CHAPTER 6

Insurance Through a Goals‐Based Lens

“All good things arrive unto them that wait and who don't die in the meantime.”

—Mark Twain

Insurance—and the various insurance products that saturate the marketplace—tend to have either a loyal following or are met with disdain by practitioners. Annuities, as a word, can evoke bristling responses from clients and practitioners alike, while others would sing their praises from the highest mountain if they could. I have myself been pitched countless clever “off label” uses of life insurance, from “it is like owning your own bank” to “it is a rich‐man's Roth IRA.” And then there is the mundane: life insurance, car insurance, homeowners insurance, even crop insurance.

Insurance is so broad a topic that there is little hope we could do it proper justice in a single chapter. Even so, this is a book about achieving goals, and insurance products very often have a role to play in aiding in their achievement—or at least preventing their failure. Unfortunately, the literature on insurance through a goals‐based lens is very limited (this would be a wonderful topic for anyone looking for a research subject), and it is not my intent to fill such a large gap in one sitting. Rather, I would like to view this chapter as a bit of a signpost, both pointing a way for future research as well as offering some direction to practitioners who would like a framework for thinking about the problem (and sifting through some of the nonsense). If all of that is agreeable, we can proceed!

From the prospective of the purchaser, insurance is a simple concept: by paying a fee, certain risks can be moved from me to someone else. The insurance company values the fee (and by pooling risks, it is in a unique position to do so) and the insured values the removal of risk. It is this basic fee‐for‐risk construct that drives all insurance. Like almost all else in the market, insurance is a transaction that represents an exchange of value. For risks of catastrophic loss—like the loss of a home—the exchange of value may be obvious. However, for other applications—like the purchase of an annuity—the exchange of value may be less obvious. Let's deal with each in turn.

The Maslow‐Brunel pyramid helps us intuitively grasp the value of catastrophic insurance. If an event destroys the bottom of the pyramid, none of our higher goals will be achieved—all surviving resources will be dedicated to rebuilding the pyramid from the bottom up.1 As the goals‐based model clearly shows, moving the probability of goal achievement to zero yields considerable loss of utility, especially when done across the whole panoply of goals!

We can model this a bit more technically. Since higher goals are contingent on achieving foundational goals, we can model the achievement probability of the higher goals as contingent on the achievement of the goals lower on the pyramid:

In this structure, the utility of the higher goals can only be achieved if the foundational goal (goal A) is achieved. This is intuitive: If we are unable to buy groceries (bottom of the pyramid) due to the loss of a job, savings that would otherwise have been dedicated to buying a vacation home (higher up the pyramid) is now at risk. We will not be buying a vacation home if we starve to death, so the achievement of that goal is contingent on achieving our goal of eating every day. We will not be donating a significant portion of our estate to a philanthropy if our assets do not survive through retirement. All goals higher on the pyramid are contingent on the achievement of goals that are beneath it.

If we look at just the two‐goal case (for simplicity), we can model the value of insurance a bit more clearly:

The utility of our goals‐space is the value of goal A times its probability of achievement plus the value of goal B times its probability of achievement times the probability of achieving goal A. This last point is what makes insurance sensible. Goal B's achievement is contingent on the achievement of goal A. When we buy insurance, we offset a catastrophic loss by paying a fee. That fee reduces the amount of wealth available to achieve higher goals, but we also gain some increase in achievement probability for our foundational goals, and any goals that rest on them.

This is where the modeling gets a bit tricky. In practice, we should evaluate the cost and benefit of the insurance through the lens of the specific scenario and its achievement probability. I can imagine some levels of wealth at which it would be advantageous to self‐insure certain types of risk. However, for the purposes of this much more general analysis, let us assume that the benefit accrues to the foundational goal and the cost is pulled from the higher goal. We are concerned with when the cost is equal to the benefit, from the goals‐based perspective. So, let us set u(buying insurance) = u(no insurance):

In this equation, we have some gain in achievement probability, represented as Δϕ(A) for the foundational goal and Δϕ(B) for the higher goal. As we apply some algebra, it is clear that Δϕ(B) is negative (hence, a cost), but exactly what level of cost is acceptable depends on a number of factors:

remembering that Δϕ(B) is not expressed here in dollar terms but in percentage points of achievement probability. One would need to convert to actual dollars to get the maximum premium cost our investor would accept.

