to constant-value currency so that they represent the same purchasing power over time.

Money in one period of time t1 can be brought to the same value as money in another period of time t2 by using the following equation:

Rupees in period t1 are called constant-value rupees or today's rupees. Rupees in period t2 are called future rupees. If f represents the inflation rate per period (years) and n is the number of time periods (years) between t1 and t2, Eq.(10.1) is

As an illustration, consider the price of a pizza as ![]() 25 on March 2009. If inflation averaged 5% during the last year, this cost is last year's equivalent of

25 on March 2009. If inflation averaged 5% during the last year, this cost is last year's equivalent of

![]() 25/(1.05) =

25/(1.05) = ![]() a23.81 on March 2008

a23.81 on March 2008

A predicted price in 2010 is

![]() 25(1.05) =

25(1.05) = ![]() 26.25 on March 2010

26.25 on March 2010

If inflation averages 5% over the next five years, Eq. (10.3) is used to predict pizza price in 2014:

![]() 25(1.05)5 =

25(1.05)5 = ![]() 31.91 on March 2014

31.91 on March 2014

This is a 27.64% increase over the 2009 price at 5% inflation. If inflation averages 8% per year, the pizza cost in 5 years will be ![]() 36.73, an increase of 46.92%. In some parts of the world, hyperinflation may average 50% per year. In such an unfortunate economy, the pizza price rises from

36.73, an increase of 46.92%. In some parts of the world, hyperinflation may average 50% per year. In such an unfortunate economy, the pizza price rises from ![]() 25 to

25 to ![]() 189.84 in five years. This is why countries experiencing hyper inflation must devalue the currency by factors of 100 and 1000 when unacceptable inflation rates persist.

189.84 in five years. This is why countries experiencing hyper inflation must devalue the currency by factors of 100 and 1000 when unacceptable inflation rates persist.

In industrial or business environment, at a reasonably low inflation rate averaging 5% per year equipment or services with a first cost of ![]() 5,00,000 will increase by 27.64% to

5,00,000 will increase by 27.64% to ![]() 6,38,200 over a span of five years.

6,38,200 over a span of five years.

It is important to understand the meaning of the following three different rates:

Real or Inflation-free Interest Rate i: It represents the rate at which interest is earned when the effects of inflation have been removed. The real interest rate presents an actual gain in purchasing power.

Inflation-adjusted Interest Rate if : It is the interest rate that has been adjusted to take inflation into account. The market interest rate, which we hear everyday, is an inflation-adjusted rate. This rate is in fact a combination of the real interest rate i and the inflation rate f, and therefore, it changes as the inflation rate changes. It is also known as the inflated interest rate.

Inflation Rate f: It is a measure of the rate of change in the value of currency.

Deflation is the opposite of inflation. In the presence of deflation, the purchasing power of the monetary unit is greater in the future than at present and therefore, it will take fewer rupees in the future to buy the same amount of goods or services as it does today. Computations considering deflation can by done by using equations (10.2) and (10.3), but the deflation rate is used as −f in these equations. For example, if deflation is estimated to be 3% per year, an asset that costs ![]() 5,00,000 today would have a first cost five years from now as:

5,00,000 today would have a first cost five years from now as:

10.3 PRESENT WORTH CALCULATIONS ADJUSTED FOR INFLATION

We have seen in Chapter 3 that the relationship between present worth (P) and future worth (F) is

In the above relation, F is a future-rupees amount with inflation built in. F can be converted into today's rupees by using Eq. (10.2).

If the term i + f+ if is defined as if, the equation becomes

The symbol if is called the inflation-adjusted interest rate and is defined as

where i=Real interest rate

f = Inflation rate

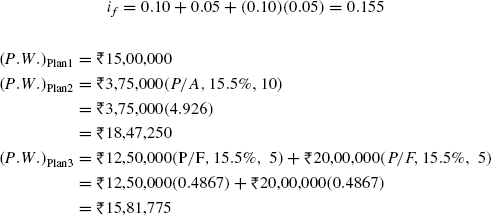

For a real interest rate of 10% per year and inflation rate of 5% per year, Eq. (10.6) yields an inflated interest rate of 15.5%.

