HAVE YOU ever wondered how you could improve your fraud analysis or audit results? With CaseWare IDEA Data Analysis Software it's easy to learn capabilities are worth it. IDEA is very powerful yet easy to learn. My students find it very intuitive. Tasks in Excel that can take hours are done within minutes in IDEA. It looks like Excel so you can play around with it for a couple of hours and grasp the features.1 My students are more apt to use IDEA not only in the classroom; many have adopted IDEA in their workplaces, simply because IDEA has shown that it is one of the most effective tools when converting data into information. In detecting fraud your goal is to establish the validity of the transactions; in conjunction with determining a specific reasoning as to why the transactions are associated with each entity. The associations are usually distinct in nature and provide an avenue to further discover additional nuances. IDEA is the tool for establishing transparency and direct correlations.2 IDEA is most useful when there is a problem in audit, financial investigations, and financial statement fraud. Examples include assessing the extent of bad loans, looking at performance in collecting cash, or simply speeding up the time to prove calculations. When there is a need to determine if items are in error, a problem needs to be quantified, or certain items identified, then IDEA should be used. IDEA can also be useful with checking procedures. An indirect way of checking procedures is to draw an inference about the effectiveness of procedures based on the results of substantive tests. If there are no errors, it can be established that the procedures must be working. If there are errors, then the data must be sifted through to decipher where the discrepancy lies.

Fraud analytic techniques are appropriate with a large volume of small-value transactions. This is true with IDEA: The greater the volume of data, the more useful IDEA will be for the investigation. If there are fewer than a few hundred records, IDEA is unlikely to provide much benefit over manual work.

For large files, say over 200,000 records, then a calculation of records should be made readily available to exercise the power of IDEA (i.e., number of records multiplied by the approximate space each record takes). IDEA can be used on files with several million records, which are adequate to fulfill the purpose of IDEA and its functions. The amount of data available for each item also makes a difference to the potential benefit of using IDEA. Items with full comprehensive detail will allow a wide variety of tests. If only limited information is available, IDEA can be constrained to simple calculations, less complex analysis, and sampling.

IDEA is typically useful for the following entities:

- Accounts receivable. More than 300 balances and 3,000 transactions

- Fixed assets. More than 2,000 items

- Inventories. More than 2,000 stock lines

- Purchases. More than 3,000 transactions

- Credit cards. More than 1,000 transactions on a given day

IDEA is used widely by major accounting firms; federal, state, and local government entities; corporate industries; and universities. The functionality and power source of IDEA has attracted those whose professions are internal and financial auditors, forensic accountants, analysts, and fraud investigators.

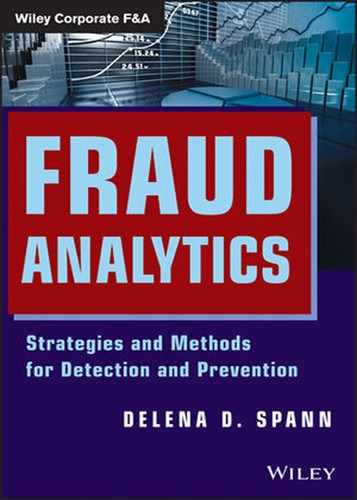

IDEA allows data to be imported from a variety of sources. The Import Assistant easily guides users to import files from text (e.g., CSV) files, Microsoft Excel and Access files, and different databases (e.g., XML, dBase). The IDEA process shown in Figure 6.1 describes how to the begin using the IDEA software component.

IDEA has a Report Reader feature that creates reports using system tools. Reports can also be saved as PDF or PRN files; then the Reader can describe and capture the data in IDEA. Data can be exported and the results of the analysis can be exported into multiple formats, such as PDF, Microsoft Word, Excel, HTML, Text, or RTF.

Source: CaseWare IDEA Software Interface. Reprinted with permission of CaseWare IDEA.

DETECTING FRAUD WITH IDEA

DETECTING FRAUD WITH IDEA

IDEA can perform quick analysis of large volumes of financial data to produce information, to import numerous different formats of data, to perform complex comparisons of different data sources, to apply Benford's Law, and to identify duplicates and gaps in data.

IDEA can assist in uncovering financial fraud and money laundering transactions with the click of a few buttons. When using trend analysis, correlation analysis, and Benford's Law functions to identify unusual transactions (duplicates, odd deposits, and transaction dates), matching accounts, and the circumvention of large numbers of transactions all can be clearly defined by using IDEA to discover the anomalies.

IDEA is a more user-friendly method of analyzing financial transactions than one might think. It is capable of handling some of the most complicated and complex analyses that an examiner faces.