This relationship is graphed in Figure 6.1, Panel A. Again, it is expressed in terms of probability of goal achievement. To convert to actual dollars, we would need to apply some algebra (assuming our portfolio is accurately represented by a logistic distribution):

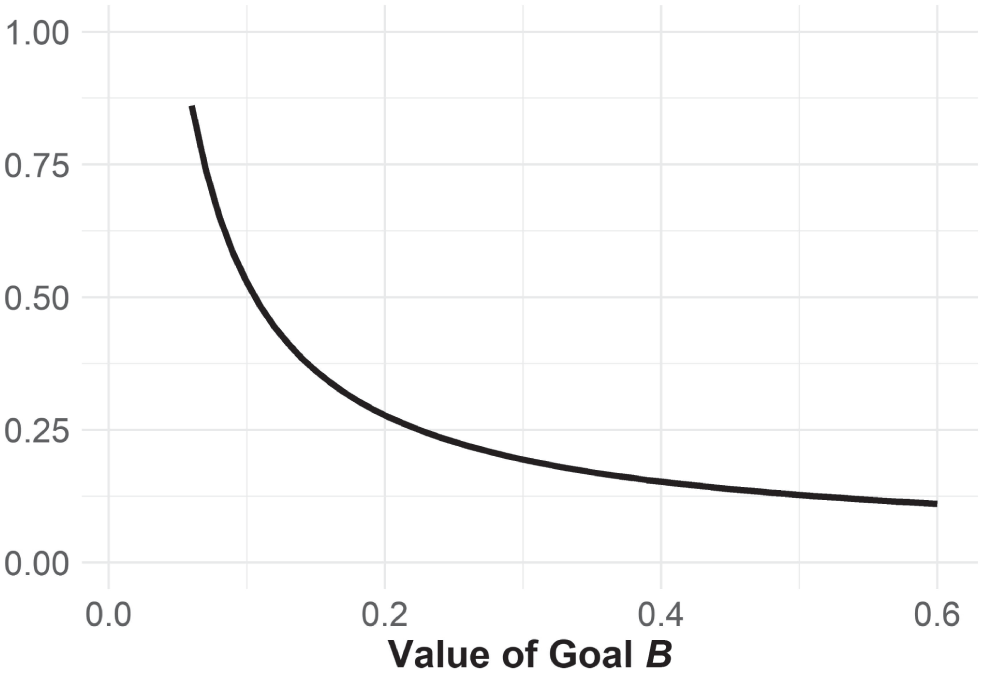

FIGURE 6.1 Example: Willingness to Pay for Insurance

Panel A: As a Function of Goal B's Value

Goal A moves from 95% probability to 100% probability with insurance; goal B carries a 55% baseline probability of achievement.