Example 10.1 An engineering alumni of Jamia Millia Islamia wishes to donate to scholarship fund of the faculty of engineering and technology. The following three options are available:

Plan 1: ![]() 15,00,000 now.

15,00,000 now.

Plan 2: ![]() 3,75,000 per year for 10 years beginning 1 year from now.

3,75,000 per year for 10 years beginning 1 year from now.

Plan 3: ![]() 12,50,000 five years from now and another

12,50,000 five years from now and another ![]() 20,00,000 five years from now.

20,00,000 five years from now.

The Dean of the faculty wants to select the plan that maximizes the buying power of the rupees received. If the donation earns a real interest rate of 10% per year and the inflation rate is expected to average 5% per year, which plan should be accepted? Evaluate the plans by taking into account the inflation.

Solution The inflation-adjusted interest rate if is calculated as:

Since (P.W.)Plan2 is the largest in today's rupees, select Plan 2.

Example 10.2 A 15-year bond of ![]() 5,00,000 that has a dividend rate of 5% per year, payable semiannually, is currently for sale. If the expected rate of return of the purchaser is 8% per year, compounded semiannually, and if the inflation rate is expected to be 1.5% each 6-month period, what is the bond worth now (a) without an adjustment for inflation and (b) when inflation is considered?

5,00,000 that has a dividend rate of 5% per year, payable semiannually, is currently for sale. If the expected rate of return of the purchaser is 8% per year, compounded semiannually, and if the inflation rate is expected to be 1.5% each 6-month period, what is the bond worth now (a) without an adjustment for inflation and (b) when inflation is considered?

Solution

(a) Without inflation adjustment: The semiannual dividend is I = [(![]() 5,00,000)(0.05)]/2 =

5,00,000)(0.05)]/2 = ![]() 12,500. At a nominal 4% per 6 months for 30 periods, the P.W. is

12,500. At a nominal 4% per 6 months for 30 periods, the P.W. is

(b) With inflation: Use the inflated rate if

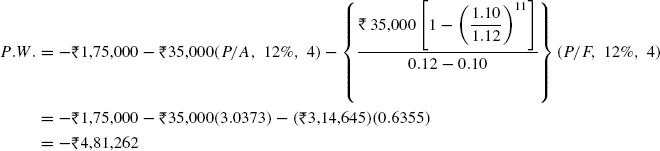

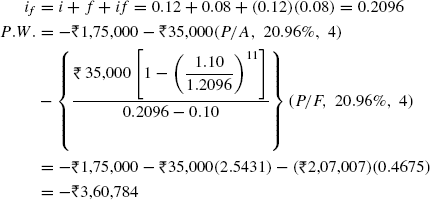

Example 10.3 The manager of a company wishes to calculate present worth (P.W.) of a small project with estimated costs of ![]() 1,75,000 now and

1,75,000 now and ![]() 35,000 per year for 5 years beginning 1 year from now with increase of 10% per year thereafter for the next 10 years. The real interest rate is 12% per year. Calculate the present worth (a) without an adjustment for inflation and (b) considering inflation at a rate of 8% per year.

35,000 per year for 5 years beginning 1 year from now with increase of 10% per year thereafter for the next 10 years. The real interest rate is 12% per year. Calculate the present worth (a) without an adjustment for inflation and (b) considering inflation at a rate of 8% per year.

Solution (a) Figure 10.1 shows the cash flow diagram. The P.W. without an adjustment for inflation is found using i = 12% and g = 10%.

Fig. 10.1 Cash flow diagram, Example 10.3

To adjust for inflation, calculate the inflated interest rate if

It is clear from the result of the above example that the present value of future inflated rupees is reasonably less when inflation adjustment is considered. Thus, in a high-inflation economy, it is advantageous for the borrower to use future (inflated) rupees whenever possible to make payments to repay a loan.

10.4 FUTURE WORTH CALCULATIONS ADJUSTED FOR INFLATION

If future worth F is the actual amount of money accumulated at time n, then it is obtained using the inflation adjusted interest rate from the following relation. It should be noted that the inflation adjusted interest rate is also known as market rate.