A seasoned analyst received financial statements of ten separate accounts from Wallstreet Financial Lending (WFL). The vice president of WFL maintained that the account holder was a longtime customer of the bank and had previously donated a sum of $1 million to a local organization that supports the treatment and diagnosis of autism in young children. Although this was indeed a kind gesture, it does not prove that the analyst received CSV files of all transactions made for the past six years. The accounts in total had well over 400,000 financial transactional details.

Another file surfaced with additional CSV and Excel files which included critical information on offshore accounts and names of shareholders and investors. IDEA was the tool of choice used to detect the red flags. The analyst imported the transaction and shareholder files into IDEA, associated each detail field with a shareholder and/or investor using the Join Databases and Extraction fields to replicate selected shareholders accounts, and used the Sort and Control totals to compare the details to other conspicuous amounts.

The fraud examiner discovered what appeared to be additional missing financial transaction details, discrepancies within the transactions were unveiled as fields were joined and understated amounts of shareholder percentages were discovered. Knowing this discrepancy, the sources were reviewed. It was determined that the original CSV and Excel files were incomplete. This meant that the 400,000 financial transaction details were now uncovered from a 500,000-detail financial statement which also assisted in determining that 100,000 records were missing.

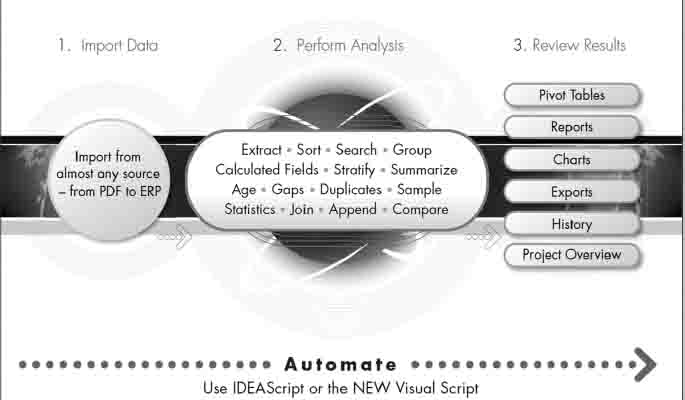

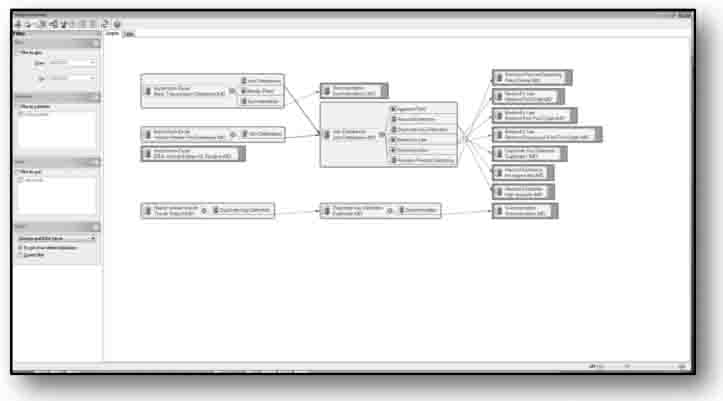

Figure 6.2 depicts the general ledger that contains balances for each account together with the transaction history and various references and descriptions. Usually balances and transactions are held in different files, but the closing balances can be proved by summarizing the transactions and opening balances.

Figure 6.3 displays the accounts receivable that are usually viewed as items of particular concern. They may include invoices, unmatched cash, and large balances, particularly where customers are in financial difficulty.

FIGURE 6.2 General Ledger Analysis

Source: CaseWare IDEA Software Interface. Reprinted with permission of CaseWare IDEA.

FIGURE 6.3 IDEA Interface Summarization

Source: CaseWare IDEA Software Interface. Reprinted with permission of CaseWare IDEA.

FRAUD ANALYSIS POINTS OF IDEA

Extractions are one of the most frequently used functions to identify items which satisfy a specific characteristic, such as transactions of more than $20,000 on any given date. IDEA will allow up to 50 separate extractions with a single pass through the database.

You can extract the top or bottom records. For example, you can extract the top ten transactions for every account. The following three key elements should be considered prior to defining the analysis:3

- Identify missing and duplicate records. Identify duplicate items within a database (e.g., duplicate financial transactions, duplicate account numbers, or duplicate insurance claims). The Duplicate Key Exclusion identifies duplicates but only where a specified field is different. Search for gaps in numerical orders, date of sequences, such as invoice numbers.