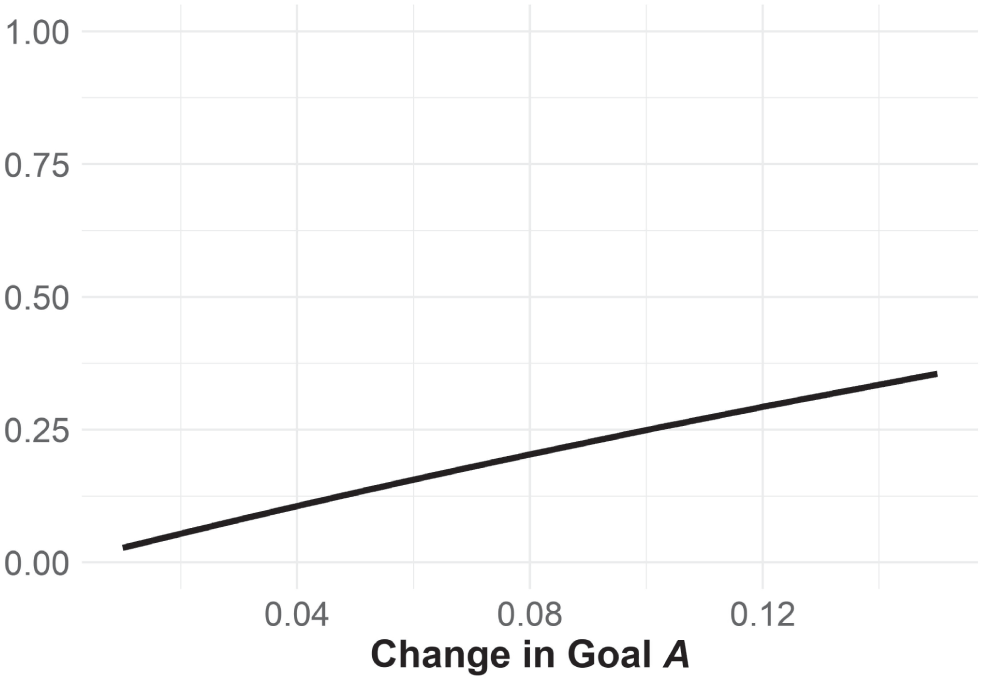

Panel B: As a Function of How Insurance Affects the Achievement of Goal A

Goal A has an 85% probability of achievement; goal B has a value of 0.55 and a probability of achievement of 55%.

where m is the portfolio's average return, s is the portfolio's volatility (though in logistic terms), W is the required wealth value to achieve the goal, and t is the time horizon. All of these terms apply to goal B. A simple example: Suppose we have $62.63 today and we need $100 in 10 years to achieve goal B, and we can expect to get 8% in a portfolio with 16% volatility. Using the equation above, we would expect our investor to be willing to pay up to $3.68 in premium to move the probability of achieving goal A from 95% to 100%. That would reduce our probability of achieving goal B by 12.5% points.

Note that this move of five percentage points for goal A is not equal in price across the whole range of achievement probabilities! For example, if we drop our probability of achieving goal A from 95% to 85%, that same five percentage point move (now moving goal A from an 85% chance of achievement to a 90% chance of achievement) is worth a bit more: $3.94 of goal B's wealth allocation. This is illustrated in Panel B of Figure 6.1.

In this category of specific and catastrophic‐type risks, I would also count risks to human capital—a primary rationale for the purchase of life insurance for many investors. The foundational work of Chen, Ibbotson, Milevsky, and Zhu describes the problem this way: “An investor's wealth consists of two parts. Human capital is defined as the present value of an investor's future labor income…although human capital is not readily tradeable, it is often the single largest asset an investor has.”2

Over time, through their labor and receipt of income, people convert their human capital into financial capital, so the risk of loss to human capital tends to decline as we age. The amount of insurance need, in this framework, is simply the present value of future human capital. Hence, the value of life insurance tends to be greater earlier in life than in later (though estate planning concerns often come into the calculus later in life). Given that this idea is widely studied, I will not rehash the techniques here, but interested readers should certainly read the footnoted article as it is an important concept in financial planning.

All of this is a way to think about offsetting very specific and measurable risks to an investor's goals‐space, such as homeowners insurance or medical insurance. Of course, not all risks are so measurable and specific. Often, investors wish to offset much fuzzier risks, such as the risk of being wrong about a forecast. To be fair, the problem is not usually framed in that way. Rather, the problem is usually framed as the risk of running out of money. While this is traditionally studied as a form of mortality risk (and it is partly that), I would also argue that this concern is a form of forecasting risk. Let me illustrate my point.

In a very simple model, the amount of money we think is needed to fund a goal is, in no small part, a function of our inflation forecast. If, for example, we expect that $74 of today's dollars are needed in 10 years to fund a goal, we must apply some inflation forecast to this figure to generate the final wealth requirement: $74×(1 + i)10 = W, where i is our inflation forecast. If we forecast inflation at 3%, then we need $100 in 10 years, but if we forecast inflation at 5%, then we need $121—quite a difference!3 Of course, actual inflation will be different from our forecast, so how could we offset the risk of being wrong—especially wrong in the wrong direction?

In my view, this is a type of fuzzy risk that investors often want to offset by buying annuities, pensions, or other insurance products with cost‐of‐living adjustments built into the policy.4 The premiums charged and payouts of these policies are usually based on mortality risks, at least primarily, but investors often buy them to offset these other, more subtle and visceral, risks. To illustrate the role this risk plays in pricing insurance, let us set up our probability model with this form of meta‐uncertainty built in (our required future value is subject to geometric Brownian motion based on our inflation forecast):

where W is our forecast for future wealth, µi is our expectation for inflation over the time horizon for the goal, dubbed t, ![]() is the variance of our inflation expectation over that time horizon, and w is the amount of wealth dedicated to the goal today.

is the variance of our inflation expectation over that time horizon, and w is the amount of wealth dedicated to the goal today. ![]() , then, is the probability density function of the final wealth requirement.