For example, if market rate (including inflation) is 12%, ![]() 10,000 invested now for 10 years will accumulate to

10,000 invested now for 10 years will accumulate to

If F represents the purchasing power of the actual amount accumulated at time n, then it is obtained from the following relation:

For example, consider the same ![]() 10,000 now, a 12% per year market rate, and inflation rate of 5% per year. In 10 years, the purchasing power has risen, but only to

10,000 now, a 12% per year market rate, and inflation rate of 5% per year. In 10 years, the purchasing power has risen, but only to ![]() 19,066.85.

19,066.85.

This is ![]() 11,991.15 (38.61%) less than the

11,991.15 (38.61%) less than the ![]() 31,058 actually accumulated at 12%. Thus, it can be concluded that 5% inflation over 10 years reduces the purchasing power of money by 38.61%.

31,058 actually accumulated at 12%. Thus, it can be concluded that 5% inflation over 10 years reduces the purchasing power of money by 38.61%.

Alternately, the future amount of money accumulated with today's buying power is determined by calculating the real interest rate and using it in the F/P factor to compensate for the decreased purchasing power of the rupees. This real interest rate is the i in Eq. (10.6)

The real interest rate i represents the rate at which today's rupees expand with their same purchasing power into equivalent future rupees. An inflation rate larger than the market interest rate leads to a negative real interest rate. The use of this interest rate is appropriate for calculating the future worth. For the example of ![]() 10,000 in today's rupees from Eq. (10.9)

10,000 in today's rupees from Eq. (10.9)

If F is required to be calculated without considering interest rate but considering only the inflation rate, then the following relation is used:

Let us once again consider the ![]() 10,000 used previously. If this amount is rising at the inflation rate of 5% per year, the amount 10 years from now will be

10,000 used previously. If this amount is rising at the inflation rate of 5% per year, the amount 10 years from now will be

If F is to be calculated for a situation in which both inflation rate and real interest rates are considered then we must use the market (inflation-adjusted) rate. The market rate is determined as

where, ![]()

Thus for the same ![]() 10,000 amount,

10,000 amount,

Thus, F = P(F/P, i′f, n) = ![]() 10,000(F/P, 12%, 10) =

10,000(F/P, 12%, 10) = ![]() 10,000(3.1058) =

10,000(3.1058) = ![]() 31,058

31,058

The result shows that ![]() 31,058 of ten years in the future will be equivalent to

31,058 of ten years in the future will be equivalent to ![]() 10,000 now with a real return of i = 6.66% per year and inflation of f = 5% per year.

10,000 now with a real return of i = 6.66% per year and inflation of f = 5% per year.

Example 10.4 A company wants to buy an equipment. The management of the company considers the following two plans:

Plan A: Buy now

Plan B: Buy later

If the company selects plan A, the equipment will be purchased now for ![]() 10,00,000. However, if the company selects plan B, the purchase will be deferred for 4 years when the cost is expected to

10,00,000. However, if the company selects plan B, the purchase will be deferred for 4 years when the cost is expected to ![]() 17,00,000. The company expects a real M.A.R.R. of 10% per year. The average inflation rate in the country is 8% per year. Determine, whether the company should purchase now or later (a) when inflation is not considered and (b) when inflation is considered

17,00,000. The company expects a real M.A.R.R. of 10% per year. The average inflation rate in the country is 8% per year. Determine, whether the company should purchase now or later (a) when inflation is not considered and (b) when inflation is considered

Solution

(a) Inflation not considered: Calculate the F.W. value for plan A at an interest rate i = M.A.R.R. = 10% and n = 4 years. Compare the calculated F.W. value with the expected cost of plan B i.e. ![]() 17,00,000 and select the one having the lower cost.

17,00,000 and select the one having the lower cost.

Select Plan A i.e. purchase now.

(b) Inflation considered: First calculate the inflation-adjusted M.A.R.R. as

Use if to compute F.W. for plan A

Select Plan B i.e. purchase later.