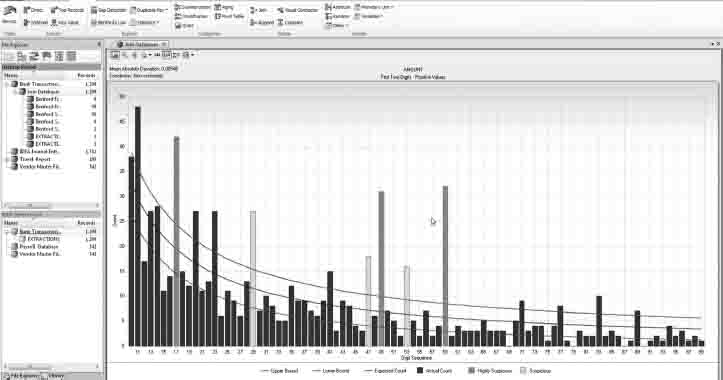

- Identify possible fraud. Detect possible errors, potential fraud, or other irregularities using Benford's Law. Benford's Law states that digits and digit sequences in a data set follow a predictable pattern. The analysis counts digit occurrences of values in the database and compares the totals to the predicted result according to Benford's Law (see Figure 6.4).

- Search. Find text easily within multiple fields of a database without using an equation to specify the criteria. By entering the text you are looking for and by using wildcards, you can locate and isolate quickly the transactions you want to find. You can search not only in all the fields in a database but also in more than one database simultaneously.

CORRELATION, TREND ANALYSIS, AND TIME SERIES ANALYSIS

These three components—correlation, trend analysis, and time series analysis—were developed in conjunction with Dr. Mark Nigrini.3 This function of IDEA allows you to analyze historical data and to predict values into the future. You can forecast the current data and identify the difference between the predicted and actual data. You can also measure the relationship between two variables, such as sales for one branch compared to the sales for the whole organization. You also can detect groups with higher potential of fraud or erroneous transactions.

Due to its functionality and user-friendliness, IDEA is one of the leading fraud data analysis software tools. Its provides innovative development, high-quality support and service, and an enthusiastic user community.

WHAT IS IDEA'S PURPOSE?

In today's fraud climate, many fraud industry professionals are asked to do more. Analysis is constantly being challenged to “value add” the techniques that are in place. Due to the collapse of several business entities within recent years (e.g., Enron, Lehman Brothers, Stanford, UBS Financial Services, etc.), fraud analytics is expected to stand at the forefront of examining complex information and volume. Fraud examiners must be aware of fraud indicators and savvy regarding the latest fraud analytics tools; they must actively use and monitor those transactions that somehow seem suspicious or potentially fraudulent, and be prepared to carry out dynamic fraud investigations.

FIGURE 6.4 Benford's Law Analysis Graph

Source: CaseWareIDEA Software Interface. Reprinted with permission of CaswWare IDEA.

Fraud investigations require a combination of intuition and a computer-based software tool. Everyone needs a tool that not only allows users to evaluate high-dollar amounts but also allows users to examine and monitor high-risk transactions, sort duplicate transactions of a 5,000-item data set, and enables continuous edits and updates. IDEA is one of the primary tools in fraud investigations that explores a “thought” and uncovers fraud that may have gone unnoticed.

Fraud examiners use fraud analytics tools to search for and identify red flags of fraud. The results of a data analysis do not constitute proof of fraud; however, the results show users where to take a closer look. IDEA is a powerful investigative tool that is widely used in the business and law enforcement sectors. Today financial crime investigations are more convoluted than in years past; therefore, investigators must make every effort to learn and navigate the tools that are available.

IDEA can examine millions of transactions, though the level of analysis requires that users understand the components analysis, interpretation and proven results when requesting a voluminous amount of data. Detecting potential fraud hinges on the ability not only to ask the right questions but to ask specific questions. Fraud analytics has the capability of revealing fraud schemes. This is the very reason that tools such as IDEA are critical to the overall success of the fraud investigation.

As a fraud examiner, it is imperative that you keep up to date on the knowledge, skills, and abilities of the latest patterns and trends that surface. The greater your effectiveness in identifying fraud and using the tools that can assist in enhancing the effort, the better you can support your organization. The Association of Certified Fraud Examiners (ACFE) is one of the best places to start in keeping abreast of the latest technology uses and trends. IDEA is a valuable tool also in performing financial statement analysis. IDEA makes it less complicated to take an account from multiple charts of accounts and manipulate sole transactions in the account and to reconcile those transactions with a summary of specific amounts. Using IDEA makes fraud examiners more efficient at discovering financial statement fraud.

When using fraud analytics, it is critical to keep in mind that one of the important factors is not how you garner a final solution but rather that you understand the data well enough to convey your findings. Most conclusions are drawn from analysis; therefore, it is critical that your data is reliable and consistent. In order to determine the quality of the data, you must examine it before you conduct your analysis. Fraud examiners must know the quality of their data.