, then, is the probability density function of the final wealth requirement.

Clearly, if we misestimate inflation the wrong way and we end up needing more money than we originally estimated (![]() ), then our client cannot achieve her goal. So, our actual probability of goal achievement is influenced by the probability that we got our inflation forecast right. We can understand that probability as the cumulative distribution function of

), then our client cannot achieve her goal. So, our actual probability of goal achievement is influenced by the probability that we got our inflation forecast right. We can understand that probability as the cumulative distribution function of ![]() , or

, or

Our final probability of achievement, then, is:

where m and s are the return and volatility of the portfolio, ϕ(⋅) is the upper‐tail cumulative distribution function for our portfolio, and ![]() is our expected future wealth requirement based on our projection for inflation. With the set up out of the way, we can turn to the meat of the analysis.

is our expected future wealth requirement based on our projection for inflation. With the set up out of the way, we can turn to the meat of the analysis.

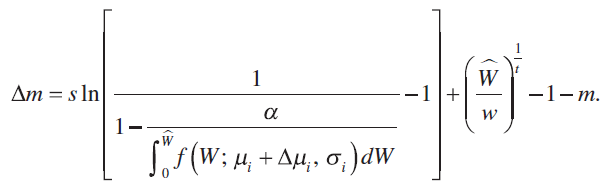

We are concerned with how much return our investor is willing to give up to change how uncertain we are about our inflation forecast. Letting α be the minimum probability of achievement our investor is willing to accept, we can let Δm stand in for the amount of return our investor is willing to give up and let Δσi be the change in the uncertainty about our inflation forecast. Plugging these into our equation above, and we have

Expanding our ϕ(⋅) function (assumed logistic) and applying some algebra to solve for Δm yields

which is the maximum amount of return drag our client would be willing to accept, given the inputs.