10.5 CAPITAL RECOVERY CALCULATIONS ADJUSTED FOR INFLATION

Due to inflation, future rupees will have less purchasing power than today's rupees and therefore, more rupees will be required to recover present investment. Thus, when inflation is considered, it is necessary to use inflated interest rate in the A/P formula. For example, if ![]() 10,000 is invested today at a real interest rate of 12% per year when the inflation rate is 7% per year, the equivalent amount that must be recovered each year for 5 years in future rupees is calculated as

10,000 is invested today at a real interest rate of 12% per year when the inflation rate is 7% per year, the equivalent amount that must be recovered each year for 5 years in future rupees is calculated as

It should also be noted that one can invest fewer rupees in present to accumulate a specified amount of future (inflated rupees). This suggests the use of a higher interest rate i.e. if rate, to produce a lower value in the A/F formula. For example, the annual equivalent (inflation adjusted) of F = ![]() 10,000 five years from now in future rupees is

10,000 five years from now in future rupees is

Example 10.5 What annual deposit is required for 5 years to accumulate an amount of money with the same purchasing power as ![]() 1,000 today, if the market interest rate is 12% per year and inflation is 7% per year.

1,000 today, if the market interest rate is 12% per year and inflation is 7% per year.

Solution First, find the actual number of future (inflated) rupees required five years from now.

F = (Present buying power)(1 + f)5 = ![]() 1,000(1.07)5 =

1,000(1.07)5 = ![]() 1,402.55

1,402.55

The actual amount of the annual deposit is calculated using the market (inflated) interest rate of 12%

PROBLEMS

- Convert

50,000 future rupees in year 8 into constant-value rupees of today if the inflation-adjusted (market) interest rate is 12% per year and the real interest rate is 5% per year.

50,000 future rupees in year 8 into constant-value rupees of today if the inflation-adjusted (market) interest rate is 12% per year and the real interest rate is 5% per year. - Convert 50,000 future rupees in year 8 into constant-value rupees of today if the inflation-adjusted (market) interest rate is 12% per year and the inflation rate is 6% per year.

- Tata Motors announced that the price of Nano car is going to increase by only the inflation rate for the next 3 years. If the current price of a car is 1,20,000 and the inflation rate is expected to average 5% per year, what is the expected price 3 years from now?

- The cost of a machine was 2,50,000 five years ago. If a similar machine costs 3,00,000 now and its price increased only by the inflation rate, what was the annual inflation rate over that 5-year period?

- What annual inflation rate is implied from a market interest rate of 12% per year when the real interest rate is 5% per year?

- What is the real interest rate per quarter when the market interest rate is 24% per year, compounded quarterly, and the inflation rate is 2.5% per quarter?

- Compare the following two alternatives on the basis of their present worth values, using a real interest rate of 8% per year and an inflation rate of 5% per year, (a) without any adjustment for inflation and (b) with inflation considered.

Alternative 1 Alternative 2 First cost, -1,50,000 -2,40,000 Annual operating cost, /year-1,40,000 -1,00,000 Salvage value, 25,000 40,000 Life in years 5 5 - A company is considering to purchase a machine for its operations. The following two alternatives are available. The company has a M.A.R.R. of a real 12% per year and it expects inflation to be 5% per year. Use P.W. analysis to determine which machine should be purchased.

Machine 1, Future Rupees Machine 2, Today’s Rupees First cost, -3,00,000 -4,75,000 Annual operating cost, /year-2,75,000 -1,75,000 Life in years 10 10 - A company wants to set aside money today so that it will be able to purchase new equipment 5 years from now. The price of the equipment is expected to increase only by the inflation rate of 5% per year for each of the next 5 years. If the total cost of the equipment now is 2,25,000, determine (a) the expected cost of the equipment after 5 years and (b) how much the company will have to set aside now, if it earns interest at a rate of 10% per year.

- If you make an investment in real estate that is guaranteed to net you 7.5 million, 20 years from now, what will be the buying power of that money with respect to today's rupees if the market interest rate is 10% per year and the inflation rate is expected to be 4% over that time period?

- What is the annual worth in then-current rupees in years 1 through 5 years of a receipt of 37,50,000 now, if the market interest rate is 8% per year and the inflation rate is 4% per year?

- Compare the following two alternatives on the basis of annual worth analysis, using M.A.R.R. equal to a real interest rate of 10% per year and an inflation rate of 5% per year, if the estimates are (a) constant-value rupees and (b) future rupees.

Alternative 1 Alternative 2 First cost, -7,50,000 -51,25,000 Annual operating cost, /year-3,50,000 -25,000 Salvage value, 2,00,000 10,00,000 Life in years 5 ∞