A SIMPLE SCHEME: THE PURCHASE FRAUD OF AN EMPLOYEE AS A VENDOR

An employee sets up his or her own company and then funnels purchases to that company. Variations include a “ghost” approach, where invoices are sent from the employee's company but no actual goods or services are provided. In other instances, actual goods may be shipped separately.

To detect this type of fraud scheme, an operational manager is asked to review a new vendor. A phone call to the vendor may reveal that some form of suspicious activity has occurred. With IDEA, you can use the sampling techniques to generate a list of vendors to verify.

Analytics is one of the most critical components in fraud investigations. When analyzing data, you may be faced with the daunting challenge of deciphering a voluminous amount of data that contains multiple fields with multiple pieces of information. Each of the pieces of information can be queried separately once you understand how and where the fields of data are displayed and the specific coding of each. Understanding this element will allow you to extend your analysis in IDEA and the results needed.

Another key point with fraud analytics and using IDEA is that you must understand the data and the type of analysis that will need to be performed. Fraud examiners can attest to the analysis only after sorting the information as thoroughly as possible. Fraud analytics is critical to preserving the integrity of the original data.

In conclusion, fraud examiners must have a keen skill set that is capable of identifying the right question at the right time, including complex questions that relate to the analytics. Prior to performing analysis, examiners must assess the data. If analysis is based on unclean data, it will yield unclean results. After examiners have determined the reliability of the data, then they can proceed to the analysis portion of the investigation.

Another critical element for fraud examiners in fraud analytics is making certain that they keep abreast of the latest trends, concepts, risks, and technology associated with fraud analytics. Avenues that provide new training, updated training, and new and refreshed skills are necessary in the field of fraud analytics. Maintaining a keen eye for the most efficient tools seems to be the overall solution in the twenty-first century as we combat fraud and continue to be proactive in our methods of detection and prevention.

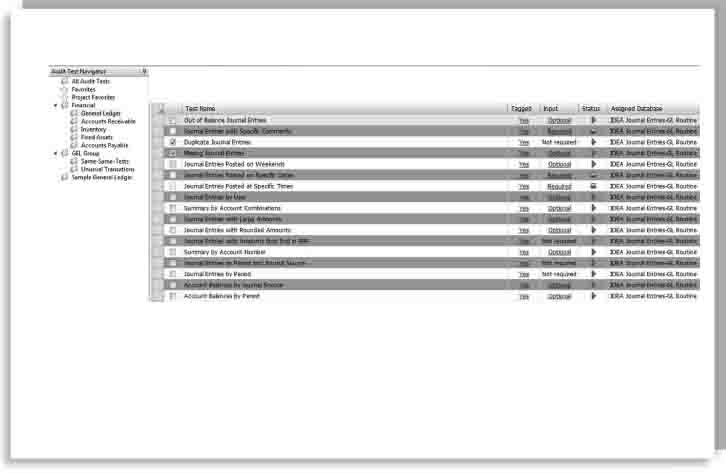

STAGES OF USING IDEA

The first three stages of using IDEA are the planning stages. They are considered the golden nuggets to getting the most out of IDEA. Figure 6.5 shows the six stages of detecting fraud with IDEA.

Using IDEA allows you to quickly import data from almost any source. IDEA is a powerful and user-friendly tool designed to help accounting, fraud examiners, and financial professionals extend their accounting capabilities, detect fraud, and support documentation standards.

Chapter 7 discusses Centrifuge Analytics, another highly regarded data analysis tool.

Centrifuge is a leading provider of Visual Network Analysis (VNA), which is by far one of the most innovatve and yet seemingly uncomplex data analysis software tools. Centrifuge has proven to be extraordinary in its abilities to detect fraudulent activities in money laundering, ATM skimming, and threat finance investigations. Fraud examiners and countless other within the fraud industry are comfortable with its interface, the uniqueness to detect trends that are most affected with subliminal data. Centrifuge VNA is becoming one of the top competitors of data analysis technology. The user-friendly interface and the comfort of knowing that results will be endless if and when the tool is adapted.4 Once an individual is comfortable with using the functions and testing its abilities on various audits, fraud examinations and financial investigations it will soon be determined that Centrifuge VNA is well suited to establish and combine patterns and associations, share information to further enhance its capabilities for merely outlining the discrepancies in the data, creates proactive visuals to display the entities within, and it clearly assists in the auspices of many social networking sites to garner information that can potentially be used to further enhance an investigation of sorts.

Source: CaseWare IDEA Software Interface. Reprinted with permission of CaseWare IDEA.

NOTES

1. Delena D. Spann, “Advanced Fraud Analysis,” Utica College, Economic Crime Management Graduate Program, PowerPoint Presentation, 2010.

2. C. Stephen Trunbull, Fraud Investigation Using IDEA, (N.P.: Ekaros Analytical, 2003), p. 51

3. Ibid.