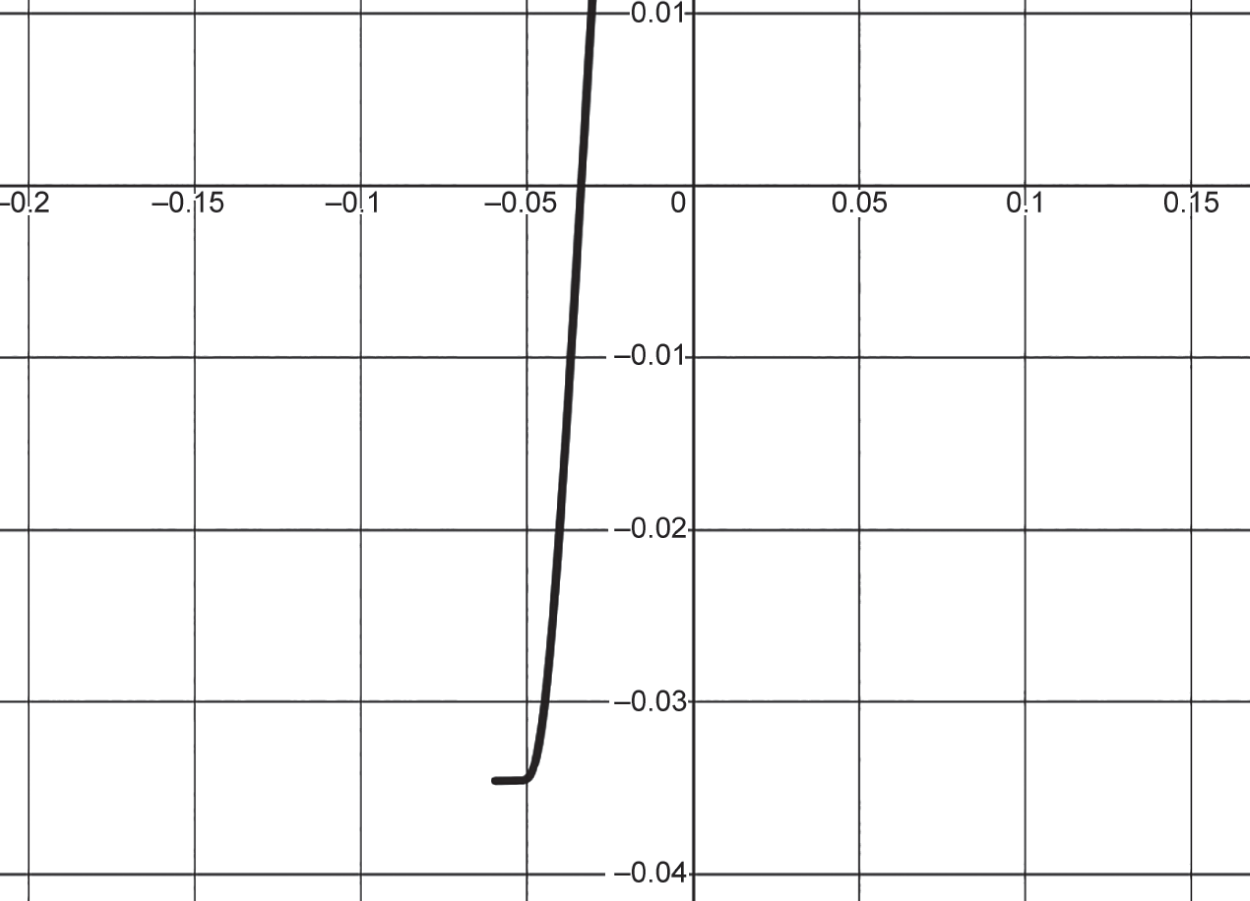

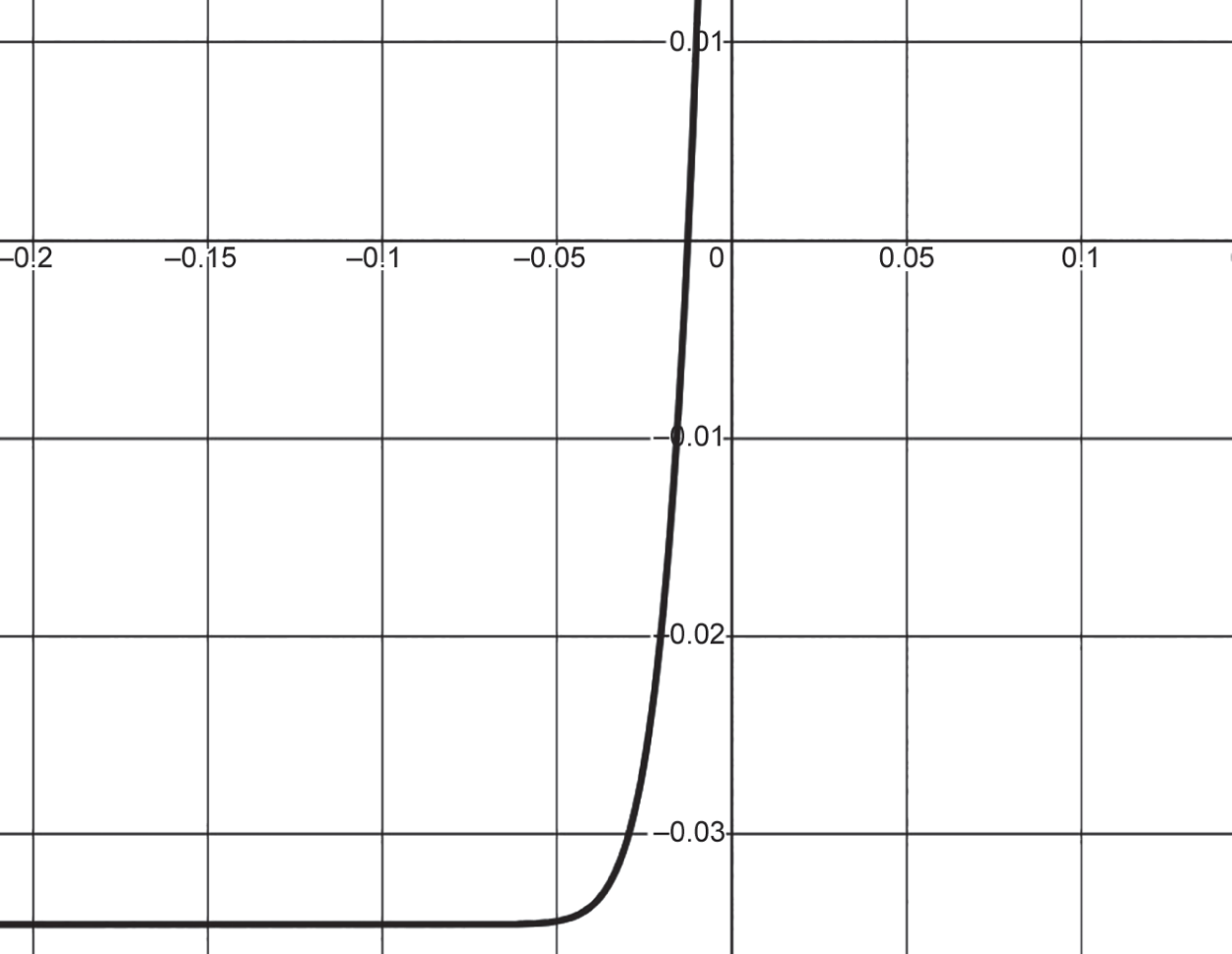

Unfortunately, this relationship is not particularly intuitive, at least at first glance. Figure 6.2 illustrates the relationship given some example parameters. On the horizontal axis, we have the amount our inflation uncertainty changes (Δσi), and on the vertical axis we have the maximum return drag that our investor is willing to accept. As becomes clear, our investor is willing to pay to offset a lot of uncertainty, but not necessarily to offset a little uncertainty. In some cases, our investor would not be willing to pay to offset any uncertainty at all, but that would of course depend on all of the various inputs. Interestingly, to completely eliminate inflation uncertainty, our investor is willing to pay quite a lot per year—over 300 basis points in this example! Intriguingly, this is just to offset uncertainty about inflation, not even to offset the effect of inflation itself!

FIGURE 6.2 Willingness to Sacrifice Return to Reduce Inflation Uncertainty

With a goal that is 67% funded, a 10‐year time horizon, a portfolio that is expected to deliver a 10% return with 15% volatility, a minimum probability of achievement of 54%, an inflation expectation of 3% with a standard deviation of 6%.

We can apply the same logic to the effect of inflation itself. In a similar vein, an individual should be willing to pay up to Δm units of return to offset the effects of inflation itself (Δμi):

Again, we can build our intuition on the topic using Figure 6.3. Similar to before, our investor is increasingly willing to sacrifice returns to offset the effects of inflation (the horizontal axis is the change in expected inflation and the vertical axis is the maximum acceptable return drag). Indeed to offset the full 3% inflation, our investor is willing to give up about 300 basis points of annual return.

The point here is simply that investors are, sometimes, willing to pay to offset inflation risks. That rational willingness can justify the use of more expensive financial products, like annuities, within which these types of benefits are usually included. There are other risks, of course, like longevity risk—the risk that I live longer than expected and thereby “outlive my money,” A group of researchers has approached this problem with some interesting results.

One group of researchers presented another very interesting look at the role of annuities in consumption goals over time.5 Their approach was slightly different and very insightful. They analyzed how an investor in the decumulation phase (in retirement, for example) could maximize the utility of their consumption over time. In essence, they sought to answer how much an investor should consume, and how much an investor should allocate to stocks, bonds, cash, and single‐premium immediate annuities (SPIAs), using their age and current capital to calculate the risk of outliving their capital. In general, they found that investors should start with smaller withdrawals and increase them every year, and SPIAs will tend to replace a significant chunk of a fixed‐income allocation as investors age. SPIAs also appear to be a much more effective way to offset longevity risk than fixed‐income allocations in their analysis. And, as the amount of present wealth dedicated to the goal grows, annuities become a more important component in the portfolio.

FIGURE 6.3 Willingness to Sacrifice Return to Reduce the Effects of Inflation

With the same parameters as Figure 6.2.

This last point is consistent with the more formal goals‐based framework. As the amount of wealth dedicated to a goal shrinks, an investor becomes more and more reliant on higher‐volatility assets (like stocks). An annuity, with its guaranteed payout and smaller uncertainty, is the antithesis of that kind of asset so an investor with low initial wealth will tend to avoid such a solution.

Their analysis is consistent with this one in another way: the pricing of and allocation to insurance products is highly individualized. The premium an investor is willing to pay to offset various types of risk is completely dependent on the goals the investor is trying to achieve and the risks being offset. To the investor, there is a different price to offset inflation risk than the risk that a house burns down. There is a different price to offset the risk of fire in a vacation home than to offset the same risk in a primary residence. No two purchasers of insurance are alike, and no two insurance purchases are alike (even if they are by the same individual!).

There is a lesson here for insurance companies. As technology grows, it may be possible to customize the insurance product as well as the price of that product based on the individual and the need. Differential pricing has long been a practice, but that has largely been based on the types of risks being offset rather than the price an investor is willing to pay. Assuming the insurance company is adding real value by offsetting investor risks, it may well be that investors are willing to shoulder higher costs to lay off those risks. In any event, the cookie‐cutter model that has dominated the industry may well be on the way out. Pricing and risk‐selection are individualized, just like everything else in goals‐based investing.

Admittedly, this is a simplistic way to model and think about insurance, but I hope it communicates the point. Insurance will be viewed through the lens of tradeoffs, and many factors go into understanding and making those tradeoffs. The thrust of this chapter is not to present a hyper‐detailed analysis, but rather to demonstrate that goals‐based investors are concerned with offsetting both specific and more nontraditional risks. It is clear that people pay money to offset very specific and fundamental risks (i.e. the risk of losing shelter to a storm), and it is also clear that people pay money to offset more subtle risks, like inflation, in real life (so they don't “outlive their money”). This behavior is both predicted and modellable using the goals‐based framework.

Research viewing insurance through a goals‐based lens is only just coming out. It is still a new perspective. Much work has been done from the perspective of an insurance company, especially in the actuarial sciences, and some very good work from a purchaser's perspective has been done using more traditional models of utility. Analysis from the perspective of the investor, the purchaser of these products, through the lens of achieving actual goals, is a boulevard that needs more light, and researchers are likely to find fruit here. Insurance companies stand to benefit by better understanding and pricing their client. More importantly to me, however, is that individuals stand to achieve their goals more often if they can see insurance within the proper context. Rather than selling insurance through clever marketing (“Be your own bank!”), the goals‐based framework can give practitioners confidence that an insurance solution will help our clients achieve their goals more often.

But there is much work to do.

Notes

- 1 Of course, at times people are required to purchase insurance (such as a bank requiring homeowners insurance to issue a mortgage), but let us set that aside for now. I want to build our intuition with voluntary insurance purchases, as ostensible as they may sometimes be.

- 2 P. Chen, R.G. Ibbotson, M.A. Milevsky, and K.X. Zhu, “Human Capital, Asset Allocation, and Life Insurance,” Financial Analysts Journal 62, no. 1 (2006): 97–109, DOI:

https://doi.org/10.2469/faj.v62.n1.4061. - 3 We will address the fragility of financial planning with respect to inflation forecasts in Chapter 10. As it turns out, this is a very critical assumption in the forecasting of goal requirements!

- 4 Though I do not detail the methods here, I would direct interested readers to the foundational work of Moshe Milevsky on annuities, especially:

M.A. Milevsky, “Optimal Asset Allocation Towards the End of the Life Cycle: To Annuitize or Not to Annuitize?” FAS #21‐96 (1996). Available at SSRN:

http://dx.doi.org/10.2139/ssrn.1077.M.A. Milevsky, Life Annuities: An Optimal Product for Retirement Income, CFA Research Foundation Monograph (2013).

M.A. Milevsky, K. Moore, and V.R. Young, “Asset Allocation and Annuity‐Purchase Strategies to Minimize the Probability of Financial Ruin,” Mathematical Finance 16, no. 4 (2006): 647–671, DOI:

https://doi.org/10.1111/j.1467-9965.2006.00288.x. - 5 J. Sun and H. Lan, “Solving the Decumulation Puzzle with Dynamic Asset Allocation and Annuities,” Journal of Wealth Management, forthcoming (2022).